Key Takeaways

- The SARL is Lebanon's most widely registered entity type, favored for its accessible minimum capital threshold and operational flexibility compared to other available structures.

- Holding companies and offshore companies in Lebanon are governed by distinct legal instruments — Decree-Law No. 45 and Decree-Law No. 46 of 1983 respectively — each restricting the entity to a specific operational purpose.

- All business entities in Lebanon are registered through the Commercial Registry (Registre du Commerce), which operates under the Lebanese Ministry of Justice.

- Lebanon's territorial tax system means foreign-sourced income is generally not subject to domestic taxation, a factor that directly influences the appeal of offshore and holding structures.

Introduction to Entity Types in Lebanon

Located on the eastern Mediterranean coast, bordered by Syria to the north and east and Israel to the south, Lebanon is an independent republic whose commercial activity is governed at the national level. Company registration falls under the jurisdiction of the Commercial Registry (Registre du Commerce), operating within the Lebanese Ministry of Justice, which oversees the formation and ongoing compliance of business entities across the country.

Lebanon operates a territorial tax system, meaning foreign-sourced income is generally not subject to domestic taxation.

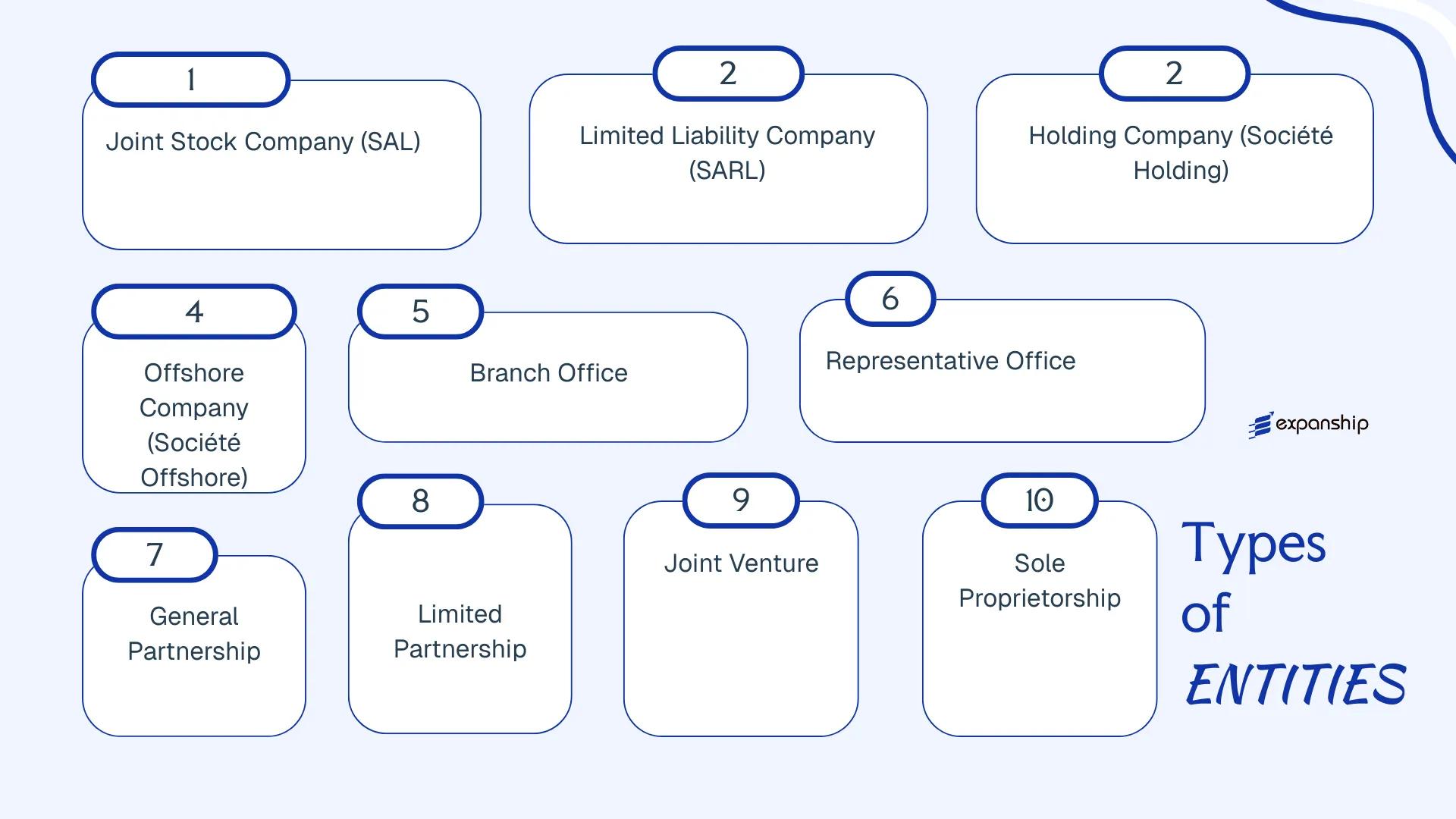

Businesses registering in Lebanon can choose from several distinct legal structures: the Joint Stock Company (Société Anonyme Libanaise – SAL), the Limited Liability Company (Société à Responsabilité Limitée – SARL), the Holding Company (Société Holding), the Offshore Company (Société Offshore), Branch Office, Representative Office, General Partnership, Limited Partnership, Joint Venture, and Sole Proprietorship.

The types of business entities in Lebanon differ significantly in terms of liability, ownership rules, minimum capital requirements, and permitted commercial activities. Each structure suits a different operational profile, and the sections that follow examine every available option in detail.

An Overview of Business Structures in Lebanon

Lebanese company law recognises several distinct legal entity types, governed primarily by the Lebanese Code of Commerce (Legislative Decree No. 304 of 24 December 1942) and supplemented by specific legislative decrees for holding and offshore structures. Each entity type is designed for a different commercial purpose, whether domestic trading, asset structuring, or cross-border operations.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Joint Stock Company (SAL) | Corporate | Limited to shares | Taxed | Yes | 3 shareholders | Ministry of Finance / Commercial Register | Code of Commerce |

| Limited Liability Company (SARL) | Corporate | Limited to capital | Taxed | Yes | 1–20 members | Commercial Register | Code of Commerce |

| Holding Company | Corporate | Limited | Partially exempt | Restricted | 3 shareholders | Ministry of Finance | Legislative Decree No. 45 (1983) |

| Offshore Company | Corporate | Limited | Exempt | No | 3 shareholders | Ministry of Finance | Legislative Decree No. 46 (1983) |

| Branch Office | Non-incorporated | Parent liable | Taxed | Yes | Parent company | Commercial Register | Code of Commerce |

| Representative Office | Non-incorporated | Parent liable | Exempt | No | Parent company | Commercial Register | Code of Commerce |

| General Partnership | Partnership | Unlimited | Taxed | Yes | 2+ partners | Commercial Register | Code of Commerce |

| Limited Partnership | Partnership | Mixed | Taxed | Yes | 2+ partners | Commercial Register | Code of Commerce |

| Sole Proprietorship | Individual | Unlimited | Taxed | Yes | 1 owner | Commercial Register | Code of Commerce |

Each of these structures is examined in full in the sections below.

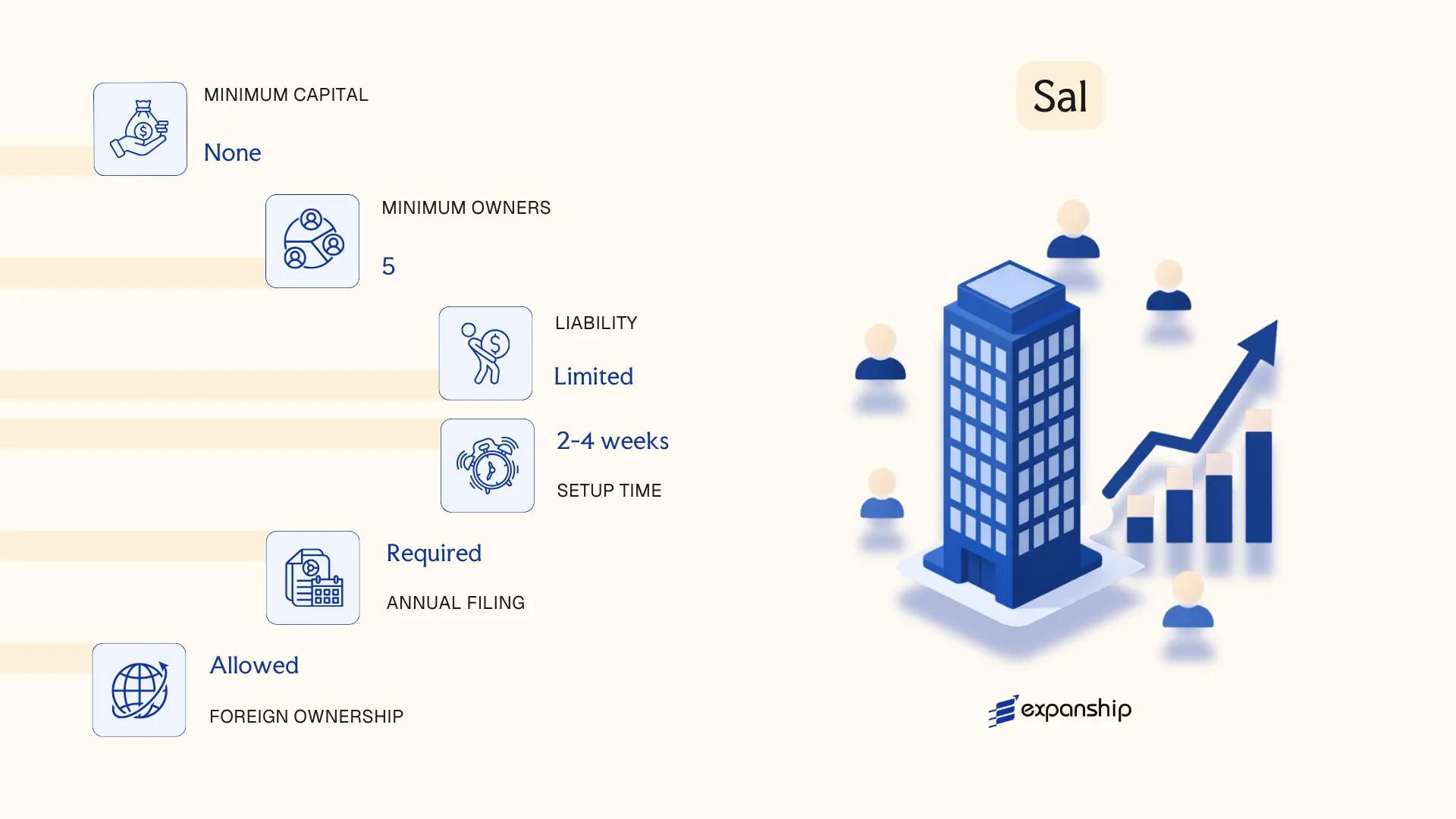

Joint Stock Company (Société Anonyme Libanaise – SAL)

The joint stock company SAL Lebanon is governed by the Lebanese Code of Commerce of 1942, as amended, along with Legislative Decree No. 304 of 1942 and subsequent amendments. It carries a separate legal personality, meaning the company's liabilities are legally distinct from those of its shareholders.

Shares in a Société Anonyme Libanaise are freely transferable, which makes this structure the standard choice for businesses seeking to raise capital from multiple investors or to accommodate future ownership changes.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme Libanaise (SAL) | Joint stock company with separate legal personality |

| Members | Shareholders; minimum 3, no statutory maximum | At least 1/3 of shares must be held by Lebanese nationals in certain regulated sectors |

| Governing Body | Board of Directors; minimum 3, maximum 12 members | Board must include a majority of Lebanese nationals |

| Capital | Minimum LBP 30,000,000 (approx. USD 20,000 at historical rate); no maximum | At least 25% must be paid up at incorporation |

| Local Presence | Registered office required in Lebanon | No requirement for a resident company secretary as a distinct role |

| Privacy | Shareholders are recorded in the Commercial Register | Register is publicly accessible; bearer shares are not permitted |

Focus Points

- Taxation: Subject to 17% corporate income tax on Lebanese-sourced profits; dividends distributed to shareholders attract a 10% withholding tax; VAT at 11% applies to taxable supplies; stamp duty applies to certain contracts and instruments. Full details are available via the Lebanese Ministry of Finance.

- Annual Compliance: Audited financial statements required annually; a statutory auditor (commissaire aux comptes) must be appointed; annual general meetings are mandatory.

- Restrictions: Certain sectors — banking, insurance, media — impose additional nationality and licensing requirements on SAL shareholders and board members.

- Treaty Access: Lebanon has concluded a limited number of double tax treaties; treaty eligibility depends on the residency status of shareholders, not the SAL's incorporation alone.

- Conversion: An SAL can be converted to a SARL or other permitted form subject to shareholder approval and re-registration with the commercial court.

Closing

The SAL suits medium-to-large enterprises, businesses preparing for institutional investment, and companies operating in regulated industries where a formal governance structure is required. The freely transferable share structure supports capital raising, though the minimum three-shareholder requirement and mandatory auditor appointment add ongoing administrative obligations compared to simpler structures.

This entity type is most appropriate for businesses with multiple investors, those seeking external financing, or operations in sectors where a formal board structure and audited accounts are a regulatory or commercial expectation.

Company Incorporation in Lebanon

Incorporate a Joint Stock Company (SAL) or other entity type in Lebanon with end-to-end support from Expanship.

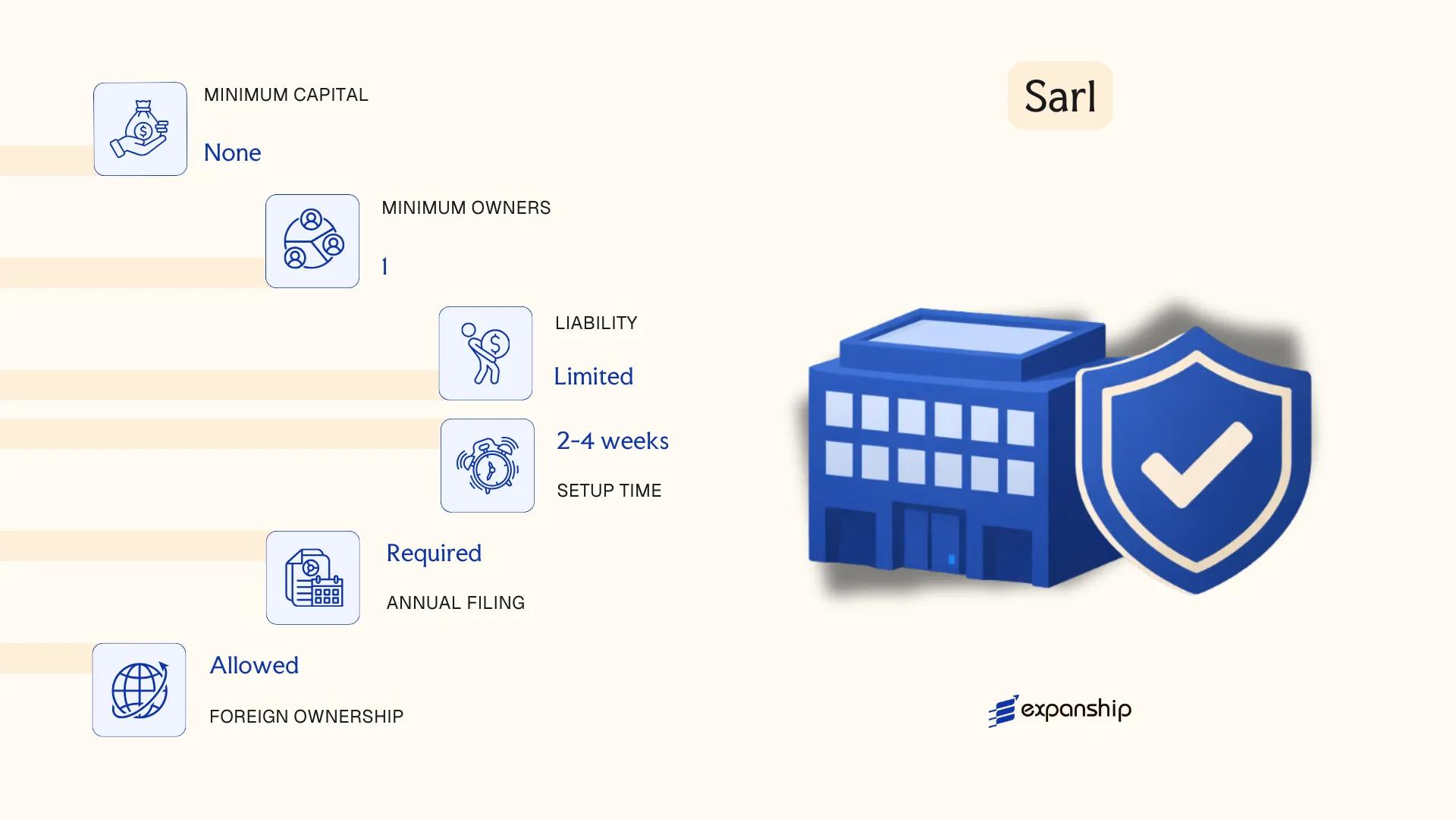

Limited Liability Company (Société à Responsabilité Limitée – SARL)

The limited liability company SARL Lebanon framework is governed by Legislative Decree No. 35 of 1967, which established the SARL as a distinct legal form under Lebanese commercial law. The entity carries separate legal personality, meaning it can own assets, enter contracts, and incur obligations in its own name, independent of its members.

Liability is capped at each member's capital contribution. This makes the Société à Responsabilité Limitée Lebanon a hybrid structure: corporate in its liability protection, yet closer to a partnership in its governance flexibility and transfer restrictions on quotas (shares).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (SARL) | Governed by Legislative Decree No. 35 of 1967 |

| Members | 3–20 members (associés) | Cannot be held by a single person; exceeding 20 requires conversion to SAL |

| Management | One or more gérants (managers) | Need not be members; no nationality restriction specified under general rules |

| Local Presence | Registered office in Lebanon required | Physical address; no statutory requirement for a local registered agent |

| Capital | No statutory minimum under current law | Denominated in Lebanese Pounds; capital divided into quotas, not publicly traded shares |

| Privacy | Members listed in the Commercial Register | Register is publicly accessible |

Focus Points

- Taxation: Subject to 17% corporate income tax on Lebanese-source profits; VAT applies at 11% where applicable; dividend distributions to non-residents may attract withholding tax; stamp duty applies to certain contracts and documents.

- Annual Compliance: Must file audited financial statements and hold an annual general assembly; appointment of a statutory auditor is required.

- Transfer Restrictions: Quota transfers to third parties require approval from members holding at least three-quarters of the capital.

- Treaty Access: May access Lebanon's double tax treaty network, though treaty eligibility depends on the specific agreement and residency conditions.

- Conversion: Can be converted to a SAL if membership exceeds 20 or if the business requires public share issuance.

Closing

The SARL suits small-to-medium trading, service, and family-owned businesses where owners want liability protection without the administrative burden of a joint stock company. Its key advantage is structural simplicity; the primary limitation is the 20-member cap, which constrains growth through equity.

Small-to-medium enterprises, family businesses, and professional service firms seeking liability protection with straightforward governance requirements.

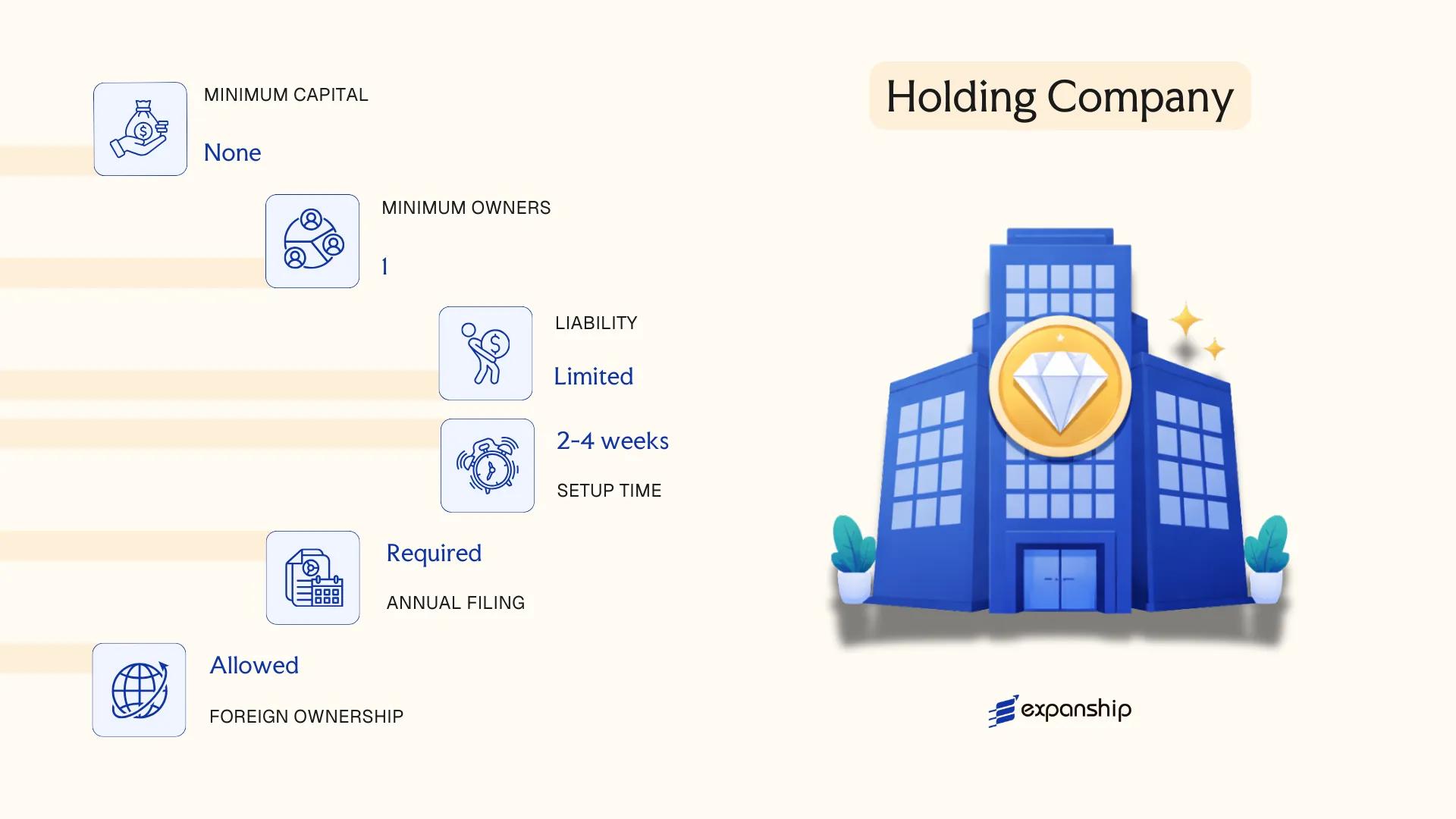

Holding Company (Société Holding)

Holding company formation Lebanon is governed by Legislative Decree No. 45 of 1983, which established a dedicated legal framework separate from the general commercial company law. A Société Holding is a distinct legal entity with its own personality, conferring limited liability on its shareholders while being structurally designed to hold shares in other companies, own intellectual property, and manage intra-group financing rather than conduct direct commercial trade.

The entity functions as a hybrid structure: its operational restrictions are offset by a preferential tax regime that makes it attractive for regional group structuring.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Holding (Joint Stock basis) | Governed by Legislative Decree No. 45 of 1983 |

| Members | Shareholders; minimum 3 | No maximum shareholder cap under the decree |

| Management | Board of Directors; minimum 3 members | Directors need not be Lebanese nationals |

| Local Presence | Registered office in Lebanon required | No mandatory local director, but a registered address is obligatory |

| Share Capital | LBP equivalent; no fixed statutory minimum under Decree 45 | Capital must reflect the scale of assets held |

| Privacy | Shareholder register maintained internally | Beneficial ownership disclosure obligations apply under AML regulations |

Focus Points

- Taxation: Exempt from corporate income tax on dividends received and capital gains from share disposals; a flat 10% tax applies to certain Lebanese-sourced income; distributions to foreign shareholders may attract reduced withholding under applicable tax treaties.

- Permitted Activities: Restricted to holding shares, owning patents or trademarks, and providing financing to subsidiaries — direct trading is prohibited.

- Annual Compliance: Annual financial statements must be filed; an auditor appointment is required under Lebanese commercial law.

- Treaty Access: Lebanon has signed a limited number of double taxation treaties; treaty eligibility depends on the holding entity's residency status and substance.

- Economic Substance: No formal substance regime equivalent to OECD-standard rules, though AML and regulatory scrutiny has increased following FATF assessments.

Closing Paragraph

A Société Holding suits groups seeking to centralise asset ownership or intra-group lending across the Middle East region, with the principal advantage being its dividend and capital gains exemptions under Lebanese holding company regulations. The key limitation is its restriction from conducting any direct commercial activity, which requires a separate operating entity for trading purposes.

Groups or family offices consolidating ownership of regional subsidiaries, IP assets, or investment portfolios under a single Lebanese holding company structure.

Offshore Company (Société Offshore)

Introduced under Legislative Decree No. 46 of 1983, the offshore company Lebanon framework — formally the Société Offshore — is a distinct legal structure designed exclusively for foreign operations conducted outside Lebanese territory. The entity carries separate legal personality and provides shareholders with limited liability, but its operational scope is strictly defined by statute.

Registered with the commercial register and supervised by the Ministry of Finance, this business form is prohibited from conducting commercial activities within Lebanon. Its income must derive entirely from operations, contracts, or services performed abroad.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock structure (SAL framework) | Governed by Legislative Decree No. 46/1983 |

| Members | Shareholders (min. 3) | No maximum; foreign ownership permitted at 100% |

| Local Presence | Registered office in Lebanon required | Physical operations within Lebanon are prohibited |

| Capital | LBP equivalent; no statutory minimum prescribed | Capital must be fully subscribed |

| Privacy | Shareholder names filed with commercial register | Beneficial ownership disclosure obligations apply |

| Auditor | Licensed auditor required | Annual audited financial statements mandatory |

Focus Points

- Taxation: Exempt from Lebanese corporate income tax on foreign-sourced income; a flat annual registration fee applies in lieu of standard taxes; VAT and withholding tax obligations on domestic payments may still apply.

- Economic Substance: No formal substance requirements currently legislated, though operational restrictions reinforce the foreign-activity mandate.

- Annual Compliance: Audited accounts and annual fee payment to the Ministry of Finance are required to maintain registration.

- Treaty Access: Access to Lebanon's tax treaty network is generally restricted for offshore entities given their exempt status.

- Restrictions: Cannot employ staff locally for commercial purposes or invoice clients operating within Lebanese territory.

Closing

A Société Offshore suits businesses using Lebanon as a registration base for holding foreign assets, managing international contracts, or centralising invoicing for non-Lebanese clients. The principal advantage is the tax exemption on foreign income; the corresponding limitation is the absolute prohibition on domestic commercial activity, which removes flexibility if your business later develops a local revenue stream.

This structure fits international trading firms, foreign asset-holding vehicles, or service businesses with no intention of generating revenue within Lebanon.

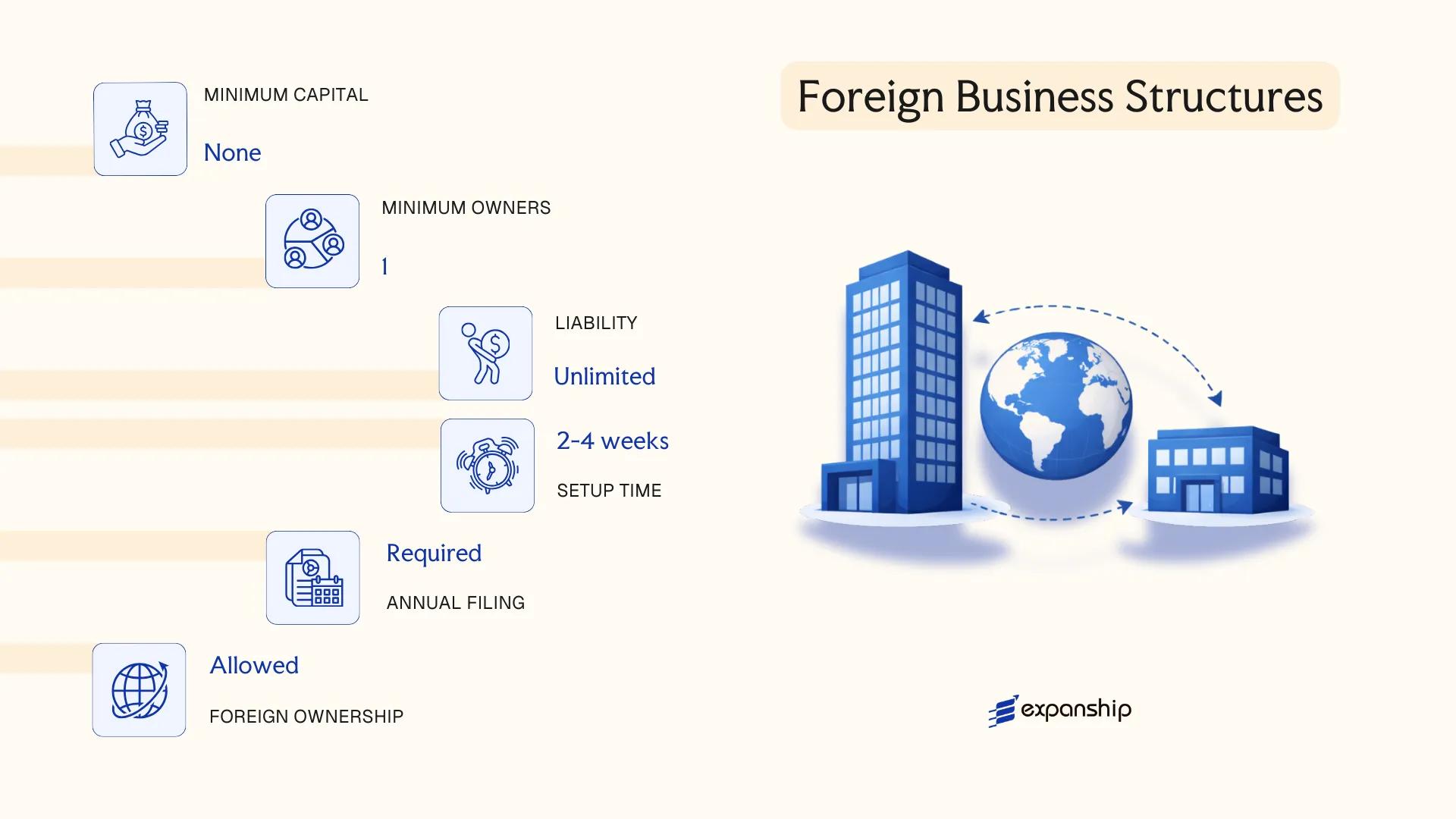

Foreign Business Structures in Lebanon [Branch Office, Representative Office]

Foreign companies seeking a presence without incorporating a separate local entity can do so through a branch office or a representative office. A foreign branch office setup in Lebanon is governed primarily by the Lebanese Code of Commerce and requires registration with the Ministry of Justice's Commercial Register. Unlike a locally incorporated entity, a branch has no separate legal personality — it is a direct extension of the parent company, which bears full liability for its obligations.

Representative offices operate under a more restricted legal framework and are not permitted to generate revenue or conduct commercial transactions within the country.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent company | None — extension of parent company |

| Commercial Activity | Permitted | Not permitted; promotional/liaison only |

| Registration Body | Commercial Register, Ministry of Justice | Commercial Register + Ministry of Economy (varies by activity) |

| Local Manager | Required; must be named in registration documents | Required |

| Capital Requirement | No prescribed minimum; parent's capital applies | None |

| Tax Exposure | Subject to Lebanese corporate income tax on locally sourced profits | Generally not taxable; no revenue activity permitted |

Focus Points

- Taxation: Branch profits sourced locally are subject to the standard 17% corporate income tax; no separate VAT registration threshold applies differently from local entities, and withholding taxes on remittances to the parent may apply depending on the nature of payments.

- Annual Compliance: Both structures must file annual financial statements with the Commercial Register and maintain a designated local representative at all times.

- Treaty Access: Lebanon has a limited network of double taxation agreements; a branch may access treaty benefits in some cases, but this depends on the treaty terms and whether the parent qualifies as a resident.

- Restrictions: Representative offices cannot invoice clients, hold inventory, or sign commercial contracts on behalf of the parent.

- Conversion: A branch can be converted into a locally incorporated entity (such as an SAL or SARL), but this requires a new incorporation process rather than a simple structural amendment.

Closing

A branch office suits foreign firms that need operational presence — such as project execution or service delivery — without the administrative overhead of a fully incorporated subsidiary, though the parent's unlimited exposure to branch liabilities is a significant structural consideration.

Foreign companies with active contracts or project-based work in Lebanon that require a registered local presence but do not yet need a standalone incorporated entity.

Partnerships in Lebanon [General Partnership, Limited Partnership, Joint Venture]

Partnership structures in Lebanon are governed primarily by the Lebanese Code of Commerce (Legislative Decree No. 304 of 1942), which defines the legal framework for general and limited partnerships. These structures do not carry separate legal personality in the same way a SAL or SARL does; partners bear direct legal relationships with the firm's obligations, though the degree of liability varies by form.

Unlike capital-based entities, partnerships are constituted on the basis of mutual agreement between partners, registered with the Commercial Register at the Ministry of Justice. Joint ventures, while commercially recognised, typically operate without registration and function through contractual arrangements between parties.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | General Partnership (Société en Nom Collectif), Limited Partnership (Société en Commandite Simple), Joint Venture (Société en Participation) | Three distinct structures under the Code of Commerce |

| Members | Partners (associés); minimum 2, no statutory maximum | General partners have unlimited liability; limited partners' liability capped at contribution |

| Local Presence | Registered office in Lebanon required for registered partnerships; joint ventures exempt | Joint ventures have no registration requirement |

| Capital | No statutory minimum capital for any partnership form | Contributions may be in cash, kind, or services |

| Privacy | Partner names disclosed in Commercial Register for registered forms | Joint ventures remain largely private |

Focus Points

- Taxation: Partnerships are generally taxed on profits distributed to partners rather than at entity level; individual partners subject to income tax under Lebanese tax law, with no separate corporate tax applied to the partnership itself.

- VAT: Partners conducting commercial activity may be required to register for VAT at the standard 11% rate depending on turnover thresholds.

- Annual Compliance: Registered partnerships must file annual financial accounts with the Commercial Register; joint ventures have no formal filing obligation.

- Treaty Access: Partnerships generally do not qualify as residents for purposes of Lebanon's double tax treaties, as treaty access is typically reserved for corporate entities with legal personality.

- Restrictions: General partners in a Société en Nom Collectif bear unlimited joint and several liability for partnership debts, which presents significant personal financial exposure.

Sub-Types

General Partnership (Société en Nom Collectif)

All partners carry unlimited, joint, and several liability for the firm's obligations. This structure is used primarily by professional practices or family businesses where partners have full operational control and mutual trust governs the arrangement.

Limited Partnership (Société en Commandite Simple)

This form distinguishes between general partners (commandités), who hold unlimited liability and manage the firm, and limited partners (commanditaires), whose liability is confined to their capital contribution. Limited partners may not participate in management without risking reclassification as general partners under Lebanese commercial law.

Joint Venture (Société en Participation)

A joint venture operates solely through a contractual agreement and is not registered with the Commercial Register, making it invisible to third parties. It is used for project-specific collaboration, typically in construction, real estate, or short-term commercial arrangements.

Closing

Partnerships suit professional services firms, family-owned trading businesses, and project-based collaborations where formal corporate structure is unnecessary. The principal advantage is formation simplicity; the primary limitation is that general partners assume unlimited personal liability.

Partnership structures are best suited to small, closely-held businesses or project-specific ventures where partners have pre-existing relationships and are prepared to accept direct liability exposure.

Sole Proprietorship

Sole proprietorship registration Lebanon follows a relatively straightforward process governed primarily by the Lebanese Commercial Code and administered through the Ministry of Economy and Trade and the relevant Chamber of Commerce, Industry, and Agriculture. Unlike the corporate structures covered elsewhere in this guide, a sole proprietorship carries no separate legal personality — the individual owner and the business are treated as a single legal unit.

This absence of a distinct legal identity means the proprietor bears unlimited personal liability for all business debts and obligations. There is no capital shield between personal assets and business liabilities, which distinguishes this structure sharply from forms such as the SAL or SARL.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Établissement Individuel) | Not a separate legal entity; owner and business are legally identical |

| Owner Title | Proprietor | Single individual only; no partners or shareholders permitted |

| Membership | 1 proprietor (minimum and maximum) | Must be a natural person; legal entities cannot hold this form |

| Local Presence | Registered business address required | Registration with the relevant regional Chamber of Commerce is mandatory |

| Capital | No statutory minimum | Owner's personal funds used; no formal capitalisation requirement |

| Privacy | Owner's name is publicly associated with the trade name | Limited privacy; the individual is directly identifiable |

Focus Points

- Taxation: Subject to personal income tax under a progressive schedule administered by the Lebanese Ministry of Finance; VAT registration is required once turnover exceeds the statutory threshold (currently LBP 100 million, though thresholds are subject to revision).

- Annual Compliance: Must renew registration with the Chamber of Commerce annually and maintain basic accounting records per Lebanese Commercial Code requirements.

- Treaty Access: Cannot access corporate tax treaties as a legal person; income is taxed at the individual level only.

- Conversion: Can be converted into a SARL or other corporate form, though conversion requires a formal incorporation process rather than a simple structural amendment.

- Restrictions: Foreign nationals face limitations on operating as sole traders in Lebanon, particularly in activities reserved for Lebanese citizens under applicable sector-specific regulations.

Closing Paragraph

A sole proprietorship suits small-scale traders, freelance professionals, and individual service providers who operate locally with modest revenues and minimal liability exposure. The primary advantage is administrative simplicity and low setup cost; the clear limitation is unlimited personal liability, which makes this structure unsuitable for any activity carrying meaningful financial or legal risk.

Lebanese nationals running small, low-risk commercial or professional activities who prioritise minimal administrative overhead over liability protection.

How to Choose the Right Entity Type in Lebanon

Choosing the right company type in Lebanon is a structural decision with direct legal and financial consequences — not an administrative formality.

Why Your Entity Choice Matters

The structure you register shapes your tax exposure, compliance obligations, and operational rights from day one. Choosing incorrectly produces concrete, often costly outcomes:

- Registering an offshore company under Decree-Law No. 46 of 1983 while conducting local trade violates the terms of that structure, exposing the entity to regulatory sanctions or cancellation.

- Opting for a holding company to benefit from its exemptions forfeits access to Lebanon's limited double tax treaty network, since treaty eligibility depends on the entity's tax residency status.

- Selecting an entity that mandates audited annual financial statements for a single-person consultancy operation generates recurring compliance costs with no corresponding regulatory benefit.

- Using a joint stock company when asset protection or succession planning is the primary objective locks you into annual shareholder meetings and board obligations that other civil-law structures do not impose.

Key Factors to Consider

- Business Activity: Active local trade, passive asset holding, and regulated sectors each require a distinct legal form under Lebanese commercial law.

- Local vs. Cross-Border Operations: Entities conducting business with Lebanese residents must be registered with the Lebanese Commercial Register and cannot operate under offshore restrictions.

- Ownership Structure: Single-owner operations or closely held businesses may find the SARL more practical, while multi-investor ventures requiring capital markets access point toward the SAL.

- Tax Objectives: Full exemption regimes and treaty access are mutually exclusive in Lebanon, so your tax position must be determined before entity selection.

- Substance Capacity: If you cannot maintain a physical presence or local management, certain structures carry compliance risks that an exempt holding or offshore form may avoid.

- Exit and Conversion: Not all Lebanese entity types permit straightforward conversion or redomiciliation, so your anticipated exit pathway should factor into the initial formation decision.

Compliance Services for Companies in Lebanon

Ongoing compliance support for Lebanese entities, including annual filings, renewal obligations, and regulatory reporting with the relevant Lebanese authorities.

Conclusion

Setting up a company in Lebanon requires matching your business objectives to a structure that fits both the legal framework and your operational needs. The SAL suits larger businesses requiring public capital-raising capacity, while the SARL remains the most widely registered entity type in Lebanon, preferred for its accessible minimum capital threshold and operational flexibility. Holding companies under Decree-Law No. 45 of 1983 serve primarily as asset and investment vehicles, and offshore companies under Decree-Law No. 46 are structured specifically for businesses operating exclusively outside Lebanese territory. Branches and representative offices extend the reach of foreign entities without establishing a separate legal person. General and limited partnerships, along with sole proprietorships, address smaller-scale or domestically focused operations.

Ongoing reforms to the Commercial Register and increased engagement with bilateral investment treaty frameworks suggest a gradual move toward greater regulatory transparency. Expanship's team works directly with these structures across all stages of the incorporation process.

How Expanship Can Assist You

Expanship company formation services Lebanon cover the full registration process, from selecting the appropriate entity type — SAL, SARL, Holding, or Offshore — through to completing filings with the Commercial Register at the Ministry of Justice. Each structure carries distinct capital requirements, governance rules, and compliance obligations, and our team works through those specifics with you directly.

From initial documentation to post-incorporation management, our service scope includes:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Commercial Register filings and liaison with the Ministry of Justice

- Ongoing compliance management, including annual filing obligations

- Banking introduction assistance for corporate account opening

Your business deserves straightforward support, not guesswork. Reach out to Expanship Lebanon to discuss your setup.

Frequently Asked Questions (FAQ)

The Société à Responsabilité Limitée (SARL) is the most frequently registered structure, primarily because it combines limited liability with a relatively low minimum capital requirement and a simpler governance framework than a SAL. Its flexibility makes it accessible to both local entrepreneurs and foreign investors entering the market.

A Société Offshore is restricted from conducting commercial activity within Lebanon and benefits from a preferential tax regime under Legislative Decree No. 46 of 1983. A SARL, by contrast, is fully authorised to trade domestically and is subject to standard corporate tax. Compliance obligations for offshore entities are lighter, but their operational scope is narrower.

The Société Holding offers a comparatively higher degree of confidentiality, as detailed beneficial ownership information is not routinely published in the Commercial Register. Nominee arrangements are available under Lebanese law, though they must be documented appropriately.

No. A SAL requires a minimum of three shareholders, and a SARL requires at least one. General and limited partnerships require at least two partners by definition. A sole proprietorship is the only structure that a single individual can form without any co-participants.

Foreigners may establish a SAL, SARL, Holding Company, or Offshore Company, subject to sector-specific foreign ownership restrictions regulated by the Ministry of Economy and Trade. Branch offices of foreign firms are also permitted following approval from the same ministry. Certain regulated industries impose additional licensing requirements regardless of the entity chosen.

Lebanese commercial law permits the transformation of a SARL into a SAL, provided the new structure meets the applicable capital and shareholder thresholds. Conversion in the reverse direction is less common and subject to procedural requirements before the Commercial Court. Not all entity types can be converted into one another directly.

A SAL, SARL, Holding Company, and Offshore Company each hold distinct legal personality under Lebanese law. General partnerships also carry legal personality, though partners remain personally liable for the firm's obligations. A sole proprietorship does not create a separate legal entity.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.