Key Takeaways

- Nepal recognizes eight distinct business entity types under its regulatory framework, ranging from the Public Limited Company (Sārvjanik Limited Company) to the Sole Proprietorship (Ekakal Byabasaya), each with different ownership, liability, and compliance requirements.

- The Private Limited Company is the most commonly registered business form under the Companies Act 2063, used by both domestic entrepreneurs and foreign investors for its combination of liability protection and operational flexibility.

- Company incorporation and regulation in Nepal falls under the Office of the Company Registrar (OCR), while corporate tax obligations are governed by the Income Tax Act, 2002 and administered by the Inland Revenue Department.

- Foreign firms requiring a limited-purpose presence in Nepal may establish a Branch Office, Liaison Office, or Project Office rather than incorporating a locally registered company.

Introduction to Entity Types in Nepal

Nepal is a landlocked country in South Asia, bordered by India to the south and China to the north. It is an independent federal democratic republic, and business registration falls under the jurisdiction of the Office of the Company Registrar (OCR), the body responsible for incorporating and regulating companies under the Companies Act, 2006.

The country operates a residence-based tax system, with corporate tax obligations governed by the Income Tax Act, 2002 and administered by the Inland Revenue Department.

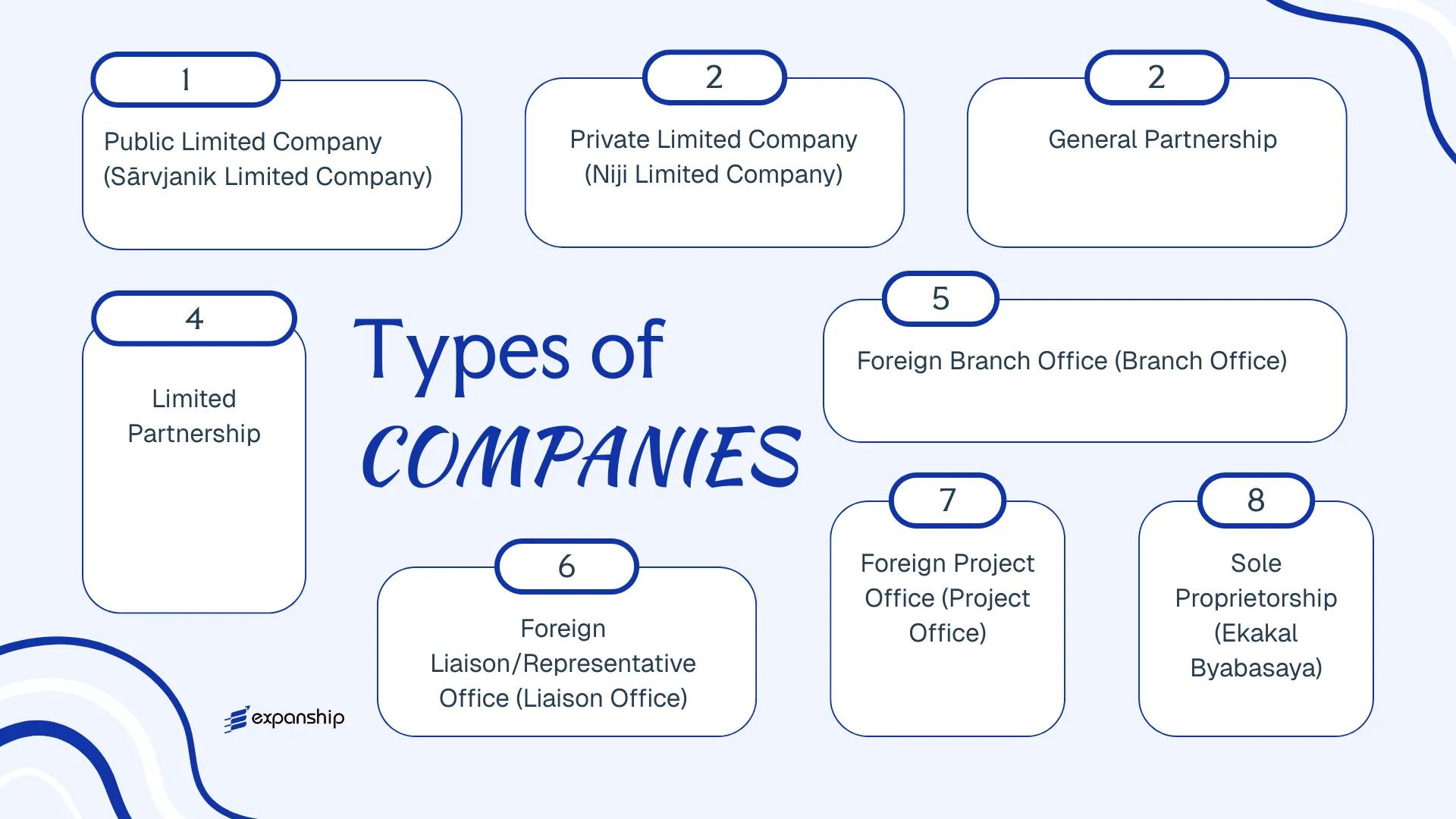

Several types of business entities in Nepal are available to both domestic and foreign investors. These include the Public Limited Company, Private Limited Company, General Partnership, Limited Partnership, Branch Office, Liaison Office, Project Office, and Sole Proprietorship. Each structure carries distinct requirements around ownership, liability, and regulatory compliance.

This article examines each of these Nepal company types in detail — covering formation requirements, capital thresholds, governance obligations, and the considerations most relevant to foreign investors and locally incorporated businesses alike.

An Overview of Business Structures in Nepal

Six principal business structures are available under Nepal's company law framework, governed primarily by the Companies Act, 2006 (2063 BS) and supplemented by the Private Firm Registration Act, 1958 and the Partnership Act, 1964. Foreign entities operating without local incorporation are additionally subject to the Foreign Investment and Technology Transfer Act, 2019 (FITTA). Each structure carries distinct liability, ownership, and operational characteristics suited to different commercial purposes.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company | Separate legal entity | Limited to shares | Taxed | Yes | 7 shareholders | OCR | Companies Act, 2006 |

| Private Limited Company | Separate legal entity | Limited to shares | Taxed | Yes | 1 shareholder | OCR | Companies Act, 2006 |

| General Partnership | Unincorporated firm | Unlimited, joint | Taxed | Yes | 2 partners | OCR | Partnership Act, 1964 |

| Limited Partnership | Unincorporated firm | Mixed | Taxed | Yes | 2 partners | OCR | Partnership Act, 1964 |

| Branch Office | Extension of parent | Parent liable | Taxed | Restricted | N/A | DoI / OCR | FITTA, 2019 |

| Liaison Office | Extension of parent | Parent liable | Exempt | No | N/A | DoI | FITTA, 2019 |

| Project Office | Extension of parent | Parent liable | Taxed | Project only | N/A | DoI | FITTA, 2019 |

| Sole Proprietorship | Unregistered / registered firm | Unlimited, personal | Taxed | Yes | 1 owner | Local authority / OCR | Private Firm Registration Act, 1958 |

Each of these structures is examined in full in the sections below.

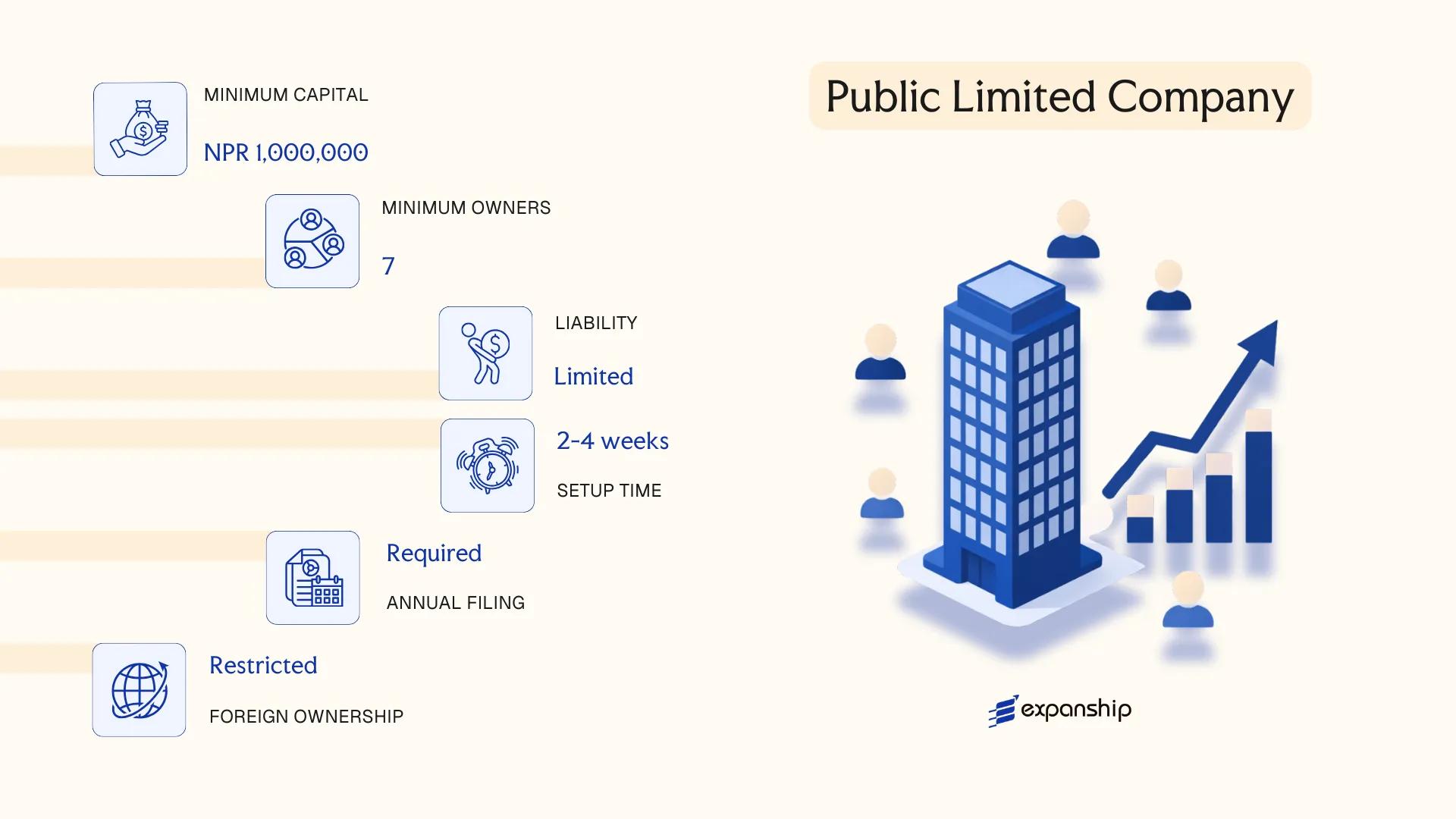

Public Limited Company (Sārvjanik Limited Company)

A public limited company Nepal Sarvjanik structure is governed by the Companies Act, 2006 (2063 BS), administered by the Office of the Company Registrar (OCR). The entity carries separate legal personality, meaning its rights and obligations are distinct from those of its shareholders.

Shares in a Sārvjanik Limited Company may be offered to the general public and, subject to regulatory approval from the Securities Board of Nepal (SEBON), listed on the Nepal Stock Exchange (NEPSE). This makes it the appropriate vehicle when your business intends to raise capital from the public.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (Sārvjanik Limited Company) | Separate legal personality; limited liability |

| Members | Shareholders: minimum 7; no statutory maximum | Directors: minimum 3; minimum 1 must be independent |

| Minimum Capital | No statutory minimum paid-up capital for non-listed firms | SEBON sets capital thresholds for listing eligibility |

| Local Presence | Registered office in Nepal required | Must maintain a physical address on OCR record |

| Shares | Shares freely transferable; public offering permitted | Secondary market listing requires SEBON approval |

| Privacy | Shareholder register and financial statements are public documents | OCR filings are publicly accessible |

Focus Points

- Taxation: Corporate income tax applies at 25% (general rate); VAT at 13% on applicable supplies; withholding tax applies to dividends, interest, and service fees; stamp duty applies on share transfers.

- Annual Compliance: Mandatory annual general meeting, audited financial statements filed with the OCR, and periodic disclosures to SEBON if listed.

- Conversion: A private limited company may convert to a public limited company under the Companies Act, 2006, subject to OCR approval and restructuring of its shareholding to meet minimum member thresholds.

- Foreign Ownership: Permitted in most sectors, though sector-specific restrictions under the Foreign Investment and Technology Transfer Act, 2019 (FITTA) may cap foreign equity.

- Treaty Access: Nepal maintains a limited network of double taxation avoidance agreements (DTAAs); access depends on the shareholder's country of residence.

Closing

A Sārvjanik Limited Company suits businesses seeking public capital investment, particularly in banking, insurance, hydropower, and manufacturing sectors where SEBON-regulated fundraising is common. The freely transferable share structure supports broad ownership, though the disclosure obligations and regulatory oversight from both OCR and SEBON add significant ongoing compliance weight.

Large-scale enterprises or joint ventures intending to list on NEPSE or raise funds from the Nepali public.

Company Incorporation in Nepal

Incorporate a public or private limited company in Nepal with end-to-end OCR filing support.

Private Limited Company (Niji Limited Company)

Governed by the Companies Act 2006 (2063 BS), the private limited company Nepal Niji structure is the most widely used corporate form for small to medium-sized businesses, joint ventures, and foreign-owned operations. The entity holds separate legal personality distinct from its shareholders, with liability confined to each member's unpaid share capital.

Registration is administered by the Office of the Company Registrar (OCR) under the Ministry of Industry, Commerce and Supplies. A Niji Limited Company Nepal registration restricts the transfer of shares and prohibits any public invitation to subscribe to its securities, which distinguishes it structurally from a public company.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company | Separate legal entity; limited liability |

| Members | Shareholders & Directors | Min. 1 shareholder, max. 101; Min. 1 director (natural person) |

| Local Presence | Registered office address in Nepal required | Must be maintained throughout the company's existence |

| Capital | NPR; no statutory minimum paid-up capital for most sectors | Sector-specific minimums may apply (e.g., banking, finance) |

| Share Transfer | Restricted by articles of association | Shares cannot be offered to the general public |

| Privacy | Shareholder details filed with OCR; public registry | Beneficial ownership disclosure required |

Focus Points

- Taxation: Subject to corporate income tax (generally 25%, with sector variations); VAT registration required if annual turnover exceeds NPR 5 million; withholding tax applies to dividends, royalties, and service payments.

- Annual Compliance: Annual general meeting, audited financial statements, and annual return filed with the OCR are mandatory each fiscal year.

- Treaty Access: Nepal has signed double taxation avoidance agreements with a limited number of countries; treaty benefits depend on the residency of the counterparty.

- Foreign Ownership: Foreign equity participation requires prior approval from the Department of Industry or relevant sector regulator, and repatriation of profits is subject to Foreign Investment and Technology Transfer Act 2019 (FITTA) procedures.

- Conversion: A private company may convert to a public limited company upon meeting the prescribed threshold requirements under the Companies Act 2006.

This structure suits trading operations, wholly owned subsidiaries, and joint ventures where direct control and contained liability are priorities. One clear limitation is that capital raising is restricted — the firm cannot issue shares to the public or list on the Nepal Stock Exchange.

Foreign investors and domestic entrepreneurs seeking a controlled, privately held operating entity with defined liability boundaries in Nepal.

Partnership Entities [General Partnership, Limited Partnership]

Governed by the Partnership Act, 2020 (2063 B.S.), partnership firms in Nepal do not carry separate legal personality — the firm and its partners are treated as one legal unit, meaning partners bear direct liability for the firm's obligations. Partnership firm registration Nepal requires filing with the relevant District Administration Office or the Department of Industry, depending on the nature of the business activity.

Two recognised structures exist under the Act: a general partnership, where all partners share management rights and unlimited liability, and a limited partnership, which introduces liability distinctions between partner classes.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated firm | No separate legal personality from partners |

| Members | Partners; minimum 2, maximum 20 | Referred to as "partners" under the Act |

| Liability | General: unlimited for all partners; Limited: general partner unlimited, limited partner capped at contribution | Mixed structures available under limited partnership |

| Registered Office | Physical office required in Nepal | Must be maintained throughout the firm's life |

| Capital | No statutory minimum; denominated in NPR | Contribution terms defined in the partnership deed |

| Privacy | Partnership deed is registered but not broadly public | Deed details accessible to regulatory authorities |

Focus Points

- Taxation: Partnership income is taxed at the firm level under the Income Tax Act, 2058; partners are also taxed on distributed income, creating a pass-through-adjacent structure with potential double taxation exposure.

- VAT: Registration required if annual turnover exceeds the prescribed threshold under the Value Added Tax Act, 2052.

- Annual Compliance: Firms must renew registration periodically and file tax returns with the Inland Revenue Department.

- Treaty Access: Partnerships generally do not qualify as tax residents for treaty purposes, limiting access to Nepal's double tax agreements.

- Conversion: Conversion from a partnership to a private limited company is permissible but requires a separate incorporation process under the Companies Act, 2063.

Sub-Types

General Partnership (Samanya Saajhedari)

All partners hold equal management authority and carry unlimited personal liability for the firm's debts. This structure is commonly used for small professional practices or family-run trading businesses where partners are closely involved in daily operations.

Limited Partnership (Seemit Saajhedari)

At least one general partner retains unlimited liability and management control, while limited partners contribute capital and face liability only to the extent of their investment. Limited partners are restricted from participating in management, which distinguishes this structure from a general partnership.

Closing

Partnership firms suit small-scale domestic trade, professional service providers, and family businesses where formal incorporation is not a priority. The absence of a separate legal personality is a practical constraint for any business seeking external financing or contractual separation from its owners.

Partnership structures are best suited for small domestic businesses or professional service arrangements where partners know each other well and external investment is not anticipated.

Foreign Business Entities [Branch Office, Liaison/Representative Office, Project Office]

Registering a foreign company branch office in Nepal is governed primarily by the Foreign Investment and Technology Transfer Act, 2019 (FITTA 2019) and the Companies Act, 2006. Unlike locally incorporated entities, these structures do not create a separate legal person distinct from the parent company — the foreign parent retains full legal liability for the operations conducted through them.

Registration and ongoing oversight fall under the Department of Industry (DoI) or the Investment Board Nepal (IBN) for larger projects, with the Office of the Company Registrar (OCR) handling formal filings.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Parent company bears all liabilities |

| Permitted Activities | Varies by entity type: trading/operations (Branch), promotion only (Liaison), specific project (Project Office) | Revenue-generating activity is restricted for Liaison Offices |

| Local Presence | Registered address in Nepal; appointed local representative required | OCR-compliant address mandatory |

| Capital | Foreign currency; minimum investment thresholds apply under FITTA 2019 | Minimum NPR 20 million for most foreign investment approvals |

| Approvals Required | DoI or IBN approval prior to OCR registration | IBN handles investments above NPR 6 billion |

| Duration | Branch and Liaison Offices renewed periodically; Project Office tied to project timeline | Renewal typically required every few years |

Focus Points

- Taxation: Branch offices are subject to corporate income tax at 25% on Nepal-sourced income; an additional 5% repatriation tax applies on remitted profits; VAT registration is required if turnover thresholds are met.

- Permitted Activities: Liaison offices cannot earn revenue locally — any commercial activity triggers reclassification obligations.

- Compliance: Annual audited accounts, tax filings with the Inland Revenue Department, and periodic renewal of registration certificates are required.

- Treaty Access: Nepal has limited double taxation agreements in force; treaty benefits may not be available depending on the parent's jurisdiction.

- Conversion: Converting a branch or liaison office into a locally incorporated entity requires fresh registration under the Companies Act, 2006 — there is no automatic conversion mechanism.

Sub-Types

Branch Office

A Branch Office may conduct operational and, subject to sector approvals, revenue-generating activities in Nepal. It is the appropriate structure when the foreign parent intends active business operations rather than mere representation.

Liaison / Representative Office

Permitted activities are restricted to market research, coordination, and promotion on behalf of the parent. A representative office Nepal setup cannot sign commercial contracts or invoice local clients in its own capacity.

Project Office

Project office registration Nepal is available where a foreign entity has secured a specific contract or government-approved project. Its existence is tied to the project duration and the office must wind down upon project completion.

Closing

Foreign business structures suit multinational firms testing the market, executing a defined contract, or supporting a parent's regional operations without committing to full local incorporation. The absence of separate legal personality is the primary structural constraint — the parent remains exposed to all liabilities incurred in-country.

Foreign companies entering Nepal for a specific project, initial market exploration, or regional coordination, before committing to a locally incorporated entity.

Sole Proprietorship (Ekakal Byabasaya)

A sole proprietorship Nepal — locally termed Ekakal Byabasaya — is the simplest form of business registration available to individual operators. Governed by the Private Firm Registration Act, 1958 (2014 B.S.), this structure carries no separate legal personality; the proprietor and the business are treated as a single legal unit.

Because the firm is not legally distinct from its owner, unlimited personal liability applies. All debts and obligations of the business extend directly to the proprietor's personal assets.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated private firm | No separate legal personality from the proprietor |

| Members | Single proprietor | Only one individual; no concept of shareholders or directors |

| Local Presence | Registered business address required | Must be registered with the relevant District Administration Office (DAO) or municipality |

| Capital | NPR; no statutory minimum | Declared capital is recorded at registration but no minimum threshold is mandated |

| Privacy | Proprietor's name is publicly linked to the firm | Registration records are accessible through the DAO |

| Registration Authority | Department of Industry or local DAO | Micro and cottage-scale firms register locally; larger trading firms may involve additional bodies |

Focus Points

- Taxation: Subject to personal income tax under the Income Tax Act, 2058 (2002); rates are progressive up to 36% for individuals; VAT registration is required if annual turnover exceeds NPR 5 million for goods or NPR 2 million for services.

- Annual Compliance: Renewal of the firm registration is required annually through the relevant local authority; tax returns must be filed with the Inland Revenue Department (IRD).

- Conversion: Can be converted into a private limited company, though the process requires fresh incorporation rather than a structural transformation of the existing firm.

- Treaty Access: As an unincorporated entity, it does not independently access double tax treaty benefits; income flows through to the proprietor as an individual.

- Restrictions: Foreign nationals are generally not permitted to register a sole proprietorship; this structure is reserved for Nepali citizens.

Closing Paragraph

Ekakal Byabasaya registration suits small-scale domestic trading, artisan work, and service providers operating independently without external investors. The primary advantage is minimal setup cost and administrative simplicity; the significant drawback is unlimited personal liability, which exposes the proprietor's private assets to all business obligations.

This structure is best suited for Nepali citizens running small, low-risk operations who require a formal business registration without the cost or complexity of incorporation.

How to Choose the Right Entity Type in Nepal

Choosing the right business entity in Nepal is a structural decision with direct legal, tax, and operational consequences — getting it wrong creates problems that are often difficult and costly to unwind.

Why Your Entity Choice Matters

The Companies Act, 2063 (2006) governs company formation and conduct in Nepal. Registering under the wrong framework can produce outcomes such as:

- Selecting a Private Limited Company when your business requires public capital raising puts you in breach of structural requirements under the Companies Act, as private companies are prohibited from inviting public subscriptions.

- Choosing a Branch Office structure when your foreign parent intends to conduct independent commercial activity — rather than extend the parent's operations — results in a mismatch with the conditions set by the Department of Industry, exposing the entity to regulatory action.

- Registering as a Sole Proprietorship when you have multiple investors creates personal unlimited liability for all parties, since that structure has no capacity for shared ownership.

- Forming a General Partnership when your activity requires foreign investment approval means the structure may be ineligible under the Foreign Investment and Technology Transfer Act, 2075 (2019).

Key Factors to Consider

- Business Activity: Trading, manufacturing, and service activities open to foreign participation each have permitted entity types under Nepal's Foreign Investment and Technology Transfer Act, 2075; your activity category determines which structures are available.

- Ownership Structure: A single Nepali national can operate as a Sole Proprietorship, but multi-party or foreign-involved ownership requires a Private or Public Limited Company registered with the Office of the Company Registrar.

- Capital Requirements: Public Limited Companies must meet minimum paid-up capital thresholds set by the Office of the Company Registrar, making this structure unsuitable for small or early-stage operations.

- Liability Exposure: Partnership entities carry unlimited personal liability for general partners, whereas limited companies provide liability limited to each shareholder's capital contribution.

- Foreign Involvement: Any entity involving foreign equity must obtain approval from the Department of Industry and comply with repatriation rules administered by Nepal Rastra Bank.

- Operational Scope: Liaison and Project Offices are restricted from generating local revenue; if your business will invoice Nepali clients, a company structure registered under the Companies Act is required.

Compliance Services for Companies in Nepal

Ongoing compliance support for companies registered in Nepal, including annual filings, audit coordination, and regulatory reporting with the Office of the Company Registrar.

Conclusion

Selecting the right structure is the first substantive decision in any Nepal company incorporation summary guide, and each entity type covered here serves a distinct purpose. Private Limited Companies remain the most commonly registered business form under the Companies Act 2063, favored by domestic entrepreneurs and foreign investors alike for their liability protection and operational flexibility. Public Limited Companies suit ventures that anticipate public capital markets participation. General and Limited Partnerships work for smaller, relationship-based commercial arrangements. Branch and Liaison Offices serve foreign firms requiring a controlled, limited-purpose presence. Sole Proprietorships fit individual traders operating at a local scale.

Nepal's regulatory framework continues to develop, with the Department of Industries and the Office of the Company Registrar progressively digitizing registration processes. Bilateral investment treaty coverage has expanded gradually, strengthening the formal protections available to foreign-owned entities. Engaging qualified local counsel alongside an international corporate services provider gives your business a structured path through these requirements.

How Expanship Can Assist You

Expanship company registration Nepal services cover the full arc of entity formation — from selecting the right structure under the Companies Act, 2063 to completing the registration process with the Office of the Company Registrar (OCR). Whether your plans involve a Private Limited Company, a Branch Office under the Foreign Investment and Technology Transfer Act, 2075, or any other form discussed in this blog, Expanship works with the specific regulatory requirements each entity type carries.

From initial document preparation through to post-incorporation obligations, our team handles the operational groundwork so your business can proceed without administrative delays.

- Document preparation and notarization

- Registered agent and registered office provision in Nepal

- Government filing and OCR liaison

- Post-incorporation compliance management

- Banking introduction assistance for corporate accounts

Reach out to Expanship Nepal to discuss your incorporation requirements directly with our team.

Frequently Asked Questions (FAQ)

The Private Limited Company (Niji Limited Company) is the most frequently incorporated structure. Its liability protection, relatively modest capital requirements, and permissibility for foreign ownership under the Foreign Investment and Technology Transfer Act (FITTA) 2019 make it the default choice for both domestic entrepreneurs and inbound investors.

A Branch Office operates as an extension of its foreign parent and cannot independently own assets or distribute profits locally, while a Private Limited Company is a separate legal entity capable of holding property, entering contracts, and repatriating dividends under FITTA. Tax obligations also differ: a Branch Office is taxed on income attributable to its Nepali operations, whereas a Private Limited Company is subject to corporate income tax on its worldwide income derived in Nepal. Compliance requirements for a Branch Office are generally tied to the parent entity's financial disclosures.

Among registered structures, a Private Limited Company does not require public disclosure of shareholder details in the same manner as a Public Limited Company, whose ownership is more openly accessible. Nominee arrangements are not formally prohibited but are subject to beneficial ownership disclosure requirements under the Companies Act 2006. Director information is filed with the Office of the Company Registrar (OCR) but is not always readily searchable through public portals.

No. A sole proprietorship requires only one individual, and a Private Limited Company can be formed with a minimum of one shareholder and one director under the Companies Act 2006. General and Limited Partnerships, however, require at least two partners, making single-person formation impossible for those structures. A Public Limited Company requires a minimum of seven shareholders.

Foreign nationals may register a Private Limited Company, a Public Limited Company, or establish a Branch, Liaison, or Project Office, provided the relevant sector is open to foreign investment under FITTA 2019 and the Industrial Enterprises Act 2020. Sole proprietorships are restricted to Nepali citizens. Foreign-owned entities typically require registration with both the OCR and the Department of Industry.

Conversion is permitted in limited circumstances. A Private Limited Company may convert to a Public Limited Company under the Companies Act 2006 by satisfying the minimum shareholder and capital thresholds. Conversion from a partnership to a company structure is not directly prescribed by statute and generally requires dissolution of the original entity followed by fresh incorporation.

Public and Private Limited Companies hold separate legal personality under the Companies Act 2006, meaning the entity can sue, be sued, and own property independently of its members. Partnerships and sole proprietorships do not carry this distinction — liability in these cases extends to the personal assets of the partners or proprietor. Branch and Liaison Offices derive their legal standing from the parent foreign entity.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.