Key Takeaways

- Morocco's most widely used business structure is the SARL, governed by Law 5-96, which permits single-shareholder formation and limits member liability to capital contributions.

- The SA, regulated under Law 17-95, is the appropriate structure for larger enterprises seeking public capital access or institutional investment in Morocco.

- Commercial entity registration in Morocco is administered through OMPIC, which maintains the Registre de Commerce and serves as the central registration authority.

- Foreign companies can establish a local presence through a branch, representative office, or liaison office, none of which carry separate legal personality under Moroccan law.

Introduction to Entity Types in Morocco

Morocco sits in northwestern Africa, bordered by Algeria to the east, Mauritania to the south, and the Atlantic Ocean and Mediterranean Sea to the west and north. It is an independent constitutional monarchy and a member of the Arab League and the African Union. Company registration falls under the jurisdiction of the Office Marocain de la Propriété Industrielle et Commerciale (OMPIC), which maintains the Registre de Commerce and serves as the central point for commercial entity registration.

The country operates a territorial tax system, meaning foreign-sourced income is generally not subject to Moroccan corporate tax.

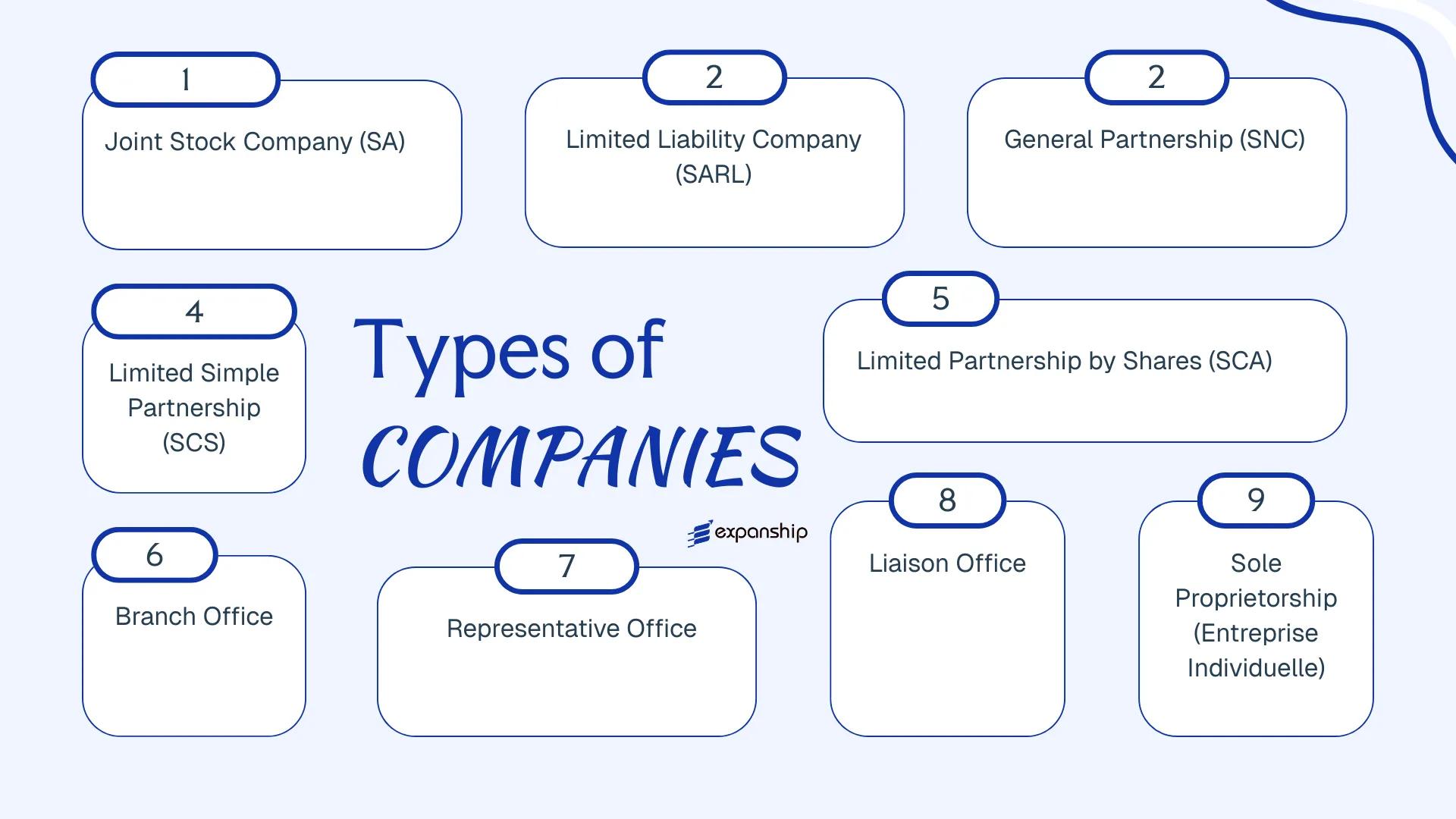

Choosing among the types of business entities in Morocco requires an understanding of how each structure differs in terms of liability, governance, and regulatory obligations. The main Moroccan legal entity structures available to investors and entrepreneurs include the Société Anonyme (SA), Société à Responsabilité Limitée (SARL), Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA), branch office, representative office, liaison office, and the Entreprise Individuelle. This article examines each of these business entity options in Morocco, covering their legal requirements, formation procedures, and practical considerations.

An Overview of Business Structures in Morocco

Morocco's company law framework provides several distinct entity types, each governed primarily by the law of 5 August 1996 on limited liability companies, the law of 17 August 1996 on public limited companies, and related provisions of the Code de Commerce. These structures range from closely held private firms to publicly listed corporations, sole proprietorships, and foreign commercial presences. Each form carries different rules on liability, governance, and capital, which the sections below address individually.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Legislation |

|---|---|---|---|---|---|---|---|

| SA | Public limited company | Limited to shares | Corporate tax liable | Permitted | 5 shareholders | OMPIC / RC | Law 17-95 |

| SARL | Private limited company | Limited to contributions | Corporate tax liable | Permitted | 1 member | OMPIC / RC | Law 5-96 |

| SNC | General partnership | Unlimited, joint | Corporate tax liable | Permitted | 2 partners | OMPIC / RC | Code de Commerce |

| SCS | Simple limited partnership | Mixed liability | Corporate tax liable | Permitted | 2 partners | OMPIC / RC | Code de Commerce |

| SCA | Partnership limited by shares | Mixed liability | Corporate tax liable | Permitted | 4 partners | OMPIC / RC | Code de Commerce |

| Branch Office | Extension of foreign entity | Parent liable | Corporate tax liable | Permitted | 1 parent entity | OMPIC / RC | Code de Commerce |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | Not permitted | 1 parent entity | Office des Changes | Code de Commerce |

| Entreprise Individuelle | Sole proprietorship | Unlimited personal | Income tax liable | Permitted | 1 individual | RC | Code de Commerce |

Each of these structures is examined in full in the sections below.

Société Anonyme (SA) — Joint Stock Company

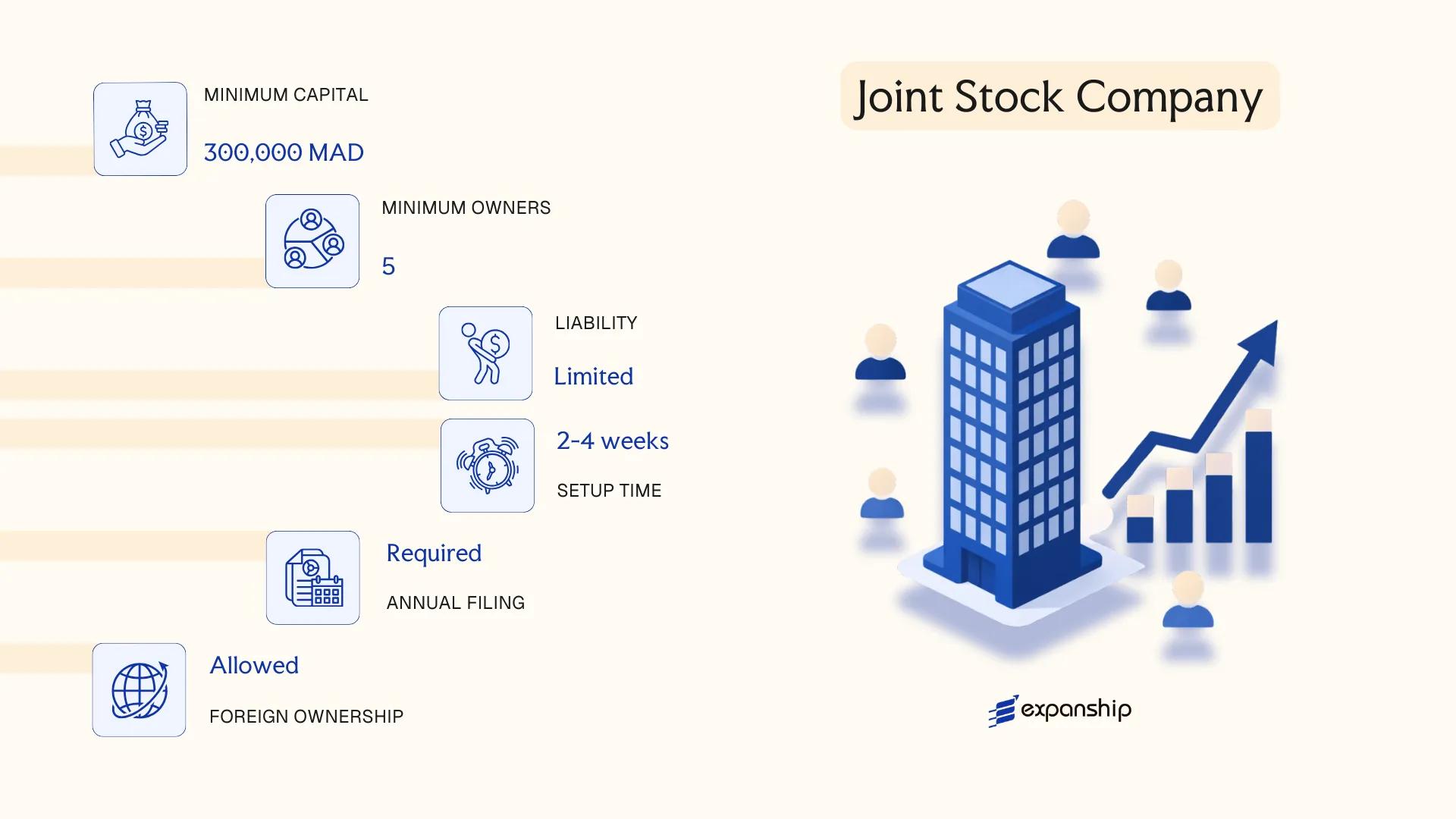

Governed by Law No. 17-95 on Joint Stock Companies, as amended by Law No. 20-05 and subsequently Law No. 78-12, the Société Anonyme is the primary corporate vehicle for large-scale commercial operations in Morocco. Société Anonyme SA Morocco registration produces a legal entity with full separate personality, meaning the company holds rights and obligations in its own name.

Shareholders bear no personal liability beyond their capital contributions. The structure supports public and private capital-raising, making it the standard choice for firms seeking institutional investment or eventual stock exchange listing on the Bourse de Casablanca.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (SA) | Separate legal personality; shareholders not liable for company debts |

| Governance | Board of Directors or Supervisory Board + Management Board | Two governance models permitted under Law 17-95 |

| Shareholders | Minimum 5; no statutory maximum | Applies to both private and publicly listed SAs |

| Capital | MAD 300,000 (private); MAD 3,000,000 (public/listed) | 25% must be paid up at incorporation; remainder within 5 years |

| Local Presence | Registered office in Morocco required | Physical address; no mandatory local director under general rules |

| Share Transferability | Freely transferable; restrictions possible via bylaws | Listed shares trade on the Bourse de Casablanca |

Focus Points

- Taxation: Subject to corporate income tax at progressive rates up to 35% (from 2023 reforms); standard VAT at 20% applies to taxable supplies; dividend withholding tax at 15% for non-residents, reducible under applicable double tax treaties; stamp duties apply to certain capital contributions.

- Annual Compliance: Mandatory statutory audit by a Commissaire aux Comptes (registered auditor); annual general meeting required; audited financial statements filed with the Tribunal de Commerce.

- Treaty Access: Morocco's tax treaty network covers 50+ countries; SA entities qualify as resident entities for treaty purposes.

- Conversion: An SA may convert to an SARL or other form by shareholder resolution, subject to compliance with applicable capital thresholds and court registration.

- Restrictions: Certain regulated sectors (banking, insurance, telecoms) require sector-specific licensing from authorities such as Bank Al-Maghrib or the ANRT, independent of corporate registration.

Closing

The SA suits holding structures, large trading operations, and businesses targeting Moroccan institutional investors or preparing for a public offering. The mandatory minimum of five shareholders and the statutory audit requirement add administrative overhead that smaller businesses may find disproportionate to their needs.

The SA is best suited for large enterprises, joint ventures with multiple investors, and businesses planning to raise capital through the Bourse de Casablanca.

Company Incorporation in Morocco

Incorporate a Société Anonyme or other business entity in Morocco with end-to-end support from Expanship.

Société à Responsabilité Limitée (SARL) — Limited Liability Company

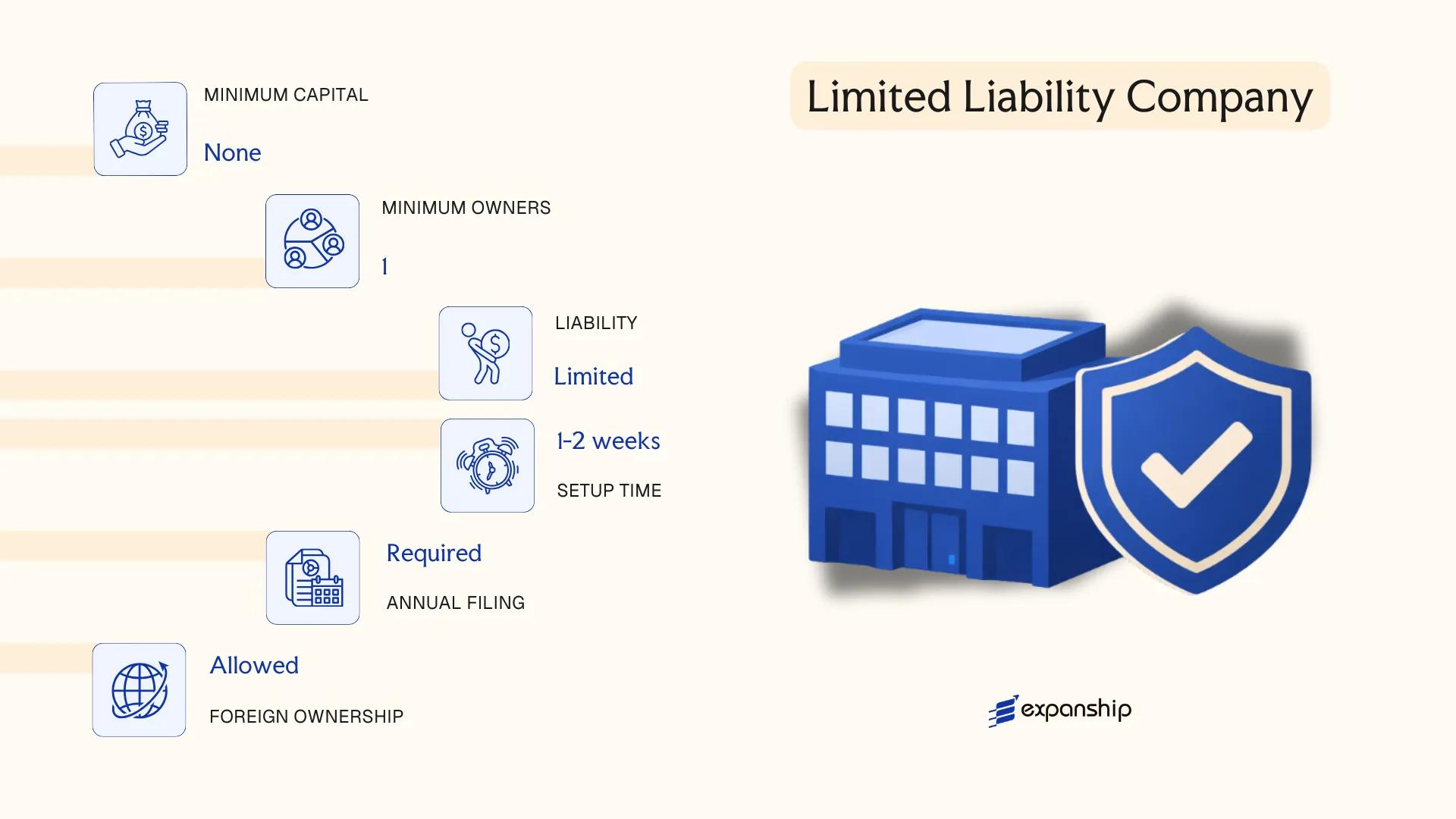

The SARL is governed by Law No. 5-96 on commercial companies, as amended, and represents the most widely used structure for SARL company formation Morocco. It carries separate legal personality, meaning the entity holds rights and obligations distinct from its members, and liability is capped at each member's capital contribution.

Structurally, the Société à Responsabilité Limitée Morocco sits between a partnership and a full joint stock company — flexible enough for small to mid-sized operations, yet sufficiently formal for regulated activities and foreign investment.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Separate legal personality; hybrid structure |

| Members | 1–50 associates | Single-member variant (SARL-AU) permitted |

| Management | One or more gérants (managers) | Need not be Moroccan nationals |

| Share Capital | MAD 10,000 minimum (general); MAD 100,000 for certain regulated activities | No par value floor per share specified by statute |

| Local Presence | Registered office address required in Morocco | No statutory requirement for a resident agent |

| Privacy | Associates' names filed with the OMPIC and Tribunal de Commerce | Register is publicly accessible |

Focus Points

- Taxation: Subject to corporate income tax at progressive rates (10%–35% depending on net profit), 20% VAT where applicable, and withholding tax on dividends distributed to non-residents, generally at 15% unless a tax treaty reduces this rate.

- Annual Compliance: Audited financial statements are mandatory only once turnover or headcount exceeds statutory thresholds; below those thresholds, a commissaire aux comptes is not required.

- Treaty Access: Morocco limited liability company SARL entities are eligible for benefits under Morocco's network of over 50 bilateral tax treaties, subject to substance and residency conditions.

- Conversion: An SARL may be converted into an SA once it meets the minimum capital and shareholder requirements under Law No. 17-95.

- Restrictions: Shares in an SARL are not freely transferable to third parties without the consent of associates holding at least three-quarters of the share capital.

Sub-Types

SARL-AU (Associé Unique)

The SARL-AU is a single-member variant permitting one individual or legal entity to hold the entire share capital. It is commonly used by foreign investors establishing a wholly owned subsidiary or by entrepreneurs structuring a sole-owned trading or service business.

Closing

The SARL suits trading companies, service businesses, and wholly owned subsidiaries where operational control and liability protection are both priorities; its principal limitation is the restriction on free share transfer, which can complicate equity raises or investor exits.

Best suited for foreign investors and SMEs seeking a straightforward, wholly owned operational presence with capped liability and manageable compliance obligations.

Société en Nom Collectif (SNC) — General Partnership

The Société en Nom Collectif Morocco SNC is governed by Law No. 5-96 on commercial companies, which also regulates several other non-SA entity forms. Unlike a SARL or SA, the SNC carries no limited liability protection for its partners.

All partners bear unlimited, joint, and several liability for the firm's debts, meaning personal assets are exposed to creditors without restriction. The entity does possess separate legal personality upon registration with the Regional Court of Commerce.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société en Nom Collectif (SNC) | Commercial entity with separate legal personality |

| Members | referred to as "associés" (partners); minimum 2, no statutory maximum | All partners hold trader (commerçant) status by default |

| Liability | Unlimited, joint and several for all partners | Personal assets are fully exposed to business debts |

| Capital | No minimum capital requirement; denominated in Moroccan Dirham (MAD) | Capital divided into parts sociales, not freely transferable |

| Local Presence | Registered office in Morocco required | Must be registered with the relevant Regional Court of Commerce |

| Privacy | Partner names publicly disclosed in the commercial register | The firm's name typically includes partner surnames |

Focus Points

- Taxation: Subject to corporate income tax (IS) at standard rates, or optionally taxed at the partner level under income tax (IR) if all partners are individuals; VAT applies to taxable supplies; withholding tax applies on dividends distributed.

- Transfer restrictions: Parts sociales require unanimous partner consent for transfer, making ownership changes operationally cumbersome.

- Annual compliance: Filing of annual financial statements with the Tribunal de Commerce is required; accounting obligations apply under the Moroccan General Chart of Accounts (CGNC).

- Conversion: An SNC can be converted to a SARL or SA by resolution, subject to compliance with applicable capital and membership requirements of the target form.

- Treaty access: As a Moroccan-resident entity, the SNC can access Morocco's tax treaty network, subject to conditions specific to the applicable convention.

Closing

The SNC suits small, closely-held businesses where partners have strong mutual trust and prefer a simple governance structure without minimum capital constraints. The absence of a capital floor reduces setup friction, but unlimited personal liability is a significant structural risk for any partner with substantial personal assets.

Best suited for two or more individuals operating a closely-held professional or family business who accept full personal liability and require minimal structural formality.

Société en Commandite (SCS, SCA) — Limited Partnership [Limited Simple Partnership, Limited Partnership by Shares]

Governed by Law No. 5-96 on General Partnerships, Limited Partnerships, and Joint Ventures, the limited partnership Morocco SCS SCA structure divides members into two distinct categories: general partners (associés commandités) who bear unlimited personal liability, and limited partners (associés commanditaires) whose exposure is capped at their capital contribution. Both the Société en Commandite Simple (SCS) and the Société en Commandite par Actions (SCA) carry separate legal personality under Moroccan law.

Registration is handled through the Regional Investment Centers (CRI) and requires entry in the Register of Commerce (Registre du Commerce) at the relevant tribunal de commerce.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Partnership (Simple or by Shares) | Two recognised sub-types under Law No. 5-96 |

| Members | Min. 1 general partner + 1 limited partner; SCA requires min. 3 limited partners | General partners have unlimited liability; limited partners are passive investors |

| Local Presence | Registered office in Morocco required | No statutory requirement for a resident agent |

| Capital | No statutory minimum for SCS; SCA requires MAD 300,000 minimum | SCA capital is divided into negotiable shares |

| Privacy | Partner names appear in Registre du Commerce | No public register of beneficial ownership currently mandated |

Focus Points

- Taxation: Subject to corporate income tax (IS) at standard rates (20%–35% progressive), VAT where applicable, and withholding tax on profit distributions to non-resident partners.

- Annual Compliance: Annual financial statements must be filed; SCA is subject to statutory audit requirements similar to those of an SA.

- Restrictions: General partners cannot limit their personal liability; limited partners who participate in management risk losing their liability shield.

- Conversion: An SCS may be converted to an SCA or other recognised form through a formal deed and amendment to the Registre du Commerce.

Sub-Types

Société en Commandite Simple (SCS)

The SCS does not divide its capital into tradeable shares, making partner interest transfers subject to unanimous consent unless the articles provide otherwise. It suits closely-held ventures where partners want flexible governance without public share issuance.

Société en Commandite par Actions (SCA)

The SCA Morocco limited partnership by shares issues negotiable shares held exclusively by limited partners, allowing capital to be raised from a wider investor base while general partners retain management control. This structure is used primarily for investment vehicles and family holding arrangements requiring a degree of investor liquidity.

Recommendations

Both forms suit investment holding structures or family businesses where separation between active management and passive capital participation is commercially necessary, though the unlimited liability of general partners remains a material structural constraint that must be addressed through careful drafting of the partnership deed.

This entity type is most appropriate for investors or family groups seeking passive participation in a managed business without direct operational exposure, provided at least one party is prepared to accept unlimited liability as general partner.

Foreign Business Presence in Morocco [Branch Office, Representative Office, Liaison Office]

Registering a foreign company branch office Morocco requires compliance with Law No. 15-95 (the Commercial Code) and, where relevant, the Foreign Exchange Office (Office des Changes) regulations governing capital movements. Unlike locally incorporated entities, a branch has no separate legal personality — it remains an extension of the parent company, which bears full liability for its operations.

Representative and liaison offices occupy a more restricted position. Neither structure is permitted to generate revenue from Moroccan clients; both exist solely to support the foreign parent through market research, promotion, or coordination activities.

Key Characteristics

| Requirement | Branch Office | Representative / Liaison Office |

|---|---|---|

| Legal Personality | None (extension of parent) | None (extension of parent) |

| Commercial Activity | Permitted | Not permitted |

| Capital Requirement | No statutory minimum | None |

| Local Presence | Registered address in Morocco required | Registered address required |

| Registration Body | Regional Investment Centre (CRI) + Trade Register | Office des Changes (for liaison offices) / CRI |

| Liability | Parent company bears full liability | Parent company bears full liability |

Focus Points

- Taxation: Branch profits are subject to Corporate Tax (IS) at standard rates; VAT applies to taxable supplies; withholding tax applies to royalties and service fees remitted abroad under domestic rules, subject to treaty relief.

- Treaty Access: Morocco's tax treaty network may provide reduced withholding rates, but treaty eligibility for branches depends on the specific convention.

- Annual Compliance: Branches must file annual financial statements with the Trade Register and submit corporate tax returns to the Direction Générale des Impôts.

- Restrictions: Representative and liaison offices cannot invoice locally, sign commercial contracts on their own account, or repatriate profits.

- Conversion: A branch can be converted into a locally incorporated entity (such as a SARL or SA), though this involves a separate incorporation process rather than a simple administrative transformation.

Sub-Types

Branch Office

A branch conducts commercial operations in Morocco on behalf of the foreign parent and must be registered in the local Trade Register (Registre de Commerce). It can execute contracts and generate local revenue, but all obligations flow back to the parent.

Representative Office

Established primarily through registration with the Office des Changes, a representative office is limited to non-commercial functions — promoting the parent's products or services without concluding transactions directly.

Liaison Office

Functionally similar to a representative office, a liaison office is used specifically for coordination and communication between the parent and local counterparties, with no authority to conduct revenue-generating activity.

A foreign business presence suits multinationals testing the market before committing to full incorporation, with the branch offering the fastest path to operational activity. The primary drawback is parent-level liability exposure, with no corporate veil separating the Moroccan operations from the foreign entity.

Foreign firms seeking an operational footprint without local incorporation — particularly those in sectors requiring direct commercial activity under the parent's existing regulatory standing.

Entreprise Individuelle — Sole Proprietorship

The Entreprise Individuelle is the simplest business structure available under Moroccan law, governed by the general provisions of the Code de Commerce. Unlike capital-based entities, it carries no separate legal personality — the individual and the business are treated as one. This means your personal assets remain directly exposed to business liabilities.

Registration is handled through the Centre Régional d'Investissement (CRI) or the Office Marocain de la Propriété Industrielle et Commerciale (OMPIC), depending on the activity type. The sole proprietorship Morocco registration process is relatively straightforward, with no minimum capital requirement and no formal articles of association.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated individual enterprise | No separate legal personality from the owner |

| Member Title | Proprietor (Exploitant individuel) | Single individual only; no partners or shareholders |

| Members | 1 (minimum and maximum) | Cannot admit additional members; must convert to convert a company form to expand ownership |

| Local Presence | Registered business address required | Must maintain a declared principal place of business in Morocco |

| Capital | No minimum capital | No paid-up or authorized capital requirement |

| Liability | Unlimited personal liability | Personal assets are exposed to all business debts |

Focus Points

- Taxation: Subject to Impôt sur le Revenu (IR) on net profit at progressive rates up to 38%; VAT obligations apply based on turnover thresholds; no corporate income tax applies.

- Annual Compliance: Must file an annual income tax return with the Direction Générale des Impôts (DGI); bookkeeping obligations vary by revenue category.

- Treaty Access: As an unincorporated entity, access to Morocco's double tax treaty network is limited compared to corporate structures.

- Conversion: Can be converted into an SARL or other corporate form, though this requires a full re-registration process rather than a simple structural amendment.

- Restrictions: Foreign nationals face restrictions on operating as sole proprietors; reciprocity conditions and residency requirements typically apply.

Closing Paragraph

The Entreprise Individuelle suits resident Moroccan nationals running low-volume, single-operator businesses such as small trade, artisanal work, or freelance services, where administrative simplicity outweighs the need for liability protection. The primary drawback is unlimited personal liability, which makes it unsuitable for activities carrying significant financial or legal risk.

This structure is best suited for resident Moroccan nationals conducting small-scale, low-risk commercial or professional activities who prioritise minimal setup costs over liability protection.

How to Choose the Right Entity Type in Morocco

Selecting the correct legal structure is a foundational decision that shapes your tax position, liability exposure, and operational capacity for the life of the business. Understanding how to choose a business structure in Morocco requires examining several concrete factors before filing anything with the Centre Régional d'Investissement (CRI) or the tribunal de commerce.

Why Your Entity Choice Matters

The structure you register has binding consequences that are difficult and costly to reverse.

- Selecting a structure without separate legal personality — such as an SNC — means personal assets remain fully exposed to business creditors, with no liability shield available.

- Forming an SA when your business has a single owner and modest revenue creates mandatory audit obligations and minimum capital requirements that do not apply to a SARL.

- Establishing a branch office when you intend to conduct sustained independent commercial activity may not satisfy the requirements for a locally incorporated entity under Moroccan commercial law, creating compliance gaps with the Office des Changes.

- Choosing a structure ineligible under a specific bilateral tax treaty means withholding tax reductions available to qualifying Moroccan-resident entities cannot be claimed.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors such as banking or insurance, and passive asset holding each point to distinct entity types under Moroccan commercial legislation.

- Ownership Structure: A sole founder typically fits a SARL unipersonnelle, while multi-investor ventures requiring formal governance lean toward an SA.

- Capital Requirements: Your available capital at formation directly limits which structures are accessible, given that an SA carries a statutory minimum that a SARL does not.

- Tax Position: Whether your firm needs access to Morocco's treaty network, a specific territorial tax regime, or full liability for corporate tax affects the appropriate structure.

- Liability Exposure: The degree to which personal assets must be shielded from commercial risk determines whether a partnership form is acceptable at all.

- Exit and Conversion: Not all entity types permit straightforward redomiciliation or conversion, so your anticipated exit route should influence the initial choice.

Compliance Services for Companies in Morocco

Maintain good standing with Moroccan regulatory requirements, including annual filings, accounting obligations, and reporting to the relevant authorities.

Conclusion

Morocco's regulatory framework offers a defined set of structures to match different operational profiles. This Morocco company incorporation conclusion guide reflects a system shaped primarily by the law governing SARLs (Law 5-96) and SAs (Law 17-95), with oversight from the registre du commerce and filings processed through the tribunaux de commerce.

The SARL remains the most registered entity type, favored by SMEs and foreign investors alike for its single-shareholder option and capped liability. The SA suits larger enterprises requiring public capital access or institutional investment. An SNC places full liability on partners, making it appropriate only where trust between associates is absolute. Commandite structures serve niche financing arrangements. Branch and liaison offices give foreign firms a local footprint without separate legal personality.

Your choice of structure determines tax treatment, governance obligations, and long-term compliance requirements under Moroccan law. Ongoing reforms and expanding tax treaty networks continue to shape the country's standing as a regional business hub.

How Expanship Can Assist You

Expanship Morocco company formation services cover the full arc of establishing a legal presence in the country — from selecting between an SA, SARL, or SNC to registering your entity with the Registre de Commerce at the Tribunal de Commerce. Our team works directly with the Centre Régional d'Investissement (CRI) and other relevant authorities to keep your registration on track from day one.

Across Morocco business setup assistance, we handle the administrative and compliance work so your focus stays on operations:

- Document preparation, legalization, and apostille coordination

- Registered agent and registered office provision

- Filing with the Registre de Commerce and liaison with the CRI

- Post-incorporation compliance management, including annual obligations

- Corporate tax registration with the Direction Générale des Impôts

- Banking introduction assistance for local account opening

Get in touch with Expanship Morocco to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The Société à Responsabilité Limitée (SARL) is by far the most frequently registered structure, primarily because it combines limited liability with a comparatively low minimum share capital and a straightforward governance framework. Its suitability for small and mid-sized enterprises, as well as single-member formation through the SARL AU variant, makes it the default choice for most new businesses.

A Branch Office is not a separate legal entity — it remains an extension of its foreign parent and is taxed in Morocco only on locally sourced income, though it carries no liability shield between the parent and local operations. A SARL, by contrast, is a distinct legal person under Moroccan law, subject to corporate income tax on its global Moroccan-source profits, and it requires compliance with annual filing obligations to the Tribunal de Commerce. The SARL offers greater operational independence and a cleaner separation of liability.

Among standard commercial structures, the SARL offers relatively limited public disclosure compared to the SA, since it is not required to publish financial statements in the same manner as a publicly held firm. Beneficial ownership information is, however, subject to disclosure requirements under anti-money laundering regulations administered by the Autorité Marocaine du Marché des Capitaux (AMMC) and related bodies. Nominee arrangements are not a formally recognized mechanism under Moroccan corporate law.

No. The SARL AU permits single-member formation, but a standard SARL requires at least two shareholders and a maximum of fifty. An SA requires a minimum of five shareholders, while a Société en Nom Collectif (SNC) and Société en Commandite (SCS) each require at least two partners by definition. Sole traders operate separately as an Entreprise Individuelle, which carries no liability separation.

Foreign individuals and entities may incorporate a SARL, SA, or establish a Branch Office without restrictions on nationality under Moroccan investment law. Foreign ownership of up to 100% is permitted in most sectors, with exceptions in agriculture and certain regulated industries. Registration is processed through the Centre Régional d'Investissement (CRI), which serves as the primary entry point for foreign investors.

Conversion between entity types is permitted under Moroccan commercial law. A SARL may be converted into an SA once it meets the relevant shareholder and capital thresholds, typically when the company grows and seeks to access capital markets or expand its shareholder base. The process requires a notarial deed, approval by the existing shareholders, and re-registration with the Tribunal de Commerce.

Not all of them. The SA, SARL, SCA, and SCS en commandite par actions each hold distinct legal personality separate from their members. The SNC, while registered, exposes partners to joint and unlimited liability, and the Entreprise Individuelle carries no separation between the business and its owner. A Branch Office, as noted, remains legally inseparable from its foreign parent company.

The Entreprise Individuelle carries the lightest administrative burden, with no board requirements, no statutory audit, and simplified tax reporting. However, this comes at the cost of unlimited personal liability. Among limited liability structures, the SARL AU imposes fewer governance formalities than the SA, which is subject to statutory audit requirements and mandatory disclosure obligations under Law No. 17-95.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.