Key Takeaways

- Under Monaco's Code de Commerce, all incorporation applications must be submitted to and approved by the Direction de l'Expansion Économique (DEE) before a company can legally operate in the Principality.

- Foreign investors structuring a SAM or SARL must satisfy a resident director requirement, which directly determines how governance arrangements are configured under Monegasque law.

- Every registered entity in Monaco must maintain a physical operational address within the Principality, as virtual or nominal office arrangements do not satisfy the registered office obligation.

- Beneficial ownership disclosure obligations apply as a distinct compliance layer, requiring identification and filing of ultimate beneficial owners with the relevant Monegasque authorities.

Entity formation in Monaco is governed by the Code de Commerce, with oversight from the Direction de l'Expansion Économique (DEE), the body responsible for reviewing and approving business registration applications.

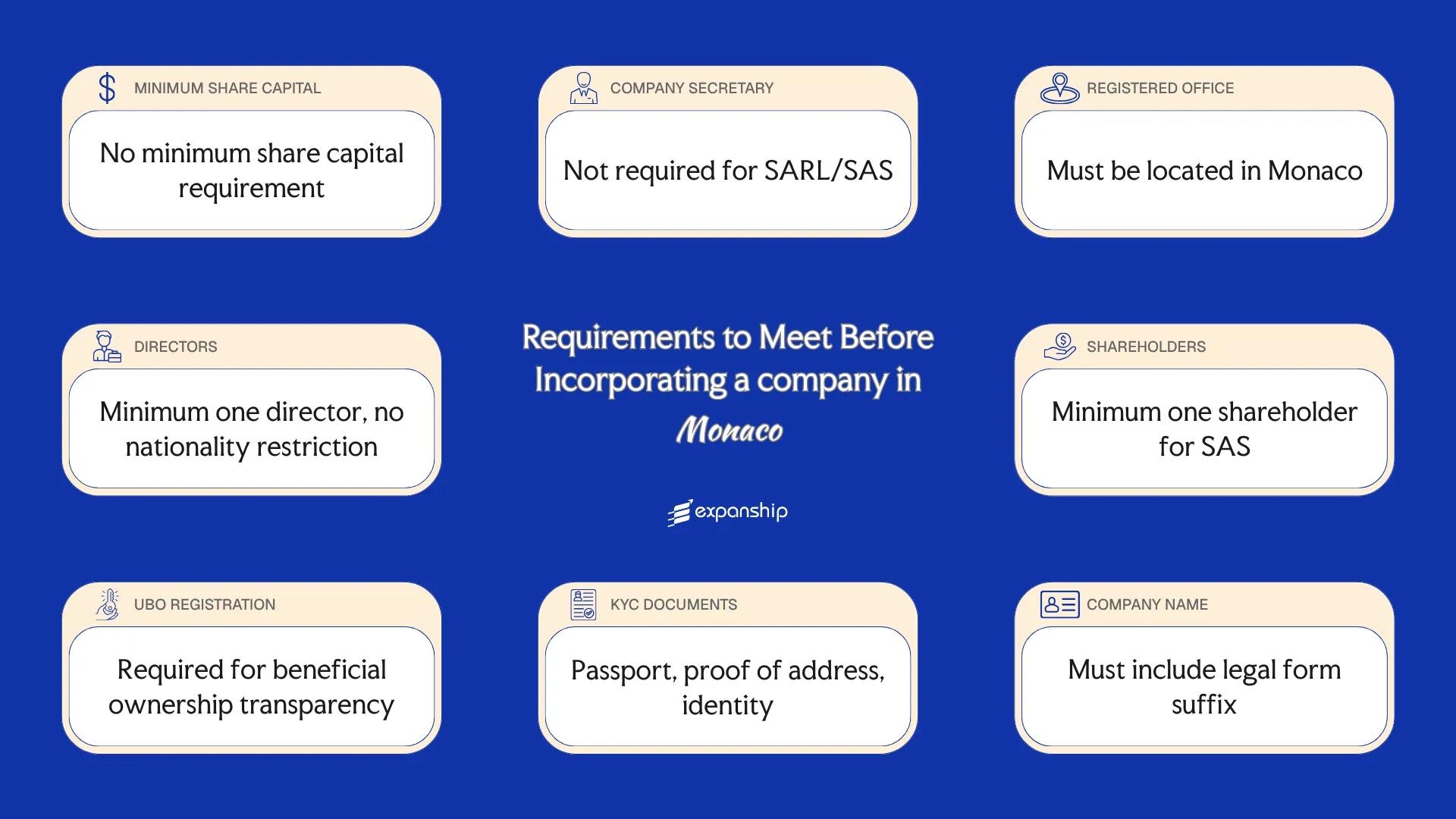

Satisfying Monaco incorporation requirements spans several distinct categories, from capital thresholds and directorship rules to registered office obligations and disclosure filings.

Failure to meet these requirements results in rejection of the application by the DEE, or in post-registration cases, potential suspension of operating authorization.

Requirements also differ depending on the legal form chosen, such as a Société Anonyme Monégasque (SAM) versus a Société à Responsabilité Limitée (SARL), as well as the sector your business intends to operate in.

This article is most relevant to foreign investors and business owners looking to establish a formal legal presence in the Principality for the first time.

Minimum Share Capital Requirements in Monaco

Monaco minimum share capital requirements differ by legal entity type, with the Société Anonyme Monégasque (SAM) and the Société à Responsabilité Limitée (SARL) subject to distinct thresholds set under Monegasque company law. Capital must be deposited into a blocked bank account prior to registration, and the Répertoire du Commerce et de l'Industrie de Monaco (RCI) verifies compliance before granting incorporation approval.

Share capital in Monaco operates on a par value system. Once deposited and confirmed, the capital obligation is a one-time incorporation requirement rather than a recurring statutory duty, though the authorised structure must remain consistent with the company's registered statutes.

| Parameter | Detail |

|---|---|

| Minimum Authorized Share Capital | EUR 150,000 for a SAM; EUR 15,000 for a SARL |

| Maximum Authorized Share Capital | No statutory maximum |

| Minimum Paid-Up Capital | 25% of the subscribed capital at incorporation for a SAM |

| Paid-Up Requirement at Incorporation | Partial payment permitted at formation; balance due within five years |

| Accepted Currency | Euro (EUR) |

| Accepted Forms of Contribution | Cash contributions; in-kind contributions subject to auditor valuation |

| Timeframe to Deposit Capital | Prior to filing with the RCI |

The full subscribed capital — not just the paid-up portion — must be referenced in the notarised statutes submitted to the RCI. Depositing only the paid-up minimum without properly documenting the total authorised amount in the founding documents will delay or invalidate registration.

Company Secretary Requirements in Monaco

Under Monaco corporate law, there is no statutory requirement for a dedicated company secretary in the same form as seen in common law jurisdictions. That said, Monaco company secretary requirements are fulfilled in practice through the obligations imposed on the société anonyme monégasque (SAM) and the société à responsabilité limitée (SARL) to maintain certain administrative and compliance functions, typically managed by a designated officer or external service provider.

Certain corporate governance duties must still be discharged, including maintaining statutory registers, preparing minutes of general meetings, and ensuring filings with the Répertoire du Commerce et de l'Industrie (RCI) remain current. Monaco company secretary compliance is therefore tied to the entity's ongoing administrative obligations rather than a formally titled role.

Qualification criteria for who may perform these functions:

- No separate licensing regime exists specifically for corporate secretaries in Monaco.

- A director, manager, or duly authorised officer of the company may assume the administrative role.

- External fiduciaries or corporate service providers operating under Monegasque law may be engaged.

- Any individual or entity must be capable of performing legal acts on behalf of the firm.

- Non-residents may serve, though local professional firms are commonly appointed for regulatory familiarity.

Incorporate a Company in Monaco

Set up your business entity in Monaco with structured guidance on legal form selection, registration with the RCI, and ongoing compliance management.

Registered Office Requirements in Monaco

Monaco registered office requirements mandate that every company maintain a physical address within the Principality, as set out under the Commercial Code and overseen by the Department of Economic Expansion (Direction de l'Expansion Économique).

- A physical address within Monaco is required; no foreign or virtual-only address is accepted.

- Virtual offices are not recognised as compliant registered office addresses under Monégasque company law.

- The address must be located within the Principality of Monaco; no cross-border arrangements satisfy this obligation.

- Proof of occupancy, such as a lease agreement or title document, must be provided to demonstrate legal entitlement to use the premises.

- The registered address is recorded in the Répertoire du Commerce et de l'Industrie (RCI) and is publicly accessible.

- Any change to the legal address requires formal notification to the RCI, typically accompanied by supporting documentation confirming the new premises.

Director Requirements in Monaco

Upon appointment, directors of a Monaco SAM (Société Anonyme Monégasque) assume statutory duties under the Code de Commerce de Monaco, including fiduciary obligations to the company and personal liability for management faults committed in the exercise of their functions.

| Parameter | Detail |

|---|---|

| Minimum Number of Directors | A minimum of three directors is required for an SAM. |

| Maximum Number of Directors | No statutory maximum is prescribed under Monaco company law. |

| Local/Resident Director Required | No statutory requirement mandates a resident director, though the board must convene in Monaco for certain decisions. |

| Nationality Restrictions | No nationality restrictions apply; foreign nationals may serve as directors. |

| Minimum Age Requirement | Directors must be at least 18 years of age. |

| Corporate Directors Permitted | Corporate directors are permitted under Monaco law. |

| Director Must Be a Shareholder | No statutory requirement obliges directors to hold shares in the company. |

| Publicly Listed on Registry | Director information is filed with the Répertoire du Commerce et de l'Industrie (RCI) and is a matter of public record. |

| Disqualification Conditions | Directors subject to bankruptcy proceedings or criminal convictions involving dishonesty may be disqualified from office. |

Unlike many jurisdictions that require at least one locally resident director, Monaco imposes no such residency obligation on any member of an SAM's board.

Shareholder Requirements in Monaco

A Monaco société anonyme monégasque (SAM) requires a minimum of two shareholders. No statutory maximum applies under Monégasque law, giving firms flexibility in their ownership structure.

Nationality and Residency Restrictions

Monaco shareholder requirements impose no mandatory residency or nationality conditions on shareholders of an SAM. Foreign nationals may hold shares without restriction on ownership percentage.

Corporate Shareholders

Corporate entities are permitted to act as shareholders in an SAM. The incorporating documentation must identify the corporate shareholder's legal form, registered address, and authorized representative.

Shareholder Liability

Shareholder liability is limited to the amount of capital each subscriber contributes. No general circumstances under Monégasque corporate law extend liability beyond that subscribed amount to personal assets.

Register of Shareholders

An SAM must maintain an internal register of shareholders recording ownership interests and any transfers. This register is not publicly accessible, though the company holds an obligation to keep it current and available for inspection by competent authorities.

Shareholder Structure Guidance for Your Monaco Incorporation

Get clarity on ownership configuration, shareholder documentation, and compliance obligations before you incorporate in Monaco.

UBO / Beneficial Ownership Disclosure Requirements in Monaco

Under Monaco's anti-money laundering framework, a beneficial owner is defined as any natural person who ultimately owns or controls 25% or more of a legal entity's shares or voting rights. The primary governing legislation is Law No. 1.362 of 3 August 2009 on combating money laundering, terrorist financing, and corruption, as amended.

- Identify all natural persons meeting the 25% ownership or control threshold before or at the point of incorporation.

- Disclose UBO information to the Service d'Information et de Contrôle sur les Circuits Financiers (SICCFIN), the Monegasque financial intelligence unit.

- Submit UBO declarations through the designated registration process within the timeframe required at formation.

- Report any change in beneficial ownership to SICCFIN promptly when it occurs.

| Parameter | Detail |

|---|---|

| Ownership Threshold for UBO Status | 25% of shares or voting rights |

| Filing Authority | SICCFIN |

| Disclosure Deadline at Incorporation | At or before incorporation |

| Publicly Accessible Register | No |

| Penalties for Non-Disclosure | Administrative and criminal sanctions under Law No. 1.362 |

| Ongoing Update Obligation | Yes; changes must be reported promptly to SICCFIN |

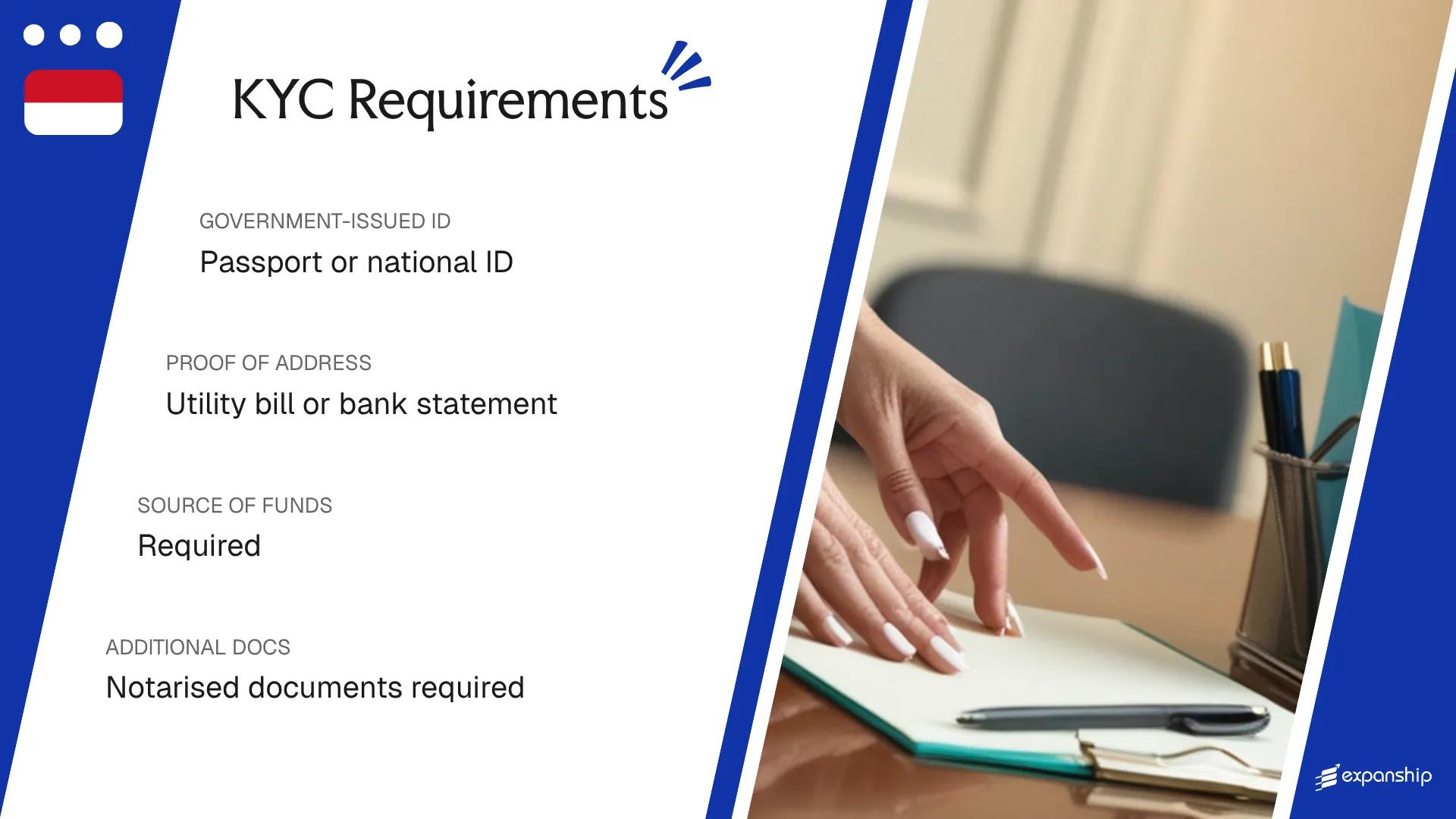

KYC / Document Requirements in Monaco

Monaco KYC document requirements apply at the point of incorporation and are governed by Law No. 1.362 of 3 August 2009 on the fight against money laundering, terrorist financing, and corruption, as amended. All parties connected to a new entity — directors, shareholders, and beneficial owners — must satisfy identification and verification checks before the Département des Affaires Juridiques processes the incorporation.

Individual / Personal Documents

- Valid government-issued photo identification (passport or national identity card)

- Proof of residential address dated within three months, such as a utility bill or bank statement

- Completed and signed KYC declaration form as required by the receiving notary or service provider

- Curriculum vitae or professional background summary may be requested for directors

Corporate Documents

- Certificate of incorporation or equivalent constitutional document from the entity's home jurisdiction

- Articles of association or bylaws in their current, up-to-date form

- Register of directors and register of shareholders certified as accurate

- Proof of the corporate entity's registered office address

Source of Funds Documentation

- Recent bank statements covering a minimum of three months

- Audited financial accounts or accountant-certified statements where bank statements are insufficient

- Documentary evidence explaining the specific origin of capital contributed to the new entity

Notarisation and Apostille Requirements

- Foreign public documents must carry an apostille under the Hague Convention of 5 October 1961

- Documents not in French require a sworn translation by a certified translator

- Notarisation by a local notaire may be required for documents executed within Monaco

The most common cause of incorporation delay is submitting address-verification documents that exceed the three-month validity threshold accepted by Monegasque authorities.

Company Name Requirements in Monaco

Monaco company name requirements are assessed by the relevant corporate authority at the point of incorporation, with each proposed name reviewed for availability and compliance before registration is confirmed. Names that duplicate or closely resemble an existing registered entity are rejected.

The firm's legal suffix must reflect the chosen corporate structure, such as "S.A.M." for a Société Anonyme Monégasque or "S.A.R.L.M." for a limited liability company. Business names must be in French, as it is the official language of the Principality.

Certain words implying state affiliation, royal connection, or regulated activities require prior approval from the relevant supervisory authority. Words suggesting banking, insurance, or financial services are subject to additional scrutiny.

Name reservation is available prior to formal incorporation, allowing you to secure a proposed name while preparing your application. The reservation period is time-limited, and the application is submitted directly to the corporate registration authority.

Corporate Compliance Services in Monaco

Maintain your company's standing in Monaco with ongoing compliance support, including annual filings, regulatory reporting, and statutory obligations.

Conclusion

Monaco incorporation requirements span several distinct legal and administrative conditions, each governed under the Monegasque commercial framework and overseen by the Direction de l'Expansion Économique. Among the more structurally significant conditions covered are the mandatory physical registered office, which must be a genuine operational address within the Principality, and the resident director requirement, which directly affects how foreign investors must structure their governance arrangements. Beneficial ownership disclosure obligations add a further compliance layer. Once these conditions are understood, the practical next step involves engaging qualified local professionals to manage the formation process with the relevant Monegasque authorities.

Expanship's Corporate Services for Monaco Expansion

Monaco's specific requirements, from minimum share capital thresholds to UBO disclosure obligations under the Direction des Services Fiscaux, create real administrative complexity for incoming businesses. Expanship's Monaco company formation services are structured to help your firm manage these requirements accurately and on time, reducing the operational burden without understating what incorporation here actually involves.

Beyond formation, our support covers the full lifecycle of your Monaco entity.

- We prepare and file all company registration documents with the Répertoire du Commerce et de l'Industrie on your behalf.

- Registered agent and local office provision is arranged to satisfy Monaco's physical presence requirements.

- Our team liaises directly with relevant government bodies throughout the filing process.

- Post-incorporation compliance obligations, including annual reporting, are tracked and managed on a continuing basis.

- Where needed, we facilitate introductions to Monaco-based banking institutions familiar with newly incorporated entities.

- Tax registration and liaison with the Direction des Services Fiscaux is handled as part of your setup.

Reach out to Expanship Monaco to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

Yes, the required share capital varies by entity type. A Société Anonyme Monégasque (SAM) requires a minimum of €150,000, while a Société à Responsabilité Limitée (SARL) requires €15,000. Choosing the wrong structure at incorporation can require a costly reconstitution of the entity, so the decision should be made with the final ownership and operational structure in mind.

Monaco imposes residency and nationality considerations on directors, particularly for SAMs where at least one director is typically required to have ties to the Principality or an approved jurisdiction. Corporate directors may be permitted depending on the entity type, but this is subject to review by the DEE during the authorisation process. Foreign nationals serving as directors may also need to satisfy additional administrative conditions.

Failure to comply with Monaco's beneficial ownership disclosure obligations, governed under Law No. 1.362 of 3 August 2009 on anti-money laundering and counter-terrorism financing as amended, can result in administrative sanctions and fines imposed by the Autorité Monégasque de Sécurité Financière (AMSF). Persistent non-compliance can lead to the suspension or revocation of the company's operating authorisation. Monaco's AMSF has enforcement powers that extend to both the entity and its officers.

A foreign national can hold shares in a Monaco company, but the Principality's authorisation process requires government approval through the DEE regardless of shareholder residency. For an SAM, shares may be held by foreign investors, but the overall structure — including the identity and background of all shareholders — is subject to scrutiny during the incorporation authorisation process. Beneficial ownership must also be disclosed, and any nominee arrangements do not eliminate the disclosure obligation.

Monaco's KYC requirements are stricter than many comparable jurisdictions in terms of the depth of due diligence applied, reflecting its obligations under FATF recommendations and EU-equivalent AML standards despite not being an EU member state. Certified and apostilled documentation is typically required for foreign-sourced identity and address documents, and source-of-funds evidence is standard for all incorporations. The DEE and notary involved in the process both conduct independent checks, meaning documentation is reviewed at multiple stages.

A post-incorporation name change in Monaco requires an amendment to the company's statutes, which must be approved by an extraordinary general meeting and submitted to the DEE for authorisation. The change must also be registered with the Répertoire du Commerce et de l'Industrie (RCI) and published in the Journal de Monaco. This process involves notarial involvement and can take several weeks, making the initial name selection an important practical decision.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.