Key Takeaways

- The Nonresident Company (NRC), governed by the Companies (Non-Resident) Act, is Nauru's most commonly registered structure due to its tax exemption on offshore income.

- Corporate registration and compliance in Nauru are administered by the Nauru Registrar of Companies, the central authority for all entity filings on the island.

- Resident companies operating in Nauru are subject to domestic tax obligations, distinguishing them from NRCs whose income is sourced abroad.

- Nauru's regulatory environment has evolved toward greater transparency under international compliance pressures, including FATF engagement and exchange of information commitments.

Introduction to Entity Types in Nauru

Nauru is a small island nation in the central Pacific Ocean, situated northeast of Australia and west of Kiribati. An independent republic and the world's smallest island state, it operates under a parliamentary system with sovereignty recognized under international law.

Understanding the types of business entities in Nauru requires familiarity with the Nauru Registrar of Companies, the authority responsible for company registration and corporate compliance on the island. Oversight sits within the broader government framework, and filings are processed through this office.

From a tax standpoint, Nauru has historically maintained a low- to zero-tax environment for certain foreign-owned structures, though domestic tax obligations apply to resident businesses.

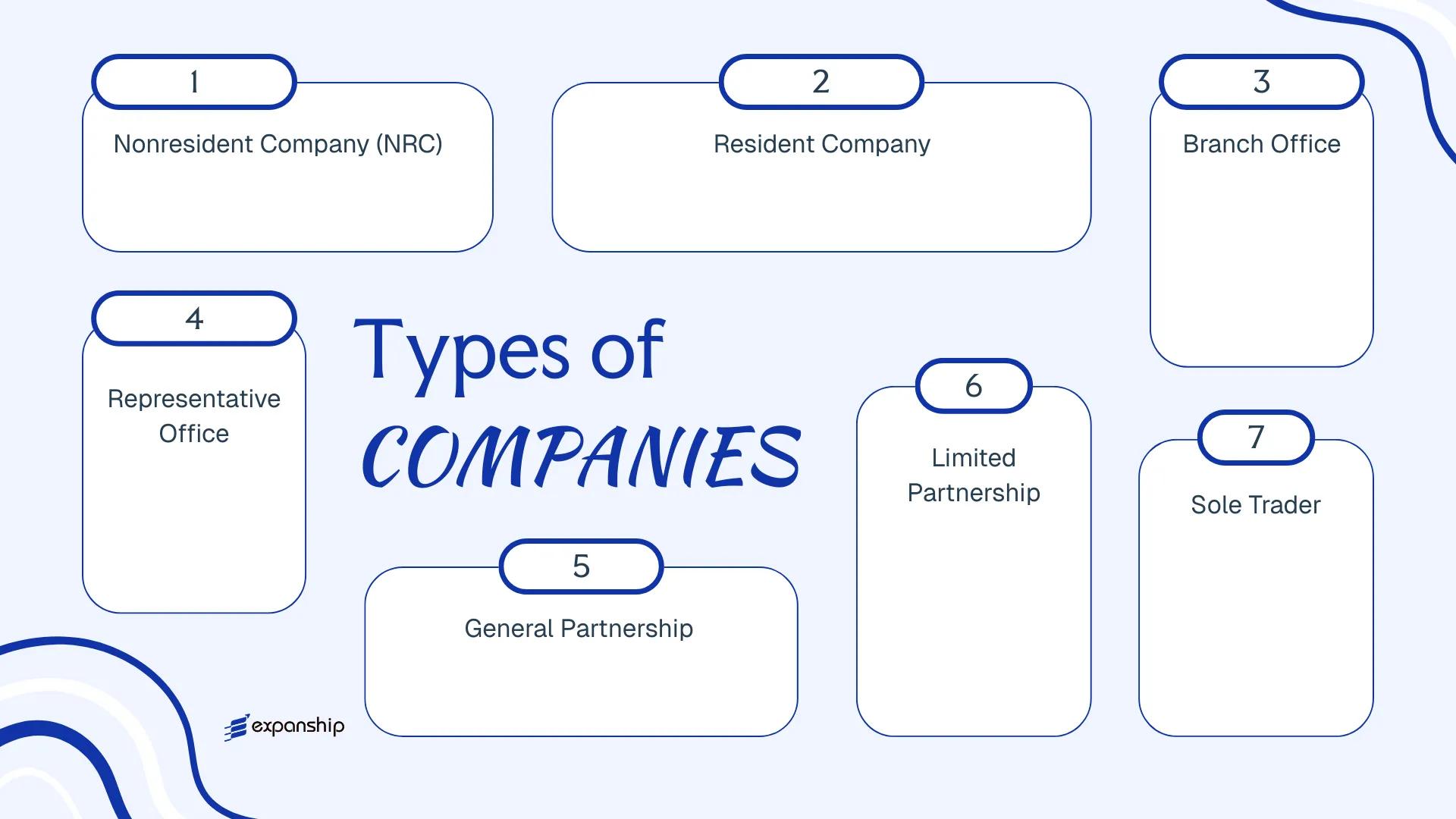

The available Nauru company structures include:

- Nonresident Company (NRC)

- Resident Company

- Branch Office

- Representative Office

- General Partnership

- Limited Partnership

- Sole Trader

Each structure carries distinct registration requirements, liability implications, and operational constraints under the Nauru Companies Act. This article examines each option in detail to help you identify which suits your specific business objectives.

An Overview of Business Structures in Nauru

Under the Nauru Companies Act 1975 and its subsequent amendments, several distinct legal structures are available to both resident and non-resident operators. The Registrar of Companies, operating under the Department of Justice, administers these formations. Each structure carries different implications for liability, tax treatment, and permitted commercial activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Nonresident Company (NRC) | Incorporated company | Limited | Exempt | Not permitted | 1 shareholder | Registrar of Companies | Nauru Companies Act 1975 |

| Resident Company | Incorporated company | Limited | Taxed | Permitted | 1 shareholder | Registrar of Companies | Nauru Companies Act 1975 |

| Branch Office | Foreign entity extension | Unlimited (parent liable) | Taxed | Permitted | N/A | Registrar of Companies | Nauru Companies Act 1975 |

| Representative Office | Foreign entity extension | Non-trading | Exempt | Not permitted | N/A | Registrar of Companies | Nauru Companies Act 1975 |

| General Partnership | Unincorporated firm | Unlimited | Taxed | Permitted | 2 partners | Registrar of Companies | General law / custom |

| Limited Partnership | Hybrid unincorporated firm | Mixed | Taxed | Permitted | 2 partners | Registrar of Companies | General law / custom |

| Sole Trader | Individual operator | Unlimited | Taxed | Permitted | 1 person | Registrar of Companies | General law / custom |

Each of these structures is examined in full in the sections below.

Nonresident Company (NRC) Under the Nauru Companies Act

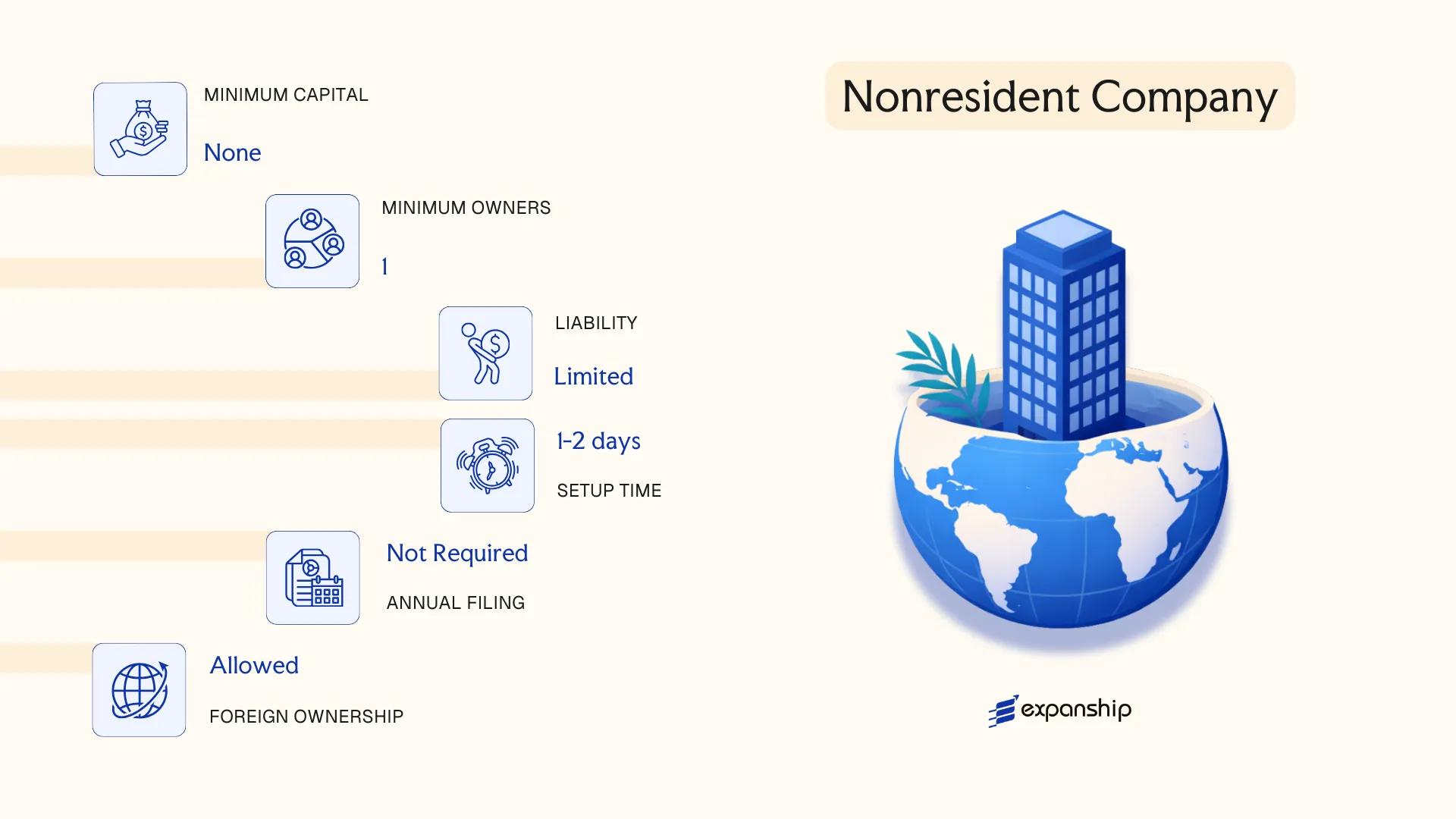

Nauru Nonresident Company (NRC) registration is governed by the Nauru Companies Act 1975, which establishes the NRC as a distinct corporate vehicle separate from domestically oriented resident companies. The entity carries its own separate legal personality, meaning it can hold assets, enter contracts, and incur liabilities in its own name.

Liability is limited to each shareholder's subscribed capital, and the structure is broadly classified as a private company with nonresident characteristics — designed for business conducted outside the republic's borders.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private company limited by shares | Incorporated under the Nauru Companies Act 1975 |

| Members | Shareholders and Directors; minimum 1 of each; no statutory maximum | Directors and shareholders may be the same person; corporate directors generally permitted |

| Local Presence | Registered agent required; no requirement for a local office | Registered agent must be based in Nauru |

| Capital | No prescribed minimum share capital; USD or other currencies accepted | Shares are typically issued at par value |

| Privacy | Beneficial ownership details not routinely placed on public record | Nominee arrangements are commonly used |

Focus Points

- Taxation: NRCs are generally exempt from Nauru corporate income tax on income derived outside the jurisdiction; no VAT, withholding tax, or capital gains tax regime currently applies to qualifying nonresident entities.

- Economic Substance: NRCs conducting relevant activities may be subject to economic substance requirements; entities with purely passive or holding functions should confirm their classification.

- Annual Compliance: Annual renewal fees are payable to maintain the registration in good standing; financial statements are not typically filed publicly.

- Treaty Access: Nauru has a limited double tax treaty network, which restricts the NRC's utility for treaty-based tax planning.

- Restrictions: NRCs are prohibited from conducting business with Nauru residents or owning real property within the republic.

Closing

The NRC suits cross-border trading, international holding structures, and asset protection arrangements where treaty access is not a primary requirement. Its principal advantage is a low compliance burden relative to many offshore jurisdictions, though the absence of a broad tax treaty network is a meaningful constraint for structures requiring treaty benefits.

The NRC is best suited for international entrepreneurs and holding structures seeking a low-cost offshore entity with no local tax exposure on foreign-sourced income.

Company Incorporation in Nauru

Register a Nonresident Company (NRC) in Nauru with end-to-end support from Expanship.

Resident Company Under the Nauru Companies Act

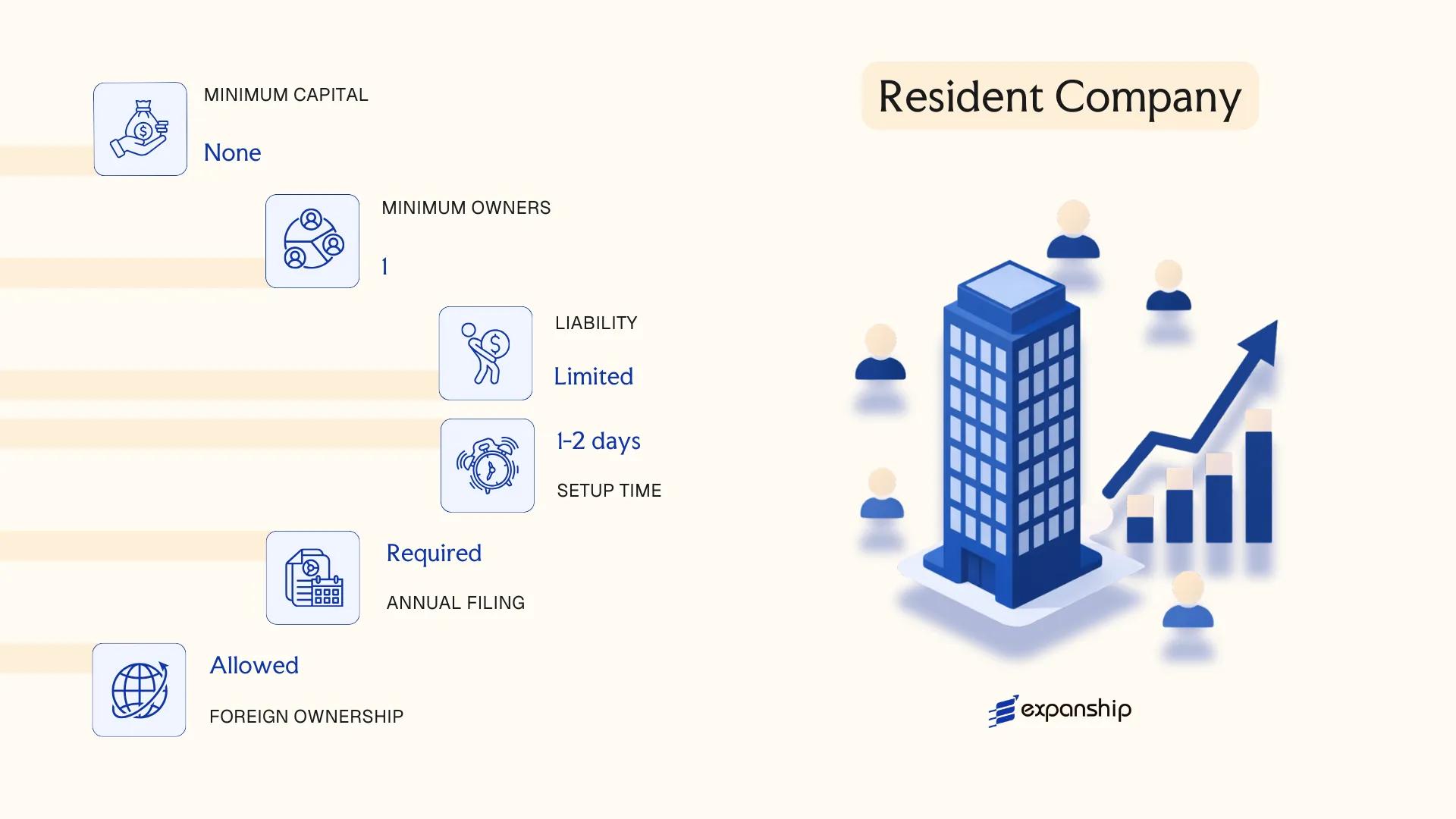

Nauru resident company incorporation is governed by the Companies Act 1972, the same legislation that established the Nonresident Company framework. A resident company carries separate legal personality, meaning the entity exists independently from its members, and shareholders benefit from limited liability protection capped at their respective capital contributions.

Resident companies are structured for ongoing domestic operations within the jurisdiction rather than purely offshore use. The entity is subject to local regulatory oversight and must maintain a registered office address within the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private or Public Company Limited by Shares | Governed under the Companies Act 1972 |

| Members | Shareholders (min. 1, no statutory maximum for private; public requires broader membership) | Directors: min. 1; no residency requirement confirmed by statute |

| Local Presence | Registered office in Nauru required | No confirmed mandatory resident company secretary requirement under general practice |

| Capital | No prescribed minimum share capital; AUD historically referenced | Shares must be denominated; par value structure applies |

| Privacy | Shareholder and director details filed with the Nauru Government | Records accessible through the corporate registry |

Focus Points

- Taxation: Nauru does not levy corporate income tax, personal income tax, capital gains tax, VAT, or withholding tax, making the tax profile of a resident company equivalent to its nonresident counterpart.

- Economic Substance: No formal economic substance legislation has been enacted; however, operational activity within the territory is expected for resident entities.

- Annual Compliance: Annual returns and maintenance of statutory registers are required under the Companies Act 1972.

- Treaty Access: Nauru has a limited tax treaty network, which restricts treaty-based withholding relief for resident entities.

- Conversion: Conversion between resident and nonresident status may be possible under the Act, though the procedural pathway should be confirmed with local counsel.

Closing

Resident companies suit businesses conducting actual trade, providing local services, or establishing an operational base within the territory. The absence of corporate tax is a genuine structural advantage, though the jurisdiction's limited infrastructure, small domestic market, and restricted treaty network present practical constraints for scaling commercial activity.

Local trading operations, domestically focused service businesses, or entities requiring a fully incorporated presence within the territory rather than an offshore holding structure.

Foreign Entities in Nauru [Branch Office, Representative Office]

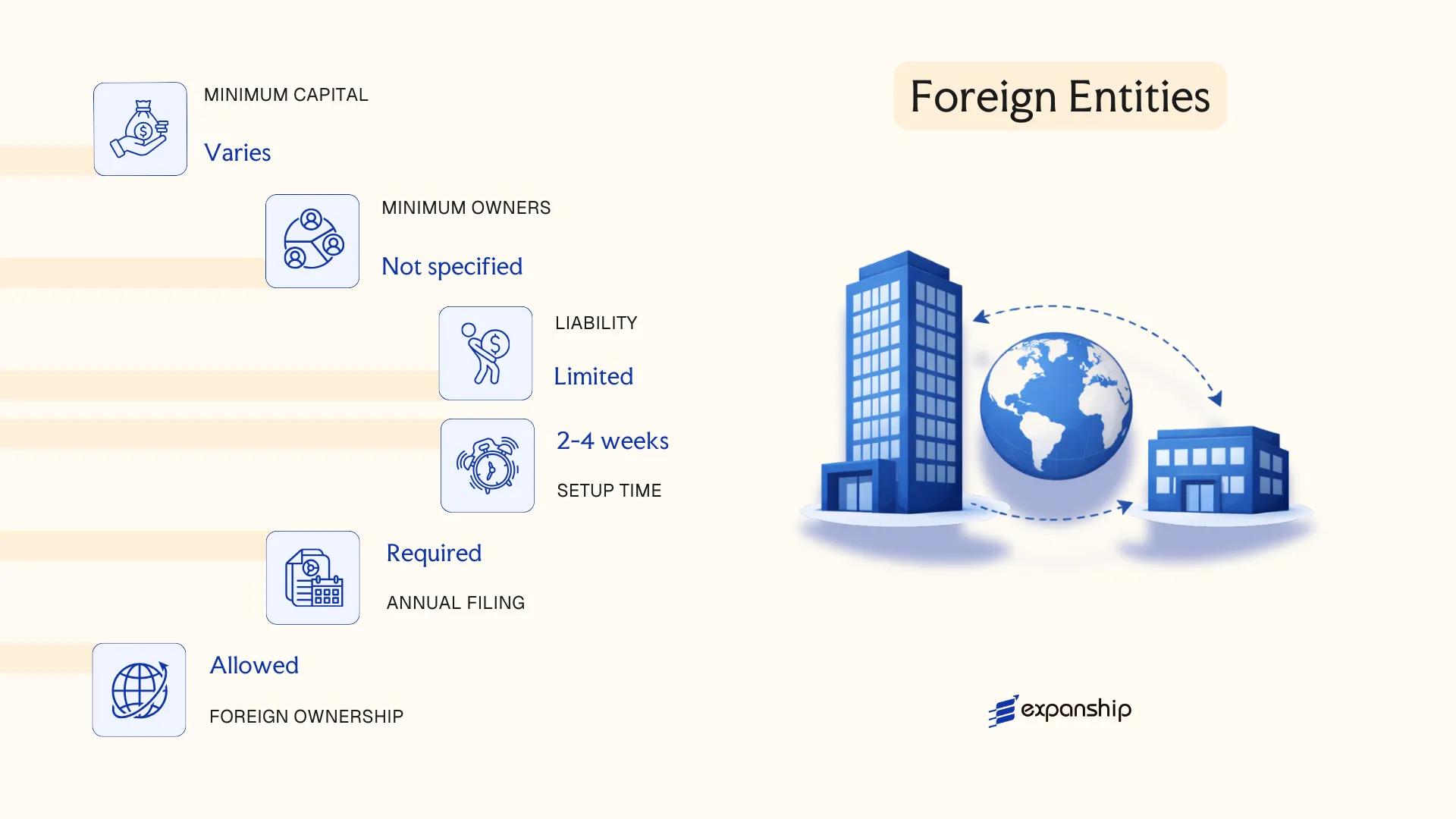

A foreign company branch office Nauru registration allows an overseas entity to conduct business activities without incorporating a separate local company. Under the Nauru Companies Act 1972, a branch is treated as an extension of its parent rather than a distinct legal entity, meaning the parent company retains full liability for the branch's obligations.

Nauru does not maintain a formally codified "representative office" structure under its companies legislation in the way some jurisdictions do. Foreign firms wishing to maintain a limited commercial presence — such as market research or liaison activities — typically operate informally or through contractual arrangements, subject to guidance from the Nauru Government's relevant administrative authorities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Extension of foreign parent | No separate legal personality; parent bears full liability |

| Registered Agent | Required | A locally appointed agent must be maintained for service of process |

| Registered Office | Required | Physical address within Nauru must be on file |

| Capital | No prescribed minimum | Parent entity's capital structure applies |

| Privacy | Parent details disclosed | Foreign company particulars filed with authorities |

| Permitted Activities | Governed by parent's objects | Activities must align with parent's constitutional documents |

Focus Points

- Taxation: Nauru does not currently impose corporate income tax, withholding tax, or VAT, though branch profits may be subject to tax in the parent's home jurisdiction.

- Annual Compliance: Filing obligations include maintaining updated particulars of the foreign parent with the registrar.

- Treaty Access: Nauru has a limited tax treaty network; branch structures should not be assumed to confer treaty benefits.

- Restrictions: Certain regulated sectors may require additional licensing regardless of the branch structure used.

Closing

A branch is suited to foreign businesses that need an operational footprint without establishing a standalone entity, though the absence of limited liability protection at the local level is a material structural drawback.

Best suited for established foreign companies seeking a direct operational presence where a subsidiary's administrative overhead is not warranted.

Partnerships in Nauru [General Partnership, Limited Partnership]

Partnership registration in Nauru is governed by general partnership law principles derived from Nauru's statutory framework, though the jurisdiction does not maintain the same depth of dedicated partnership legislation found in larger offshore centers. Partnerships do not carry separate legal personality in the way a company does — partners remain personally liable for the obligations of the firm unless liability is formally limited by structure.

A limited partnership separates passive investors from active managers, with limited partners shielded from personal liability beyond their capital contribution, while general partners retain unlimited exposure.

Key Characteristics

| Requirement | General Partnership | Limited Partnership |

|---|---|---|

| Legal Personality | None — partners contract directly | None — entity acts through general partner |

| Members | Partners (minimum 2, no statutory maximum) | Minimum 1 general partner + 1 limited partner |

| Liability | Unlimited for all partners | Unlimited for general partner; limited for limited partners |

| Local Presence | Registered address required | Registered address required |

| Capital | No minimum; contributions defined in partnership agreement | Defined by limited partner's agreed contribution |

| Privacy | Partnership agreement not publicly filed | Partial — general partner details may be disclosed |

Focus Points

- Taxation: Nauru does not levy corporate income tax, personal income tax, or VAT, so partnership income generally passes through to partners without entity-level tax; withholding tax and stamp duty obligations should be confirmed under current regulations.

- Annual Compliance: Partnership agreements govern internal obligations; external filings depend on registration requirements under applicable Nauru law.

- Treaty Access: Partnerships typically do not access tax treaties directly, as treaty benefits flow to the partners based on their own residency status.

- Restrictions: General partners in a limited partnership must not allow limited partners to participate in management, or those partners risk losing liability protection.

- Conversion: Conversion between partnership types or to a corporate structure is possible but requires formal legal restructuring.

Sub-Types

General Partnership

All partners share management authority and bear unlimited joint and several liability. This structure suits small, closely held business arrangements where all participants are actively involved and mutually accountable.

Limited Partnership

Designed for investment arrangements where passive capital contributors participate without taking on management risk. The general partner administers the business; limited partners receive profit distributions proportionate to their contribution without exposure beyond their invested capital.

Partnerships suit joint ventures, professional services arrangements, or investment vehicles where pass-through treatment and flexible governance are priorities. The absence of entity-level taxation is a structural advantage, though the unlimited liability exposure of at least one partner remains a material drawback for risk-sensitive structures.

Partnerships in Nauru are best suited for two or more parties seeking a light-compliance, pass-through structure for a defined commercial or investment purpose, where at least one party is prepared to accept general partner liability.

Sole Trader

Operating as a sole trader business Nauru is the simplest form of commercial activity available to individuals. Governed primarily by general business registration requirements under Nauruan law, this structure involves no separation between the individual and the business — the proprietor and the enterprise are legally the same person.

There is no limited liability protection. All debts and obligations of the business rest directly with you as the individual, meaning personal assets are fully exposed to business risk.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Members | Single individual proprietor | No minimum capital partners or shareholders |

| Local Presence | Business registration with the Nauru government | A local registered address is generally required |

| Capital | No statutory minimum | Funded entirely by the proprietor |

| Privacy | Owner's identity tied directly to the business | No beneficial ownership separation |

Focus Points

- Taxation: Subject to personal income tax on business profits; no corporate tax layer applies, and VAT obligations depend on turnover thresholds under applicable Nauruan fiscal rules.

- Annual Compliance: Basic renewal of business registration; no audited financial statements required.

- Liability: Unlimited personal liability for all business debts and legal claims.

- Conversion: Can be converted into a registered company structure if the business grows or requires limited liability.

- Restrictions: Not suitable for raising external capital or issuing equity to third parties.

Closing

This structure suits individuals providing services or conducting small-scale local trade where administrative simplicity is the priority, though the absence of liability protection makes it unsuitable for higher-risk commercial activity.

Local individual traders or self-employed professionals operating on a small scale with limited third-party risk exposure.

How to Choose the Right Entity Type in Nauru

Choosing the right business entity in Nauru depends on operational intent, tax position, and compliance capacity — not on which structure appears simplest at registration.

Why Your Entity Choice Matters

Misalignment between structure and purpose produces concrete legal and financial consequences.

- Registering a Nonresident Company and then conducting local trading operations puts the entity in breach of the Nauru Companies Act, which can result in striking off or financial penalties.

- Selecting a tax-exempt offshore entity forecloses any access to double taxation treaty benefits, since treaty entitlement generally requires tax residency in the contracting state.

- Choosing a structure that requires audited financial statements when your business is a single-person operation creates recurring compliance costs that serve no regulatory purpose at that scale.

- Forming a standard company when asset protection or succession planning is the primary objective locks you into annual shareholder obligations that would not apply under a trust or foundation arrangement.

Key Factors to Consider

- Business Activity: Passive asset holding, active trading, and regulated sectors each point toward a distinct structure under Nauruan law.

- Local vs. Offshore Operations: Transacting with Nauruan residents requires a resident company or registered foreign entity, not an offshore vehicle.

- Tax Objectives: Your need for full tax exemption or treaty network access determines whether a resident or nonresident structure is appropriate.

- Ownership and Management: Single-owner consultancies and multi-party joint ventures have materially different governance requirements that the choice of entity must accommodate.

- Substance Capacity: If you cannot maintain a genuine operational presence on the island, your entity type must not carry substance obligations you are unable to satisfy.

- Exit Strategy: Not all Nauruan structures permit redomiciliation or conversion, so your anticipated exit path should inform the initial formation decision.

Compliance Services for Companies in Nauru

Maintain your Nauruan entity in good standing with registered agent support, annual filing management, and ongoing regulatory monitoring.

Conclusion

Setting up a company in Nauru means working within a small but distinct legislative framework, primarily governed by the Nauru Companies Act and the Companies (Non-Resident) Act. The Nonresident Company remains the most registered structure, favored by foreign investors for its tax exemption on offshore income. Resident companies suit locally operating businesses subject to domestic tax obligations. Branch and representative offices serve foreign entities testing the market without separate legal incorporation. Partnerships and sole trader arrangements address smaller-scale or professional operations where limited liability is not a priority.

Nauru's regulatory posture has shifted toward greater transparency in recent years, reflecting broader international compliance pressures, including FATF engagement and exchange of information commitments. Your choice of structure will ultimately depend on residency status, operational scope, and the nature of your business activities. Expanship's team works directly with these frameworks to help you proceed with clarity.

How Expanship Can Assist You

Expanship's Nauru company formation services cover the full process — from selecting between a Nonresident Company and a Resident Company under the Nauru Companies Act to filing with the Nauru Registrar of Companies. Each structure carries distinct obligations, and getting the initial setup right determines how smoothly ongoing compliance runs.

Across the incorporation and post-registration cycle, Expanship assists with:

- Document preparation and notarization or legalization

- Registered agent and registered office provision in Nauru

- Government filing and direct liaison with the Registrar of Companies

- Post-incorporation compliance management, including annual returns

- Banking introduction assistance for newly incorporated entities

Corporate services in Nauru involve a small but specific regulatory environment, and every step has a defined procedural path. Expanship's team handles that path on your behalf.

Reach out directly through Expanship Nauru to discuss your business registration requirements.

Frequently Asked Questions (FAQ)

The Nonresident Company (NRC) under the Nauru Companies Act is the most frequently registered structure. Its appeal stems primarily from the absence of corporate income tax on foreign-sourced profits and the minimal local presence requirements.

A Resident Company is subject to local tax obligations and is permitted to trade within Nauru, while an NRC is restricted from conducting business with Nauruan residents and derives its tax advantages specifically from operating outside the jurisdiction. Compliance obligations for resident entities are considerably more extensive, including local accounting and reporting requirements that do not apply to NRCs in the same form.

The NRC offers the most privacy among available structures. Beneficial ownership details are not required to be disclosed on a public register, and nominee director and shareholder arrangements are permissible under the Nauru Companies Act.

A sole trader is by definition a one-person operation, and an NRC or Resident Company can be formed with a single director and shareholder. General and limited partnerships, however, require a minimum of two partners, making sole formation legally impossible under those structures.

Foreign nationals may register an NRC, Resident Company, or establish a branch of a foreign corporation. The NRC is specifically structured to accommodate nonresident foreign entrepreneurs, with no requirement for local directors or shareholders under the standard provisions of the Nauru Companies Act.

The Nauru Companies Act provides general mechanisms for corporate restructuring, though specific conversion procedures between entity types, such as from a partnership to a company, would require dissolution and re-registration rather than a statutory conversion. Professional legal advice specific to the target structure is advisable before initiating any such transition.

NRCs and Resident Companies hold separate legal personality distinct from their shareholders. Sole traders and general partnerships do not, meaning personal liability exposure remains for the individual or partners involved in those arrangements.

The NRC carries the lightest compliance burden among registered structures, with no requirement to file annual financial statements publicly and reduced local regulatory interaction. By contrast, Resident Companies and branch offices face more regular reporting obligations tied to their domestic activity.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.