Key Takeaways

- Forming a Société Anonyme (SA) or Sàrl in Luxembourg requires a mandatory notarized deed under the amended Company Law of 10 August 1915, adding procedural delay and notarial costs that do not apply in jurisdictions permitting online or self-certified incorporation.

- Luxembourg's substance requirements under domestic tax law oblige companies to maintain genuine local management, staffing, and premises, creating ongoing operational costs that exceed those of a nominal registered-address arrangement.

- Registration with both the Registre de Commerce et des Sociétés (RCS) and, where applicable, the CSSF involves multi-stage procedural requirements that extend formation timelines beyond what most non-EU investors accustomed to simpler regimes anticipate.

- Luxembourg's small domestic labor market constrains the availability of qualified local personnel needed to satisfy substance requirements, forcing many foreign-owned entities to compete for a limited pool of experienced professionals at above-average compensation levels.

Luxembourg operates under a heavily regulated corporate and financial framework, overseen by bodies such as the Commission de Surveillance du Secteur Financier (CSSF) and governed primarily by the amended Company Law of 10 August 1915. The disadvantages of incorporating in Luxembourg span procedural, financial, and operational dimensions that vary considerably depending on your chosen entity type, industry, and intended business activity.

Not every foreign investor will encounter the same friction points. A holding company has a substantially different compliance burden than a regulated fund structure or an active trading entity.

This article is most relevant to foreign entrepreneurs, non-EU investors, and multinational groups evaluating a Luxembourg subsidiary or regulated entity for the first time.

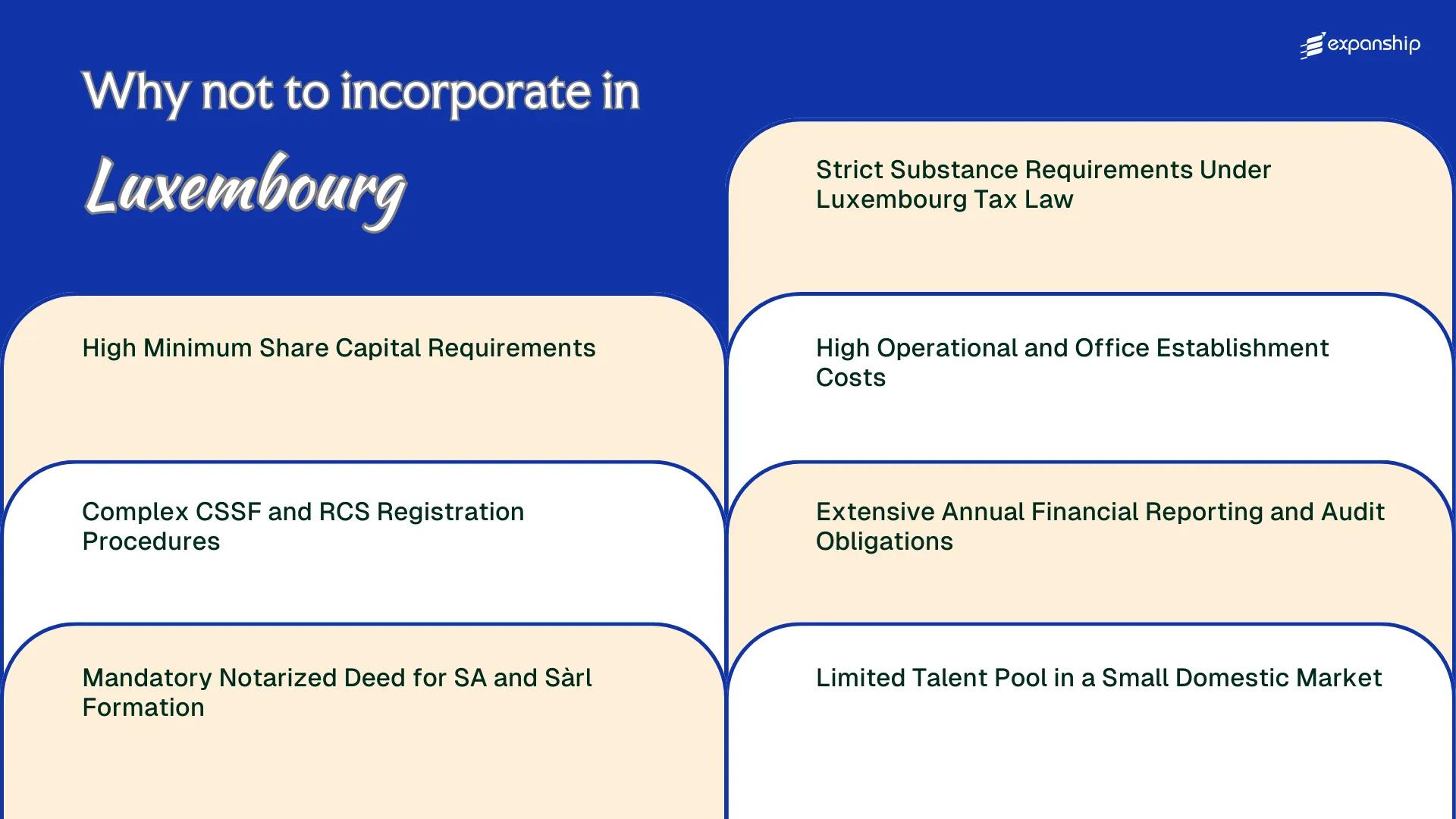

High Minimum Share Capital Requirements

Luxembourg minimum share capital requirements create a direct financial barrier before your business generates its first euro of revenue. The threshold varies by entity type, and for some structures, the amount is substantial.

Capital Thresholds by Entity Type

Under the amended law of 10 August 1915 on commercial companies, a société anonyme (SA) requires a minimum share capital of EUR 30,000, fully subscribed at incorporation. For many foreign founders accustomed to lower-threshold jurisdictions elsewhere in the EU, this represents a significant upfront commitment that sits locked in the entity rather than funding operations.

The société à responsabilité limitée (Sàrl) carries a lower minimum of EUR 12,000, but this figure still exceeds the nominal EUR 1 thresholds available in jurisdictions such as France or the United Kingdom.

Structural Restrictions on Capital Flexibility

For the SA specifically, at least 25% of each share's nominal value must be paid up at incorporation, with the remainder callable later. This staged payment structure does not eliminate the cash burden; it redistributes it, leaving your entity with contingent capital obligations on its balance sheet.

Sàrl share capital limitations in Luxembourg also include restrictions on the number of shareholders, capped at 100, which constrains equity-raising options compared to the SA format.

If your business enters financial difficulty before operations generate returns, the fully subscribed SA capital requirement means those funds are exposed to creditor claims from inception.

Complex CSSF and RCS Registration Procedures

Luxembourg CSSF registration challenges catch many foreign founders off guard, particularly those accustomed to single-window digital registration systems elsewhere in the EU.

Two separate regulatory tracks apply depending on your business type. Regulated financial entities must obtain authorisation from the Commission de Surveillance du Secteur Financier (CSSF) before operating, a process that requires submitting detailed business plans, fit-and-proper assessments of directors, IT infrastructure documentation, and internal control frameworks. For non-financial entities, registration with the Registre de Commerce et des Sociétés (RCS) through the Luxembourg Business Registers (LBR) portal is mandatory before any commercial activity begins.

The practical friction this creates for a foreign business owner includes:

- Preparing CSSF application dossiers in French or German imposes translation and legal advisory costs that are difficult to estimate upfront

- Fit-and-proper vetting of non-resident directors extends timelines unpredictably, delaying your operational launch

- RCS registration problems in Luxembourg can arise when foreign corporate documents require notarised apostilles, adding administrative cycles

- Parallel CSSF and RCS filings for holding structures with regulated subsidiaries require coordination across multiple legal workstreams simultaneously

Processing timelines at the CSSF for fund-related authorisations can extend to several months. That delay directly defers your ability to market to investors or generate revenue.

Company Incorporation in Luxembourg

Understand the full registration process across the CSSF and RCS before committing to a Luxembourg structure.

Mandatory Notarized Deed for SA and Sàrl Formation

Both the Société Anonyme and the Société à responsabilité limitée require a Luxembourg notarized deed at formation. This is not optional or replaceable with a standard private written agreement, meaning you cannot simply file incorporation documents with the Registre du Commerce et des Sociétés directly.

The obligation derives from the Luxembourg law of 10 August 1915 on commercial companies, as amended. Every deed must be executed before a Luxembourg notary, who charges fees on a sliding scale based on share capital and transaction complexity, making the notarial step a material cost line even for a modestly capitalized entity.

| Factor | Implication for Foreign Incorporators |

|---|---|

| Notary fee basis | Calculated proportionally on share capital value, not a flat administrative fee |

| Remote execution | Physical or power-of-attorney presence typically required; remote digital notarization not yet standard practice |

| Timeline added | Notary scheduling and deed registration extend incorporation timelines beyond a simple online filing |

| Language requirement | Deed must be executed in French, German, or Luxembourgish, requiring translation costs for non-speakers |

Your appointed notary also performs a substantive review of the articles of association before execution. If documents require revision, the process restarts, adding further delay.

For a foreign business owner unacquainted with civil law notarial systems, this creates an unavoidable gatekeeping layer. Unlike jurisdictions that permit company formation through a purely administrative or digital process, the Sàrl notarial deed requirement means professional intermediaries are structurally necessary, not merely convenient.

Strict Substance Requirements Under Luxembourg Tax Law

Luxembourg substance requirements tax law has become a genuine operational constraint for foreign-owned holding companies and intermediary structures established in the Grand Duchy. Under the ATAD framework and domestic anti-avoidance provisions, entities must demonstrate real economic presence to access treaty benefits and the participation exemption regime.

A shell structure with a registered address and no local personnel will not satisfy the Administration des contributions directes. Authorities assess whether decision-making genuinely occurs in Luxembourg, which means passive holding vehicles face direct scrutiny.

For foreign groups, the cost of satisfying these conditions is material. Appointing qualified resident directors, maintaining a functional office, and holding board meetings locally all generate recurring expenditure with no equivalent in jurisdictions that impose lighter substance thresholds.

Luxembourg tax substance rules restrictions apply with particular force to intra-group financing and IP holding entities, where the OECD BEPS framework has further tightened the standard.

- At least one qualified Luxembourg-resident director must participate in substantive decision-making

- Board minutes must reflect that key decisions were made locally, not rubber-stamped from abroad

- IP and financing entities face additional substance benchmarks under BEPS Action 5 and local implementation

- The Administration des contributions directes can deny treaty benefits to entities failing substance tests

- Substance must be maintained continuously, not only at the time of incorporation

Luxembourg holding company substance challenges mean that even a fully compliant SA with proper local directors can lose its participation exemption eligibility if the economic substance is later found to have lapsed between annual reviews.

High Operational and Office Establishment Costs

Luxembourg business operational costs drawbacks extend well beyond incorporation fees, affecting the day-to-day financial structure of any foreign-owned entity.

The Cost of Physical Presence

Securing a registered office in Luxembourg City, where most financial and holding entities are based, carries significant expense. Grade-A commercial space in the capital consistently ranks among the highest-priced in the eurozone, and regulators expect substance to be genuine, meaning a letterbox address rarely satisfies compliance expectations under the amended 2019 substance framework.

What This Means for Foreign-Owned Entities

Running payroll in Luxembourg compounds the cost burden further, as the country's mandatory minimum wage is one of the highest in the European Union. For a foreign business owner who assumed a holding or investment vehicle would operate lightly, the combination of qualified local staff, real office space, and associated administrative overhead can substantially exceed initial projections. This cost structure applies regardless of whether your entity generates revenue domestically.

Managing Operational Cost Challenges in Luxembourg

Understand the full cost implications of establishing and maintaining a compliant business presence in Luxembourg before committing to incorporation.

Extensive Annual Financial Reporting and Audit Obligations

Luxembourg annual financial reporting obligations extend well beyond basic bookkeeping, placing structured disclosure and audit demands on most commercial entities regardless of size.

- All SAs are subject to statutory audit under the amended law of 19 December 2002, requiring appointment of a réviseur d'entreprises agréé, which adds recurring professional fees to your annual cost base.

- Sàrls exceeding two of three thresholds — balance sheet total of EUR 4.4 million, net turnover of EUR 8.8 million, or 50 employees — also trigger mandatory audit, meaning growth itself escalates compliance costs.

- Annual accounts must be filed with the Registre de Commerce et des Sociétés within one month of approval, and late filing carries financial penalties.

- Consolidated accounts are required under specific conditions governed by the law of 19 July 2004, creating a separate reporting layer for group structures.

- Foreign-owned entities without local finance personnel must typically outsource these obligations, converting a statutory requirement into an ongoing third-party expense.

Limited Talent Pool in a Small Domestic Market

Luxembourg's talent pool limitations are a structural constraint tied directly to the country's population of roughly 660,000 people. For firms requiring specialized professionals in areas like fund administration, compliance, or financial technology, domestic supply is quickly exhausted.

The grand duchy relies heavily on cross-border workers, who account for approximately 47% of the employed workforce according to STATEC, Luxembourg's national statistics institute. Recruiting cross-border commuters from Belgium, France, and Germany introduces scheduling dependencies and limits your ability to build on-site teams with consistent availability.

Salary expectations compound this pressure. Competition for qualified professionals among the high concentration of financial institutions, EU institutions, and international firms drives compensation well above regional averages, which directly inflates your operational payroll costs.

Multilingual requirements add another layer of difficulty. Many roles require fluency in Luxembourgish, French, and German alongside English, which narrows the qualified candidate pool further when hiring locally.

A fintech firm establishing a ten-person compliance team in Luxembourg City could face average annual salaries exceeding €80,000–€95,000 per role, based on financial sector pay benchmarks reported by Michael Page Luxembourg's 2023 salary guide, resulting in a payroll base of €800,000–€950,000 annually before social contributions.

Navigating These Disadvantages Effectively

Overcoming Luxembourg incorporation drawbacks requires structural planning before the company is formed, not after. The jurisdiction's regulatory architecture does not accommodate reactive compliance.

- Elect the Sàrl-S vehicle if eligible, as it reduces minimum share capital to €1 and bypasses the standard notarised deed requirement under the 2016 reform.

- Establish genuine economic substance from incorporation by appointing resident directors and securing a registered operational address to satisfy the OECD-aligned substance rules enforced by the Luxembourg tax authorities.

- Register directly with the RCS through the Luxembourg Business Registers portal to ensure filings meet statutory timelines and avoid administrative rejection.

- Budget for mandatory annual audit fees if your entity meets the thresholds triggering statutory audit obligations under the Luxembourg law on commercial companies.

- Source talent through cross-border hiring within the EU single market to offset the constraints of the domestic labour pool.

These steps address the structural and compliance dimensions of operating a business here, though they do not remove the underlying regulatory obligations. The CSSF, Luxembourg tax authorities, and RCS each maintain independent oversight functions that operate concurrently.

Luxembourg's Overall Appeal for Businesses

Despite the disadvantages covered in this blog, Luxembourg remains a credible incorporation destination for foreign businesses that can meet its regulatory and financial thresholds. The Grand Duchy's position as an EU member state, its established investment fund framework under the CSSF, and its network of double tax treaties create a verifiable foundation that many jurisdictions cannot match.

| Pros | Cons |

|---|---|

| EU-domiciled entity with access to single market passporting rights | SA and Sàrl formation requires a notarized deed, adding procedural time and cost |

| Extensive double tax treaty network reduces withholding tax exposure | Strict economic substance requirements under Luxembourg tax law demand genuine local presence |

| CSSF-regulated environment provides institutional credibility for fund structures | CSSF and RCS registration procedures involve multiple filings across distinct regulatory bodies |

| No ceiling on foreign ownership in most standard entity types | High operational and office establishment costs relative to peer EU jurisdictions |

| Stable legal framework under Luxembourg company law (law of 10 August 1915) | Limited domestic talent pool constrains local hiring for staffing substance obligations |

Compliance Services for Companies in Luxembourg

Meet your annual filing, audit, and regulatory obligations under Luxembourg law, including RCS submissions, financial reporting, and CSSF-related requirements.

Conclusion

Luxembourg holds a well-established position as a European financial and holding company hub, yet the Luxembourg incorporation disadvantages summary is clear: structural costs, regulatory obligations, and substance requirements create genuine friction for many businesses. The mandatory notarized deed for SA and Sàrl formation, the CSSF oversight for regulated entities, and the RCS registration process each add time and professional fees that compound quickly. Substance requirements under Luxembourg tax law further restrict how your firm can operate. Structural preparation before registration reduces exposure to these constraints considerably.

Expanship's Luxembourg Incorporation Support

From managing notarized deed requirements with a Luxembourg notary to satisfying substance criteria under Luxembourg tax law, the compliance obligations tied to Luxembourg company formation support services are specific and resource-intensive. Expanship works alongside your business to reduce the operational burden these requirements place on your team during and after incorporation.

Our support spans the full formation and post-incorporation cycle:

- We prepare and file all registration documents with the Registre de Commerce et des Sociétés on your behalf.

- A registered agent and office address in Luxembourg are provided to satisfy local presence requirements.

- We liaise directly with the CSSF, RCS, and other relevant authorities throughout the filing process.

- Ongoing compliance obligations, including annual filings and reporting deadlines, are managed for your entity.

- We facilitate introductions to Luxembourg banking institutions familiar with foreign-owned structures.

- Tax registration and liaison with the Administration des Contributions Directes are handled as part of your setup.

Reach out to Expanship Luxembourg to discuss how we can support your incorporation process.

Frequently Asked Questions (FAQ)

No, but it applies to the two most commonly used structures. Both the SA and the Sàrl require formation through a notarized deed before a Luxembourg notary, which adds professional fees and scheduling delays to the setup timeline. Simpler structures like the société en nom collectif are not subject to the same notarial requirement, though they carry unlimited liability, which makes them unsuitable for most commercial purposes.

Without genuine economic substance, your firm risks losing access to Luxembourg's tax treaty network and the participation exemption regime. The Luxembourg tax authorities can reclassify income or deny treaty benefits entirely if the entity is deemed a shell, particularly following the Anti-Tax Avoidance Directives (ATAD I and ATAD II) transposed into Luxembourg law. Substance failures can also trigger reputational scrutiny from the Luxembourg Inland Revenue (Administration des contributions directes).

For regulated entities such as investment fund managers or payment institutions, CSSF authorization fees and ongoing supervisory levies can run into tens of thousands of euros annually, separate from legal and compliance advisory costs. The application process itself is document-intensive and can take six to twelve months, meaning your business absorbs professional fees well before it is authorized to operate. Unregulated commercial companies do not deal with the CSSF directly, but any financial services activity triggers that layer of cost.

Luxembourg's audit threshold is lower than Ireland's and broadly comparable to the Netherlands, but the combination of Luxembourg GAAP reporting, mandatory RCS filings, and the requirement for a réviseur d'entreprises agréé for many entity types makes the annual compliance burden particularly layered. SAs are subject to statutory audit regardless of size, which is a stricter default than in several peer jurisdictions. For small commercial entities, that creates a fixed annual cost that does not scale down with turnover.

Partially, but substance requirements complicate a fully remote model. If your entity needs to demonstrate genuine local management and decision-making to satisfy Luxembourg tax law, key personnel must be physically present and active in the Grand Duchy. Hiring all operational staff abroad while maintaining only a registered address in Luxembourg is precisely the arrangement regulators scrutinize most closely, and it puts treaty access and tax residency status at risk.

Failure to file annual accounts with the Registre de Commerce et des Sociétés (RCS) within the statutory deadline can result in administrative fines and, in persistent cases, court-ordered dissolution of the entity. Directors bear personal responsibility for ensuring timely filing under the Luxembourg Commercial Companies Law (loi du 10 août 1915 sur les sociétés commerciales, as amended). Repeated non-compliance also damages the company's standing with counterparties and financial institutions that conduct RCS due diligence checks.

Larger operations feel the constraint most acutely, but even a small firm requiring bilingual financial professionals or sector-specific compliance expertise will encounter competition from the fund industry and major financial institutions that dominate the local hiring market. Luxembourg's population of roughly 660,000 means the domestic supply of qualified professionals in finance, law, and accounting is structurally limited. Firms that require a team of ten or more locally-based staff often find themselves competing directly with global banks and fund administrators for the same narrow candidate pool.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.