Key Takeaways

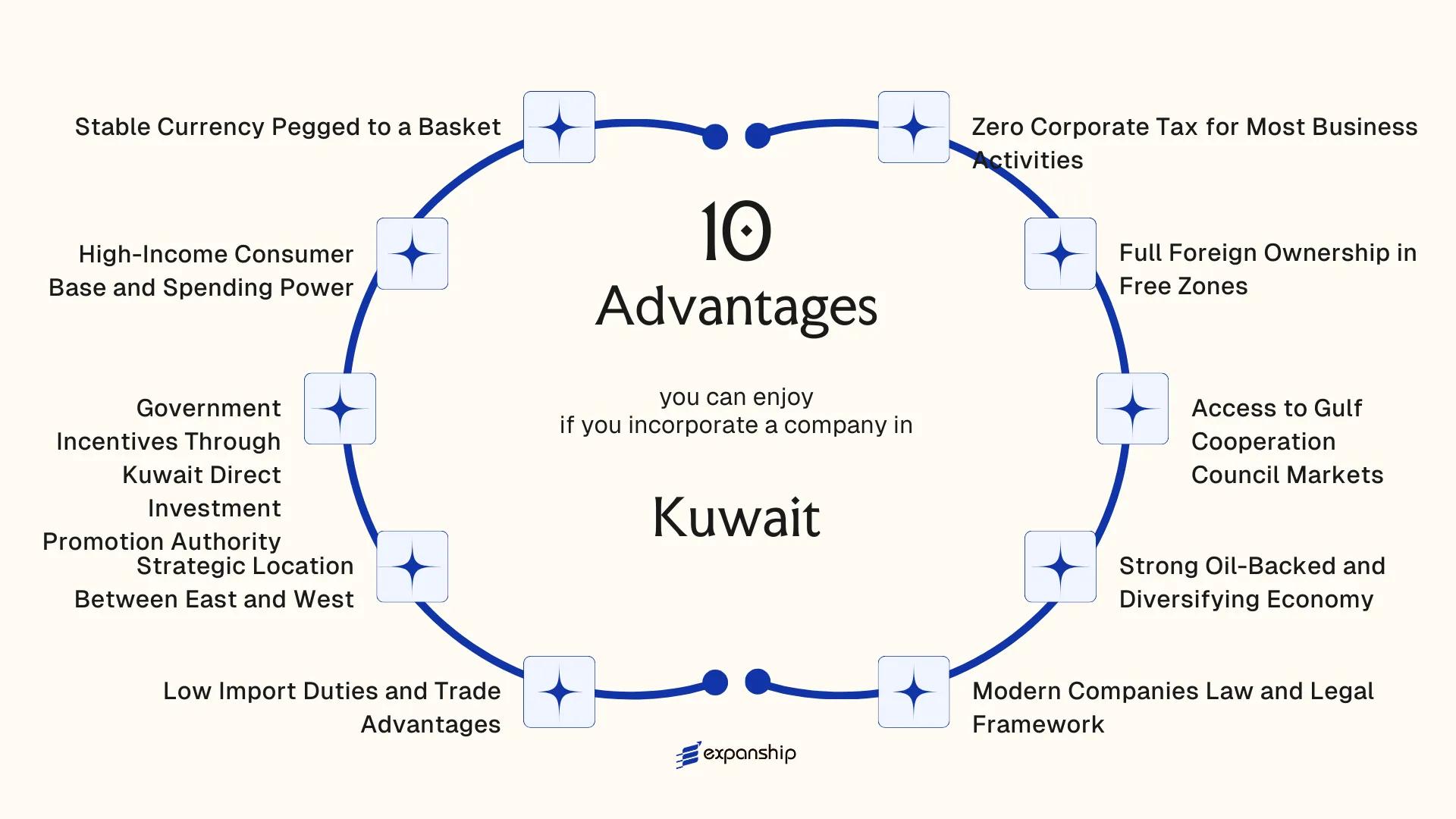

- Kuwait's zero corporate tax posture on most commercial activities means foreign-owned entities can structure profit repatriation without the burden of domestic income tax eroding returns from day one.

- Companies incorporated in Kuwait's free zones benefit from full foreign ownership, removing the local equity partner requirement that has historically complicated Gulf market entry for international investors.

- As a founding member of the Gulf Cooperation Council, a single Kuwait-registered entity can access the combined markets of all six GCC member states under preferential trade terms, reducing the structural cost of regional expansion.

- The Kuwait Direct Investment Promotion Authority serves as the designated regulatory body administering foreign direct investment policy, meaning investors have a defined institutional pathway for navigating sector-specific ownership restrictions and licensing requirements.

Situated at the northern tip of the Arabian Gulf, Kuwait is a sovereign state and a founding member of the Gulf Cooperation Council. For businesses evaluating the benefits of incorporating in Kuwait, the starting point is understanding how the country's regulatory environment is structured. Company registration falls under the purview of the Ministry of Commerce and Industry, which oversees commercial licensing and the formation of legal entities operating within the country. Foreign businesses entering the market most commonly do so through a With Limited Liability company.

Kuwait operates a largely zero-tax posture for many categories of commercial activity, making it a fiscally attractive destination for foreign capital. The government has taken deliberate steps to open its economy to international investors, with foreign direct investment policy administered through the Kuwait Direct Investment Promotion Authority.

Openness to foreign participation varies depending on the sector and the structure chosen, with free zones offering considerably more flexibility than onshore arrangements. This article examines the principal advantages that company formation here presents to international businesses.

Zero Corporate Tax for Most Business Activities

Kuwait zero corporate tax for businesses is not a temporary incentive or a free zone carve-out. It is the default position under Kuwaiti tax law for entities wholly owned by nationals of GCC member states.

How the Tax Structure Works

Under Decree Law No. 3 of 1955, as amended, corporate income tax applies only to foreign-owned entities, defined as companies with non-Kuwaiti (and non-GCC) shareholding. A business structured entirely under GCC ownership falls outside the scope of corporate tax. This means your operating profits are not subject to any corporate income tax at the entity level.

What This Means for Foreign Investors

Foreign investors operating through a locally incorporated entity with Kuwaiti partners, or structuring through a GCC-national holding arrangement, can access the same tax-free environment. Retained earnings are not taxed within the entity, which directly improves capital efficiency. The Zakat obligation applies to Kuwaiti shareholders separately and does not function as a corporate income tax on the company itself.

Profits generated by a qualifying Kuwaiti entity are not reduced by corporate income tax, leaving more capital available for reinvestment or distribution.

Full Foreign Ownership in Free Zones

Foreign companies operating within Kuwait's designated free zones can hold 100 percent ownership of their entities without requiring a local Kuwaiti partner. Outside these zones, the Commercial Companies Law generally restricts foreign equity to 49 percent, making the free zone structure a materially different arrangement for international investors who want full operational and financial control.

The Boubyan Island Special Economic Zone is the most prominent example, positioned to function as a logistics and industrial hub at the northern end of the Arabian Gulf. For businesses where ownership structure directly affects profit repatriation, decision-making authority, and investor confidence, operating under Kuwait free zone full foreign ownership rules removes a significant structural constraint.

Practical advantages of this ownership structure include:

- Profits flow entirely to the foreign parent without mandatory local profit-sharing arrangements

- Corporate governance remains under the foreign owner's control, simplifying group-level reporting

- Equity structures are cleaner for international financing and cross-border investment documentation

- No need to negotiate or maintain a local sponsor relationship over the company's operational life

Eligibility for full ownership is tied to operating within an approved free zone boundary and conducting activities consistent with the zone's designated commercial or industrial purposes.

Company Incorporation in Kuwait

Set up your Kuwait-registered entity with full structural guidance across free zone and mainland options.

Access to Gulf Cooperation Council Markets

Kuwait GCC market access benefits extend to any company incorporated under Kuwaiti law, giving your business preferential standing across all six member states of the Gulf Cooperation Council: Saudi Arabia, the UAE, Bahrain, Qatar, and Oman.

Under the GCC Economic Agreement, goods manufactured in Kuwait and meeting the required local content threshold can move across member state borders without customs duties. For a firm producing or assembling goods locally, this effectively opens a combined market of over 57 million people without the tariff friction that applies to companies incorporated outside the bloc.

| Member State | Approximate Population | GDP (USD, approx.) |

|---|---|---|

| Saudi Arabia | 36 million | $1.1 trillion |

| UAE | 10 million | $504 billion |

| Kuwait | 4.9 million | $162 billion |

| Qatar | 2.9 million | $235 billion |

| Bahrain | 1.7 million | $44 billion |

| Oman | 4.5 million | $108 billion |

GCC mutual recognition of professional licenses and business registrations also reduces the procedural burden of expanding operations into neighboring states. A Kuwaiti-registered entity can apply for commercial registration in several GCC countries through simplified bilateral procedures rather than full foreign incorporation processes.

This regional access is not automatic for free zone entities, which may carry restrictions under the GCC's rules of origin framework. Companies incorporated in the mainland under the Companies Law No. 1 of 2016 are better positioned to fully utilize these cross-border trade privileges.

Strong Oil-Backed and Diversifying Economy

Kuwait's sovereign wealth position gives it a degree of macroeconomic stability that few jurisdictions in the region can match. The Kuwait Investment Authority (KIA), established in 1953 and widely regarded as one of the world's oldest sovereign wealth funds, manages assets estimated to exceed $800 billion. For a foreign business operating in the country, this translates into a government with significant fiscal capacity to sustain public infrastructure spending and economic continuity even during periods of global commodity pressure.

Petroleum revenues have historically funded over 80% of state revenues, but the New Kuwait Vision 2035 initiative is actively redirecting public investment toward non-oil sectors, including financial services, logistics, and healthcare. This diversification signals expanding commercial demand in areas where foreign-owned entities can participate.

Consistent government spending supports reliable demand for goods and services, which directly reduces commercial risk for businesses entering the market.

Keep these points in mind:

- KIA's fiscal buffers reduce the risk of sudden regulatory or tax shifts driven by budget pressure

- Vision 2035 sector priorities identify where government procurement and incentives are concentrated

- Non-oil GDP growth creates market entry windows before sectors reach saturation

- Oil price dependency remains a structural feature; monitor fiscal breakeven prices in annual budget announcements

Kuwait has no personal income tax and no value-added tax, making it one of the very few Gulf states that has not yet introduced VAT, unlike Saudi Arabia and the UAE which both levy 15% and 5% respectively.

Modern Companies Law and Legal Framework

Kuwait Companies Law No. 1 of 2016 replaced legislation that had governed commercial entities for decades, introducing a more structured regime for company formation, governance, and foreign participation. For foreign business owners, the practical benefit is predictability: the law defines clear entity types, sets out shareholder rights, and establishes disclosure rules that reduce legal ambiguity when structuring an investment.

Defined Entity Structures That Reduce Setup Risk

Under Law No. 1 of 2016, the Limited Liability Company and the Closed Joint Stock Company are the most commonly used vehicles for foreign-linked operations. Each structure carries defined liability limits, minimum capital thresholds, and board governance requirements, which means your legal exposure is quantifiable from the outset rather than subject to interpretation.

Regulatory oversight sits with the Ministry of Commerce and Industry, which administers company registration and ongoing compliance filings. Having a single primary authority reduces coordination complexity when managing annual obligations.

Governance Rules That Protect Investor Interests

The law introduced mandatory provisions around minority shareholder protections and related-party transaction disclosures. These rules give foreign co-investors or minority stakeholders a statutory basis for recourse, rather than relying solely on contractual arrangements between parties.

Updated provisions also addressed electronic records and modernised procedural requirements, reducing reliance on paper-based processes. For firms operating across multiple jurisdictions, alignment with recognisable corporate governance standards lowers the due diligence burden when onboarding international partners or institutional counterparties.

Structure Your Kuwait Entity Under the Right Legal Framework

Get guidance on which company structure under Kuwait Companies Law No. 1 of 2016 fits your business objectives and foreign ownership requirements.

Low Import Duties and Trade Advantages

Kuwait low import duties trade advantages make it a cost-efficient entry point for businesses moving goods into the Gulf. Under the GCC Unified Customs Tariff, most imported goods are subject to a standard 5% ad valorem duty. That single rate applies across all six GCC member states, meaning goods cleared through a Kuwaiti port of entry can move onward to Saudi Arabia, the UAE, Bahrain, Qatar, and Oman without additional customs assessments at each border.

- The 5% standard tariff rate is among the lowest applied customs ceilings in the broader Middle East and North Africa region, directly reducing landed costs for importers relative to markets with tiered or sector-specific duty schedules.

- A defined list of goods, including basic foodstuffs and certain agricultural inputs, carries a zero-duty rate under the GCC tariff schedule, which lowers supply chain costs for firms in food distribution or agricultural processing.

- Kuwait customs duty benefits for importers are further extended through bilateral and multilateral trade agreements to which Kuwait is party as a GCC member, including the GCC-Singapore Free Trade Agreement, which provides preferential access for qualifying goods.

- Goods destined for re-export can benefit from duty suspension mechanisms, preserving cash flow during transit operations.

Eligibility for preferential rates generally requires a valid certificate of origin and compliance with GCC rules of origin criteria.

Strategic Location Between East and West

Kuwait sits at the northern tip of the Arabian Gulf, sharing borders with Iraq and Saudi Arabia while maintaining direct maritime access to global shipping lanes. For companies engaged in international trade, this position places your business within a short transit radius of three major economic zones: South Asia, East Africa, and the European market via the Suez Canal route.

Shuwaikh and Shuaiba ports handle substantial cargo volumes and connect to established freight corridors running east toward India and southeast Asia, and west toward Europe and North America. Mubarak Al-Kabeer Port, under development on Boubyan Island, is designed to position the country as a northern Gulf transshipment point once fully operational.

Kuwait's geographic advantage for international trade is reinforced by its position as a GCC member state, meaning goods entering here can transit across a tariff-unified bloc covering five additional countries without repeated customs clearance at each border crossing.

A company shipping goods from South Asia into the GCC can use Kuwait as a northern entry point, reducing onward land freight distances to Iraq and beyond compared to routing through UAE ports in the south, a practical cost differential for firms targeting both Gulf and Levant markets simultaneously.

Government Incentives Through Kuwait Direct Investment Promotion Authority

Kuwait Direct Investment Promotion Authority (KDIPA) operates under Law No. 116 of 2013, which replaced the earlier foreign investment law and granted KDIPA the mandate to attract and facilitate inward investment. For foreign businesses, this means dealing with a single, dedicated government body rather than navigating multiple ministries independently.

KDIPA benefits for foreign investors include a formal incentives package tied to the nature and scale of the proposed business activity. Approved projects can receive exemptions from corporate income tax for a defined period, customs duty relief on imported equipment and machinery, and protection against expropriation. These concessions are granted through a licensing mechanism that KDIPA administers directly.

Eligibility is not automatic. KDIPA evaluates applications based on the extent to which a project contributes to knowledge transfer, employment of Kuwaiti nationals, or economic diversification aligned with Kuwait Vision 2035. Projects in priority sectors, including technology, healthcare, and logistics, generally receive more favorable treatment.

- KDIPA advantages for foreign businesses also include facilitation support during setup, which can reduce time spent on government liaison.

- Approved investors gain access to a formal dispute resolution framework under the same law.

KDIPA incentives apply only to projects that receive formal approval under Law No. 116 of 2013; operating without KDIPA registration means no access to tax exemptions or duty relief.

High-Income Consumer Base and Spending Power

Kuwait's high-income consumer market advantages are grounded in measurable economic data, not regional generalizations. The country consistently records one of the highest GDP per capita figures in the world, driven by oil revenues distributed across a relatively small population of approximately 4.9 million. That concentration of wealth directly affects how consumers spend.

Household consumption patterns in Kuwait skew toward premium goods, imported products, and branded services. Retail, food and beverage, electronics, and luxury segments all record sustained demand. For a foreign business selling higher-margin products or services, this spending profile reduces the need to compete on price alone.

The expatriate population, which accounts for roughly 70% of residents, adds a distinct consumer layer. This group includes professionals from South Asia, Europe, and the Arab world with stable incomes and consumption habits tied to global brands and service standards familiar to international firms.

Consumer spending in Kuwait is supported by the absence of personal income tax, which means households retain a larger share of earnings compared to most OECD economies. That disposable income flows directly into private consumption rather than being absorbed by wage taxation.

Key consumer segments relevant to foreign operators include:

- Healthcare and wellness services

- Premium food retail and hospitality

- Education and professional development

- Consumer electronics and technology products

- Financial and insurance services

Market entry through a Kuwaiti entity gives your business direct access to this spending base within a single, compact geography, reducing distribution complexity relative to larger regional markets.

Stable Currency Pegged to a Basket

The Kuwaiti dinar is the highest-valued currency unit in the world, and Kuwait stable currency benefits for businesses extend well beyond simple exchange rate comfort. Unlike most Gulf currencies pegged solely to the US dollar, the dinar is pegged to an undisclosed basket of currencies, a policy managed by the Central Bank of Kuwait under the Central Bank of Kuwait Law No. 32 of 1968 (as amended). This basket peg mechanism insulates the currency from single-currency volatility, giving your business a more stable pricing environment than a straight dollar peg would provide.

For foreign companies pricing contracts, repatriating profits, or managing multi-currency exposure, this stability has a direct operational value. Currency unpredictability forces businesses to hedge, absorb losses, or reprice regularly. The dinar's consistent performance reduces those costs.

Kuwaiti dinar stability advantages for investors also appear in financial planning and asset valuation. When your local revenues hold their value against a diversified reference basket, long-term investment modeling becomes more reliable. This matters particularly for firms entering multi-year service or supply contracts with government entities or large local conglomerates.

- The dinar has maintained a narrow trading band, with the Central Bank of Kuwait actively intervening to prevent deviation

- Contract values denominated in dinars carry lower currency risk for cross-border settlement than contracts in emerging market currencies

- Foreign companies do not face capital controls on profit repatriation, meaning stable dinar earnings can be converted and transferred without restriction under current Kuwait Foreign Capital Investment Law provisions

Why Kuwait Stands Out Among Regional Business Hubs

Foreign investors comparing Gulf incorporation options typically weigh Kuwait against the UAE and Bahrain, two jurisdictions with established free zone infrastructure and longer track records with international firms. That comparison, however, tends to underweight factors where Kuwait holds a distinct structural position: its currency stability against a basket of currencies, a domestic consumer base with among the highest GDP per capita in the region, and direct access to GCC markets under the same unified customs framework.

Where Kuwait's competitive profile diverges most clearly is in the combination of a large, high-income domestic market and a relatively underpenetrated commercial environment. The UAE absorbs the bulk of regional foreign direct investment, leaving Kuwait with less competitive saturation in several sectors. For businesses targeting Gulf consumers rather than using a jurisdiction purely as a holding or re-export base, this distinction carries real commercial weight. Kuwait Direct Investment Promotion Authority provides the regulatory entry point for foreign investors seeking to understand sector-specific conditions.

| Parameter | Kuwait | UAE | Bahrain |

|---|---|---|---|

| Foreign Ownership (Free Zone) | 100% | 100% | 100% |

| Foreign Ownership (Mainland) | Up to 100% in licensed sectors (Law No. 116/2013) | Up to 100% in most sectors (post-2021 reform) | Up to 100% in most sectors |

| Corporate Tax Rate | 0% for GCC-owned entities; 15% for foreign-owned mainland companies | 9% federal rate (from June 2023) | 0% (except oil sector) |

| Currency Stability | Pegged to a currency basket (KWD) | Pegged to USD (AED) | Pegged to USD (BHD) |

| GCC Customs Union Access | Yes | Yes | Yes |

| Domestic Market Size (GDP per capita) | ~USD 32,000+ | ~USD 44,000+ | ~USD 26,000+ |

| Free Zone Options | Limited (KFZ primary zone) | Extensive (40+ free zones) | Moderate (Bahrain International Investment Park, others) |

Compliance Services for Companies in Kuwait

Stay aligned with Kuwait's regulatory requirements, from annual filings to corporate governance obligations under the Companies Law and KDIPA frameworks.

Conclusion

Kuwait's position as a GCC member state, combined with a tax structure that exempts most foreign-registered entities from corporate income tax, makes the benefits of incorporating in Kuwait more concrete than they might appear at first glance. Zero corporate tax on qualifying activities and unrestricted repatriation of profits are not minor incentives — they directly affect the financial architecture of a foreign-owned business from day one.

For firms where free zone incorporation aligns with their operational model, full foreign ownership eliminates the need for a local equity partner, which has historically been one of the more significant structural barriers across the Gulf. Access to the GCC market through a single registered entity adds further weight to that advantage, given the combined economic scale of six member states under preferential trade terms.

Not every business structure will fit the same Kuwait formation pathway. Sectors subject to foreign ownership restrictions outside free zones, or industries that fall under specific licensing regimes governed by the Kuwait Direct Investment Promotion Authority, will require closer analysis of eligibility before committing to a structure. The case for Kuwait company formation rests on a specific combination of tax treatment, market access, and economic stability — and that combination performs differently depending on your industry and intended operations. Understanding exactly where your business sits within that framework is the necessary starting point for any formation decision.

Start Your Kuwait Company Formation With Expanship Today

Expanship Kuwait business incorporation services cover the full formation process across the entity types discussed in this blog, including the With-Limited-Liability Company, the Kuwaiti Shareholding Company, and free zone structures under the Kuwait Free Trade Zone framework. Filings are coordinated with the Ministry of Commerce and Industry, and where applicable, with the Kuwait Direct Investment Promotion Authority. Your corporate structure is handled in alignment with the Companies Law No. 1 of 2016 and its subsequent amendments.

From document preparation through to post-incorporation compliance, Expanship's service scope across Kuwait company formation with Expanship includes:

- Document preparation, notarization, and official legalization for use with Kuwaiti authorities

- Registered agent and registered office provision within Kuwait

- Government filing and direct liaison with the Ministry of Commerce and Industry

- Post-incorporation compliance management, including annual filings and regulatory reporting

- Banking introduction assistance to support corporate account establishment with local financial institutions

- Ongoing corporate secretarial support to maintain good standing

To discuss how Expanship Kuwait can assist with your entity formation or compliance requirements, contact the team directly.

Frequently Asked Questions (FAQ)

Kuwait does not impose corporate income tax on companies owned by nationals of other Gulf Cooperation Council states or on most domestic commercial activities. Foreign-owned companies operating onshore are subject to a corporate tax rate of 15% under the Income Tax Decree, while entities structured within free zones may qualify for tax exemptions. The applicable rate depends on the ownership structure and the jurisdiction of the parent company.

The Kuwait Direct Investment Promotion Authority, known as KDIPA, is the statutory body responsible for licensing and facilitating foreign direct investment under Law No. 116 of 2013. It can grant approved foreign investors benefits including full ownership rights and exemptions from certain fees. Applications are assessed against defined criteria, including the economic contribution and sector of the proposed business.

The Kuwaiti dinar is pegged to an undisclosed basket of currencies managed by the Central Bank of Kuwait, which has historically produced low exchange rate volatility. This structure reduces the currency risk associated with repatriating profits or maintaining working capital in the local denomination. The dinar consistently holds one of the higher valuations among global currencies, which affects the real value of capital held in-country.

Incorporation timelines in Kuwait vary depending on the entity type, the completeness of submitted documents, and whether the application is routed through KDIPA or the Ministry of Commerce and Industry. Onshore company formation can take several weeks when accounting for ministerial approvals, commercial registration, and sector-specific licensing. Free zone incorporations may follow a separate and potentially faster administrative track.

Companies incorporated in Kuwait benefit from its membership in the Gulf Cooperation Council, which operates a customs union and common market agreement among Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates. This allows goods and, under certain conditions, services to move across member states with reduced barriers. Kuwait also applies the GCC's common external tariff, which sets import duties at 5% for most goods, creating a uniform trade cost structure.

Changing the registered business activity of an entity in Kuwait typically requires an amendment to the commercial registration and, depending on the nature of the new activity, fresh approvals from the Ministry of Commerce and Industry or relevant sector regulators. If the entity holds a KDIPA licence, modifications to the approved scope of activities would require notification or re-evaluation by that authority. Operating outside the scope of a registered activity can result in regulatory penalties or suspension of the commercial licence.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.