Key Takeaways

- The Private Limited Company is the most commonly registered entity type in the Maldives, offering limited liability without the public disclosure requirements attached to listed structures.

- Company formation in the Maldives is governed by the Companies Act 1/2014 and administered by the Registrar of Companies under the Ministry of Economic Development.

- Branch offices and representative offices serve distinct purposes for multinational firms, with each carrying specific operational or liaison mandates under Maldivian regulatory requirements.

- Compliance obligations in the Maldives are increasing, with the Maldives Inland Revenue Authority expanding enforcement and tightening beneficial ownership reporting requirements across all entity types.

Introduction to Entity Types in Maldives

The Maldives is an archipelagic nation in the Indian Ocean, situated southwest of Sri Lanka and India, comprising over 1,000 coral islands grouped into 26 natural atolls. It is an independent republic, and company formation is governed by the Registrar of Companies, operating under the Ministry of Economic Development. Business registration and ongoing compliance requirements are administered through this authority in accordance with the Companies Act of the Maldives.

The tax posture is generally low, with no personal income tax and a limited corporate tax framework applicable primarily to larger businesses and banking institutions.

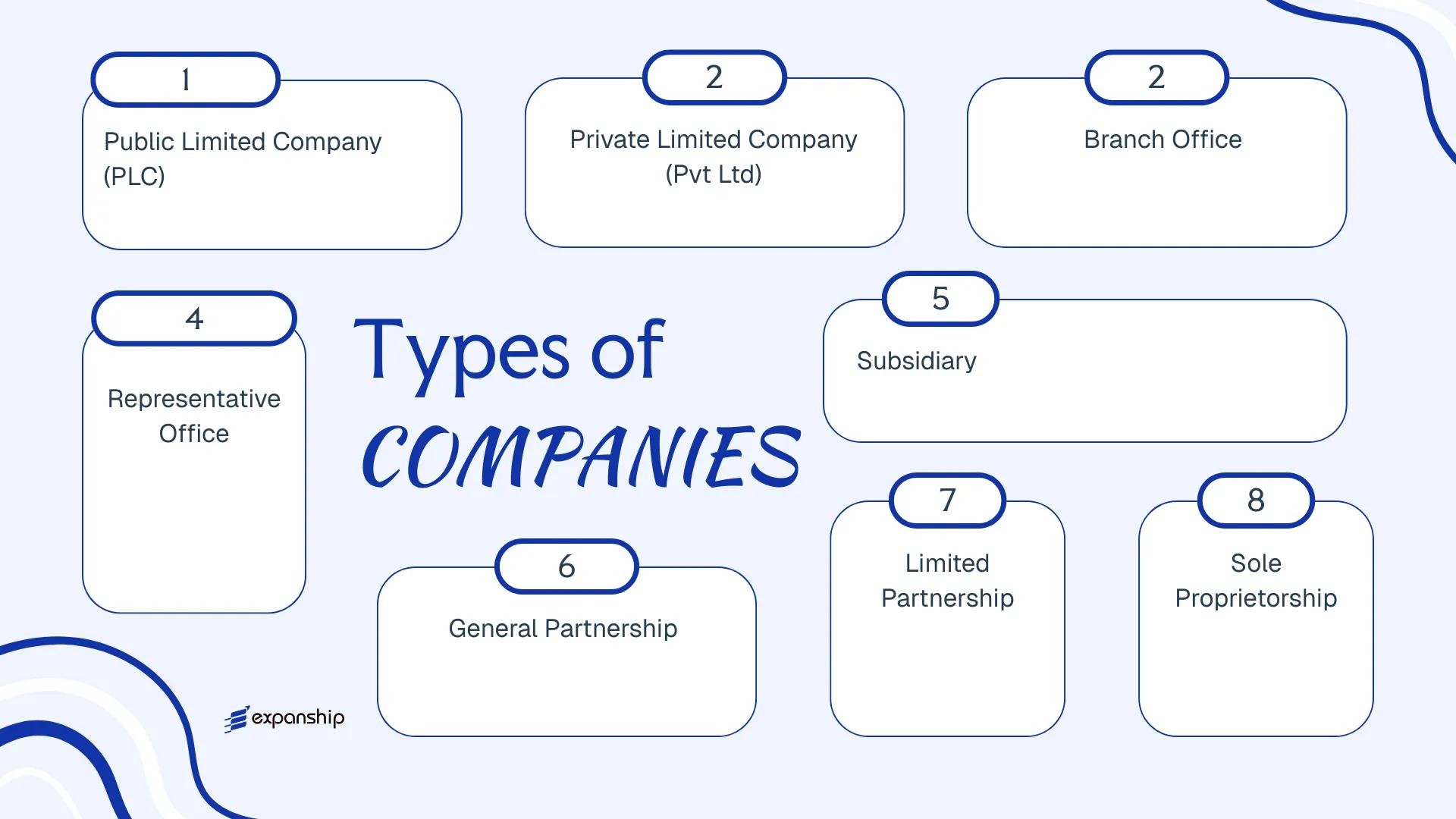

Understanding the types of business entities in Maldives is essential before committing to a structure, as each carries distinct requirements around ownership, liability, and regulatory obligations. The entity options available include the Public Limited Company, Private Limited Company, Branch Office, Representative Office, Subsidiary, General Partnership, Limited Partnership, and Sole Proprietorship. This article examines each structure — covering formation requirements, ownership rules, and compliance obligations — to give your business a factual basis for making that decision.

An Overview of Business Structures in Maldives

The business structures available in Maldives are governed primarily by the Companies Act of the Maldives (Law No. 10/96), along with supplementary regulations administered by the Ministry of Economic Development. Several distinct entity types exist under this framework, each designed to serve a different commercial purpose — from domestic trading operations to foreign market entry.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (PLC) | Incorporated company | Limited | Taxed | Yes | 7 shareholders | Ministry of Economic Development | Companies Act (10/96) |

| Private Limited Company (Pvt Ltd) | Incorporated company | Limited | Taxed | Yes | 2 shareholders | Ministry of Economic Development | Companies Act (10/96) |

| Branch Office | Extension of foreign entity | Unlimited (parent liable) | Taxed | Restricted | 1 parent entity | Ministry of Economic Development | Companies Act (10/96) |

| Representative Office | Non-trading presence | Unlimited (parent liable) | Exempt | No | 1 parent entity | Ministry of Economic Development | Companies Act (10/96) |

| Subsidiary | Incorporated company | Limited | Taxed | Yes | 1 shareholder | Ministry of Economic Development | Companies Act (10/96) |

| General Partnership | Unincorporated firm | Unlimited | Taxed | Yes | 2 partners | Ministry of Economic Development | Partnership law |

| Limited Partnership | Unincorporated firm | Mixed | Taxed | Yes | 2 partners | Ministry of Economic Development | Partnership law |

| Sole Proprietorship | Unincorporated individual | Unlimited | Taxed | Yes | 1 owner | Ministry of Economic Development | Business registration regulations |

Each of these structures is examined in full in the sections below.

Public Limited Company (PLC) under the Maldives Companies Act

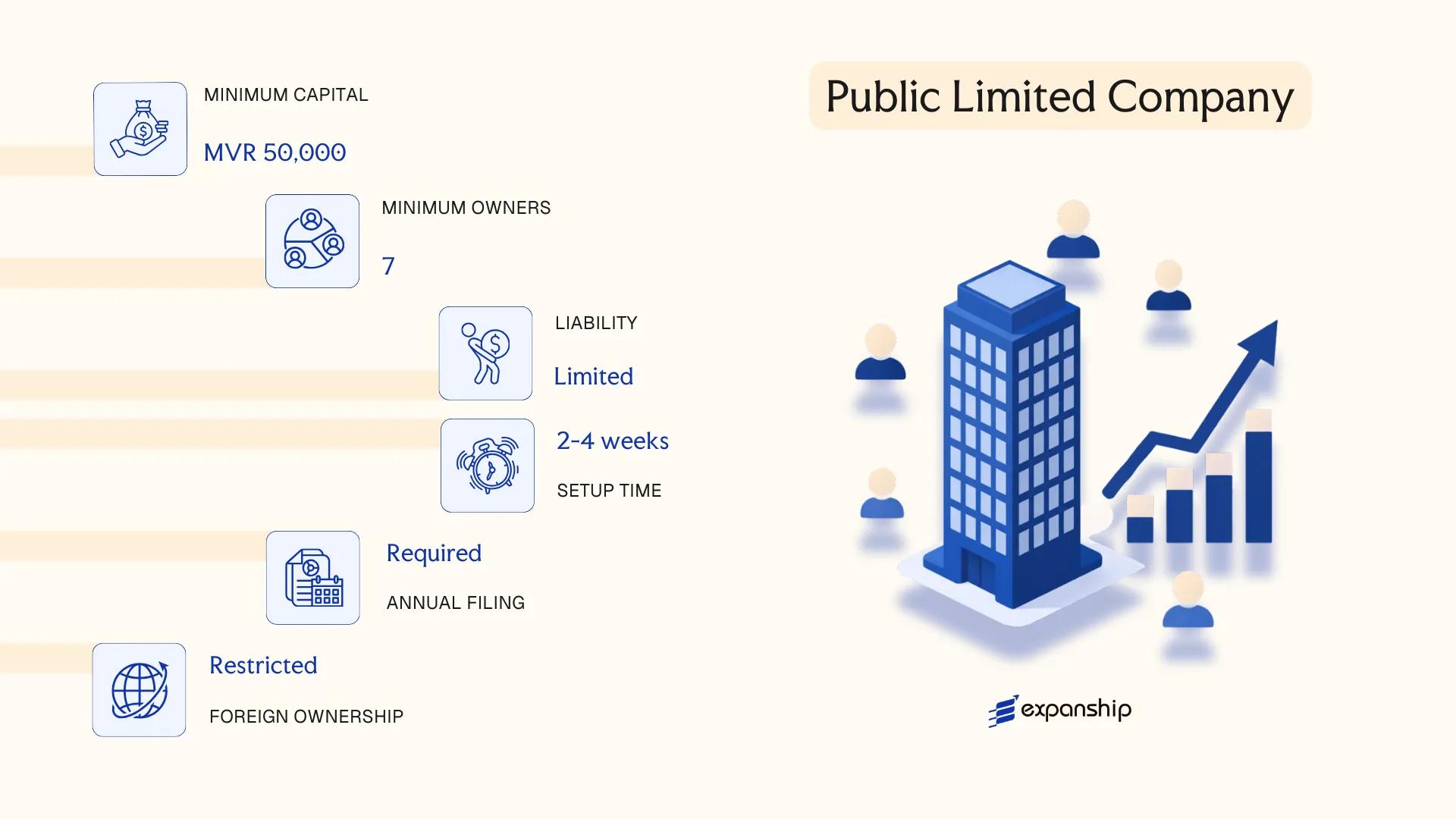

Maldives Public Limited Company registration is governed by the Companies Act (Law No. 10/96), the primary legislation regulating corporate entities in the jurisdiction. A PLC carries separate legal personality, meaning the company exists as a distinct legal entity from its shareholders, and liability is limited to the amount unpaid on shares.

Shares in a PLC can be offered to the public, distinguishing it structurally from its private counterpart. The Maldives Capital Market Development Authority (CMDA) oversees public offerings and securities-related obligations for listed entities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (PLC) | Separate legal personality; limited liability by shares |

| Members | Shareholders (min. 2, no statutory maximum) | Directors: minimum 3; a director may also be a shareholder |

| Local Presence | Registered office in Maldives | Must maintain a physical registered address; no mandatory resident director requirement confirmed under general statute |

| Capital | MVR denomination; no prescribed statutory minimum for all PLCs | Listed PLCs must meet CMDA capital thresholds for public offerings |

| Privacy | Shareholder and director information filed with the Registrar of Companies | Information is generally accessible through official filings |

Focus Points

- Taxation: Corporate income tax applies under the Business Profit Tax Act; standard BPT rate is 15%; no general VAT on most financial instruments, though GST applies to tourism and certain sectors; no withholding tax on dividends under current statute.

- Economic Substance: No formal economic substance regime equivalent to offshore financial centre standards, but operational presence may be required for certain regulated activities.

- Annual Compliance: Annual returns and audited financial statements must be filed with the Registrar of Companies; listed PLCs have additional CMDA disclosure obligations.

- Restrictions: Foreign ownership restrictions apply in specific sectors, including land ownership and certain licensed industries.

- Conversion: A PLC may be converted to a private limited company subject to shareholder approval and Registrar consent under the Companies Act.

Closing

A PLC structure suits larger enterprises seeking public capital through share issuance, including firms targeting a stock exchange listing on the Maldives Stock Exchange. The ability to raise funds publicly is the principal advantage; the corresponding limitation is the heightened regulatory and disclosure burden imposed by both the Companies Act and CMDA.

PLCs are most appropriate for large-scale commercial or financial enterprises intending to access public equity markets or institutional investors.

Company Incorporation in Maldives

Incorporate a public or private limited company in Maldives with end-to-end support from entity selection through to regulatory registration.

Private Limited Company (Pvt Ltd) under the Maldives Companies Act

The Private Limited Company is the most widely used structure for Maldives Private Limited Company setup, offering a combination of limited liability and operational flexibility under a single legislative framework. Governed by the Companies Act 2019 (Law No. 18/2019), administered by the Maldives Economic Development Authority (EDA), this entity holds a separate legal personality distinct from its shareholders, meaning the company can own assets, enter contracts, and incur liabilities in its own name.

Pvt Ltd registration Maldives requires at least one shareholder, with a defined ceiling on the total number of members. Foreign ownership is permitted, though certain sectors restrict or cap foreign equity participation under the Foreign Investment Act.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company (Pvt Ltd) | Separate legal personality; liability limited to unpaid share capital |

| Members | Shareholders: min. 1, max. 50 | Corporate shareholders permitted; public subscription prohibited |

| Directors | Min. 1 director required | No mandatory residency requirement for directors |

| Local Presence | Registered office address in Maldives required | Must be maintained with the EDA throughout the company's life |

| Share Capital | Denominated in MVR; no statutory minimum for local companies | Foreign-invested companies may face sector-specific capital thresholds |

| Privacy | Shareholder and director details filed with EDA | No public beneficial ownership register currently mandated |

Focus Points

- Taxation: Subject to Business Profit Tax (BPT) at 15% on net profits above MVR 500,000; a 25% corporate tax rate applies to large businesses; no general VAT obligation unless turnover exceeds the GST/T-GST registration threshold; withholding tax applies to certain payments to non-residents.

- Economic Substance: No formal economic substance regime currently enacted, though sector-specific licensing may impose operational presence requirements.

- Annual Compliance: Annual financial statements and an annual return must be filed with the EDA; audit requirements depend on company size and sector.

- Treaty Access: Maldives has a limited double tax treaty network; access to treaty benefits is not a primary driver for this structure.

- Conversion: A Pvt Ltd may convert to a Public Limited Company upon satisfying the membership and disclosure requirements under the Companies Act 2019.

Closing

The Pvt Ltd structure suits trading operations, joint ventures, and sector-specific businesses where foreign equity is permitted, with limited liability as its principal structural advantage. Its restriction on public share subscription limits capital-raising options for growth-stage businesses requiring broad investor access.

This structure fits small to mid-sized businesses, foreign-invested joint ventures, and sector-licensed operators seeking legal separation between personal and business assets.

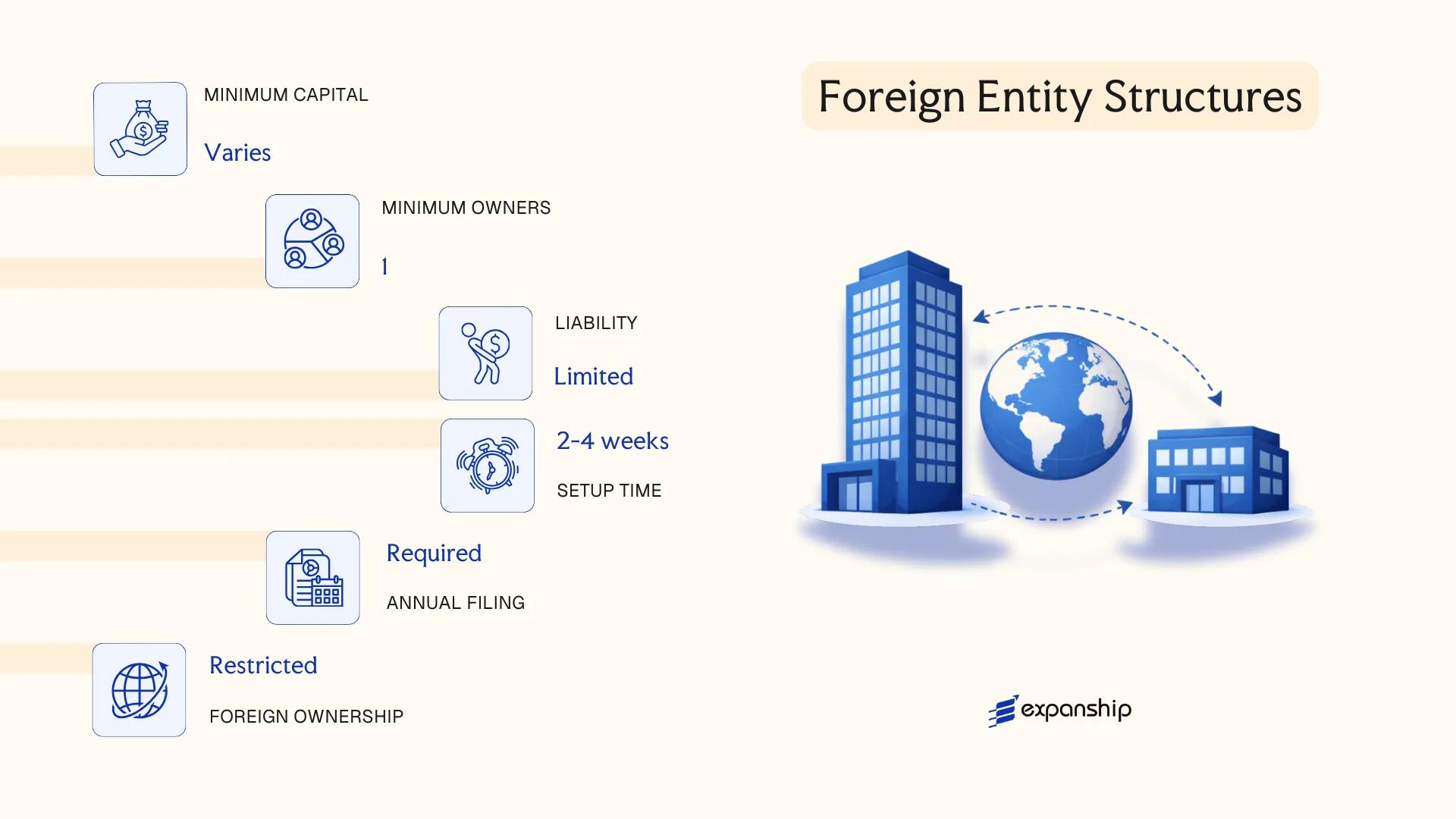

Foreign Entity Structures in Maldives [Branch Office, Representative Office, Subsidiary]

Foreign businesses entering the Maldivian market operate under the Companies Act (Law No. 10/96) and must register with the Registrar of Companies under the Ministry of Economic Development. Establishing a foreign company branch office Maldives requires specific approval from this authority, and certain sectors additionally require clearance from the Maldives Investment Promotion Authority (MIPA) or relevant line ministries.

Foreign ownership rules in the Maldives are sector-dependent. Some industries mandate a local Maldivian partner holding a minimum equity stake, while others permit 100% foreign ownership subject to investment thresholds.

Key Characteristics

| Requirement | Branch Office | Representative Office | Foreign Subsidiary |

|---|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; limited operational scope | Separate legal entity (Private Limited Company) incorporated locally |

| Liability | Parent company bears full liability | Parent company bears full liability | Limited to subsidiary's own capital |

| Permitted Activities | Commercial operations within approved scope | Liaison, market research, promotion only | Full commercial operations |

| Local Presence | Registered local address required | Registered local address required | Registered office in Maldives required |

| Capital | No statutory minimum, but investment thresholds may apply by sector | No statutory minimum | Subject to Pvt Ltd minimum capital rules |

| Privacy | Parent company details disclosed on registration | Parent company details disclosed | Directors and shareholders on public record |

Focus Points

- Taxation: Branch profits are subject to Business Profit Tax (BPT) at 15%; GST applies to taxable supplies; no withholding tax on dividends currently exists under Maldivian law, though the general tax framework applies equally to foreign entities.

- Economic Substance: No formal economic substance regime has been enacted to date; sector-specific operational requirements may apply under investment agreements.

- Annual Compliance: All registered foreign entities must file annual returns and audited financial statements with the Registrar of Companies.

- Restrictions: Representative offices are prohibited from revenue-generating activities; foreign ownership caps apply in tourism, fishing, and certain retail sectors.

- Conversion: A branch can typically be converted to a subsidiary structure, though this requires a fresh incorporation process rather than a direct administrative conversion.

Sub-Types

Branch Office

A branch is a direct extension of the foreign parent and conducts revenue-generating business under the parent's name. It carries no separate legal identity, meaning contractual and financial obligations flow back to the parent entity.

Representative Office

Representative office setup in Maldives is restricted to non-commercial functions such as liaison work, sourcing, and promotional activities. It cannot sign commercial contracts or invoice local clients on its own account.

Foreign Subsidiary

Foreign subsidiary registration in Maldives results in a locally incorporated Private Limited Company with its own legal personality, separate from the foreign parent. This structure is generally used when full operational capacity and limited liability protection are required simultaneously.

Foreign entity structures suit businesses entering the Maldives for tourism-linked services, trade, or regional coordination, with the subsidiary offering the clearest liability separation and the branch providing a faster route to operational activity. The principal limitation across all three structures is sector-specific foreign ownership restrictions, which can constrain equity control.

Foreign subsidiaries are best suited for businesses requiring full operational control and liability separation; branch offices suit those seeking a faster market entry with direct parent accountability.

Partnership Structures in Maldives [General Partnership, Limited Partnership]

Partnership registration in Maldives is governed by the Partnership Act of the Maldives, which provides the framework for both general and limited partnership formations. Neither structure carries separate legal personality distinct from its partners, meaning partners bear direct exposure to the obligations of the business.

Partnerships are relatively uncommon among foreign investors compared to corporate structures, but they remain a recognised option for certain professional arrangements and joint ventures among Maldivian nationals or qualifying foreign participants.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business association | No separate legal personality from partners |

| Members | Partners (minimum 2, no statutory maximum) | Designated as general partners or limited partners depending on structure |

| Local Presence | Registered address in Maldives required | Business registration through the Ministry of Economic Development |

| Capital | No statutory minimum; MVR denominated | Capital contributions defined by partnership agreement |

| Liability | Unlimited for general partners; capped for limited partners | Limited partners restricted from active management |

| Privacy | Partnership agreements are not publicly filed in full | Basic registration details are publicly recorded |

Focus Points

- Taxation: Partnerships are generally treated as pass-through entities for income tax purposes; individual partners are taxed on their share of profits under the Maldives Income Tax Act, with no separate corporate tax at the entity level. No GST or withholding tax obligations typically arise at the partnership level on domestic profit distributions.

- Annual Compliance: Partnerships must renew their business registration annually with the Ministry of Economic Development and maintain basic financial records.

- Foreign Participation: Foreign nationals face restrictions on forming local partnerships in certain sectors; sector-specific approvals may be required.

- Conversion: Converting a partnership to a private limited company is possible but requires a formal restructuring process and fresh incorporation filings.

- Treaty Access: Partnerships generally do not qualify as residents for purposes of Maldives tax treaty benefits, as treaty access is typically limited to corporate taxpayers.

Sub-Types

General Partnership

All partners share equal management authority and bear joint and several liability for partnership debts. This structure is typically used by small professional firms or co-owned trading businesses where partners are closely involved in day-to-day operations.

Limited Partnership

At least one general partner assumes unlimited liability while limited partners contribute capital and enjoy liability capped at their investment. Limited partners must not participate in management; doing so risks losing their liability protection under the Partnership Act.

Who Should Consider This Structure

Partnerships suit arrangements where two or more parties wish to operate jointly without the administrative requirements of a corporate structure, though unlimited liability for general partners represents a significant constraint for commercial ventures.

Partnership structures in Maldives are best suited to small-scale professional collaborations or joint ventures among Maldivian nationals where the parties have an existing trust relationship and limited external liability exposure.

Sole Proprietorship in Maldives

Sole proprietorship registration in Maldives is governed under the Business Registration Act (Law No. 18/2014), administered by the Ministry of Economic Development. This structure carries no separate legal personality — the business and its owner are treated as a single legal entity, meaning personal assets are exposed to business liabilities.

Registration is straightforward but limited by its nature. Only Maldivian nationals are eligible to register as sole traders; foreign individuals cannot operate under this structure directly.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated individual business | No separate legal personality from the owner |

| Members | Single proprietor | Must be a Maldivian national; no minimum capital requirement |

| Local Presence | Registered business address required | Must maintain a physical address in the Maldives |

| Capital | MVR; no statutory minimum | Proprietor funds the business entirely from personal resources |

| Liability | Unlimited personal liability | Owner is personally liable for all debts and obligations |

| Privacy | Owner's name tied to the business registration | Limited privacy; details are publicly accessible through MIRA |

Focus Points

- Taxation: Subject to Business Profit Tax (BPT) if annual turnover exceeds the applicable threshold; GST registration required once turnover crosses the prescribed limit; no corporate tax distinction applies given the absence of separate legal personality.

- Annual Compliance: Annual renewal of business registration with the Ministry of Economic Development is required.

- Restrictions: Foreign nationals are ineligible; the structure cannot issue shares or admit partners.

- Conversion: Can be converted into a private limited company if the business grows beyond the sole trader format.

- Treaty Access: No access to double tax treaty benefits applicable to corporate entities.

Closing

A sole proprietorship suits small-scale, locally operated businesses where simplicity of administration outweighs the need for liability protection. The primary advantage is low setup cost and minimal ongoing compliance; the key drawback is unlimited personal liability, which exposes the proprietor's personal assets entirely.

This structure is suited to Maldivian nationals operating small, single-owner businesses with limited financial exposure and no plans for external investment or growth-stage scaling.

How to Choose the Right Entity Type in Maldives

Choosing the right company structure in Maldives determines your legal exposure, tax position, and operational capacity before your business earns a single dollar.

Why Your Entity Choice Matters

The structure you register has binding legal consequences that are difficult and costly to unwind.

- Registering a foreign branch to conduct local trade when the activity requires a locally incorporated entity places the firm in breach of the Companies Act 2021 (Law Number 1/2021), which can result in deregistration or financial penalties.

- Selecting a structure without reviewing its eligibility under applicable tax arrangements may prevent your business from accessing withholding tax relief in counterpart jurisdictions.

- Forming a private limited company when your purpose is asset holding or succession planning locks your estate into annual shareholder obligations, director filings, and audit thresholds that a trust or similar instrument would not carry.

- Choosing an entity that mandates audited financial statements for a single-operator consultancy introduces recurring professional fees with no corresponding compliance benefit.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each require distinct structures under Maldivian law.

- Ownership Configuration: A sole founder operating locally has different structural needs than a multi-party joint venture requiring defined governance arrangements.

- Tax Objectives: Your need for full exemption, a specific rate, or treaty eligibility should be confirmed against the Business Profit Tax Act before entity selection.

- Substance Capacity: If you cannot maintain local staff or a physical office, confirm whether your chosen structure carries substance obligations that you cannot satisfy.

- Exit and Conversion: Confirm in advance whether the structure permits redomiciliation, conversion, or voluntary winding-up under the Companies Act 2021.

- Public Disclosure Tolerance: The Registrar of Companies maintains a public register; if director or shareholder privacy is a priority, review what nominee arrangements are permissible.

Corporate Compliance Services for Companies in the Maldives

Maintain statutory filings, annual returns, and regulatory obligations for your Maldivian entity.

Conclusion

Selecting the right structure is one of the more consequential early decisions in any Maldives company incorporation guide summary, since the choice shapes tax exposure, ownership flexibility, and ongoing compliance obligations under the Companies Act 1/2014 and the oversight of the Maldives Inland Revenue Authority. Private Limited Companies account for the majority of registrations and suit resident and foreign investors who want limited liability without the disclosure requirements of a listed entity. The Public Limited Company structure is reserved for firms seeking public capital markets access. Branch and representative offices serve multinational firms with specific operational or liaison mandates, while partnerships and sole proprietorships remain practical for smaller domestic ventures.

Regulatory direction in the Maldives has trended toward greater formalization, with expanded MIRA enforcement and tighter beneficial ownership reporting obligations shaping what starting a company in Maldives overview documents need to address. Matching your entity to that trajectory from the outset reduces remediation risk later. Expanship's jurisdiction-specific experience can support that process directly.

How Expanship Can Assist You

Expanship company formation services Maldives cover the full incorporation process — from selecting the right entity type under the Maldives Companies Act 1996 to filing with the Registrar of Companies at the Ministry of Economic Development. Your specific circumstances determine whether a Private Limited Company, Branch Office, or another structure best suits your goals, and that determination shapes every step that follows.

Expanship handles both the formation process and the obligations that come after registration.

- Document preparation and notarization

- Registered agent and local office provision

- Filing and liaison with the Registrar of Companies

- Post-incorporation compliance management, including annual returns

- Banking introduction assistance for corporate account opening

- Ongoing corporate secretarial support

Get in touch with Expanship Maldives to discuss your incorporation requirements directly.

Frequently Asked Questions (FAQ)

The Private Limited Company (Pvt Ltd) is the most frequently registered structure. Its combination of limited liability protection, a relatively straightforward incorporation process, and suitability for both resident and foreign-owned businesses makes it the default choice for most commercial ventures.

A Branch Office is not a separate legal entity; it remains an extension of its foreign parent and carries the parent's full liability. A Private Limited Company, by contrast, holds independent legal personality, files its own accounts, and can own assets in its own name. From a compliance standpoint, a locally incorporated Pvt Ltd generally faces more ongoing obligations than a Branch.

Among registered entities, details of directors and shareholders of a Private Limited Company are held on file with the Registrar, but public disclosure practices vary. Nominee arrangements are permissible in principle, though any nominee relationship must remain consistent with the Anti-Money Laundering Act (Act No. 14/2014) requirements.

A sole proprietorship and a Private Limited Company can each be formed by one person. Partnership structures, whether general or limited, require a minimum of two partners by definition. A Public Limited Company requires a higher minimum shareholder threshold.

Foreign investors may register a Private Limited Company, establish a Branch Office, or set up a Representative Office. Foreign ownership in certain sectors is subject to restrictions under the Foreign Investment Act and may require approval from the Maldives Investment Services Bureau (MIBA).

Conversion between entity types, such as from a Private Limited Company to a Public Limited Company, is contemplated under the Companies Act, subject to regulatory approval and satisfaction of the relevant capital and shareholder requirements. Re-registration procedures must be completed through the Registrar of Companies.

No. A sole proprietorship and a general partnership do not have legal personality distinct from their owner or partners. The Private Limited Company, Public Limited Company, and Limited Partnership each hold varying degrees of legal separateness, with incorporated companies enjoying full separate legal identity under the Companies Act.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.