Key Takeaways

- Liechtenstein's Commercial Register is maintained by the Office of Justice (Amt für Justiz), which oversees the registration and compliance of all recognized business entity types in the principality.

- The Anstalt (Establishment) is a distinctly Liechtenstein legal instrument with no direct equivalent elsewhere in Europe, making it unique among the structures available for asset-holding and special-purpose functions.

- Entity selection among the AG, GmbH, Stiftung, and other forms carries distinct consequences for liability, governance, and tax treatment under Liechtenstein's low-rate corporate income tax regime.

- Regulatory oversight by the Financial Market Authority (FMA) operates in alignment with FATF and OECD standards, shaping ongoing compliance obligations for businesses formed under the Personen- und Gesellschaftsrecht (PGR).

Introduction to Entity Types in Liechtenstein

Liechtenstein is a landlocked principality in Central Europe, bordered by Switzerland to the west and Austria to the east. It is an independent constitutional monarchy and a member of the European Economic Area (EEA), which shapes the regulatory framework governing business entity types in Liechtenstein.

Company registration and oversight fall under the Office of Justice (Amt für Justiz), which maintains the Commercial Register (Handelsregister). The principality operates a low-tax regime, with corporate income tax rates among the lowest in Europe.

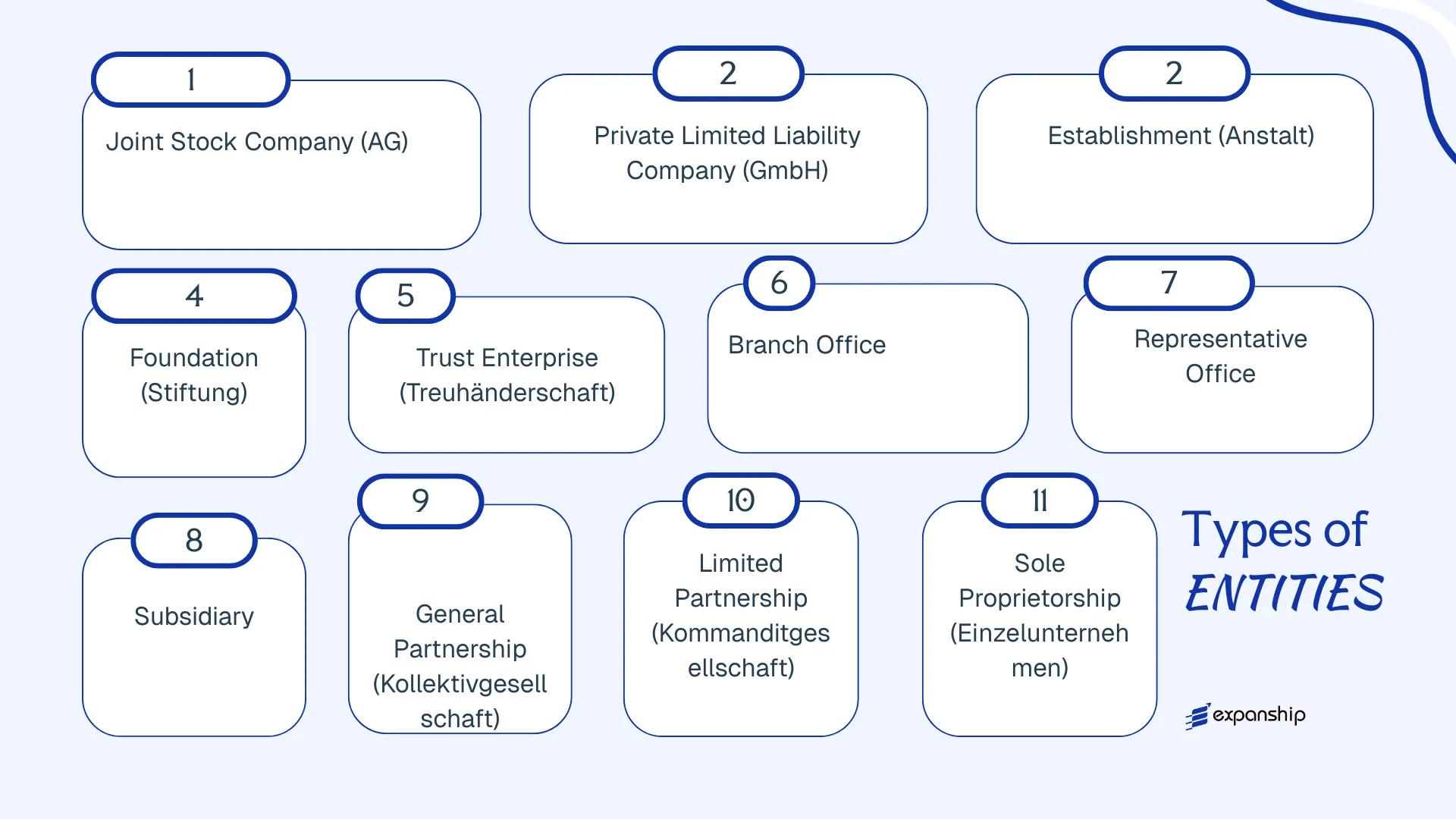

Businesses operating here can be structured as one of several legally recognized forms: Aktiengesellschaft (AG), Gesellschaft mit beschränkter Haftung (GmbH), Anstalt, Stiftung, Trust Enterprise (Treuhänderschaft), General Partnership (Kollektivgesellschaft), Limited Partnership (Kommanditgesellschaft), Sole Proprietorship (Einzelunternehmen), or as a foreign branch or representative office.

Each structure carries distinct implications for liability, governance, taxation, and compliance obligations. This article examines each corporate structure in detail to help you determine which form suits your business objectives.

An Overview of Business Structures in Liechtenstein

Liechtenstein's company law framework accommodates a broad range of entity types, governed primarily by the Persons and Companies Act (Personen- und Gesellschaftsrecht, PGR) of 1926, which has been amended several times since. The PGR is one of the most structurally diverse corporate statutes in Europe, covering everything from joint stock companies to foundations and trust enterprises. Each structure carries distinct legal characteristics suited to different commercial, asset-holding, or administrative purposes.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| AG (Joint Stock Company) | Corporation | Limited to share capital | Taxed | Permitted | 1 shareholder | Office of Justice (Amt für Justiz) | PGR |

| GmbH (Private Limited Company) | Corporation | Limited to share capital | Taxed | Permitted | 1 shareholder | Office of Justice | PGR |

| Anstalt (Establishment) | Hybrid entity | Limited | Taxed or exempt | Permitted | 1 founder | Office of Justice | PGR |

| Stiftung (Foundation) | Non-membership body | N/A | Taxed or exempt | Restricted | 1 founder | Office of Justice | PGR |

| Trust Enterprise (Treuhänderschaft) | Fiduciary structure | Limited | Taxed | Restricted | 1 trustee | Office of Justice | PGR |

| General Partnership (Kollektivgesellschaft) | Partnership | Unlimited | Taxed | Permitted | 2 partners | Office of Justice | PGR |

| Limited Partnership (Kommanditgesellschaft) | Partnership | Mixed | Taxed | Permitted | 2 partners | Office of Justice | PGR |

| Branch Office | Foreign extension | Parent liable | Taxed | Permitted | Parent company | Office of Justice | PGR |

| Representative Office | Foreign presence | Parent liable | Generally exempt | Not permitted | Parent company | Office of Justice | PGR |

| Sole Proprietorship (Einzelunternehmen) | Individual trader | Unlimited | Taxed | Permitted | 1 individual | Office of Justice | PGR |

Each of these structures is examined in full in the sections below.

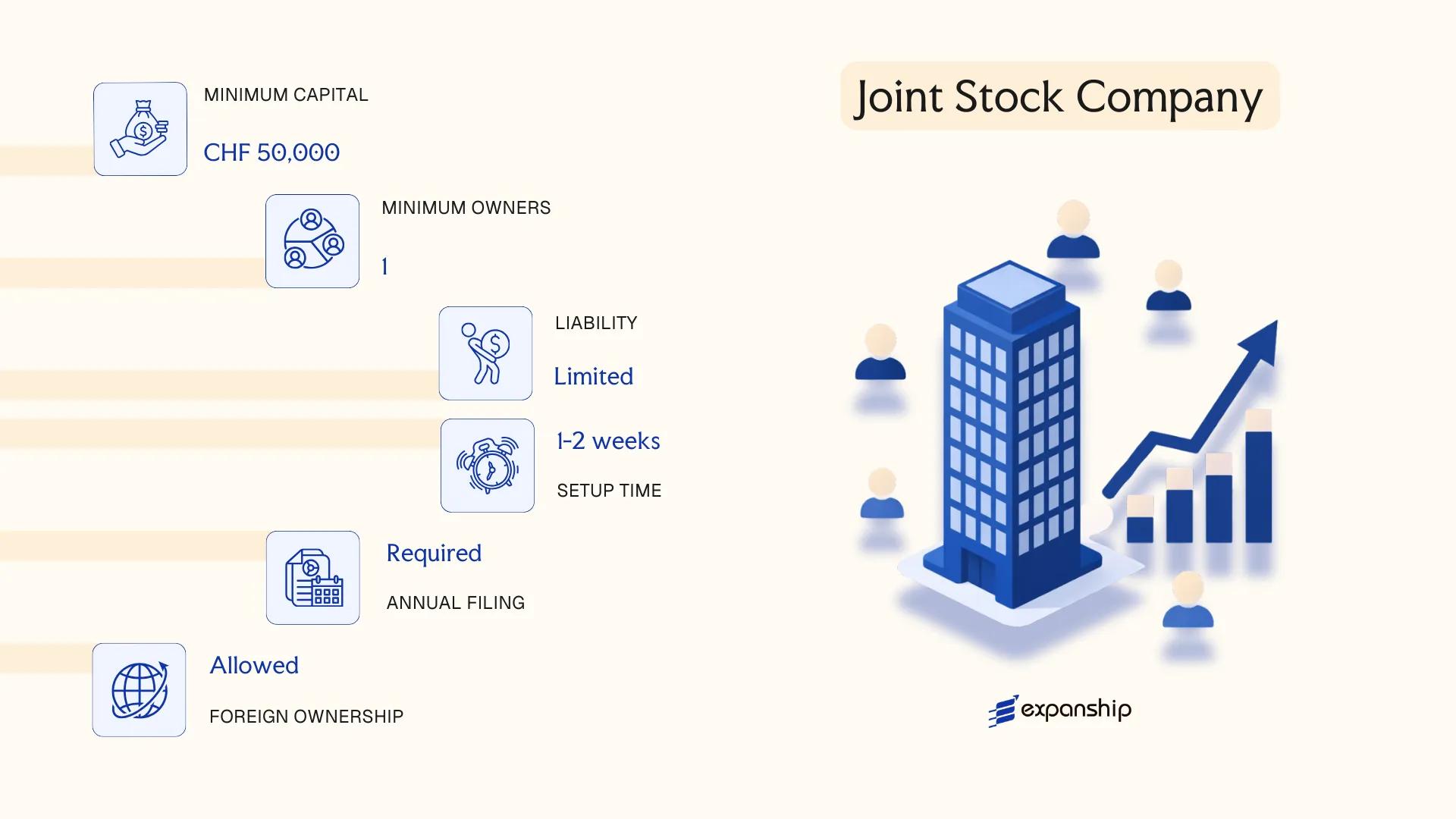

Aktiengesellschaft (AG) – Joint Stock Company

The Liechtenstein AG joint stock company is governed by the Person and Company Act (Personen- und Gesellschaftsrecht, PGR) of 1926, which remains the primary statutory framework for corporate entities in the principality. It carries full legal personality separate from its shareholders, meaning the entity can own assets, enter contracts, and incur liabilities in its own name.

Shareholder liability is capped at their subscribed capital contribution. The AG can be structured as either a publicly traded or closely held entity, making it suitable across a range of ownership and operational configurations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company (Aktiengesellschaft) | Governed by PGR 1926 |

| Members | Shareholders (min. 1); no maximum | Directors: min. 1; no residency requirement for shareholders |

| Local Presence | Registered office and at least one locally resident authorized representative required | Managed through a licensed fiduciary in practice |

| Share Capital | CHF 50,000 minimum; at least 50% paid up at formation | Shares may be registered or bearer (bearer shares subject to disclosure rules) |

| Privacy | Shareholder register not publicly disclosed; directors appear in the public register | Beneficial ownership reported to the Office of Justice |

Focus Points

- Taxation: Subject to a flat 11.5% corporate income tax on net income; no withholding tax on dividends paid to non-residents; no capital gains tax; VAT applies at 8.1% under the Swiss VAT system.

- Economic Substance: No statutory substance requirements for holding structures, though substance is relevant for treaty access and avoiding re-characterization under foreign CFC rules.

- Annual Compliance: Annual financial statements required; audit obligation applies above certain thresholds; annual report filed with the Commercial Registry.

- Treaty Access: Liechtenstein's tax treaty network is limited; the principality relies partly on the EEA agreement for cross-border structuring within Europe.

- Conversion: An AG may be converted into a GmbH or other permitted entity form under the PGR without dissolution.

Sub-Types

Publicly Traded AG

Shares of a publicly traded AG may be listed on a recognized exchange. Additional prospectus, disclosure, and governance obligations apply under EEA-aligned securities regulations, distinguishing it from the standard closely held form.

Single-Member AG

A sole shareholder may incorporate and fully own an AG. No structural differences apply to the entity itself, but sole ownership concentrates all voting and economic rights in one party, which has implications for governance documentation.

The AG is commonly used for holding structures, IP ownership, and intra-group financing arrangements, particularly where capital market access or share transferability is a priority. The primary limitation is the CHF 50,000 minimum capital requirement and the compliance overhead relative to simpler entity forms.

The AG suits established businesses and international groups seeking a capital-based structure with transferable shares and clear separation between ownership and management.

Company Incorporation in Liechtenstein

Incorporate an Aktiengesellschaft or other entity type in Liechtenstein with end-to-end support from Expanship.

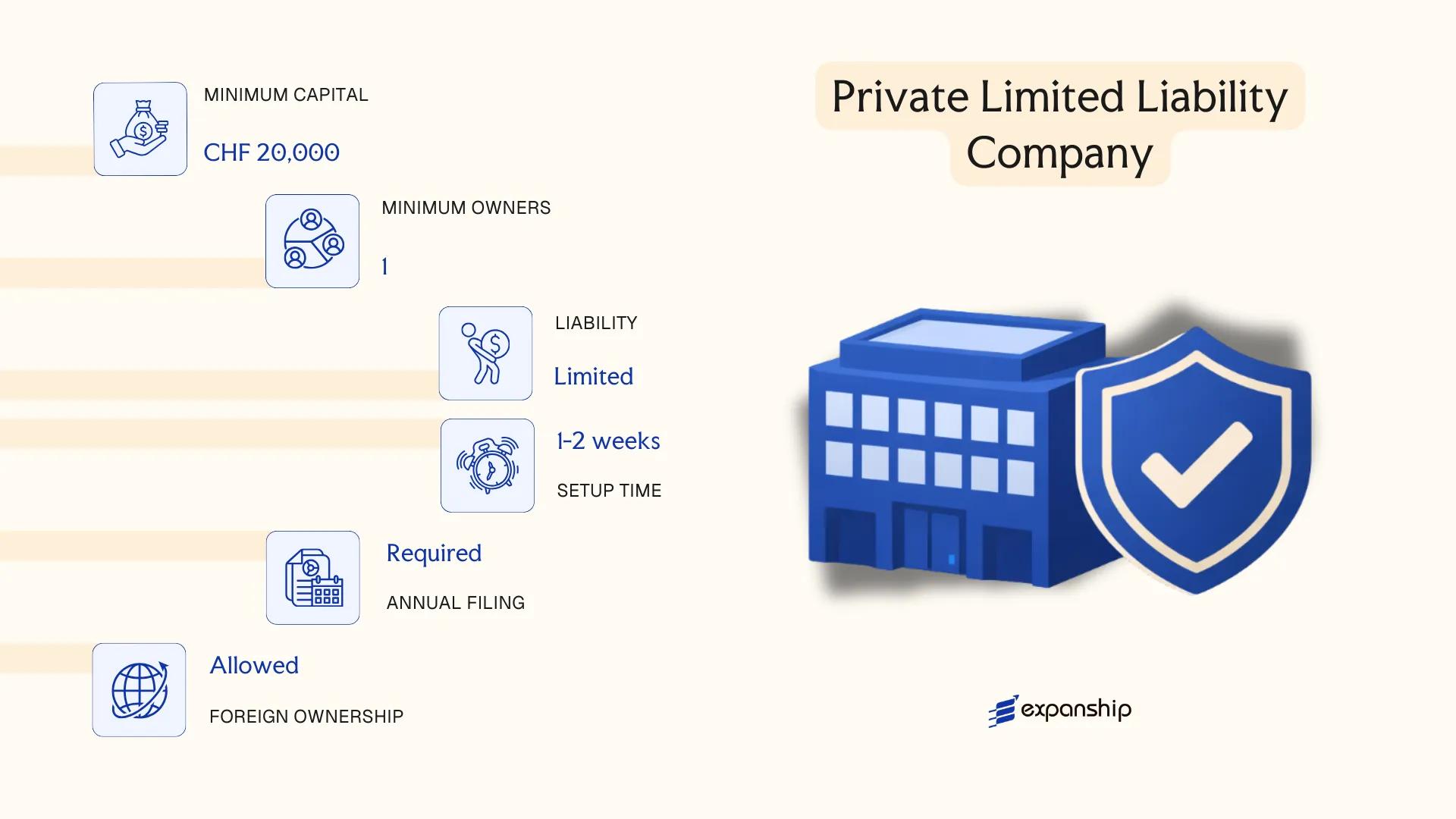

Gesellschaft mit beschränkter Haftung (GmbH) – Private Limited Liability Company

The Liechtenstein GmbH private limited company is governed by the Persons and Companies Act (Personen- und Gesellschaftsrecht, PGR) of 1926, which remains the primary legislative framework for corporate entities in the principality. It carries separate legal personality, meaning the company holds rights and obligations in its own name, entirely distinct from those of its members.

Liability is limited to the amount contributed to the share capital, making this structure a hybrid between a partnership and a joint stock company. Shares in a GmbH are not freely transferable without member consent, which supports use in closely held business arrangements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Gesellschaft mit beschränkter Haftung (GmbH) | Separate legal personality; limited liability |

| Members | Shareholders (Gesellschafter); minimum 1, no maximum | Single-member GmbH is permitted |

| Management | One or more managers (Geschäftsführer); no nationality restriction | At least one manager must be authorised to act |

| Local Presence | Registered office and a local authorised representative required | Must maintain a physical address in Liechtenstein |

| Share Capital | CHF 30,000 minimum; fully paid-up at formation | No-par-value shares are not permitted |

| Privacy | Shareholder names are recorded in the commercial register | Beneficial ownership is reported to the FMA |

Focus Points

- Taxation: Subject to corporate income tax at a flat rate of 12.5%; a minimum tax applies; VAT registration required if annual turnover exceeds CHF 100,000; no withholding tax on dividend distributions to non-residents under domestic law.

- Economic Substance: Managed and controlled requirements apply; passive holding arrangements without local substance may attract regulatory scrutiny from the Liechtenstein Financial Market Authority (FMA).

- Annual Compliance: Annual financial statements must be prepared; audit requirements apply above certain size thresholds; annual filing with the Office of Justice (Amt für Justiz) is mandatory.

- Treaty Access: Liechtenstein's tax treaty network is limited but growing; EU savings and interest arrangements may apply given the EEA relationship.

- Share Transfers: Transfers require notarial deed and member approval, restricting free tradability.

Closing

The Liechtenstein GmbH suits trading operations, holding structures, and IP-holding entities where ownership control and restricted transferability are priorities; its fully paid-up capital requirement and mandatory register disclosure of shareholders are practical constraints for founders seeking confidentiality.

GmbH registration in Liechtenstein is most appropriate for closely held operating businesses or family-controlled holding companies requiring clear liability separation with retained ownership control.

Anstalt – Establishment

Unique to Liechtenstein, the Anstalt (establishment) is governed by the Persons and Companies Act (Personen- und Gesellschaftsrecht, PGR) of 1926. The Liechtenstein Anstalt establishment structure occupies a hybrid position in corporate law: it holds separate legal personality and offers limited liability, yet it need not have shareholders in the traditional sense, functioning instead as a purpose-driven entity with a founder and defined beneficiaries or objectives.

Structurally, the Anstalt can be configured to conduct commercial activities, hold assets, or pursue a defined purpose — making it one of the more flexible vehicles available under PGR.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Separate legal entity with limited liability | Hybrid structure; no mandatory shareholder class |

| Governing Parties | Founder (Gründer); Board of Directors (Verwaltungsrat) | Founder's rights may be transferred or retained |

| Capital | CHF 30,000 minimum; may be in cash or in-kind | No shares required; capital represented by founder's rights |

| Local Presence | Registered office and licensed representative in Liechtenstein required | Representative must hold a PGR licence |

| Privacy | Founder identity not publicly disclosed; beneficial ownership filed with authorities | Public register shows the entity, not the founder |

| Beneficiaries | Optional; defined in statutes or internal regulations | Beneficiary structure resembles foundation mechanics |

Focus Points

- Taxation: Subject to a flat 12.5% corporate income tax on net income; no withholding tax on profit distributions; VAT applies if commercial activity thresholds are met; no wealth or capital tax.

- Economic Substance: Commercial Anstalt entities engaging in active business must demonstrate genuine operational substance in Liechtenstein.

- Annual Compliance: Annual accounts must be filed; audit requirements depend on the entity's size and activity type under PGR thresholds.

- Treaty Access: Liechtenstein's tax treaty network is limited; treaty eligibility depends on the Anstalt's residency status and activity.

- Restrictions: Banking and financial services activities require additional licensing from the Financial Market Authority (FMA).

Sub-Types

Commercial Anstalt (Gewerbliche Anstalt)

Permitted to conduct business and generate income through trade or services. This variant operates similarly to a corporate entity and must maintain commercial accounts accordingly.

Non-Commercial Anstalt

Restricted from carrying out commercial activities; used primarily for asset holding, wealth structuring, or administering defined purposes. It more closely resembles a foundation in function.

Closing

The Anstalt is commonly used for asset protection, IP holding, private wealth structuring, and as a holding vehicle for family assets. Its flexibility in configuring governance and beneficiary arrangements is a distinct advantage, though the limited tax treaty access can reduce its efficiency for cross-border income flows.

The Anstalt suits high-net-worth individuals or family offices seeking a private, purpose-driven structure for asset consolidation outside traditional shareholder frameworks.

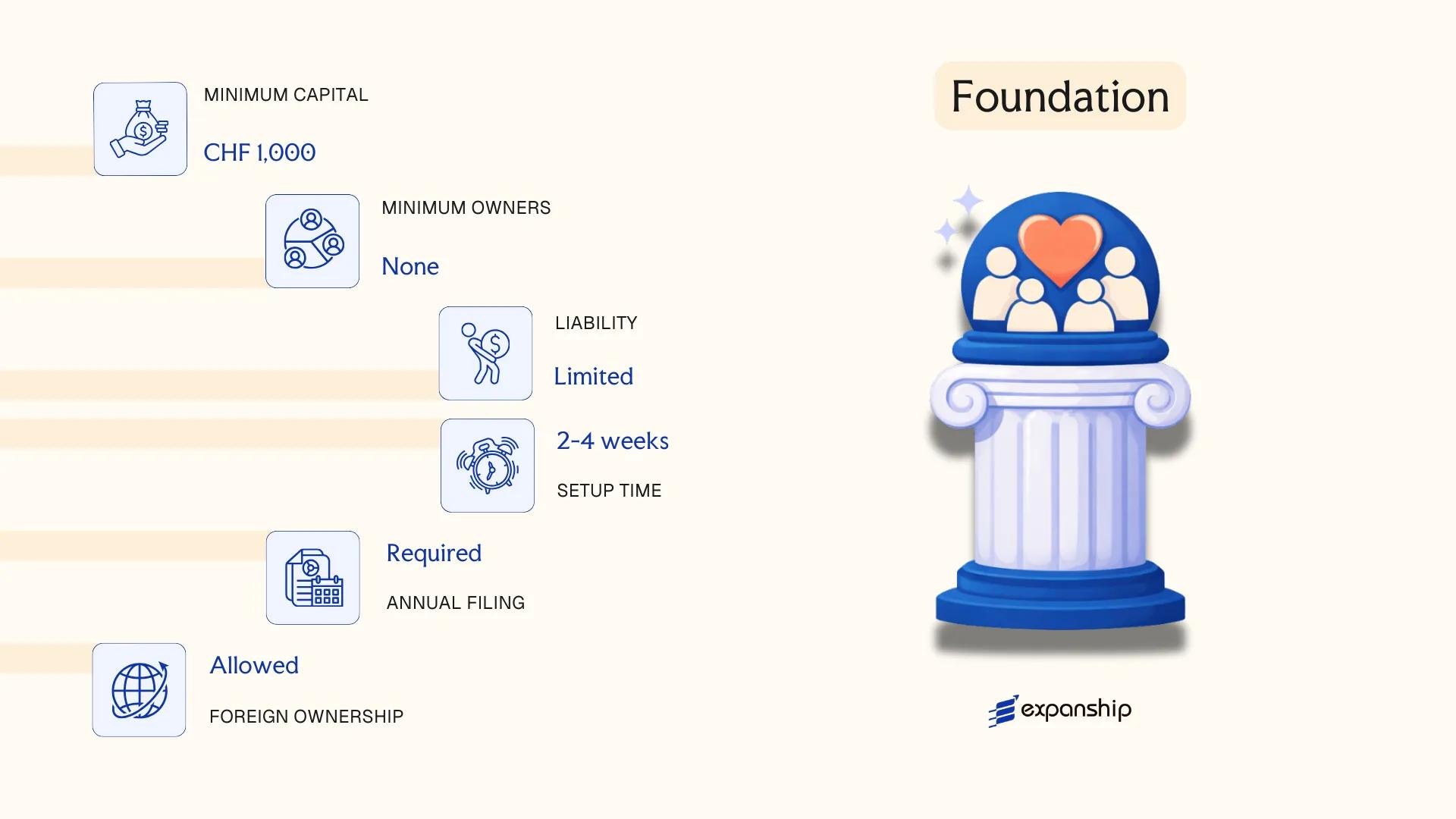

Stiftung – Foundation

Governed by the Persons and Companies Act (PGR) of 1926, the Stiftung is a dedicated asset structure with full legal personality under Liechtenstein law. A Liechtenstein Stiftung foundation setup separates the founder's assets from their personal estate at the point of transfer, meaning those assets are held in the name of the foundation itself and administered for defined purposes or beneficiaries.

Unlike a company, the Stiftung has no shareholders or members. Assets are committed irrevocably to the foundation's purpose, which can be private, charitable, or a combination of both, making it a commonly used instrument in cross-border estate and Stiftung Liechtenstein private foundation wealth planning.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Independent legal entity (Stiftung) | Governed by PGR; holds assets in its own name |

| Governing Bodies | Foundation Council (Stiftungsrat); optional Beneficiary Representative | Minimum 1 Foundation Council member required |

| Founder | One or more individuals or legal entities | Founder may retain reserved powers if documented in the deed |

| Local Presence | Registered office in Liechtenstein; licensed representative required | Must maintain a local address; representative is typically a licensed fiduciary |

| Capital | CHF 30,000 minimum endowment | No share capital; assets are endowed, not invested as equity |

| Privacy | Deed of Foundation filed with the Public Registry; beneficiaries not publicly disclosed | Beneficial ownership reported to the Financial Intelligence Unit (FIU) under AML rules |

Focus Points

- Taxation: Foundations are subject to a minimum annual tax of CHF 1,800; distributions to non-resident beneficiaries may attract withholding considerations depending on the recipient's home jurisdiction; no capital gains tax applies at the foundation level.

- Economic Substance: Private wealth foundations holding only passive assets are generally exempt from substance requirements, though foundations conducting commercial activities face standard substance rules.

- Annual Compliance: Mandatory filing of annual accounts with the Foundation Supervisory Board (Stiftungsaufsichtsbehörde, SAB) where the foundation has charitable purposes; private foundations file accounts internally but must retain them for audit.

- Treaty Access: Access to Liechtenstein's tax treaties depends on the foundation's purpose and structure; private family foundations do not automatically qualify for treaty benefits in all cases.

- Conversion: A Stiftung can be converted into other legal forms under PGR provisions, subject to supervisory approval where applicable.

Sub-Types

Private Foundation (Privatstiftung)

Established for the benefit of defined private beneficiaries, typically family members. The purpose is non-commercial, and assets are administered over generations without public charitable obligations.

Charitable Foundation (Gemeinnützige Stiftung)

Operates exclusively for public benefit purposes such as education, culture, or social welfare. Subject to oversight by the SAB and eligible for certain tax exemptions not available to private foundations.

Mixed-Purpose Foundation

Combines private and charitable objectives within a single structure. Governance documents must clearly delineate how assets are allocated between each purpose category.

Closing

The Stiftung is used primarily for intergenerational wealth transfer, asset protection, and Liechtenstein foundation wealth planning involving multi-jurisdictional family structures. Its key structural advantage is the clean separation of assets from the founder's estate; however, the irrevocable nature of asset transfer means founders must accept a genuine loss of direct ownership, which requires careful advance planning.

The Stiftung is best suited for high-net-worth individuals and family offices seeking a governed, long-term structure for holding and transferring private assets across generations.

Trust Enterprise (Treuhänderschaft)

The Liechtenstein trust enterprise (Treuhänderschaft) is governed by the Persons and Companies Act (Personen- und Gesellschaftsrecht, PGR) of 1926, which remains the foundational statute for all legal entities in the principality. This structure occupies a unique position in domestic law: it carries separate legal personality and offers limited liability, while combining elements of civil law trust and corporate law into a single hybrid form.

Unlike a conventional trust relationship under common law jurisdictions, the Treuhänderschaft is a registered legal entity that holds assets in its own name. Treuhänderschaft registration in Liechtenstein is administered through the Office of Justice (Amt für Justiz), and the entity must be entered in the Public Register (Öffentlichkeitsregister) to acquire legal existence.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Trust Enterprise (Treuhänderschaft) | Hybrid civil law entity with separate legal personality |

| Members / Roles | Founder (Treugeber), Trustee (Treuhänder), Beneficiaries | The trustee administers assets on behalf of beneficiaries |

| Minimum Members | One founder; one trustee | Trustee may be a licensed professional or corporate entity |

| Local Presence | Registered office in Liechtenstein; licensed trustee required | Trustee must hold a professional licence under the Trustee Act (Treuhändergesetz) |

| Capital | No statutory minimum capital requirement | Assets transferred by the founder constitute the operating base |

| Privacy | Beneficial ownership disclosed to authorities; not fully public | Register entry is public; beneficiary details are not publicly accessible |

Focus Points

- Taxation: Subject to standard corporate income tax at 12.5%; no withholding tax on distributions to non-resident beneficiaries under domestic law; VAT obligations arise only if the entity conducts commercial activity.

- Economic Substance: Commercial Treuhänderschaft structures may attract substance requirements if used for income-generating activity; pure asset-holding arrangements are assessed separately.

- Annual Compliance: Annual accounts must be prepared; filing obligations depend on whether the entity qualifies as a small, medium, or large entity under PGR classification thresholds.

- Treaty Access: Access to Liechtenstein's tax treaties is not guaranteed for all Treuhänderschaft structures and depends on the entity's qualification as a tax resident and treaty eligibility under each bilateral agreement.

- Restrictions: The trustee must be licensed under the Trustee Act; unlicensed administration is prohibited and constitutes a regulatory offence.

Closing

The Treuhänderschaft is used primarily for asset protection, family wealth structuring, and holding arrangements where a hybrid legal form offers procedural advantages over a pure foundation or company. Its key advantage is the combination of legal personality with flexible asset administration; the principal limitation is the mandatory involvement of a licensed trustee, which introduces ongoing professional fees and a layer of regulatory dependency.

Best suited for high-net-worth individuals and family offices seeking a registered, legally distinct vehicle for structured asset holding under Liechtenstein law.

Foreign Business Structures in Liechtenstein [Branch Office, Representative Office, Subsidiary]

A foreign company branch office Liechtenstein establishes as an extension of its parent carries no separate legal personality — the parent entity remains fully liable for its obligations. Registration is governed by the Persons and Companies Act (Personen- und Gesellschaftsrecht, PGR) of 1926, which sets out the conditions under which foreign businesses may operate within the jurisdiction.

Registration with the Liechtenstein Commercial Register (Handelsregister) is mandatory before commencing operations. A subsidiary, by contrast, is incorporated as a standalone legal entity under Liechtenstein law and offers the liability separation that a branch does not.

Key Characteristics

| Requirement | Branch Office | Representative Office | Subsidiary |

|---|---|---|---|

| Legal Personality | None (extension of parent) | None | Separate legal entity |

| Liability | Parent bears full liability | Parent bears full liability | Limited to subsidiary's assets |

| Permitted Activities | Commercial operations | Liaison, market research only | Full commercial operations |

| Local Presence | Registered address + local representative required | Registered address required | Registered office + directors required |

| Registration Body | Handelsregister | Handelsregister | Handelsregister |

| Capital Requirement | None (parent capital applies) | None | Depends on chosen entity form (AG or GmbH) |

Focus Points

- Taxation: Subsidiaries are subject to the standard 12.5% corporate income tax; branches are taxed on Liechtenstein-sourced profits at the same rate. VAT registration may apply if annual turnover exceeds the applicable threshold.

- Economic Substance: Representative offices must not generate direct revenue; exceeding liaison activities risks reclassification by authorities.

- Annual Compliance: All registered structures must file annual reports with the Handelsregister; subsidiaries carry the full reporting obligations of their chosen legal form.

- Treaty Access: Subsidiaries may access Liechtenstein's tax treaties and the EEA agreement benefits; branches and representative offices have more restricted access depending on the parent's domicile.

- Restrictions: Representative offices cannot enter contracts, invoice clients, or conduct revenue-generating activity in their own name.

Closing

A subsidiary suits foreign firms seeking operational independence and liability separation, while a branch works for businesses that require a direct commercial presence without a separate incorporation. The primary limitation of a branch is the unrestricted exposure it creates for the parent entity.

Foreign companies already operating in EEA markets that want a foothold in Liechtenstein with minimal setup complexity are best served by a branch office, whereas those building a standalone operation should incorporate a subsidiary.

Partnerships in Liechtenstein [General Partnership (Kollektivgesellschaft), Limited Partnership (Kommanditgesellschaft)]

The Liechtenstein Kollektivgesellschaft (general partnership) and Kommanditgesellschaft (limited partnership) are both governed by the Personen- und Gesellschaftsrecht (PGR) of 1926, the same statute that underpins most Liechtenstein commercial entities. Neither form carries separate legal personality in the way a corporation does, yet both can hold assets, enter contracts, and sue in their own name under the PGR framework.

Registration with the Öffentlichkeitsregisteramt (the Public Registry Office) is mandatory for both structures before commercial activity begins. Partnership registration in Liechtenstein requires at least one partner with unlimited personal liability, making these forms more exposed than capital-based entities.

Key Characteristics

| Requirement | Kollektivgesellschaft (General Partnership) | Kommanditgesellschaft (Limited Partnership) |

|---|---|---|

| Legal Form | Non-corporate commercial partnership | Non-corporate commercial partnership with tiered liability |

| Members | General partners (Gesellschafter); minimum 2; no statutory maximum; all bear unlimited liability | At least 1 general partner (unlimited liability) + at least 1 limited partner (Kommanditist); liability capped at contribution |

| Local Presence | Registered office in Liechtenstein required | Registered office in Liechtenstein required |

| Minimum Capital | No statutory minimum | No statutory minimum; limited partner's contribution must be defined in the partnership agreement |

| Privacy | Partner names are recorded in the Public Registry and are publicly accessible | General partner names publicly visible; limited partner details also registered |

Focus Points

- Taxation: Partnerships are fiscally transparent; profits are attributed to partners and taxed at their level under Liechtenstein's 12.5% corporate or personal income tax rate, with no separate entity-level tax; VAT registration applies if turnover thresholds are met.

- Annual Compliance: Annual accounts are required; audit obligations depend on the size and structure of the partnership.

- Treaty Access: As non-corporate entities, partnerships may face restrictions accessing Liechtenstein's tax treaties depending on the residence and status of partners.

- Conversion: Both forms can be converted into a capital company (AG or GmbH) through a formal restructuring process under the PGR.

- Restrictions: General partners bear unlimited personal liability, which is a structural risk that cannot be contractually eliminated.

Sub-Types

Kollektivgesellschaft (General Partnership)

All partners hold equal management rights and unlimited joint and several liability for the entity's obligations, unless the partnership agreement restricts management authority to specific partners.

Kommanditgesellschaft (Limited Partnership)

Limited partners are excluded from management by statute; exercising management functions risks forfeiting limited liability status. This structure suits arrangements where passive investors contribute capital alongside an active managing partner.

Closing

Both structures are used primarily for smaller domestic trading operations or family business arrangements where the partners accept personal exposure in exchange for operational simplicity. The absence of a minimum capital requirement lowers the entry threshold, but unlimited liability for general partners remains a significant structural drawback.

These partnership forms suit closely held domestic ventures or family-run businesses where all partners are personally involved and comfortable with direct liability exposure.

Sole Proprietorship (Einzelunternehmen)

The Liechtenstein sole proprietorship (Einzelunternehmen) is the simplest business form available under the Person und Gesellschaftsrecht (PGR) of 1926, the same legislation governing most of the country's commercial entities. It carries no separate legal personality — the proprietor and the business are treated as one and the same.

Because the business and its owner are legally indistinguishable, personal assets are fully exposed to business liabilities. Registration with the Liechtenstein Commercial Register (Handelsregister) is mandatory once annual turnover exceeds a statutory threshold, although smaller operations may qualify for simplified registration.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Einzelunternehmen) | No separate legal personality |

| Member Type | Sole Proprietor | One individual only; no partners or shareholders |

| Local Presence | Registered business address in Liechtenstein required | Physical or c/o address acceptable in many cases |

| Capital | No statutory minimum | CHF is the functional currency |

| Liability | Unlimited personal liability | All personal assets exposed to business debts |

| Privacy | Proprietor's name appears in the Commercial Register | Limited privacy; publicly accessible record |

Focus Points

- Taxation: Subject to personal income tax on business profits; VAT registration required if turnover exceeds the applicable threshold; no corporate income tax applies at entity level.

- Annual Compliance: Annual financial statements required above certain thresholds; smaller sole traders may face reduced reporting obligations under the PGR.

- Economic Substance: No formal substance requirements specific to this structure, though the proprietor must conduct genuine activity.

- Conversion: Can be converted into a GmbH or AG, which requires a formal restructuring process through the Commercial Register.

- Treaty Access: Generally excluded from double tax treaty benefits, as treaty entitlement is typically reserved for corporate entities.

Closing

The Einzelunternehmen suits resident individuals carrying out small-scale trade, freelance services, or local professional activity, with its main advantage being minimal setup formality. The absence of liability protection is a significant structural drawback for anyone operating with meaningful financial exposure.

Self-employed residents and individual traders seeking a straightforward self-employed business structure in Liechtenstein without the administrative overhead of a corporate entity.

How to Choose the Right Entity Type in Liechtenstein

Knowing how to choose the right company type in Liechtenstein before committing to a structure prevents costly regulatory and tax problems that are difficult to reverse after incorporation.

Why Your Entity Choice Matters

The wrong structure carries concrete consequences:

- Registering a tax-exempt entity when you need access to double taxation agreements means withholding tax reductions in counterpart countries cannot be claimed — your firm will bear the full withholding burden on dividends, interest, and royalties.

- Forming a shareholding company when your objectives are estate planning or asset protection locks you into annual general meeting obligations and shareholder disclosure requirements that foundations are not subject to under the Persons and Companies Act (PGR).

- Selecting a structure without adequate substance capacity when economic substance requirements apply triggers reporting failures under Liechtenstein's tax compliance framework.

- Choosing an entity that mandates audited financial statements for a single-person consultancy introduces annual audit costs that serve no operational purpose.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as fund management each require a structurally different vehicle.

- Tax Objectives: Your need for treaty access, a specific flat-rate regime, or full tax exemption narrows the eligible entity types considerably.

- Ownership and Management: Single-owner operations and multi-party ventures have different governance requirements that not all structures accommodate equally.

- Privacy Requirements: Some structures permit nominee arrangements; others require public register disclosure of beneficial owners and directors.

- Substance Capacity: If maintaining local office space and decision-making presence is not feasible, certain entity types carry lower or no substance thresholds.

- Exit Strategy: Redomiciliation and conversion rules vary across structures, and not all entities support both options under Liechtenstein law.

Compliance Services for Companies in Liechtenstein

Maintain your Liechtenstein entity in good standing with ongoing compliance support, including annual filings, registered office, and regulatory reporting.

Conclusion

Completing an incorporating a company in Liechtenstein guide requires understanding how sharply differentiated the available structures are. The AG suits publicly oriented or larger capital ventures, while the GmbH fits closely held operating businesses. Established as a uniquely Liechtenstein instrument, the Anstalt serves asset-holding and special-purpose functions without a direct equivalent elsewhere in Europe. The Stiftung remains the primary vehicle for wealth preservation and philanthropic purposes. Trusts and trust enterprises operate under the Personen- und Gesellschaftsrecht (PGR), catering to estate planning and fiduciary arrangements. Among registered entities, foundations and establishments account for a significant share of formations, reflecting the country's positioning as a private wealth jurisdiction.

Regulatory direction continues toward greater FATF and OECD alignment, with the Financial Market Authority (FMA) maintaining active supervisory oversight. For businesses evaluating starting a company in Liechtenstein, understanding which structure fits your ownership profile determines both compliance obligations and long-term operational flexibility. Expanship's formation specialists can help you assess those variables in detail.

How Expanship Can Assist You

Expanship's Liechtenstein company incorporation services cover the full setup process — from selecting the correct entity type under the Personen- und Gesellschaftsrecht (PGR) to registering with the Handelsregister (Commercial Register) administered by the Office of Justice. Whether your focus is an Anstalt, a Stiftung, or a GmbH, every structure carries distinct capital, governance, and disclosure requirements that your Expanship Liechtenstein corporate services provider account team handles directly.

From document preparation to post-registration obligations, here is what we assist with:

- Preparation and notarization of constitutional documents

- Registered office and resident agent provision

- Filing with the Handelsregister and liaison with the Office of Justice

- Ongoing annual compliance and reporting management

- Beneficial ownership declarations under AML regulations

- Banking introduction support within Liechtenstein's financial sector

Reach out to discuss your structure through the Expanship Liechtenstein contact page.

Frequently Asked Questions (FAQ)

The Anstalt (Establishment) has historically been among the most frequently formed structures, valued for its structural flexibility and the ability to function as either a commercial or non-commercial entity under the Persons and Companies Act (PGR). Its hybrid nature allows it to serve holding, asset management, and operational purposes without requiring share capital in a traditional sense.

A GmbH is a conventional share-based company subject to standard corporate income tax and full commercial registration requirements, while an Anstalt can be structured without publicly disclosed beneficiaries under certain conditions. For local trading, the GmbH carries clearer statutory rights, whereas the Anstalt is more commonly used for holding or private wealth purposes. Compliance obligations under the Anstalt are generally lighter for non-trading structures.

The Stiftung (Foundation) and the Anstalt both permit beneficial ownership to remain outside public disclosure in certain configurations. The Stiftung does not require public registration of beneficiaries, and nominee foundation council members are available. Disclosure obligations do exist toward the Liechtenstein Financial Market Authority (FMA) under anti-money laundering regulations.

An AG requires a minimum of one shareholder and can be formed by a sole individual, as can a GmbH and an Anstalt. Partnerships — both the Kollektivgesellschaft and Kommanditgesellschaft — require at least two participants by their legal definition under the PGR. A Stiftung requires a founder but does not require multiple parties.

Foreign nationals face no statutory nationality restrictions when forming an AG, GmbH, or Anstalt. A local registered address and, in most cases, a licensed local representative or trustee are required under Liechtenstein law. The Office of Justice (Amt für Justiz) oversees registration, and compliance with the Due Diligence Act (SPG) applies regardless of the founder's nationality.

Conversion between certain structures is permitted under the PGR, though not all combinations are available by default. A GmbH can generally be converted into an AG through a formal transformation procedure involving notarization and re-registration. Conversion involving an Anstalt or Stiftung requires individual legal assessment given their atypical constitutional documents.

The AG, GmbH, and Anstalt each hold full legal personality under the PGR, allowing them to contract, own assets, and be liable independently of their members or founders. The Stiftung also has legal personality. A Treuhänderschaft (Trust Enterprise) is a partial exception — it operates under trust principles where legal ownership rests with the trustee rather than within a separate incorporated entity.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.