Key Takeaways

- New Caledonia's corporate structures — including the SA, SAS, SARL, and EURL — are registered through the Registre du Commerce et des Sociétés administered by the Tribunal Mixte de Commerce de Nouméa, not through metropolitan French authorities.

- Despite its status as a French special collectivity under the Nouméa Accord, New Caledonia operates its own tax system with locally determined rates independent of France's national fiscal framework.

- The SARL is the most widely registered entity form for small and medium-sized businesses, while the SA is better suited to large enterprises requiring access to capital markets.

- Foreign businesses entering New Caledonia can choose between a branch, representative office, or liaison office, each carrying different levels of operational scope and regulatory obligation.

Introduction to Entity Types in New Caledonia

New Caledonia is a French special collectivity located in the southwestern Pacific Ocean, approximately 1,500 kilometres east of Australia and north of New Zealand, within the Melanesian arc of islands. Its political status is distinct: it holds a sui generis status under the French Republic, with significant autonomy governed by the Nouméa Accord and codified in Title XIII of the French Constitution.

Business entity types in New Caledonia are registered through the Registre du Commerce et des Sociétés (RCS), administered locally by the Tribunal Mixte de Commerce de Nouméa. The territory operates its own tax system, separate from metropolitan France, with locally determined rates on corporate income, goods and services, and other fiscal matters.

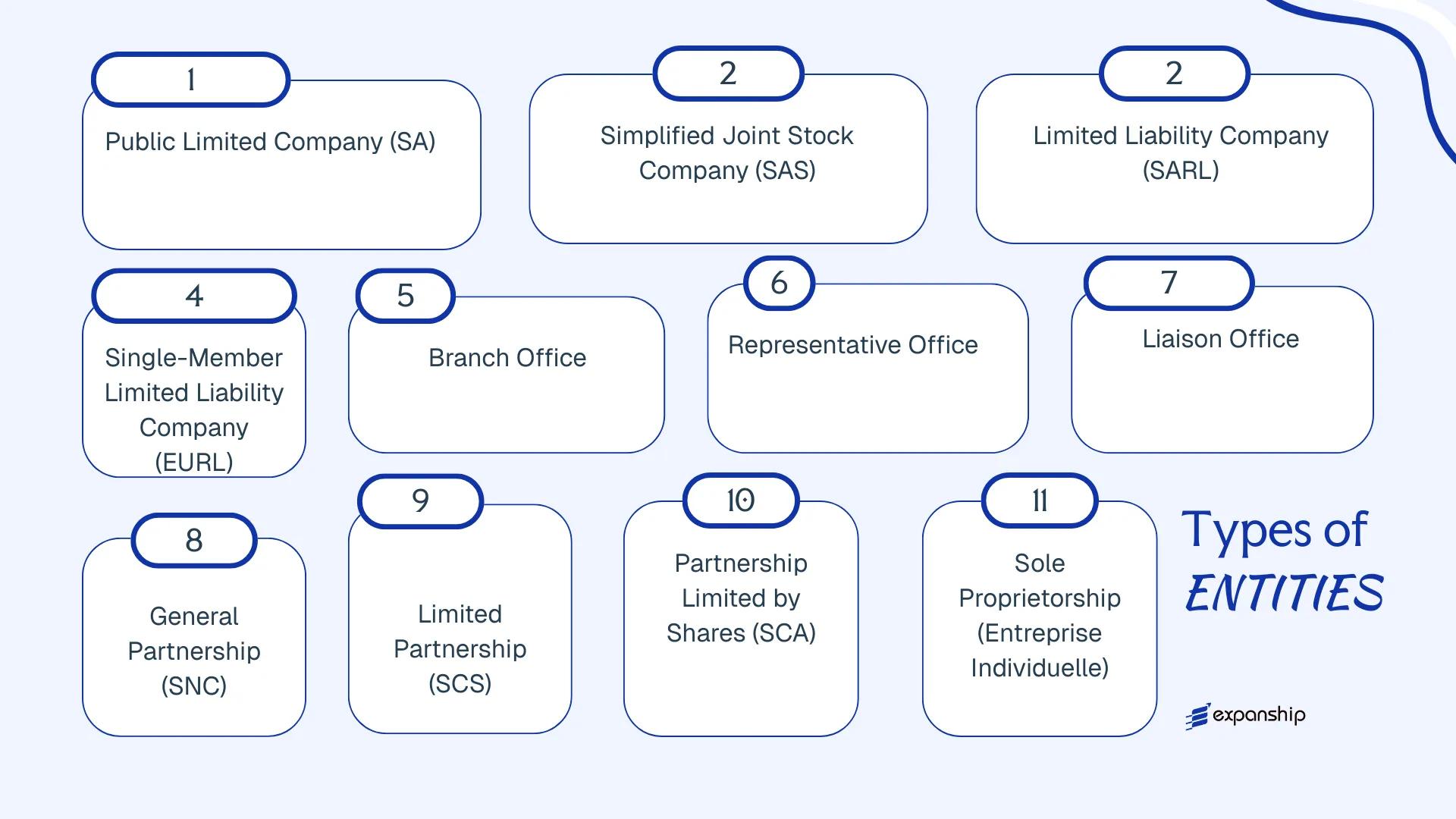

Available corporate structures include the Société Anonyme (SA), Société par Actions Simplifiée (SAS), Société à Responsabilité Limitée (SARL), and Entreprise Unipersonnelle à Responsabilité Limitée (EURL). Foreign businesses may establish a branch, representative office, or liaison office. Partnership forms — the Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), and Société en Commandite par Actions (SCA) — are also recognised, alongside sole proprietorship arrangements including the Entreprise Individuelle and the Auto-Entrepreneur regime.

Each of these New Caledonia company structures is examined in detail across the sections that follow.

An Overview of Business Structures in New Caledonia

New Caledonia's company law framework recognises several distinct legal forms, governed primarily by local adaptations of French commercial law as applied through the territorial legal system administered by the Tribunal Mixte de Commerce. Each structure carries different implications for liability, taxation, governance, and membership requirements. The sections that follow examine each form in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| SA | Share company | Limited to shares | Taxed (IS) | Permitted | 7 shareholders | Tribunal Mixte de Commerce | French Commercial Code (adapted) |

| SAS | Simplified share company | Limited to shares | Taxed (IS) | Permitted | 1 shareholder | Tribunal Mixte de Commerce | French Commercial Code (adapted) |

| SARL | Limited liability company | Limited to contribution | Taxed (IS) | Permitted | 1–100 associates | Tribunal Mixte de Commerce | French Commercial Code (adapted) |

| EURL | Single-member LLC | Limited to contribution | Taxed (IR or IS) | Permitted | 1 associate | Tribunal Mixte de Commerce | French Commercial Code (adapted) |

| SNC | General partnership | Unlimited, joint | Taxed (IR) | Permitted | 2 partners | Tribunal Mixte de Commerce | French Commercial Code (adapted) |

| SCS | Limited partnership | Mixed liability | Taxed (IR) | Permitted | 2 partners | Tribunal Mixte de Commerce | French Commercial Code (adapted) |

| SCA | Partnership limited by shares | Mixed liability | Taxed (IS) | Permitted | 4 members | Tribunal Mixte de Commerce | French Commercial Code (adapted) |

| Branch Office | Foreign branch | Parent liable | Taxed (IS) | Permitted | N/A | Tribunal Mixte de Commerce | French Commercial Code (adapted) |

| Representative Office | Non-trading office | Parent liable | Generally exempt | Not permitted | N/A | Territorial authorities | Local regulatory framework |

| Entreprise Individuelle | Sole proprietorship | Unlimited | Taxed (IR) | Permitted | 1 individual | Tribunal Mixte de Commerce | French Commercial Code (adapted) |

| Auto-Entrepreneur | Micro-enterprise | Unlimited | Taxed (IR) | Permitted | 1 individual | Territorial tax authority | Local territorial ordinance |

Each of these structures is examined in full in the sections below.

Société Anonyme (SA)

The Société Anonyme (SA) in New Caledonia is governed by French commercial law principles as adapted and applied through local ordinances and regulations, given the territory's status as a French collectivity with significant legislative autonomy. The SA carries separate legal personality, meaning the company holds rights and obligations independently of its shareholders, with liability confined to each shareholder's capital contribution.

Structured for larger enterprises or those anticipating public investment, an SA company formation in New Caledonia requires a formal governance framework, including a board of directors or a two-tier supervisory structure, making it more administratively demanding than most other local entity forms.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (SA) | Equivalent to a public limited company |

| Members | Shareholders (actionnaires); minimum 7 | No statutory maximum on shareholders |

| Governance | Board of Directors (Conseil d'Administration) or Supervisory Board + Management Board | Minimum 3, maximum 18 directors on the CA |

| Minimum Capital | XPF 10,000,000 (approximately EUR 84,000) | At least half must be paid up on incorporation |

| Local Presence | Registered office required in New Caledonia | Physical address; not a PO box |

| Privacy | Shareholder identity disclosed in public filings | Directors named in RIDET registry records |

Focus Points

- Taxation: Subject to the Impôt sur les Sociétés (IS) at the standard corporate rate applicable in New Caledonia; dividend distributions may attract local withholding tax, and indirect taxes including the Taxe Générale sur les Services (TGS) apply to qualifying transactions.

- Annual Compliance: Mandatory statutory audit by a commissaire aux comptes, annual general meetings, and financial statement filings with the RIDET commercial registry.

- Economic Substance: No formalised economic substance regime equivalent to some offshore jurisdictions, but operational and governance presence is implicit given the SA's structural requirements.

- Conversion: An SA may be converted into an SAS or SARL, subject to meeting the target entity's capital and membership conditions, and requires shareholder resolution and re-registration.

- Restrictions: Foreign shareholders may hold equity without restriction in most sectors, though regulated industries such as mining and broadcasting involve sector-specific approval requirements.

Closing

The SA suits large commercial enterprises, joint ventures with institutional investors, or businesses seeking eventual access to capital markets, though the minimum capital threshold and mandatory audit obligations represent a meaningful administrative and financial commitment. The two-tier governance option provides structural flexibility for complex ownership arrangements.

Best suited for large-scale enterprises, institutional joint ventures, or businesses structured for future capital-raising activity.

Company Incorporation in New Caledonia

Expanship assists with SA formation, registry filings, and ongoing compliance in New Caledonia.

Société par Actions Simplifiée (SAS)

The Société par Actions Simplifiée SAS New Caledonia framework derives from French corporate law transposed into the territory's legal order, operating under the provisions of the French Commercial Code as applied locally. As a legal entity distinct from its shareholders, the SAS carries its own rights and obligations, with member liability confined to capital contributions.

Structurally, the SAS occupies a middle ground between the rigidity of a Société Anonyme and the informality of a SARL. Its statutes (articles of association) govern most internal arrangements, giving founders wide latitude to define governance, share transfer conditions, and decision-making procedures.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société par Actions Simplifiée | Separate legal personality; limited liability |

| Members | Shareholders: minimum 2 (no maximum) | A sole shareholder triggers SASU status |

| Management | President (required); other officers optional | President can be a legal entity |

| Capital | No statutory minimum | Contributions can be cash or in kind |

| Local Presence | Registered office in New Caledonia required | Must be a physical address |

| Privacy | Shareholder identity filed with the RIDET registry | Not fully private |

Focus Points

- Taxation: Subject to corporate income tax (Impôt sur les Sociétés) at the rate applicable in New Caledonia; VAT obligations apply to taxable supplies; dividend distributions may attract withholding tax under local rules.

- Annual Compliance: Annual accounts must be filed; statutory audit is not required unless the entity exceeds defined thresholds.

- Economic Substance: No standalone economic substance regime mirrors offshore jurisdictions, but genuine local activity is expected to support tax residency claims.

- Conversion: An SAS can generally be converted into another commercial form (SA or SARL) subject to shareholder approval and regulatory formalities.

- Restrictions: Shares in an SAS cannot be offered to the public; the entity cannot be listed on a stock exchange.

Closing

The SAS suits holding structures, joint ventures, and businesses where founding shareholders require customised governance arrangements. Its flexibility on capital and internal rules is a practical advantage; however, the prohibition on public share offerings limits growth financing options.

The SAS is best suited for two or more investors or corporate groups seeking contractual freedom in governance without the administrative burden of a full Société Anonyme.

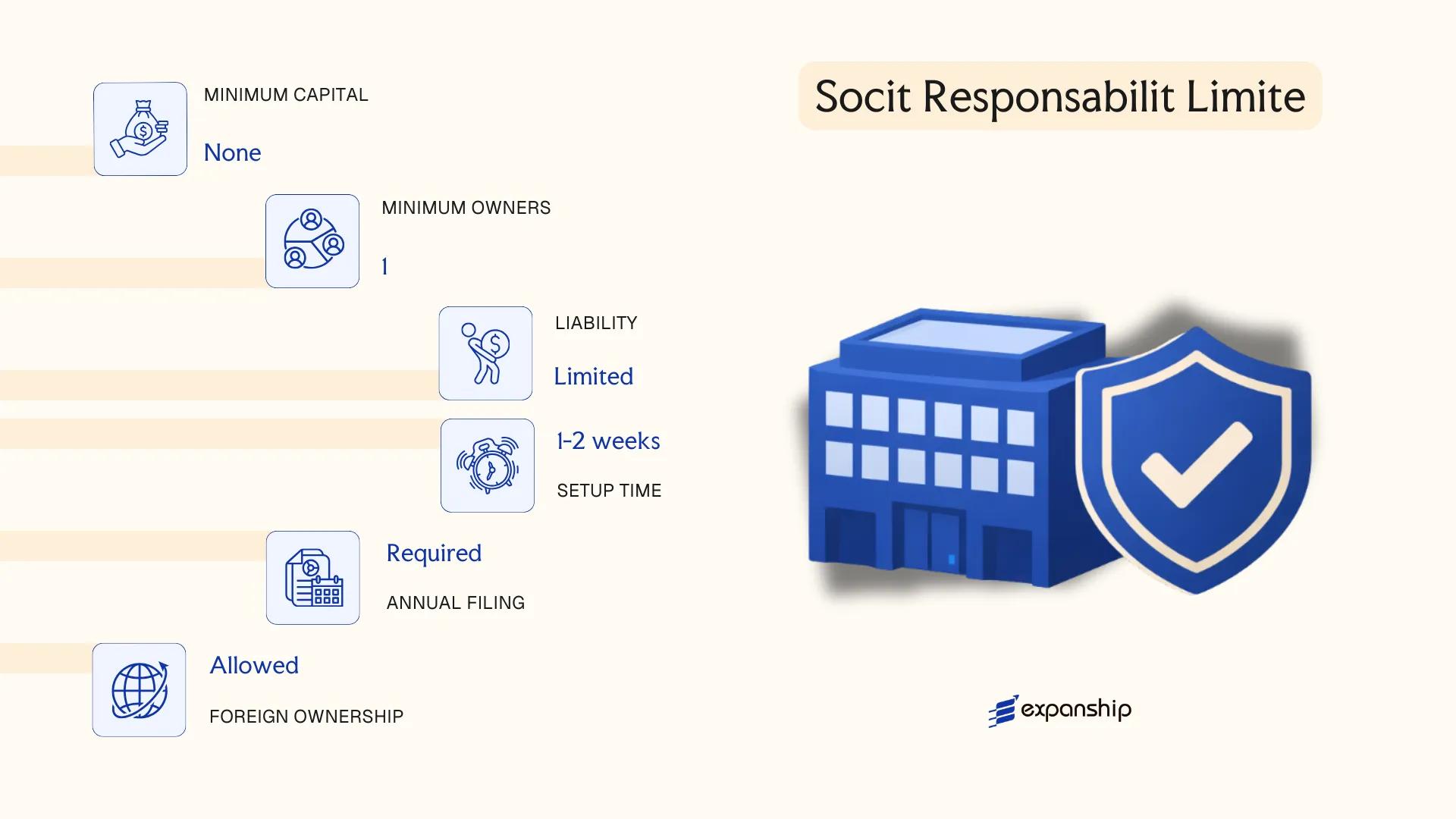

Société à Responsabilité Limitée (SARL)

The Société à Responsabilité Limitée SARL New Caledonia framework derives from French commercial law as adapted and applied through the territory's legal system, which mirrors the French Code de commerce in its foundational structure. As a hybrid entity, it combines the liability protection of a capital company with the operational flexibility typically associated with smaller, closely held businesses.

Each associate's liability is capped at their contribution to the share capital, meaning personal assets remain insulated from company debts. Registration is handled through the Registre du Commerce et des Sociétés (RCS) at the Tribunal Mixte de Commerce de Nouméa.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société à Responsabilité Limitée | Separate legal personality upon RCS registration |

| Members | Associates (associés); 2–100 | Managed by one or more gérants (managers), who may or may not be associates |

| Local Presence | Registered office (siège social) in New Caledonia | Physical address required; virtual offices may be accepted in practice |

| Capital | No statutory minimum; denominated in CFP Franc (XPF) | Capital divided into parts sociales (non-negotiable shares) |

| Share Transfer | Restricted; requires majority approval of associates | Parts sociales cannot be freely traded on a market |

| Privacy | Associates listed in RCS; gérant identity is public | Beneficial ownership disclosure follows applicable local requirements |

Focus Points

- Taxation: Subject to Impôt sur les Sociétés (IS) at the applicable New Caledonia corporate rate; VAT (TVA) obligations apply where thresholds are met; dividend distributions may attract withholding tax under local rules.

- Annual Compliance: Annual accounts must be filed; a gérant is required to present financial statements to associates within six months of the financial year-end.

- Treaty Access: New Caledonia is a French collectivity and does not independently conclude tax treaties; treaty access depends on the application of French conventions, which is limited in this territory.

- Conversion: An SARL may be converted to an SA or SAS upon meeting the relevant conditions and following the prescribed formalities under commercial law.

- Restrictions: Parts sociales cannot be offered to the public; the 100-associate cap makes this structure unsuitable for entities anticipating broad investor participation.

Closing

The SARL suits small to medium-sized trading or service businesses where the founders want liability protection without the governance formality required of an SA. The absence of a minimum capital requirement lowers the barrier to SARL formation in New Caledonia, though the restricted transferability of shares limits flexibility for businesses that may seek outside investment.

Best suited for resident entrepreneurs or small foreign-owned operating subsidiaries with a defined group of associates and no plans for public capital-raising.

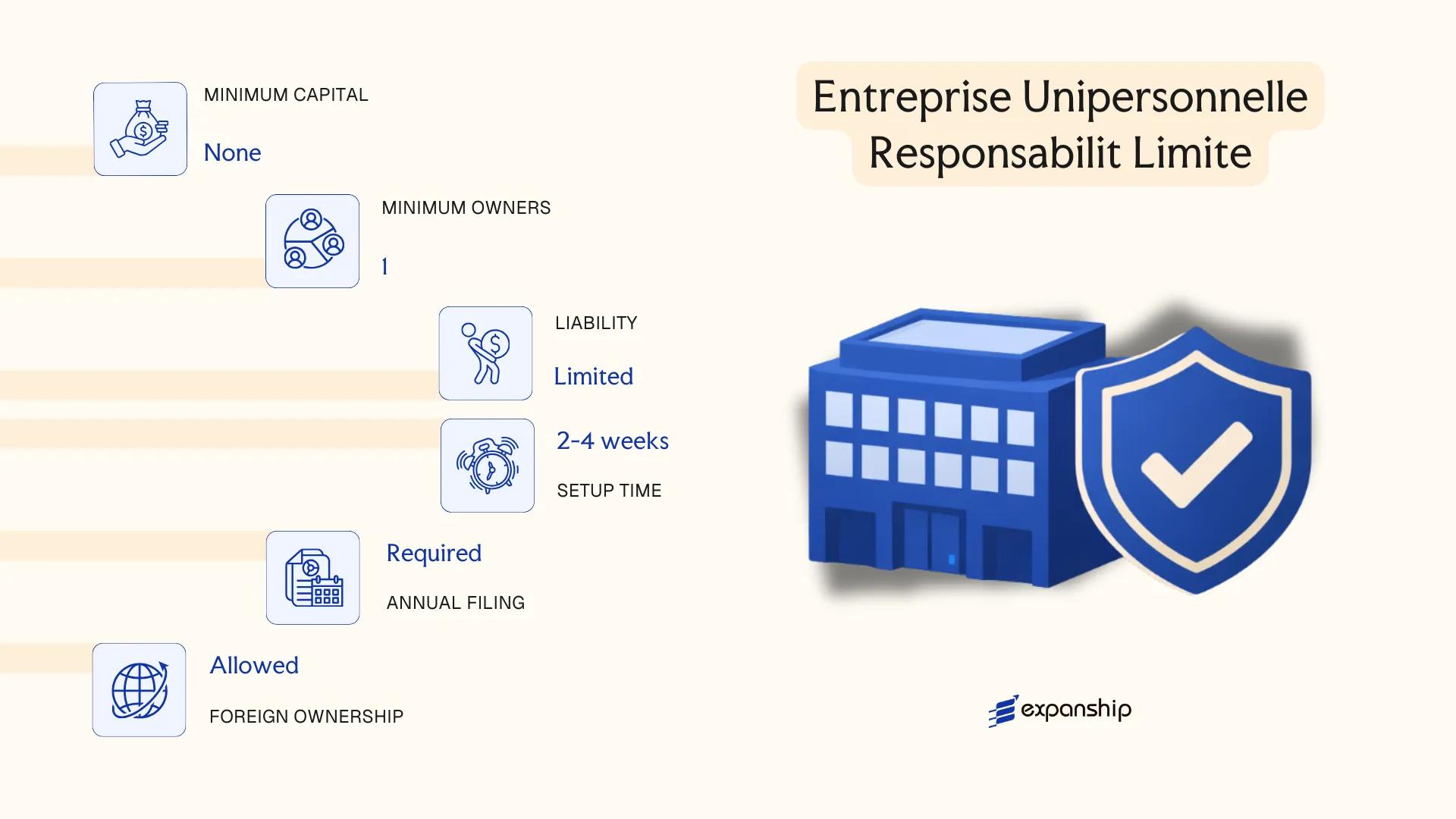

Entreprise Unipersonnelle à Responsabilité Limitée (EURL)

The EURL single member company in New Caledonia is a single-shareholder variant of the SARL, governed by the same foundational commercial law framework adapted from the French Code de commerce and applied through local ordinances under New Caledonia's statute of autonomy. As a distinct legal entity, it carries separate legal personality from its sole owner, meaning the shareholder's personal assets remain protected from business liabilities. This hybrid structure sits between a sole proprietorship and a multi-member company, offering formal limited liability within a simplified governance model.

Registration of an Entreprise Unipersonnelle à Responsabilité Limitée in New Caledonia is processed through the Centre de Formalités des Entreprises (CFE), which coordinates filings with the Registre du Commerce et des Sociétés (RCS). A single natural person or legal entity may hold 100% of the shares.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Single-member limited liability company | Treated as an SARL with one shareholder |

| Members | 1 sole shareholder (associé unique) | Cannot be held by another single-member SARL |

| Management | Gérant (manager); may be the sole shareholder | No board requirement |

| Local Presence | Registered office address in New Caledonia | Physical address required for RCS filing |

| Capital | No statutory minimum; denominated in XPF | Capital must be fully declared at formation |

| Privacy | Shareholder identity disclosed in RCS register | Publicly accessible records |

Focus Points

- Taxation: Subject to New Caledonia's territorial corporate tax (impôt sur les sociétés) unless the sole shareholder elects transparency for personal income tax; local TGC (taxe générale sur la consommation) applies to qualifying transactions; no French metropolitan withholding tax regime applies directly.

- Annual Compliance: Annual accounts must be filed with the RCS; a gérant's management report is required each fiscal year.

- Conversion: An EURL converts automatically to an SARL upon the admission of a second shareholder, without requiring a new incorporation procedure.

- Treaty Access: New Caledonia operates under a distinct tax jurisdiction and is not party to France's tax treaty network, limiting treaty-based withholding tax relief.

- Restrictions: The sole shareholder may not simultaneously be the sole shareholder of another EURL.

Closing Paragraph

The EURL suits solo entrepreneurs and foreign investors seeking a single-owner trading or holding vehicle with defined liability protection. Its principal advantage is the ability to operate as a formal limited liability entity without co-shareholders; the primary constraint is exclusion from France's metropolitan tax treaty network, which affects cross-border structuring.

Best suited for individual entrepreneurs or a single foreign parent company establishing a wholly owned subsidiary in New Caledonia with straightforward operational or holding activity.

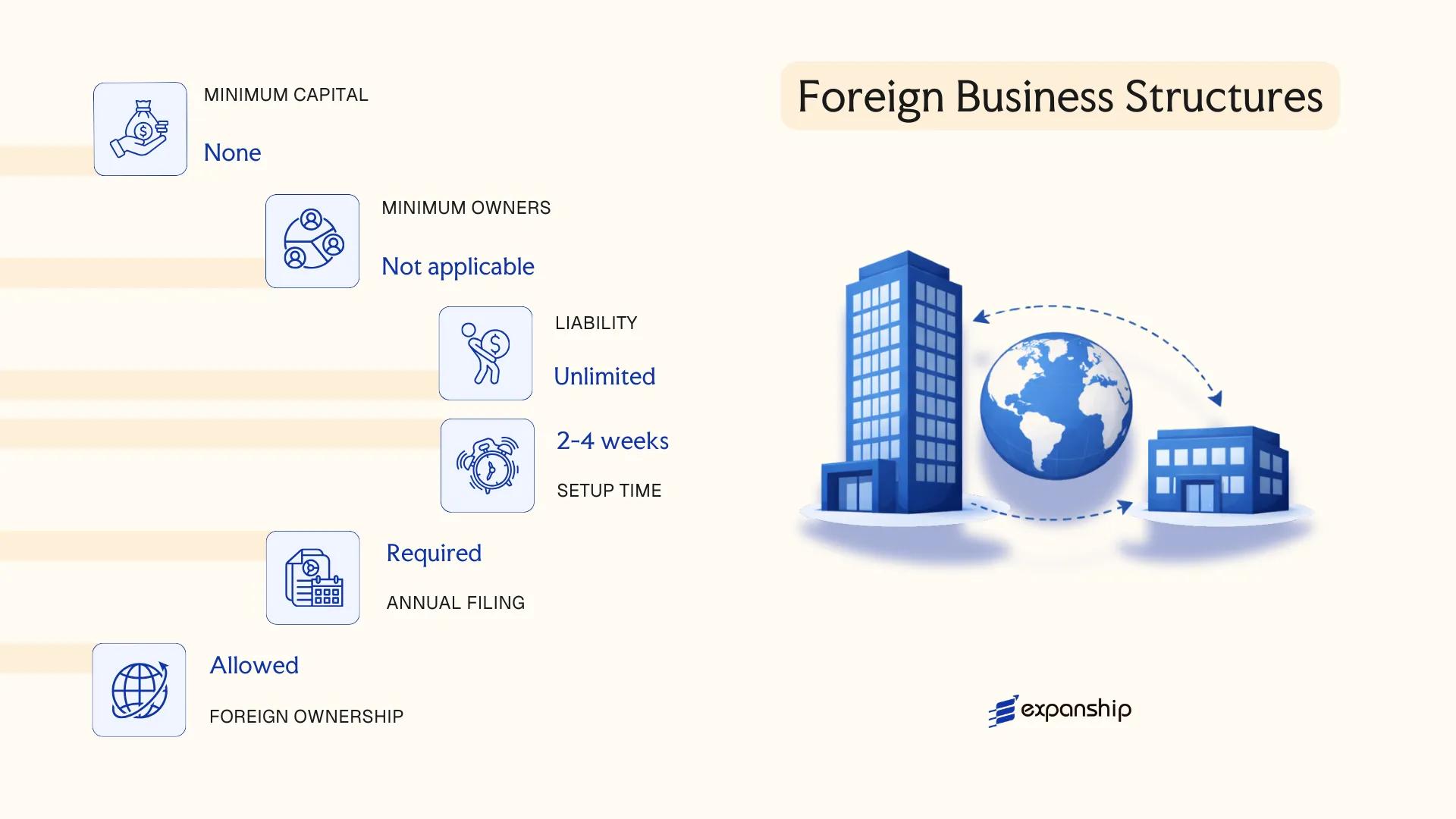

Foreign Business Structures in New Caledonia [Branch Office, Representative Office, Liaison Office]

Foreign companies seeking a presence without incorporating a local entity can establish a foreign company branch office New Caledonia through procedures governed by the French commercial law framework, which applies in adapted form under New Caledonia's institutional arrangements. A branch has no separate legal personality — it remains an extension of the parent company, which bears full liability for its obligations.

Registration is handled through the Registre du Commerce et des Sociétés (RCS) administered by the Tribunal Mixte de Commerce in Nouméa. The parent company must submit certified constitutional documents, translated into French where necessary, alongside proof of the parent's legal existence in its home jurisdiction.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch / Representative / Liaison Office | No separate legal personality in any form |

| Parent Liability | Full liability borne by parent company | Unlimited exposure for branch obligations |

| Local Representative | Mandatory appointed representative | Must be resident or locally reachable |

| Registered Address | Physical address in New Caledonia required | P.O. Box not accepted |

| Capital Requirement | None | Parent's capital structure applies |

| Commercial Activity | Permitted for branch; restricted for rep/liaison offices | Liaison offices may not generate local revenue |

Focus Points

- Taxation: Branches are subject to New Caledonia's local corporate tax (impôt sur les sociétés) on locally sourced profits; withholding tax may apply on profit remittances to the parent; representative and liaison offices generating no local income generally fall outside the corporate tax net.

- Economic Substance: Branches conducting commercial activity are expected to maintain genuine operational presence; purely administrative offices face less scrutiny but must not exceed their permitted scope.

- Annual Compliance: Annual accounts and any modifications to the parent's structure must be filed with the RCS; failure to update registrations can result in deregistration.

- Treaty Access: France's tax treaties do not automatically extend to New Caledonia; treaty coverage depends on the specific bilateral instrument and its territorial scope clause.

- Conversion: A branch can be converted into a locally incorporated entity, though the process requires fresh incorporation and transfer of assets rather than a simple transformation.

Sub-Types

Branch Office

A branch (succursale) is registered with the RCS and may conduct full commercial operations on behalf of the parent. It is the only foreign establishment form through which revenue-generating activity is permitted.

Representative Office

A representative office carries out market research, promotional activities, and liaison functions on behalf of the parent but may not conclude contracts or generate revenue directly in the territory.

Liaison Office

Functionally similar to a representative office, a liaison office is limited strictly to administrative coordination and communication between the parent and local contacts. It is the most restricted form and unsuitable for any commercial engagement.

A branch suits foreign firms testing the local market or executing specific projects, with the advantage of straightforward setup relative to full incorporation; the principal limitation is that the parent company assumes unlimited liability for all branch obligations.

Foreign companies with defined, short-to-medium-term commercial objectives or preparatory market activity before committing to full local incorporation.

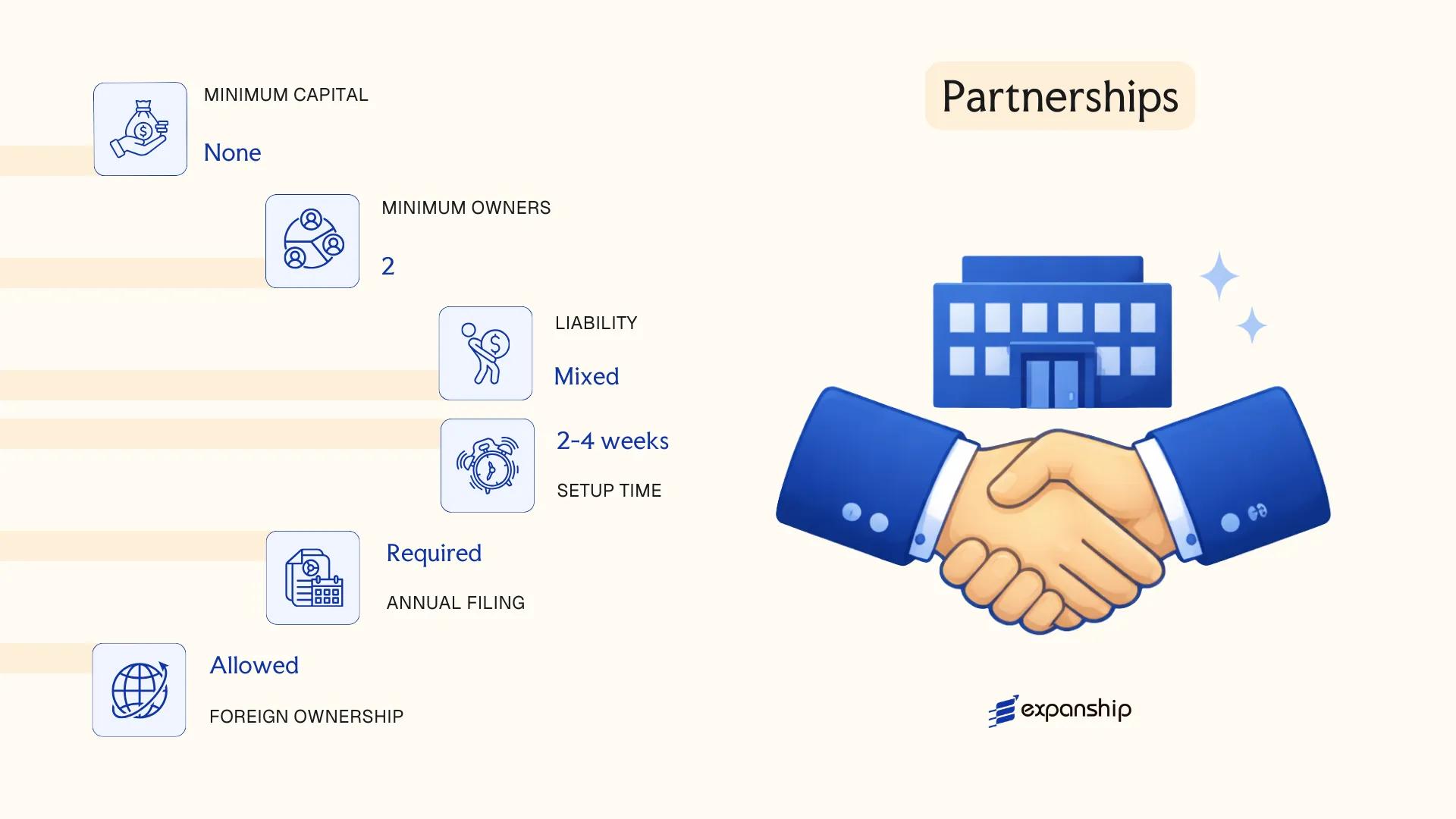

Partnerships in New Caledonia [Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA)]

Partnership structures in New Caledonia SNC SCS SCA are governed by the French commercial code as applied locally, given that New Caledonia operates under a framework derived from French civil and commercial law. Three principal forms exist: the Société en Nom Collectif (SNC), the Société en Commandite Simple (SCS), and the Société en Commandite par Actions (SCA).

Each form constitutes a distinct legal entity upon registration with the Tribunal Mixte de Commerce. Liability treatment varies across the three: SNC partners bear unlimited joint liability, while the SCS and SCA structures introduce a tiered liability model separating active managers from passive investors.

Key Characteristics

| Requirement | SNC | SCS | SCA |

|---|---|---|---|

| Legal Form | General partnership | Limited partnership | Partnership limited by shares |

| Members | Associés (min. 2, no maximum; all bear unlimited liability) | At least 1 general partner (unlimited liability) + 1 limited partner | At least 1 general partner (unlimited liability) + min. 3 shareholders |

| Capital | No statutory minimum | No statutory minimum | Minimum capital required (aligned with French SCA rules) |

| Local Presence | Registered office in New Caledonia required | Registered office in New Caledonia required | Registered office in New Caledonia required |

| Privacy | Partner identities disclosed in public registration filings | Partner identities disclosed; limited partners have some separation | General partners publicly disclosed; shareholders may have limited disclosure |

Focus Points

- Taxation: Profits are generally taxed at the partner level under pass-through treatment; corporate income tax may apply depending on elections made; local provincial tax rules and the Impôt sur les Sociétés framework govern where applicable.

- Annual Compliance: Financial statements must be filed; SCA entities face additional reporting obligations comparable to share-capital companies.

- Treaty Access: New Caledonia is not an independent treaty jurisdiction; French tax treaties do not automatically extend, which limits access to reduced withholding rates.

- Restrictions: SNC partners cannot transfer their shares without unanimous consent of all other partners, creating significant liquidity constraints.

- Conversion: An SNC may convert to an SARL or SA subject to compliance with applicable transformation procedures under commercial law.

Sub-Types

Société en Nom Collectif (SNC)

The SNC is the base general partnership form, where every partner assumes unlimited, joint, and several liability for the entity's debts. It is most commonly used by professional firms or family-owned trading businesses where all participants are actively involved in management.

Société en Commandite Simple (SCS)

The SCS New Caledonia limited partnership structure separates the gérant (general partner) who manages the business and bears unlimited liability, from commanditaires (silent partners) whose liability is capped at their capital contribution. This form suits investors who wish to participate financially without exposure to operational liability.

Société en Commandite par Actions (SCA)

The SCA New Caledonia partnership by shares combines partnership governance with a share capital structure, allowing the firm to raise capital from shareholders while retaining management control with general partners. Its relative complexity makes it uncommon among small operators but relevant for structured investment vehicles.

These partnership forms are most frequently used for family businesses, professional services, and structured investment arrangements where management control must remain with a defined group. The tiered liability structure of the SCS and SCA offers capital-raising flexibility, though the unlimited liability exposure of general partners across all three forms remains a significant operational risk.

Partnership structures in New Caledonia are best suited to closely held businesses or investment vehicles where founders require strict control over management and are prepared to accept the liability implications of the general partner role.

Sole Proprietorship in New Caledonia [Entreprise Individuelle, Auto-Entrepreneur]

A sole proprietorship in New Caledonia, registered as an Entreprise Individuelle, carries no separate legal personality — the business and its owner are legally the same entity. This means the proprietor bears unlimited personal liability for all business debts, with personal assets exposed to creditors.

Registration is handled through the Registre du Commerce et des Sociétés (RCS) or the Répertoire des Métiers, depending on the nature of the activity — commercial or craft-based. Auto-entrepreneur New Caledonia registration follows a simplified administrative path under a micro-enterprise regime, designed to reduce bureaucratic friction for small-scale self-employed operators.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole proprietorship (no separate legal entity) | Owner and business are legally identical |

| Members | Sole proprietor (1 individual) | No shareholders or directors; owner operates directly |

| Local Presence | Registered business address required | Must register with RCS or Répertoire des Métiers |

| Capital | No minimum capital requirement | No formal capital injection needed |

| Liability | Unlimited personal liability | Personal assets at risk for business obligations |

| Privacy | Owner's identity publicly registered | RCS records are accessible |

Focus Points

- Taxation: Subject to personal income tax on business profits; turnover-based flat-rate taxation available under the auto-entrepreneur regime; local territorial tax rules apply in place of French metropolitan rates.

- Annual Compliance: Annual income declaration required; auto-entrepreneurs report turnover periodically to the relevant social and tax authorities.

- Conversion: Can be converted into a limited liability structure such as an EURL, though conversion requires a formal incorporation process.

- Treaty Access: As an unincorporated structure, treaty benefits under double taxation agreements do not generally apply.

- Restrictions: Foreign nationals may face additional authorisation requirements to operate as self-employed in New Caledonia.

Sub-Types

Entreprise Individuelle (Standard)

The standard form registers the individual as a commercial or craft operator without any liability cap. This structure suits tradespeople, consultants, and small retailers who operate independently with low external risk.

Auto-Entrepreneur (Micro-Enterprise Regime)

Available to individuals below defined turnover thresholds, this variant simplifies tax and social contribution calculations through a flat-rate system. It is used primarily by freelancers and part-time self-employed operators with limited revenue.

Sole Proprietorship as a Business Vehicle

This structure functions primarily as a vehicle for individual traders, artisans, and freelancers operating at small scale. The absence of a capital requirement lowers the barrier to entry, though unlimited personal liability remains a material drawback for any activity carrying financial or legal risk.

Sole proprietorship in New Caledonia suits resident individuals conducting low-risk, single-operator activities — particularly those testing a business concept before committing to a formal corporate structure.

How to Choose the Right Entity Type in New Caledonia

Choosing the right business entity in New Caledonia determines your tax exposure, liability profile, and long-term compliance obligations — not just your registration costs.

Why Your Entity Choice Matters

The structure you register has binding legal consequences that are difficult and costly to reverse.

- Registering a branch or representative office when your firm intends to trade locally may place you in breach of applicable commercial law, exposing you to penalties or forced dissolution.

- Selecting an entity structure that cannot access France's treaty network — relevant given New Caledonia's fiscal relationship with the French state — may prevent you from claiming withholding tax reductions on cross-border payments.

- Forming a multi-shareholder company such as an SA when your business is a single-person consultancy generates annual audit and governance obligations that add material cost without proportionate benefit.

- Choosing a structure without the capacity to demonstrate genuine local activity, where substance indicators are examined, can trigger reporting failures and regulatory scrutiny by the Direction des Affaires Économiques (DAE).

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors each point toward a different structure under New Caledonian commercial law.

- Ownership and Management: Single-owner operations suit the EURL, while multi-party ventures with board requirements are better served by the SA or SAS framework.

- Tax Objectives: Your need for a specific provincial tax regime or access to broader fiscal arrangements should guide the entity form before registration.

- Substance Capacity: If you cannot realistically maintain staff and decision-making locally, choose a structure with lower or no substance thresholds.

- Privacy Requirements: Public disclosure of directors and shareholders varies by entity type; nominee arrangements are permissible under certain structures but must comply with beneficial ownership reporting rules.

- Exit Strategy: Not all entity types permit redomiciliation or conversion — confirm your intended exit path is legally available before incorporating.

New Caledonia's commercial entity framework is governed by locally adapted provisions of the French Code de Commerce, the full text of which is accessible through the Journal Officiel de la Nouvelle-Calédonie.

Corporate Compliance Services in New Caledonia

Maintain your entity's standing with ongoing compliance support covering reporting, renewals, and regulatory filings in New Caledonia.

Conclusion

This company incorporation New Caledonia guide has covered the full range of legal structures available under the territory's French-derived commercial framework. Each entity serves a distinct function: the SA suits large enterprises requiring capital market access; the SAS offers governance flexibility for structured investments; the SARL remains the most widely registered form for small and medium-sized businesses; and the EURL provides single-shareholder liability protection. Partnerships accommodate specific risk-sharing arrangements, while branch and representative offices serve foreign firms testing the market.

Regulated under the local commercial code administered through the Tribunal Mixte de Commerce, New Caledonia's corporate registry continues to align with French metropolitan standards. Your choice of structure will determine tax treatment, liability exposure, and administrative obligations for the life of your business.

How Expanship Can Assist You

Expanship company formation New Caledonia services are built around the specific requirements of the territory's legal framework, which operates under French civil law adapted through local congres legislation. From registering a SARL with the Tribunal Mixte de Commerce de Nouméa to filing the statuts constitutifs for a SAS or SA, every structure discussed in this blog comes with distinct obligations that require accurate, jurisdiction-specific handling.

Here is what Expanship supports you with directly:

- Document preparation and notarization for all entity types

- Registered agent and registered office provision in New Caledonia

- Government filing and liaison with the Tribunal Mixte de Commerce

- Post-incorporation compliance management, including annual reporting

- Banking introduction assistance for newly incorporated entities

- Legalization and apostille of corporate documents where required

Get in touch with our team through Expanship New Caledonia to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The SARL is the most frequently registered entity, largely because it combines limited liability protection with a relatively straightforward formation process and no minimum share capital requirement. Its governance structure suits small to medium-sized businesses operated by a defined group of associates.

A Branch Office has no separate legal personality and its parent company bears full liability for its operations, whereas a SARL is a distinct legal entity with liability confined to contributed capital. Tax treatment also differs: a branch is taxed only on locally sourced profits, while a SARL is subject to corporate tax on all territorial income under New Caledonian fiscal rules.

Among locally registered structures, the SAS offers comparatively greater flexibility in restricting the disclosure of shareholder information through its bylaws. Beneficial ownership details are not comprehensively published in a central public register under the current New Caledonian framework. Nominee arrangements are legally permissible but remain subject to applicable anti-money laundering obligations.

No. The SA requires a minimum of seven shareholders, and the SNC requires at least two partners with unlimited joint liability. By contrast, the SARL, SAS, and EURL can each be formed by a single individual, with the EURL being specifically designed for sole ownership.

Foreign nationals may form or hold shares in an SA, SAS, SARL, or EURL without a residency requirement, though certain regulated sectors may impose additional conditions. Establishing a Branch Office requires the parent company to be registered in a recognised jurisdiction and to appoint a local representative. Professional activities subject to licensing under New Caledonian provincial authority rules may carry separate approval processes.

Conversion between entity types is permitted under the legal framework applicable in New Caledonia, which broadly follows French company law principles. A SARL may be converted into an SA or SAS provided the relevant statutory conditions, including minimum shareholder thresholds and capital requirements, are satisfied. The conversion must be formally approved and registered with the Registry of Commerce and Companies (RIDET).

Not all of them. The SARL, SA, SAS, EURL, SCA, and SNC each hold separate legal personality upon registration. A Representative Office and Liaison Office do not constitute independent legal entities and cannot enter into contracts or generate revenue in their own name.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.