Key Takeaways

- The TOO (Tovarishchestvo s Ogranichennoy Otvetstvennostyu) is Kazakhstan's most widely registered entity type, governed by the Law on Limited Liability Partnerships and favored by small and mid-sized businesses for its straightforward formation process.

- Company registration in Kazakhstan falls under the Ministry of Justice of the Republic of Kazakhstan, which maintains the State Register of Legal Entities.

- Foreign companies can establish a market presence in Kazakhstan without creating a separate legal person by registering a Branch Office or Representative Office.

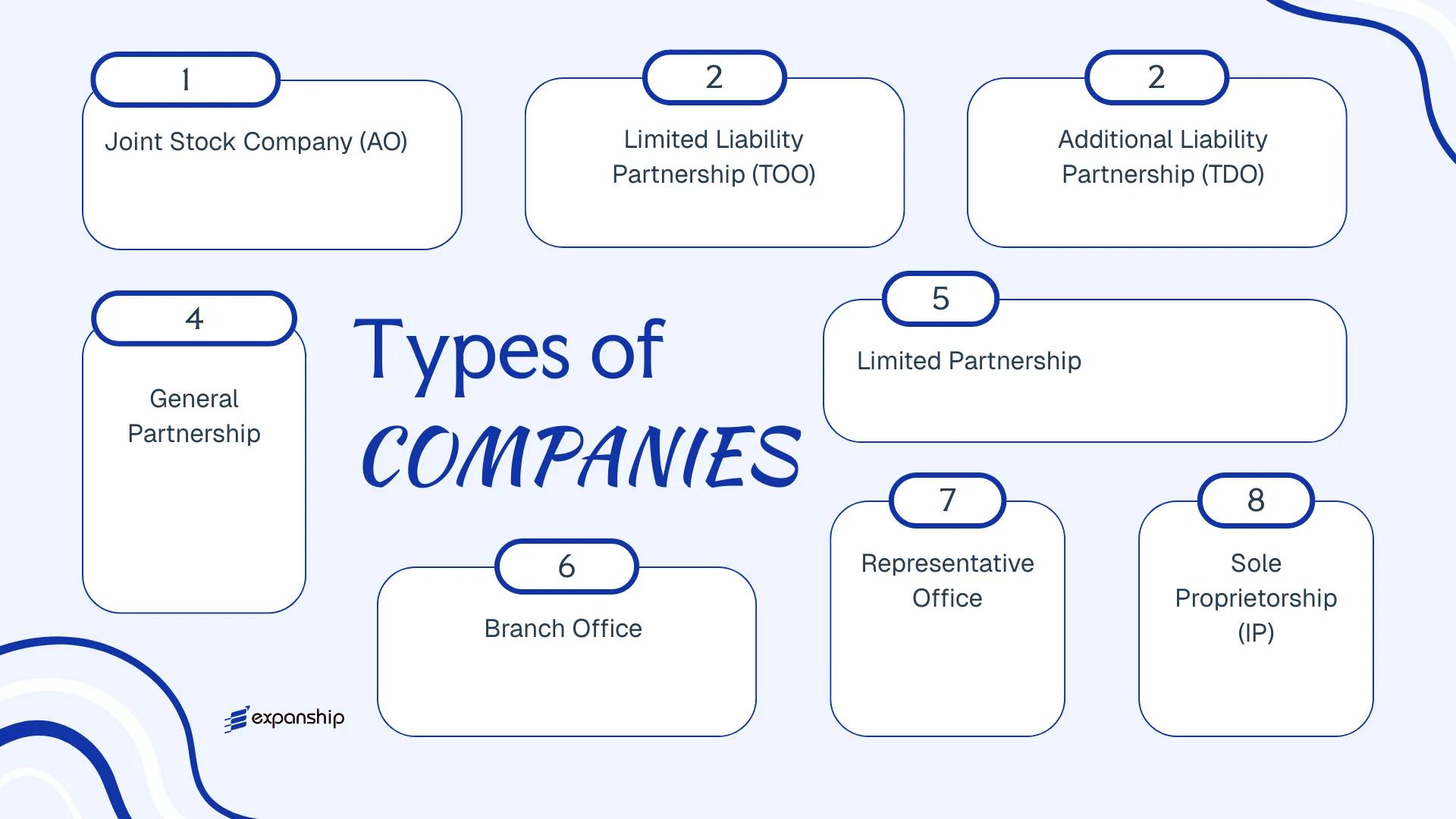

- Kazakhstan's available legal entity types span eight distinct structures — including the AO, TOO, TDO, General Partnership, Limited Partnership, and Sole Proprietorship — each carrying different requirements around liability, ownership, and governance.

Introduction to Entity Types in Kazakhstan

Kazakhstan is a landlocked nation in Central Asia, bordered by Russia, China, Kyrgyzstan, Uzbekistan, and Turkmenistan. As the world's largest landlocked country by area, it operates as a unitary presidential republic with a legal framework shaped substantially by civil law traditions. Selecting among the available types of business entities in Kazakhstan requires an understanding of that framework before any registration step begins.

Company registration falls under the jurisdiction of the Ministry of Justice of the Republic of Kazakhstan, which oversees the State Register of Legal Entities. The primary legislation governing corporate structures is the Civil Code of the Republic of Kazakhstan and a series of entity-specific laws, including the Law on Joint Stock Companies and the Law on Partnerships.

Kazakhstan applies a standard corporate tax regime with a general corporate income tax rate, and has signed a substantial number of double taxation treaties. Available Kazakhstan legal entity types include the Joint Stock Company (AO), Limited Liability Partnership (TOO), Additional Liability Partnership (TDO), General Partnership, Limited Partnership, Branch Office, Representative Office, and Sole Proprietorship (IP). Each structure carries distinct requirements around liability, ownership, governance, and registration — all of which the sections below examine in full.

An Overview of Business Structures in Kazakhstan

Kazakh company law recognises several distinct entity types, each governed primarily by the Civil Code of the Republic of Kazakhstan and specific statutes such as the Law on Joint Stock Companies (No. 415-II) and the Law on Partnerships (No. 220-I). Each structure carries a different liability profile, ownership model, and operational scope. The sections that follow examine each form in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Joint Stock Company (AO) | Corporate entity | Limited to shares | Taxed | Yes | 1 shareholder | Ministry of Justice | Law No. 415-II |

| Limited Liability Partnership (TOO) | Partnership | Limited to contribution | Taxed | Yes | 1 participant | Ministry of Justice | Law No. 220-I |

| Additional Liability Partnership (TDO) | Partnership | Additional personal liability | Taxed | Yes | 2+ participants | Ministry of Justice | Law No. 220-I |

| General Partnership (PT) | Partnership | Unlimited, joint | Taxed | Yes | 2+ partners | Ministry of Justice | Civil Code |

| Limited Partnership (KT) | Partnership | Mixed | Taxed | Yes | 1 general + 1 limited | Ministry of Justice | Civil Code |

| Branch Office | Non-legal entity | Parent company liable | Taxed | Yes | Parent company | Ministry of Justice | Civil Code |

| Representative Office | Non-legal entity | Parent company liable | Generally exempt | No | Parent company | Ministry of Justice | Civil Code |

| Sole Proprietorship (IP) | Individual | Unlimited personal | Taxed | Yes | 1 individual | State Revenue Committee | Entrepreneurial Code |

Each of these structures is examined in full in the sections below.

Joint Stock Company (Aktsionernoye Obshchestvo, AO)

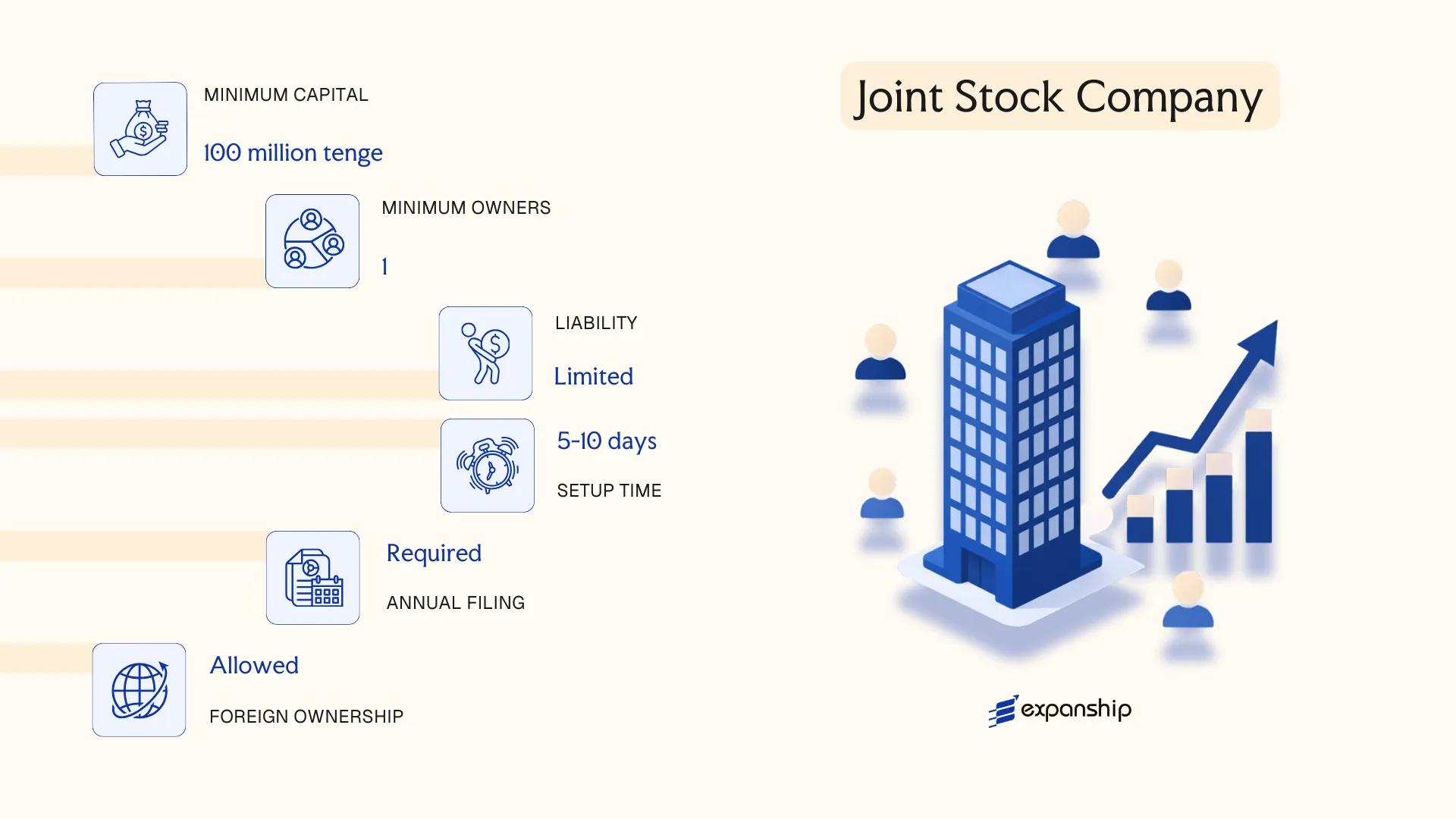

Governed by the Law of the Republic of Kazakhstan No. 415-II "On Joint Stock Companies" (2003, as amended), the joint stock company AO Kazakhstan is the primary vehicle for large-scale commercial activity and public capital markets. The AO carries separate legal personality, meaning the entity itself — not its shareholders — bears legal and financial obligations.

Liability is limited to the value of shares held. This structure accommodates both private and public ownership, making it a hybrid instrument suited to domestic conglomerates, financial institutions, and foreign-backed enterprises seeking capital flexibility.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company (AO) | Recognised under Kazakhstani civil and corporate law |

| Members | Shareholders | Minimum 1 shareholder; no statutory maximum |

| Governing Bodies | General Meeting, Board of Directors, Executive Body | Board of Directors mandatory for public AOs |

| Local Presence | Registered legal address required | Must be a physical address in Kazakhstan |

| Share Capital | Minimum KZT 100,000 for private AO; higher thresholds apply for regulated sectors (e.g., banking, insurance) | Capital divided into shares; both common and preferred shares permitted |

| Privacy | Shareholder register maintained; public AOs subject to mandatory disclosure | Private AOs have limited public disclosure obligations |

Focus Points

- Taxation: Subject to corporate income tax at 20%, VAT at 12% (if turnover exceeds the registration threshold), and dividend withholding tax at 15% (reduced under applicable double tax treaties).

- Annual Compliance: Mandatory audited financial statements, annual general meeting, and regulatory reporting to the Agency for Regulation and Development of the Financial Market (for regulated AOs).

- Treaty Access: Kazakhstan's broad DTT network can reduce withholding tax rates on dividends, interest, and royalties for qualifying foreign shareholders.

- Conversion: An AO may be reorganised into a TOO or other entity form under Chapter 5 of the Civil Code of Kazakhstan, subject to creditor notification procedures.

- Restrictions: Certain strategic sectors (subsoil use, banking, media) impose additional licensing, foreign ownership caps, or prior regulatory approval requirements.

Sub-Types

Public Joint Stock Company (Publichnoye AO)

Shares are offered to the public and traded on an exchange such as the Astana International Exchange (AIX) or Kazakhstan Stock Exchange (KASE). This sub-type carries enhanced disclosure obligations and stricter corporate governance requirements relative to the private form.

Private Joint Stock Company (Zakrytoye AO)

Share placement is restricted to a defined circle of persons; public subscription is not permitted. This structure suits closely held businesses that require the AO's corporate framework without the compliance burden of public listing.

The AO suits holding structures, regulated financial entities, and businesses with institutional investors or planned public offerings. Its principal advantage is unrestricted share transferability and access to capital markets; however, ongoing corporate governance obligations — mandatory board structures, audited accounts, and regulatory filings — make it operationally heavier than simpler entity forms.

The AO is most appropriate for large enterprises, regulated institutions, and businesses actively seeking external investment or eventual public listing.

Company Incorporation in Kazakhstan

Expanship assists with AO formation, registered address, and ongoing compliance support across Kazakhstan.

Limited Liability Partnership (Tovarishchestvo s Ogranichennoy Otvetstvennostyu, TOO)

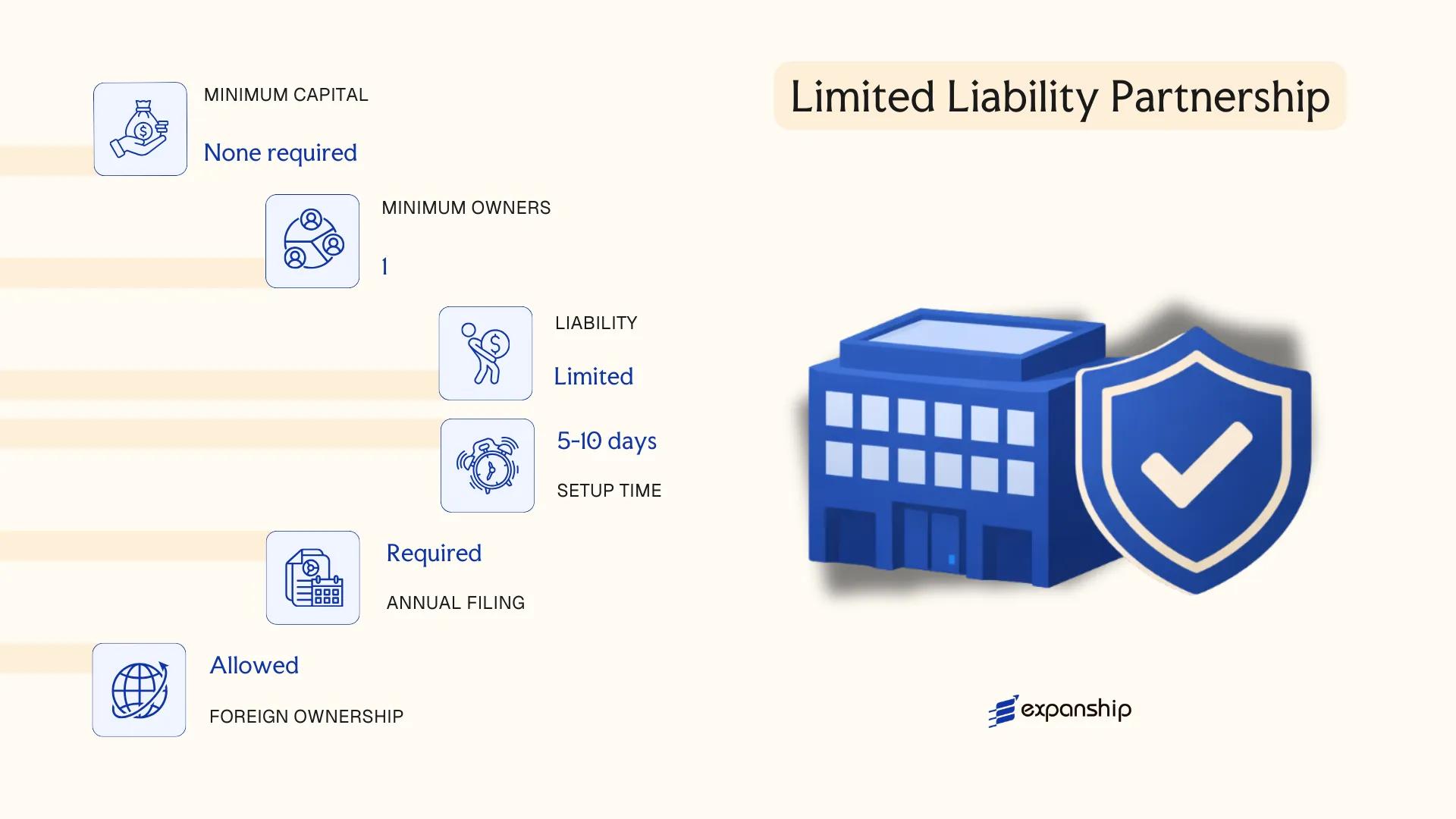

The limited liability partnership TOO Kazakhstan is governed primarily by the Law of the Republic of Kazakhstan "On Partnerships with Limited and Additional Liability" No. 220-I, enacted in 1998, along with the Civil Code of Kazakhstan. A TOO holds separate legal personality, meaning it exists independently of its participants, and liability is confined to the entity's assets.

Participants are not personally responsible for the TOO's obligations beyond their contributed capital. This structural separation makes the form suitable for foreign investors and domestic operators alike, functioning as a hybrid between a full partnership and a corporate structure.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Partnership (TOO) | Separate legal personality; governed by Law No. 220-I (1998) |

| Members | Participants (founders/shareholders); 1–50 | A sole participant TOO is permitted; exceeding 50 requires conversion to an AO |

| Management | General Director (executive body) + Supreme Body (participants' meeting) | Single-member entities may combine both roles |

| Local Presence | Registered legal address in Kazakhstan required | Physical office or registered address service acceptable |

| Capital | Minimum 100 MRP (Monthly Calculation Index); denominated in KZT | MRP value is set annually by the government |

| Privacy | Participant information filed with the State Revenue Committee | Not publicly searchable via a free central registry |

Focus Points

- Taxation: Subject to corporate income tax at 20%, VAT at 12% (registration threshold applies), and withholding tax on dividends paid to non-residents at 15% (reducible under applicable tax treaties).

- Treaty Access: TOOs qualify for Kazakhstan's double tax treaty network, covering 50+ jurisdictions, subject to beneficial ownership requirements.

- Annual Compliance: Mandatory annual financial statements; audits required when thresholds on revenue or headcount are met under Kazakhstani accounting law.

- Foreign Participation: No statutory restriction on 100% foreign ownership, though certain regulated sectors impose nationality or licensing conditions.

- Conversion: A TOO exceeding 50 participants must convert to a Joint Stock Company (AO) under the governing legislation.

Closing

A TOO suits trading operations, holding structures, and service businesses where operational flexibility and contained liability are priorities; the participant cap of 50 is the primary structural constraint for businesses anticipating significant equity distribution.

Best suited for small-to-medium foreign-owned businesses, joint ventures, or domestic operators seeking a straightforward corporate structure without the disclosure and governance obligations of a Joint Stock Company.

Additional Liability Partnership (Tovarishchestvo s Dopolnitelnoy Otvetstvennostyu, TDO)

The additional liability partnership TDO Kazakhstan is governed by the Law of the Republic of Kazakhstan "On Partnerships with Limited and Additional Liability" (No. 220-I, 1998), the same legislation that regulates the TOO. It holds a separate legal personality, meaning the entity itself — not its participants — enters into contracts, owns assets, and bears obligations.

What distinguishes a TDO company Kazakhstan from a standard TOO is the liability structure. Participants bear responsibility not only to the value of their contributed capital but also to an additional, pre-agreed multiple of that contribution. This makes it a hybrid: limited liability by default, with a defined layer of personal exposure layered on top.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability partnership with additional liability | Separate legal personality; governed by Law No. 220-I, 1998 |

| Members | Participants (1–100) | Referred to as "participants"; no board requirement for small firms |

| Liability Exposure | Contribution plus a fixed additional multiple | The multiple must be defined in the charter |

| Local Presence | Registered legal address required | No mandatory resident director, but a registered address in Kazakhstan is obligatory |

| Capital | Minimum 100 MCI (Monthly Calculation Index) | Denominated in Kazakhstani Tenge |

| Privacy | Participant register filed with the Ministry of Justice | Beneficial ownership disclosure required under AML regulations |

Focus Points

- Taxation: Subject to corporate income tax at 20%, VAT at 12% (if turnover exceeds the registration threshold), and withholding tax on dividends paid to non-residents, typically at 15% unless a tax treaty applies.

- Annual Compliance: Mandatory financial reporting and tax filings with the State Revenue Committee; audit requirements depend on entity size thresholds.

- Treaty Access: Qualifies as a Kazakhstan tax resident entity, granting access to the country's double tax treaty network, subject to substance requirements.

- Conversion: A TDO may be reorganised into a TOO or AO through a formal restructuring procedure under civil and corporate law.

- Practical Use: Rarely chosen over the TOO in practice; the additional liability clause discourages adoption except where contractual counterparties specifically require it.

Closing

A TDO suits businesses in sectors where counterparties or regulators demand a higher accountability threshold than a standard TOO provides, though the additional personal exposure of participants remains its defining constraint.

Firms operating in industries where demonstrating enhanced participant accountability is a commercial or regulatory requirement — such as certain financial services or professional service structures.

Partnerships in Kazakhstan [General Partnership, Limited Partnership]

Governed by the Civil Code of the Republic of Kazakhstan (1994) and the Law on Partnerships and Joint Stock Companies, general and limited partnership Kazakhstan structures occupy a narrow but defined space in the corporate registry. Both forms carry separate legal personality, meaning the entity can enter contracts and hold property in its own name. Liability treatment differs sharply between the two, which is the primary structural distinction that shapes how each is used.

Registration is handled through the State Corporation "Government for Citizens," and the entity must be entered into the National Register of Business Identification Numbers to obtain legal status. A polnoye tovarishchestvo Kazakhstan (full/general partnership) holds all partners jointly and severally liable, while the limited partnership (Kommanditnoye Tovarishchestvo) introduces a tiered membership structure separating liability exposure between partner classes.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Polnoye Tovarishchestvo (General) / Kommanditnoye Tovarishchestvo (Limited) | Both carry separate legal personality |

| Members | General Partners: min. 2, no statutory maximum; Limited Partners (KT only): min. 1 | General partners manage; limited partners contribute capital only |

| Liability | General Partners: joint and several, unlimited; Limited Partners: capped at contribution | No liability protection for general partners |

| Local Presence | Registered legal address in Kazakhstan required | No statutory registered agent requirement |

| Capital | No prescribed statutory minimum; denominated in Kazakhstani Tenge (KZT) | Contributions documented in the foundation agreement |

| Privacy | Founding agreement and partner details filed with the registry | No public share register, but partner identities are disclosed |

Focus Points

- Taxation: Profits allocated to partners are subject to individual income tax at 10% or corporate income tax depending on partner status; VAT registration required if annual turnover exceeds the statutory threshold; withholding tax applies to non-resident partners on Kazakhstani-sourced income.

- Annual Compliance: Partners must file financial statements; full accounting records are maintained at the registered address.

- Treaty Access: Access to Kazakhstan's double tax treaty network depends on the tax residency of individual partners, not the partnership itself.

- Restrictions: Foreign nationals may participate as limited partners; participation as a general partner by a foreign legal entity may trigger additional regulatory review.

- Conversion: Partnerships may be reorganised into other legal forms, including a TOO, subject to Civil Code reorganisation procedures.

Sub-Types

General Partnership (Polnoye Tovarishchestvo)

All participants hold the status of general partner, bearing unlimited joint liability for obligations of the firm. This structure is used almost exclusively among closely held professional or family-run enterprises where partners are willing to accept full personal exposure.

Limited Partnership (Kommanditnoye Tovarishchestvo)

At least one general partner manages the business and accepts unlimited liability, while one or more limited partners contribute capital without taking on management responsibility or personal liability beyond their contribution. This split makes the structure marginally more attractive to passive investors.

Closing

Both partnership forms are most applicable to small, closely held operations where the participants have an established relationship and limited external financing needs; the unlimited liability of general partners makes these structures unsuitable for ventures carrying significant commercial or financial risk.

Partnerships in Kazakhstan are best suited for small professional practices or family enterprises where all principals are prepared to accept personal liability exposure.

Foreign Business Presence in Kazakhstan [Branch Office, Representative Office]

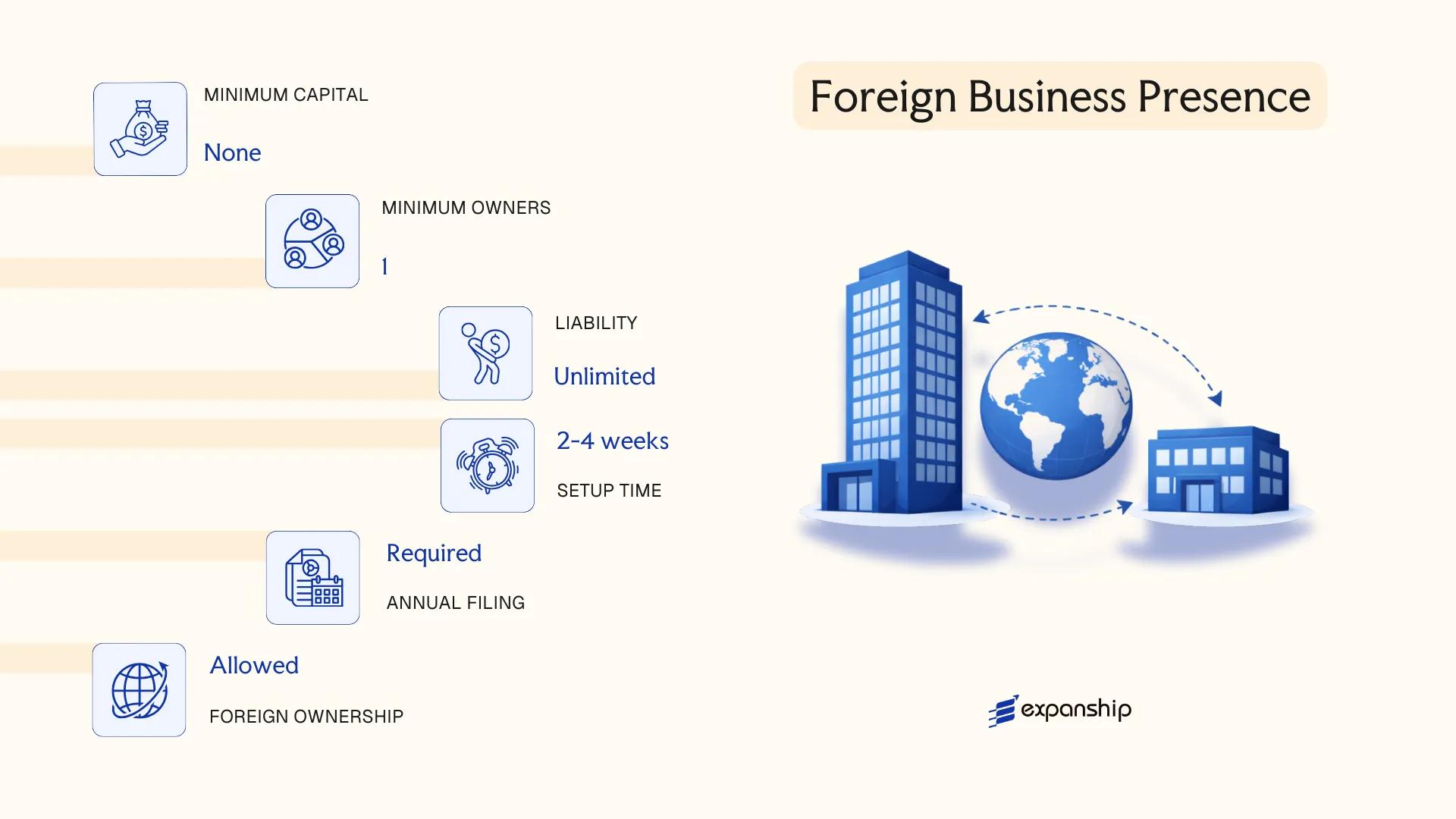

A foreign company branch office Kazakhstan registration is governed primarily by the Law of the Republic of Kazakhstan "On Legal Entities" (No. 2-I, 1995) and the Law "On State Registration of Legal Entities and Record Registration of Branches and Representative Offices" (No. 562-II, 2004). Neither a branch nor a representative office constitutes a separate legal entity — both are structurally dependent subdivisions of the parent company and carry no independent legal personality.

Accreditation for both forms is handled through the Ministry of Justice of Kazakhstan. A branch may conduct commercial operations on behalf of the parent, while a representative office is restricted to non-commercial functions such as market research, promotional activities, and liaison work.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Non-legal entity subdivision of a foreign company | Non-legal entity subdivision of a foreign company |

| Permitted Activities | Commercial and operational activities | Non-commercial only (marketing, liaison, research) |

| Management | Head appointed by parent; acts under power of attorney | Representative appointed by parent; acts under power of attorney |

| Local Presence | Registered legal address in Kazakhstan required | Registered legal address required |

| Capital | No statutory minimum capital requirement | No statutory minimum capital requirement |

| Accreditation Body | Ministry of Justice of Kazakhstan | Ministry of Justice of Kazakhstan |

| Accreditation Term | Up to 3 years, renewable | Up to 3 years, renewable |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at 20%; VAT applies at 12% on taxable supplies; withholding tax on remittances to the parent may apply at rates varying by applicable tax treaty; representative offices generally have no taxable income but must maintain accounting records.

- Compliance: Both forms must file annual financial statements and maintain accounting records under Kazakhstani standards regardless of operational status.

- Treaty Access: Tax treaty benefits available to the parent company may extend to branch operations, subject to the terms of the applicable double taxation agreement.

- Restrictions: A representative office cannot generate revenue or enter into commercial contracts in its own right; any commercial activity requires conversion to a branch or locally incorporated entity.

- Conversion: Neither form can be directly converted into a legal entity — dissolution and fresh incorporation are required if the parent seeks to establish a TOO or AO.

Closing

Branch offices suit foreign firms testing operational presence before committing to full incorporation, while representative offices serve companies whose local activity is limited to information-gathering or client support. The primary limitation of both forms is their complete legal and financial dependency on the parent entity.

Foreign companies seeking a controlled, temporary, or preparatory presence without incorporating a standalone legal entity in Kazakhstan.

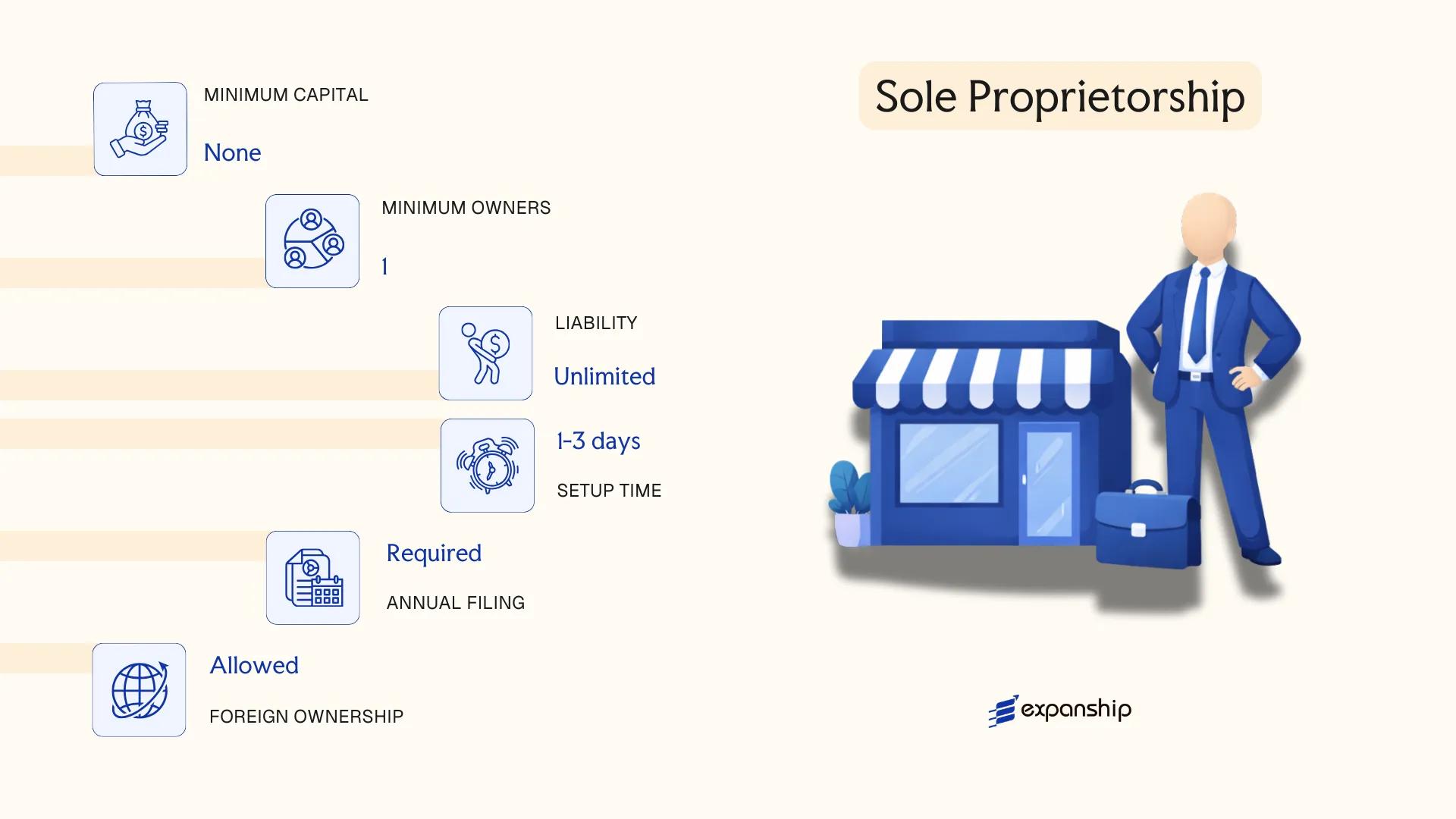

Sole Proprietorship (Individualny Predprinimatel, IP)

A sole proprietorship IP Kazakhstan operates under the Law of the Republic of Kazakhstan "On Private Entrepreneurship" (No. 124-IV, 2006), alongside the Entrepreneurial Code adopted in 2015, which consolidated the regulatory framework for individual business activity. Unlike a TOO or AO, an IP does not constitute a separate legal entity — the individual and the business are one and the same in law.

Registration is handled through the State Revenue Committee or via the eGov portal, and in many cases qualifies for a simplified notification-based procedure rather than a full registration process, depending on the scale of activity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Individual business activity; no separate legal personality | Proprietor bears unlimited personal liability |

| Members | Single individual (proprietor) | Foreign nationals may register subject to residency conditions |

| Local Presence | Registered address required | Home address permissible in many cases |

| Capital | No statutory minimum | No paid-up capital requirement |

| Privacy | Name of proprietor is publicly linked to the business | No shareholder register distinct from the individual |

Focus Points

- Taxation: Subject to individual income tax (IIT) at 10%; VAT registration required if annual turnover exceeds the statutory threshold; simplified patent or general tax regime available depending on activity type.

- Annual Compliance: Submission of tax declarations; no audit obligation at this scale.

- Treaty Access: Limited access to Kazakhstan's tax treaty network compared to corporate entities.

- Conversion: Can be converted into a TOO by re-registering; assets and liabilities transfer by the proprietor's decision.

- Restrictions: Cannot issue shares, bring in partners, or raise equity capital.

Closing

An IP suits individual consultants, freelancers, and small traders who operate domestically with low administrative overhead, though the absence of liability separation exposes personal assets to business creditors without any protective structure.

An IP is most appropriate for resident individuals running small-scale, low-risk operations who prioritise minimal compliance costs over liability protection.

How to Choose the Right Entity Type in Kazakhstan

Knowing how to choose a business entity in Kazakhstan before registration prevents structural problems that are costly or procedurally complex to unwind later.

Why Your Entity Choice Matters

The structure you register has binding legal and financial consequences.

- Registering a representative office when your operations involve direct commercial transactions violates the permitted scope under Kazakhstani law, exposing the parent company to penalties and potential forced closure of the presence.

- Selecting a TOO that qualifies for a simplified tax regime when your counterparties require withholding tax treaty benefits may disqualify you from claiming reductions under Kazakhstan's double tax agreements.

- Choosing a general partnership structure when your activity requires regulatory licensing — such as financial services overseen by the Agency of the Republic of Kazakhstan for Regulation and Development of the Financial Market — creates a compliance mismatch, as certain licences are only issued to specific entity forms.

- Forming a TOO when a sole proprietorship would suffice for a single-person consultancy adds mandatory statutory obligations, including capital requirements and formal liquidation procedures, that do not apply to an IP.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each correspond to distinct permitted entity forms under the Law of the Republic of Kazakhstan No. 220-I "On Business Partnerships" and related legislation.

- Ownership and Management: A sole founder can form a TOO without a board, whereas an AO mandates a board of directors and a general shareholders' meeting, making it more appropriate for multi-investor structures.

- Tax Objectives: Your eligibility for the simplified declaration regime, general tax regime, or specific sector incentives determines which entity type serves your fiscal position.

- Substance Capacity: If your firm cannot maintain a physical office and resident staff, an entity type with lower presence thresholds reduces the risk of being treated as lacking local substance.

- Privacy Requirements: The Business Identification Number register is publicly accessible, so nominee arrangements or specific structuring may be necessary if shareholder confidentiality is a priority.

- Exit Strategy: Conversion between entity types in Kazakhstan follows distinct statutory procedures; a TOO can be reorganised into an AO, but the reverse requires meeting minimum capital thresholds and re-registration with the State Revenue Committee.

Compliance Services for Companies in Kazakhstan

Ongoing compliance support for Kazakhstani entities, including annual filings, regulatory reporting, and statutory maintenance.

Conclusion

Selecting the right structure is the first substantive decision in any incorporating a company in Kazakhstan guide, and it carries consequences for liability, governance, and tax treatment that persist throughout the life of the business. The TOO remains the most registered entity type in the country, favored by small and mid-sized businesses for its straightforward formation process under the Law on Limited Liability Partnerships. The AO suits firms requiring equity capital structures or public investor access. Branches and representative offices serve foreign companies testing the market without establishing a separate legal person. The TDO and partnership forms occupy narrower use cases tied to specific liability arrangements.

Regulatory activity under the Agency for Regulation and Development of the Financial Market, combined with Kazakhstan's expanding double tax treaty network, signals continued institutional development. Professional guidance can reduce exposure to procedural errors during registration and ongoing compliance.

How Expanship Can Assist You

Expanship's Kazakhstan company formation services cover the full registration process, from selecting the right legal form under the Law on Partnerships and Joint Stock Companies to filing with the State Corporation "Government for Citizens," which serves as the primary registrar for new legal entities. Your choice of structure, whether a TOO, AO, or branch of a foreign company, shapes every compliance obligation that follows, and our corporate services in Kazakhstan are built around those specific requirements.

From document preparation to post-registration maintenance, our team handles the operational details so your business can function without administrative delays:

- Document preparation, notarisation, and apostille/legalisation

- Registered agent and legal address provision in Kazakhstan

- Filing and liaison with the State Corporation "Government for Citizens"

- Tax registration with the State Revenue Committee

- Post-incorporation compliance and annual reporting support

- Banking introduction assistance with local financial institutions

Reach out to Expanship Kazakhstan to discuss your incorporation requirements directly.

Frequently Asked Questions (FAQ)

The Limited Liability Partnership (TOO) is the most frequently registered business structure, governed by the Law of the Republic of Kazakhstan No. 220-I "On Partnerships with Limited and Additional Liability." Its combination of single-member eligibility, capped liability, and relatively straightforward registration at the Ministry of Justice makes it the default choice for small and medium-sized businesses.

A TOO is an independent legal entity subject to corporate income tax at 20% on its own profits, while a Branch Office has no separate legal personality and is taxed as an extension of its foreign parent. The TOO can enter contracts, own assets, and trade locally in its own name; a Branch derives all legal capacity from the parent company and carries higher ongoing compliance reporting obligations to the parent's home jurisdiction.

Among registered structures, the TOO offers a relatively contained disclosure profile. Beneficial ownership information is held in the State Register of Legal Entities, but day-to-day director and shareholder details are not published in a centrally accessible public database comparable to some Western registries. Nominee arrangements are legally permissible, though substance requirements under Kazakhstan's tax legislation must be observed.

No. A General Partnership requires at least two participants, and a Limited Partnership requires at least one general partner and one limited partner. A TOO, a Joint Stock Company (AO), and a Sole Proprietorship (IP) can each be established by a single individual or legal entity, subject to minimum capital requirements where applicable.

Foreign individuals and legal entities may establish a TOO, an AO, a Branch Office, or a Representative Office without restriction on ownership percentage, subject to sector-specific licensing rules in areas such as banking, telecommunications, and natural resources. Foreign nationals may also register as a Sole Proprietor (IP) if they hold a valid residence permit. The TOO remains the most practical entry point for foreign investors seeking full operational capacity.

Conversion between entity types is permitted under the Civil Code of the Republic of Kazakhstan. A TOO may be reorganised into an AO, and partnerships may be converted into other commercial structures through a formal reorganisation procedure filed with the Ministry of Justice. The process requires shareholder or participant approval, updated charter documents, and re-registration of the entity under its new legal form.

Not all. A TOO, AO, TDO, General Partnership, and Limited Partnership all hold the status of legal entities under Kazakhstan civil law. A Representative Office and a Branch Office do not — both are structural subdivisions of a foreign company and cannot independently enter binding legal obligations. A Sole Proprietor (IP) operates as a natural person rather than a distinct legal entity, which directly affects liability exposure.

The Sole Proprietorship (IP) has the most limited compliance burden, with simplified tax reporting available under the special tax regimes established in the Tax Code of the Republic of Kazakhstan. That said, its unlimited personal liability and restrictions on scale make it unsuitable for ventures requiring external investment or multi-party ownership. For structured businesses, a TOO under the general tax regime represents the next most manageable compliance profile.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.