Key Takeaways

- Foreign investors incorporating in Morocco must satisfy share capital, director, and beneficial ownership disclosure obligations before the registration application can be accepted by the Regional Investment Centers (CRI) or OMPIC.

- Under Law No. 17-95 and Law No. 5-96, the chosen entity type — whether a Société Anonyme (SA), Société à Responsabilité Limitée (SARL), or foreign branch — determines which specific structural and documentary requirements apply.

- Beneficial ownership disclosure is a mandatory compliance obligation from the moment of formation, formalized under Morocco's Anti-Money Laundering legislation and not an optional post-registration step.

- Notarization and coordination with the Registre de Commerce are procedural requirements that must be completed within prescribed timelines, making early engagement with a notary a compliance necessity rather than an administrative convenience.

Entity formation in Morocco is governed by Law No. 17-95 on Public Limited Companies and Law No. 5-96 on Other Business Companies, with registration administered through the Regional Investment Centers (CRI) and the Office Marocain de la Propriété Industrielle et Commerciale (OMPIC). Meeting the full set of incorporation requirements in Morocco is a prerequisite for obtaining legal standing as a registered business.

This article covers the structural, documentary, and regulatory requirements that apply across the formation process, as defined under Moroccan company law. Failure to satisfy these requirements results in rejection of the registration application or, in cases of post-registration non-compliance, exposure to administrative penalties and potential deregistration.

Requirements differ depending on whether the entity is a Société Anonyme (SA), Société à Responsabilité Limitée (SARL), or a branch of a foreign company. Sector-specific regulations and the investor's residency status can also affect applicable obligations.

This article is most relevant to foreign investors and business owners evaluating Morocco company formation requirements prior to establishing a commercial presence in the country.

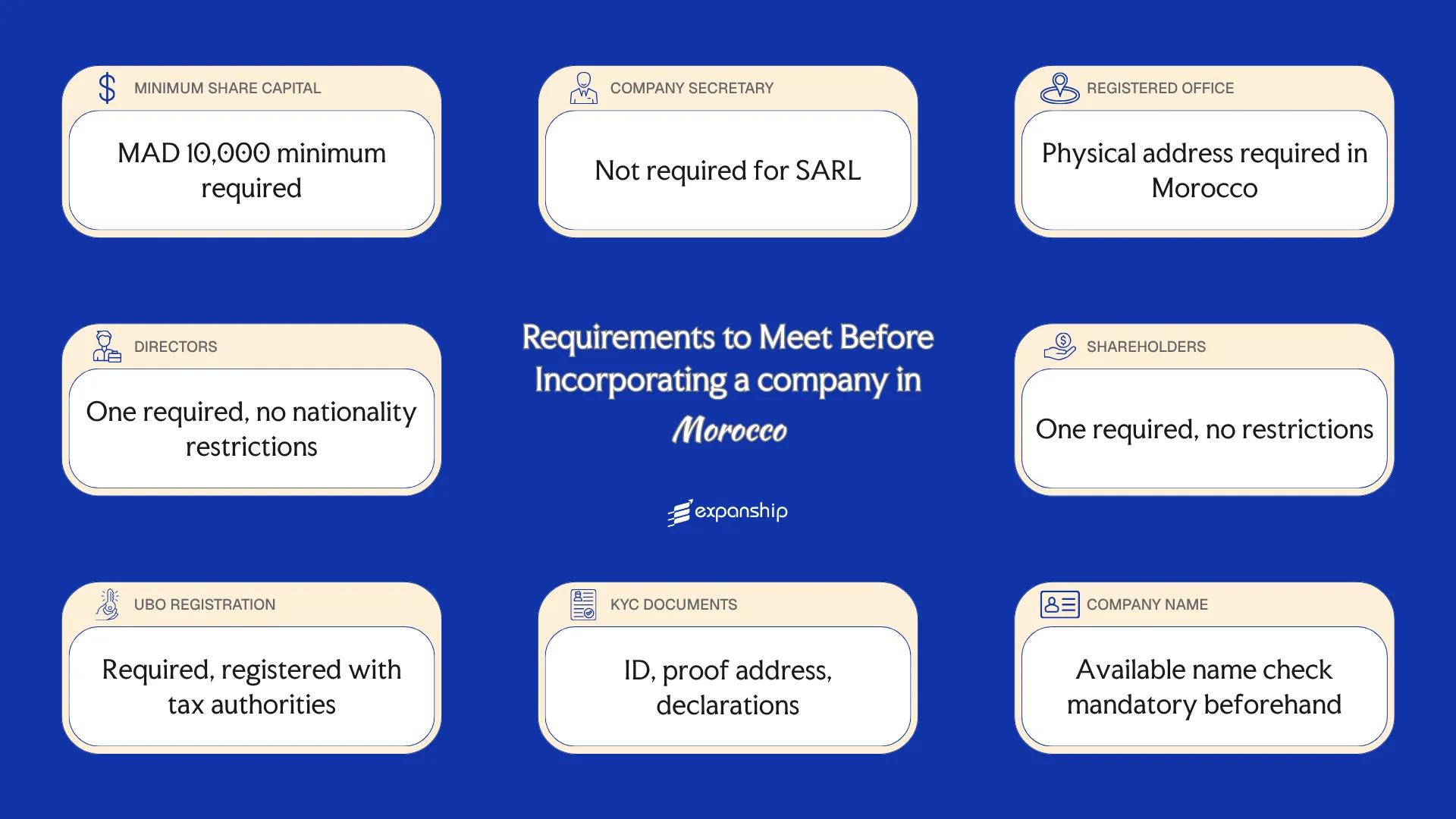

Minimum Share Capital Requirements in Morocco

Morocco minimum share capital requirements differ by entity type and are governed by the Code Général des Sociétés. The Centre Régional d'Investissement (CRI) and the relevant tribunal de commerce oversee the registration process, while a licensed bank account is used to deposit and certify paid-up capital before incorporation is finalized.

For a Société Anonyme (SA), the statutory minimum is MAD 300,000 for privately held companies and MAD 3,000,000 for those making a public offering of shares. SARL capital requirements in Morocco carry no statutory minimum following reforms that reduced the threshold to MAD 1, though the structure must still reflect a defined authorized capital in the articles of association.

| Parameter | Detail |

|---|---|

| Minimum Authorized Share Capital | MAD 1 for SARL; MAD 300,000 for SA (private); MAD 3,000,000 for SA (public offering) |

| Maximum Authorized Share Capital | No statutory requirement |

| Minimum Paid-Up Capital | MAD 1 for SARL; MAD 300,000 for SA (private) |

| Paid-Up Requirement at Incorporation | SARL: full amount; SA: minimum one-quarter of cash contributions at incorporation |

| Accepted Currency | Moroccan Dirham (MAD) |

| Accepted Forms of Contribution | Cash and in-kind contributions; in-kind assets require auditor valuation for SA |

| Timeframe to Deposit Capital | SA: remaining cash balance must be paid up within three years of incorporation |

For an SA, only 25% of cash contributions must be deposited at incorporation, but the remaining 75% must be fully paid up within three years. Failure to meet this timeline constitutes a statutory breach under the Code Général des Sociétés.

Company Secretary Requirements in Morocco

Under Morocco company secretary requirements, there is no statutory obligation to appoint a company secretary for a Société à Responsabilité Limitée (SARL) or most other standard business forms. Corporate governance functions are instead distributed among the gérant (manager) and, where applicable, the supervisory bodies established under the company's articles of association.

The gérant holds primary responsibility for maintaining statutory registers, filing annual accounts with the Tribunal de Commerce, and ensuring regulatory submissions reach the relevant authorities. Morocco corporate secretary obligations, where they arise in larger structures such as a Société Anonyme (SA), are typically assigned to the board or a designated officer rather than a formally titled secretary.

Qualification criteria for any person or entity fulfilling secretarial or equivalent governance functions:

- No statutory licensing requirement exists for individuals performing secretarial duties in a SARL.

- In an SA, the board secretary is generally an officer appointed internally, with no mandatory professional qualification prescribed by law.

- Both Moroccan nationals and foreign individuals may serve in this capacity.

- Corporate entities can be assigned governance support functions, subject to the company's internal statutes.

- No residency requirement is imposed on individuals fulfilling this role.

Incorporate a Company in Morocco

Set up your business entity in Morocco with full compliance support, from initial structuring through to registration with the Tribunal de Commerce.

Registered Office Requirements in Morocco

Morocco registered office requirements mandate that every company maintain a physical siege social within the country, recorded in the Registre du Commerce et du Mobilier (RC) held at the relevant Tribunal de Commerce.

- A physical address located within Morocco is required; P.O. boxes do not satisfy the siege social obligation.

- Virtual office addresses are generally not accepted as a compliant registered address under Moroccan commercial law.

- The address must be supported by proof of occupancy, such as a title deed, lease agreement, or a domiciliation contract with an accredited domiciliation company.

- The siege social is publicly listed in the Registre du Commerce and appears on the company's statutory documents.

- Any change of registered address requires a formal amendment filing with the Tribunal de Commerce and re-registration in the RC.

- Failure to maintain a valid legal address can result in administrative sanctions and may affect the company's standing with the Direction Générale des Impôts for tax registration purposes.

Director Requirements in Morocco

Under Morocco director requirements incorporation rules, directors assume personal liability for breaches of their fiduciary duties, violations of the company's statutes, and non-compliance with the provisions of Law No. 17-95 on Sociétés Anonymes or Law No. 5-96 governing the SARL. Upon appointment, a gérant or board member is legally bound to act in the corporate interest, maintain accurate accounting records, and file annual financial statements with the Tribunal de Commerce.

| Parameter | Detail |

|---|---|

| Minimum Number of Directors | One gérant for an SARL; a minimum of three directors for an SA under Law No. 17-95. |

| Maximum Number of Directors | No statutory maximum for an SARL; an SA board may not exceed twelve members under standard provisions. |

| Local/Resident Director Required | No statutory requirement for a resident or locally domiciled director. |

| Nationality Restrictions | No nationality restrictions apply; foreign nationals may serve as directors or gérants. |

| Minimum Age Requirement | Directors must be at least 18 years of age and have full legal capacity. |

| Corporate Directors Permitted | Corporate entities may serve as directors in an SA; natural persons are required as gérant in an SARL. |

| Director Must Be a Shareholder | No statutory requirement, though the company's statutes may impose this condition. |

| Publicly Listed on Registry | Director appointments are filed with the Registre de Commerce and are publicly accessible. |

| Disqualification Conditions | Persons subject to a court-imposed prohibition, bankruptcy order, or criminal conviction affecting commercial capacity are disqualified. |

An SA in Morocco can appoint a non-shareholder as a board member by default, unless the company's own statutes explicitly require directors to hold shares.

Shareholder Requirements in Morocco

Morocco shareholder requirements for incorporation vary by entity type. A Société à Responsabilité Limitée (SARL) requires a minimum of one associé and permits up to 50, making a sole-associate structure legally valid under Law No. 5-96.

Nationality and Residency Restrictions

Foreign nationals may hold shares in a Moroccan company without restriction in most sectors. Certain regulated industries, such as audiovisual media and some agricultural activities, impose foreign ownership caps under sector-specific legislation.

Corporate Shareholders

Corporate entities, whether domestic or foreign, are permitted to act as shareholders in a SARL or SA. No additional conditions are imposed solely on the basis of the shareholder being a legal person rather than an individual.

Shareholder Liability

In a SARL, each associé's liability is limited to their capital contribution. Extended personal liability generally does not arise unless a court pierces the corporate veil due to commingling of assets or fraudulent conduct.

Register of Shareholders

A SARL must maintain an internal register of associates. This register is not publicly accessible, though ownership information is filed with the Tribunal de Commerce upon incorporation and must reflect any subsequent transfers.

Shareholder Structuring Support for Your Moroccan Entity

Get guidance on associé requirements, ownership structuring, and compliance obligations when setting up a company in Morocco.

UBO / Beneficial Ownership Disclosure Requirements in Morocco

Morocco beneficial ownership disclosure requirements are governed by Law No. 18-46 on the register of beneficial owners, which defines a beneficial owner as any natural person who ultimately owns or controls, directly or indirectly, a legal entity through a shareholding exceeding 30% of capital or voting rights.

- Identify all natural persons meeting the 30% ownership or control threshold within the entity's structure.

- Prepare the beneficial ownership declaration, listing each UBO's identity, nationality, country of residence, and the nature of their controlling interest.

- Submit the declaration to the Registry of Commerce (Registre de Commerce) at the time of incorporation.

- File any updates to the register within 30 days of a change in beneficial ownership.

| Parameter | Detail |

|---|---|

| Ownership Threshold for UBO Status | 30% of capital or voting rights |

| Filing Authority | Registre de Commerce (Registry of Commerce) |

| Disclosure Deadline at Incorporation | At the time of incorporation |

| Publicly Accessible Register | No statutory requirement for full public access |

| Penalties for Non-Disclosure | Sanctions apply under Law No. 18-46; specific fines subject to judicial determination |

| Ongoing Update Obligation | Within 30 days of any change in UBO information |

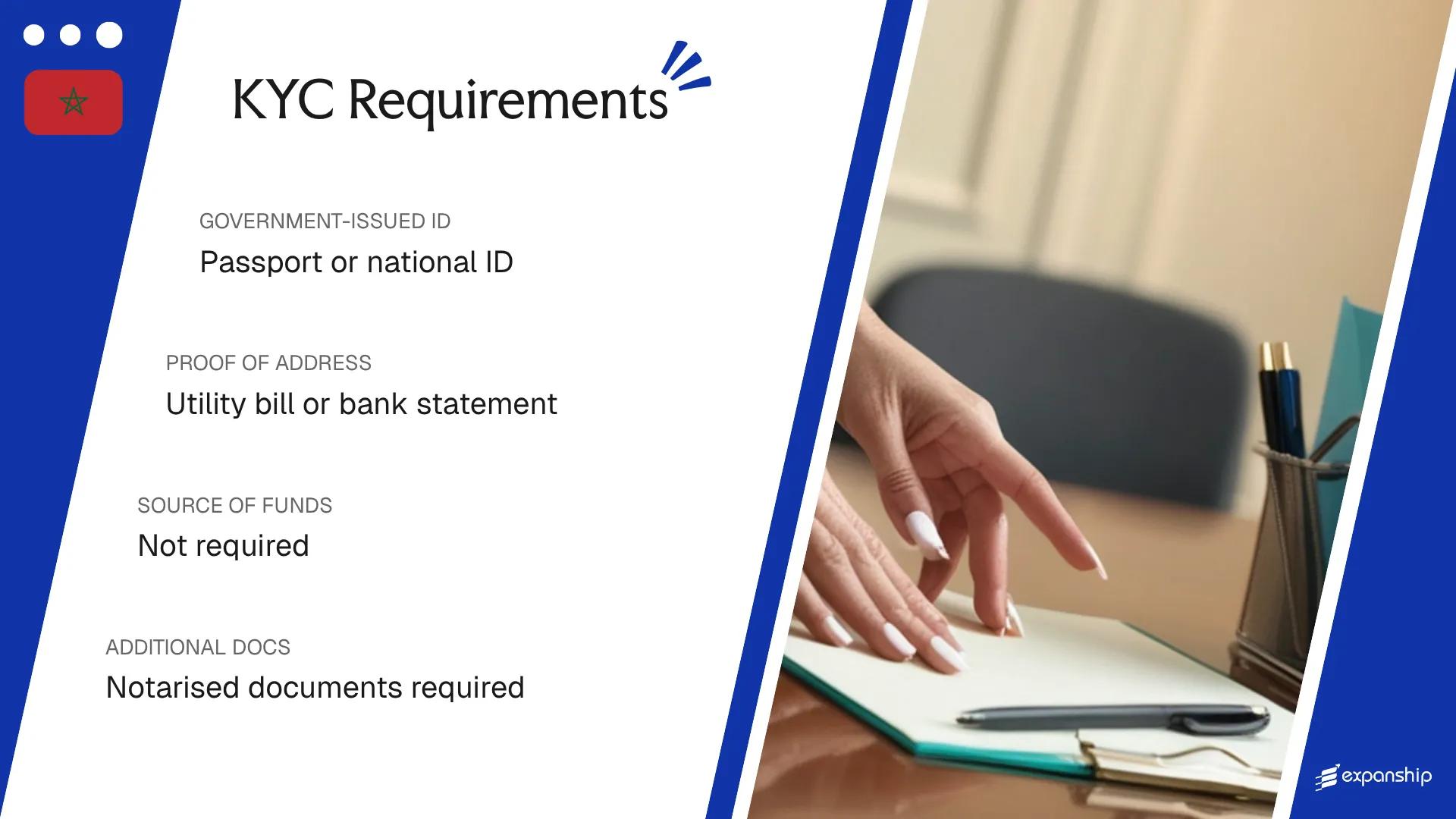

KYC / Document Requirements in Morocco

Morocco KYC requirements for company registration are governed by Law No. 12-18 relating to the fight against money laundering and terrorist financing, administered by the Unité de Traitement du Renseignement Financier (UTRF). All parties involved in the incorporation must be identified and verified before the entity is registered with the Regional Investment Centre (CRI).

Individual / Personal Documents

- Valid passport or national identity card for each individual director, shareholder, or beneficial owner

- Proof of residential address dated within three months, such as a utility bill or bank statement

- Signed KYC declaration form as required by the notary or CRI processing the incorporation

- Curriculum vitae or professional background summary may be requested for regulated sector filings

Corporate Documents

- Certificate of incorporation of the parent or shareholder entity, issued by the relevant home jurisdiction authority

- Constitutional documents, including articles of association or equivalent instrument

- Official register of directors and shareholders from the home jurisdiction

- Proof of registered address of the corporate shareholder, such as a utility bill or official correspondence

Source of Funds Documentation

- Recent bank statements covering a minimum of three months prior to incorporation

- Audited financial statements of the investing entity where available

- Signed declaration of the origin of funds if bank documentation is insufficient

Notarisation and Apostille Requirements

- Foreign documents must generally be apostilled under the Hague Convention or, where Morocco has no treaty with the issuing country, legalised through the relevant Moroccan consulate

- All non-Arabic and non-French documents must be translated by a certified translator recognised in Morocco

- Notarised copies are typically required for constitutional documents submitted to the CRI

Inconsistencies between the declared beneficial owner and the information in submitted corporate documents are the most common cause of incorporation rejection at the CRI.

Company Name Requirements in Morocco

Your proposed company name is assessed for availability and compliance during the registration process administered by the Office Marocain de la Propriété Industrielle et Commerciale (OMPIC). Names that conflict with existing registered entities or trademarks are rejected at this stage.

All company names must include a legal suffix corresponding to the chosen entity type, such as "SARL" for a société à responsabilité limitée or "SA" for a société anonyme. Arabic or French are the accepted languages for the dénomination sociale, reflecting Morocco's official administrative languages.

Certain words are restricted from use without prior authorisation from relevant authorities. Terms implying government affiliation, financial institution status, or national significance generally require regulatory approval before OMPIC will accept the name.

Name reservation is available through OMPIC prior to formal incorporation. A reserved name is protected for a defined period, allowing you to proceed with the remaining registration steps without risk of a competing filing claiming the same dénomination sociale.

Compliance Services for Companies in Morocco

Expanship supports businesses in meeting their ongoing statutory and regulatory obligations under Moroccan corporate law, from annual filings to regulatory reporting.

Conclusion

Morocco company incorporation requirements span several distinct obligations governed primarily by Law No. 17-95 on public limited companies and Law No. 5-96 covering other corporate forms, with the Registre de Commerce serving as the central point of registration.

Share capital thresholds and director residency conditions are among the more consequential factors for foreign investors to assess early. Beneficial ownership disclosure, now formalized under Anti-Money Laundering legislation, adds a compliance layer that applies from the moment of formation.

Once these requirements are understood, the practical focus shifts to execution: assembling documentation, engaging a notary, and coordinating with the relevant authorities within the prescribed timelines.

Expanship's Corporate Services for Morocco Expansion

Expanship supports your Morocco corporate services expansion by handling the procedural requirements that make formation here more demanding than in many comparable markets. From coordinating notarised deed execution to liaising with the Regional Investment Centre and the tax authorities for ICE registration, the firm manages the steps that consume the most time for incoming businesses.

Beyond formation, Expanship offers a structured range of ongoing services to support your entity in Morocco:

- Preparing and filing all company registration documents with the relevant authorities on your behalf.

- Providing a registered agent and a compliant local office address for your entity.

- Managing government filings and acting as the direct liaison with Moroccan regulatory bodies.

- Handling post-incorporation compliance obligations to keep your company in good standing.

- Facilitating introductions to banking institutions suited to your business profile.

- Registering your firm with the tax authorities and coordinating with local administrative offices.

To discuss your setup requirements, contact Expanship Morocco.

Frequently Asked Questions (FAQ)

Foreign nationals can serve as directors of a Moroccan company without a residency requirement, but non-resident directors who take an active management role may trigger tax residency considerations under Moroccan tax law. An SA requires a board of at least three directors, while a SARL is managed by one or more gérants who can be foreign nationals. Holding a management position does not automatically grant the right to work in Morocco; a separate work authorization is required if the director is physically present and remunerated locally.

A standard SARL requires at least two shareholders, whereas the SARL-AU (Société à Responsabilité Limitée à Associé Unique) was introduced precisely to allow sole-shareholder incorporation. Both structures are governed under Law No. 5-96 on commercial companies. The SARL-AU functions identically to a standard SARL in terms of liability and compliance obligations, with the sole distinction being the number of shareholders.

Failure to declare or update beneficial ownership information as required under Law No. 12-18 and the obligations administered through the Office des Changes and AMSSNMF can result in administrative sanctions and fines against the company. The non-compliant entity may also face restrictions on banking relationships, as Moroccan financial institutions are required to verify UBO data before opening or maintaining accounts. Persistent non-disclosure can escalate to criminal liability for the responsible managers under Morocco's anti-money laundering framework.

A company name can incorporate Latin-script words or foreign-language terms, but the registered name must be compatible with the naming conventions accepted by the Registre du Commerce at the relevant Tribunal de Commerce. The Office Marocain de la Propriété Industrielle et Commerciale (OMPIC) conducts the name availability search, and any name that conflicts with a registered trademark or an existing entity name will be rejected. Names that are contrary to public order or morality are also prohibited under the Commercial Code.

Yes, corporate shareholders face additional documentary requirements compared to individual shareholders. An individual shareholder typically provides a certified copy of their passport and proof of address, while a corporate shareholder must submit its certificate of incorporation, articles of association, and evidence of authorized signatories, all of which generally require apostille certification or legalization depending on the country of origin. Documents issued in a language other than Arabic or French must be accompanied by a certified translation before submission to the Registre du Commerce.

A change of registered office must be formally recorded by filing an amendment with the Registre du Commerce at the competent Tribunal de Commerce, and the update must be published in a legal gazette. Operating with an outdated registered office address can result in the company missing official correspondence from the tax authority (Direction Générale des Impôts) or the court, which may lead to default judgments or administrative penalties being issued without the company's knowledge. The amendment process requires a notarized decision from the company's governing body authorizing the change.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.