Key Takeaways

- The SARL is the most commonly registered business structure in Madagascar, making it the default choice for small to medium enterprises seeking limited liability without the governance requirements of a public company.

- Madagascar operates a territorial tax system, meaning companies are generally taxed only on income sourced within the country rather than on worldwide earnings.

- Foreign firms entering Madagascar can establish a branch or representative office as a market-entry foothold without creating a separate legal entity subject to full local incorporation requirements.

- Business registration and investment facilitation in Madagascar fall under the authority of the EDBM (Economic Development Board of Madagascar), which oversees company setup across all entity types.

Introduction to Entity Types in Madagascar

Madagascar is an island nation located in the Indian Ocean, off the southeastern coast of Africa, separated from the mainland by the Mozambique Channel. As an independent republic, its company registration and corporate governance fall under the authority of the Agence Économique de Madagascar (EDBM), the body responsible for facilitating business registration and investment in the country.

The tax regime operates on a territorial basis, meaning businesses are generally taxed on income sourced within the country rather than on worldwide earnings.

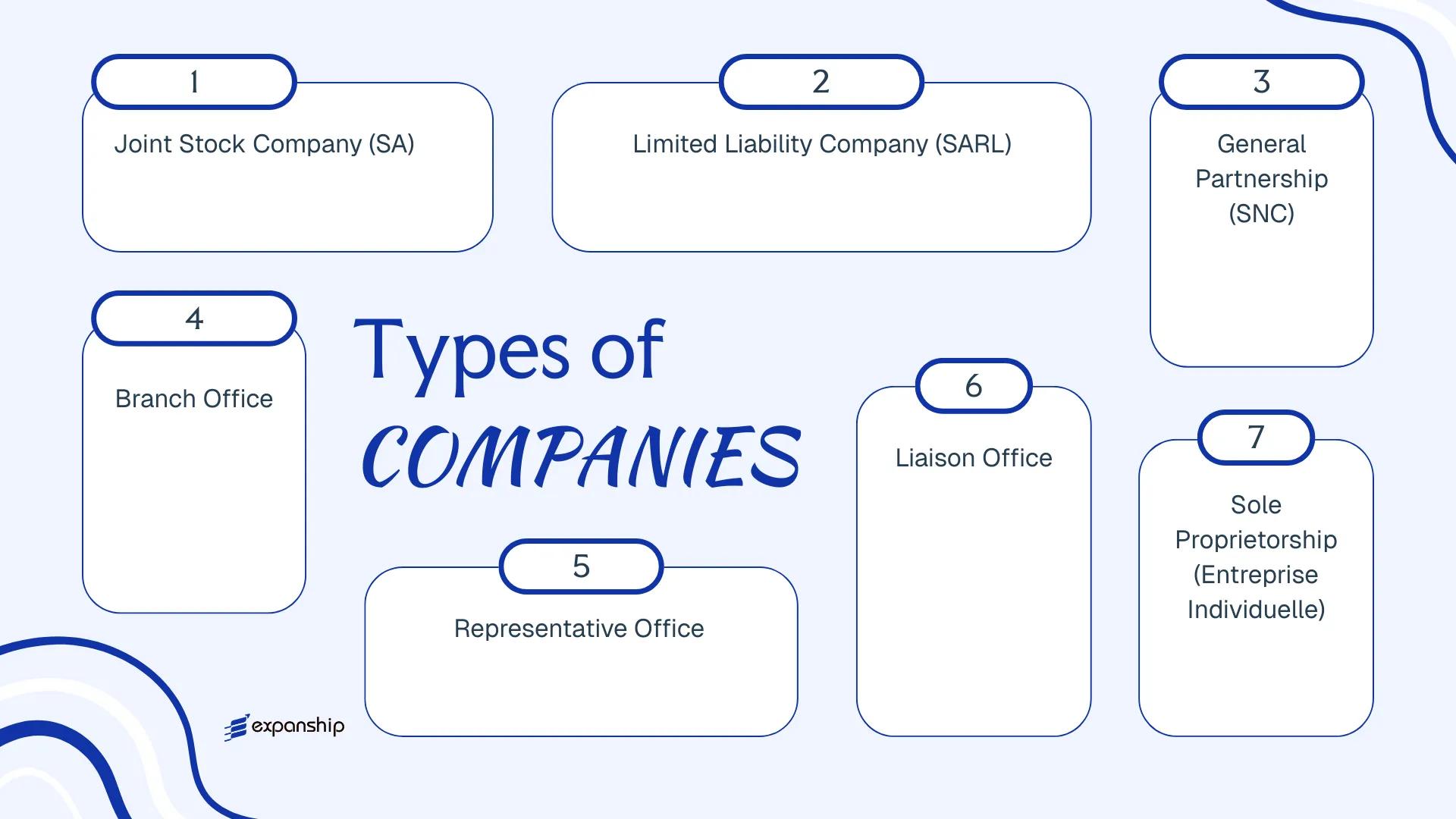

Several business entity types in Madagascar are available to both resident and foreign investors. These include the Société Anonyme (SA), Société à Responsabilité Limitée (SARL), Société en Nom Collectif (SNC), Sole Proprietorship (Entreprise Individuelle), and foreign business structures such as branch offices, representative offices, and liaison offices. Each structure carries distinct implications for liability, governance, and taxation.

This article examines each of these Madagascar company structures in detail — covering registration requirements, capital thresholds, ownership rules, and operational considerations — to help you identify the structure that aligns with your business objectives.

An Overview of Business Structures in Madagascar

Madagascar's company law framework provides several distinct legal forms, governed primarily by Law No. 2003-036 on Commercial Companies (the OHADA-influenced Commercial Companies Act) alongside the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, which Madagascar applies as part of its regional commercial law commitments. Each structure carries different implications for liability, ownership, taxation, and operational scope.

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| SA | Joint Stock Company | Limited to shares | Taxed | Yes | 3 shareholders | EDBM / RCS | OHADA Uniform Act |

| SARL | Limited Liability Company | Limited to contribution | Taxed | Yes | 1 shareholder | EDBM / RCS | OHADA Uniform Act |

| SNC | General Partnership | Unlimited, joint | Taxed | Yes | 2 partners | RCS | OHADA Uniform Act |

| Branch Office | Foreign branch | Parent liable | Taxed | Yes | N/A (parent entity) | EDBM / RCS | Investment Law |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | No | N/A (parent entity) | EDBM | Investment Law |

| Sole Proprietorship | Individual trader | Unlimited, personal | Taxed | Yes | 1 individual | RCS | Commercial Code |

Each of these structures is examined in full in the sections below.

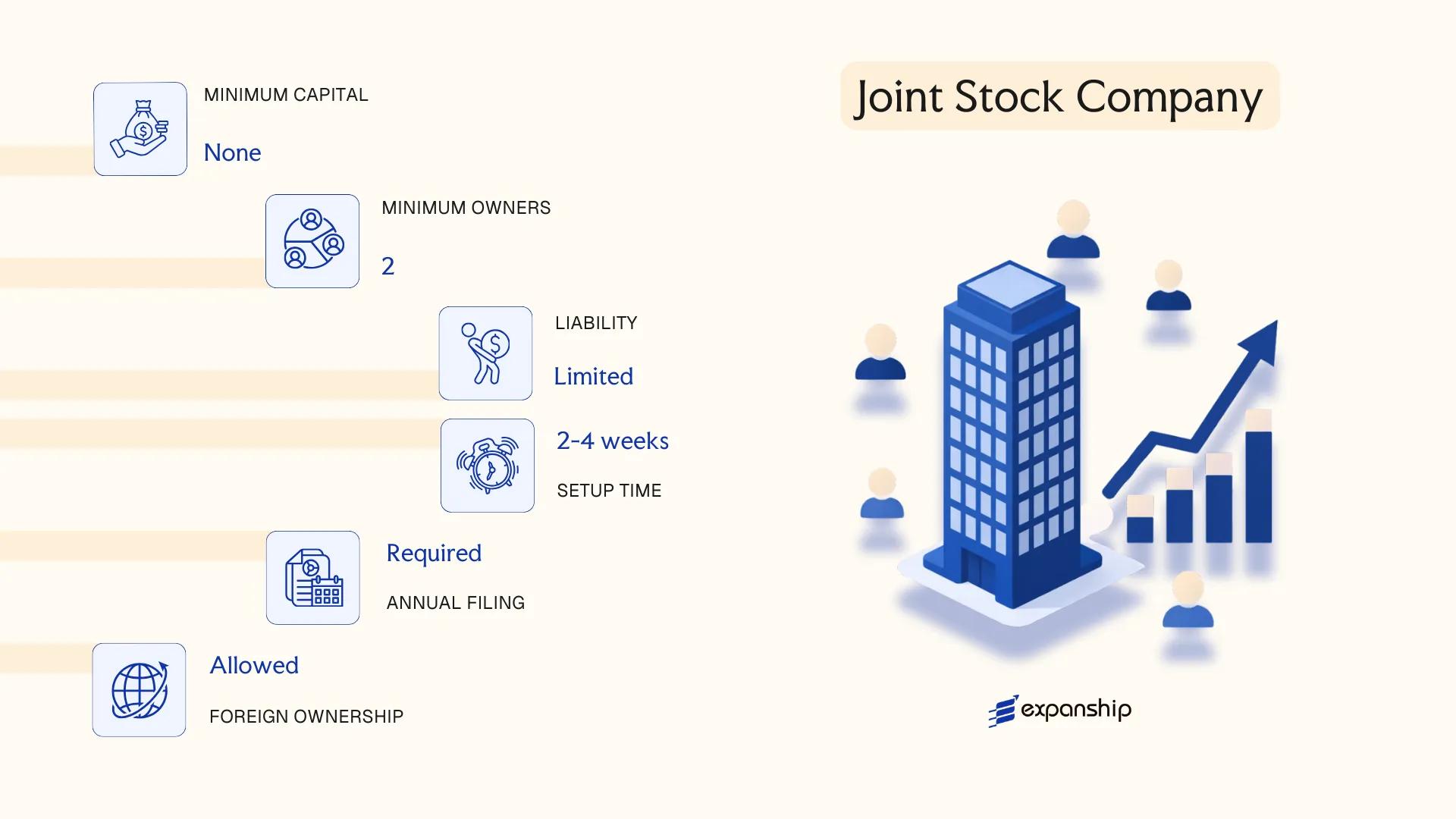

Société Anonyme (SA) — Joint Stock Company

The Société Anonyme SA Madagascar framework is governed by Law No. 2003-036 on Commercial Companies (OHADA-aligned legislation), which grants the SA separate legal personality distinct from its shareholders. Liability is limited to each shareholder's capital contribution.

Structured for larger commercial operations, the SA can issue transferable shares to multiple investors, making it suitable for businesses seeking external financing or eventual public listing.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (SA) | Separate legal personality; governed by Law No. 2003-036 |

| Members | Shareholders (min. 3) | No statutory maximum; directors (min. 3) manage the entity |

| Local Presence | Registered office in Madagascar required | A local director is generally required |

| Capital | MGA minimum (generally MGA 20,000,000) | Divided into transferable shares; partial paid-up on incorporation may be permitted |

| Privacy | Shareholder register maintained; publicly accessible filings with EDBM | Limited privacy for major shareholders |

Focus Points

- Taxation: Corporate income tax applies at the standard rate; VAT registration required above threshold; withholding tax applies to dividends, interest, and royalties paid to non-residents — consult the Direction Générale des Impôts for current rates.

- Annual Compliance: Statutory audit mandatory; annual general meeting required; financial statements must be filed with the relevant commercial court registry.

- Treaty Access: Madagascar has a limited tax treaty network; treaty benefits depend on shareholder residency.

- Conversion: An SA may convert to a SARL subject to shareholder approval and compliance with capital and membership thresholds.

- Restrictions: Certain sectors (mining, telecoms) require additional ministerial authorisations regardless of entity form.

Closing

The SA suits foreign investors establishing trading, holding, or large-scale operational entities that require institutional investment or structured share capital. The freely transferable share structure supports equity raises, though the mandatory audit and three-director minimum add ongoing administrative cost.

Best suited for larger enterprises, joint ventures, or businesses anticipating external equity investment or regulatory licensing requirements.

Company Incorporation in Madagascar

Incorporate an SA or other entity type in Madagascar with end-to-end support from Expanship.

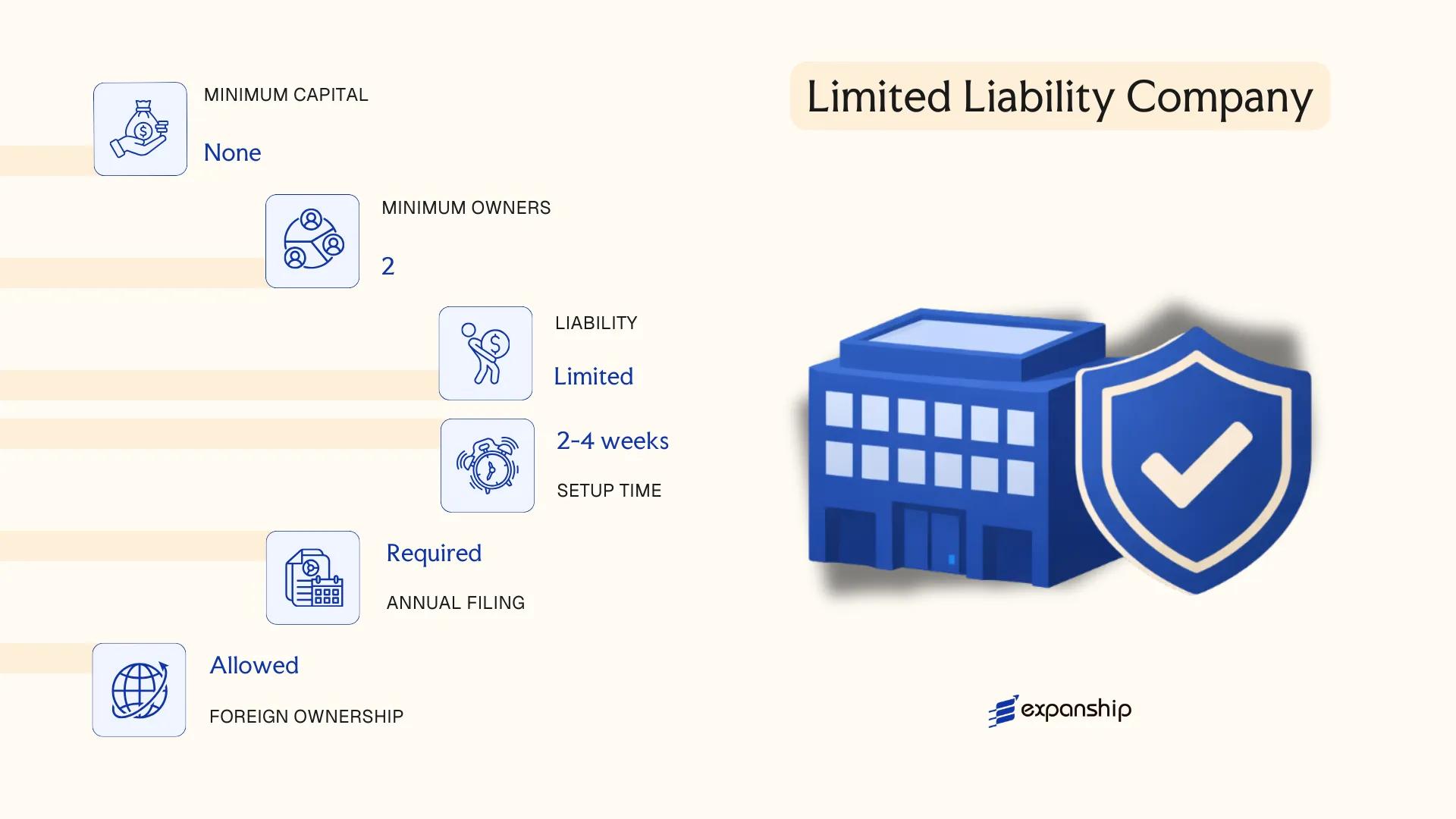

Société à Responsabilité Limitée (SARL) — Limited Liability Company

The Société à Responsabilité Limitée SARL Madagascar is governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, which Madagascar adopted as part of its integration into the OHADA treaty framework. The SARL offers separate legal personality, meaning the entity exists independently of its members, and liability is capped at each member's capital contribution.

This hybrid structure sits between a sole proprietorship and a full joint stock company. It accommodates small to mid-sized businesses seeking limited liability without the administrative weight of a Société Anonyme. SARL registration Madagascar is processed through the Economic Development Board of Madagascar (EDBM), which serves as the single window for business formalization.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société à Responsabilité Limitée (SARL) | Separate legal personality under OHADA law |

| Members | 1 to 50 associates (associés) | A single-member SARL is permitted (SARL unipersonnelle) |

| Management | One or more gérants (managers) | Need not be a member; nationality restrictions may apply |

| Local Presence | Registered office address required | No mandatory resident agent under OHADA, but local address is compulsory |

| Share Capital | No statutory minimum under OHADA | Capital must be fully subscribed at incorporation; stated in Ariary (MGA) |

| Privacy | Names of associates filed in the commercial register | Register is publicly accessible |

Focus Points

- Taxation: SARLs are subject to corporate income tax (Impôt sur les Revenus des Sociétés) at the standard rate; VAT applies to taxable supplies; withholding taxes apply to dividends, interest, and royalties paid to non-residents.

- Annual Compliance: Audited financial statements and annual general meeting required; filing obligations with the commercial court registry apply.

- Economic Substance: No formal economic substance regime, but genuine local activity is expected for tax residency purposes.

- Treaty Access: As a resident entity, a SARL may access Madagascar's tax treaty network, though the network remains limited in scope.

- Conversion: An SARL may be converted into a Société Anonyme once member thresholds or capital requirements warrant the change.

Closing

The SARL suits trading operations, service businesses, and local subsidiaries of foreign groups that require limited liability without full public company obligations. Its primary constraint is the 50-associate cap, which restricts equity structuring for larger ventures requiring broad investor participation.

This entity type is most appropriate for small to medium foreign-owned subsidiaries and locally operated businesses that prioritize liability protection over capital market access.

Société en Nom Collectif (SNC) — General Partnership

The Société en Nom Collectif SNC Madagascar structure is governed by the OHADA Uniform Act on Commercial Companies and the Economic Interest Group (Acte Uniforme relatif au droit des sociétés commerciales et du groupement d'intérêt économique), which Madagascar adopted upon joining the OHADA treaty framework. Unlike most commercial entities, the SNC carries a distinct legal characteristic: it possesses separate legal personality, yet all partners bear unlimited, joint, and several liability for the firm's debts.

Personal liability exposure is the defining feature that separates this structure from limited-liability entities. Each associé (partner) is directly answerable for the company's obligations with their personal assets, and creditors may pursue any individual partner for the full outstanding amount.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | General Partnership (Société en Nom Collectif) | Governed by OHADA Uniform Act on Commercial Companies |

| Members | Referred to as Associés (Partners); minimum 2, no statutory maximum | All partners must have merchant (commerçant) status under OHADA rules |

| Liability | Unlimited, joint, and several | Personal assets of each partner are exposed to business debts |

| Local Presence | Registered office (siège social) required in Madagascar | No mandatory resident agent requirement under OHADA, but local address is compulsory |

| Share Capital | No statutory minimum capital required | Contributions may be in cash, kind, or industry |

| Privacy | Partner names are publicly disclosed | SNC name typically incorporates partner surnames |

Focus Points

- Taxation: Subject to corporate income tax (Impôt sur les Revenus des Personnes Morales) at the standard rate; VAT obligations apply where turnover thresholds are met; partner-level distributions may attract withholding tax under domestic rules.

- Annual Compliance: Financial statements must be prepared in accordance with the OHADA Uniform Act on Accounting Law (SYSCOHADA); annual general meetings and filing obligations apply.

- Treaty Access: Access to Madagascar's tax treaty network is available, though the unlimited-liability structure limits practical use for holding or IP arrangements.

- Conversion: An SNC may be converted into another OHADA-compliant entity form, such as a SARL or SA, subject to partner unanimous consent and regulatory re-registration.

- Restrictions: Non-merchant individuals and certain regulated categories may be barred from holding associé status.

Closing

The SNC suits closely held professional or family trading businesses where partners accept mutual liability in exchange for a flexible, minimal-capital structure. Its primary drawback is the unrestricted personal exposure of every partner, which makes it unsuitable where asset protection is a priority.

Best suited for two or more established merchants or family-owned trading ventures where all parties have full confidence in one another and are prepared to accept unlimited personal liability.

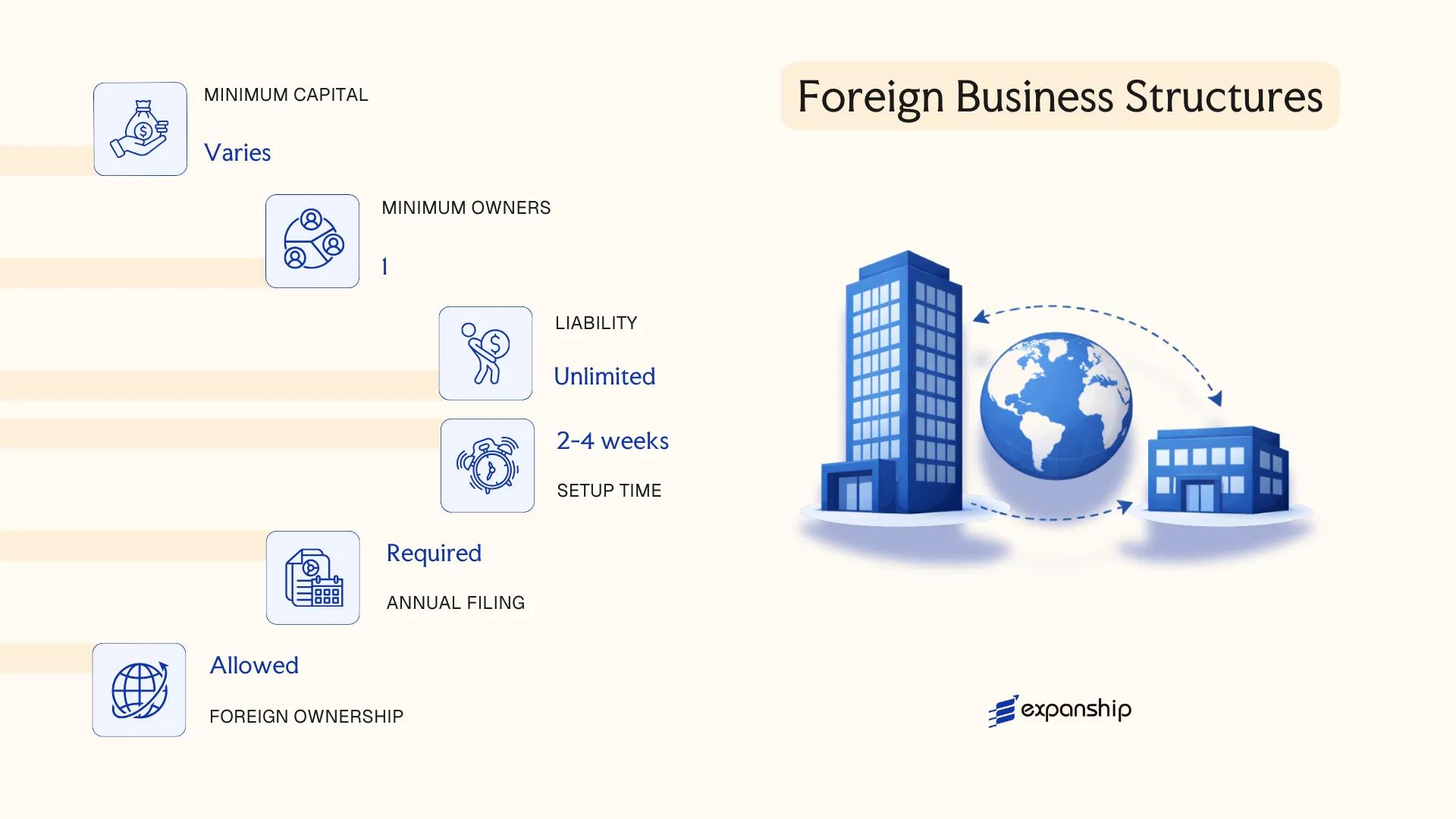

Foreign Business Structures in Madagascar [Branch Office, Representative Office, Liaison Office]

Foreign business structures registered under Malagasy law are governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, along with national investment legislation administered by the Economic Development Board of Madagascar (EDBM). Foreign branch office registration Madagascar follows a distinct track from local entity formation: the branch has no separate legal personality and its parent company bears full liability for its obligations.

Registration is handled through the EDBM's one-stop-shop window and requires filing the parent company's constitutional documents, certified and translated into French, alongside proof of the parent's legal existence in its home jurisdiction.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch / Representative / Liaison Office | Branch conducts commercial activity; representative and liaison offices are restricted to non-commercial functions |

| Head of Structure | Resident or non-resident Permanent Representative | Must hold a valid power of attorney from the parent entity |

| Local Presence | Registered address in Madagascar required | Physical office mandatory for branch; liaison offices may use a registered address |

| Capital | No statutory minimum for branch registration | Branch funding flows from the parent; no share capital is issued locally |

| Liability | Parent company bears unlimited liability | No liability ring-fencing at branch level |

| Privacy | Parent company details are publicly filed | Beneficial ownership of the parent may be disclosed depending on home jurisdiction |

Focus Points

- Taxation: Branches are subject to corporate income tax at the standard rate applicable to resident entities; VAT obligations apply to taxable supplies, and withholding tax applies to remittances to the parent.

- Economic Substance: Branches conducting active trade must demonstrate genuine operational presence; representative and liaison offices face restrictions on revenue-generating activity.

- Annual Compliance: Annual financial statements must be filed with the EDBM and the tax authority (DGI); the branch must maintain accounts separate from those of the parent.

- Treaty Access: Access to Madagascar's double taxation treaties depends on whether the branch constitutes a permanent establishment under the relevant treaty terms.

- Restrictions: Representative and liaison offices are legally barred from generating local revenue or entering commercial contracts in their own name.

Sub-Types

Branch Office

A branch conducts full commercial operations on behalf of the parent and is treated as a permanent establishment for tax purposes. It is used when a foreign firm wants direct market presence without incorporating a separate local entity.

Representative Office

This structure is limited to market research, promotional activity, and liaison functions. It cannot sign contracts or invoice clients, making it suitable for preliminary market entry before committing to a permanent structure.

Liaison Office

Functionally similar to a representative office, a liaison office serves primarily as a communication channel between the parent company and local partners or authorities. Its operational scope is the most restricted of the three structures.

Closing

Foreign business structures are most appropriate for firms testing the Malagasy market or managing regional operations from a single parent entity; the branch office suits active trading, while representative and liaison offices suit preparatory functions. The primary drawback across all three is the absence of liability separation from the parent company.

These structures are best suited for established foreign companies seeking a controlled, low-commitment entry into the Malagasy market before deciding on full local incorporation.

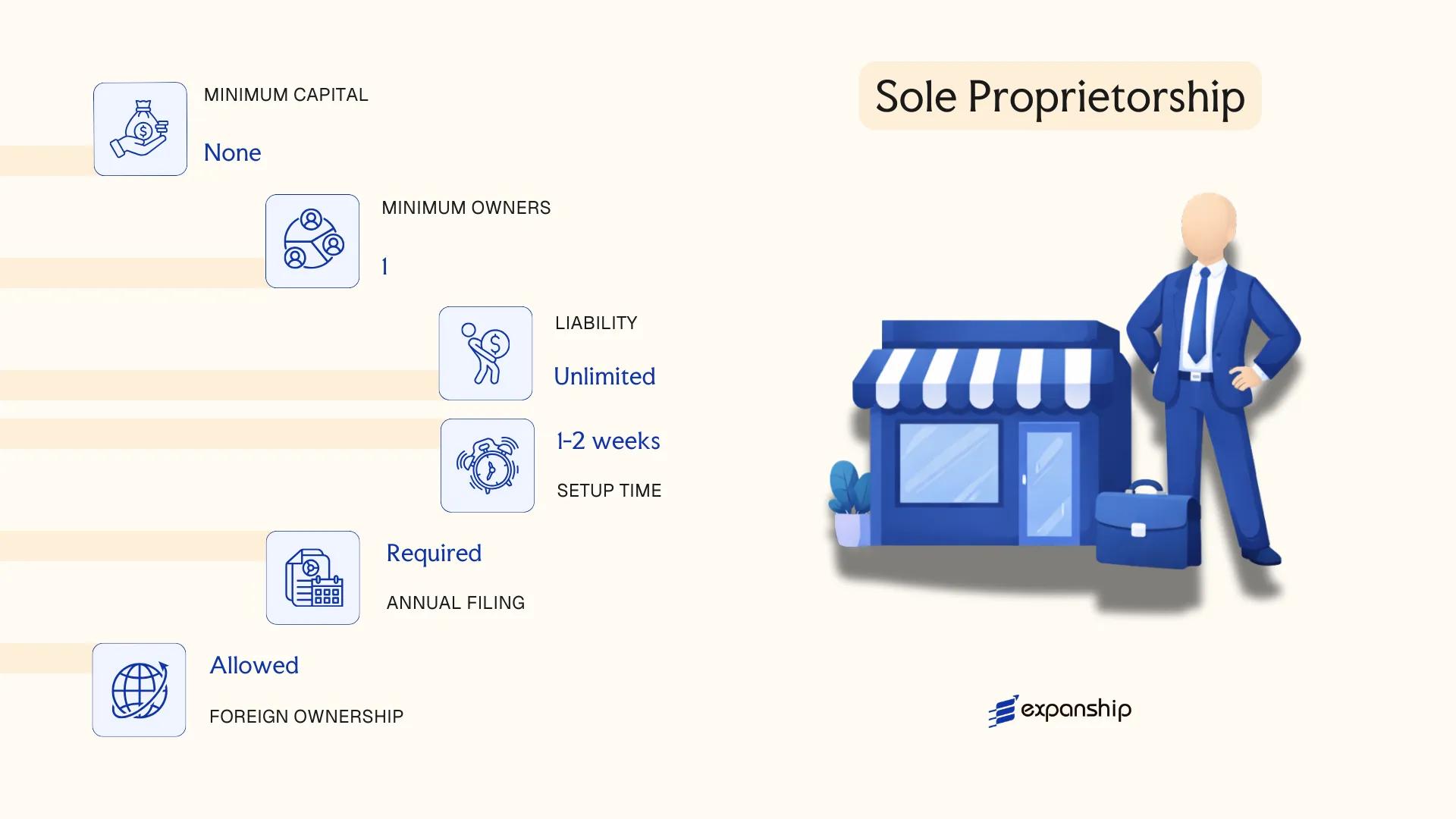

Sole Proprietorship (Entreprise Individuelle)

The sole proprietorship Entreprise Individuelle Madagascar framework governs the simplest form of business registration available under Malagasy commercial law. Governed broadly by the OHADA Uniform Act on General Commercial Law, as adopted and applied in Madagascar, this structure carries no separate legal personality — the business and its owner are treated as one legal unit.

Because no distinction exists between personal and business assets, the proprietor bears unlimited liability for all commercial obligations incurred. Registration is handled through the Guichet Unique de Formalisation des Entreprises (GUIDE), the one-stop-shop for business formalization.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Entreprise Individuelle) | No separate legal personality from the owner |

| Members | Single natural person (proprietor) | No shareholders or directors; owner operates directly |

| Local Presence | Registered business address in Madagascar | No registered agent requirement; physical address required |

| Capital | No statutory minimum capital | Capital is not formally defined or required at registration |

| Liability | Unlimited personal liability | Personal assets exposed to business debts |

| Privacy | Owner's identity publicly linked to the business | No shareholder register separate from the proprietor |

Focus Points

- Taxation: Subject to income tax (IRSA or IR depending on classification) on business profits; VAT applies if annual turnover exceeds the applicable threshold; no corporate income tax applies since profits pass directly to the individual.

- Annual Compliance: Annual tax filing required; accounting obligations depend on turnover classification under the simplified or real regime.

- Economic Substance: No formal substance requirements, though the proprietor must conduct business activities from a registered address.

- Conversion: Can be converted into a SARL or other corporate form, though this requires a full re-registration process rather than a structural amendment.

- Treaty Access: Access to Madagascar's tax treaties is limited, as the proprietor is taxed as an individual rather than a corporate entity.

Closing

This structure suits freelancers, sole traders, and micro-entrepreneurs conducting low-risk, low-volume activity who want minimal administrative overhead. The absence of capital requirements and straightforward Madagascar sole trader registration process are practical advantages, but unlimited liability remains a significant constraint for any business with meaningful financial exposure.

Best suited for individual entrepreneurs and self-employed professionals testing a local market or operating small-scale service businesses with limited financial risk.

How to Choose the Right Entity Type in Madagascar

Selecting how to choose a business structure in Madagascar requires more than comparing registration fees. The structure you form determines your tax exposure, your liability profile, and your legal capacity to operate.

Why Your Entity Choice Matters

Registering the wrong entity type produces concrete, documented consequences:

- A branch office that exceeds its permitted scope of activity — such as executing contracts or generating local revenue — operates in breach of the OHADA Uniform Act on Commercial Companies, which can result in administrative penalties or forced dissolution.

- Choosing a structure with no treaty eligibility means your business cannot claim withholding tax reductions under Madagascar's bilateral tax agreements, resulting in full withholding rates applied to dividends, royalties, or service fees.

- Selecting an SA when your business is a single-person consultancy imposes statutory audit requirements under Malagasy corporate law, adding annual costs that a SARL or sole proprietorship would not trigger.

- Forming an SNC when limited liability is commercially necessary exposes all partners to unlimited personal liability for company debts.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors such as banking or insurance, and passive asset-holding each point to structurally different entities under Malagasy law.

- Ownership Structure: An SA suits multi-shareholder arrangements requiring a formal board; a SARL accommodates smaller ownership groups with less administrative overhead.

- Tax Position: Your eligibility for Madagascar's applicable tax regimes, including the impôt sur les revenus des capitaux mobiliers on distributed profits, depends on entity classification.

- Liability Exposure: Partners in an SNC bear joint and unlimited liability, while SARL and SA shareholders are protected to the extent of their contributions.

- Exit and Redomiciliation: Not all Malagasy entity types support conversion or redomiciliation, so anticipated structural changes should factor into the initial decision.

Madagascar's primary company formation framework is governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, which sets the binding legal parameters for each structure.

Compliance Services for Companies in Madagascar

Maintain your entity's good standing with ongoing compliance support covering statutory filings, annual returns, and regulatory obligations under Malagasy and OHADA frameworks.

Conclusion

Incorporating a company in Madagascar requires selecting a structure that matches your operational scope, ownership model, and liability tolerance. The SARL suits small to medium enterprises where a single or small group of shareholders wants contained liability without the governance burden of a public entity. The SA fits businesses that anticipate external investment or eventual capital market activity. The SNC places full liability on its partners, making it appropriate only where partners accept that exposure. For foreign firms testing the market, a branch or representative office provides a foothold without establishing a separate legal entity.

The SARL remains the most commonly registered structure in Madagascar. Regulatory oversight falls under the EDBM (Economic Development Board of Madagascar), which continues to work toward reducing registration timelines. Treaty coverage is still developing, a factor worth weighing when structuring cross-border activity. Expanship's team works directly within this framework to assist with Madagascar company setup across all entity types.

How Expanship Can Assist You

Expanship company formation services Madagascar cover the full process of registering your business with the Economic Development Board of Madagascar (EDBM) — from selecting the right structure, whether a SARL, SA, or branch office, to meeting the ongoing compliance obligations each entity type carries. Our team works directly with the relevant registrar to keep your incorporation timeline on track.

Beyond initial registration, we handle the practical requirements that follow:

- Document preparation and notarization

- Registered agent and registered office provision

- EDBM filing and government liaison

- Post-incorporation compliance management

- Corporate secretarial support

- Banking introduction assistance

Your business deserves a Madagascar corporate services provider that knows the local regulatory environment in detail. To discuss your specific situation, reach out to Expanship Madagascar directly.

Frequently Asked Questions (FAQ)

The Société à Responsabilité Limitée (SARL) is the most widely registered entity in Madagascar. Its relatively low capital requirements and simplified governance structure make it the default choice for small to medium-sized enterprises operated by local and foreign founders alike.

A Branch Office has no separate legal personality from its foreign parent, meaning the parent company bears full liability for the branch's obligations. An SARL, by contrast, is a distinct legal entity whose members' liability is limited to their capital contributions. Compliance obligations for a Branch are tied to the foreign parent's reporting standards, whereas an SARL follows Malagasy corporate law under the OHADA Uniform Acts as adopted locally.

Among available structures, the SARL offers a degree of privacy in that detailed shareholder information is not routinely published in public commercial registers. Nominee services can be used where permitted, though ultimate beneficial ownership disclosure requirements are increasingly enforced. Madagascar's alignment with OHADA frameworks has progressively tightened transparency standards across entity types.

A sole proprietorship (Entreprise Individuelle) and a single-member SARL can both be formed by one individual. The Société Anonyme requires a minimum of one shareholder but has a mandatory board structure that typically involves multiple persons. A Société en Nom Collectif (SNC) requires at least two partners by definition, making it structurally unsuitable for sole founders.

Foreign nationals may register an SARL, SA, or establish a Branch Office or Representative Office in Madagascar. There are no general nationality restrictions preventing foreign ownership, though certain regulated sectors may impose local participation requirements. Registration is processed through the Economic Development Board of Madagascar (EDBM), which serves as the primary one-stop shop for business incorporation.

Conversion between entity types is legally possible under the OHADA Uniform Act on Commercial Companies, which Madagascar applies. An SARL can be converted into an SA, for example, provided the conditions for the target entity type are met, including any minimum capital thresholds. The process requires shareholder approval, updated constitutional documents, and re-registration with the competent authority.

Not all structures carry separate legal personality. The SARL, SA, and SNC are distinct legal entities. Branch Offices and Representative Offices are extensions of their foreign parent company and do not constitute independent legal persons under Malagasy law, which has direct implications for liability, taxation, and contract enforceability.

The Entreprise Individuelle carries the lightest compliance burden, with no requirement for audited financial statements or formal board governance. The SARL sits in the middle range, requiring annual financial reporting but no mandatory external audit below certain revenue thresholds. The SA carries the most extensive obligations, including statutory audit requirements and structured board governance under applicable OHADA rules.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.