Key Takeaways

- El Salvador's Código de Comercio provides eight distinct entity structures, ranging from the Sociedad Anónima to the Sole Proprietorship, each carrying different consequences for liability, governance, and capital requirements.

- The Sociedad Anónima (S.A.) remains the most commonly registered structure in El Salvador and is best suited for medium-to-large operations and foreign investors requiring capital flexibility.

- All commercial entity registrations in El Salvador fall under the jurisdiction of the Centro Nacional de Registros (CNR), which also maintains public corporate records.

- Because El Salvador operates a territorial tax system, only income generated within the country is generally subject to taxation by the DGII.

Introduction to Entity Types in El Salvador

El Salvador operates as an independent republic in Central America, bordered by Guatemala, Honduras, and the Pacific Ocean. Businesses registering in the country fall under the jurisdiction of the Centro Nacional de Registros (CNR), the national registry authority that processes commercial entity registrations and maintains public corporate records.

The tax system is territorial in structure, meaning only income generated within the country is generally subject to local taxation.

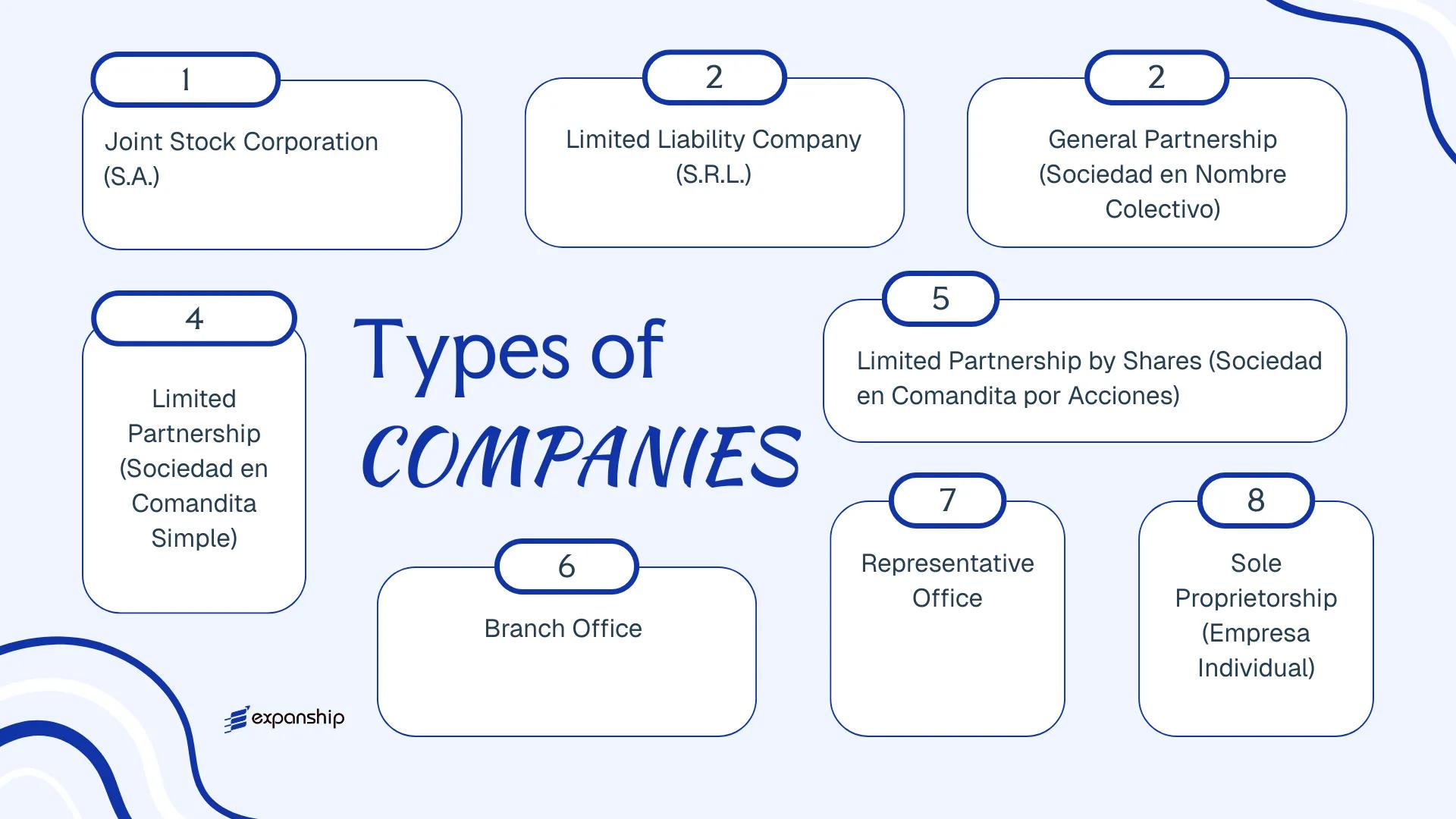

Several distinct entity types are available under the Salvadoran Commercial Code (Código de Comercio), each carrying different implications for liability, ownership, and governance. These include the Sociedad Anónima (S.A.), Sociedad de Responsabilidad Limitada (S.R.L.), Sociedad en Nombre Colectivo, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones, Branch Office, Representative Office, and Sole Proprietorship (Empresa Individual).

Each structure differs in how it treats shareholder liability, minimum capital requirements, and management obligations. This article examines each option in detail so your business can make a well-informed registration decision.

An Overview of Business Structures in El Salvador

El Salvador recognizes several distinct legal forms for conducting commercial activity, all governed primarily by the Código de Comercio (Commercial Code) enacted by Legislative Decree No. 671. Each structure carries different implications for liability, taxation, governance, and the profile of the business using it.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima (S.A.) | Corporation | Limited to shares | Taxable | Permitted | 2 shareholders | CNR / Ministry of Economy | Código de Comercio |

| Sociedad de Responsabilidad Limitada (S.R.L.) | LLC | Limited to capital quota | Taxable | Permitted | 2 members, max 25 | CNR / Ministry of Economy | Código de Comercio |

| Sociedad en Nombre Colectivo | General Partnership | Unlimited, joint | Taxable | Permitted | 2 partners | CNR | Código de Comercio |

| Sociedad en Comandita Simple | Limited Partnership | Mixed | Taxable | Permitted | 1 general + 1 limited | CNR | Código de Comercio |

| Sociedad en Comandita por Acciones | Share-based Partnership | Mixed | Taxable | Permitted | 1 general + 1 limited | CNR | Código de Comercio |

| Branch Office | Foreign entity extension | Parent liable | Taxable | Permitted | N/A | CNR / MH | Código de Comercio |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | Not permitted | N/A | CNR / MH | Código de Comercio |

| Empresa Individual | Sole proprietorship | Unlimited | Taxable | Permitted | 1 individual | CNR | Código de Comercio |

Each of these structures is examined in full in the sections below.

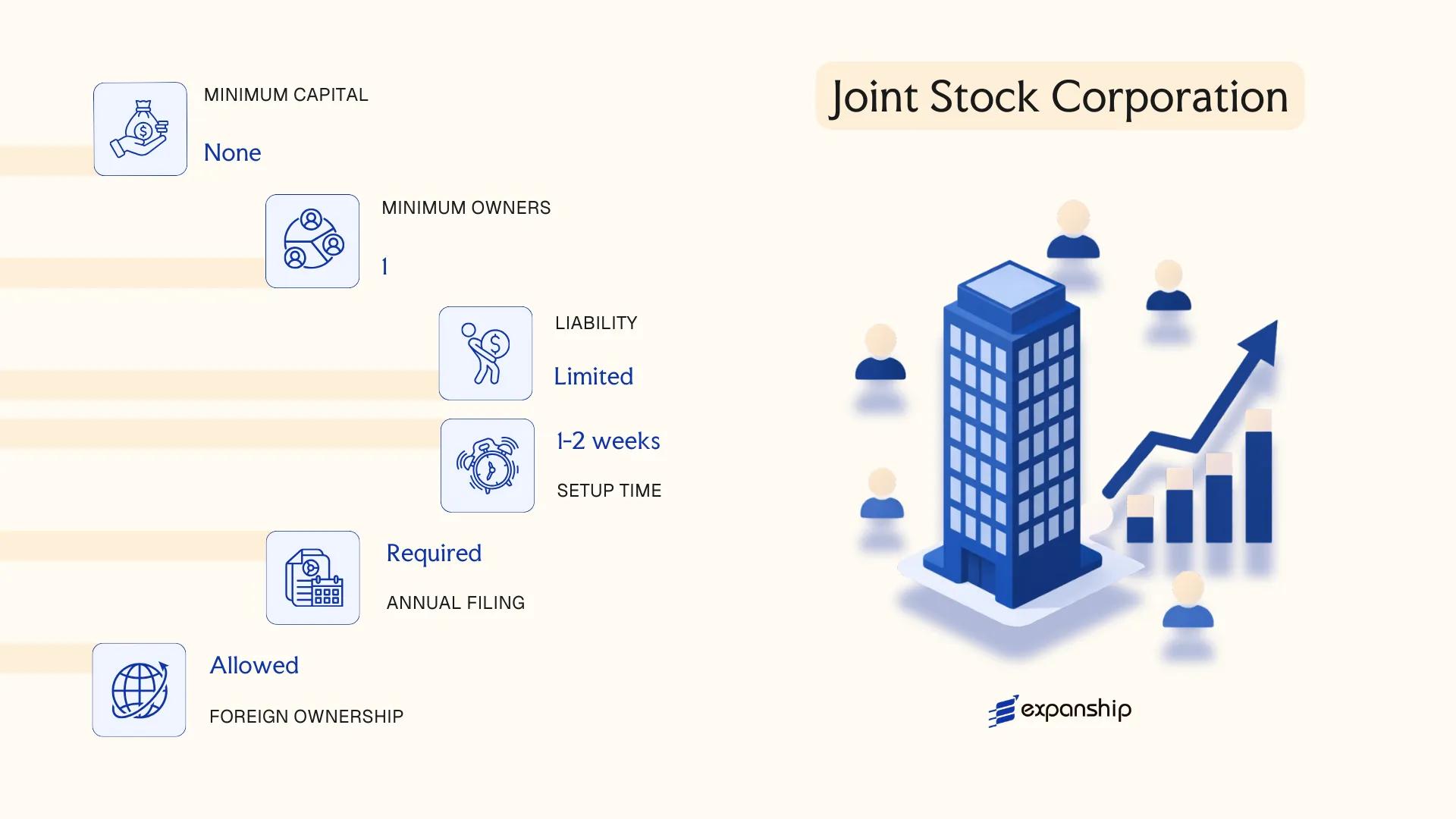

Sociedad Anónima (S.A.) — Joint Stock Corporation

The Sociedad Anónima El Salvador framework is governed primarily by the Código de Comercio de El Salvador (Commercial Code, 1970), which establishes the S.A. as a capital-based entity with full separate legal personality. Shareholders bear no personal liability for corporate obligations beyond their subscribed capital contributions.

Capital is divided into negotiable shares, which can be transferred without requiring the consent of other shareholders — a structural feature that distinguishes this entity from most other Salvadoran business forms.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima (S.A.) | Governed by the Código de Comercio (1970) |

| Members | Shareholders (accionistas); minimum 2, no statutory maximum | No corporate nationality restriction on shareholders |

| Directors | Minimum 1 Director (or a Board); a statutory auditor (auditor fiscal) is required | Directors need not be resident in El Salvador |

| Local Presence | Registered agent and registered address required | Must maintain a local legal domicile |

| Capital | No statutory minimum capital under general rules; denominated in USD | Shares must be subscribed and partially paid-up at incorporation |

| Privacy | Shareholder names appear in public registry records | Bearer shares are prohibited under AML legislation |

Focus Points

- Taxation: Corporate income tax is levied at 25% on net taxable income (30% for entities earning over USD 150,000); VAT applies at 13%; dividends paid to non-residents are subject to withholding tax; no stamp duty on share transfers.

- Annual Compliance: Mandatory filing of audited financial statements, annual tax returns, and renewal of registration with the Centro Nacional de Registros (CNR).

- Economic Substance: No formal substance requirements, though entities with active Salvadoran operations must maintain adequate local records.

- Treaty Access: El Salvador has a limited tax treaty network; treaty benefits are generally unavailable for most cross-border structures.

- Conversion: An S.A. may be converted into another commercial form (including an S.R.L.) by following the transformation procedures set out in the Código de Comercio, subject to creditor notification requirements.

Closing

The S.A. is commonly used for medium-to-large trading operations, holding structures, and businesses seeking external investment through share issuance. The transferability of shares without shareholder consent supports capital raising, though the mandatory auditor fiscal requirement and public disclosure of shareholder records add compliance overhead that smaller firms may find disproportionate.

The S.A. structure suits businesses anticipating investor participation, multi-shareholder ownership, or eventual capital market activity in El Salvador.

Company Incorporation in El Salvador

Incorporate a Sociedad Anónima or other business entity in El Salvador with end-to-end support from Expanship.

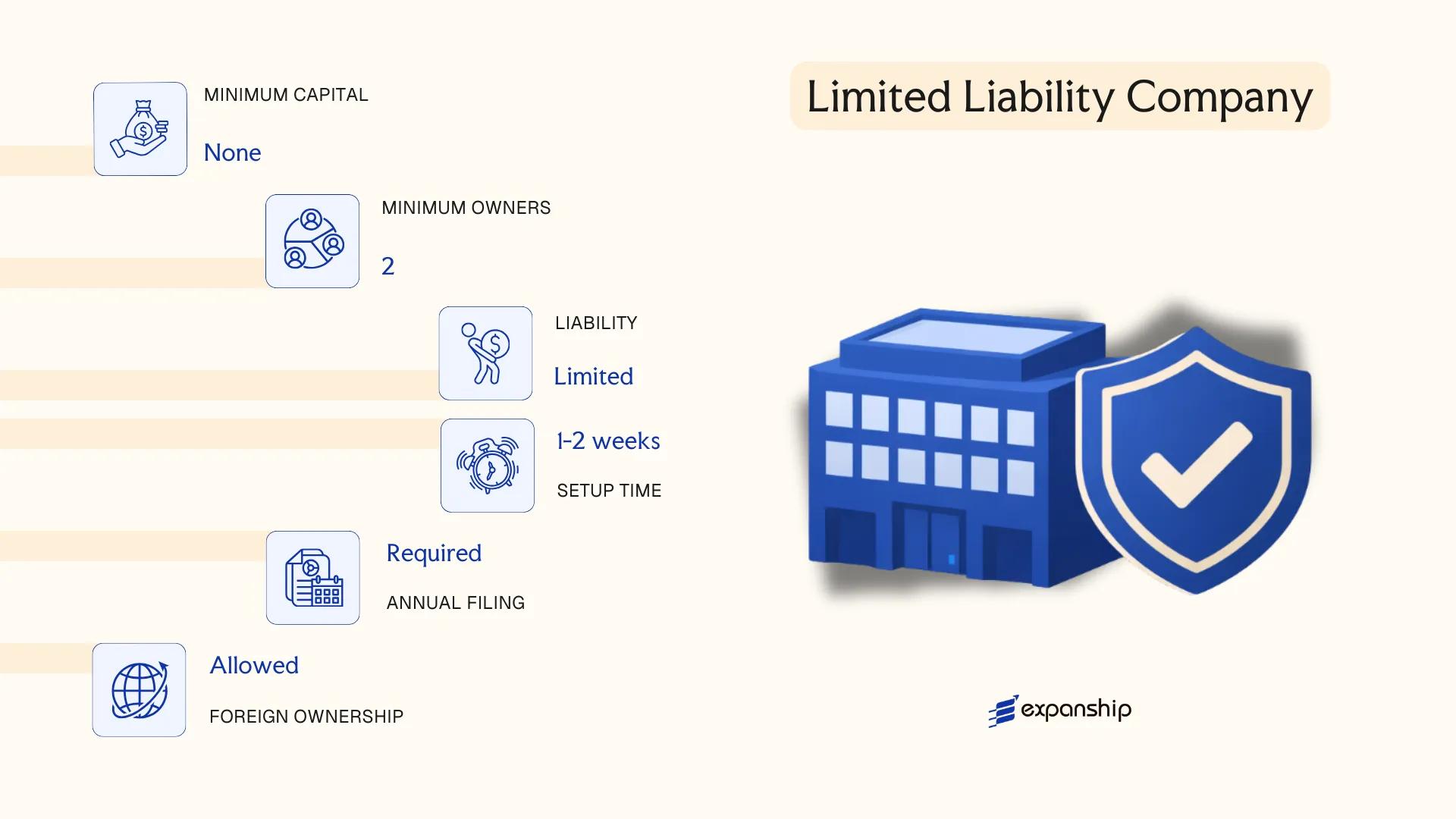

Sociedad de Responsabilidad Limitada (S.R.L.) — Limited Liability Company

The Sociedad de Responsabilidad Limitada El Salvador is governed by the Código de Comercio (Commercial Code) enacted in 1970, which remains the primary legislative framework for this entity type. It carries separate legal personality, meaning the firm exists independently from its members, and liability is confined to each member's capital contribution.

Structured as a hybrid between a corporation and a partnership, this entity suits closely held businesses that require formal liability protection without the administrative requirements of a joint stock company. Capital is divided into quotas rather than freely transferable shares, which gives members tighter control over ownership changes.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad de Responsabilidad Limitada (S.R.L.) | Governed by the Código de Comercio |

| Members | 2 minimum, 25 maximum | Members hold quotas, not shares; referred to as "socios" |

| Capital | No statutory minimum; denominated in USD | Divided into equal-value quotas; transfers require member consent |

| Local Presence | Registered address in El Salvador required | A local legal representative is standard practice |

| Privacy | Member names appear in public registry | Beneficial ownership disclosures apply under anti-money laundering regulations |

Focus Points

- Taxation: Subject to a flat corporate income tax of 30% on net profits (25% for taxable income under USD 150,000); VAT applies at 13%; dividends paid to non-residents are subject to a 5% withholding tax; no stamp duty on commercial transactions.

- Annual Compliance: Filing of audited financial statements and income tax return with the Ministerio de Hacienda; registration renewal with the Centro Nacional de Registros (CNR).

- Quota Transfers: Any transfer of quotas to a third party requires the consent of members holding at least 75% of capital, unless the articles of incorporation state otherwise.

- Treaty Access: El Salvador has a limited tax treaty network; S.R.L. entities are generally eligible for any applicable bilateral investment treaty protections.

- Conversion: An S.R.L. may be converted into a Sociedad Anónima by following the transformation procedure under the Código de Comercio, subject to notarial deed and CNR registration.

Closely held trading companies, family businesses, and joint ventures with a fixed ownership group represent the most common use cases for this structure. The quota-based ownership model provides meaningful control over who enters the business, though the 25-member cap makes it unsuitable for entities anticipating broad investor participation.

Small-to-medium enterprises and joint ventures with a defined, stable group of investors seeking liability protection without the governance formality of an S.A.

Partnerships [Sociedad en Nombre Colectivo, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones]

Partnership structures in El Salvador are governed by the Código de Comercio (Commercial Code), which recognizes three distinct partnership forms. Each carries separate legal personality upon registration with the Centro Nacional de Registros (CNR), distinguishing them from simple contractual arrangements between individuals.

Liability treatment varies across these forms. In a Sociedad en Nombre Colectivo, all partners bear unlimited, joint, and personal liability for the firm's obligations. The two comandita structures introduce a hybrid model, separating active managing partners from passive capital contributors.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership with separate legal personality | Registered through CNR |

| Partners | General partners (socios gestores) and, in comandita types, limited partners (socios comanditarios) | Nombre Colectivo has only general partners |

| Minimum Members | 2 partners minimum across all three forms | No statutory maximum under general rules |

| Local Presence | Registered address and local legal representative required | CNR registration mandatory |

| Capital | No statutory minimum; denominated in USD | Comandita por Acciones divides limited partners' capital into shares |

| Liability | Unlimited for general partners; limited to capital contribution for comanditarios | Core structural distinction |

Focus Points

- Taxation: Subject to standard corporate income tax at 30% (25% for firms with net income under USD 150,000); VAT at 13% applies to commercial activity; withholding taxes apply on dividends and cross-border payments.

- Annual Compliance: Annual financial statements and tax filings required; comandita por acciones has additional reporting obligations closer to those of a corporation.

- Treaty Access: El Salvador's limited tax treaty network may restrict treaty benefits for partnership income distributed abroad.

- Conversion: Partnership forms can generally be converted to a Sociedad Anónima through a formal restructuring process before the CNR.

- Restrictions: General partners in all three forms cannot limit their personal liability by agreement; only the comandita structures permit passive investors to cap exposure.

Sub-Types

Sociedad en Nombre Colectivo

All partners hold unlimited personal liability and the firm trades under a collective name. This structure suits small, closely held professional or family businesses where partners are directly involved in management.

Sociedad en Comandita Simple

Two classes of partners coexist: general partners with unlimited liability who manage the business, and limited partners whose liability is capped at their agreed capital contribution. No shares are issued to limited partners.

Sociedad en Comandita por Acciones

The limited partners' interests are divided into transferable shares (acciones), which introduces a degree of capital flexibility absent in the Sociedad en Comandita Simple. This form is subject to certain provisions of corporate law under the Código de Comercio.

Closing

Partnership forms are used primarily by small family businesses, professional service providers, and joint ventures where at least one party accepts full personal liability. The comandita structures offer a route to passive investment without full corporate formalities, though the unlimited liability exposure for general partners remains a significant structural constraint.

These structures are most appropriate for closely held family businesses or professional firms where the controlling partners are comfortable with personal liability and do not require the capital-raising capacity of a corporation.

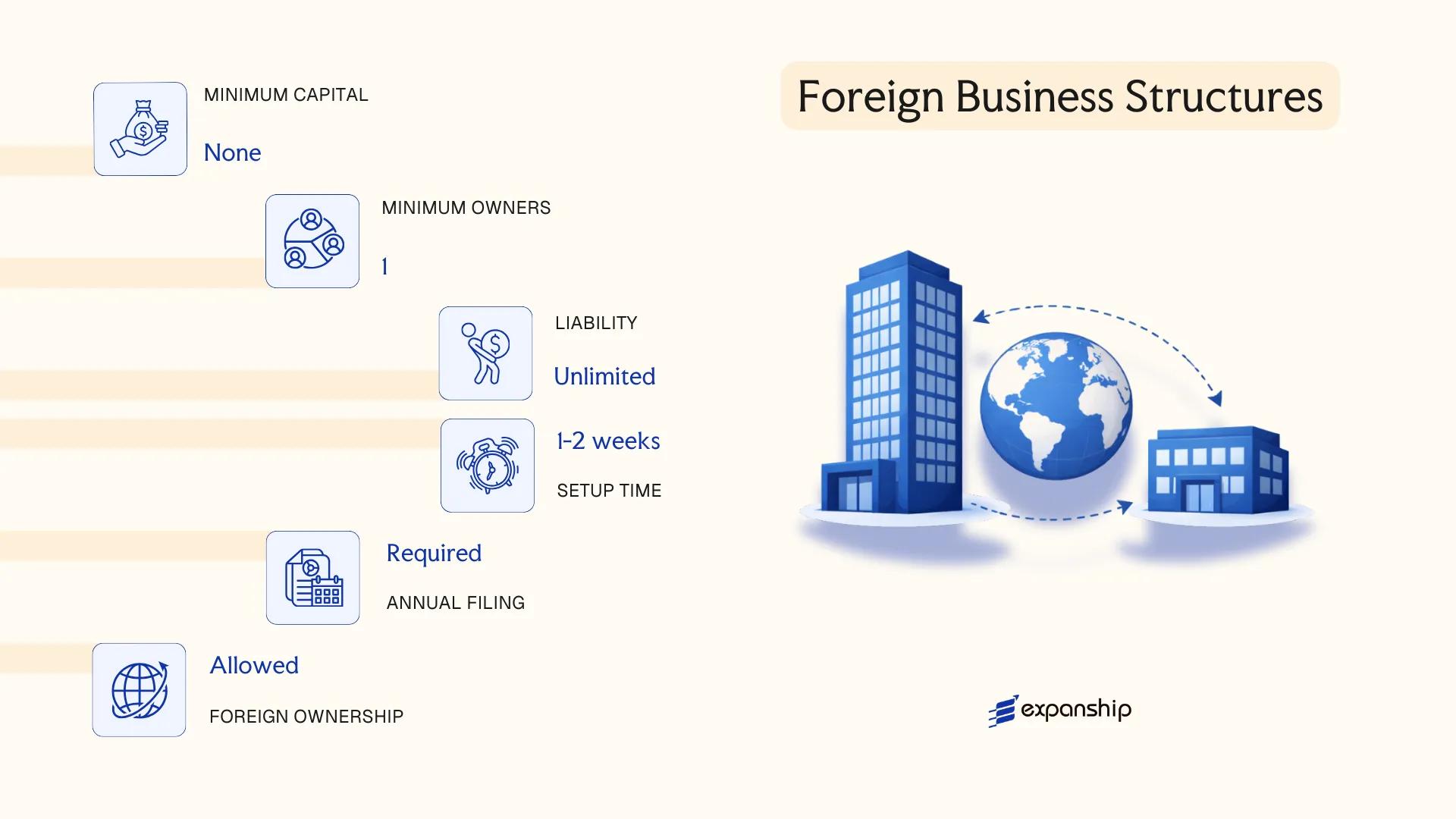

Foreign Business Structures [Branch Office, Representative Office]

Foreign companies seeking a presence in El Salvador without incorporating a separate local entity have two principal options: a branch office or a representative office. Both are governed by the Código de Comercio (Commercial Code) and require registration with the Centro Nacional de Registros (CNR). Neither structure constitutes a separate legal entity from the parent company, which means the foreign firm retains direct legal and financial responsibility for local operations.

Completing a foreign branch office El Salvador registration requires the parent company to submit authenticated constitutional documents, a board resolution authorizing the establishment, and the appointment of a local legal representative. The representative office setup follows a similar process but operates under tighter functional restrictions.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Permitted Activities | Full commercial operations | Promotional and liaison activities only; no revenue-generating transactions |

| Local Representative | Mandatory (natural person resident in El Salvador) | Mandatory |

| Registered Address | Required | Required |

| Capital Requirement | No statutory minimum; parent's capital backs operations | None |

| Tax Registration | Required with Ministerio de Hacienda (MH) | Required; limited tax exposure |

Focus Points

- Taxation: Branch profits are subject to the standard corporate income tax rate of 30%; VAT at 13% applies to taxable supplies; withholding tax applies to remittances to the parent; no separate stamp duty regime exists.

- Economic Substance: No formal substance requirements exist under current legislation, though the local representative must maintain operational authority.

- Annual Compliance: Annual financial statements must be filed; the branch must renew its commercial registration and maintain updated records at the CNR.

- Treaty Access: El Salvador has a limited tax treaty network; branch offices do not independently qualify as tax residents, which restricts access to treaty benefits.

- Restrictions: A representative office cannot invoice clients, hold inventory for sale, or conclude contracts on behalf of the parent in a commercial capacity.

Sub-Types

Branch Office (Sucursal)

A sucursal conducts full commercial activity in El Salvador and is the structure used when the parent intends to generate revenue directly. It must register with the CNR, obtain a tax identification number (NIT), and comply with all local commercial and labour obligations as if it were an operating business.

Representative Office (Oficina de Representación)

An oficina de representación is restricted to market research, promotion, and liaison functions. It cannot generate local income, making it suitable only for foreign firms assessing the market or coordinating regional operations without transacting directly with local clients.

A branch office suits foreign companies that need operational capability without the administrative burden of a separately capitalized local entity; the representative office fits firms in an exploratory or coordination phase. The primary limitation of both structures is full parent liability — there is no liability ring-fence separating local exposure from the parent's global assets.

Both structures are best suited to established foreign companies with a defined purpose in the local market — the branch for active operations, the representative office for pre-market or support functions only.

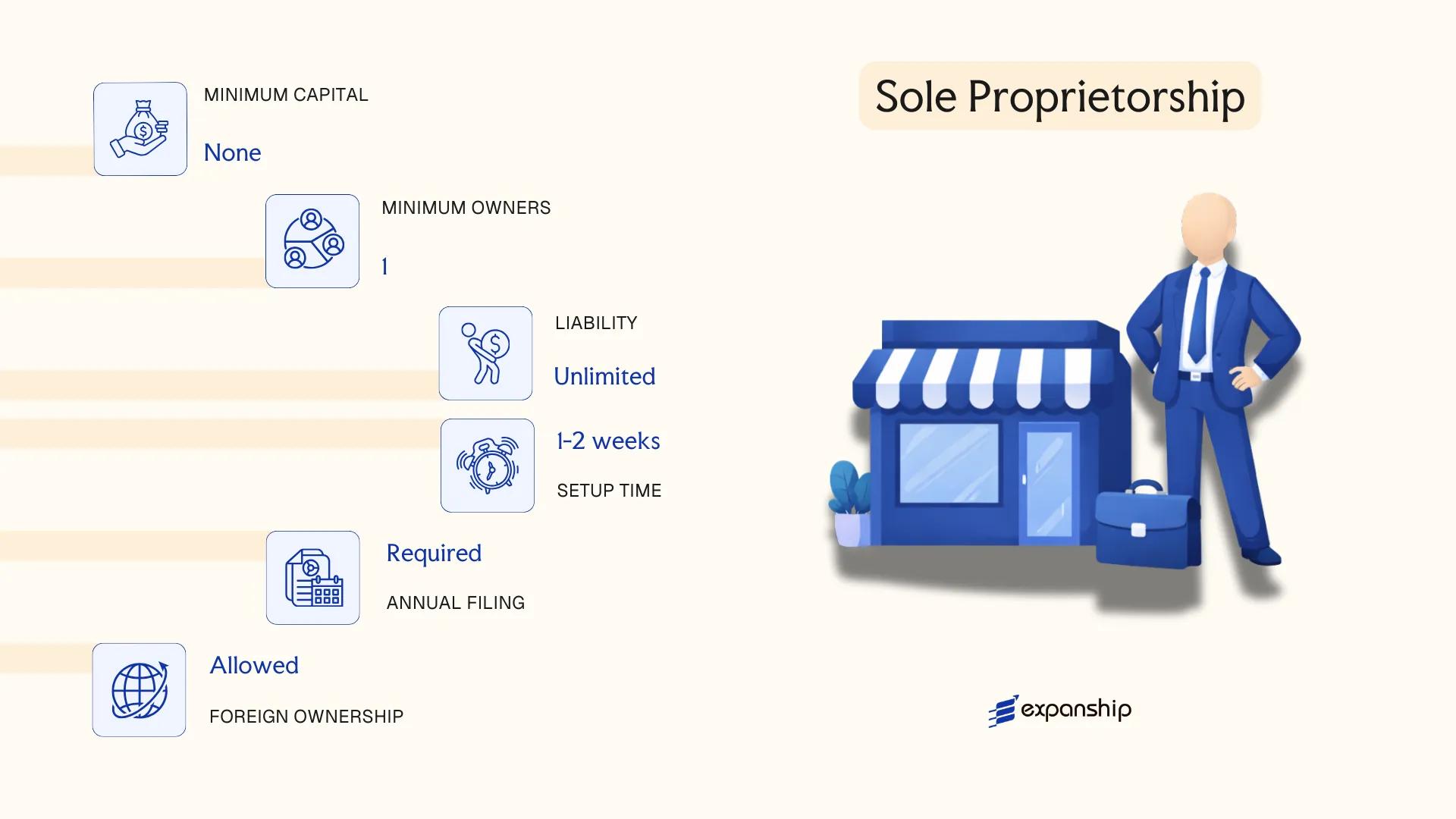

Sole Proprietorship (Empresa Individual)

A sole proprietorship El Salvador recognizes is governed by the Código de Comercio (Commercial Code) and, for registration purposes, the Ley del Registro de Comercio. Unlike corporate structures, the Empresa Individual does not confer separate legal personality — the proprietor and the business are legally the same entity.

Personal assets remain exposed to business liabilities, which is the defining structural feature of this form. Registration is carried out through the Centro Nacional de Registros (CNR), and the business must also register with the Ministerio de Hacienda for tax identification purposes.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Empresa Individual) | No separate legal personality from the owner |

| Owner | Single natural person (Propietario) | Legal and beneficial ownership held by one individual |

| Local Presence | Registered address in El Salvador required | Must maintain a physical or operational address for CNR registration |

| Capital | No statutory minimum | Declared capital is registered but not subject to a legal floor |

| Liability | Unlimited personal liability | Owner's personal assets are fully exposed to business debts |

| Privacy | Owner's name appears in public registry | CNR records are accessible to third parties |

Focus Points

- Taxation: Subject to income tax at graduated rates under the Ley del Impuesto sobre la Renta; VAT registration required if annual turnover exceeds the threshold set by the DGII; no separate corporate tax applies.

- Annual Compliance: Annual income tax return filing with Ministerio de Hacienda; accounting records must be maintained per the Código de Comercio.

- Conversion: Can be converted into a corporate entity (such as an S.A. or S.R.L.), though this requires a formal incorporation process rather than a direct structural amendment.

- Restrictions: Foreign nationals may establish an Empresa Individual, but must hold a valid residency or legal authorization to conduct commercial activity in the country.

- Treaty Access: As a non-corporate entity, access to El Salvador's bilateral tax treaties may be limited or unavailable depending on treaty provisions.

Closing

The Empresa Individual suits small-scale, owner-operated commercial activity where administrative simplicity outweighs the need for liability protection. Its primary advantage is low compliance overhead; its principal drawback is unlimited personal liability, which presents real financial exposure as business operations grow.

Local entrepreneurs or self-employed individuals operating low-risk, small-revenue businesses who do not require a distinct legal entity.

How to Choose the Right Entity Type in El Salvador

Knowing how to choose a business entity in El Salvador before you register prevents structural problems that are far more costly to correct after incorporation.

Why Your Entity Choice Matters

The structure you select has binding legal and financial consequences from the moment it is registered with the Centro Nacional de Registros (CNR).

- Registering a branch office when your operations involve independent local trading may place your business in breach of the Código de Comercio, exposing the parent entity to liability for debts incurred locally.

- Selecting an S.A. or S.R.L. without confirming eligibility under El Salvador's tax treaty network can result in withheld treaty benefits, leaving you subject to full withholding rates in counterpart jurisdictions.

- Forming an S.A. when a single-owner consultancy is all you require adds mandatory audit and shareholders' meeting obligations that generate recurring administrative costs with no corresponding benefit.

- Choosing a structure without the minimum capital or shareholder requirements mandated under the Código de Comercio can result in registration rejection or subsequent nullification.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each correspond to distinct permissible structures under Salvadoran commercial law.

- Ownership and Management: A sole operator may find an S.R.L. sufficient, while multi-party ventures requiring a formal board structure point toward an S.A.

- Tax Objectives: Your eligibility for El Salvador's territorial tax system or any applicable treaty benefits depends on the entity type and its registered activities.

- Substance Capacity: If you cannot maintain a physical presence, employees, or local decision-making, confirm that your chosen structure does not trigger substance-related compliance obligations.

- Privacy Requirements: Director and shareholder information filed with the CNR is accessible through public registry searches, which may influence your structuring approach.

- Exit Strategy: Not all Salvadoran entities permit redomiciliation or conversion; verify whether your preferred structure allows those options before committing.

The full text of the Código de Comercio is available on the Asamblea Legislativa's official legal database.

Compliance Services for Companies in El Salvador

Maintain good standing with the CNR and meet your ongoing statutory obligations under Salvadoran commercial law.

Conclusion

Selecting the right structure is one of the first binding decisions in any El Salvador company incorporation process. Each entity under the Código de Comercio carries distinct implications for liability, governance, and operational scope. The Sociedad Anónima suits medium-to-large operations and foreign investors requiring capital flexibility; the S.R.L. fits smaller ventures where ownership control takes priority. Partnerships serve closely held arrangements with specific liability preferences, while branches and representative offices meet the needs of foreign firms testing or maintaining a local presence without a separate legal entity.

The S.A. remains the most commonly registered structure in El Salvador. Regulatory oversight continues to evolve, with the CNR and tax authority DGII both expanding digital filing capabilities. Your choice of entity shapes everything from shareholder exposure to ongoing compliance obligations, making the corporate setup guide principles covered here the starting point for any serious market entry assessment.

How Expanship Can Assist You

Expanship's company formation services El Salvador cover every structure examined in this guide — from a Sociedad Anónima registered with the Centro Nacional de Registros to a Sociedad de Responsabilidad Limitada or a branch office operating under a foreign parent. Each engagement is handled with full awareness of the Commercial Code and the CNR's documentary requirements.

From initial incorporation through ongoing obligations, your firm receives end-to-end support:

- Document preparation, notarization, and apostille legalization

- Registered agent and local registered office provision

- Filing and liaison with the Centro Nacional de Registros (CNR)

- Tax registration with the Ministerio de Hacienda

- Post-incorporation compliance management, including annual reporting

- Banking introduction assistance for corporate account opening

Setting up a business in El Salvador involves multiple government bodies and sequenced deadlines. Expanship coordinates that process on your behalf, so nothing falls through the gaps.

Reach out through Expanship El Salvador to discuss your specific structure and timeline.

Frequently Asked Questions (FAQ)

The Sociedad Anónima (S.A.) is the most frequently formed entity. Its flexible share structure and broad recognition among banks, counterparties, and regulators make it the default choice for both domestic and foreign-owned businesses.

Both structures offer limited liability, but the S.A. can issue transferable shares freely, while transfer of S.R.L. quotas requires consent from other members and is governed by specific provisions of the Commercial Code. Compliance obligations for the S.A. are generally more formal, including statutory audit requirements above certain thresholds.

The S.R.L. provides a relatively higher degree of ownership privacy, as member quotas are not represented by publicly traded instruments. Nominee arrangements are legally permissible but must comply with beneficial ownership disclosure requirements under anti-money-laundering regulations enforced by the Superintendencia del Sistema Financiero.

No. Both the S.A. and S.R.L. require a minimum of two shareholders or quota-holders at formation under the Commercial Code. Partnerships require at least two partners, and a Sociedad en Comandita Simple requires at least one general and one limited partner.

Yes. Foreign nationals may form an S.A. or S.R.L. without residency requirements. A branch office is also available to foreign firms already incorporated abroad, though it requires appointment of a local legal representative and registration with the Centro Nacional de Registros (CNR).

Transformation between entity types is permitted under the Commercial Code through a formal process involving shareholder resolutions, notarial documentation, and re-registration with the CNR. An S.R.L. can be converted to an S.A., though the process involves restating constitutional documents and fulfilling capital requirements applicable to the target structure.

The S.A., S.R.L., Sociedad en Comandita por Acciones, and Sociedad en Comandita Simple all hold separate legal personality upon registration. General partnerships (Sociedad en Nombre Colectivo) also acquire legal personality through CNR registration, though partners retain unlimited joint liability for obligations of the firm.

The Sole Proprietorship (Empresa Individual) has the lightest formal compliance burden, with no board requirements or annual shareholder resolutions. However, the owner bears unlimited personal liability, which limits its suitability for ventures with meaningful financial exposure.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.