Key Takeaways

- The Sociedad Anónima (S.A.) is the most registered entity type in Nicaragua, preferred for its transferable share structure and liability separation between the company and its shareholders.

- Company registration in Nicaragua is administered by the Registro Mercantil under MIFIC, with a separate tax registration requirement through the Dirección General de Ingresos (DGI).

- Nicaragua operates a territorial tax system, meaning foreign-sourced income is generally exempt from local income tax regardless of the entity type used.

- Partnerships formed under the Código de Comercio — including the Sociedad en Nombre Colectivo and both Comandita forms — carry unlimited liability for at least some partners, limiting their appeal to specific professional service contexts.

Introduction to Entity Types in Nicaragua

Nicaragua is a Central American republic bordered by Honduras to the north and Costa Rica to the south, with coastlines on both the Pacific Ocean and the Caribbean Sea. Choosing among the available types of business entities in Nicaragua requires an understanding of how local corporate law assigns liability, ownership rights, and operational structure to each form.

Company registration falls under the jurisdiction of the Registro Mercantil, which operates under the Ministry of Development, Industry and Commerce (MIFIC). Businesses must also register with the Dirección General de Ingresos (DGI) for tax purposes.

Nicaragua applies a territorial tax system, meaning income earned outside the country is generally not subject to local income tax.

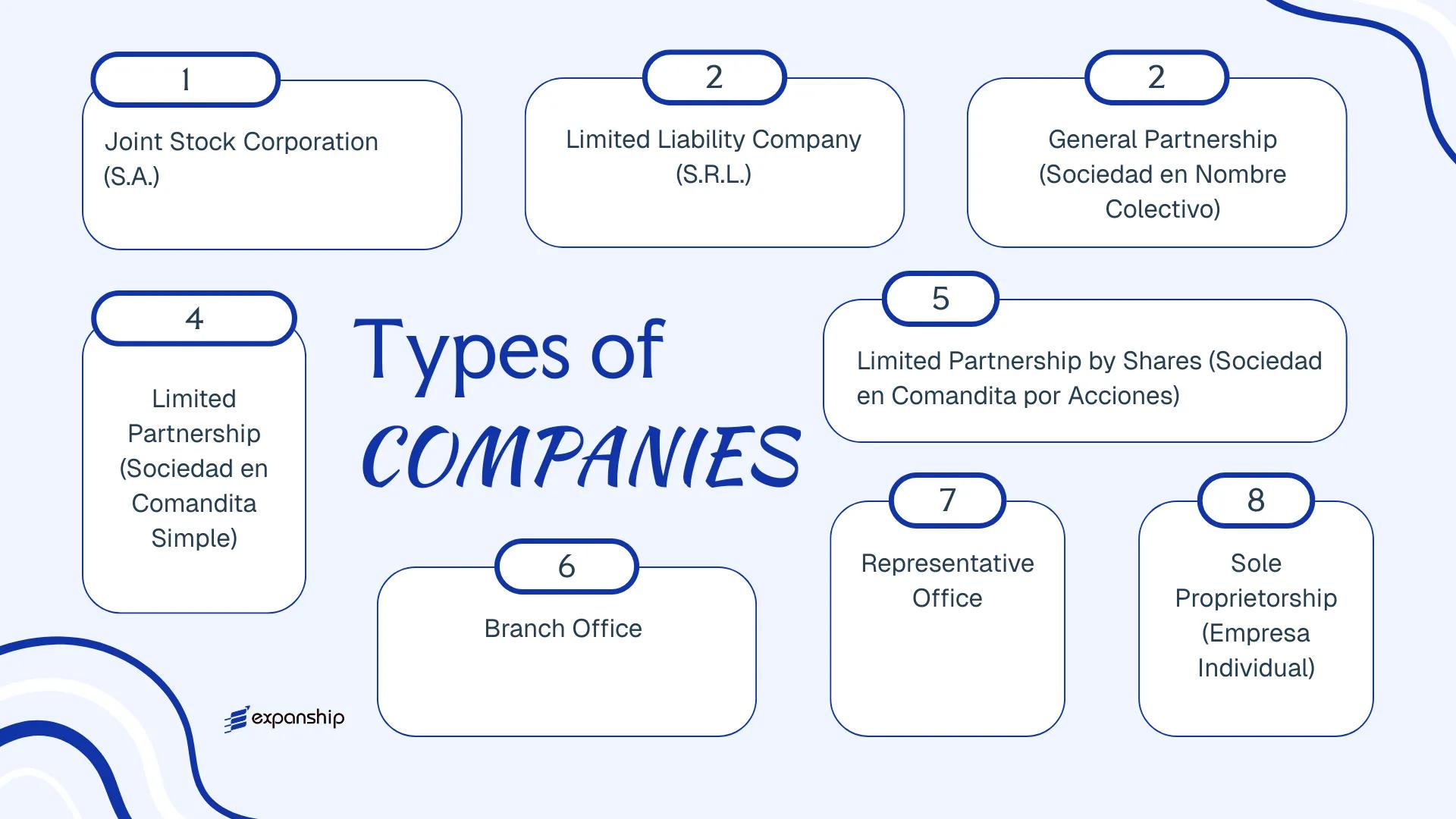

The corporate forms available include:

- Sociedad Anónima (S.A.)

- Sociedad de Responsabilidad Limitada (S.R.L.)

- Sociedad en Nombre Colectivo

- Sociedad en Comandita Simple

- Sociedad en Comandita por Acciones

- Branch Office

- Representative Office

- Empresa Individual (Sole Proprietorship)

Each of these legal entity structures in Nicaragua carries distinct requirements for capital, governance, and member liability, all of which this article examines in turn.

An Overview of Business Structures in Nicaragua

Nicaragua business structures are governed primarily by the Código de Comercio de Nicaragua (Commercial Code), which dates to 1916 and has been amended over time to accommodate modern commercial activity. The Code establishes several distinct legal forms, each structured to serve a different commercial purpose, scale of operation, or ownership configuration. The sections that follow examine each form in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima (S.A.) | Corporation | Limited to shares | Taxable | Yes | 2 shareholders | Registro Mercantil | Código de Comercio |

| Sociedad de Responsabilidad Limitada (S.R.L.) | LLC | Limited to quota | Taxable | Yes | 2 partners | Registro Mercantil | Código de Comercio |

| Sociedad en Nombre Colectivo | General Partnership | Unlimited | Taxable | Yes | 2 partners | Registro Mercantil | Código de Comercio |

| Sociedad en Comandita Simple | Limited Partnership | Mixed | Taxable | Yes | 2 partners | Registro Mercantil | Código de Comercio |

| Sociedad en Comandita por Acciones | Partnership by Shares | Mixed | Taxable | Yes | 2 partners | Registro Mercantil | Código de Comercio |

| Branch Office | Foreign branch | Parent liable | Taxable | Yes | N/A | Registro Mercantil | Código de Comercio |

| Representative Office | Non-trading entity | Parent liable | Limited scope | No | N/A | Registro Mercantil | Código de Comercio |

| Empresa Individual | Sole proprietorship | Unlimited | Taxable | Yes | 1 owner | Registro Mercantil | Código de Comercio |

Each of these structures is examined in full in the sections below.

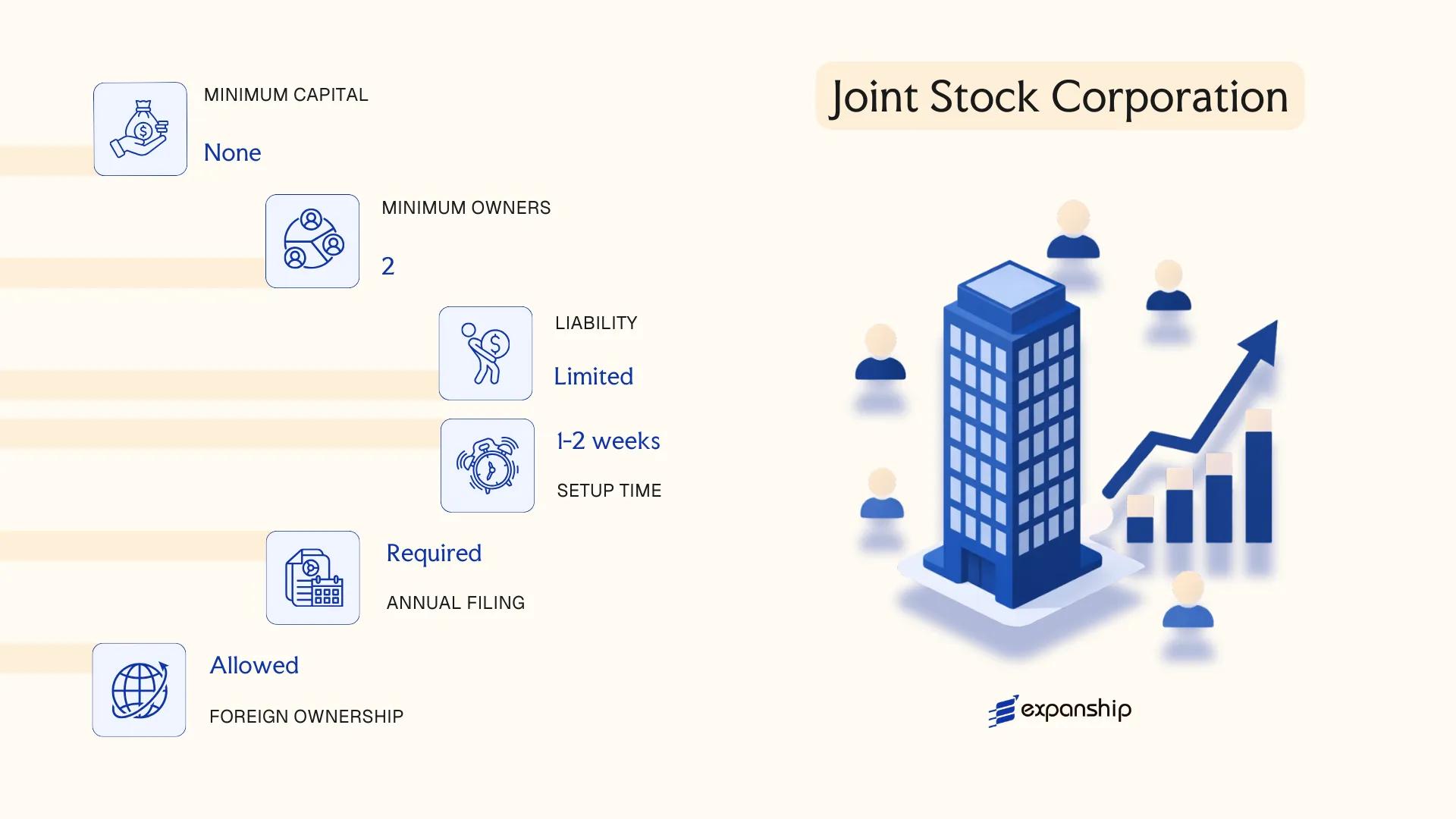

Sociedad Anónima (S.A.) — Joint Stock Corporation

Nicaragua Sociedad Anónima registration is governed by the Code of Commerce (Código de Comercio) of 1916, which remains the primary legislative framework for commercial entities in the country. The S.A. is a separate legal entity, meaning it holds rights and obligations independent of its shareholders.

Liability is limited to each shareholder's capital contribution. Capital is divided into transferable shares, which makes this structure suitable for businesses seeking to admit investors or facilitate ownership transfers without restructuring the entire entity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima (S.A.) | Separate legal personality; governed by the Código de Comercio 1916 |

| Members | Shareholders (Accionistas) | Minimum 2 shareholders; no statutory maximum; can be individuals or legal entities |

| Directors | Board of Directors (Junta Directiva) | Minimum 3 directors required; nationals not mandatory |

| Local Presence | Registered Agent + Registered Address | A local registered agent and a registered office address within Nicaragua are required |

| Share Capital | Nicaraguan Córdoba (NIO) | No mandatory minimum capital under general rules; must be stated in the deed of incorporation |

| Privacy | Shareholder names appear in public deed | Bearer shares are not permitted; nominee arrangements may provide some privacy |

Focus Points

- Taxation: Corporate income tax applies at 30% on net income, with a minimum tax (IR Definitivo) based on gross income in certain cases; VAT is levied at 15%; withholding taxes apply to dividends remitted abroad, generally at 15%.

- Annual Compliance: Annual financial statements must be filed; entities are required to maintain accounting records and renew their municipal business licence (matrícula) annually.

- Economic Substance: Nicaragua does not currently impose a formal economic substance regime comparable to those in dedicated offshore jurisdictions, though commercial activity must be genuine to support local tax treatment.

- Treaty Access: Nicaragua has a limited tax treaty network; treaty benefits are not broadly available, which may affect cross-border structures.

- Conversion: An S.A. can generally be converted to another commercial entity type through a deed of transformation registered with the Mercantile Registry (Registro Mercantil).

Closing

The S.A. is commonly used for trading operations, holding structures, and businesses requiring multiple investors or phased equity participation. Shares are freely transferable, which supports investment flexibility, but the public nature of incorporation deeds means full shareholder anonymity is not achievable.

The Sociedad Anónima suits foreign investors and multi-shareholder businesses seeking a structured, scalable entity with limited liability under Nicaraguan commercial law.

Company Incorporation in Nicaragua

Incorporate a Sociedad Anónima or other business entity in Nicaragua with Expanship's end-to-end support.

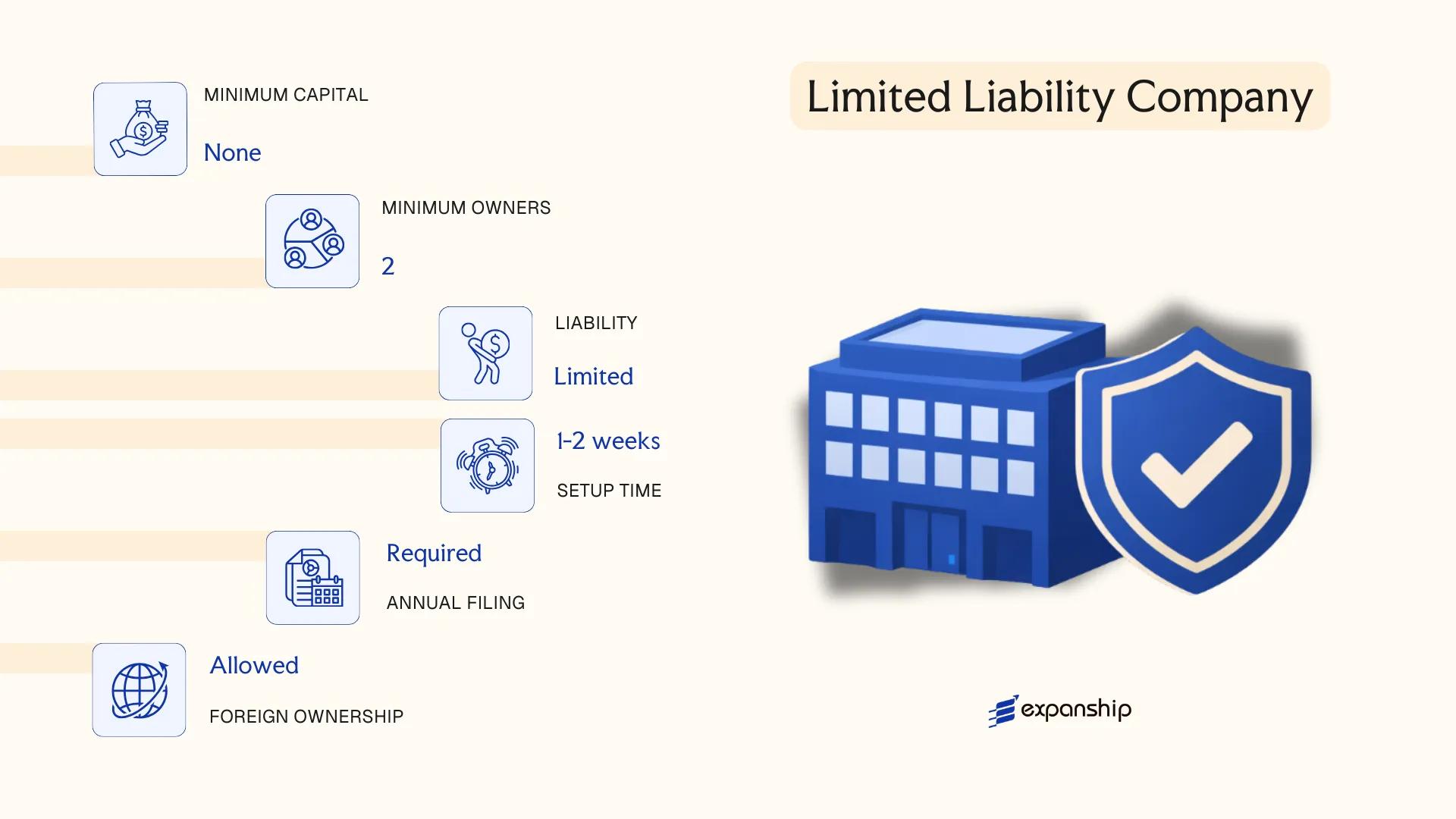

Sociedad de Responsabilidad Limitada (S.R.L.) — Limited Liability Company

The Nicaragua Sociedad de Responsabilidad Limitada is governed by the Código de Comercio de Nicaragua and supplementary corporate legislation. It carries separate legal personality, meaning the entity holds rights and obligations distinct from its members.

Liability is capped at each member's capital contribution. This hybrid character — combining elements of a corporation and a partnership — makes the SRL company Nicaragua practitioners frequently register for small to mid-sized ventures where close ownership control is a priority.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad de Responsabilidad Limitada (S.R.L.) | Governed by the Código de Comercio |

| Members | 2 minimum, 20 maximum | Members hold quotas (cuotas), not shares |

| Management | One or more managers (gerentes) | Can be members or third parties |

| Local Presence | Registered agent and registered address in Nicaragua required | Must be maintained continuously |

| Capital | No statutory minimum; denominated in Nicaraguan Córdobas (NIO) | Capital divided into quotas, not freely transferable |

| Privacy | Member names appear in the public registry | Limited confidentiality |

Focus Points

- Taxation: Subject to corporate income tax at a 30% rate on net profits or 1% on gross income (whichever is higher); standard VAT at 15% applies to taxable supplies; withholding taxes apply to dividends, royalties, and service payments to non-residents.

- Transfer restrictions: Quota transfers require prior consent from remaining members, providing built-in ownership control.

- Annual compliance: Entities must file annual financial statements and tax returns with the Dirección General de Ingresos (DGI).

- Treaty access: Nicaragua has a limited tax treaty network; confirm applicable treaties before structuring cross-border arrangements.

- Conversion: An SRL may be converted into an S.A. through a formal restructuring process requiring notarial deed and re-registration with the Registro Mercantil.

Closing

The SRL suits trading operations, family-owned businesses, and joint ventures where ownership transfer restrictions are desirable, though the 20-member cap and limited quota liquidity restrict its use for businesses anticipating significant investor growth.

This entity type works best for small to mid-sized businesses with a fixed, closely held ownership group seeking straightforward management and capped liability.

Partnerships [Sociedad en Nombre Colectivo, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones]

Nicaragua partnership company structures are governed by the Código de Comercio de Nicaragua (Commercial Code), enacted in 1914 and still the primary legislation regulating commercial entities. Unlike a Sociedad Anónima, partnership forms do not universally grant separate legal personality to their members — liability exposure varies significantly depending on the specific structure chosen.

Three distinct partnership forms exist under the Code. Each carries different liability profiles and internal governance requirements, making the choice of structure a substantive legal decision rather than a procedural one.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad en Nombre Colectivo / Sociedad en Comandita Simple / Sociedad en Comandita por Acciones | Three distinct forms; each registered separately with the Registro Mercantil |

| Members | Partners (socios or socios comanditados/comanditarios) | Nombre Colectivo: minimum 2 general partners, no cap; Comandita forms: at least 1 general + 1 limited partner |

| Liability | General partners: unlimited personal liability; Limited partners (comanditarios): liability capped at capital contribution | Nombre Colectivo has no limited partners — all partners bear full liability |

| Local Presence | Registered agent and registered address in Nicaragua required | Must maintain a physical or legal domicile for official correspondence |

| Capital | No statutory minimum capital in córdobas (NIO); contributions can be in cash or in kind | Comandita por Acciones divides limited partner contributions into transferable shares |

| Privacy | Partner names appear in public registry filings | No beneficial ownership register equivalent to some modern jurisdictions |

Focus Points

- Taxation: General partners in all three forms are subject to corporate income tax at 30% on net profits, with VAT (IVA) at 15% on applicable transactions; withholding tax obligations apply on payments to non-residents.

- Annual Compliance: Entities must file annual financial statements and tax returns with the Dirección General de Ingresos (DGI) and maintain updated registration with the Registro Mercantil.

- Restrictions: Foreign nationals may participate as limited partners, but general partners bear unlimited liability — a significant exposure consideration for foreign investors.

- Conversion: Conversion to a Sociedad Anónima is legally possible but requires a formal amendment process through the Registro Mercantil and public deed execution before a Nicaraguan notary.

- Treaty Access: Nicaragua has a limited network of double taxation agreements; partnership income treatment under any applicable treaty depends on whether the structure is treated as transparent or opaque by the counterpart jurisdiction.

Sub-Types

Sociedad en Nombre Colectivo

All partners carry unlimited, joint, and several liability for the firm's obligations. This form is rarely used for commercial operations involving significant financial exposure, as no partner can limit personal liability through the structure itself.

Sociedad en Comandita Simple

This form distinguishes between general partners (socios comanditados), who bear unlimited liability, and limited partners (socios comanditarios), whose liability is confined to their agreed capital contribution. Limited partners are prohibited from participating in day-to-day management — doing so risks reclassification of their liability status.

Sociedad en Comandita por Acciones

The limited partner's interest is divided into transferable shares (acciones), which functions similarly to a hybrid between a partnership and a corporation. General partners retain unlimited liability, while share-based limited partners gain a degree of transferability not available in the Comandita Simple.

Partnership structures in Nicaragua are generally suited to family-held businesses, professional services arrangements, or joint ventures where at least one party is willing to accept unlimited liability. The Comandita por Acciones offers the most structural flexibility among the three forms, while the unlimited liability of general partners across all three variants remains a significant constraint for most foreign-owned commercial operations.

These structures are most appropriate for closely held domestic businesses or arrangements where the general partner is a corporate entity with limited assets, effectively containing personal liability exposure.

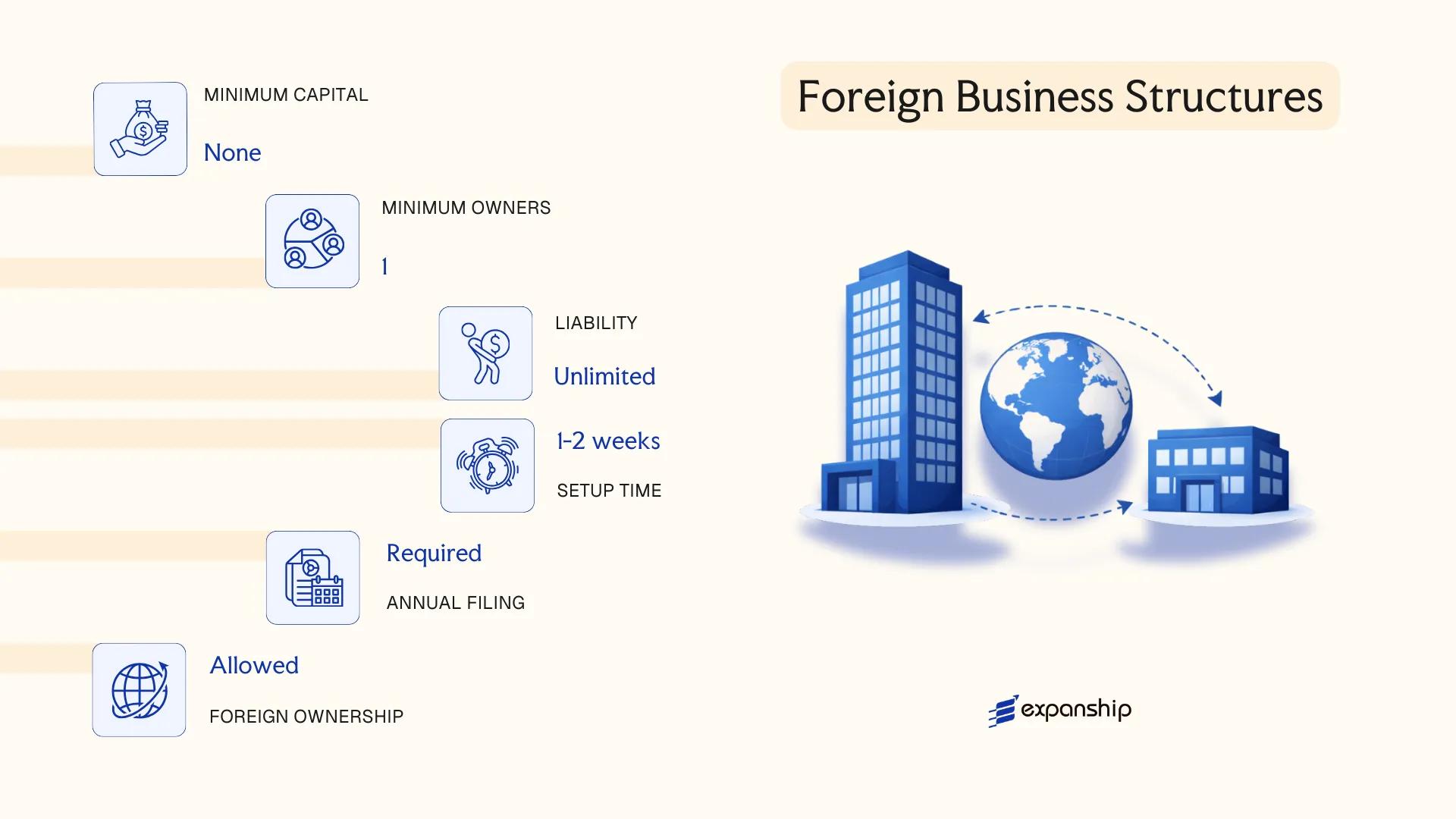

Foreign Business Structures [Branch Office, Representative Office]

A foreign company considering foreign branch office Nicaragua setup operates under the country's Commercial Code (Código de Comercio, 1917) and must register with the Registro Mercantil (Mercantile Registry). Unlike locally incorporated entities, a branch does not constitute a separate legal person — it remains an extension of the parent company, which retains full liability for its obligations.

Registration involves filing authenticated copies of the parent company's constitutive documents, a power of attorney for a local legal representative, and proof of legal existence in the home jurisdiction. The Dirección General de Ingresos (DGI) handles tax registration separately once Mercantile Registry inscription is complete.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; non-trading presence |

| Local Representative | Mandatory — appointed attorney-in-fact resident in Nicaragua | Mandatory — local representative required |

| Registered Address | Physical office address required | Physical address required |

| Minimum Capital | No statutory minimum prescribed | No statutory minimum prescribed |

| Liability | Parent company bears full liability | Parent company bears full liability |

| Privacy | Beneficial ownership of parent disclosed in registry filings | Same disclosure obligations as branch |

Focus Points

- Taxation: Branch profits subject to 30% corporate income tax on Nicaraguan-source income; VAT at 15% applies to taxable supplies; withholding tax obligations apply on remittances to the parent depending on payment type.

- Economic Substance: No formal substance legislation equivalent to offshore regimes, but the DGI may scrutinize thin operations when assessing deductibility of inter-company charges.

- Annual Compliance: Annual tax returns, municipal tax declarations (Impuesto de Matrícula), and renewal of the local operating license (matrícula) with the relevant Alcaldía are required.

- Activity Restrictions: A representative office is limited to promotional, liaison, and market research activities; it cannot invoice clients or generate revenue directly.

- Treaty Access: Nicaragua has a limited tax treaty network; branch structures do not automatically benefit from treaties available to resident corporations.

Sub-Types

Branch Office (Sucursal)

A branch office is authorized to conduct full commercial operations, enter contracts, and generate revenue in its own name on behalf of the parent. This structure suits firms that want operational presence without incorporating a separate local entity.

Representative Office (Oficina de Representación)

A representative office is restricted to non-commercial functions such as supplier coordination, market research, and liaison activities. No commercial invoicing is permitted, which limits its use to preparatory or support roles for the parent's wider operations.

Branch structures are typically chosen by foreign firms testing the market or managing projects with a defined timeline, where establishing a full subsidiary is not commercially justified. The primary advantage is avoiding a separate incorporation process; the clear limitation is that the parent company assumes unlimited liability for all branch obligations.

A branch office suits foreign companies with ongoing project-based work or those evaluating the market before committing to a locally incorporated subsidiary; a representative office is appropriate only where the intended activities are strictly non-commercial.

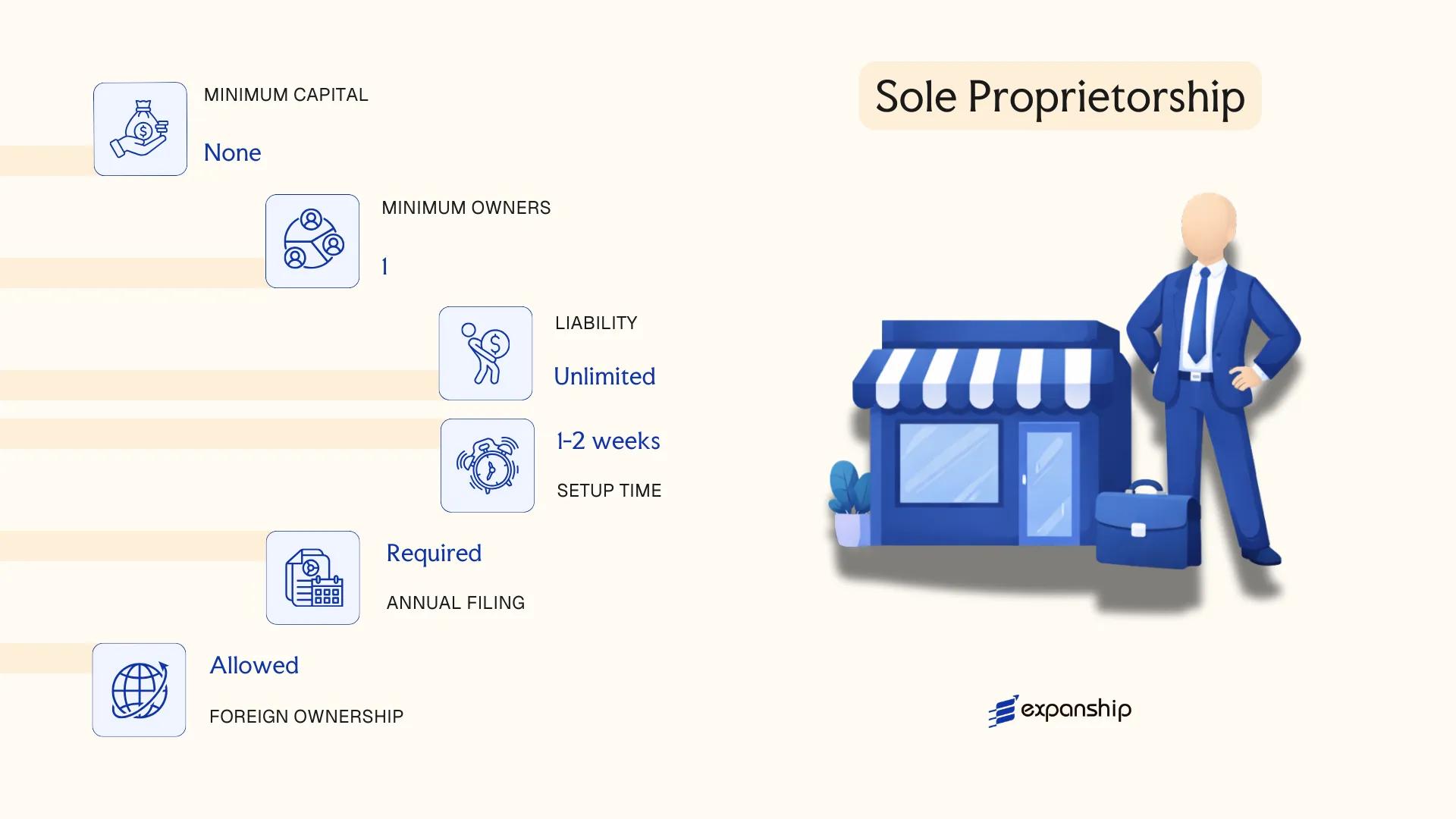

Sole Proprietorship (Empresa Individual)

A Nicaragua sole proprietorship, locally referred to as an Empresa Individual, is the most basic form of business registration available to natural persons. Governed by the Código de Comercio de Nicaragua (Commercial Code of 1914, as amended), this structure grants no separate legal personality — the proprietor and the business are treated as a single legal unit.

Because there is no legal distinction between personal and business assets, the owner bears unlimited personal liability for all commercial obligations incurred. Registration is processed through the Registro Mercantil (Commercial Registry) in the department where the business operates, and the entity must also enroll with the Dirección General de Ingresos (DGI) for tax identification purposes.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Empresa Individual) | No separate legal personality from the owner |

| Owner Title | Proprietor (Propietario) | Single natural person only; legal entities cannot hold this form |

| Members | 1 proprietor; maximum 1 | Cannot be jointly owned |

| Local Presence | Registered address in the operating department | No mandatory local agent requirement, but a physical address is required for registry purposes |

| Capital | No statutory minimum capital requirement; denominated in Nicaraguan Córdoba (NIO) | Declared capital is noted in the commercial registration |

| Liability | Unlimited personal liability | Personal assets are exposed to business debts |

Focus Points

- Taxation: Subject to income tax (IR) under the Ley de Concertación Tributaria (Law 822); general corporate rate applies to business income, with a minimum tax (pago mínimo definitivo) of 1% on gross income; VAT registration required if turnover exceeds statutory thresholds; no separate withholding tax regime distinct from the owner's personal obligations.

- Annual Compliance: Annual income tax return filed with the DGI; municipal business tax (Impuesto de Matrícula) payable to the local Alcaldía; annual renewal of the operating license (matrícula) required.

- Conversion: Can be converted into a formal corporate entity such as an S.A. or S.R.L., though this requires a new registration process rather than a statutory conversion mechanism.

- Treaty Access: As a non-corporate structure, access to Nicaragua's bilateral tax treaties may be limited or unavailable depending on treaty partner definitions of "resident" entities.

- Restrictions: Foreign nationals face practical restrictions; non-residents typically cannot register as a sole trader without establishing legal residency or a local presence.

Closing Paragraph

The Empresa Individual suits local entrepreneurs, freelancers, and micro-business operators who require a low-cost, administratively simple structure for domestic commercial activity. The primary advantage is minimal setup cost and straightforward compliance, while the defining limitation is unlimited personal liability, which exposes the proprietor's personal estate to all business risks.

This structure is most appropriate for resident individuals operating small-scale, low-risk domestic businesses who do not require liability separation or external investment capacity.

How to Choose the Right Entity Type in Nicaragua

Selecting how to structure your business in Nicaragua has direct legal and financial consequences that extend well beyond registration day.

Why Your Entity Choice Matters

The structure you register determines your compliance obligations, tax exposure, and operational capacity from the outset. Choosing incorrectly produces concrete, sometimes costly outcomes:

- Selecting an S.A. when a single-person consultancy is the intended operation adds unnecessary overhead, including annual shareholder meeting requirements and potential audit obligations that do not apply to a Sole Proprietorship.

- Choosing an entity without the capacity to establish genuine local presence when the Dirección General de Ingresos requires demonstrable economic activity can trigger compliance failures and penalties under Nicaragua's tax administration framework.

- Forming a standard commercial company when your primary objective is asset protection or succession planning locks you into annual corporate obligations that a different structure may not require.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each point toward distinct entity types under Nicaragua's Commercial Code.

- Ownership and Management: Single-founder operations suit a Sole Proprietorship or S.R.L., while multi-party ventures requiring a board structure align more naturally with an S.A.

- Tax Objectives: Your eligibility for specific regimes under Nicaragua's tax legislation depends partly on the entity form you select.

- Privacy Requirements: The S.A. involves public registry disclosure of corporate officers; nominee arrangements may be necessary if confidentiality is a priority.

- Substance Capacity: If maintaining a physical presence or local payroll is not feasible, your entity choice should reflect that operational reality.

- Exit Strategy: Not all structures permit redomiciliation or conversion; confirm these options before formation.

Corporate Compliance Services in Nicaragua

Maintain your Nicaraguan entity in good standing with registered agent, annual filings, and regulatory support.

Conclusion

Selecting the right structure is one of the first consequential decisions in any incorporating a company in Nicaragua guide. The Sociedad Anónima remains the most registered entity type in the country, favored by foreign investors and domestic operators alike due to its transferable share structure and separation of liability. The Sociedad de Responsabilidad Limitada suits smaller operations where ownership is closely held and share transferability is less of a priority. Partnerships under the Código de Comercio carry unlimited liability and are generally chosen by professionals in specific service sectors. Branch offices and representative offices serve multinationals with defined, limited mandates rather than full operational presence.

Nicaragua has been gradually expanding its bilateral investment treaty network, and ongoing reforms to the Registro Mercantil process reflect a broader administrative modernization effort. For businesses weighing a Nicaragua company formation summary against other Central American jurisdictions, understanding which structure aligns with your operational scope and ownership model is the foundation of sound entity planning.

How Expanship Can Assist You

Expanship's Nicaragua company incorporation services cover the full registration process, from selecting the right entity structure, whether a Sociedad Anónima or a Sociedad de Responsabilidad Limitada, to filing with the Registro Mercantil and obtaining your operating licence through the Dirección General de Ingresos (DGI). Every step involves jurisdiction-specific requirements, and our team works directly within those frameworks.

Our Expanship Nicaragua business registration support includes:

- Preparation and legalization of incorporation documents

- Registered agent and registered office provision

- Filing and liaison with the Registro Mercantil and DGI

- Post-incorporation compliance management, including annual obligations

- Banking introduction assistance for corporate accounts in Nicaragua

Reach out to Expanship Nicaragua to discuss your entity setup.

Frequently Asked Questions (FAQ)

The Sociedad Anónima (S.A.) is the most frequently registered entity. Its ability to issue transferable shares and admit an unlimited number of shareholders makes it the default choice for both domestic operators and foreign investors.

Both structures offer limited liability, but the S.R.L. restricts the transfer of membership quotas and caps participation at thirty members, whereas an S.A. places no such ceiling. For compliance purposes, the S.A. carries slightly heavier administrative requirements, including formal shareholder meeting procedures under the Commercial Code.

The S.A. historically offers the most privacy, as bearer shares were once permitted, though reforms have tightened beneficial ownership disclosure. Nominee shareholder arrangements remain legally permissible, but registered information is filed with the Registro Mercantil.

No. A Sociedad en Nombre Colectivo and both Comandita forms require a minimum of two partners by statute. An S.A. and an S.R.L. can technically be formed by a single founder, though ongoing governance requirements apply to each.

Foreign nationals may form an S.A. or S.R.L. without restriction on nationality. Full foreign ownership is permitted, though the entity must register with the Registro Mercantil and obtain a Registro Único del Contribuyente (RUC) from the Dirección General de Ingresos.

Conversion between entity types is generally addressed through transformation procedures under the Commercial Code, though it is not uniformly standardized for all combinations. An S.R.L. converting to an S.A. is the most legally established path; other transformations may require dissolution and re-incorporation.

The S.A., S.R.L., Sociedad en Comandita por Acciones, and Sociedad en Comandita Simple all hold separate legal personality once registered. The Sociedad en Nombre Colectivo also acquires legal personality upon Registro Mercantil inscription, though partners remain jointly and severally liable for firm obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.