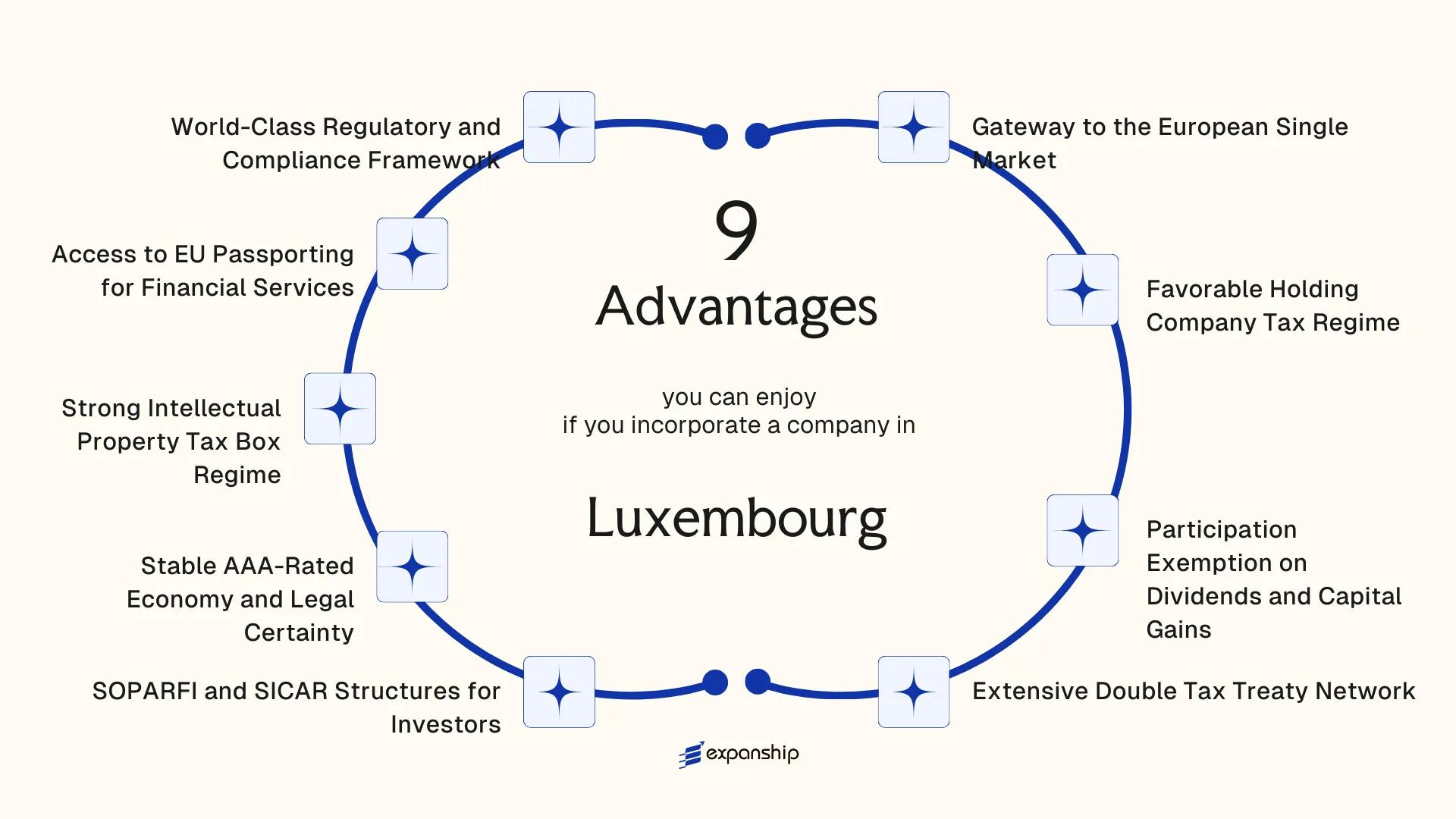

Key Takeaways

- Luxembourg's participation exemption regime eliminates corporate tax on qualifying dividends and capital gains received from subsidiaries, making it a structurally efficient base for multi-jurisdictional holding structures.

- Under Article 50ter of the Income Tax Law, income derived from qualifying intellectual property benefits from a reduced effective tax rate, providing a codified advantage for IP-intensive businesses registered in the jurisdiction.

- With over 80 bilateral double tax treaties in force, Luxembourg-incorporated entities can substantially reduce withholding tax exposure on cross-border income flows involving major trading and investment partners.

- Regulated financial services firms incorporated in Luxembourg can passport their authorizations across EU member states without requiring separate licensing in each jurisdiction, a direct consequence of the EU's single market framework that the jurisdiction is fully positioned to deliver.

Situated in the heart of Western Europe, Luxembourg is a sovereign Grand Duchy bordered by Belgium, France, and Germany, giving businesses incorporated there direct physical proximity to the continent's largest economies. Company registration falls under the oversight of the Luxembourg Business Registers, which administers filings and maintains the Registre de Commerce et des Sociétés. Foreign businesses most commonly establish a Société à Responsabilité Limitée when entering the market.

The tax posture is treaty-based and territorial in character, with an extensive network of bilateral agreements shaping how cross-border income is treated. Foreign ownership faces no general statutory restrictions, and the jurisdiction consistently ranks among the top recipients of foreign direct investment in Europe relative to GDP. Non-resident shareholders may hold 100% of a locally registered entity without requiring a domestic co-owner.

The benefits of incorporating in Luxembourg span tax structuring, regulatory access, and legal predictability. This article examines the concrete advantages your business can expect from a Luxembourg company formation.

Gateway to the European Single Market

Luxembourg's position at the geographic and institutional centre of the EU gives incorporated entities direct Luxembourg access to EU single market without the friction of cross-border re-establishment. A company registered under Luxembourg law operates within a jurisdiction that is a full EU member state, subject to EU regulations and directives from day one.

Operating Under EU Law From Incorporation

Any entity incorporated in Luxembourg is automatically subject to EU treaties, directives, and regulations. This means your business can sell goods, provide services, and move capital across all 27 member states under the same legal framework that governs domestic EU operators — no separate market-entry filings required per country.

What Single Market Membership Means in Practice

Incorporating in Luxembourg for European market access eliminates the need to establish a locally regulated entity in each target country for many commercial activities. Regulations such as the EU Prospectus Regulation and AIFMD apply directly, giving your firm recognised standing across member states under a single regulatory authorisation rather than fragmented national approvals.

One Luxembourg registration can serve as your legal operating base across all 27 EU member states.

Favorable Holding Company Tax Regime

Luxembourg holding company tax advantages stem from a clearly defined statutory framework, not informal policy. The primary vehicle is the SOPARFI (Société de Participations Financières), a standard commercial company that qualifies for a specific tax treatment under the Luxembourg Income Tax Law (Loi concernant l'impôt sur le revenu).

At the corporate level, the standard combined rate sits at approximately 24.94% in Luxembourg City, covering corporate income tax, municipal business tax, and the solidarity surcharge. For a holding structure, however, the effective rate on qualifying investment income can fall substantially below this figure, because dividend income and capital gains meeting specific ownership thresholds are largely exempt from taxation.

The SOPARFI tax regime advantages are rooted in domestic law, not dependent on treaty access alone. This distinction matters for your business because it provides a stable, predictable base that does not shift with bilateral renegotiations.

Why the conditions attached to this regime work in your favour:

- The minimum participation threshold of 10% or an acquisition cost of EUR 1.2 million is a fixed statutory bar, not a discretionary test

- The required holding period of 12 months applies uniformly, making planning straightforward

- The regime covers both resident and qualifying non-resident subsidiaries, widening the structure's practical scope

Incorporate a Holding Company in Luxembourg

Set up a SOPARFI or other qualifying entity in Luxembourg with full compliance support across registration, structuring, and ongoing obligations.

Participation Exemption on Dividends and Capital Gains

Under Article 166 of the Luxembourg Income Tax Law (LITL), the Luxembourg participation exemption on dividends and capital gains eliminates corporate tax on qualifying income derived from subsidiary holdings. For a foreign investor structuring a holding entity in the Grand Duchy, this means dividend income and gains from share disposals can flow through the holding company without triggering corporate income tax or municipal business tax at the Luxembourg level.

To qualify, your company must hold at least 10% of the subsidiary's share capital, or alternatively acquire a participation with a minimum acquisition cost of EUR 1.2 million for dividends or EUR 6 million for capital gains. The holding period required is at least 12 months of uninterrupted ownership.

| Income Type | Minimum Participation | Minimum Holding Period |

|---|---|---|

| Dividends | 10% or EUR 1.2M acquisition cost | 12 months |

| Capital Gains | 10% or EUR 6M acquisition cost | 12 months |

The subsidiary must also be a qualifying entity, either a fully taxable Luxembourg resident company, an EU entity covered by the Parent-Subsidiary Directive, or a non-EU company subject to a comparable tax regime. This qualifying entity requirement prevents the exemption from applying to purely low-taxed shell structures, which gives your overall corporate architecture greater defensibility against anti-avoidance scrutiny. For groups managing multiple subsidiaries across jurisdictions, concentrating ownership through a Luxembourg holding firm means accumulated profits and exit gains can be repatriated or reinvested without erosion at the intermediate holding level.

Extensive Double Tax Treaty Network

Luxembourg's double tax treaty network benefits foreign businesses through one of the widest treaty frameworks in Europe. As of 2024, the Grand Duchy has signed over 80 bilateral tax treaties, covering major economies across North America, Asia, the Middle East, and Africa. For a holding or finance entity, this means dividend flows, royalties, and interest payments can cross borders with significantly reduced withholding taxes — often to rates between 0% and 5%.

Treaties are governed under Luxembourg's domestic tax law alongside the OECD Model Convention framework. The practical effect is direct: where a non-treaty country might impose 25–30% withholding on outbound dividends, your Luxembourg entity can reduce that liability substantially by interposing a properly structured vehicle.

For foreign investors routing capital through a Luxembourg holding company, treaty access is conditional on meeting substance requirements under domestic anti-abuse rules and the EU Anti-Tax Avoidance Directives (ATAD I and II). Treaty shopping without genuine economic substance will not qualify.

Keep these points in mind:

- Confirm the specific treaty between Luxembourg and your target jurisdiction before structuring

- Substance requirements must be satisfied at the Luxembourg entity level

- Withholding rates vary by treaty; dividend, interest, and royalty provisions differ within the same agreement

- ATAD I and II compliance is mandatory for treaty-based structures

Luxembourg's treaty with the United Arab Emirates — a non-EU, no-income-tax jurisdiction — allows UAE investors to benefit from reduced withholding rates on Luxembourg-sourced income, a combination that most investors assume is unavailable without an EU-resident counterparty.

SOPARFI and SICAR Structures for Investors

Luxembourg SOPARFI and SICAR benefits for investors stem from two distinct legal forms that serve fundamentally different purposes, each backed by a precise regulatory framework rather than general enabling legislation.

SOPARFI as a Holding and Finance Vehicle

A SOPARFI (Société de Participations Financières) is not a regulated fund but a standard commercial company, typically incorporated as an S.A. or S.à r.l., that accesses Luxembourg's participation exemption regime under Article 166 of the Income Tax Law. This distinction matters because it means a SOPARFI operates without CSSF oversight as an investment vehicle, reducing ongoing regulatory burden while still qualifying for full exemption on dividends and capital gains from qualifying participations. Your firm must hold at least 10% or an acquisition cost of EUR 1.2 million in a subsidiary for a minimum of 12 months to meet eligibility thresholds.

SICAR as a Regulated Private Equity Structure

Governed by the Law of 15 June 2004, a SICAR (Société d'Investissement en Capital à Risque) is specifically designed for private equity and venture capital, reserved for well-informed investors with a minimum commitment of EUR 125,000. Tax treatment at the SICAR level exempts income and gains derived from securities held for risk capital purposes, which allows carried interest and portfolio returns to pass through without corporate-level taxation on qualifying assets. The CSSF supervises SICARs, which adds a layer of regulatory credibility that institutional co-investors and fund-of-funds typically require before committing capital.

Structure Your Luxembourg Investment Vehicle Correctly

Get expert guidance on whether a SOPARFI or SICAR fits your investment strategy, ownership structure, and regulatory requirements.

Stable AAA-Rated Economy and Legal Certainty

Rated AAA by all three major credit agencies, Moody's, S&P, and Fitch, Luxembourg's sovereign credit standing reflects a pattern of fiscal discipline and structural economic stability that has persisted across decades. For a foreign business owner, that rating is not symbolic. It signals that the banking sector, public institutions, and financial infrastructure operate within a predictable and well-capitalized environment, which directly reduces counterparty and operational risk for entities incorporated there.

- Legal certainty is grounded in codified civil law, with commercial activity governed primarily by the amended law of 10 August 1915 on commercial companies. Courts interpret that law consistently, and the legal framework has not undergone disruptive restructuring, giving your entity a stable contractual and statutory foundation.

- Political stability reinforces this predictability. Coalition governments have maintained continuity in economic and regulatory policy across administrations, meaning the tax and corporate rules your business relies on today are unlikely to shift abruptly.

- The Commission de Surveillance du Secteur Financier (CSSF) and the Commissariat aux Assurances (CAA) operate under EU-aligned mandates. Regulatory decisions follow transparent, rule-based processes, reducing exposure to discretionary or inconsistent enforcement that foreign businesses often encounter in less institutionalized markets.

Strong Intellectual Property Tax Box Regime

Luxembourg IP box regime tax benefits are grounded in Article 50ter of the Income Tax Law (Loi concernant l'impôt sur le revenu), which provides an 80% income exemption on qualifying net IP income. The effective tax rate on that income therefore falls to approximately 5.2%, against a standard corporate rate of around 24.94%.

Qualifying assets include patents, software protected by copyright, and certain other IP rights developed or acquired through qualifying R&D activity. Income derived from licensing, royalties, or the embedded IP component of product sales can fall within scope, giving multinationals a mechanism to align IP holding with tax efficiency inside an EU member state.

The regime conforms to the OECD's modified nexus approach under BEPS Action 5, requiring a genuine economic link between the IP income and R&D expenditure incurred by the entity itself. This compliance with international standards reduces treaty challenge risk and satisfies substance requirements that purely offshore IP structures cannot meet.

Hypothetical scenario: A software firm earns €2,000,000 in annual royalty income. Under the 80% exemption, only €400,000 is subject to corporate tax. At the 24.94% standard rate, the effective tax charge is approximately €99,760, compared to €498,800 without the regime, a saving of roughly €399,040 per year.

Access to EU Passporting for Financial Services

Luxembourg EU passporting financial services benefits are grounded in the country's status as a regulated EU member state, which allows financial firms incorporated there to operate across all 27 EU member states under a single authorization.

Under the EU passporting framework, a firm authorized by the Commission de Surveillance du Secteur Financier (CSSF) can provide services into other member states without obtaining separate licenses in each. For fund managers and investment firms, this removes a significant structural barrier to cross-border distribution.

Key passporting rights available through a Luxembourg authorization include:

- UCITS passport: allows retail fund distribution across the EU under Directive 2009/65/EC

- AIFMD passport: grants access for marketing alternative funds to professional investors under Directive 2011/61/EU

- MiFID II passport: covers investment firms providing services across member states under Directive 2014/65/EU

Luxembourg AIFMD and UCITS passporting advantages are particularly relevant for asset managers targeting European institutional and retail investors. Authorization in one jurisdiction, rather than 27, means lower legal costs and faster market entry timelines.

Passporting rights apply only to entities holding a valid CSSF authorization in the relevant regulated category; an unregulated holding company does not carry these rights.

World-Class Regulatory and Compliance Framework

Luxembourg's regulatory framework advantages for companies stem largely from how its supervisory architecture is structured. The Commission de Surveillance du Secteur Financier (CSSF) serves as the primary financial sector regulator, overseeing banks, investment funds, payment institutions, and fintech operators under a single authority. That consolidated oversight model reduces the administrative fragmentation that often affects businesses operating across multiple EU regulatory bodies.

Predictable Regulatory Conduct

CSSF oversight benefits businesses specifically because the authority publishes detailed circulars and formal guidance on regulatory expectations. This transparency means your legal and compliance teams can build internal frameworks against published standards rather than interpreting vague regulatory intent. The regulator's engagement approach, which includes pre-application meetings for fund authorization and licensing procedures, gives foreign firms a defined pathway before committing significant capital.

AML and Substance Requirements

The compliance framework for foreign investors is anchored in EU directives transposed through local legislation, including the Law of 12 November 2004 on combating money laundering and terrorist financing, as amended. Substance requirements under Luxembourg tax and company law mean that firms registered here must demonstrate genuine operational presence, which in practice protects against treaty abuse challenges from other jurisdictions.

Legal Form and Filing Infrastructure

- Annual accounts must be filed with the Luxembourg Trade and Companies Register (Registre de Commerce et des Sociétés)

- Société Anonyme (SA) and Société à Responsabilité Limitée (SARL) entities follow distinct capital and reporting requirements under the Law of 10 August 1915 on commercial companies

- Accounting standards align with both Luxembourg GAAP and IFRS, giving multinational groups flexibility in consolidated reporting

Why Luxembourg Outshines Competing EU Jurisdictions

Comparing Luxembourg vs other EU jurisdictions for incorporation reveals a pattern that goes beyond headline tax rates. The jurisdictions most frequently evaluated alongside Luxembourg, namely the Netherlands, Ireland, and Belgium, share a common profile: EU membership, treaty depth, and holding-friendly tax rules. Where they diverge is in structural specificity, regulatory stability, and the breadth of compliant vehicles available to foreign investors.

Ireland's 12.5% corporate rate draws attention, but its participation exemption framework carries conditions that can limit its utility for complex multi-tier structures. Belgium's notional interest deduction was reformed significantly under its 2018 tax reform, narrowing its prior advantage. The Netherlands introduced a conditional withholding tax on dividends paid to low-tax jurisdictions from 2021, adding a compliance layer absent in Luxembourg's outbound dividend framework for qualifying SOPARFI structures.

| Parameter | Luxembourg | Netherlands | Ireland | Belgium |

|---|---|---|---|---|

| Participation Exemption (Dividends) | 100% exempt (qualifying conditions) | 100% exempt (subject to conditions) | Available with restrictions | Available, post-2018 reform |

| IP Box Effective Rate | ~5.2% (80% income exemption) | 9% (OECD-compliant) | 6.25% (Knowledge Development Box) | 3.75% effective (Innovation Income Deduction) |

| Regulated Fund Vehicles | SICAR, SIF, RAIF, SICAV | Limited equivalent | ICAV, QIAIF | Limited equivalent |

| CSSF / Equivalent Regulator | CSSF | AFM / DNB | Central Bank of Ireland | FSMA |

| Withholding Tax on Outbound Dividends | 15% standard; exemptions apply | 15%; conditional WHT from 2021 | 25%; broad treaty relief | 30%; reduced via treaties |

| SOPARFI Equivalent | SOPARFI (specific statutory vehicle) | BV / NV (no dedicated holding law) | No dedicated holding vehicle | No dedicated holding vehicle |

Compliance Services for Companies in Luxembourg

Maintain good standing with CSSF requirements, annual filings, and ongoing statutory obligations for your Luxembourg entity.

Conclusion

Luxembourg's position as a holding company and fund domicile within the EU is built on concrete structural features: a participation exemption regime that eliminates tax on qualifying dividends and capital gains, an IP box regime governed by Article 50ter of the Income Tax Law, and access to the EU's passporting framework for regulated financial services. These are not incidental advantages but features that directly reduce tax friction and regulatory duplication for cross-border business structures.

The benefits of incorporating in Luxembourg are most pronounced for businesses that hold subsidiaries across multiple jurisdictions, manage intellectual property, or operate regulated financial products across the EU. A firm's specific situation, including its ownership structure, the nature of its income, and its investor base, will determine how much of this framework applies in practice.

Determining whether this jurisdiction fits your structure requires accurate interpretation of the relevant laws, including the Law of 10 August 1915 on commercial companies and the conditions set by the Luxembourg tax authorities under LIR provisions. Getting that assessment right from the outset shapes the long-term efficiency of the entity you establish.

Start Your Luxembourg Company with Expanship Today

Incorporating in Luxembourg with Expanship means working with a team that understands the specific requirements of the Registre de Commerce et des Sociétés (RCS), the Société à Responsabilité Limitée and SOPARFI structures discussed throughout this blog, and the compliance obligations that attach to each. From the IP box regime under Article 50ter of the Income Tax Law to participation exemption thresholds, the regulatory detail matters — and errors at formation stage create downstream liability.

Expanship's service scope across Luxembourg company formation covers the full administrative cycle:

- Preparation and notarization of incorporation documents, including articles of association

- Registered agent and registered office provision in compliance with RCS requirements

- Filing coordination with the RCS and liaison with the Administration des contributions directes where applicable

- Post-incorporation compliance management, including annual filing obligations and director register maintenance

- Assistance with corporate bank account introductions for newly incorporated entities

- Support with VAT registration through the Administration de l'enregistrement, des domaines et de la TVA

Your business engages with one of Europe's most technically demanding jurisdictions for corporate structuring. Getting the formation right from the outset protects the tax positions and structural advantages that make this jurisdiction worth choosing.

Reach out to Expanship Luxembourg to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

A SOPARFI incorporated as a Société à Responsabilité Limitée requires a minimum share capital of EUR 12,000, while a Société Anonyme requires EUR 30,000, of which at least 25% must be paid up at the time of incorporation. The SOPARFI is not a distinct legal form but rather a standard commercial company that uses Luxembourg's participation exemption regime to optimize holding and financing activities. No special license is required to operate as a SOPARFI, which distinguishes it from regulated vehicles such as the SICAR.

Under Article 166 of the Luxembourg Income Tax Law, dividends received from a qualifying subsidiary are fully exempt from corporate income tax, provided the Luxembourg parent holds at least 10% of the subsidiary's share capital, or an acquisition cost of at least EUR 1.2 million, for an uninterrupted period of twelve months. The subsidiary must also be a resident of a country with which Luxembourg has a tax treaty or be subject to a tax comparable to Luxembourg's corporate income tax. The exemption applies equally to liquidation proceeds distributed by the subsidiary.

Incorporation through a Luxembourg notary typically takes between five and ten business days once all required documentation has been submitted and verified. Registration with the Luxembourg Trade and Companies Register (Registre de Commerce et des Sociétés) and publication in the Recueil Electronique des Sociétés et Associations follow notarial deed execution and generally add a few additional days. Delays most commonly arise from incomplete due diligence documentation or pending apostille certifications on foreign-issued identity documents.

Treaty eligibility is not formally conditioned on having a local director, but substance requirements under Luxembourg's anti-abuse provisions and the OECD's Base Erosion and Profit Shifting framework make genuine management and control within the country a practical necessity. Tax authorities in counterparty states may challenge treaty benefits if the entity lacks demonstrable decision-making activity in Luxembourg, such as board meetings held locally by qualified directors. The Luxembourg tax administration has also issued circulars reinforcing that entities must have sufficient economic substance to be respected as the beneficial owner of income.

If a company fails to maintain the required nexus between qualifying research and development expenditure and income from qualifying intellectual property assets, the proportion of IP income eligible for the 80% exemption under Article 50ter of the Luxembourg Income Tax Law is reduced accordingly. The exemption is calculated based on the ratio of qualifying expenditure to total expenditure on the relevant asset, so a reduction in eligible R&D spending directly reduces the tax benefit without disqualifying the regime entirely. Companies are expected to document their expenditure allocation on an ongoing basis to substantiate the nexus fraction in the event of an audit.

The two jurisdictions are structurally comparable, and the preferable choice depends on the specific asset class, investor base, and treaty requirements of the group. Luxembourg holds an advantage for investment fund structures and certain private equity arrangements, given the depth of its regulated fund infrastructure and the availability of vehicles such as the SICAR and the Reserved Alternative Investment Fund. The Netherlands may be preferred where specific treaty positions or the Dutch cooperative structure offer advantages for particular transaction types, but Luxembourg's treaty network of over 85 agreements and its EU Directive access make it a direct alternative for most holding and financing mandates.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.