Key Takeaways

- Foreign investors operating in Kuwait under the Companies Law face mandatory Kuwaiti national partnership requirements that structurally limit full ownership and operational control from the outset.

- Sector-specific licensing restrictions and the government's multi-stage approval process through the Ministry of Commerce and Industry extend the timeline before a foreign entity can legally begin commercial operations.

- Companies with foreign involvement must satisfy Kuwaitization workforce quotas, creating an ongoing staffing compliance burden that restricts hiring flexibility regardless of operational need.

- Zakat obligations and the National Labour Support Tax add recurring fiscal costs beyond standard corporate taxation, increasing the effective financial load on foreign-linked entities operating in Kuwait.

Kuwait operates under a heavily regulated corporate framework, shaped by the Companies Law and overseen by the Ministry of Commerce and Industry. The disadvantages of incorporating in Kuwait span ownership restrictions, workforce obligations, licensing constraints, and capital controls — each addressed in the sections that follow.

Not every foreign investor will encounter these challenges equally. The extent to which they apply depends on your business structure, the sector you intend to operate in, and whether your entity involves Kuwaiti partners.

This article is most relevant to foreign entrepreneurs and multinational firms seeking direct operational presence in Kuwait, particularly those unfamiliar with Gulf Cooperation Council regulatory norms. The drawbacks of Kuwait company formation tend to surface most sharply during the setup phase and early operational period, when compliance obligations are at their most concentrated.

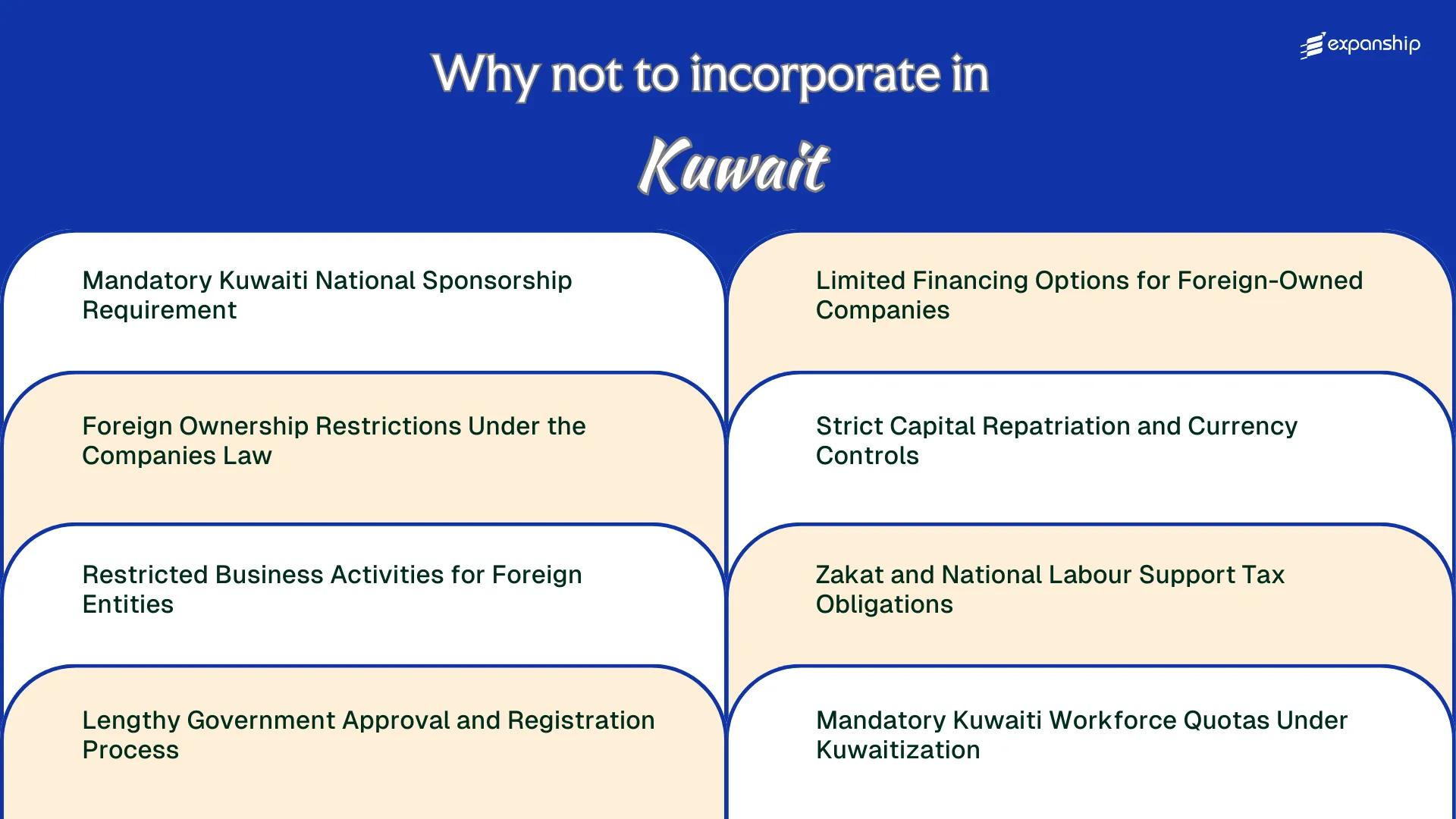

Mandatory Kuwaiti National Sponsorship Requirement

Kuwait national sponsorship restrictions remain one of the most structurally limiting aspects of establishing a foreign business presence in the country.

The Kafala Framework and Its Ownership Implications

Under the kafala system, most foreign-owned commercial entities require a Kuwaiti national sponsor holding at least 51% of the company's shares. This majority stake requirement, embedded in the Commercial Companies Law No. 1 of 2016, means your business is legally controlled by a party whose interests may not align with yours.

The Kuwaiti sponsor requirement for foreign business is not merely administrative. Profit distribution, decision-making authority, and exit terms all become subject to the sponsor's consent, which exposes your firm to operational and financial dependency from the outset.

Structural Dependency as an Ongoing Liability

Even when the Kuwaiti partner plays a passive role, their legal ownership position grants them standing in any dispute before the Ministry of Commerce and Industry. Negotiating a side agreement to retain operational control is common practice, but such arrangements carry their own enforceability risks under Kuwaiti contract law.

A Kuwaiti national holding 51% of your company's shares retains the legal authority to block critical decisions, transfer shares, or challenge your operational control through Kuwaiti courts, regardless of any private arrangement you hold.

Foreign Ownership Restrictions Under the Companies Law

Foreign ownership restrictions in Kuwait are codified under Law No. 1 of 2016 (the Companies Law) and its executive regulations, which cap non-Kuwaiti equity participation at 49% in most onshore commercial structures. That ceiling means your business cannot hold a controlling stake in a standard Kuwaiti entity, regardless of capital contribution or operational control.

The 51% Kuwaiti shareholding requirement is not merely procedural. It transfers ultimate legal authority over the company to local partners, including decisions on profit distribution, asset disposal, and governance structure.

Certain sectors permit 100% foreign ownership through the Kuwait Direct Investment Promotion Authority (KDIPA), but qualifying conditions are restrictive and approval is discretionary. That carve-out is narrow enough that most foreign businesses do not qualify.

In practical terms, the Kuwait foreign shareholding limitations create friction across multiple operational areas:

- Minority equity status limits your ability to block resolutions that affect dividend policy or exit terms

- Dispute resolution defaults to Kuwaiti courts, where the majority local shareholder holds structural advantage

- Renegotiating shareholder agreements requires partner consent, removing unilateral restructuring options

- Selling or transferring your equity stake depends on local partner approval under most articles of association

Company Incorporation in Kuwait

Understand the legal structures available to foreign investors and what equity participation rules apply to your specific business activity.

Restricted Business Activities for Foreign Entities

Certain sectors in Kuwait are entirely off-limits to foreign participation, and others impose conditions that make meaningful foreign control functionally impossible. Under Kuwait's Companies Law No. 1 of 2016 and its predecessors, restricted business activities for Kuwait foreigners cover a wide range of industries central to the economy.

Sectors tied to natural resources, primary retail trade, and government contracting are among those where foreign entities face categorical exclusion or severe participation caps. Your business cannot hold a general commercial trading licence in Kuwait without a Kuwaiti partner holding the majority stake, which structurally limits the operational scope of any foreign-owned entity.

| Sector | Restriction Type | Practical Impact |

|---|---|---|

| Oil and gas upstream operations | Closed to private foreign ownership | No direct equity participation permitted |

| General retail and trading | Majority Kuwaiti ownership required | Foreign firm cannot independently trade |

| Real estate ownership | Largely restricted to GCC and Kuwaiti nationals | Foreign companies cannot hold land title |

| Import agencies | Reserved for Kuwaiti nationals | Foreign entities cannot act as registered agents |

| Government services contracting | Preference rules heavily favour local firms | Foreign firms structurally disadvantaged in bids |

Prohibited sectors for foreign companies in Kuwait extend into areas like manpower supply and select professional services, where licensing is contingent on Kuwaiti national ownership. Even where foreign participation is technically permitted, Kuwait foreign entity activity limitations under the Commercial Companies Law mean that strategic decisions remain outside your control.

The Foreign Direct Investment Law No. 116 of 2013, administered by the Kuwait Direct Investment Promotion Authority (KDIPA), does allow exceptions in designated sectors, but these apply narrowly and are subject to case-by-case ministerial discretion.

Lengthy Government Approval and Registration Process

The Kuwait company registration process delays are among the most operationally disruptive aspects of setting up a foreign business here. Unlike single-window registration systems common in Singapore or the UAE's free zones, Kuwait's incorporation process involves sequential approvals across multiple government bodies, each with its own processing timeline.

The Ministry of Commerce and Industry (MOCI) oversees the primary registration of commercial entities, but approval rarely stops there. Depending on your business activity, you may require clearances from the Ministry of Interior, the Capital Markets Authority, or sector-specific regulators before the entity is legally operational.

Each approval stage is handled independently. A delay at one ministry does not pause the clock elsewhere, meaning coordinating submissions across agencies becomes its own administrative burden.

- MOCI approval is required before any commercial registration is finalized

- Sector-specific ministries may impose additional licensing rounds beyond MOCI clearance

- Government offices observe Friday-Saturday weekends and extended public holiday closures

- All documentation submitted to Kuwaiti authorities must be officially translated into Arabic and authenticated

Total incorporation timelines can stretch from several weeks to several months, depending on activity type and document completeness. This directly delays when your business can legally generate revenue or sign contracts in Kuwait.

Kuwait does not currently offer an expedited or premium-fee fast-track registration pathway for foreign investors, meaning no amount of additional payment can formally shorten the government approval queue.

Limited Financing Options for Foreign-Owned Companies

Financing challenges foreign companies face in Kuwait stem largely from how local banks assess creditworthiness for entities with significant foreign ownership.

Structural Barriers in the Local Credit Market

Kuwaiti commercial banks typically require established local credit histories, collateral held within the country, and demonstrated ties to the domestic economy before extending lending facilities to a business. Foreign-owned firms, particularly those structured under the Foreign Direct Investment Law No. 116 of 2013, rarely satisfy these criteria in their early operating years, making access to working capital and growth financing materially difficult.

Practical Consequences for Foreign Investors

Limited bank lending to foreign-owned Kuwait firms means you are largely dependent on equity contributions or intracompany loans from your parent entity abroad to fund operations. This concentration of funding sources increases financial exposure and eliminates the leverage that locally incorporated Kuwaiti firms routinely access through established banking relationships. Firms operating in sectors requiring significant upfront capital investment feel this constraint most acutely, as Kuwait credit access restrictions for foreign businesses leave few institutional alternatives to conventional bank lending.

Addressing Financing and Incorporation Challenges in Kuwait

Understand the structural financing constraints affecting foreign-owned entities in Kuwait and how to approach your incorporation with realistic capital planning in place.

Strict Capital Repatriation and Currency Controls

Kuwait capital repatriation restrictions are relatively permissive on paper, but the structural and regulatory conditions surrounding profit remittance create real friction for foreign investors operating through locally incorporated entities.

- Under the Foreign Capital Investment Law No. 8 of 2001, foreign investors are technically permitted to repatriate profits, but this right is contingent on full compliance with tax clearance requirements from the Ministry of Finance, creating a procedural dependency that delays access to your own funds.

- All foreign exchange transactions must be conducted through licensed banks regulated by the Central Bank of Kuwait, which means your firm has no flexibility to use alternative financial channels even for routine cross-border transfers.

- Any outstanding Zakat, National Labour Support Tax, or corporate tax liability will block the issuance of a tax clearance certificate, effectively freezing profit remittance until all obligations are resolved.

- Currency exchange in Kuwait is conducted in Kuwaiti Dinar, one of the highest-valued currencies globally, meaning conversion costs on repatriated profits can be materially significant depending on your home currency.

Zakat and National Labour Support Tax Obligations

Kuwait Zakat tax obligations for companies are governed by Law No. 46 of 2006, which imposes a 1% Zakat levy on the net profits of Kuwaiti-listed and certain other entities. The National Labour Support Tax (NLST), established under Law No. 19 of 2000, adds a further 2.5% charge on net profits of Kuwaiti public and closed shareholding companies.

For foreign-owned entities operating through a Kuwaiti structure with local shareholders, both obligations can apply at the shareholder or entity level depending on the corporate form chosen. This creates a cumulative tax burden that is not always apparent at the incorporation stage.

The NLST is specifically directed at supporting Kuwaiti national employment and is administered through the Ministry of Finance. Your entity's profit calculations must account for both charges separately, requiring distinct compliance filings rather than a single consolidated return.

A foreign investor holding 49% in a Kuwaiti closed shareholding company reporting KWD 500,000 in net profit faces an NLST charge of KWD 12,500 and a Zakat liability of KWD 5,000 applied at the entity level before any dividend distribution — reducing effective returns before repatriation costs are considered.

Mandatory Kuwaiti Workforce Quotas Under Kuwaitization

Kuwaitization workforce quota restrictions require private sector employers to maintain a minimum percentage of Kuwaiti nationals on their payroll, enforced through the Ministry of Human Resources and Labour Manpower. The exact ratio varies by sector, meaning your compliance burden is not uniform across different business activities.

Sourcing qualified Kuwaiti nationals who meet specific technical or operational requirements can be difficult, particularly in industries where the local talent pool is limited. You may end up carrying salaried Kuwaiti employees in roles that don't generate proportionate output, which directly inflates your payroll costs.

Non-compliance carries real consequences, including fines and restrictions on obtaining or renewing work permits for your expatriate staff. Since most operational roles in Kuwait are filled by foreign nationals, losing work permit access can functionally halt day-to-day business.

The Kuwaitization ratio also affects your ability to scale. Each new expatriate hire may require a corresponding Kuwaiti hire to maintain the mandated balance, making rapid headcount expansion structurally expensive.

Certain free zone entities or specific licensed activities may face different quota thresholds, but the general private sector obligation still applies to the majority of foreign-owned firms operating outside those structures.

If your business cannot demonstrate active Kuwaiti national employment at the required ratio, the Ministry of Human Resources and Labour Manpower can block the issuance or renewal of expatriate work permits, which may render your operations non-functional regardless of your entity's legal standing.

How to Navigate These Incorporation Challenges

Navigating Kuwait incorporation challenges requires structural decisions made before registration, not adjustments after the fact. The Foreign Capital Investment Law No. 8 of 2001 and the Companies Law No. 1 of 2016 together define the boundaries within which foreign entities must operate.

- Identify whether your business activity qualifies for the KDIPA exemption list, which permits up to 100% foreign ownership in approved sectors under Law No. 116 of 2013.

- Appoint a Kuwaiti national sponsor who holds at least 51% equity, structuring the sponsorship agreement to protect operational control through a side agreement.

- Register under the Ministry of Commerce and Industry's procedures and confirm activity licensing aligns with permitted foreign business categories.

- Build Kuwaitization quota targets into your staffing plan from the outset, using the ratio applicable to your sector under the Public Authority for Manpower framework.

- Establish a currency repatriation mechanism through a licensed local bank before profit distribution begins.

These steps address the principal structural barriers, but each remains subject to ministerial discretion and evolving regulatory interpretation.

Kuwait's Overall Business Appeal Despite the Drawbacks

Despite the restrictions and administrative burdens covered throughout this blog, the Kuwait business environment risks and benefits calculation is not uniformly negative. The Gulf state holds strategic relevance as a high-income oil economy with a substantial sovereign wealth base and proximity to GCC consumer markets. For businesses that can meet the structural requirements, the jurisdiction remains a credible operating base.

| Pros | Cons |

|---|---|

| No corporate income tax on most foreign companies operating under the Foreign Direct Investment Law | Mandatory Kuwaiti national sponsorship is required for most commercial structures |

| Access to a high-income consumer market with strong purchasing power | Foreign ownership is capped at 49% under the Companies Law in most sectors |

| GCC geographic positioning supports regional distribution and logistics | Government registration and approval processes involve multiple agencies with extended timelines |

| Zakat and National Labour Support Tax obligations are fixed and calculable in advance | Kuwaitization quotas require hiring a defined proportion of Kuwaiti nationals across most business activities |

| Kuwait Dinar is one of the highest-valued currencies globally | Financing access for foreign-owned entities through local banks is limited without established local relationships |

Capital repatriation regulations add a further layer of operational complexity that foreign firms must account for before committing to incorporation.

Compliance Services for Companies in Kuwait

Maintain your Kuwait entity's standing with accurate filings, Zakat obligations, Kuwaitization reporting, and regulatory submissions handled in full.

Conclusion

The cons of Kuwait company formation are concentrated in structural areas that directly affect how a foreign-owned business operates day to day. Mandatory national sponsorship, foreign equity caps under the Companies Law, and Kuwaitization quotas enforced by the Public Authority for Manpower collectively create a compliance burden that requires sustained local expertise to manage. Structural constraints of this nature do not disappear with experience; they require ongoing attention. For your business, understanding which requirements apply before incorporation determines whether the jurisdiction is workable at all.

Expanship's Kuwait Incorporation Support

Incorporating in Kuwait places specific demands on foreign businesses, from satisfying Ministry of Commerce and Industry registration requirements to managing Kuwaitization quotas and Zakat obligations. Expanship's Kuwait incorporation support is structured around these particular compliance layers, helping your firm handle the administrative and regulatory burden without disrupting your core operations.

Our team works across the full scope of Kuwait company formation, from initial setup through ongoing compliance.

- Your company registration and all supporting documentation are prepared and submitted in the correct format for Kuwaiti authorities.

- A registered agent and local office address are provided to meet residency requirements.

- Government filings and liaison with the Ministry of Commerce and Industry are handled on your behalf.

- Post-incorporation compliance obligations, including renewals and statutory filings, are managed on an ongoing basis.

- Banking introductions are facilitated to support your entity's operational setup in Kuwait.

- Tax registration and coordination with the Kuwait Tax Authority are managed as part of your broader compliance picture.

Reach out to Expanship Kuwait to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

It applies broadly to onshore entities but the specific form it takes varies by structure. A foreign company establishing a branch or a with-limited-liability company will typically require a Kuwaiti national sponsor or agent under the Commercial Agencies Law No. 36 of 1964, which grants the local agent considerable legal standing. This dependency creates real exposure if the relationship deteriorates, since terminating a commercial agency arrangement in Kuwait can trigger compensation obligations.

Non-compliant firms face restrictions on renewing work permits and obtaining new visas through the Public Authority for Manpower. In practice, your ability to hire additional expatriate staff is directly tied to meeting the Kuwaitization ratio set for your sector, so falling short blocks workforce expansion rather than triggering a simple fine. Persistent non-compliance can also affect your business's good standing with other government authorities during licence renewals.

Kuwait's registration timeline is widely regarded as longer than Bahrain and the UAE, where single-window digital systems have compressed incorporation to days or weeks. In Kuwait, approval typically involves multiple ministries, the Ministry of Commerce and Industry, and in some cases the Foreign Capital Investment Bureau, with no guaranteed processing timeline. The sequential nature of these approvals means delays at one stage cascade through the entire process.

Zakat is levied at 1% of net profits on Kuwaiti-listed companies, while the National Labour Support Tax is set at 2.5% of net profit for companies listed on the Kuwait Stock Exchange. For unlisted foreign-owned entities, the direct applicability of these levies varies, but businesses operating through Kuwaiti-majority structures may still carry indirect exposure through their local partner's obligations. These costs sit on top of the standard 15% corporate income tax applicable to foreign company profits under the Income Tax Decree No. 3 of 1955.

The Kuwaiti Silk City and Shuwaikh free zones offer modified ownership terms, but these zones remain limited in scope and the range of permitted activities is narrower than onshore incorporation. Free zone entities face restrictions on conducting business directly within the Kuwaiti domestic market without a separate licensed presence. This means a free zone structure solves the ownership problem only if your commercial activity is confined to what those zones explicitly permit.

Transferring funds out of Kuwait without proper documentation through the Central Bank of Kuwait's framework can trigger scrutiny and delays on future transactions. Foreign investors are required to register their inward capital with the Foreign Capital Investment Bureau to secure the legal right to repatriate profits and principal, and failing to do this at the outset is difficult to remedy retroactively. The consequence is not always an immediate penalty but a practical freeze on your ability to move money out of the jurisdiction cleanly.

The restricted list is substantial. Sectors including retail trade, real estate brokerage, and several professional services categories are either fully closed to foreign ownership or require specific ministerial approval under the Negative List maintained by the Foreign Capital Investment Bureau. Foreign firms targeting consumer-facing or locally sensitive industries will find far fewer entry points than in comparable Gulf Cooperation Council markets.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.