Key Takeaways

- The With Limited Liability Company (WLL) is the most commonly registered structure for foreign investors in Kuwait, though it requires a Kuwaiti partner arrangement under the Kuwait Companies Law No. 1 of 2016.

- Corporate tax in Kuwait applies primarily to foreign-owned entities, while Kuwaiti and GCC-owned businesses are generally exempt from income tax depending on ownership structure.

- Foreign Direct Investment Law No. 116 of 2013, administered alongside the Ministry of Commerce and Industry, governs the conditions under which foreign capital may enter the Kuwaiti market.

- Available legal forms in Kuwait range from capital-intensive Closed Joint Stock Companies to bounded-mandate structures such as branch offices and representative offices, each serving distinct operational purposes.

Introduction to Entity Types in Kuwait

Kuwait is a sovereign state in the northern Arabian Gulf, bordered by Iraq to the north and Saudi Arabia to the south. As a member of the Gulf Cooperation Council (GCC), its commercial environment is shaped by both domestic legislation and regional economic frameworks. Company registration and corporate governance fall under the authority of the Ministry of Commerce and Industry (MOCI), which administers business formation under the Kuwait Companies Law No. 1 of 2016.

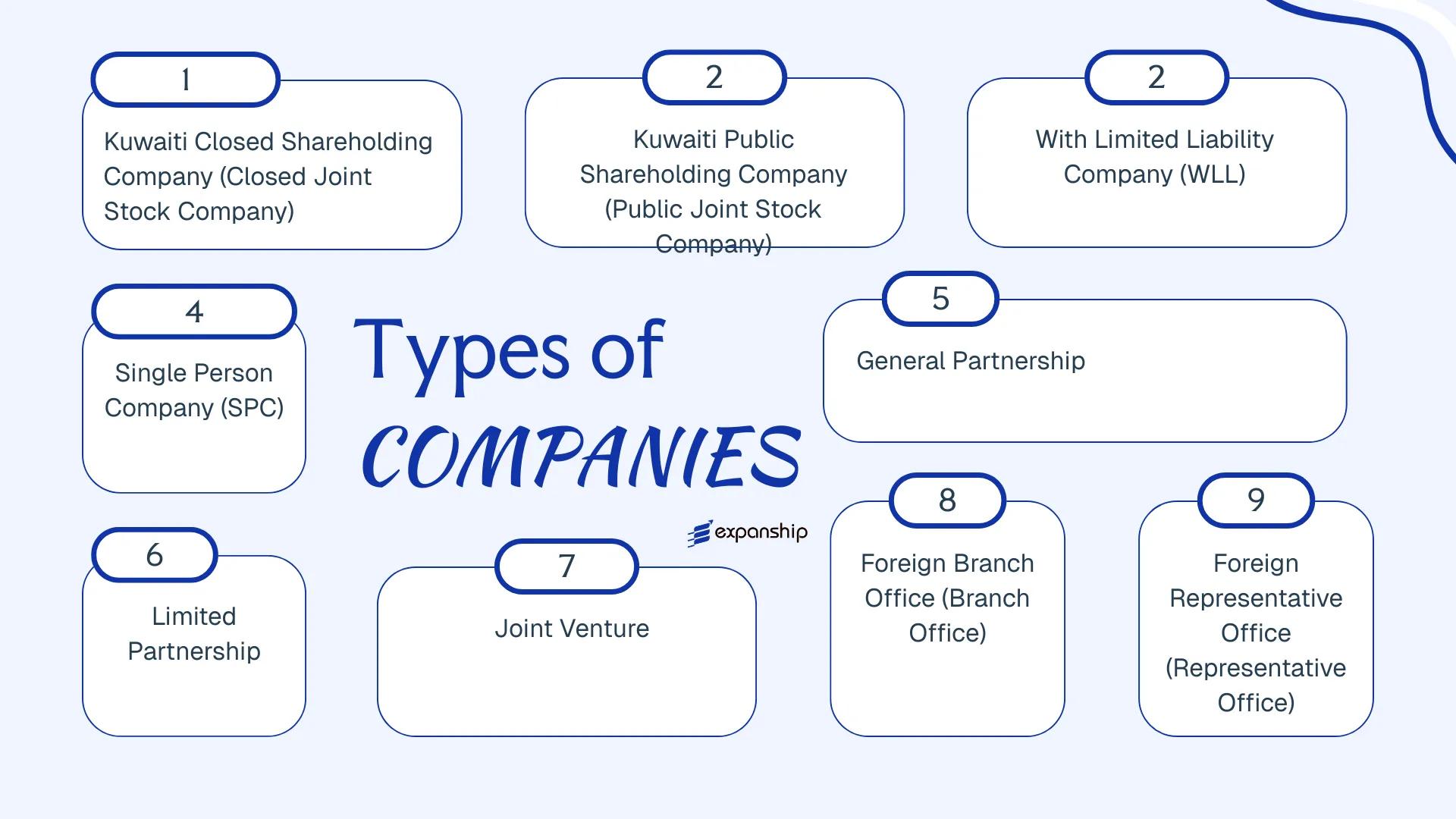

The types of business entities in Kuwait span several distinct legal forms, each governed by specific provisions within that law. Available structures include the Kuwaiti Shareholding Company (both closed and public joint stock), the With Limited Liability Company (WLL), the Single Person Company, the General Partnership, the Limited Partnership, the Joint Venture, the Branch Office, and the Representative Office.

Corporate tax in Kuwait applies primarily to foreign-owned entities, while Kuwaiti and GCC-owned businesses are generally exempt from income tax — though the precise rules depend on ownership structure. This article examines each entity type in detail, covering formation requirements, ownership restrictions, liability treatment, and applicable regulatory obligations.

An Overview of Business Structures in Kuwait

Kuwait's commercial framework provides several distinct entity types, each governed primarily by the Commercial Companies Law (Law No. 1 of 2016) and its amendments. The Ministry of Commerce and Industry (MOCI) serves as the principal regulatory authority overseeing company formation and ongoing compliance. Each structure carries different implications for ownership, liability, and permitted commercial activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Joint Stock Company (PJSC) | Corporate | Limited to shares | Taxed | Yes | 5 shareholders | MOCI / CMA | Law No. 1 of 2016 |

| Closed Joint Stock Company (CJSC) | Corporate | Limited to shares | Taxed | Yes | 2 shareholders | MOCI | Law No. 1 of 2016 |

| With Limited Liability Company (WLL) | Corporate | Limited to shares | Taxed | Yes | 2–50 partners | MOCI | Law No. 1 of 2016 |

| Single Person Company (SPC) | Corporate | Limited | Taxed | Yes | 1 shareholder | MOCI | Law No. 1 of 2016 |

| General Partnership | Unincorporated | Unlimited | Taxed | Yes | 2+ partners | MOCI | Law No. 1 of 2016 |

| Limited Partnership | Unincorporated | Mixed | Taxed | Yes | 2+ partners | MOCI | Law No. 1 of 2016 |

| Joint Venture | Contractual | Per agreement | Taxed | Restricted | 2+ parties | MOCI | Law No. 1 of 2016 |

| Branch Office | Foreign branch | Parent liable | Taxed | Yes | Parent company | MOCI | Foreign Capital Law |

| Representative Office | Non-trading | Parent liable | Exempt | No | Parent company | MOCI | Foreign Capital Law |

Each of these structures is examined in full in the sections below.

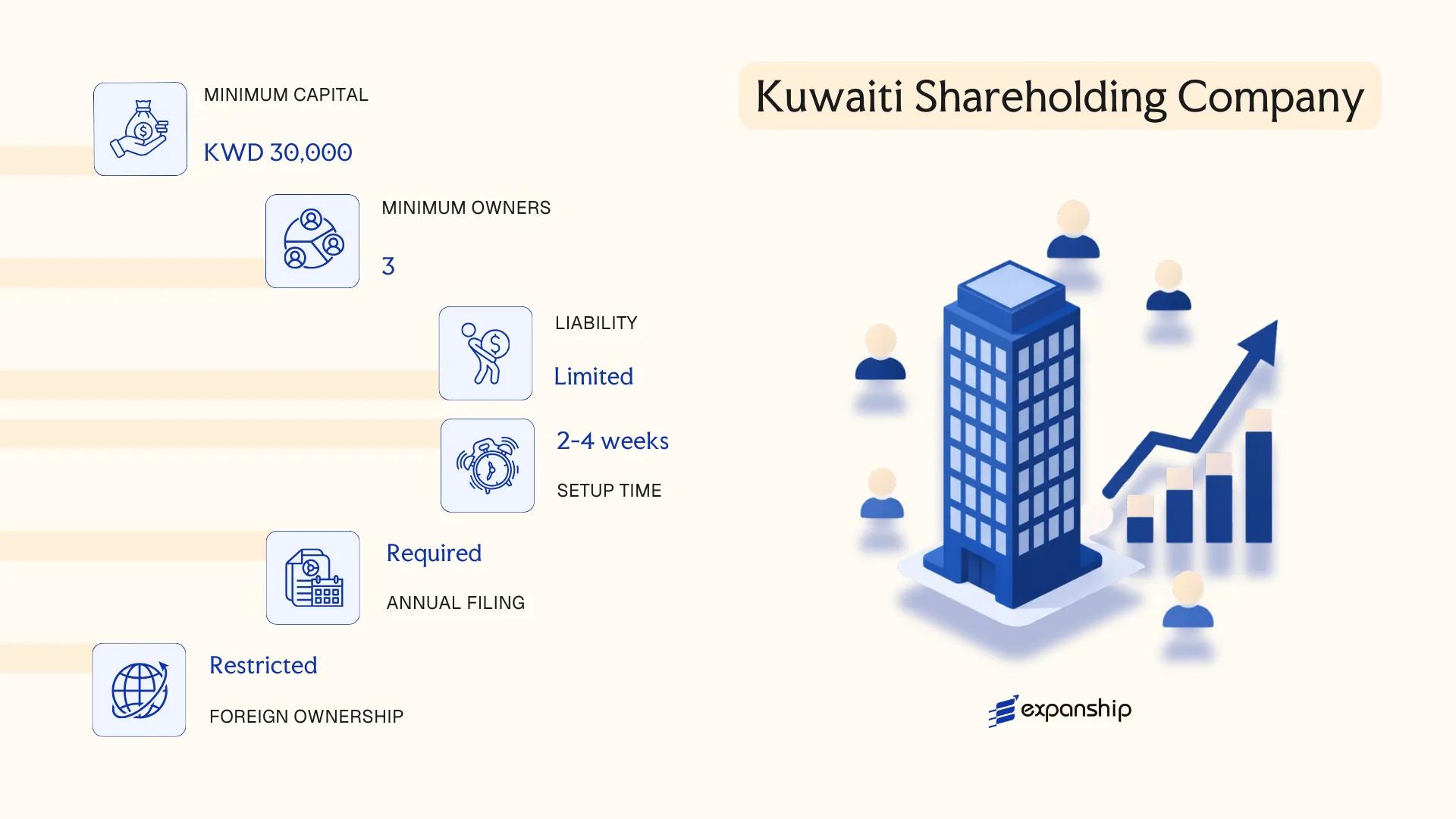

Kuwaiti Shareholding Company (Closed or Public Joint Stock Company)

Governed by the Companies Law No. 1 of 2016 and its subsequent amendments, the shareholding company is the primary vehicle for Kuwait joint stock company formation at scale. It carries separate legal personality, meaning the company's obligations are distinct from those of its shareholders, and liability is capped at the value of shares held.

Capital is divided into transferable shares of equal value. This structure suits enterprises requiring broad capital pools or those intending to eventually offer securities to the public.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Shareholding Company (KSC / KSCC) | KSC for public; KSCC for closed |

| Members | Shareholders | Closed: min. 5; Public: min. 5 founders |

| Share Capital | KWD 100,000 (closed); KWD 250,000 (public) | Must be fully subscribed at incorporation |

| Local Presence | Registered office in Kuwait required | No registered agent requirement per se |

| Kuwaiti Ownership | 51% Kuwaiti shareholding generally required | Exceptions apply in certain sectors under KDIPA |

| Privacy | Shareholder details filed with MOCI | Public companies subject to greater disclosure |

Focus Points

- Taxation: Subject to corporate income tax at 15% on foreign-owned profit shares; no VAT currently; no withholding tax on dividends; Zakat applies to Kuwaiti shareholders' portions.

- Annual Compliance: Audited financial statements required; public companies must file with the Capital Markets Authority (CMA) and publish financials.

- Economic Substance: No formal economic substance regime, but physical presence and operational activity are expected for licensed entities.

- Treaty Access: Kuwait maintains a network of double tax treaties; treaty benefits are generally accessible to resident corporate entities.

- Restrictions: Foreign ownership caps apply in most sectors; full foreign ownership is only available under specific KDIPA-approved investment arrangements.

Sub-Types

Kuwait Public Shareholding Company (KSC)

A KSC may offer shares to the public through the Boursa Kuwait exchange and is subject to CMA oversight, including prospectus requirements and ongoing disclosure obligations. This structure is used for large-scale commercial and financial enterprises seeking public capital.

Kuwait Closed Shareholding Company (KSCC)

A Kuwait closed shareholding company KSCC restricts share transfers and does not offer securities to the public, making it suited to family-held enterprises and joint ventures between institutional partners where ownership stability is a priority.

Recommendations

Shareholding companies are used primarily for large commercial operations, banking, insurance, and joint ventures with government-linked entities. The structure's capacity to raise capital through share issuance is a material advantage; however, the mandatory Kuwaiti majority ownership requirement and multi-layered regulatory oversight — particularly for public entities under CMA jurisdiction — represent meaningful operational constraints for foreign investors.

This structure is most appropriate for foreign investors entering Kuwait as part of a joint venture with a Kuwaiti partner, or for large-scale enterprises requiring substantial capital and a formal corporate governance framework.

Company Incorporation in Kuwait

Expanship assists with the formation of Kuwaiti shareholding companies, including KSCC and KSC structures, MOCI registration, and KDIPA coordination.

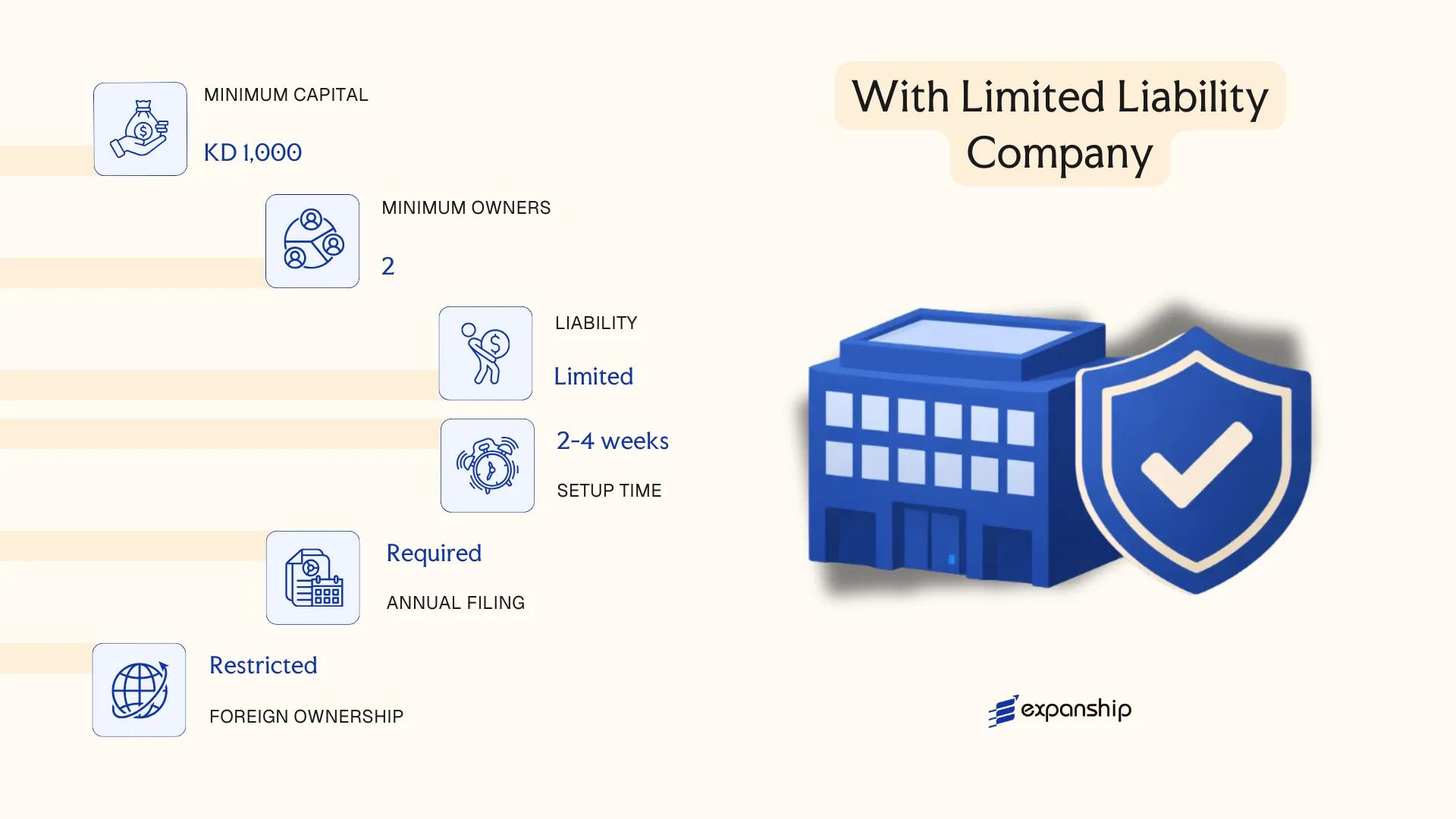

With Limited Liability Company (WLL)

The With Limited Liability Company is governed by Kuwait Commercial Companies Law No. 1 of 2016, as amended, which consolidates the regulatory framework administered by the Ministry of Commerce and Industry (MOCI). Kuwait WLL company registration produces a separate legal entity, meaning the company's obligations are distinct from those of its members, with liability capped at each member's capital contribution.

Structurally, the WLL sits between a simple partnership and a joint stock company — it offers limited liability without the public disclosure obligations attached to listed entities, making it a common choice for privately held commercial operations and joint ventures with foreign participation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | With Limited Liability Company (WLL) | Separate legal personality; governed by Law No. 1 of 2016 |

| Members | Referred to as partners; minimum 2, maximum 50 | At least 51% Kuwaiti ownership required in most sectors |

| Management | One or more managers (need not be members) | Managers appointed by the partners via the memorandum or a resolution |

| Local Presence | Registered office address in Kuwait required | Virtual offices are generally not accepted; physical address mandatory |

| Share Capital | Minimum KWD 1,000; no maximum | Capital divided into equal shares; shares are not publicly tradeable |

| Privacy | Memorandum filed with MOCI; not publicly listed | Beneficial ownership details held on register but not broadly publicised |

Focus Points

- Taxation: No corporate income tax on Kuwaiti-owned entities; foreign shareholding portions may be subject to the Kuwait Foreign Companies Tax (KFCT) at 15%; no VAT currently imposed in Kuwait; no withholding tax or stamp duty on share transfers under general rules.

- Annual Compliance: Audited financial statements must be submitted annually to MOCI; commercial registration must be renewed each year.

- Economic Substance: Kuwait does not currently impose a formal economic substance regime equivalent to those in certain Gulf free zones, but commercial activity must genuinely occur within the registered entity.

- Conversion: A WLL may be converted to a closed joint stock company subject to MOCI approval and fulfilment of the higher capital and governance thresholds.

- Restrictions: Foreign ownership is capped at 49% in most onshore sectors; certain regulated activities (banking, insurance, investment) require additional licences and may prohibit the WLL structure entirely.

Closing

The WLL suits trading, services, and light manufacturing operations where founders seek liability protection without the governance overhead of a shareholding company. Its primary constraint is the mandatory Kuwaiti majority ownership requirement, which limits operational control for foreign investors in most sectors.

Foreign businesses entering Kuwait through a local joint venture partner, and Kuwaiti-owned SMEs seeking a structured, limited-liability vehicle for commercial trading or service operations.

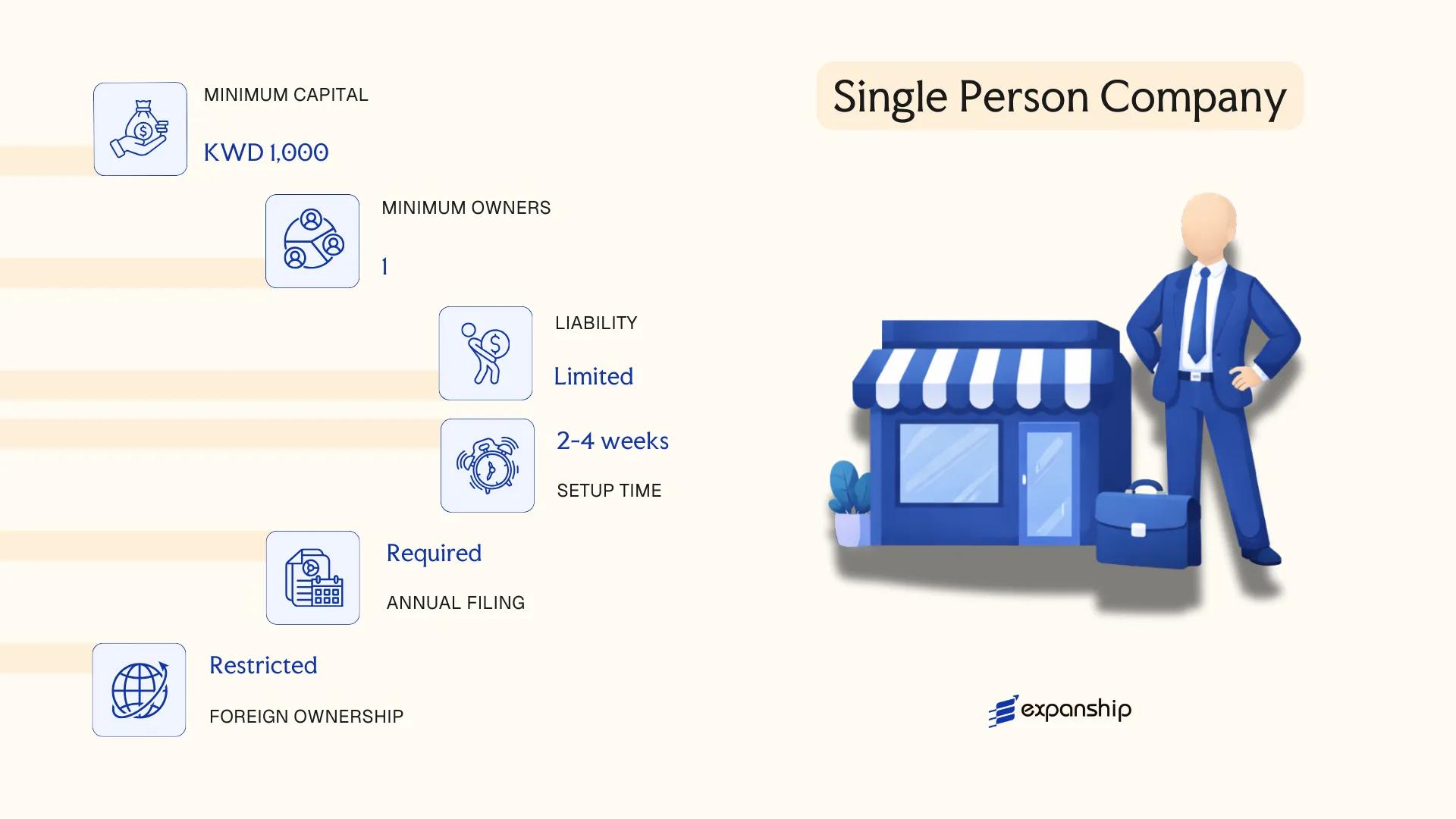

Single Person Company (SPC)

Introduced under Kuwait's Companies Law No. 1 of 2016, the Kuwait Single Person Company (SPC) is a distinct legal entity owned entirely by one individual or one corporate body. It carries separate legal personality, meaning the owner's personal assets are shielded from the company's liabilities.

Structurally, the SPC sits between a sole proprietorship and a limited liability company. Ownership and management can rest with the same person, yet the entity remains legally independent from its founder.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Single Person Company (SPC) | Governed by Companies Law No. 1 of 2016 |

| Member Title | Sole Owner / Manager | One individual or one corporate entity; owner typically acts as manager |

| Ownership | Minimum 1, Maximum 1 | Transfer of a share to a second party triggers mandatory conversion |

| Local Presence | Registered office address in Kuwait required | Must maintain a physical or registered address; no mandatory local agent |

| Capital | KWD 1,000 minimum (general guideline) | Fully paid at incorporation; denominated in Kuwaiti Dinar |

| Privacy | Owner details filed with Ministry of Commerce and Industry (MOCI) | Public registry; beneficial ownership disclosure required |

Focus Points

- Taxation: No corporate income tax applies to Kuwaiti-owned entities under current law; VAT has not been implemented; no withholding tax on dividends distributed to the sole owner; no stamp duty on share transfers in standard practice.

- Economic Substance: SPCs engaged in certain activities may fall under Kuwait's economic substance requirements; maintaining genuine operational presence is advisable.

- Annual Compliance: Annual financial statements must be filed with MOCI; an auditor appointment is required regardless of turnover.

- Conversion: If the owner wishes to add a second shareholder, the SPC must convert to a With Limited Liability Company (WLL) or another permitted multi-member structure under the Companies Law.

- Restrictions: Foreign individuals cannot hold 100% ownership through an SPC under standard foreign investment rules; a Kuwaiti national or entity must typically be involved unless operating within a designated free zone or under a specific investment licence.

Closing

The SPC suits a Kuwaiti national or eligible entity seeking full operational control without co-ownership obligations, commonly used for trading, consulting, or holding domestic assets. The single-owner structure eliminates shareholder disputes, though the mandatory conversion requirement upon any ownership change limits flexibility for businesses anticipating future investment.

The SPC is best suited for Kuwaiti nationals or eligible corporate bodies seeking sole ownership with limited liability for a single-operator business.

Partnerships in Kuwait [General Partnership, Limited Partnership, Joint Venture]

Partnership company registration in Kuwait is governed by the Commercial Companies Law, Law No. 1 of 2016 and its amendments. Partnership structures under this law vary in how liability is allocated among partners, and no single form automatically confers separate legal personality in the same manner as a corporate entity.

Depending on the chosen structure, partners may bear unlimited joint liability or a combination of limited and unlimited exposure based on their designated role.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (Civil or Commercial) | Separate legal personality is generally recognised under the Companies Law for registered commercial partnerships |

| Members | Partners (general or limited) | General Partnership: minimum 2, no statutory maximum; Limited Partnership: minimum 1 general + 1 limited partner |

| Local Presence | Registered address in Kuwait required | Must maintain a physical business address; no standalone registered agent regime |

| Capital | Kuwaiti Dinar (KWD); no statutory minimum for general partnerships | Limited partnership capital divided per partnership agreement |

| Liability | General partners: unlimited personal liability; Limited partners: capped at contributed capital | Mixed liability structures are a defining feature of limited partnerships |

| Privacy | Partner names disclosed in the commercial register | No confidentiality provisions for partnership ownership |

Focus Points

- Taxation: Partnerships involving foreign partners are subject to Kuwait's corporate income tax at 15% on the foreign partner's share of profits; Kuwaiti partners are generally exempt. VAT is not currently levied in Kuwait. No withholding tax or stamp duty applies in standard form.

- Economic Substance: Partnerships conducting relevant activities must satisfy substance requirements under the Kuwait Ministry of Commerce and Industry (MOCI) directives aligned with BEPS frameworks.

- Annual Compliance: Annual renewal of the commercial licence with MOCI is required; financial records must be maintained and may be subject to audit depending on the partnership's scale.

- Treaty Access: Access to Kuwait's double tax treaty network depends on the residency status and structure of the partners; treaty benefits are not automatically available to all partnership forms.

- Restrictions: Foreign ownership in a general partnership is restricted; foreign partners typically require a Kuwaiti national partner holding at least 51% unless operating under a licensed free zone or specific sector authorisation.

Sub-Types

General Partnership (Sharikat Tadamun)

All partners carry unlimited, joint, and several liability for the firm's obligations. This structure is generally used by Kuwaiti nationals for trading or professional businesses where the partners have an established trust relationship and direct operational control is preferred.

Limited Partnership (Sharikat Tawsiya Basita)

One or more general partners assume unlimited liability while limited partners' exposure is confined to their capital contribution. Limited partners cannot participate in management without risking reclassification as general partners under the Commercial Companies Law.

Joint Venture (Sharikat Muhasa)

A joint venture under Kuwaiti law is an unregistered, contractual arrangement with no separate legal personality and no public commercial register entry. It is commonly used for specific projects or time-bound collaborations between two or more parties, with the arrangement governed entirely by the joint venture agreement Kuwait parties execute privately.

Closing Remarks

Partnership structures in Kuwait are primarily used for professional services, trading operations, and project-specific collaborations between parties with defined roles. The absence of limited liability for general partners is a material constraint, particularly for foreign investors who may face exposure beyond their invested capital.

Kuwait partnership structures are most appropriate for Kuwaiti-led businesses or project-specific ventures where the partners have clearly delineated roles and the foreign party's involvement is contractually managed rather than operationally direct.

Foreign Business Presence in Kuwait [Branch Office, Representative Office]

Foreign firms seeking to operate in Kuwait without establishing a locally incorporated entity can do so through two principal structures: a branch office or a representative office. Registration of a foreign company branch office Kuwait falls under the Companies Law (Law No. 1 of 2016) and is processed through the Ministry of Commerce and Industry (MOCI).

A branch office carries no separate legal personality — it is an extension of the parent company, which retains full liability for the branch's obligations. A representative office, by contrast, is restricted to promotional and liaison activities; it cannot generate revenue or execute commercial contracts within the country.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None (extension of parent) | None (extension of parent) |

| Commercial Activity | Permitted | Not permitted |

| Revenue Generation | Allowed | Not allowed |

| Local Agent | Kuwaiti commercial agent required under agency law | Kuwaiti sponsor may be required |

| Registered Address | Physical office in Kuwait mandatory | Physical office required |

| Capital Requirement | No statutory minimum, but proof of parent financials required | None |

Focus Points

- Taxation: Branch profits are subject to the 15% corporate income tax applicable to foreign entities; no VAT is currently imposed in Kuwait; no withholding tax on remitted profits, though this may be reviewed under ongoing GCC tax harmonisation discussions.

- Economic Substance: No formal economic substance regime is currently mandated for branch structures, but physical presence and local staffing are implicit requirements for MOCI licensing.

- Annual Compliance: Branches must file audited financial statements with MOCI annually and renew their commercial registration each year.

- Treaty Access: The parent company's tax treaty entitlements may extend to the branch, depending on treaty language; independent legal advice should confirm applicability per specific treaty.

- Restrictions: Representative offices cannot hire local staff for revenue-generating roles or sign commercial contracts; branches in certain sectors require additional ministry approvals beyond MOCI.

Sub-Types

Branch Office

Operates under MOCI registration and can conduct the same commercial activities as the parent entity, subject to sector-specific licensing. Commonly used by contractors, consultancies, and service firms executing specific projects.

Representative Office

Permitted solely for market research, brand promotion, and liaison functions. No contracts may be concluded on behalf of the parent from within Kuwait, making this a limited-duration, low-footprint option.

When to Consider This Structure

Both structures suit foreign businesses testing the market or fulfilling specific project mandates without committing to full local incorporation. The branch offers operational capacity but exposes the parent to unlimited liability; the representative office limits exposure but also limits activity entirely.

A branch office suits established foreign firms with confirmed Kuwaiti project awards or clients; a representative office is appropriate only for preliminary market presence where no direct revenue is anticipated.

How to Choose the Right Entity Type in Kuwait

Choosing the right company structure in Kuwait is not a formality — the structure you register determines your legal obligations, liability exposure, and operational permissions from day one.

Why Your Entity Choice Matters

Selecting the wrong business entity type in Kuwait carries concrete legal and financial consequences:

- A foreign branch registered without MOCI approval to conduct local commercial activity operates in violation of Kuwait Commercial Companies Law No. 1 of 2016, exposing the firm to administrative penalties or forced closure.

- Forming a With Limited Liability Company when the intended activity requires a Kuwaiti Shareholding Company structure — such as banking or insurance — results in the activity licence being denied outright.

- Registering a Representative Office and then conducting revenue-generating transactions breaches the permitted scope of that structure, creating undisclosed permanent establishment exposure.

- Choosing an entity without audited financial reporting obligations when a regulated activity requires them places the business in non-compliance with the Capital Markets Authority or sector-specific regulator.

Key Factors to Consider

- Business Activity: Regulated sectors such as banking, insurance, and securities require a Kuwaiti Public Shareholding Company, while trading and services typically suit a WLL.

- Ownership Structure: A Single Person Company suits sole proprietors, whereas multi-party ventures require a WLL or partnership depending on liability preferences.

- Foreign Ownership: If full foreign ownership is required, the activity must fall within sectors permitted under the Direct Foreign Capital Investment Law.

- Substance Capacity: If your business cannot maintain a physical office and locally based management, a Representative Office may be more appropriate than a Branch.

- Exit Strategy: Consider whether the structure permits redomiciliation or conversion, as Kuwaiti law imposes specific procedures for dissolution and liquidation under the Companies Law.

- Tax Position: Kuwait imposes corporate tax on foreign-owned entities; your structure determines whether profits are subject to the 15% rate under the Income Tax Decree.

Corporate Compliance Services in Kuwait

Maintain your entity's good standing with ongoing compliance support covering annual filings, regulatory reporting, and licence renewals in Kuwait.

Conclusion

Selecting the right structure is a foundational decision in any Kuwait company incorporation summary exercise, and each entity type serves a distinct function. The With Limited Liability Company (WLL) remains the most commonly registered structure, particularly among foreign investors entering through the required Kuwaiti partner arrangement. Closed Joint Stock Companies suit capital-intensive ventures, while the Single Person Company offers sole proprietors a vehicle with limited liability. General and limited partnerships carry full personal exposure and fit closely held, professionally operated businesses. Branch offices and representative offices serve foreign firms with specific, bounded operational mandates.

Regulatory oversight from the Ministry of Commerce and Industry, alongside the Foreign Direct Investment Law No. 116 of 2013, continues to shape the conditions under which foreign capital enters the market. Ongoing updates to investment regulations signal a gradual broadening of allowable foreign ownership in select sectors.

How Expanship Can Assist You

Expanship's Kuwait company formation services cover every stage of the process, from selecting between a With Limited Liability Company (WLL), a Single Person Company (SPC), or a Kuwaiti Shareholding Company, through to filing with the Ministry of Commerce and Industry (MOCI) and obtaining the necessary commercial licenses. Each entity type carries distinct ownership, capital, and activity restrictions — and we work with you to match the right structure to your specific business model.

Our team handles the full scope of corporate setup and ongoing maintenance:

- Document preparation, attestation, and legalization

- Registered agent and registered office provision

- Government filing and MOCI liaison

- Post-incorporation compliance management

- Banking introduction assistance

Reach out to Expanship Kuwait to discuss your incorporation requirements directly with our corporate services team.

Frequently Asked Questions (FAQ)

The With Limited Liability Company (WLL) is the most frequently formed structure for commercial operations. Its combination of capped liability, a relatively straightforward incorporation process, and suitability for small-to-medium foreign joint ventures makes it the default choice for most investors entering the market.

A Branch Office cannot hold equity independently and must be wholly owned by its parent foreign company, while a WLL is a locally incorporated legal entity with its own rights and obligations. For tax treatment, both are subject to Kuwait's corporate income tax on the portion of profits attributable to foreign ownership, but the WLL provides greater operational flexibility and the ability to enter government contracts under certain conditions.

The Single Person Company (SPC) discloses minimal information publicly, though registered details are filed with MOCI. Nominee arrangements are not a formally recognized mechanism under Kuwaiti corporate law, so ownership transparency remains a regulatory requirement across all entity types.

No. A General Partnership requires at least two partners, and a WLL requires a minimum of two shareholders. Only the SPC is structured for sole ownership, as its name reflects under Law No. 1 of 2016.

Foreigners can participate in a WLL, a Kuwaiti Shareholding Company (subject to foreign ownership caps in certain sectors), or establish a Branch or Representative Office under the Foreign Capital Investment Law (Law No. 116 of 2013). Direct ownership of a General Partnership or Limited Partnership by a non-Kuwaiti national is subject to restrictions, and sector-specific approvals may apply regardless of entity type.

Conversion is permitted in principle under the Companies Law, with the most common pathway being a WLL converting to a Kuwaiti Shareholding Company as the business scales. The process requires MOCI approval, updated articles of association, and compliance with the capital requirements applicable to the target structure.

The WLL, SPC, and both forms of Kuwaiti Shareholding Company hold separate legal personality distinct from their shareholders. A Joint Venture, by contrast, does not constitute an independent legal entity and exists contractually between its parties without independent registration.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.