Key Takeaways

- The Macao Commercial Registry (Conservatória do Registo Comercial e de Bens Móveis) serves as the primary authority for entity formation across all available business structures in the SAR.

- Macao's legal framework derives from Portuguese civil law and operates independently from mainland China's commercial legislation under the "one country, two systems" arrangement.

- The Sociedade por Quotas (Lda.) is the most commonly registered entity in Macao, favoured for its lower capital threshold and simplified governance structure under the Commercial Code.

- Branch offices and representative offices allow foreign entities to establish a legal presence in Macao without local incorporation, though each form carries defined restrictions on permissible activities.

Introduction to Entity Types in Macao

Macao is a Special Administrative Region (SAR) of China, situated on the western side of the Pearl River Delta, bordered by Guangdong province and across the water from Hong Kong. Governed under a "one country, two systems" framework, it maintains a distinct legal order based on Portuguese civil law — a legacy of its colonial administration — and operates independent commercial legislation from mainland China.

Understanding the types of business entities in Macao begins with the Macao Commercial Registry (Conservatória do Registo Comercial e de Bens Móveis), the authority responsible for company registration and maintenance of the commercial register. Separate regulatory oversight applies depending on the sector, but the Commercial Registry is the primary body for entity formation.

Macao applies a territorial tax system, meaning only income sourced within the SAR is subject to corporate profit tax.

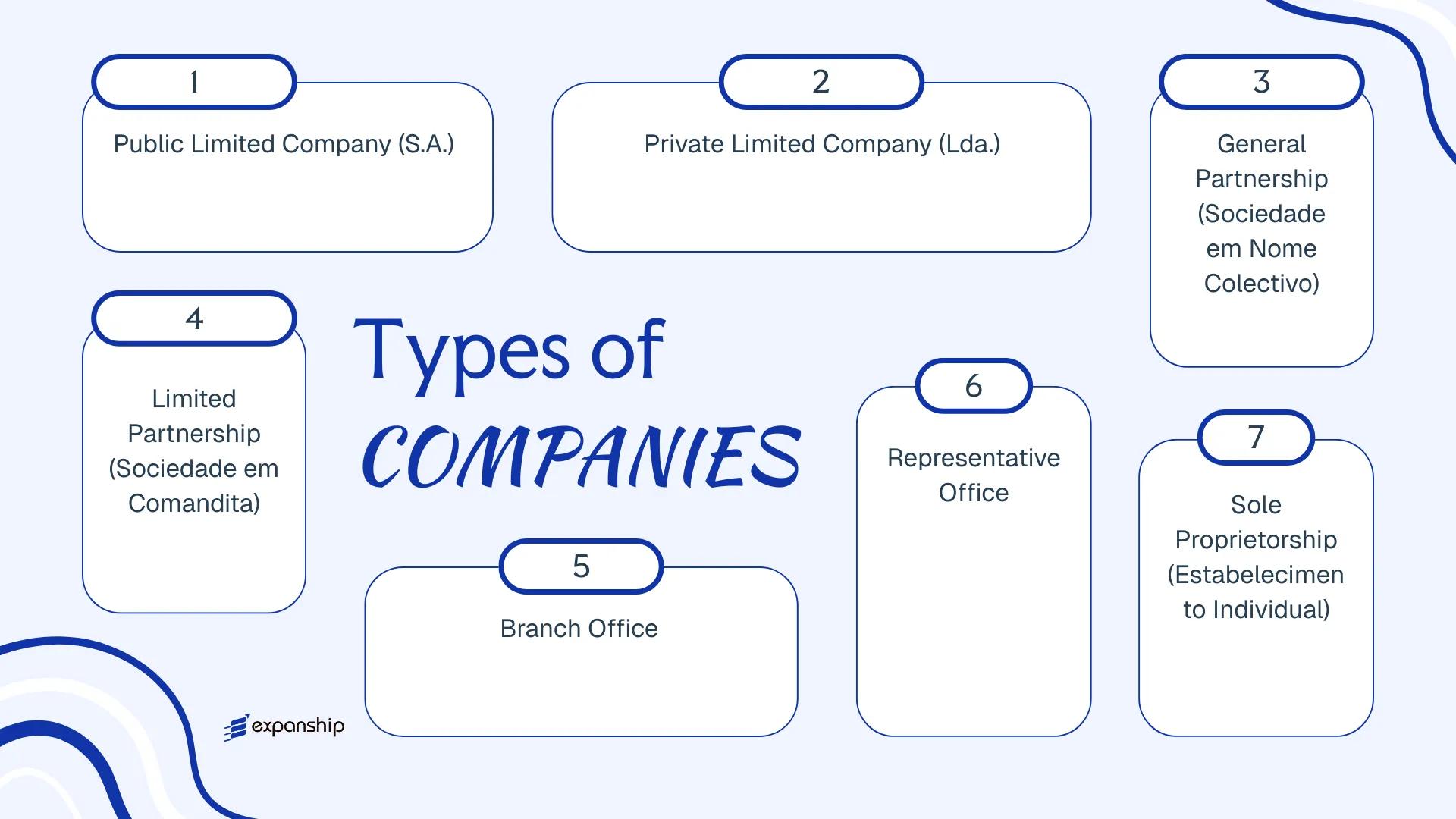

The legal forms available for business incorporation or establishment include: the Sociedade Anónima (S.A.), the Sociedade por Quotas (Lda.), the Sociedade em Nome Colectivo, the Sociedade em Comandita, the Branch Office, the Representative Office, and the Estabelecimento Individual. Each structure carries distinct requirements regarding liability, capital, and governance — all of which are examined in detail throughout this article.

An Overview of Business Structures in Macao

Macao's company law framework provides several distinct business structures available in Macao, each governed primarily by the Commercial Code (Código Comercial) of Macao SAR. Registration and ongoing compliance fall under the oversight of the Macao SAR government's business registry, the Conservatória do Registo Comercial e de Bens Móveis. Each structure carries different implications for liability, ownership, and operational scope.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (S.A.) | Corporate entity | Limited to share capital | Taxable (Complementary Tax) | Yes | 3 shareholders | Conservatória do Registo Comercial | Commercial Code |

| Private Limited Company (Lda.) | Corporate entity | Limited to quota value | Taxable (Complementary Tax) | Yes | 1 member | Conservatória do Registo Comercial | Commercial Code |

| General Partnership | Unincorporated | Unlimited, joint | Taxable | Yes | 2 partners | Conservatória do Registo Comercial | Commercial Code |

| Limited Partnership | Unincorporated | Mixed (general/limited) | Taxable | Yes | 2 partners | Conservatória do Registo Comercial | Commercial Code |

| Branch Office | Extension of foreign entity | Parent bears liability | Taxable on local income | Yes | N/A | Conservatória do Registo Comercial | Commercial Code |

| Representative Office | Non-trading presence | Parent bears liability | Generally exempt | No | N/A | Macao SAR Government | Commercial Code |

| Sole Proprietorship | Individual trader | Unlimited, personal | Taxable (Complementary Tax) | Yes | 1 individual | Conservatória do Registo Comercial | Commercial Code |

Each of these structures is examined in full in the sections below.

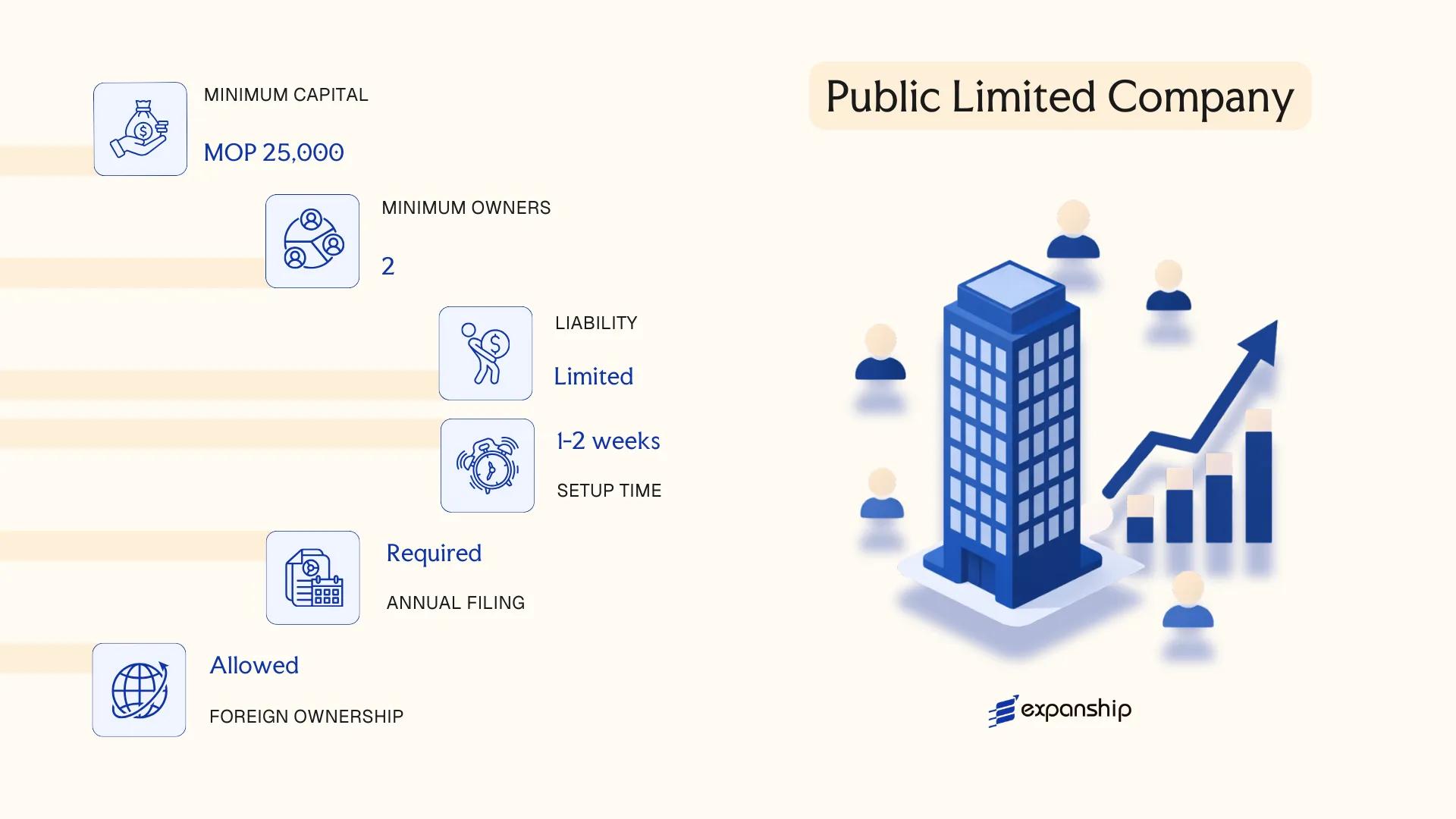

Public Limited Company (Sociedade Anónima, S.A.)

Macao Sociedade Anónima SA formation is governed by the Commercial Code of Macao (Decreto-Lei n.º 40/99/M), which provides the statutory framework for this share-capital based entity. The S.A. carries full separate legal personality, meaning creditors have recourse only against company assets, and shareholders bear no personal liability beyond their subscribed capital.

Shares in an S.A. are freely transferable by default, which distinguishes its capital structure from the quota-based private limited company. This transferability makes the form particularly relevant for businesses anticipating external investment or eventual public listing on a recognised exchange.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedade Anónima (S.A.) | Share capital company with separate legal personality |

| Governance | Board of Directors (minimum 3) + Supervisory Board or Statutory Auditor | Single-director structure not permitted |

| Shareholders | Minimum 5; no statutory maximum | Shareholders may be natural persons or legal entities, resident or non-resident |

| Local Presence | Registered office in Macao SAR required | No mandatory local director requirement under general law |

| Share Capital | MOP 500,000 minimum; divided into shares with a nominal value | Shares may be registered or bearer (subject to applicable restrictions) |

| Privacy | Shareholder register maintained internally; directors disclosed in public filings with the Conservatória do Registo Comercial | Beneficial ownership rules apply under AML legislation |

Focus Points

- Taxation: Subject to Macao's Complementary Tax (corporate income tax) at a progressive rate up to 12% on assessable profits; no VAT, no withholding tax on dividends distributed to non-residents under general domestic law, and stamp duty applies to specific instruments.

- Annual Compliance: Annual accounts must be prepared, audited, and filed; an audit is mandatory regardless of size for S.A. entities.

- Economic Substance: No formal economic substance regime comparable to certain offshore jurisdictions; standard registered office and local filing obligations apply.

- Treaty Access: Macao has a limited tax treaty network; treaty benefits are available under concluded agreements, primarily with mainland China and Portugal.

- Conversion: An S.A. may be converted into a Sociedade por Quotas subject to shareholder resolution and compliance with the Commercial Code's conversion procedures.

Closing

The S.A. structure is used for larger trading operations, joint ventures requiring multiple institutional shareholders, and businesses seeking a governance framework suited to external capital participation. Its mandatory supervisory requirements add administrative overhead that smaller operations may find disproportionate.

Best suited for businesses with five or more shareholders, institutional investors, or ventures planning to raise capital through share issuance.

Company Incorporation in Macao

Incorporate a Sociedade Anónima or other entity type in Macao SAR with end-to-end support from Expanship's corporate specialists.

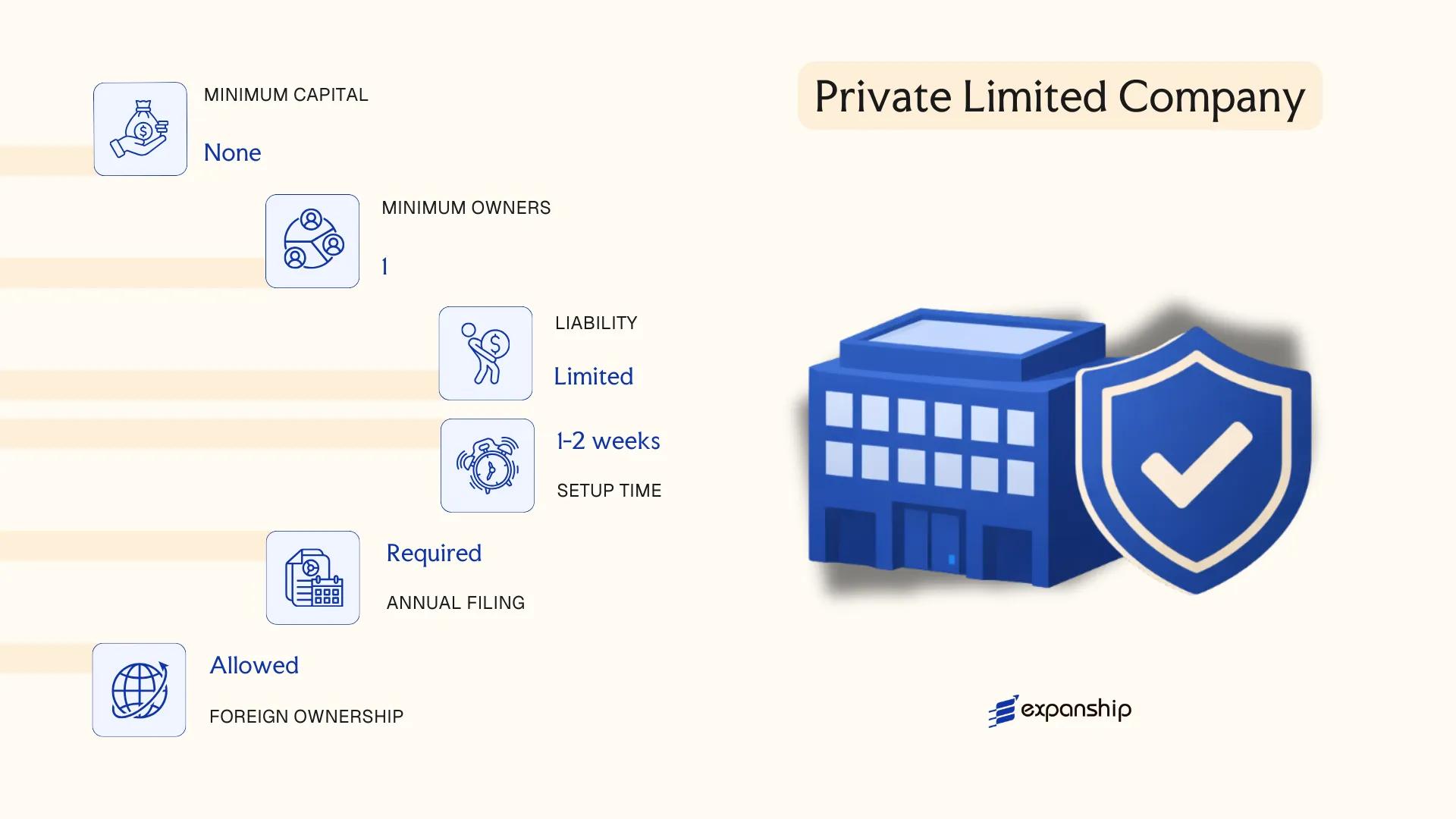

Private Limited Company (Sociedade por Quotas, Lda.)

The Sociedade por Quotas, Lda. is the most widely used corporate structure for Macao Sociedade por Quotas Lda registration, governed primarily by the Macao Commercial Code (Código Comercial). It carries separate legal personality, meaning the company's obligations are distinct from those of its members. Liability is limited to each member's subscribed quota, making it structurally comparable to a limited liability company in common-law jurisdictions.

Quotas — rather than shares — represent ownership interests. These are not freely transferable without the consent of other members, which distinguishes this private limited company Macao structure from publicly traded forms and gives founding members meaningful control over ownership succession.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company (Lda.) | Quota-based ownership; not share-based |

| Members | Referred to as quotistas (quota holders); minimum 1, maximum no statutory cap | Single-member Lda. is permitted |

| Management | One or more gerentes (managers); no board requirement for smaller firms | Managers may be non-members |

| Local Presence | Registered office address in Macao SAR required | Registered agent not mandatorily prescribed by statute |

| Capital | MOP 25,000 minimum paid-up capital; denominated in Macanese Pataca (MOP) | No par value requirement per quota |

| Privacy | Member details filed with the Financial Services Bureau (DSF); not publicly searchable in a central online registry | Beneficial ownership obligations apply |

Focus Points

- Taxation: Subject to Macao's Complementary Tax (Imposto Complementar de Rendimentos) at a progressive rate up to 12% on profits; no VAT regime; dividends generally not subject to withholding tax; stamp duty applies to certain instruments.

- Annual Compliance: Annual accounts must be prepared and submitted to the DSF; audit requirements depend on company size thresholds.

- Economic Substance: No formal substance legislation equivalent to certain offshore jurisdictions, but physical presence through a registered office is required.

- Treaty Access: Macao has a limited tax treaty network; treaty benefits should be assessed on a case-by-case basis.

- Quota Transfer Restrictions: Transfers to non-members require prior approval from existing quota holders unless the articles provide otherwise.

Closing

This structure suits Lda company formation Macao SAR for trading operations, holding local assets, or running professional services businesses where ownership control is a priority. Its simplified governance is an advantage; however, the restriction on quota transferability can constrain exit strategies for investors seeking liquidity.

Small-to-medium businesses, family-owned enterprises, and foreign investors seeking a controlled ownership structure with limited liability.

Partnerships in Macao [General Partnership (Sociedade em Nome Colectivo), Limited Partnership (Sociedade em Comandita)]

Partnership structures in Macao SAR are governed by the Commercial Code (Código Comercial), which traces its origins to the Portuguese legal tradition and remains the principal instrument regulating commercial associations. Two distinct forms exist: the Sociedade em Nome Colectivo (general partnership) and the Sociedade em Comandita (limited partnership). Neither structure is widely adopted for commercial activity today, as both carry characteristics that limit their appeal relative to quota-based companies.

Under Macao law, both partnership forms possess separate legal personality upon registration with the Conservatória do Registo Comercial e de Bens Móveis (CRCBM). General partnerships expose all partners to unlimited joint liability for the firm's obligations, while limited partnerships introduce a two-tier membership structure separating active management from passive investment.

Key Characteristics

| Requirement | General Partnership (S. em Nome Colectivo) | Limited Partnership (S. em Comandita) |

|---|---|---|

| Legal Form | Separate legal personality | Separate legal personality |

| Members | Partners (minimum 2; no statutory maximum) | General partners (min. 1, unlimited liability) + limited partners (min. 1, liability capped at contribution) |

| Local Presence | Registered office in Macao required | Registered office in Macao required |

| Minimum Capital | No statutory minimum prescribed | No statutory minimum prescribed |

| Liability | All partners bear unlimited personal liability | General partners: unlimited; limited partners: limited to capital contributed |

| Privacy | Partner names disclosed in the commercial register | Both partner classes disclosed publicly at CRCBM |

Focus Points

- Taxation: Partnerships are generally subject to Macao's Complementary Tax (Imposto Complementar de Rendimentos) on assessable profits, with a standard rate up to 12%; no VAT system applies, though stamp duty (Imposto do Selo) may arise on specific transactions and instruments.

- Annual Compliance: Filing of annual accounts with the CRCBM and submission of tax returns to the Direcção dos Serviços de Finanças (DSF) are required.

- Treaty Access: Macao has a limited tax treaty network; partnerships may not qualify for treaty benefits depending on how the counterpart jurisdiction classifies the entity.

- Conversion: Conversion to a Sociedade por Quotas is legally permissible but requires a formal restructuring process and re-registration.

- Restrictions: Limited partners in a Sociedade em Comandita may not participate in management without risking reclassification to unlimited liability status.

Sub-Types

General Partnership (Sociedade em Nome Colectivo)

All partners hold equal management rights and bear joint, unlimited liability for partnership debts. This structure is typically used by small professional groups or family businesses where all participants intend to be actively involved in operations.

Limited Partnership (Sociedade em Comandita)

Distinguishes between sócios comanditados (general partners) who manage the business and bear unlimited liability, and sócios comanditários (limited partners) who contribute capital and remain passive. A Sociedade em Comandita por Acções variant exists where limited partners hold transferable shares rather than fixed quota interests.

Closing

Both partnership forms are infrequently used for mainstream commercial or investment activity, given the availability of the Sociedade por Quotas which offers limited liability with comparable flexibility. The principal drawback of the general partnership remains the unlimited personal exposure of every partner to business liabilities.

These structures suit small, closely-held professional practices or family ventures where all active participants accept personal liability and formal capital structuring is not required.

Foreign Business Presence in Macao [Branch Office, Representative Office]

A foreign company branch office in Macao is not a separate legal entity — it operates as an extension of the parent company, which retains full liability for its activities. Registration is governed by the Macao Commercial Code (Código Comercial de Macau) and administered through the Conservatória do Registo Comercial e de Bens Móveis (CRCBM), Macao's commercial registry. The branch must appoint a local representative authorised to act on behalf of the parent firm.

A representative office, by contrast, is restricted to liaison, market research, and promotional activities. It cannot generate revenue or enter into commercial contracts directly. This structure is used when a foreign business wants to establish a physical foothold without undertaking trading operations.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None (extension of parent) | None (extension of parent) |

| Permitted Activities | Full commercial operations | Non-commercial only (liaison, research) |

| Local Representative | Mandatory; must be appointed in writing | Mandatory |

| Registered Address | Required in Macao SAR | Required in Macao SAR |

| Capital Requirement | None prescribed locally; parent's capital applies | None |

| Liability | Parent company bears full liability | Parent company bears full liability |

Focus Points

- Taxation: Branch profits are subject to Macao's Complementary Tax (Imposto Complementar de Rendimentos) at rates up to 12%; representative offices earning no local income are generally not taxable, though the position should be confirmed given the entity's specific activities.

- Annual Compliance: Branches must file audited accounts with the CRCBM and submit tax returns annually; representative offices have lighter filing obligations.

- Treaty Access: Macao maintains its own tax agreements independent of mainland China; access depends on the parent's jurisdiction and the applicable arrangement.

- Restrictions: A representative office cannot invoice clients, sign commercial contracts, or repatriate profits in its own name.

- Conversion: A branch can be converted into a locally incorporated entity, though this involves a separate registration process and does not carry over the branch's legal standing automatically.

Sub-Types

Branch Office

A branch is the standard vehicle for foreign firms wishing to conduct active business in the territory. It is bound by the parent's constitutional documents and must register those documents, translated into Portuguese or Chinese, with the CRCBM.

Representative Office

Representative offices are suited to companies in an early-entry phase. Because the structure prohibits revenue-generating activity, it carries lower compliance overhead but also provides no path to direct commercial operations without a separate registration.

Closing

Both structures serve foreign businesses testing or entering the Macao market, with the branch offering full operational capacity and the representative office serving as a low-commitment presence limited to non-commercial functions.

A branch office suits established foreign companies ready to conduct active trade; a representative office is appropriate for firms in a pre-commercial reconnaissance phase.

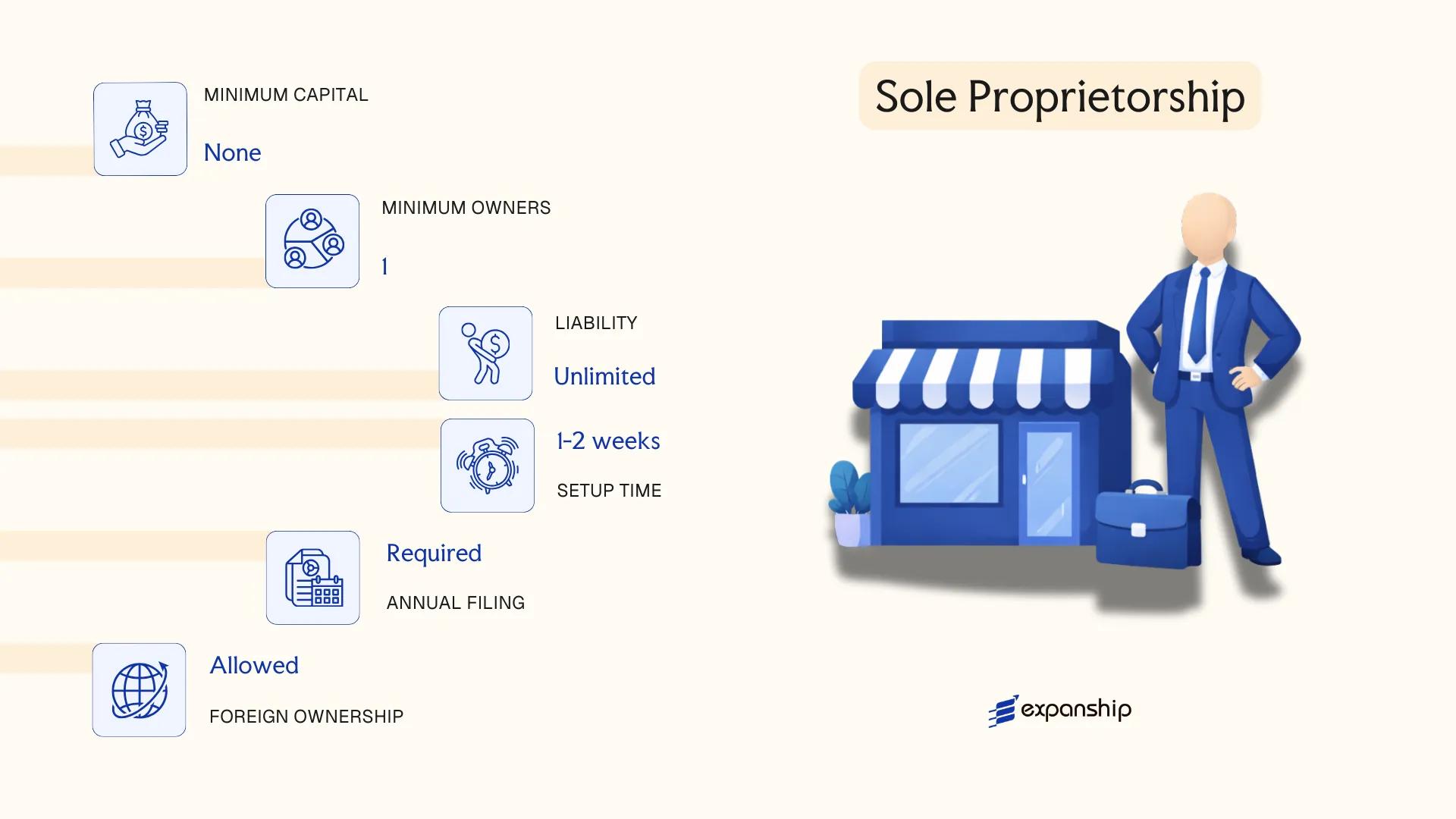

Sole Proprietorship (Estabelecimento Individual)

A Macao sole proprietorship (Estabelecimento Individual) is the simplest form of business registration available to individuals operating under their own name or a trade name. Governed by the Macao Commercial Code (Código Comercial), this structure carries no separate legal personality — the proprietor and the business are treated as one legal entity, meaning personal assets are directly exposed to business liabilities.

Registration is handled through the Macao Trade and Investment Promotion Institute (IPIM) and the Financial Services Bureau (DSF) for tax purposes. Sole trader registration in Macao SAR is straightforward relative to corporate structures, making it a common starting point for self-employed professionals and small-scale operators.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the proprietor |

| Member Type | Sole Proprietor (one natural person) | Minimum 1, maximum 1; legal persons cannot register as sole proprietors |

| Local Presence | Local registered business address required | No registered agent requirement, but a physical address for correspondence is mandatory |

| Capital | No statutory minimum capital | Declared in MOP; capital reflects proprietor's own investment |

| Liability | Unlimited personal liability | All personal assets are at risk for business debts |

| Privacy | Name appears on public commercial registry | No meaningful privacy protection for the proprietor's identity |

Focus Points

- Taxation: Subject to Macao's Complementary Tax (Imposto Complementar de Rendimentos) on net business profits; no separate corporate tax applies, as income is assessed at the proprietor level. No VAT exists in Macao; stamp duty may apply to certain transactions.

- Annual Compliance: Annual tax declaration required with the DSF; accounting records must be maintained, though simplified bookkeeping is permitted below certain turnover thresholds.

- Treaty Access: As an unincorporated individual business, access to double taxation agreements is determined by the proprietor's personal tax residency, not the business structure itself.

- Conversion: The Estabelecimento Individual can be converted into a Sociedade por Quotas (Lda.) if the business grows, though this requires a formal incorporation process rather than a simple structural change.

- Restrictions: Only natural persons resident or legally authorised to conduct business in Macao may register; foreign nationals must satisfy applicable residency or work authorisation requirements.

Recommendations

Individual business setup in Macao through this structure suits low-capital, low-risk operations where administrative simplicity outweighs the need for liability protection — the complete absence of limited liability is the defining constraint any prospective registrant must account for before proceeding.

This structure is most appropriate for self-employed individuals, freelancers, and micro-business operators with limited external financial exposure.

How to Choose the Right Entity Type in Macao

Choosing the right company type in Macao is not a purely administrative decision — it carries direct legal, financial, and operational consequences that are difficult to reverse once incorporation is complete.

Why Your Entity Choice Matters

The structure you register determines your compliance obligations, liability exposure, and tax treatment from day one. Selecting the wrong form can result in concrete problems:

- Choosing an entity without the capacity to trade locally, then conducting business with Macao residents, puts your firm in breach of the Commercial Code and may result in administrative penalties or forced dissolution.

- Selecting a structure that does not qualify under the terms of a double taxation agreement means your business cannot claim reduced withholding tax rates in counterpart jurisdictions, even if it is otherwise tax-resident in Macao.

- Forming a Sociedade Anónima when a sole proprietorship or Lda. would suffice binds your firm to mandatory auditor appointments and more structured governance obligations that generate recurring costs disproportionate to the business's scale.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or insurance each correspond to distinct permissible structures under Macao commercial law.

- Ownership and Management: Single-owner operations suit a Estabelecimento Individual or single-quota Lda., while multi-party ventures or those requiring a formal board point toward a Sociedade Anónima.

- Tax Objectives: Macao's complementary income tax and the applicability of its double taxation agreements vary by entity type and residency status, which directly affects your effective tax position.

- Local vs. External Operations: A representative office cannot generate revenue locally, so businesses intending to invoice Macao clients must register a fully incorporated entity.

- Substance Capacity: If you cannot maintain a genuine physical presence, management, and decision-making locally, consider whether your chosen structure triggers substance-related reporting obligations.

- Exit Strategy: Not all Macao entity types support redomiciliation or conversion; verify that your chosen structure permits the exit mechanism you may eventually need.

The full text of the Commercial Code of Macao governs formation, operation, and dissolution requirements across all entity types and should be consulted alongside professional legal advice before committing to a structure.

Compliance Services for Companies in Macao SAR

Ongoing compliance support for Macao-registered entities, covering annual filings, tax reporting, and regulatory obligations.

Conclusion

Incorporating a business in Macao SAR requires selecting a structure that aligns with your ownership model, liability exposure, and operational scope. Among the available forms, the Sociedade por Quotas remains the most commonly registered entity, favoured for its lower capital threshold and straightforward governance under the Commercial Code. The Sociedade Anónima suits larger enterprises requiring transferable share capital, while partnerships serve smaller ventures with defined partner roles. Branch offices and representative offices extend foreign legal presence without local incorporation, though each carries distinct limitations on permissible activities.

Macao's status as a Special Administrative Region, its growing network of tax information exchange arrangements, and its role as a gateway between mainland China and Portuguese-speaking markets continue to shape its regulatory development. Expanship's team works directly with these structures across the jurisdiction's registration and compliance framework.

How Expanship Can Assist You

Expanship's Macao company formation services cover the full registration process under the Commercial Code, from selecting the right entity — a Sociedade por Quotas, Sociedade Anónima, or branch structure — through to filing with the Conservatória do Registo Comercial. Our team works directly with the Macao Financial Services Bureau (DSF) on tax registration obligations, so nothing falls through the gaps after incorporation.

Our professional incorporation services in Macao SAR extend well beyond initial registration. Here is what we handle on your behalf:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Government filings and Conservatória liaison

- Post-incorporation compliance management

- Business account introduction assistance

- Ongoing annual maintenance and statutory filings

Ready to move forward? Reach out to Expanship Macao to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Sociedade por Quotas (Lda.) is the most frequently registered business structure in Macao. Its lower capital requirements, straightforward governance, and suitability for small-to-medium operations make it the default choice for both local entrepreneurs and foreign investors establishing a trading presence.

A branch is not a separate legal entity — liabilities flow directly to the foreign parent company. A Sociedade por Quotas, by contrast, holds independent legal personality under the Macao Commercial Code, limiting member liability to their quota contributions. Compliance obligations also differ: branches must file accounts aligned with the parent, while a Lda. maintains its own standalone books with the Conservatória do Registo Comercial.

The Sociedade por Quotas offers relatively limited public disclosure compared to the Sociedade Anónima, whose shareholder register is more broadly accessible. Beneficial ownership information is subject to Macao's anti-money laundering framework, so complete anonymity is not achievable under current regulations. Nominee arrangements are legally permissible but must comply with disclosure obligations under applicable financial intelligence legislation.

Not across all structures. A sole proprietorship (Estabelecimento Individual) and a Sociedade por Quotas can each be formed by one person. General partnerships (Sociedade em Nome Colectivo) and limited partnerships (Sociedade em Comandita) require at least two partners by definition, as the structure is inherently multi-party.

Foreign nationals face no statutory nationality restriction when registering a Sociedade por Quotas or Sociedade Anónima. Both structures are open to non-residents, though a registered address in Macao and a local fiscal representative are required. Foreign companies preferring not to incorporate separately may instead establish a branch or representative office under the foreign parent's existing legal identity.

Conversion between entity types is recognized under the Macao Commercial Code, most commonly from a Sociedade por Quotas to a Sociedade Anónima as a business scales. The process involves filing amended constitutional documents with the Conservatória do Registo Comercial and meeting the capital thresholds of the target structure. Not all conversions are straightforward — restructuring from a partnership to a limited liability form, for instance, requires more substantive legal reorganization.

No. Sole proprietorships and general partnerships do not create a legal barrier between the business and its owners, meaning personal assets remain exposed to business liabilities. The Sociedade por Quotas, Sociedade Anónima, and limited partnership (to the extent of the comanditário's contribution) each carry distinct legal personality under Macao commercial law.

The sole proprietorship imposes the lightest administrative burden, with no statutory audit requirement and simplified registration through the Conservatória do Registo Comercial. The trade-off is unlimited personal liability, which limits its suitability for higher-risk or capital-intensive activities. Among incorporated forms, the Sociedade por Quotas generally requires less governance formality than the Sociedade Anónima.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.