Key Takeaways

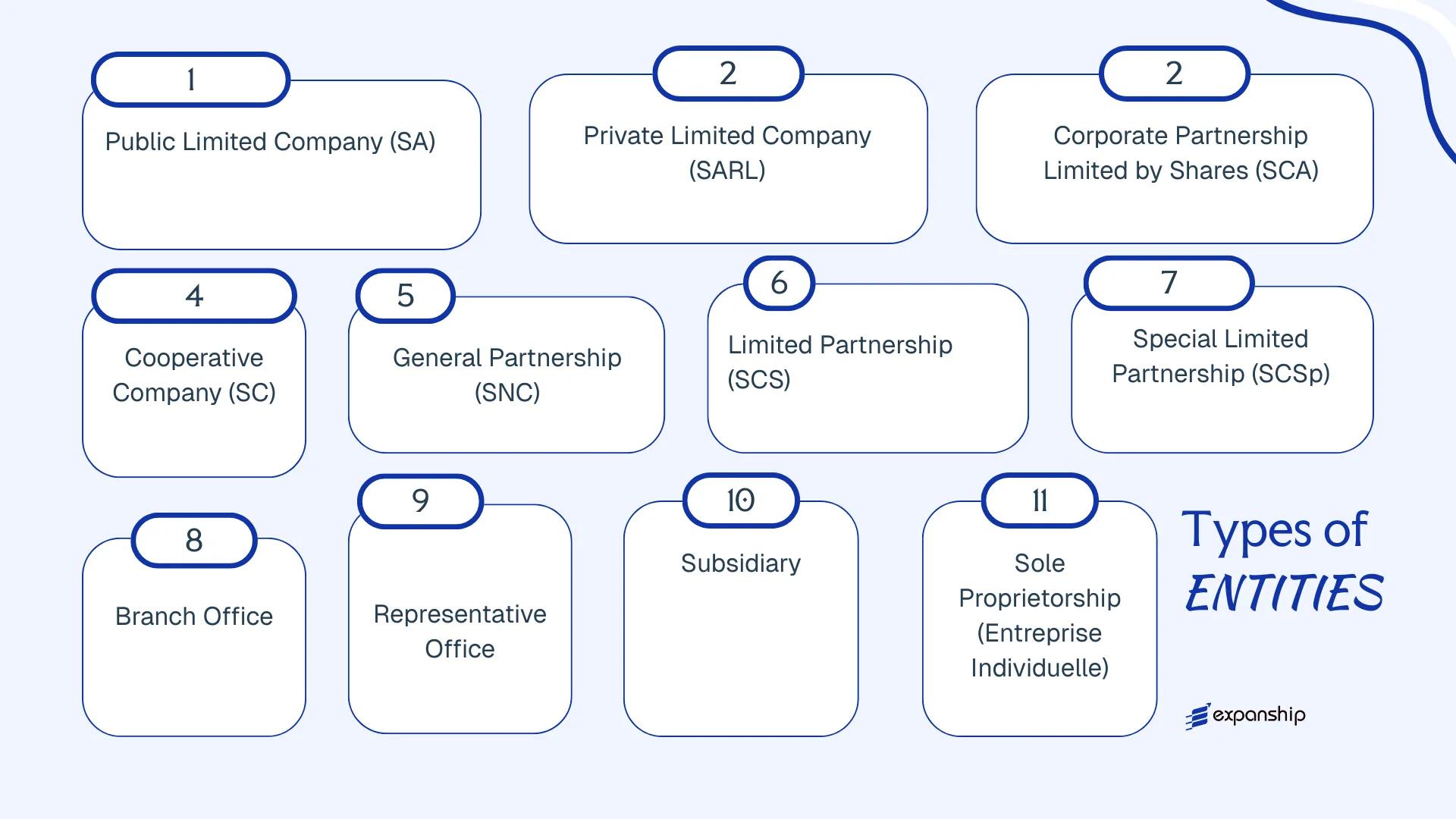

- Luxembourg recognises ten distinct business entity types under the law of 10 August 1915 on commercial companies, each carrying different governance rules, liability implications, and capital requirements.

- The SARL is the most widely registered entity in Luxembourg, used by SMEs and holding structures, while the SCSp has become the dominant vehicle for alternative investment funds under the AIFMD framework.

- All companies must register through the Registre de Commerce et des Sociétés (RCS), the official trade and companies register operating under Luxembourg law.

- Entity selection in Luxembourg is shaped by the country's treaty-based tax posture, extensive double tax treaty network, and access to EU directives governing cross-border income.

Introduction to Entity Types in Luxembourg

Luxembourg is a landlocked grand duchy in Western Europe, bordered by Belgium, France, and Germany. As an independent sovereign state and founding member of the European Union, it operates one of the most established corporate registration frameworks on the continent. Companies are registered through the Registre de Commerce et des Sociétés (RCS), the official trade and companies register administered under Luxembourg law.

The country's tax posture is treaty-based, with an extensive network of double tax treaties and EU directive access informing how resident entities are taxed on cross-border income.

Several corporate forms are available under Luxembourg law, each governed primarily by the law of 10 August 1915 on commercial companies (as amended). The recognised types of business entities in Luxembourg include:

- Société Anonyme (SA)

- Société à Responsabilité Limitée (SARL)

- Société en Commandite par Actions (SCA)

- Société Coopérative (SC)

- Société en Nom Collectif (SNC)

- Société en Commandite Simple (SCS)

- Société en Commandite Spéciale (SCSp)

- Branch Office

- Representative Office

- Entreprise Individuelle

Each of these Luxembourg legal entity structures carries distinct governance rules, liability implications, and capital requirements that this article examines in detail.

An Overview of Business Structures in Luxembourg

Luxembourg company law recognises several distinct entity types, each governed primarily by the law of 10 August 1915 on commercial companies (loi du 10 août 1915 concernant les sociétés commerciales), as amended most recently by the law of 10 August 2016. A parallel framework under the law of 19 December 2002 addresses accounting and annual reporting obligations. Each structure carries different rules on liability, governance, and capital requirements, reflecting different commercial purposes.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Société Anonyme (SA) | Public limited company | Limited to share capital | Taxed | Yes | 1 shareholder | RCS / CSSF (if regulated) | Law of 10 Aug 1915 |

| Société à Responsabilité Limitée (SARL) | Private limited company | Limited to share capital | Taxed | Yes | 1 shareholder | RCS | Law of 10 Aug 1915 |

| Société en Commandite par Actions (SCA) | Partnership limited by shares | Mixed (general/limited) | Taxed | Yes | 2 partners | RCS | Law of 10 Aug 1915 |

| Société Coopérative (SC) | Cooperative | Limited | Taxed | Yes | 3 members | RCS | Law of 10 Aug 1915 |

| Société en Nom Collectif (SNC) | General partnership | Unlimited (all partners) | Transparent | Yes | 2 partners | RCS | Law of 10 Aug 1915 |

| Société en Commandite Simple (SCS) | Limited partnership | Mixed (general/limited) | Transparent | Yes | 2 partners | RCS | Law of 10 Aug 1915 |

| Société en Commandite Spéciale (SCSp) | Special limited partnership | Mixed (general/limited) | Transparent | Yes | 2 partners | RCS | Law of 10 Aug 2016 |

| Branch Office | Foreign company extension | Parent bears liability | Taxed (local profits) | Yes | N/A | RCS | Law of 10 Aug 1915 |

| Representative Office | Non-trading presence | Parent bears liability | Generally exempt | No | N/A | RCS | General commercial law |

| Entreprise Individuelle | Sole proprietorship | Unlimited (owner) | Personal income tax | Yes | 1 (owner) | RCS | General commercial law |

Each of these structures is examined in full in the sections below.

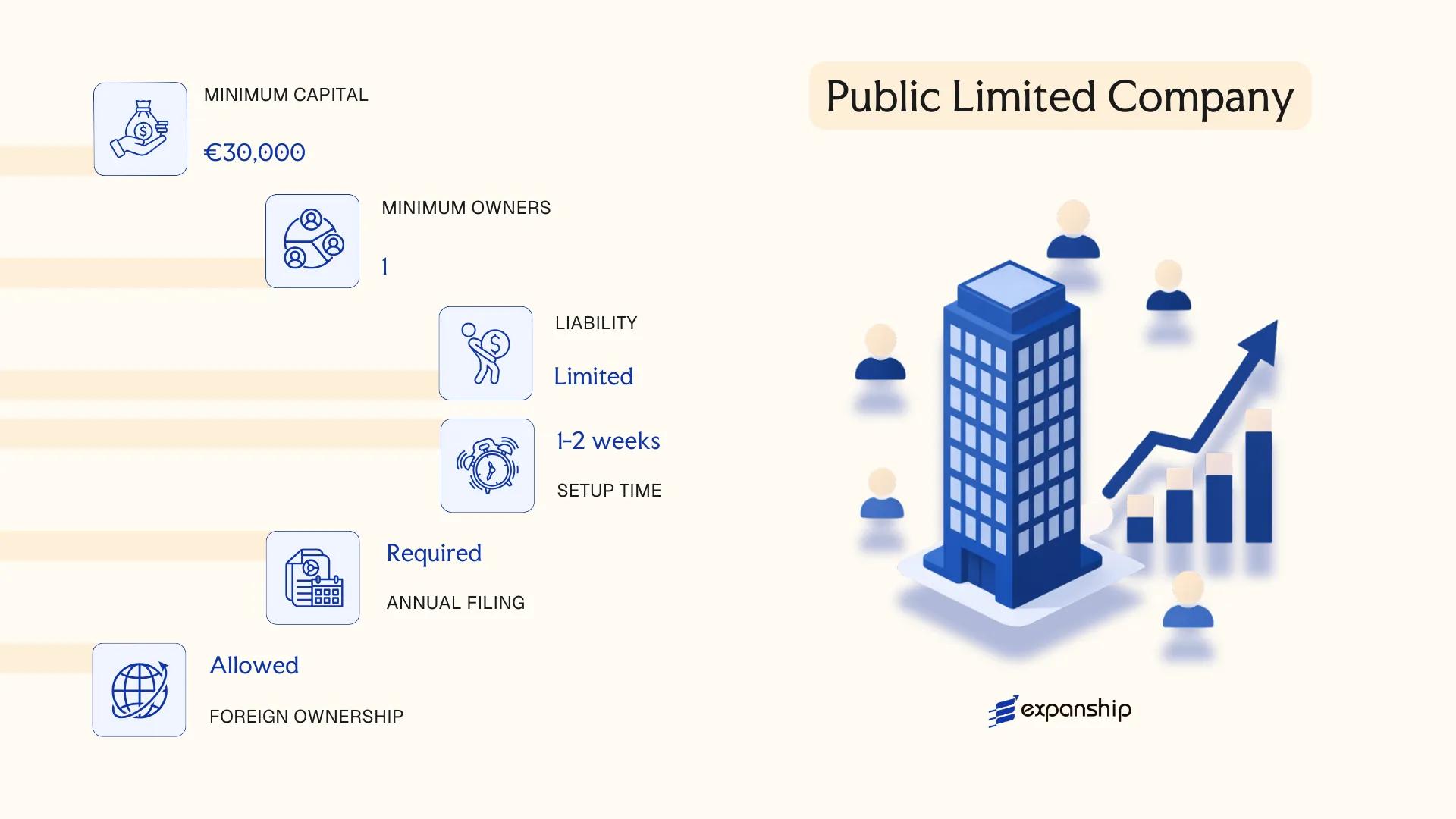

Société Anonyme (SA) — Public Limited Company

Governed by the Luxembourg law of 10 August 1915 on commercial companies (as amended, most recently by the law of 10 August 2023), the Luxembourg Société Anonyme SA formation produces a distinct legal entity with full separate legal personality. Shareholders bear no personal liability beyond their capital contribution.

Structurally, the SA accommodates both privately held and publicly listed businesses. Its share capital can be divided into transferable securities, which makes it the standard vehicle for capital markets activity, institutional investment, and large-scale holding structures.

Company Incorporation in Luxembourg

Incorporate a Société Anonyme or any other legal entity in Luxembourg with end-to-end support from Expanship.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (SA) | Separate legal personality; limited liability |

| Members | Shareholders (min. 1, no maximum) | Single-shareholder SA permitted since the 2016 reform |

| Governance | Board of Directors (min. 3 directors) or Single Director (if single shareholder) | Two-tier board (Management Board + Supervisory Board) also permitted |

| Local Presence | Registered office in Luxembourg required | Domiciliation through a licensed provider is permitted |

| Share Capital | Min. EUR 30,000, fully subscribed; at least 25% paid up at incorporation | Bearer shares are prohibited; shares must be registered |

| Privacy | Shareholders registered in the RCS (Registre de Commerce et des Sociétés); beneficial owners disclosed in the RBE | Luxembourg's Registre des Bénéficiaires Effectifs (RBE) is publicly accessible |

Focus Points

- Taxation: Subject to corporate income tax at 17% (for profits above EUR 200,001), municipal business tax (varying by commune, 6.75% in Luxembourg City), and net wealth tax at 0.5%; standard VAT rate is 17%; withholding tax of 15% applies to dividend distributions, subject to reduction under applicable tax treaties or the EU Parent-Subsidiary Directive.

- Treaty Access: Qualifies as a resident taxpayer, granting access to Luxembourg's extensive double tax treaty network (80+ treaties).

- Annual Compliance: Mandatory filing of audited annual accounts with the RCS; statutory audit required unless the entity qualifies as a small company under specific thresholds.

- Economic Substance: No statutory substance requirement for holding activities, but functional substance is advisable to support treaty positions and transfer pricing defensibility.

- Conversion: An SA may be converted into another commercial form (e.g., SARL) by shareholders' resolution, subject to notarial deed and RCS re-registration.

Closing

The SA suits large trading companies, listed entities, investment holding structures, and businesses anticipating capital raises or institutional co-investment. Its primary advantage is structural flexibility for complex ownership arrangements; the main drawback is the comparatively higher administrative burden, including mandatory audit requirements and minimum capital thresholds.

The SA is best suited for institutional investors, large corporates, and fund promoters requiring a publicly offering-capable or multi-investor structure.

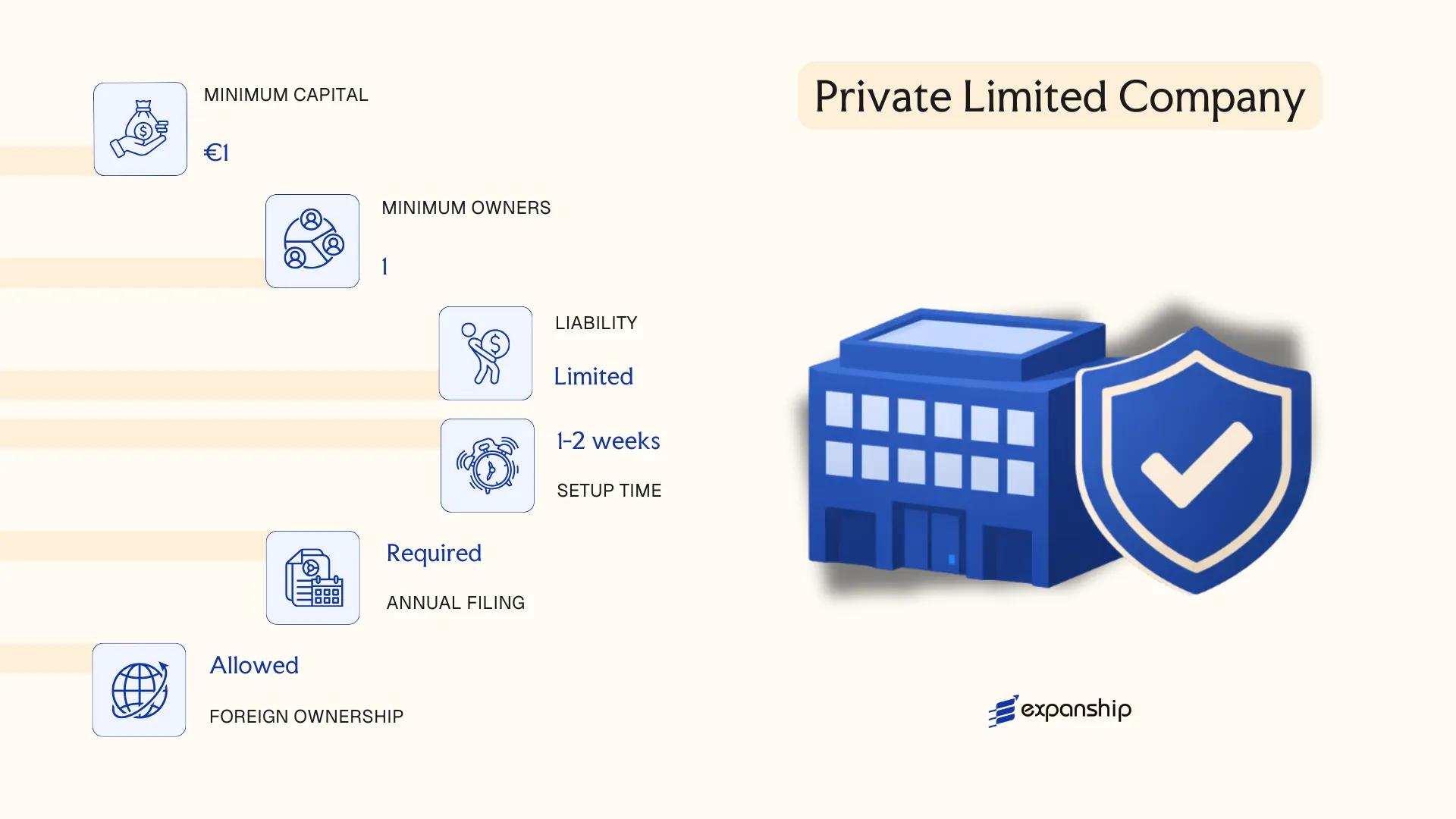

Société à Responsabilité Limitée (SARL) — Private Limited Company

The Luxembourg SARL private limited company is governed by the law of 10 August 1915 on commercial companies, as amended, most significantly by the law of 10 August 2016 which modernised its structural framework. It carries separate legal personality, meaning the entity exists independently from its shareholders, and liability is confined to each member's capital contribution.

Structurally, the SARL occupies a middle ground: it offers the limited liability protection of a capital company while retaining the more restricted transferability of shares typically associated with a partnership-type structure. Shares cannot be freely transferred to third parties without prior shareholder approval, which makes it a preferred vehicle for closely held businesses.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société à Responsabilité Limitée (SARL) | Private limited company; separate legal personality |

| Members | 1–100 shareholders | Single-member variant permitted (SARL-S or standard sole shareholder); no corporate restriction on nationality |

| Management | One or more gérants (managers) | Need not be shareholders; no nationality or residency requirement under company law |

| Local Presence | Registered office in Luxembourg | Physical address required; no statutory requirement for a local resident manager, though substance considerations apply |

| Share Capital | Minimum EUR 12,000 | Must be fully paid up at incorporation; divided into parts sociales, not freely negotiable |

| Privacy | Shareholders disclosed in the RCS | Beneficial ownership registered in the Luxembourg Register of Beneficial Owners (RBE) |

Focus Points

- Taxation: Subject to corporate income tax (currently 17% for profits above EUR 200,001), municipal business tax (varying by commune, approximately 6.75% in Luxembourg City), and net wealth tax; VAT registration required if thresholds are met; withholding tax of 15% applies to dividend distributions, subject to reduction under EU directives or double tax treaties.

- Annual Compliance: Annual accounts must be filed with the Registre de Commerce et des Sociétés (RCS); financial statements are subject to audit if two of three statutory thresholds are exceeded.

- Share Transfer Restrictions: Transfer of parts sociales to non-shareholders requires approval by members holding at least three-quarters of the share capital.

- Conversion: A SARL may be converted into an SA or other recognised form by notarial deed, subject to shareholder vote and compliance with the target entity's capital requirements.

- Treaty Access: As a Luxembourg tax resident entity, the SARL has access to Luxembourg's extensive double tax treaty network, currently covering over 80 jurisdictions.

Sub-Types

SARL-S (Société à Responsabilité Limitée Simplifiée)

Introduced by the 2016 reform, the SARL-S requires a minimum share capital of only EUR 1, making it accessible for early-stage ventures. It is restricted to natural persons as shareholders (maximum 5) and prohibits certain regulated activities; the reduced capital must be built up to EUR 12,000 through a mandatory legal reserve mechanism before distribution.

Closing

The SARL is widely used for trading operations, family-owned businesses, joint ventures, and subsidiary structures where shareholder control over ownership transfers is a priority. Its principal constraint is the 100-shareholder ceiling, which limits scalability for structures requiring broader investor participation.

The SARL is best suited for SMEs, wholly owned subsidiaries of foreign groups, and founder-led businesses seeking liability protection without the governance formality of a public company.

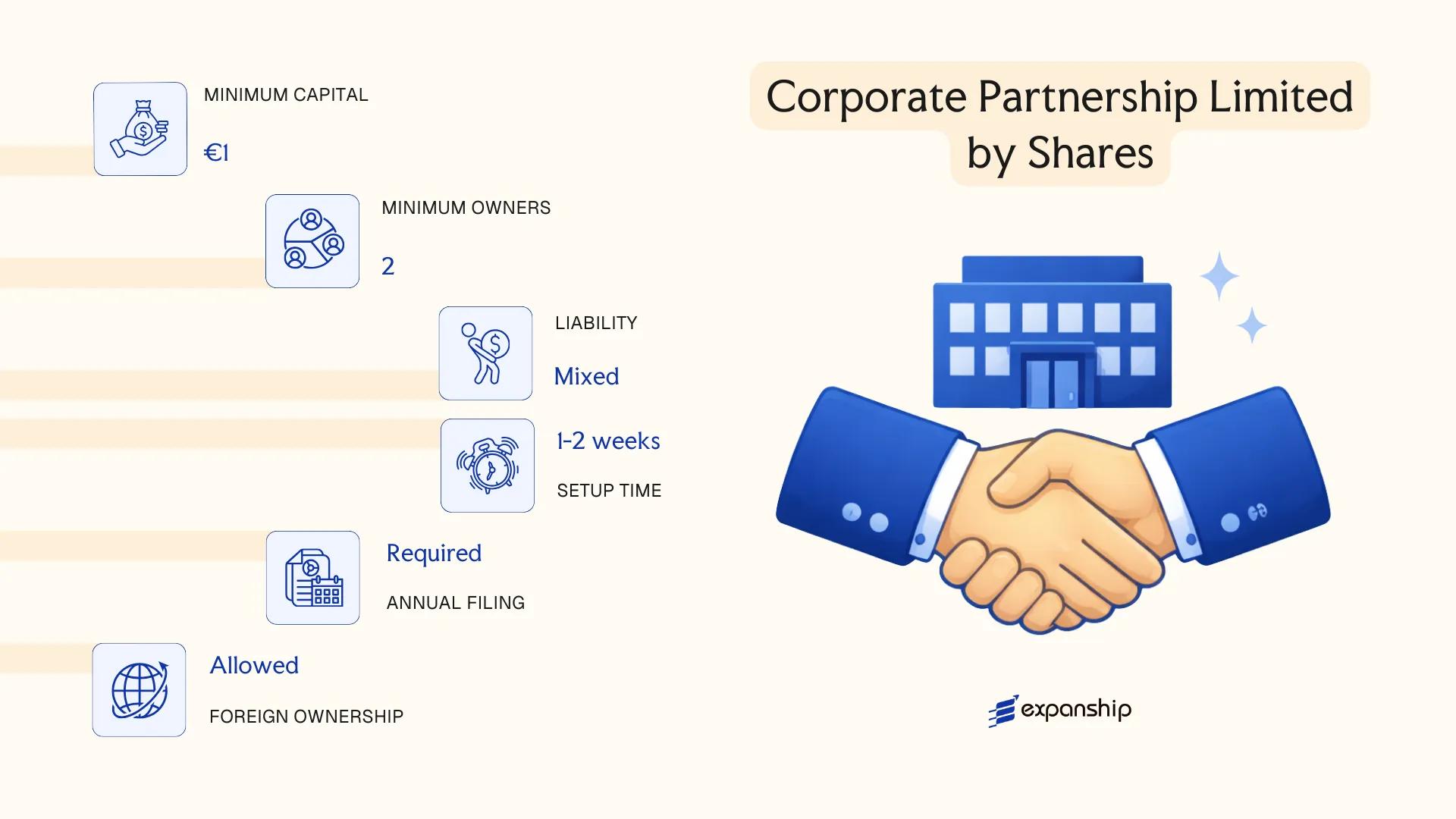

Société en Commandite par Actions (SCA) — Corporate Partnership Limited by Shares

The Luxembourg SCA corporate partnership shares structure is governed by the amended Law of 10 August 1915 on Commercial Companies. It carries separate legal personality and combines features of both a partnership and a share-based company, making it a hybrid form with limited liability for most participants.

Two distinct categories of members define the SCA. General partners hold unlimited liability and manage the entity, while limited partners hold transferable shares and bear liability only to the extent of their contribution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société en Commandite par Actions (SCA) | Hybrid structure; separate legal personality |

| Members | At least 1 general partner (unlimited liability) + at least 1 shareholder (limited partner); no maximum for shareholders | General partner is often a corporate entity to contain liability exposure |

| Management | Managed exclusively by general partners | Shareholders cannot participate in management without losing limited liability protection |

| Local Presence | Registered office in Luxembourg required | No mandatory resident director, but substance considerations apply |

| Share Capital | Minimum EUR 30,000; shares must be fully subscribed | Shares are transferable; general partner interest is not freely transferable without consent |

| Privacy | Shareholders not in public register; general partners disclosed | Beneficial ownership reported to the RBE (Registre des Bénéficiaires Effectifs) |

Focus Points

- Taxation: Subject to corporate income tax (currently 17% for profits above EUR 200,001), municipal business tax, net wealth tax, and standard 15% withholding tax on dividends; VAT registration required for taxable activities; access to the EU Parent-Subsidiary Directive may reduce withholding obligations.

- Treaty Access: Qualifies as a Luxembourg resident entity and can access Luxembourg's extensive double tax treaty network, subject to substance requirements.

- Annual Compliance: Mandatory annual accounts filed with the Registre de Commerce et des Sociétés (RCS); audit required if thresholds under the 2015 Accounting Law are met.

- Conversion: Can be converted into other corporate forms, including the SA, subject to shareholder and general partner approval and compliance with the 1915 Law.

- Restrictions: General partners cannot be shielded from personal liability; regulated activities require additional authorisation from the relevant supervisory authority (e.g., CSSF for financial services).

Closing

The SCA is used primarily as a private equity or investment holding vehicle, where sponsors need direct control through the general partner role while offering investors transferable, limited-liability shares. The transferability of shares is a structural advantage; the unlimited liability of general partners remains a persistent constraint that typically requires a corporate entity to serve in that role.

The SCA suits institutional fund sponsors, private equity managers, and family holding structures where a distinction between controlling and passive participants is a structural requirement.

Société Coopérative (SC) — Cooperative Company

Governed by the Law of 10 August 1915 on Commercial Companies, as amended, the Société Coopérative is designed for entities with a variable membership base and an open-door structure. Luxembourg Société Coopérative registration follows the same commercial law framework as other capital companies, but the SC is distinguished by its mutuality-driven purpose and the ability to freely admit or exclude members without amending its articles.

The SC holds separate legal personality upon incorporation and offers limited liability to its members. Its hybrid character — part commercial entity, part member-serving organisation — makes it useful for collective commercial activities where the membership composition is expected to change over time.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Coopérative (SC) | Separate legal personality; governed by the 1915 Companies Law |

| Governance | Board of Directors or Manager(s); General Meeting of Members | Voting rights may be allocated on a one-member-one-vote basis |

| Members | Minimum 3 members; no statutory maximum | Members may be natural or legal persons |

| Local Presence | Registered office in Luxembourg required | No mandatory resident director, but effective management should be demonstrable |

| Capital | No statutory minimum capital | Variable capital structure; shares are not freely transferable without member approval |

| Privacy | Member register not publicly disclosed | Articles of incorporation filed with the RCS (Registre de Commerce et des Sociétés) |

Focus Points

- Taxation: Subject to corporate income tax (CIT) at 17%, municipal business tax, and net wealth tax; VAT registration required if commercial thresholds are met; withholding tax applies to profit distributions unless exemptions under the Parent-Subsidiary Directive or applicable tax treaties reduce the rate.

- Compliance: Annual accounts must be filed with the RCS; a statutory auditor (réviseur d'entreprises agréé) is required if the SC exceeds two of the three size thresholds under Luxembourg accounting law.

- Treaty Access: As a Luxembourg tax-resident entity, the SC can access Luxembourg's extensive double tax treaty network, subject to meeting beneficial ownership and substance requirements.

- Conversion: An SC may be converted into another corporate form by resolution of the general meeting, subject to notarial deed and RCS filing.

- Restrictions: The cooperative purpose must be reflected in the articles; purely profit-driven structures with no cooperative rationale may face regulatory scrutiny.

Sub-Types

Société Coopérative Organisée Comme une Société Anonyme (SCOSA)

The SCOSA adopts the organisational framework of a Société Anonyme while retaining the variable membership structure of the cooperative form. It is used when a cooperative requires greater capital-raising capacity or a more formalised governance structure, including a board of directors and supervisory board as applicable under SA rules.

Recommendations

The SC cooperative company Luxembourg structure is suited for collective trading ventures, agricultural groups, consumer organisations, and professional service cooperatives where membership fluidity is a practical necessity. Its variable capital structure removes the administrative burden of deed amendments each time a member joins or departs, though the absence of a statutory capital floor means creditor protection relies heavily on the financial terms set in the articles.

The SC is most appropriate for member-driven commercial ventures or professional groups that require an open and variable membership structure under Luxembourg law.

Partnerships in Luxembourg [Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite Spéciale (SCSp)]

Three partnership structures are available under the amended Luxembourg law of 10 August 1915 on commercial companies: the Société en Nom Collectif (SNC), the Société en Commandite Simple (SCS), and the Luxembourg SCSp special limited partnership (Société en Commandite Spéciale). The SNC and SCS carry separate legal personality, while the SCSp does not — a distinction with significant consequences for fund structuring and asset segregation.

All three forms are transparent for tax purposes, meaning income is taxed at the level of the partners rather than the entity itself. The SCSp in particular has become the preferred vehicle for alternative investment funds since its introduction in 2013.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | SNC: General Partnership / SCS: Limited Partnership / SCSp: Special Limited Partnership | Only the SCSp lacks separate legal personality |

| Members | SNC: minimum 2 general partners, no maximum / SCS: minimum 1 general + 1 limited partner / SCSp: same as SCS | No upper limit on partners in any form |

| Liability | SNC: all partners bear unlimited joint liability / SCS & SCSp: limited partners capped at contribution | General partners in SCS and SCSp retain unlimited liability |

| Registered Office | Physical registered address in Luxembourg required for all three | No mandatory local manager unless required by sector |

| Capital | No statutory minimum for any of the three forms | Contributions may be in cash, kind, or industry |

| Privacy | Partner identities disclosed in the RCS (Registre de Commerce et des Sociétés) for SNC and SCS | SCSp limited partners not publicly listed under standard filings |

Focus Points

- Taxation: All three structures are fiscally transparent — no corporate income tax at entity level; partners are taxed individually according to their own tax status. No withholding tax applies to profit distributions from an SCSp.

- AIFMD compliance: SCSp vehicles used for alternative investment funds must appoint an authorised Alternative Investment Fund Manager (AIFM) regulated by the Commission de Surveillance du Secteur Financier (CSSF).

- Annual compliance: SNC and SCS must file annual accounts with the RCS; the SCSp is exempt from this filing requirement, which contributes to its popularity among fund sponsors.

- Conversion: An SCSp may be converted into an SCS or other corporate form without dissolution, subject to partner consent and RCS notification.

- Treaty access: Fiscal transparency means treaty benefits flow to partners individually; access depends on each partner's residence and applicable bilateral conventions.

Sub-Types

Société en Nom Collectif (SNC)

The SNC is a general partnership in which all partners act as merchants and bear joint, unlimited liability for the firm's obligations. It is rarely used for investment structures but suits small professional firms where partners accept personal exposure.

Société en Commandite Simple (SCS)

The SCS separates general partners (unlimited liability, active management) from limited partners (liability capped at their contribution, passive role). It predates the SCSp and retains separate legal personality, which some cross-border structures require for contractual reasons.

Société en Commandite Spéciale (SCSp)

Introduced by the law of 12 July 2013, the SCSp mirrors the SCS structurally but has no legal personality of its own. Contracts are entered into through the general partner on behalf of the partnership. This design aligns closely with the Anglo-American limited partnership model, making it the dominant SNC SCS SCSp Luxembourg partnership structure used by private equity and real estate fund managers.

Common Use Cases and Considerations

The SCSp is the standard vehicle for alternative investment funds, carried interest arrangements, and co-investment structures; the SNC and SCS see limited use outside specific professional or holding contexts. The key advantage of the SCSp is its combination of fiscal transparency and structural flexibility without the formality of a corporate entity; the principal limitation is that the absence of legal personality requires careful drafting of third-party agreements.

The SCSp suits institutional fund managers, private equity sponsors, and asset managers establishing regulated or unregulated alternative investment funds in Luxembourg.

Foreign Presence in Luxembourg [Branch Office, Representative Office, Subsidiary]

Foreign companies pursuing opening a branch office in Luxembourg must register with the Luxembourg Trade and Companies Register (Registre de Commerce et des Sociétés, RCS) under the amended Companies Act of 1915. Each option for establishing foreign presence carries distinct legal consequences, particularly regarding liability, tax exposure, and operational scope.

A branch has no separate legal personality — the parent company remains fully liable for its obligations. A subsidiary, incorporated as a distinct Luxembourg entity (typically an SA or SARL), holds separate legal personality and limits liability to its own assets. A representative office occupies a narrower role, restricted to non-commercial activities such as market research or liaison functions, and is generally not registered with the RCS.

Key Characteristics

| Requirement | Branch Office | Representative Office | Subsidiary |

|---|---|---|---|

| Legal Personality | None (extension of parent) | None | Separate legal entity |

| Liability | Parent bears full liability | Parent bears full liability | Limited to subsidiary assets |

| Registration | Mandatory RCS registration | Generally not required | Mandatory RCS registration |

| Permitted Activities | Commercial operations | Non-commercial only | Full commercial scope |

| Local Presence | Registered address in Luxembourg required | Physical office typically maintained | Registered address required |

| Capital Requirement | None | None | Varies by entity form (e.g., EUR 12,000 for SARL) |

Focus Points

- Taxation: Branches are subject to corporate income tax (up to 17%) on Luxembourg-sourced profits; subsidiaries are taxed as resident entities and may access the participation exemption regime. VAT registration applies to commercial activities regardless of structure.

- Treaty Access: Subsidiaries qualify as Luxembourg tax residents and can access the extensive double tax treaty network; branches have more limited treaty access depending on the parent's residence jurisdiction.

- Economic Substance: Substance requirements apply particularly to holding subsidiaries under ATAD and BEPS frameworks; branches must demonstrate genuine operational activity.

- Annual Compliance: Branches must file the parent's audited accounts with the RCS annually; subsidiaries file their own statutory accounts.

- Commercial Restrictions: Representative offices cannot invoice clients, sign contracts, or generate revenue directly.

Closing

A foreign company representative office in Luxembourg suits preliminary market exploration, while a branch works for direct operational extension without a separate entity. The Luxembourg subsidiary vs branch office decision ultimately turns on liability ring-fencing and treaty access needs — the subsidiary offers both, but at higher administrative cost and setup complexity.

A Luxembourg subsidiary is best suited for foreign groups seeking full liability separation, access to EU directives, and treaty-eligible holding or operational structures.

Sole Proprietorship (Entreprise Individuelle)

The Luxembourg sole proprietorship, or Entreprise Individuelle, is the simplest form of business registration available to self-employed individuals operating in the Grand Duchy. It is governed primarily by the amended Law of 2 September 2011 regulating access to the professions of craftsman, merchant, and industrialist, as well as general commercial law principles.

Unlike capital companies, this structure carries no separate legal personality. The proprietor and the business are legally one and the same, meaning personal assets are fully exposed to business liabilities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship | No separate legal personality from the owner |

| Proprietor | Single natural person | Cannot be held by a legal entity |

| Members | 1 proprietor only | No partners, shareholders, or co-owners permitted |

| Local Presence | Registered business address in Luxembourg required | Must hold a valid business permit (autorisation d'établissement) |

| Capital | No minimum capital requirement | Personal assets serve as the financial base |

| Liability | Unlimited personal liability | Proprietor's private estate is fully exposed to creditors |

| Privacy | Proprietor's name is publicly associated with the business | No beneficial ownership separation |

Focus Points

- Taxation: Subject to individual income tax (impôt sur le revenu) at progressive rates up to 42%; VAT registration required once annual turnover exceeds the applicable threshold; no corporate income tax or withholding tax applies.

- Business Permit: An autorisation d'établissement issued by the Direction générale des Classes moyennes is mandatory before commencing activity.

- Annual Compliance: Simplified accounting obligations apply; full IFRS-standard bookkeeping is not required, though commercial registers may require filings depending on activity.

- Social Security: The proprietor must register with the Centre commun de la sécurité sociale (CCSS) as a self-employed individual.

- Conversion: The structure can be converted into a capital company (e.g., SARL) as the business grows, though this requires a formal incorporation process.

Closing

The Entreprise Individuelle suits freelancers, sole traders, and artisans testing a local market without the administrative burden of a capital company, though the unlimited personal liability exposure makes it unsuitable for higher-risk or capital-intensive activities.

Independent professionals and sole traders with low liability risk who require a straightforward self-employed registration in Luxembourg with minimal setup costs and ongoing compliance obligations.

How to Choose the Right Entity Type in Luxembourg

Knowing how to choose a company structure in Luxembourg requires more than a general preference for limited liability. The governing framework — the Law of 10 August 1915 on Commercial Companies, as amended — defines what each structure can and cannot do, and mismatches between structure and purpose carry concrete consequences.

Why Your Entity Choice Matters

Selecting the wrong entity type is not merely an administrative inconvenience. Consider the following outcomes:

- A tax-exempt entity, such as a SICAR or certain reserved alternative investment funds, cannot claim reduced withholding tax rates under Luxembourg's treaty network, because treaty access generally requires the entity to be a taxable resident person.

- Choosing a structure without substance capacity when the OECD's BEPS framework or Luxembourg's domestic substance rules apply can trigger ATAD reporting failures and potential tax reassessments.

- Forming a commercial company when a foundation (under the Law of 21 April 1928) would serve asset protection or succession purposes locks your structure into annual shareholder meeting obligations and capital maintenance rules that foundations do not carry.

- Selecting an entity that requires a statutory audit when your firm is a single-operator consultancy below the SARL thresholds adds avoidable annual costs.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated activities such as fund management each require distinct structures under Luxembourg law.

- Tax Objectives: Your need for full tax exemption, participation exemption eligibility, or access to the treaty network will narrow the field significantly.

- Ownership and Management: Single-owner businesses and multi-party joint ventures have structurally different governance needs that map to different entity types.

- Substance Capacity: If you cannot maintain genuine management, staff, or office presence locally, your entity selection must account for applicable substance thresholds.

- Privacy Requirements: The Luxembourg Business Registers (LBR) mandate public disclosure of certain director and shareholder information for most commercial entities, with limited exceptions.

- Exit Strategy: Not all Luxembourg entities permit redomiciliation or conversion without dissolution; this constrains long-term flexibility if your plans may change.

Compliance Services for Companies in Luxembourg

Maintain good standing with Luxembourg's regulatory and filing requirements across all commercial entity types.

Conclusion

Selecting the right structure is among the most consequential decisions in any Luxembourg company incorporation. The SA suits publicly traded firms or large capital-intensive ventures; the SARL remains the most widely registered entity in the country, favored by SMEs and holding structures alike. An SCA serves private equity sponsors requiring a separation between management and investor liability. The SCSp has become the vehicle of choice for alternative investment funds governed under the AIFMD framework. Cooperatives address member-owned enterprises, while the SNC and SCS carry unlimited liability for those who accept that exposure. Sole proprietorships cover micro-activity at the lowest administrative threshold.

Governed primarily by the law of 10 August 1915 on commercial companies, as amended, the jurisdiction continues to refine its corporate framework in response to EU directives, keeping entity selection both structured and consequential. A qualified corporate services provider can translate that framework into a formation strategy suited to your business objectives.

How Expanship Can Assist You

Expanship Luxembourg company formation services cover the full lifecycle of establishing a legal presence, from selecting between an SA, SARL, SCSp, or SCA through to filing with the Luxembourg Trade and Companies Register (RCS) and meeting Business Permit requirements issued by the Direction générale des classes moyennes. Every engagement is structured around your entity type, not a generic checklist.

From there, our corporate services in Luxembourg span the practical steps that most businesses underestimate:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- RCS filing and liaison with Luxembourg authorities

- Business Permit application support

- Post-incorporation compliance management, including annual accounts and UBO register filings

- Banking introduction assistance for corporate account setup

Ready to move forward? Contact our team through Expanship Luxembourg to discuss your specific structure and timeline.

Frequently Asked Questions (FAQ)

The Société à Responsabilité Limitée (SARL) is the most frequently incorporated structure. Its lower minimum capital requirement of EUR 12,000 and single-shareholder eligibility make it accessible for small and medium-sized businesses.

Both structures allow full commercial activity within Luxembourg and access to its double tax treaty network, but the SA faces heavier ongoing obligations, including mandatory statutory audit requirements below certain thresholds and a minimum share capital of EUR 30,000. A SARL restricts the free transferability of shares and limits the number of shareholders to 100, while the SA can issue publicly tradable securities.

The Société en Commandite Spéciale (SCSp) does not require disclosure of the limited partners' identities in the Recueil Électronique des Sociétés et Associations (RESA) under ordinary circumstances. The general partner's identity is registered, but internal ownership arrangements among limited partners remain outside public commercial registers. Nominee arrangements are available within the bounds of anti-money laundering regulations under the law of 12 November 2004.

Not all structures permit single-founder formation. A SARL and SA can each be formed by one shareholder, while a Société en Nom Collectif (SNC) and Société en Commandite Simple (SCS) require at least two partners by statutory definition. The SCSp similarly requires a minimum of one general partner and one limited partner.

All principal commercial structures, including the SA, SARL, SCA, SNC, SCS, and SCSp, are available to non-resident founders without a residency requirement for shareholders. Directors of an SA or SARL who actively manage operations within the country may require a business permit issued by the Direction générale des Classes moyennes under the law of 2 September 2011. Foreign-held entities face the same tax and compliance obligations as domestically owned ones.

Conversion is permitted under Luxembourg corporate law, most commonly between the SARL and SA. A notarial deed is required, and the conversion must satisfy the capital and structural requirements of the target form. Transformation from a partnership such as the SNC into a capital company is also possible, subject to unanimous partner consent and compliance with capital adequacy rules.

The SCA and SCSp are the structures most frequently used for regulated and unregulated alternative investment fund vehicles. The SCSp, in particular, has become the standard vehicle for private equity and venture capital funds since its introduction in 2013, given its tax transparency and structural flexibility under the amended law of 10 August 1915.

No. The SCSp is the notable exception: it lacks legal personality under Luxembourg law, meaning it cannot hold assets, enter contracts, or sue in its own name. All other principal commercial forms, including the SA, SARL, SCA, SNC, and SCS, possess full legal personality upon registration with the Registre de Commerce et des Sociétés (RCS).

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.