Key Takeaways

- The Besloten Vennootschap (BV) is the most widely registered entity in the Netherlands, permitting single-shareholder ownership under the Wet vereenvoudiging en flexibilisering bv-recht with no minimum share capital requirement.

- All legal entities and businesses operating in the Netherlands must register with the Kamer van Koophandel (KVK), which maintains the Handelsregister as the central commercial register.

- Partnerships such as the Vennootschap onder Firma (VOF), Commanditaire Vennootschap (CV), and Maatschap do not offer limited liability protection, exposing partners to personal liability for business obligations.

- Foreign companies can establish a presence in the Netherlands without forming a separate legal person by operating through a branch office or representative office.

Introduction to Entity Types in Netherlands

Located in northwestern Europe and bordered by Germany, Belgium, and the North Sea, the Netherlands is an independent nation with a civil law legal system. Companies are registered through the Kamer van Koophandel (KVK), the Dutch Chamber of Commerce, which maintains the Handelsregister — the central commercial register for all legal entities and businesses operating in the country.

The Netherlands operates a territorial tax system with an extensive network of double tax treaties, making it a structurally significant jurisdiction for multinational operations.

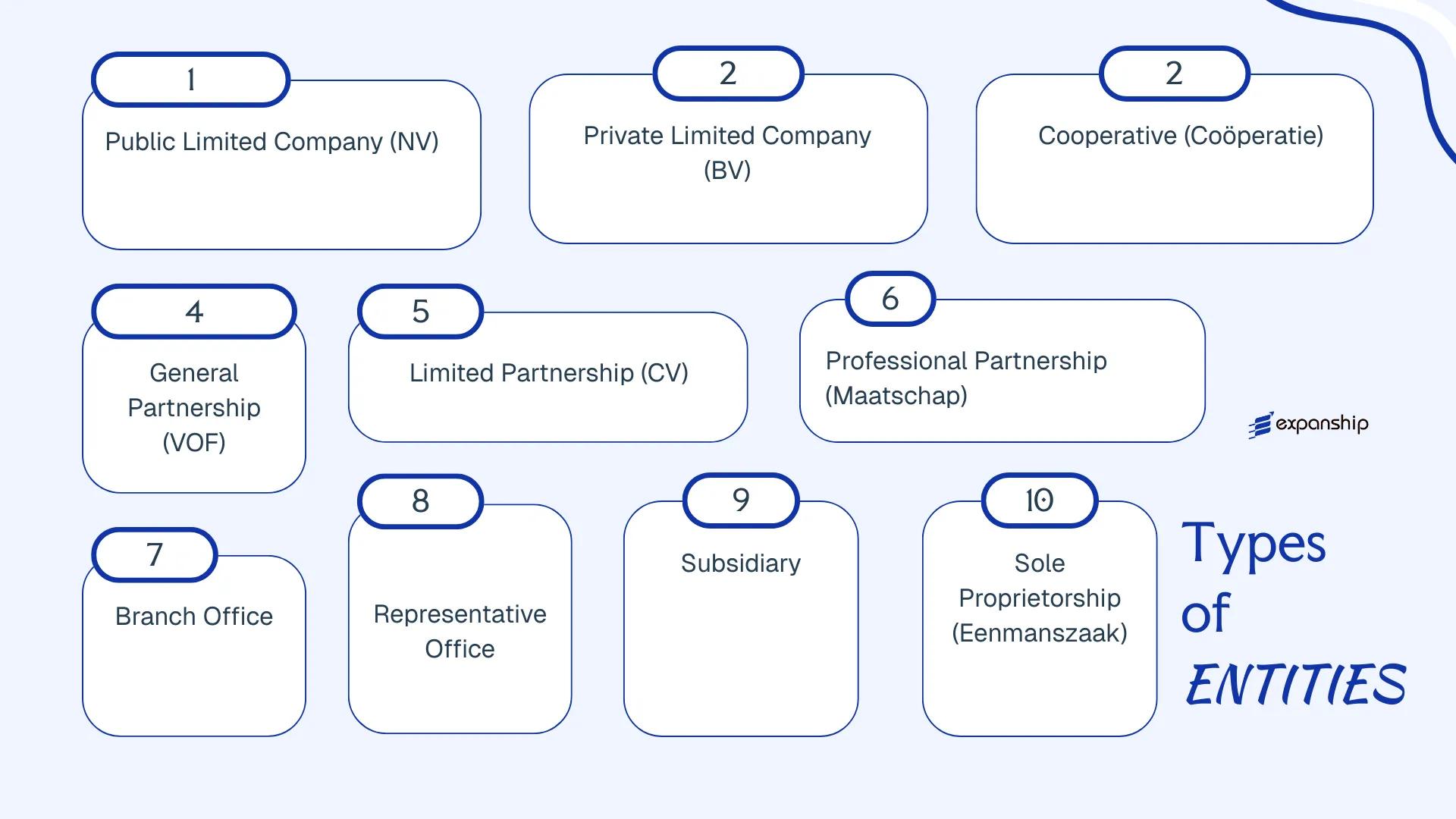

Choosing among the types of business entities in Netherlands depends on factors including liability, capital requirements, governance structure, and the nature of your intended activities. The available legal forms include the Naamloze Vennootschap (NV), Besloten Vennootschap (BV), Coöperatie, Vennootschap onder Firma (VOF), Commanditaire Vennootschap (CV), Maatschap, Eenmanszaak, and various foreign business presences such as branch offices and representative offices.

Each structure carries distinct legal, tax, and operational implications. This article examines every major Dutch company type in detail to help you determine which form suits your business objectives.

An Overview of Business Structures in Netherlands

Dutch company law provides several distinct entity types, each governed primarily by Book 2 of the Burgerlijk Wetboek (Dutch Civil Code), with supplementary rules under the Wet op de formeel buitenlandse vennootschappen for foreign entities operating locally. A Netherlands business structures comparison reveals forms ranging from the sole proprietorship to the public limited company, with each structure carrying different implications for liability, governance, and taxation. The sections that follow examine each in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Naamloze Vennootschap (NV) | Public limited company | Limited | Taxable (CIT) | Yes | 1 shareholder | KVK / AFM | Book 2, Civil Code |

| Besloten Vennootschap (BV) | Private limited company | Limited | Taxable (CIT) | Yes | 1 shareholder | KVK | Book 2, Civil Code |

| Coöperatie | Cooperative | Limited (default) | Taxable (CIT) | Yes | 2 members | KVK | Book 2, Civil Code |

| Vennootschap onder Firma (VOF) | General partnership | Unlimited | Pass-through (IB) | Yes | 2 partners | KVK | Civil Code / Commercial Code |

| Commanditaire Vennootschap (CV) | Limited partnership | Mixed | Pass-through / CIT | Yes | 2 partners | KVK | Civil Code |

| Maatschap | Professional partnership | Unlimited | Pass-through (IB) | Yes | 2 partners | KVK | Book 7A, Civil Code |

| Eenmanszaak | Sole proprietorship | Unlimited | Pass-through (IB) | Yes | 1 owner | KVK | Civil Code |

| Branch Office | Foreign branch | Unlimited (parent) | Taxable (CIT) | Yes | N/A | KVK / Belastingdienst | WFBV |

| Representative Office | Non-trading presence | N/A | Generally exempt | No | N/A | KVK | Civil Code |

Each of these structures is examined in full in the sections below.

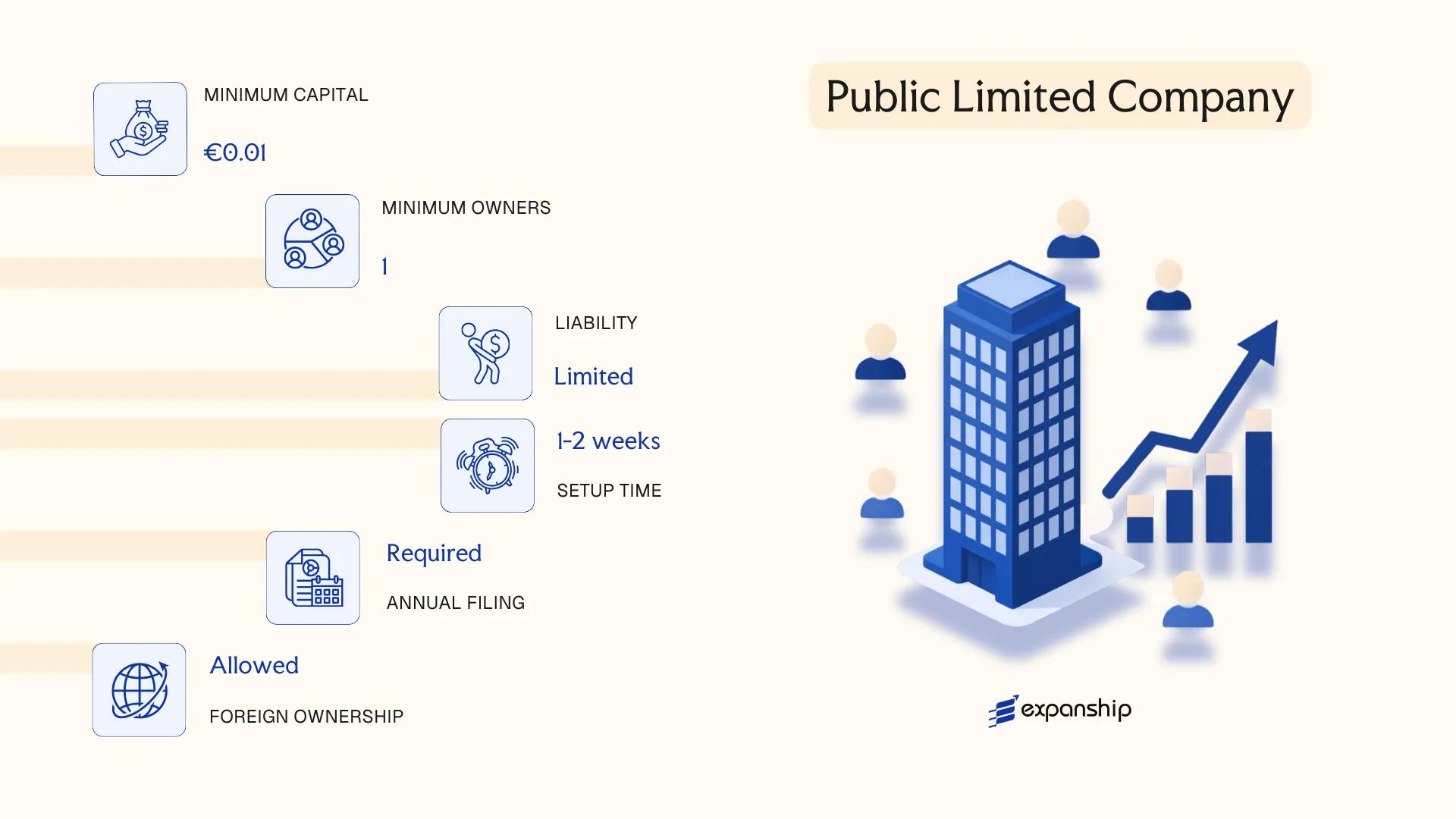

Naamloze Vennootschap (NV) — Public Limited Company

The Naamloze Vennootschap (NV) Netherlands is governed by Book 2 of the Dutch Civil Code (Burgerlijk Wetboek), specifically the provisions applicable to public companies. It carries separate legal personality, meaning the entity itself holds rights and obligations distinct from its shareholders.

Shares in an NV are freely transferable without restriction, which differentiates this structure from its private counterpart. This transferability makes the NV the required legal form for companies listed on Euronext Amsterdam or any other regulated exchange.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Naamloze Vennootschap (NV) | Public limited company; separate legal personality |

| Governance | Board of Directors (one-tier or two-tier) | Two-tier: Supervisory Board + Management Board; one-tier: combined |

| Shareholders | Minimum 1; no maximum | Shares must be registered or bearer (bearer largely phased out) |

| Capital | Minimum €45,000 authorised; at least 20% paid up at incorporation | Denominated in euros; notarial deed required |

| Local Presence | Registered office in the Netherlands | Must have a Dutch notary execute the deed of incorporation |

| Privacy | Shareholder register not fully public | Directors registered at the Dutch Chamber of Commerce (Kamer van Koophandel) |

Focus Points

- Taxation: Subject to Dutch corporate income tax at 19% (up to €200,000 profit) and 25.8% above that threshold; standard VAT rate of 21% applies; dividend withholding tax at 15%, reducible under tax treaties or the EU Parent-Subsidiary Directive.

- Economic Substance: Listed or regulated NVs face enhanced scrutiny; genuine management and control must be demonstrably exercised from the Netherlands to maintain treaty benefits.

- Annual Compliance: Mandatory financial statement filing with the Kamer van Koophandel; large companies are subject to statutory audit requirements under Dutch law.

- Treaty Access: The Netherlands maintains an extensive tax treaty network; NV entities generally qualify, subject to anti-abuse provisions under the Principal Purpose Test (MLI).

- Conversion: An NV may be converted to a BV by shareholder resolution and notarial deed, without dissolution, under Book 2 of the Burgerlijk Wetboek.

Closing

The NV suits large enterprises, publicly traded companies, and structures requiring freely transferable shares — such as joint ventures with institutional investors. The primary advantage is capital market access; the clear drawback is the higher administrative and compliance burden relative to a private entity.

The NV is most appropriate for businesses seeking a public listing, institutional investment, or a structure where unrestricted share transferability is a commercial requirement.

Company Incorporation in the Netherlands

Expanship assists with NV and BV incorporation in the Netherlands, including notarial deed coordination and Chamber of Commerce registration.

Besloten Vennootschap (BV) — Private Limited Company

Besloten Vennootschap BV Netherlands registration is governed primarily by Book 2 of the Dutch Civil Code (Burgerlijk Wetboek), as significantly reformed by the Flex-BV Act (Wet Vereenvoudiging en Flexibilisering BV-recht), which came into force on 1 October 2012. The BV is a private company with separate legal personality, meaning it exists independently of its shareholders and can hold assets, enter contracts, and incur liabilities in its own name.

Shareholder liability is limited to the amount of their capital contribution. This structure accommodates both closely held family businesses and multi-investor ventures, making it a widely used vehicle for Dutch private limited company BV arrangements across trading, holding, and operational activities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Besloten Vennootschap (BV) | Private company with separate legal personality |

| Members | Shareholders (aandeelhouders); Directors (bestuurders); optional Supervisory Board (Raad van Commissarissen) | Min. 1 shareholder; no maximum. Min. 1 director; no nationality restriction |

| Local Presence | Registered office (statutaire zetel) must be in the Netherlands; physical or c/o address accepted | No mandatory resident director, but substance considerations apply |

| Capital | EUR currency; no statutory minimum share capital since the Flex-BV Act (€0.01 minimum per share is sufficient) | No notarial capital verification requirement at formation |

| Share Transferability | Shares are not freely transferable; transfer restrictions (blokkeringsregeling) apply unless articles provide otherwise | Shares cannot be publicly traded |

| Privacy | Shareholders and directors disclosed in the Handelsregister (KvK); UBO register (UBO-register) requires disclosure of beneficial owners with 25%+ interest | UBO register is partially accessible to the public |

Focus Points

- Taxation: Subject to Dutch corporate income tax (vennootschapsbelasting) at 19% on the first €200,000 profit and 25.8% above that threshold; VAT (BTW) applies to taxable supplies; dividend withholding tax (dividendbelasting) levied at 15%, subject to reduction under applicable tax treaties or EU Parent-Subsidiary Directive.

- Economic Substance: Substance requirements matter for treaty access and transfer pricing; the Dutch tax authority (Belastingdienst) may challenge holding or IP structures lacking genuine local management.

- Annual Compliance: Annual accounts must be filed with the KvK within 8 days of adoption by the general meeting (generally within 12 months of the financial year-end); audit required once two of three thresholds are met.

- Treaty Access: The Netherlands maintains an extensive double tax treaty network; BV incorporation Netherlands provides access, contingent on substance requirements being satisfied.

- Conversion: A BV can be converted into an NV or other legal form through a notarial deed and shareholder resolution, without requiring liquidation.

Closing

The BV suits trading companies, intermediate holding structures, joint ventures, and IP ownership vehicles. Its flexible share capital rules are a practical advantage, though the mandatory notarial incorporation deed adds a procedural step and associated cost that some jurisdictions do not require.

The BV is well-suited to foreign investors and entrepreneurs seeking a recognised, tax-treaty-accessible vehicle for operating or holding activities in the Netherlands.

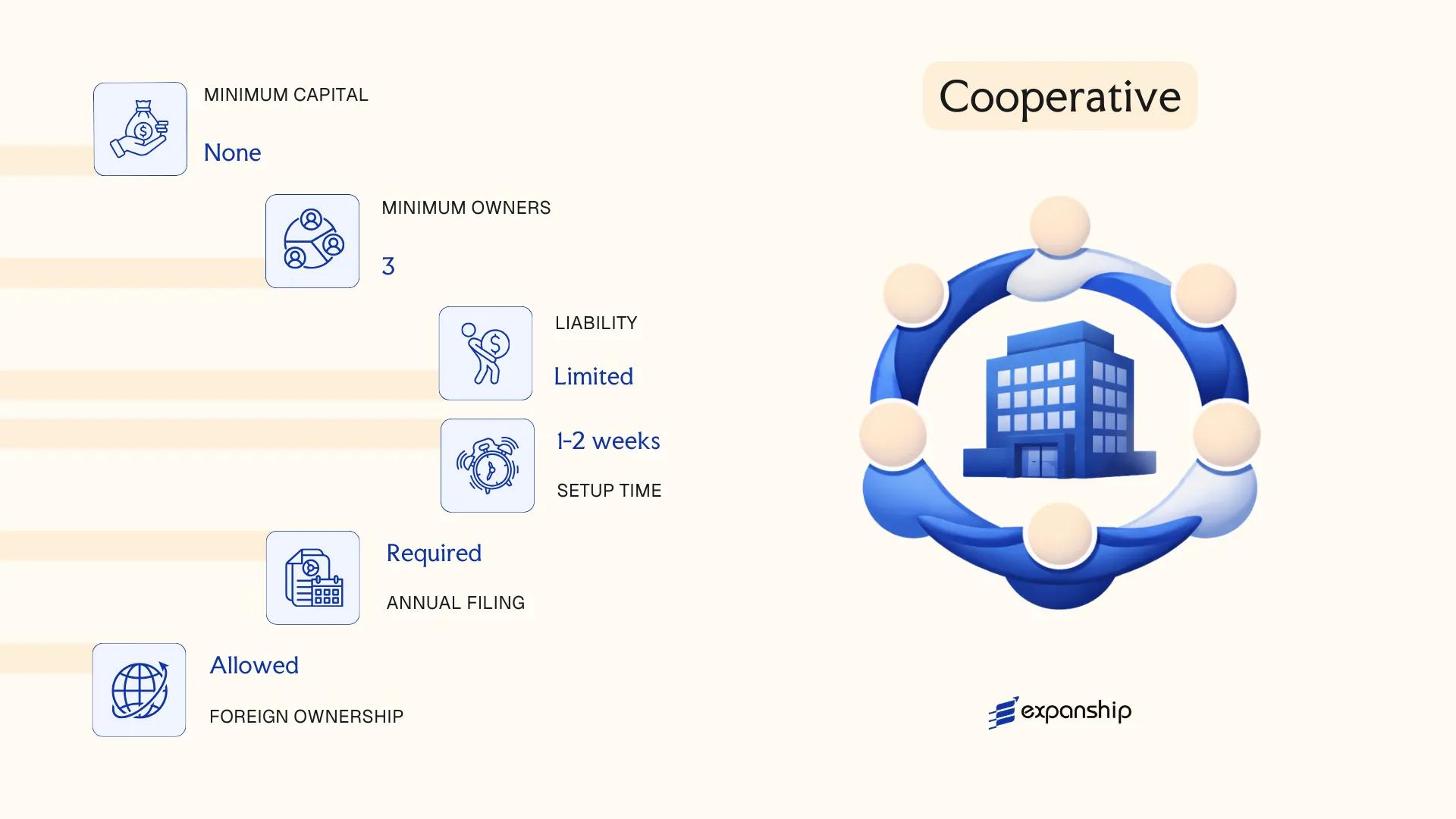

Coöperatie — Cooperative

The Coöperatie Netherlands cooperative structure is governed by Book 2 of the Dutch Civil Code (Burgerlijk Wetboek), specifically Articles 53–63. Established as a separate legal entity with full legal personality, it operates on a membership basis rather than a shareholding model.

Liability is excluded or limited through a clause in the articles of association. This makes the Coöperatie a hybrid structure — functionally comparable to a BV in terms of legal standing, yet organised around collective member interests rather than capital ownership.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Legal entity with separate legal personality | Governed by Book 2, Articles 53–63 BW |

| Members | Minimum 2 members; no statutory maximum | Members can be individuals or legal entities |

| Governing Body | General Members' Meeting + Board of Directors | Board manages day-to-day operations |

| Local Presence | Registered office required in the Netherlands | No mandatory local director requirement under statute |

| Capital | No minimum capital requirement | Financial contributions defined in the articles |

| Liability | Excluded (UA), limited (BA), or unlimited (A) | Liability clause must be stated in the name suffix |

| Privacy | Deed of incorporation filed with the Chamber of Commerce (KvK) | Member identities may be disclosed in the articles |

Focus Points

- Taxation: Subject to Dutch corporate income tax (Vpb) at standard rates (19% up to €200,000; 25.8% above); member distributions may attract dividend withholding tax at 15%; VAT registration required for commercial activities; no stamp duty on formation.

- Treaty Access: Qualifies as a tax resident entity and can access Dutch tax treaties, subject to substance requirements and the Principal Purpose Test under BEPS-aligned rules.

- Annual Compliance: Annual accounts must be filed with the KvK; audit requirements depend on size classification under Book 2 BW.

- Economic Substance: Boards meeting in the Netherlands and demonstrable local management activity are required to maintain Dutch tax residency.

- Conversion: A Coöperatie can be converted into a BV or NV through a notarial deed process, subject to member approval.

Sub-Types

UA — Uitgesloten Aansprakelijkheid (Excluded Liability)

Members bear no liability for cooperative deficits upon dissolution. This is the most commonly used variant, offering members the strongest liability protection.

BA — Beperkte Aansprakelijkheid (Limited Liability)

Members hold limited liability for any shortfall on winding up. The articles define the extent of each member's financial exposure.

A — Aansprakelijkheid (Unlimited Liability)

Members are fully liable for cooperative deficits. This form is rarely used in commercial practice.

Closing

The Coöperatie is used frequently as a holding structure within multinational groups, particularly for pooling IP rights or centralising treasury functions, given its flexibility in distributing profits without mandatory dividend procedures. Its main limitation is administrative complexity relative to a BV, particularly in drafting articles that address member contributions and liability clauses correctly.

Best suited for multinational groups seeking a flexible holding or profit-pooling entity, and for sector-based businesses — such as agriculture, healthcare, or finance — operating on a collective membership model.

Partnerships in the Netherlands [Vennootschap onder Firma (VOF), Commanditaire Vennootschap (CV), Maatschap]

Dutch partnership structures are governed primarily by the Dutch Civil Code (Burgerlijk Wetboek) and, for commercial partnerships, by the Commercial Code (Wetboek van Koophandel). The three main Netherlands VOF CV Maatschap partnership types share one defining characteristic: none possess separate legal personality, meaning creditors can pursue partners personally for business debts.

Registration for the Vennootschap onder Firma and Commanditaire Vennootschap is mandatory with the Dutch Chamber of Commerce (Kamer van Koophandel, KvK). The Maatschap, traditionally used by professionals, operates under a cooperation agreement but follows the same general registration process.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | No separate legal personality | Partners bear personal liability |

| Members | Partners (VOF: 2+ general; CV: 1+ general + 1+ limited; Maatschap: 2+ participants) | General partners have unlimited liability in all forms |

| Registered Office | Dutch business address required | Must be registered with KvK |

| Capital | No statutory minimum | Contributions can be cash, goods, or labour |

| Privacy | Partnership agreements not publicly filed | Partner identities recorded at KvK |

| Liability | VOF/Maatschap: unlimited for all; CV: limited partners capped at contribution | Limited partners in CV lose protection if they act in management |

Focus Points

- Taxation: Partnerships are fiscally transparent; profits are attributed to individual partners and taxed under personal income tax (inkomstenbelasting) or corporate tax if the partner is a legal entity; VAT registration applies if turnover thresholds are met.

- Annual Compliance: Partners must file annual income tax returns individually; no separate entity-level corporate tax return is required for the partnership itself.

- Economic Substance: No formal substance requirements apply, though genuine business activity is expected to support claims of partnership status.

- Conversion: A VOF or CV can be converted into a BV through a notarial deed, subject to KvK re-registration.

- Restrictions: Limited partners in a CV must not conduct management activities; doing so removes their liability shield entirely.

Sub-Types

Vennootschap onder Firma (VOF)

A general commercial partnership in which all partners carry joint and several liability for the firm's obligations. It is commonly used by two or more individuals running a shared trading or service business under a single firm name.

Commanditaire Vennootschap (CV)

The CV introduces a two-tier partner structure: one or more general (beherende) partners manage the business with unlimited liability, while one or more limited (stille) partners contribute capital without taking part in management. This structure is also used as a Dutch CV holding arrangement in certain international tax planning contexts, though its tax treatment has been subject to legislative review in recent years.

Maatschap

A professional partnership used predominantly by lawyers, doctors, accountants, and similar regulated professionals. Each partner is liable only for their own share of obligations unless a joint commitment is made, making individual liability proportionate rather than joint and several.

Choosing a Partnership Structure

Partnerships suit small businesses, professional practices, and joint ventures where formal incorporation is not warranted. The absence of minimum capital requirements is a practical advantage, but unlimited personal liability for general partners is a material constraint for businesses carrying financial or operational risk.

Dutch partnership structures are best suited for professionals and small business operators seeking a low-cost, flexible operating structure where the partners are willing to accept personal liability exposure.

Foreign Business Presences in the Netherlands [Branch Office, Representative Office, Subsidiary]

Establishing a foreign company presence in Netherlands typically takes one of three structural forms: a branch office (bijkantoor), a representative office, or a locally incorporated subsidiary. Each carries distinct legal and operational implications. A branch has no separate legal personality — the parent company remains directly liable for its activities — while a subsidiary incorporated as a BV or NV constitutes an independent legal entity with its own liability shield.

Registration requirements are governed by the Dutch Civil Code (Burgerlijk Wetboek) and administered through the Dutch Chamber of Commerce (Kamer van Koophandel, KvK). Any branch conducting business activities must register with the KvK and file certain parent company documents, including translated versions where applicable.

Key Characteristics

| Requirement | Branch Office | Representative Office | Subsidiary (BV) |

|---|---|---|---|

| Legal Personality | None (extension of parent) | None | Separate legal entity |

| Liability | Parent bears full liability | Parent bears full liability | Limited to entity's own assets |

| KvK Registration | Mandatory | Not formally required | Mandatory |

| Local Director | Not required | Not required | At least one director required |

| Minimum Capital | None | None | None (€0.01 nominal) |

| Annual Accounts | Must file parent's accounts | No filing obligation | Must file own accounts |

Focus Points

- Taxation: Branches are taxed on Dutch-sourced profits under standard corporate income tax (25.8% above €200,000; 19% below); subsidiaries are fully subject to Dutch CIT, VAT (21% standard rate), and dividend withholding tax at 15%, though treaty reductions may apply.

- Economic Substance: Representative offices must genuinely limit activities to preparatory or auxiliary functions; commercial activity triggers branch registration obligations.

- Treaty Access: A subsidiary as a resident entity has broader access to the Netherlands' extensive tax treaty network than a branch, which may face source-state restrictions.

- Annual Compliance: Branches must deposit the parent's audited financial statements with the KvK; subsidiaries file their own accounts and are subject to Dutch corporate governance rules.

- Conversion: A branch can be converted into a BV, though this involves a formal incorporation process rather than a straightforward structural change.

Sub-Types

Branch Office (Bijkantoor)

A branch is a registered operational extension of the foreign parent, permitted to conduct full commercial activity. It does not require separate share capital but inherits the parent's legal exposure entirely.

Representative Office

This structure is suited for market research, liaison, or promotional activities only. Because it cannot generate revenue or enter binding commercial contracts, it falls outside the standard KvK registration requirement, though internal Dutch tax authority guidance may still require notification.

Subsidiary

Incorporated as a BV under Dutch law, a subsidiary is the most structurally independent option. It enables Netherlands branch office vs subsidiary distinctions to be resolved in favour of liability separation and access to participation exemption on qualifying dividends and capital gains.

Closing

A subsidiary is the standard choice for foreign businesses seeking operational autonomy, tax treaty access, and participation exemption benefits, while a branch suits firms wanting a lighter administrative footprint without a separate capitalisation requirement.

Foreign companies expanding business to Netherlands that require a full commercial presence with liability separation and access to the participation exemption should incorporate a BV subsidiary.

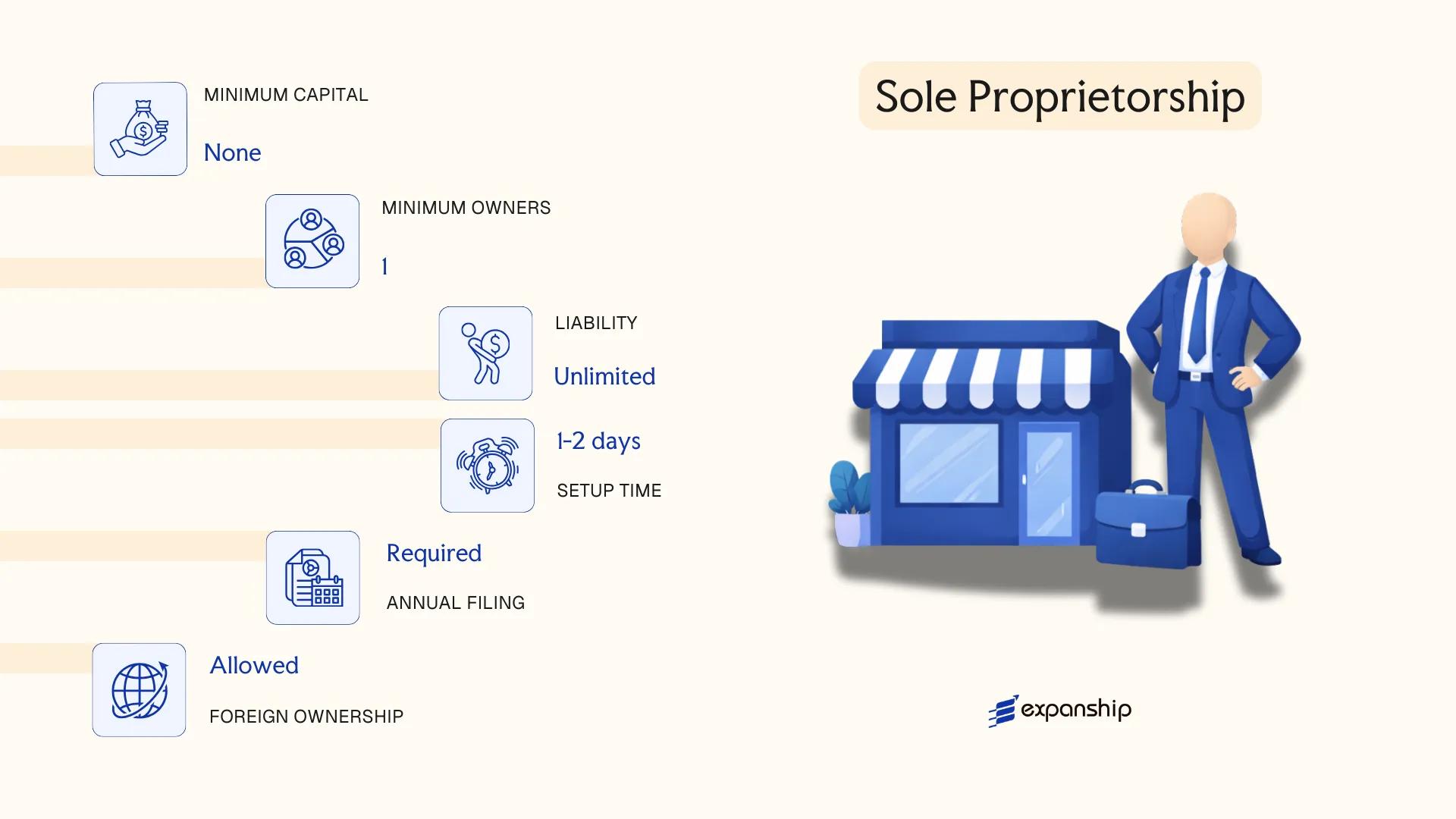

Eenmanszaak — Sole Proprietorship

The Eenmanszaak sole proprietorship Netherlands is governed by the Dutch Commercial Register Act (Handelsregisterwet 2007) and general provisions within the Dutch Civil Code (Burgerlijk Wetboek). It carries no separate legal personality, meaning you and your business are treated as a single legal and financial unit.

Registration with the Dutch Chamber of Commerce (Kamer van Koophandel, KvK) is mandatory before or within one week of starting operations. Once registered, you receive a KvK number and, if applicable, a VAT identification number (BTW-identificatienummer) from the Dutch Tax and Customs Administration (Belastingdienst).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Eenmanszaak) | No separate legal personality |

| Member Designation | Proprietor | One natural person only; no partners or shareholders |

| Liability | Unlimited personal liability | Personal assets are fully exposed to business debts |

| Local Presence | Registered address in the Netherlands required | Must be listed in the KvK Commercial Register |

| Capital | No minimum capital requirement | No statutory capital contribution needed |

| Privacy | Proprietor's name and address are publicly registered in the KvK | Limited privacy protection |

Focus Points

- Taxation: Business profits are taxed as personal income under Box 1 of the Dutch income tax system (inkomstenbelasting); VAT registration required if annual turnover exceeds the applicable threshold; no corporate income tax (vennootschapsbelasting) applies; self-employed deductions (zelfstandigenaftrek) may reduce taxable income.

- Annual Compliance: Annual income tax return filed with the Belastingdienst; no separate corporate filing required; basic bookkeeping records must be retained for seven years.

- Conversion: Can be converted into a BV, though the process involves notarial deed execution and KvK re-registration; asset transfers may trigger tax consequences.

- Treaty Access: As a pass-through structure with no separate legal personality, access to Dutch tax treaty benefits flows through the individual proprietor's personal tax position.

- Restrictions: Cannot have employees as co-owners; the structure does not support equity investment or shareholding arrangements.

Closing

The Eenmanszaak suits freelancers, consultants, and sole traders operating small-scale service or trading activities where administrative simplicity outweighs the need for liability protection. Its primary advantage is minimal setup cost and compliance burden, while its clear limitation is unlimited personal liability for all business obligations.

The Eenmanszaak is best suited for individual self-employed professionals in the Netherlands who operate with low financial risk and do not require external investment.

How to Choose the Right Entity Type in Netherlands

Knowing how to choose a business entity in Netherlands before you register prevents structural problems that are difficult and costly to unwind later.

Why Your Entity Choice Matters

The structure you register has binding legal and financial consequences.

- A BV used purely for holding foreign assets may still be subject to Dutch corporate income tax if management and control are exercised from the Netherlands, even without local trading activity.

- Selecting a Coöperatie for treaty access purposes without ensuring it qualifies as a resident taxpayer under the applicable double tax agreement can result in withheld tax that is non-recoverable.

- Forming a VOF when your activity requires separate legal personality means personal assets remain exposed to business creditors with no liability shield.

- Registering a NV when your business has no public share offering requirement imposes ongoing compliance costs, including the mandatory supervisory board threshold obligations, that a BV would not.

Key Factors to Consider

- Business Activity: Actively trading firms, passive holding structures, and regulated sectors such as fund management each point to a distinct entity under Book 2 of the Dutch Civil Code.

- Liability Exposure: If personal asset protection is a priority, only legal entities with separate legal personality — the BV, NV, or Coöperatie — provide that separation.

- Tax Objectives: Your need for participation exemption access, the innovation box regime, or treaty network eligibility will narrow the viable structures considerably.

- Ownership Structure: Multi-party ventures with profit-sharing arrangements may suit a CV or VOF, while institutional investors typically require a BV or NV.

- Substance Capacity: If you cannot maintain genuine management, staff, or office presence locally, structures with lower substance thresholds or specific holding arrangements may be more appropriate.

- Exit Strategy: Not all Dutch entities permit redomiciliation or conversion; confirming this before formation avoids restructuring costs later.

Compliance Services for Companies in the Netherlands

Ongoing compliance support for Dutch entities, including annual filing, KvK obligations, and corporate secretarial services.

Conclusion

The Netherlands company formation summary comes down to matching your operational profile, ownership structure, and liability requirements to the correct legal form. The BV remains the most widely registered entity, favoured by resident and foreign entrepreneurs alike for its limited liability and single-shareholder eligibility under the Wet vereenvoudiging en flexibilisering bv-recht. The NV serves capital-intensive businesses or those pursuing public listings. Cooperatives suit member-based commercial arrangements, while partnerships such as the VOF, CV, and Maatschap are suited to professionals and closely-held ventures accepting personal liability exposure. Branch and representative offices extend foreign entities without creating separate legal persons.

Dutch corporate governance is overseen by the Kamer van Koophandel, and the Netherlands' extensive tax treaty network continues to reinforce its position as a holding and intermediary jurisdiction. Selecting the correct entity at formation shapes your compliance obligations, tax treatment, and structural flexibility over the life of your business.

How Expanship Can Assist You

Expanship provides corporate services Netherlands company setup across the full range of Dutch legal structures covered in this blog, from the commonly used BV to the more specialist NV and Coöperatie. Our team works directly with the Dutch Chamber of Commerce (Kamer van Koophandel) and coordinates with the Dutch Tax and Customs Administration (Belastingdienst) to keep your registration accurate and your obligations on track.

Our services at each stage of formation and beyond include:

- Document preparation and notarial deed coordination for entities requiring civil-law notary involvement

- Registered office and local agent provision in the Netherlands

- KVK filing and post-registration liaison

- VAT and corporate tax registration support with the Belastingdienst

- Ongoing compliance management, including annual reporting requirements

- Banking introduction assistance for newly incorporated Dutch entities

Reach out to Expanship Netherlands to discuss how we can support your Dutch incorporation.

Frequently Asked Questions (FAQ)

The Besloten Vennootschap (BV) is the most frequently incorporated entity, registered in large volumes annually through KVK. Its €0.01 minimum share capital requirement, single-shareholder eligibility, and limited liability make it the default choice for both domestic entrepreneurs and foreign investors.

A BV restricts share transferability and cannot list shares on a public exchange, while an NV permits public offerings and has a €45,000 minimum share capital. Both structures carry full legal personality and corporate tax obligations under the Vennootschapsbelasting regime, but the NV carries heavier governance and disclosure requirements.

A BV's shareholder register is not publicly accessible through KVK; only directors appear in the public trade register. Nominee director and shareholder arrangements are legally permissible, though the Ultimate Beneficial Owner (UBO) register requires disclosure of individuals holding over 25% ownership to the relevant authorities.

A BV and Eenmanszaak can each be formed by one individual. A VOF and Maatschap each require at least two partners by definition, and a CV requires at minimum one general partner and one limited partner.

All principal entity types, including the BV, NV, and branch office, are open to foreign nationals without residency requirements. A non-resident can serve as sole director and shareholder of a BV, though substance considerations under Dutch tax law may require local management presence to access treaty benefits.

Dutch law permits statutory conversion (omzetting) under Book 2 of the Burgerlijk Wetboek, most commonly from a BV to an NV or the reverse. The process requires a notarial deed, shareholder resolution, and updated KVK registration; continuity of legal personality is maintained throughout.

The BV, NV, and Coöperatie each hold full legal personality. Partnerships, including the VOF, CV, and Maatschap, do not hold separate legal personality under Dutch law, meaning partners retain personal liability exposure to varying degrees.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.