Key Takeaways

- Monaco's business environment is regulated by the Direction de l'Expansion Économique, which oversees company registration and licensing across all entity types in the Principality.

- The Société Anonyme Monégasque (SAM) is the most commonly registered structure in Monaco, particularly within the financial services and real estate sectors.

- Corporate tax in Monaco applies only to profits generated from outside the Principality under specific conditions, distinguishing it from both standard territorial and zero-tax regimes.

- Structures such as the Société en Nom Collectif (SNC) and Société en Commandite Simple (SCS) remain available for professional partnerships where partners accept personal liability in exchange for operational flexibility.

Introduction to Entity Types in Monaco

Monaco is a sovereign city-state on the French Riviera, bordered by France on three sides and the Mediterranean Sea to the south. Despite covering less than 2.1 square kilometres, it functions as a fully independent principality with its own legal framework governing commercial activity. Company registration and business licensing fall under the jurisdiction of the Direction de l'Expansion Économique, the government body responsible for approving and regulating business establishments in the principality.

Residents and certain qualifying entities benefit from an absence of personal income tax, while corporate tax applies only to profits generated from outside Monaco under specific conditions — making the tax posture distinct from both standard territorial and zero-tax regimes.

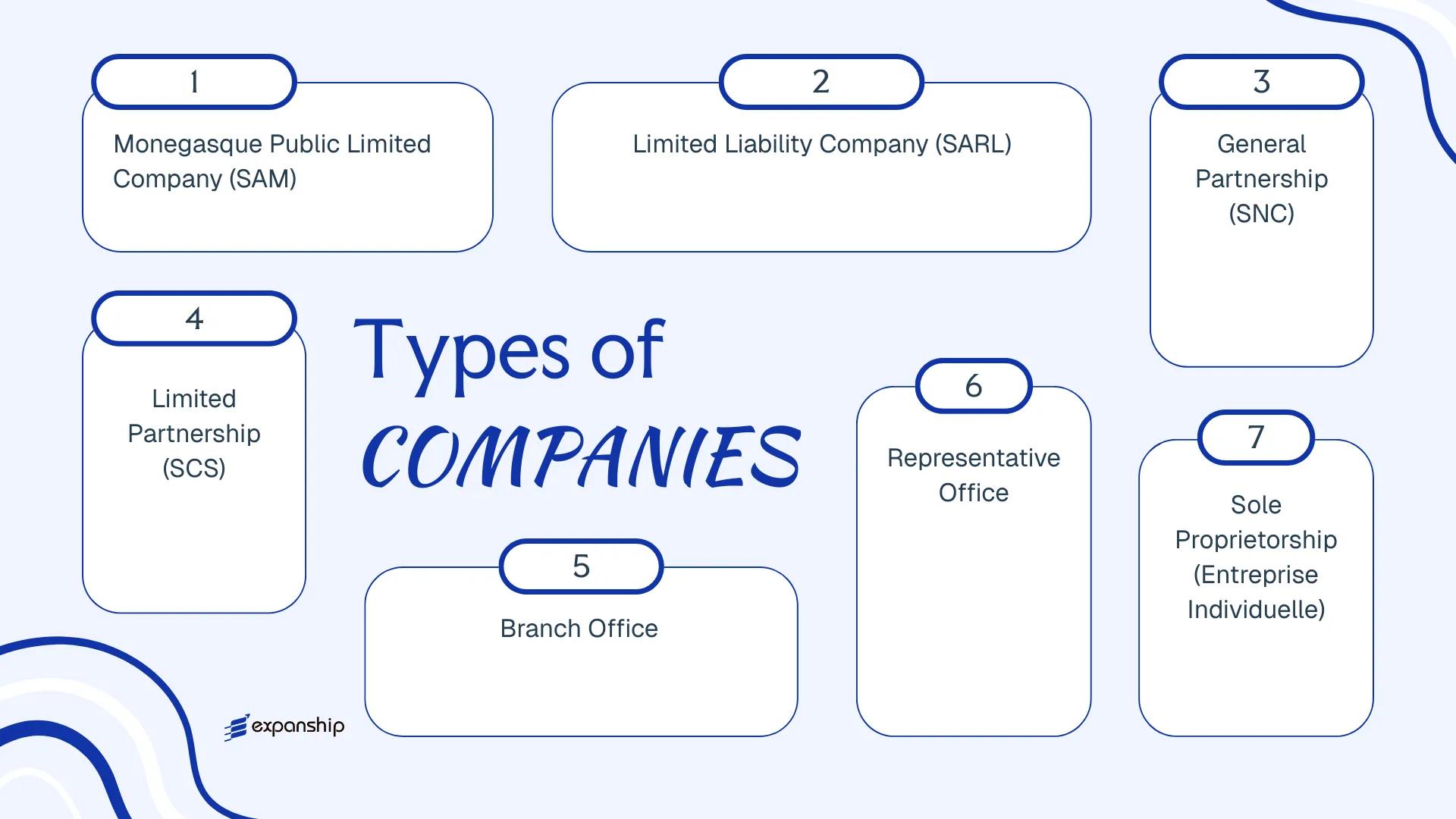

Several types of companies in Monaco are available to entrepreneurs and foreign investors. The main Monaco business entity types include the Société Anonyme Monégasque (SAM), Société à Responsabilité Limitée (SARL), Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), branch offices, representative offices, and sole proprietorships. Each structure carries different requirements around capital, liability, and permitted activity. This article covers each of these options in detail to help you assess which structure fits your operational needs.

An Overview of Business Structures in Monaco

Monaco's company law framework accommodates several distinct legal structures, each governed primarily by the Code de Commerce and supplemented by specific legislation such as the law of 25 June 1999 on société anonymes. The Direction de l'Expansion Économique (DEE) oversees commercial registration and authorisation for all entities operating in the Principality. Each structure differs in liability exposure, governance requirements, and permitted commercial activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| SAM | Corporation | Limited | Taxable (profit-based) | Permitted | 2 shareholders | DEE / RCI | Law of 25 June 1999 |

| SARL | Limited liability company | Limited | Taxable (profit-based) | Permitted | 1–100 shareholders | DEE / RCI | Code de Commerce |

| SNC | General partnership | Unlimited | Taxable | Permitted | Min. 2 partners | DEE / RCI | Code de Commerce |

| SCS | Limited partnership | Mixed | Taxable | Permitted | Min. 2 partners | DEE / RCI | Code de Commerce |

| Branch Office | Foreign establishment | Parent liable | Taxable | Permitted | Parent company | DEE / RCI | Code de Commerce |

| Representative Office | Non-trading establishment | Parent liable | Generally exempt | Not permitted | Parent company | DEE | Code de Commerce |

| Sole Proprietorship | Individual trader | Unlimited | Taxable | Permitted | 1 individual | DEE / RCI | Code de Commerce |

Each of these structures is examined in full in the sections below.

Société Anonyme Monégasque (SAM)

The Société Anonyme Monégasque (SAM) is Monaco's primary vehicle for Société Anonyme Monégasque SAM formation at scale, governed principally by the Monégasque Commercial Code and Sovereign Ordinance No. 408 of 1945, with subsequent amendments regulating its structure and governance. As a SAM Monaco joint stock company, it holds separate legal personality, meaning the entity can own assets, enter contracts, and incur liabilities in its own name.

Shareholders' liability is limited to the value of their capital contribution. This structure suits businesses seeking to attract multiple investors or operate across multiple sectors, as shares are transferable subject to the entity's statutes.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme Monégasque (SAM) | Joint stock company with separate legal personality |

| Members | Minimum 2 shareholders; no statutory maximum | Shareholders may be natural or legal persons; corporate shareholders permitted |

| Governance | Board of Directors (minimum 3 members) or a dual-tier structure | Directors need not be Monégasque nationals |

| Local Presence | Registered office in Monaco required | Physical address; registered agent not mandatory but advisable |

| Share Capital | Minimum EUR 150,000 | At least 25% paid up at incorporation; remainder within 5 years |

| Privacy | Shareholder names filed with the Trade and Industry Register (RCI) | Beneficial ownership disclosure required under AML regulations |

Focus Points

- Taxation: Subject to corporate income tax at 26.5% on profits derived from outside Monaco; businesses earning 75% or more of revenues within Monaco are generally exempt; no personal income tax, capital gains tax, or withholding tax on dividends; VAT applies at French rates under a customs union arrangement.

- Economic Substance: No formal substance requirements comparable to some offshore regimes, but a genuine registered office and operational presence are expected for tax exemption eligibility.

- Annual Compliance: Annual accounts must be filed with the RCI; statutory audit required above certain thresholds; annual general meeting of shareholders is mandatory.

- Treaty Access: Monaco has a limited double tax treaty network; a specific treaty with France governs cross-border arrangements; access to EU directives is not available as Monaco is not an EU member state.

- Restrictions: Certain regulated activities (banking, insurance, real estate) require prior government authorisation regardless of entity type.

Closing

The SAM is used primarily for trading operations, holding structures, and regulated financial activities requiring a credible corporate form with transferable share capital. The transferability of shares provides structural flexibility for investor entry and exit, though the minimum capital threshold of EUR 150,000 and mandatory audit requirements add a layer of administrative burden relative to smaller entity types.

Best suited for medium-to-large businesses, joint ventures, or investor-backed operations requiring a formally governed, scalable corporate structure in Monaco.

Company Incorporation in Monaco

Incorporate a Société Anonyme Monégasque (SAM) or other entity type with end-to-end support from Expanship's corporate services team.

Société à Responsabilité Limitée (SARL)

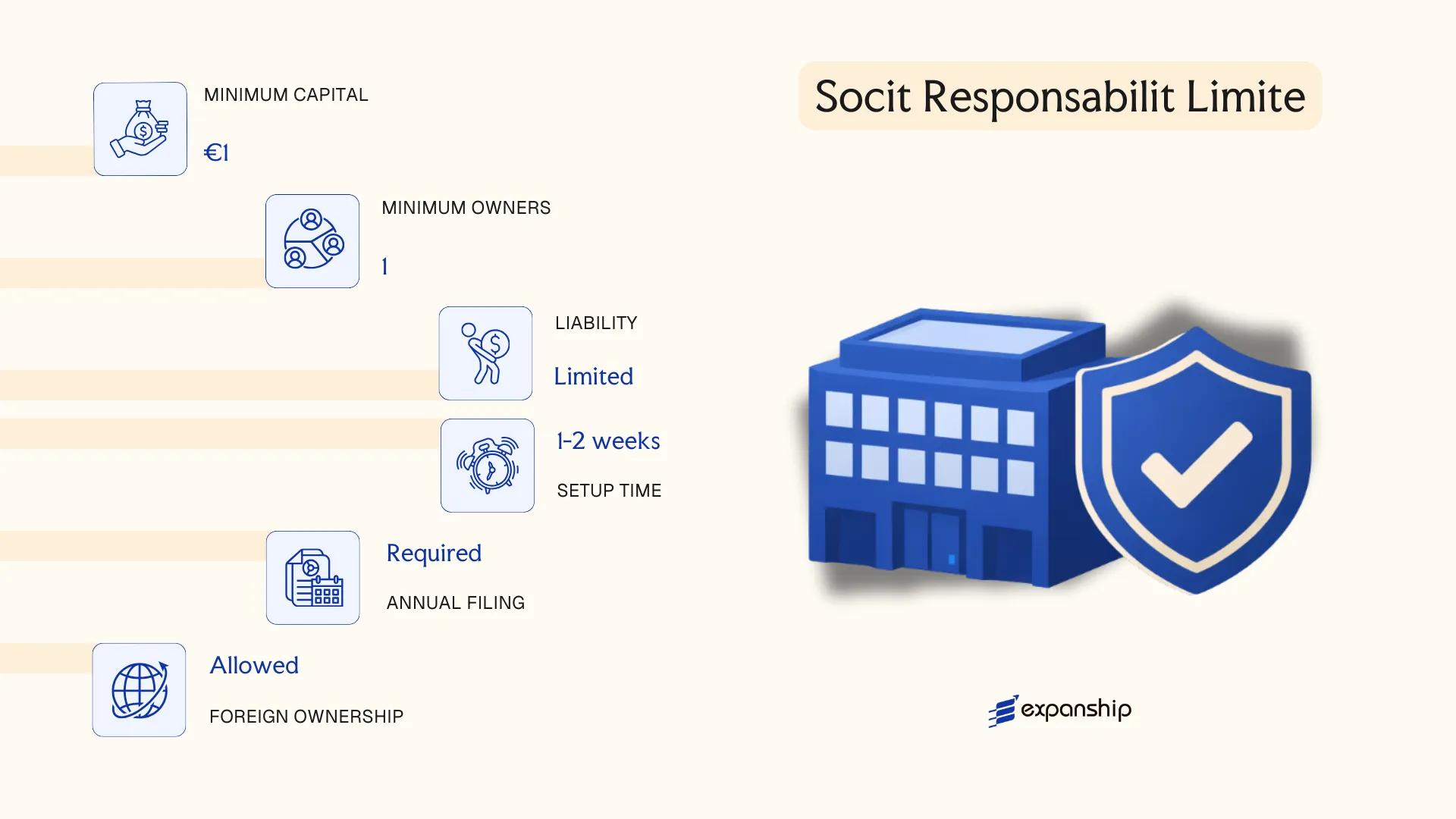

The Monaco SARL limited liability company is governed by Law No. 408 of 1945 and subsequent amendments incorporated into the Monegasque Commercial Code. As a distinct legal entity, the SARL carries its own rights and obligations separately from its members, with liability confined to each member's capital contribution.

Structurally, the SARL occupies a middle ground between a sole proprietorship and a full joint-stock company. It suits smaller commercial operations and family-run businesses where the formalities of a Société Anonyme Monégasque would be disproportionate to the scale of activity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Separate legal personality; members not personally liable beyond their contributions |

| Members | 1–50 associés (members) | No distinction between voting and non-voting classes under standard structure |

| Management | One or more gérants (managers) | Gérant need not be a member; appointment recorded in company statutes |

| Local Presence | Registered office in Monaco required | Physical address mandatory; virtual offices may not satisfy substance requirements |

| Share Capital | No statutory minimum under current rules | Capital divided into parts sociales; contributions can be cash or in-kind |

| Privacy | Members' names filed with the Trade and Industry Register (RCI) | Beneficial ownership disclosures required under AML legislation |

Focus Points

- Taxation: Monaco levies no personal income tax; corporate tax at 33.33% applies only where more than 25% of turnover derives from outside Monaco — VAT obligations depend on the nature of transactions.

- Annual Compliance: Annual accounts must be filed with the RCI; a statutory audit is not mandatory below certain thresholds.

- Economic Substance: A registered office alone is insufficient; genuine management activity within the Principality is expected for non-taxable status to hold.

- Restrictions: Certain regulated activities require prior authorisation from the Direction de l'Expansion Économique regardless of the chosen structure.

- Transfer of Interests: Transfer of parts sociales to third parties outside the existing membership requires approval from members representing at least three-quarters of the share capital.

Closing

The SARL is used primarily for trading operations, retail, and service businesses where the founders want liability protection without the administrative burden of a SAM. The main constraint is the 50-member ceiling, which limits its utility for businesses anticipating a broad investor base or future public fundraising.

The Monaco SARL is most appropriate for small to mid-sized owner-operated businesses seeking limited liability without the capital and governance requirements of a joint-stock structure.

Société en Nom Collectif (SNC) and Société en Commandite Simple (SCS) [General Partnership, Limited Partnership]

Both the SNC and SCS are governed by Monegasque commercial law, with their foundational rules derived from the Code de Commerce as applied in Monaco. Neither structure is widely used for commercial operations today, yet each serves a distinct purpose when the Monaco SNC SCS partnership structures are considered within a broader corporate planning context.

An SNC is a general partnership in which all partners hold unlimited, joint and several liability for the firm's debts. The SCS introduces a two-tier membership model: at least one general partner bears unlimited liability, while one or more limited partners remain liable only up to their capital contribution.

Key Characteristics

| Requirement | SNC | SCS |

|---|---|---|

| Legal Form | General Partnership | Limited Partnership |

| Members | Minimum 2 associates (gérants); no maximum; all bear unlimited liability | Minimum 1 general partner (associé commandité) + 1 limited partner (associé commanditaire) |

| Liability | Unlimited, joint and several for all partners | Unlimited for general partners; limited to contribution for limited partners |

| Minimum Capital | No statutory minimum | No statutory minimum |

| Local Presence | Registered office in Monaco required | Registered office in Monaco required |

| Privacy | Partner identities disclosed in registration filings | General partner identity disclosed; limited partner identity may have reduced exposure |

Focus Points

- Taxation: Profits are generally taxed at partner level rather than entity level; partners engaged in commercial activity may be subject to Monaco's business profit tax where applicable thresholds are met.

- Annual Compliance: Partners must file with the Répertoire du Commerce et de l'Industrie (RCI) and maintain updated statutory records.

- Treaty Access: Partnership structures typically do not benefit directly from double tax treaties; access depends on the tax residency of individual partners.

- Restrictions: Foreign nationals must obtain prior authorisation from the Direction de l'Expansion Économique before participating as a partner.

- Conversion: Conversion to a SAM or SARL is possible but requires a formal restructuring process and regulatory approval.

Sub-Types

Société en Nom Collectif (SNC)

The SNC operates without any limitation on partner liability, making it structurally unsuitable where asset protection is a priority. It is occasionally used for professional services arrangements or family-owned trading activities where all parties accept shared exposure.

Société en Commandite Simple (SCS)

The SCS separates active management from passive investment by distinguishing between commandités and commanditaires. This structure can serve family wealth arrangements or joint ventures where one party contributes capital without participating in management.

Closing

These structures suit closely-held arrangements where partners have aligned interests and where limited liability is either unnecessary or addressed through contractual means. The absence of a minimum capital requirement offers flexibility, though the exposure to unlimited liability for at least one partner represents a significant structural constraint.

SNC and SCS structures are best suited to professional partnerships or family-controlled ventures where all principal parties are known, trusted, and prepared to accept the corresponding liability exposure.

Foreign Business Establishments in Monaco [Branch Office, Representative Office]

Registering a foreign branch office in Monaco allows an overseas parent company to conduct business activities directly, without forming a separate local entity. The branch carries no independent legal personality — it remains an extension of the parent, which retains full liability for its obligations. This structure is governed by the general commercial law framework overseen by the Direction de l'Expansion Économique (DEE), the body responsible for approving commercial activity in the Principality.

Establishing a foreign business in Monaco through a branch requires prior government authorisation. The DEE reviews the application, and approval is tied to the nature of the intended activity, which must align with one of the permitted commercial categories.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch (établissement secondaire) | No separate legal personality; parent bears all liability |

| Registered Representative | Local authorised representative required | Must be resident in Monaco |

| Local Presence | Registered business address mandatory | Physical office address required for DEE registration |

| Capital | No minimum capital requirement | Parent company's capital structure applies |

| Privacy | Parent company details are publicly linked | Branch registration references the parent entity |

| Regulatory Approval | DEE authorisation required before commencing activity | Activity scope is fixed at approval stage |

Focus Points

- Taxation: Branches are subject to Monaco's corporate profit tax (impôt sur les bénéfices) at 33.33% only when more than 25% of turnover originates outside Monaco; no VAT applies within Monaco, though cross-border transactions may trigger French VAT obligations under the customs union with France.

- Economic Substance: The branch must demonstrate genuine operational presence tied to its approved activity category.

- Annual Compliance: Annual financial statements of the parent must generally be filed; the branch is subject to ongoing DEE reporting obligations.

- Treaty Access: Monaco has a limited tax treaty network; branch structures do not independently qualify for treaty benefits separate from the parent's home jurisdiction treaties.

- Restrictions: Activity is confined to the scope approved by the DEE; expanding into a new business category requires a separate authorisation.

Closing

A foreign branch suits multinational firms that need a commercial presence in Monaco without the cost and time of incorporating a new entity. The primary advantage is operational simplicity; the clear drawback is that the parent bears unlimited liability for all branch obligations.

Established foreign companies seeking a direct operational foothold in Monaco under an existing corporate structure, particularly in financial services, consulting, or trading sectors already approved by the DEE.

Sole Proprietorship (Entreprise Individuelle)

A Monaco sole proprietorship, known locally as the entreprise individuelle, is the simplest form of self-employed registration available under Monégasque commercial law. Unlike corporate structures, this form carries no separate legal personality — the proprietor and the business are legally the same person, meaning personal assets are directly exposed to business liabilities.

Registration is handled through the Répertoire du Commerce et de l'Industrie (RCI), which maintains records for all commercial operators in the Principality. Foreign nationals seeking to operate in this form must also satisfy residency and work authorisation requirements administered by the Direction de l'Emploi.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole proprietorship (no separate legal entity) | Proprietor bears unlimited personal liability |

| Member Type | Sole proprietor | Single individual only; no partners or shareholders |

| Local Presence | Registered business address in Monaco required | Must be a genuine operating address, not a mailbox |

| Capital | No statutory minimum | Proprietor contributes personal funds as needed |

| Privacy | Owner's name appears on RCI public register | No beneficial ownership shield |

| Permitted Activities | Subject to activity-specific licensing | Regulated professions require separate authorisation |

Focus Points

- Taxation: Subject to personal income tax rules applicable to residents; Monaco does not levy personal income tax on resident individuals, but non-resident proprietors may face tax obligations in their home jurisdiction on Monaco-sourced income.

- Social Contributions: The proprietor must register with the Caisse Autonome des Retraites (CAR) and contribute to social security schemes applicable to self-employed persons.

- Annual Compliance: Annual renewal of the RCI registration and any applicable trade licence (patente) is required to maintain legal standing.

- Treaty Access: As a sole proprietorship with no distinct legal personality, access to double tax treaty benefits depends entirely on the proprietor's individual tax residency status.

- Conversion: This structure can generally be converted into a corporate form such as an SARL, though the process requires a new incorporation and transfer of business assets.

Closing Paragraph

The entreprise individuelle suits freelancers, artisans, and individual consultants operating on a small scale without need for capital investment or multiple stakeholders. Its primary advantage is minimal administrative burden at formation; the significant drawback is unlimited personal liability, which exposes the proprietor's private assets to any business debts or legal claims.

Best suited for Monaco-resident individuals conducting low-risk, small-scale commercial or artisanal activities who do not require liability protection or external investors.

How to Choose the Right Entity Type in Monaco

Choosing the right company type in Monaco is a structural decision with direct legal and financial consequences — not a formality to revisit later.

Why Your Entity Choice Matters

The structure you register determines your compliance obligations from day one. Specific missteps produce concrete outcomes:

- Forming a SAM when your activity requires prior government authorisation under Ordinance No. 5.413 but failing to obtain it exposes you to administrative suspension before operations begin.

- Selecting an SNC, where all partners carry unlimited liability, when your business involves significant third-party credit risk leaves personal assets legally exposed to creditor claims.

- Establishing a branch of a foreign entity when local trading is intended without meeting the requirements administered by the Direction de l'Expansion Économique can result in operating without valid establishment, subject to penalties.

- Opting for a structure that does not permit nominee arrangements when full beneficial owner confidentiality is required creates disclosure exposure through Monaco's public commercial register.

Key Factors to Consider

- Business Activity: Active trading, regulated activities such as banking or insurance, and passive asset holding each correspond to different permitted structures under Monégasque commercial law.

- Ownership Structure: A single-owner operation may be better served by an SARL or sole proprietorship than a SAM, which requires a minimum of two shareholders and a board.

- Liability Exposure: Your tolerance for personal liability determines whether a limited-liability structure or a partnership form is appropriate.

- Minimum Capital: The SAM requires a minimum share capital of EUR 150,000, which directly affects which structures are financially accessible to your business.

- Exit and Redomiciliation: If you anticipate converting the entity or transferring its registered seat, verify in advance which structures Monégasque law permits to undergo that process.

- Regulatory Authorisation: Certain activities require sector-specific approval from bodies such as the Commission de Contrôle des Activités Financières (CCAF), which constrains entity choice independently of commercial preference.

Formation requirements and permitted structures are governed by the Monaco Commercial Code, though the authoritative source for Monégasque legislation is the Journal de Monaco, where relevant ordinances and laws are published officially.

Compliance Services for Companies in Monaco

Ongoing compliance support for Monégasque entities, including annual filings, registered office maintenance, and regulatory reporting.

Conclusion

Each entity type available in Monaco serves a distinct commercial purpose. The SAM suits larger enterprises or those seeking outside investment through share capital. For smaller, closely-held operations, the SARL offers limited liability without the capital requirements of a SAM. The SNC and SCS structures remain relevant for professional partnerships where personal liability is an accepted trade-off. Branch offices and representative offices allow foreign companies to establish a presence without incorporating a separate local entity, while the Entreprise Individuelle fits sole traders operating at a modest scale.

Among these, the SAM remains the most commonly registered structure, particularly among businesses drawn to Monaco's financial services and real estate sectors. Ongoing Monaco company formation activity reflects steady international interest, shaped by the Principality's expanding tax treaty network and its reputation as a stable, well-regulated jurisdiction. Incorporating in Monaco involves engagement with the Direction de l'Expansion Économique, and your choice of structure will shape both your compliance obligations and operational flexibility from the outset.

How Expanship Can Assist You

Expanship's Monaco company registration services cover the full arc of establishing a legal presence in the Principality — from selecting the appropriate entity type (SAM, SARL, or branch structure) through to securing the mandatory government authorisation issued by the Direction de l'Expansion Économique. Every step involves precise documentation, and our team manages that process on your behalf.

From initial filing to ongoing obligations, our support includes:

- Document preparation, notarisation, and legalization

- Registered agent and registered office provision

- Government filing and liaison with Monaco's trade register (Répertoire du Commerce et de l'Industrie)

- Post-incorporation compliance management

- Banking introduction assistance

Your business gets a single point of contact throughout — no hand-offs between unconnected providers.

Ready to move forward? Reach out to Expanship Monaco to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Société Anonyme Monégasque (SAM) is the most frequently chosen structure, primarily because it accommodates multiple shareholders, allows public capital-raising, and satisfies the requirements for regulated activities such as banking and insurance. Its defined governance framework under the Commercial Code also appeals to institutional investors and multinational groups establishing a presence in the Principality.

Both structures permit local commercial activity and are subject to Monaco's standard profit-based taxation regime. The SAM carries higher minimum capital requirements and mandatory auditing obligations, whereas a SARL operates with a simpler governance structure suited to closely held businesses with a smaller number of shareholders.

The SARL generally affords greater confidentiality, as detailed shareholder information is not routinely published in the same manner as for larger public-facing entities. Nominee arrangements are legally permissible, though all beneficial ownership disclosures must still be made to the relevant authorities under applicable anti-money laundering regulations.

Not all structures are available to a sole founder. A SARL can be formed by a single associate, but a Société en Nom Collectif requires at least two partners, and a Société en Commandite Simple requires at least one general partner alongside one limited partner.

Foreign nationals may incorporate a SAM or SARL, though all commercial activities require prior authorisation from the Direction du Développement Économique under Sovereign Ordinance No. 3.413. Non-residents must also demonstrate that the proposed activity meets specific economic contribution criteria before approval is granted.

Conversion is possible in limited circumstances, most notably from a SARL to a SAM once the business meets the applicable capital and shareholder thresholds. The process requires a formal resolution, updated articles of association, and re-registration with the Répertoire du Commerce et de l'Industrie.

The SAM, SARL, and SCS each carry separate legal personality, meaning the entity holds rights and obligations distinct from its members. The SNC does not provide this separation in the same way — general partners remain jointly and severally liable for all obligations of the firm.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.