Key Takeaways

- Japan's corporate legal framework, governed by the Companies Act (Kaisha-hō) of 2006, offers eight distinct business structures, each with different implications for liability, governance, and taxation.

- The Kabushiki Kaisha remains the most registered corporate form in Japan due to its recognized credibility among local counterparties, partners, and financial institutions.

- Foreign entities operating through a branch office retain parent company liability, while a representative office is legally prohibited from conducting revenue-generating activities.

- Registration of all corporate entities in Japan falls under the Legal Affairs Bureau (Hōmukyoku), operating within the Ministry of Justice, with records maintained in the Commercial Register (Shōgyō Tōki).

Introduction to Entity Types in Japan

Japan is an island nation in East Asia, bordered by the Sea of Japan to the west and the Pacific Ocean to the east, with South Korea, China, and Russia among its closest neighbors. As an independent sovereign state, it maintains a well-established legal framework for business formation governed primarily by the Companies Act (Kaisha-hō) of 2006. Company registration falls under the jurisdiction of the Legal Affairs Bureau (Hōmukyoku), which operates under the Ministry of Justice, and registered entities are recorded in the Commercial Register (Shōgyō Tōki).

Japan operates a residence-based tax system with corporate tax obligations applied to worldwide income for domestic entities, while foreign firms may face different treatment depending on their structure.

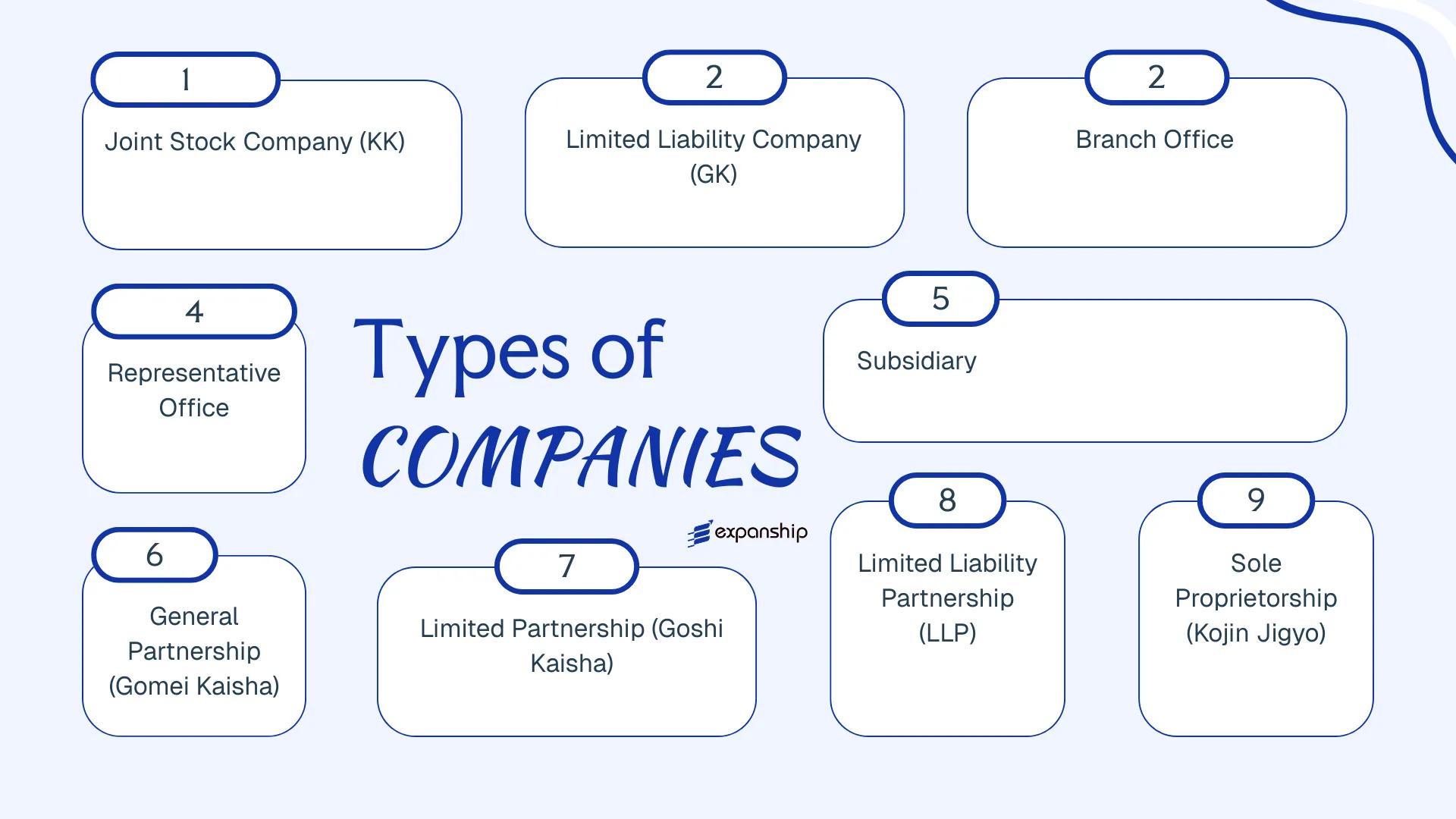

For those assessing types of business entities in Japan, the legal framework provides several distinct options: Kabushiki Kaisha (KK), Godo Kaisha (GK), Gomei Kaisha, Goshi Kaisha, Limited Liability Partnership (LLP), Branch Office, Representative Office, and Sole Proprietorship (Kojin Jigyo). Each structure carries different implications for liability, governance, taxation, and compliance. This article examines each of these Japanese legal entity structures in detail to help you determine which suits your business objectives.

An Overview of Business Structures in Japan

Four principal entity types are available under the Companies Act of Japan (Kaisha-ho), enacted in 2005 and consolidated under Act No. 86. This legislation governs all incorporated business structures, while sole proprietorships and partnerships operate under separate statutory frameworks including the Civil Code and the Limited Liability Partnership Act. Each structure carries distinct rules on liability, governance, and taxation that make it suited to different commercial purposes.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Kabushiki Kaisha (KK) | Corporation | Limited | Taxed | Yes | 1 shareholder | Legal Affairs Bureau | Companies Act (2005) |

| Godo Kaisha (GK) | LLC | Limited | Taxed | Yes | 1 member | Legal Affairs Bureau | Companies Act (2005) |

| Gomei Kaisha | General Partnership | Unlimited | Taxed | Yes | 2 partners | Legal Affairs Bureau | Companies Act (2005) |

| Goshi Kaisha | Limited Partnership | Mixed | Taxed | Yes | 2 partners | Legal Affairs Bureau | Companies Act (2005) |

| LLP (Yugen Sekinin Jigyo Kumiai) | Partnership | Limited | Pass-through | Yes | 2 partners | Legal Affairs Bureau | LLP Act (2005) |

| Branch Office | Foreign branch | Unlimited (parent) | Taxed on Japan income | Yes | 1 representative | Legal Affairs Bureau | Companies Act (2005) |

| Representative Office | Non-legal entity | N/A | Generally exempt | No | 1 representative | None (no registration) | No specific act |

| Sole Proprietorship (Kojin Jigyo) | Individual | Unlimited | Personal income tax | Yes | 1 individual | Tax Office (NTA) | Income Tax Act |

Each of these structures is examined in full in the sections below.

Kabushiki Kaisha (KK) — Joint Stock Company

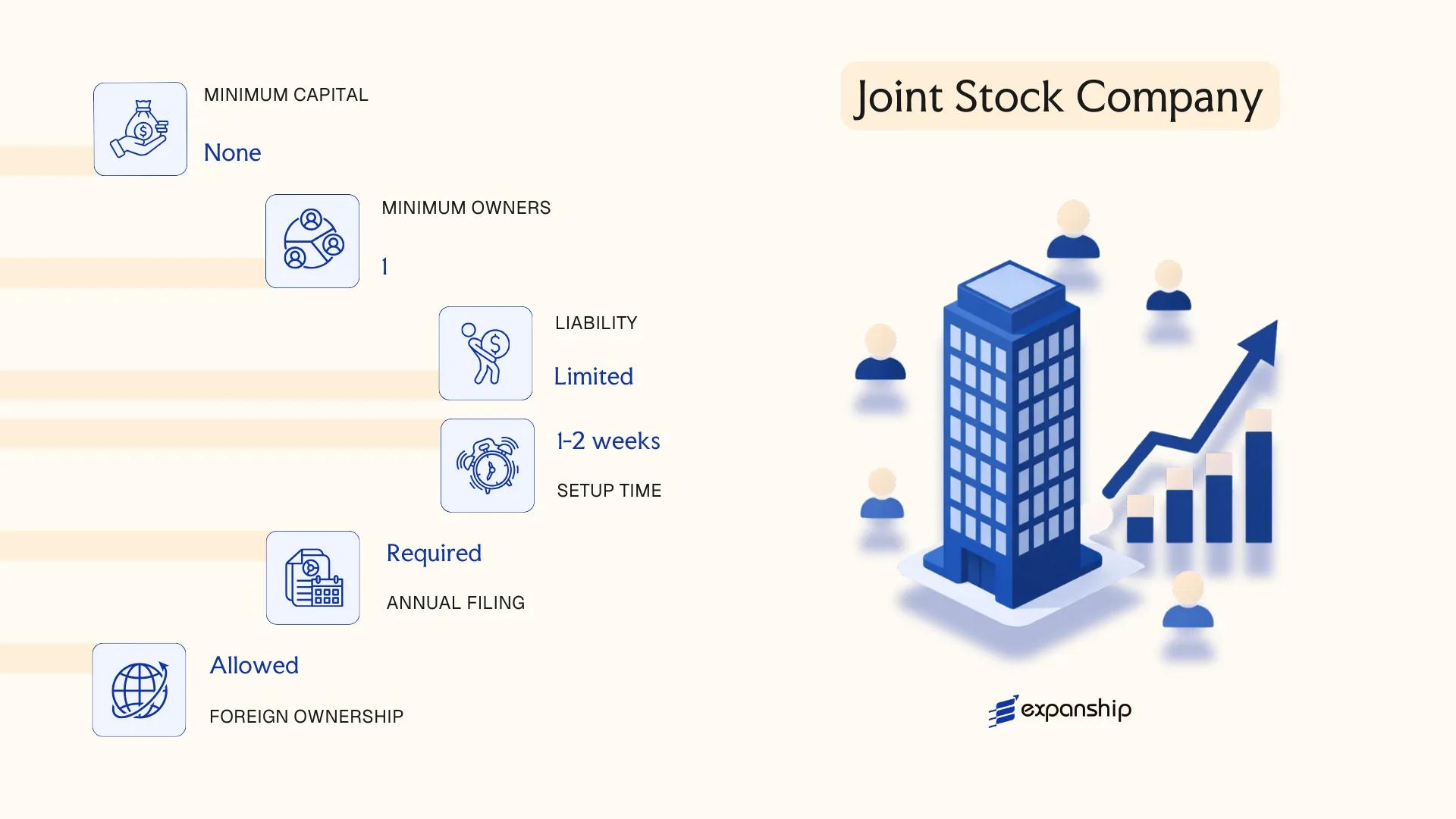

The Kabushiki Kaisha (KK) is the most widely recognised corporate form in Japan, governed by the Companies Act (Kaisha-ho) enacted in 2005. It carries separate legal personality, meaning the entity exists independently of its shareholders, and liability is limited to each shareholder's capital contribution.

Shares in a KK are freely transferable by default, which makes the structure suitable for businesses seeking external investment, public listing, or multi-party ownership arrangements.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Kabushiki Kaisha (KK) | Incorporated under the Companies Act 2005 |

| Members | Shareholders (Kabunushi); minimum 1, no maximum | Directors (Torishimariyaku): minimum 1; a Large Company (Daigaisha) requires a Board of at least 3 directors plus a statutory auditor |

| Local Presence | Registered address in Japan required | A representative director must be appointed; no statutory requirement that the representative director be a Japan resident as of 2015 amendment |

| Share Capital | JPY 1 minimum | No minimum capital requirement under current law; paid-in capital recorded on the balance sheet |

| Privacy | Shareholder names not publicly disclosed | Director names and registered address appear in the Commercial Registry (Shogyō Tōki) |

| Accounting Reference | Fiscal year defined in articles of incorporation | Annual financial statements filed with the Legal Affairs Bureau |

Focus Points

- Taxation: Corporate income tax applies at the national level (approximately 23.2% for large corporations); local inhabitant and enterprise taxes bring the effective combined rate to roughly 30–34%; consumption tax (JCT) at 10% applies to taxable supplies; withholding tax applies to dividends, interest, and royalties paid to non-residents — rates vary under applicable tax treaties. (See [National Tax Agency](https://www.nta.go.jp/english/) for current rates.)

- Treaty Access: A KK qualifies as a Japanese resident company for purposes of Japan's tax treaty network, currently covering 80+ jurisdictions.

- Annual Compliance: Annual general meeting of shareholders required within three months of fiscal year-end; financial statements must be approved and filed; changes to directors or registered details require Commercial Registry updates.

- Conversion: A KK may convert into a Godo Kaisha (GK) or other entity form under the Companies Act without dissolution, subject to shareholder approval.

- Share Transfer Restrictions: Articles of incorporation may restrict share transfers, requiring board approval — a common provision in closely held firms.

Sub-Types

Public Company (Kokai Kaisha)

A KK whose articles do not restrict share transfers is classified as a Kokai Kaisha. This classification triggers stricter governance requirements, including a mandatory board of directors and, in most cases, a statutory auditor or audit committee.

Private Company (Hikokai Kaisha)

Where the articles of incorporation restrict all share transfers to board approval, the entity is a Hikokai Kaisha. Governance requirements are lighter, making this the standard structure for owner-managed or foreign-owned subsidiaries.

Large Company (Daigaisha)

A KK with paid-in capital of JPY 500 million or more, or total liabilities exceeding JPY 20 billion, is classified as a Daigaisha under the Companies Act. This triggers mandatory audit requirements, including appointment of a certified public accountant (Kōnin Kaikeishi) or audit firm.

Closing

A KK suits trading operations, Japanese subsidiaries of foreign multinationals, and businesses that anticipate raising capital or eventual listing on a Japanese exchange. The structure's credibility with local banks and counterparties is a practical advantage; however, ongoing governance and reporting obligations are more demanding than those of a Godo Kaisha, which can increase administrative costs for smaller operations.

The KK structure is best suited for foreign companies establishing a fully operational Japanese subsidiary, businesses targeting Japanese institutional clients, or ventures planning a future public offering on the Tokyo Stock Exchange.

Company Incorporation in Japan

Incorporate a Kabushiki Kaisha or other Japanese entity with end-to-end support from registration through post-incorporation compliance.

Godo Kaisha (GK) — Limited Liability Company

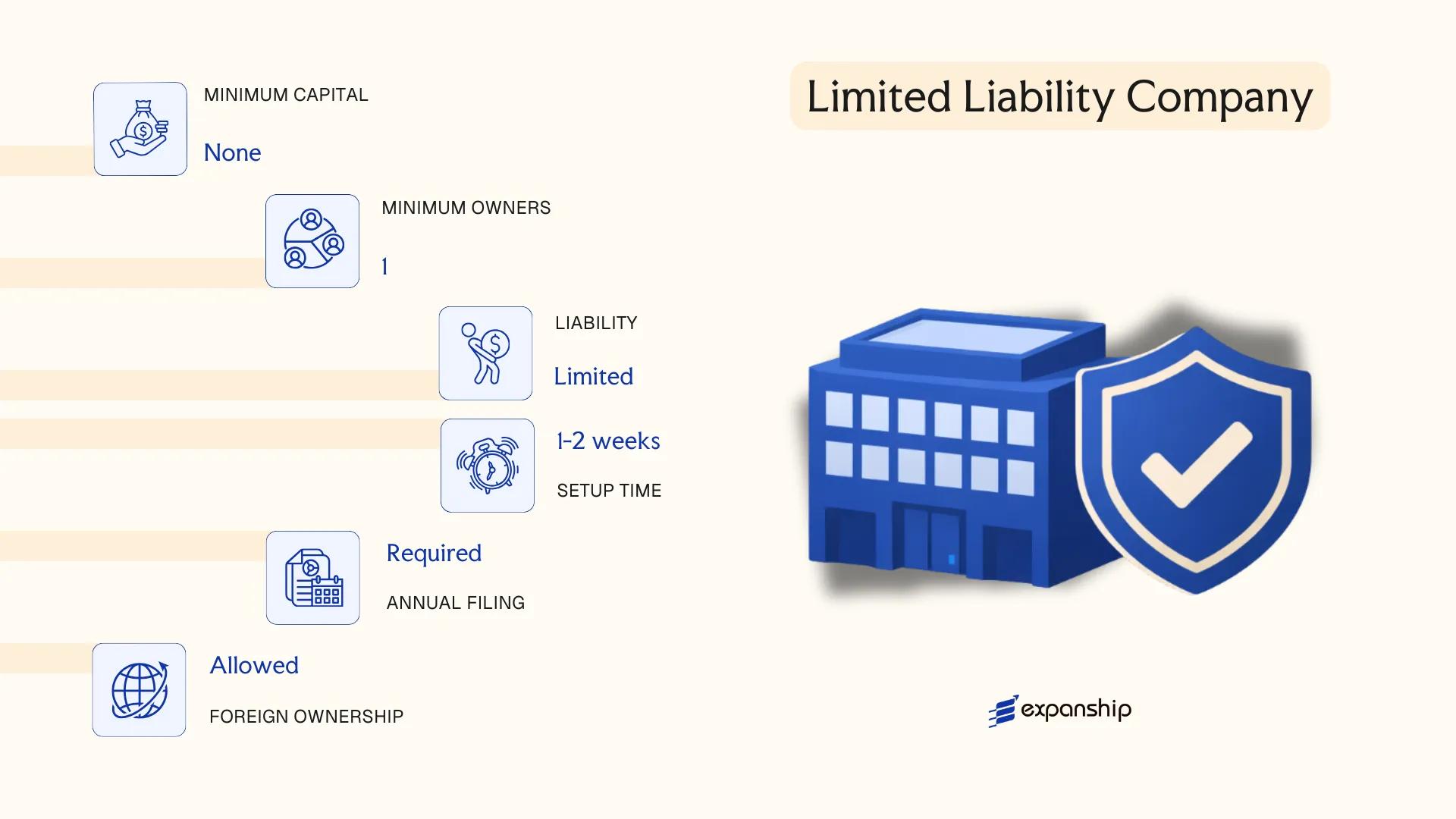

Introduced under the Companies Act of 2005 (Kaisha-ho), the Godo Kaisha GK Japan LLC structure gives members both limited liability protection and considerable operational flexibility. Unlike the more rigid Kabushiki Kaisha, a GK allows members to define internal governance and profit distribution through a private members' agreement rather than statutory defaults.

As a separate legal entity, the GK can hold assets, enter contracts, and incur liabilities in its own name. This hybrid character — borrowing from both the US LLC and traditional Japanese partnership models — has made it a common choice for foreign investors seeking a lighter compliance footprint.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Yugen Sekinin Kaisha (limited liability company) | Registered with the Legal Affairs Bureau (Homukyoku) |

| Members | referred to as "sha-in" (members); minimum 1, no maximum | Members can also act as managers; no separate director class required |

| Local Presence | Registered address in Japan required; no mandatory resident director under GK rules | A registered agent service can satisfy the address requirement |

| Capital | No statutory minimum; JPY 1 is legally permissible | Capital must be recorded in the articles of incorporation |

| Privacy | Member names appear in the commercial register | Less public disclosure than a KK; no public financial statements required |

Focus Points

- Taxation: Subject to corporate income tax (national rate approximately 23.2%), local inhabitant and business taxes, consumption tax (10% JCT where applicable), and withholding tax on dividends paid to foreign members; no separate GK-specific tax regime.

- Annual Compliance: No mandatory audit or public financial statement filing for most GKs; annual tax returns must be filed with the National Tax Agency.

- Treaty Access: GKs are generally treated as opaque entities under Japanese domestic law, which supports access to Japan's tax treaty network, though treaty eligibility depends on the counterpart jurisdiction's classification of the GK.

- Conversion: A GK can be converted into a KK under the Companies Act without dissolution, a process that requires a special resolution and re-registration.

Closing

The Japan limited liability company Godo Kaisha structure suits holding arrangements, single-asset vehicles, and wholly-owned operating subsidiaries where internal flexibility matters more than public credibility. The primary limitation is perception: some Japanese business counterparts still regard a GK as less established than a KK.

Foreign companies establishing a wholly-owned Japanese subsidiary where simplified governance and lower compliance costs outweigh the need for public market access.

Foreign Entities [Branch Office, Representative Office, Subsidiary]

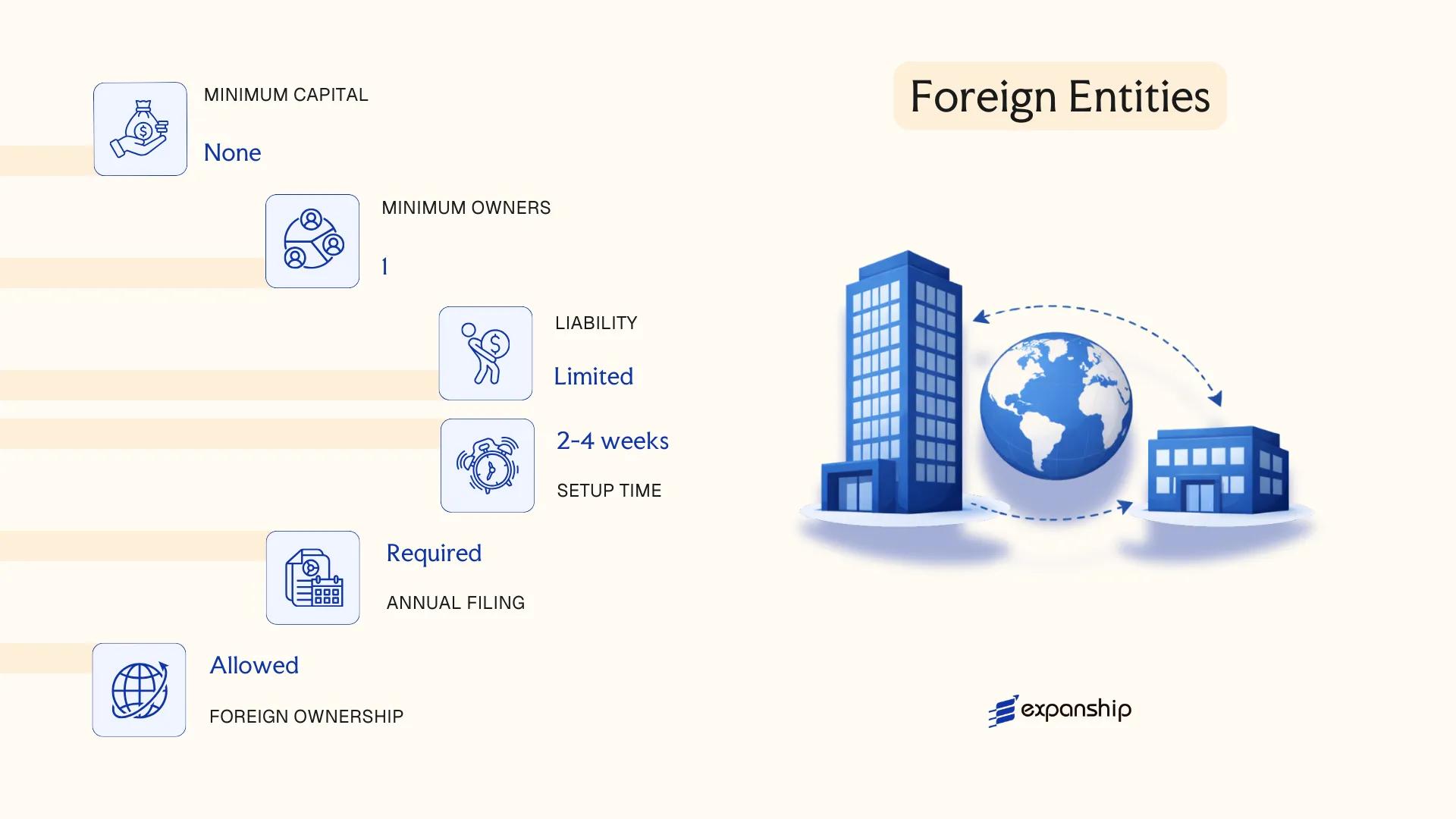

Foreign companies seeking a presence in Japan without forming a new domestic entity have three recognised structural options: a branch office, a representative office, or a locally incorporated subsidiary. Establishing a foreign company branch office Japan requires registration under the Companies Act 2005 (Kaisha-ho) and the Commercial Registration Act, with the branch treated as an extension of the parent rather than a separate legal entity.

A representative office holds no legal registration under Japanese law and cannot execute commercial contracts or generate revenue directly. It exists purely for market research, liaison activities, and promotional functions. Because it falls outside the scope of formal registration, it carries limited compliance obligations but also limited operational capacity.

Key Characteristics

| Requirement | Branch Office | Representative Office | Subsidiary |

|---|---|---|---|

| Legal Form | Extension of foreign parent | Unregistered presence | Separate legal entity (KK or GK) |

| Registration | Required under Companies Act 2005 | Not required | Required; standalone incorporation |

| Local Representative | Mandatory resident representative in Japan | Appointed internally | Director (residency not legally mandated post-2015) |

| Registered Address | Required in Japan | Required in Japan | Required in Japan |

| Minimum Capital | None | None | None (KK: no minimum since 2006) |

| Liability | Parent bears full liability | Parent bears full liability | Limited to subsidiary assets |

Focus Points

- Taxation: Branch profits are subject to Japanese corporate tax (standard rate approximately 23.2% national); a branch also faces a branch profits remittance tax in certain treaty contexts, and consumption tax (JCT) applies to taxable supplies at 10%.

- Tax Treaties: Subsidiaries generally access Japan's tax treaty network more reliably; branch treatment under treaties varies by the parent company's home jurisdiction.

- Compliance: Branches must file annual financial statements with the Legal Affairs Bureau and submit corporate tax returns to the National Tax Agency; representative offices have no statutory filing obligations.

- Restrictions: Representative offices are prohibited from engaging in revenue-generating or sales activities; any commercial transaction triggers the obligation to register as a branch or subsidiary.

- Conversion: A branch cannot convert directly into a KK or GK; a separate incorporation process is required, though operational assets can be transferred.

Sub-Types

Branch Office

Registered with the Legal Affairs Bureau under Article 933 of the Companies Act, the branch conducts business on behalf of the foreign parent and must appoint at least one resident representative. All liabilities remain with the parent entity.

Representative Office

Operates without formal legal registration and is commonly used during early-stage market assessment. Activities are strictly limited to non-commercial functions such as information gathering and relationship building.

Subsidiary

Incorporated as a domestic KK or GK, the subsidiary is legally independent from its foreign parent. This structure is covered in detail under the respective KK and GK sections above.

Closing

A branch office suits foreign firms that want direct operational presence without the administrative burden of full incorporation, though the parent's unlimited liability exposure is a material drawback. A subsidiary, while more complex to establish, provides liability separation and a cleaner profile for local contracting and banking.

A branch office is most practical for foreign companies testing the Japanese market or executing specific projects, where maintaining a standalone corporate structure is not yet warranted.

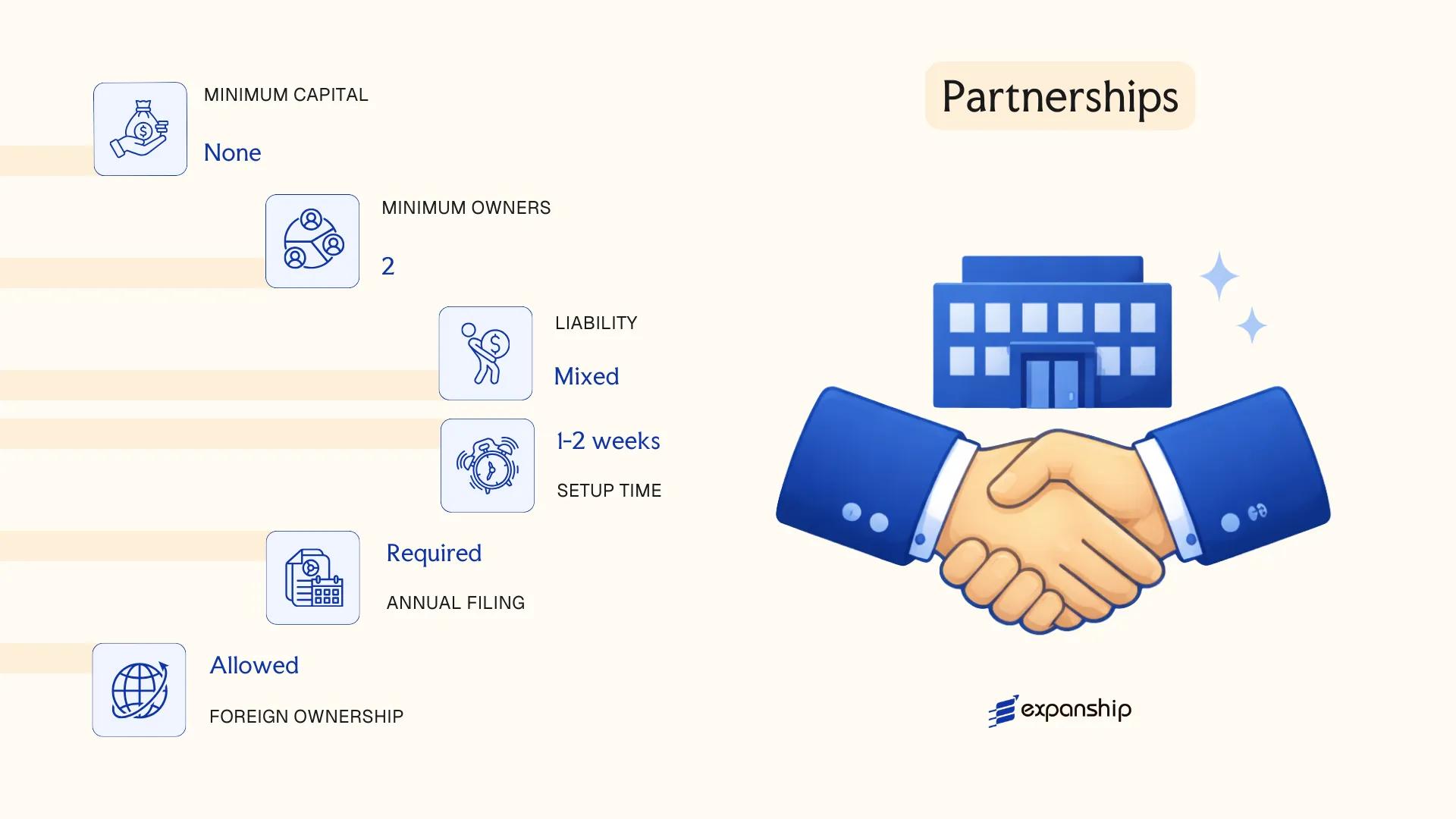

Partnerships [Gomei Kaisha (General Partnership), Goshi Kaisha (Limited Partnership), Limited Liability Partnership (LLP)]

Gomei Kaisha, Goshi Kaisha, and Japan partnership structures broadly are governed by the Companies Act 2005 (Kaisha-ho), which unified and modernised the earlier commercial code provisions. Unlike a KK or GK, both the Gomei Kaisha and Goshi Kaisha lack separate legal personality, meaning creditors can pursue individual members directly for business debts.

The Limited Liability Partnership (LLP), regulated under the Act on Limited Liability Partnerships 2005, does carry separate contractual standing but is not a corporation. Its internal profit-sharing can deviate from capital contribution ratios, a flexibility not available in most incorporated structures.

Key Characteristics

| Requirement | Gomei Kaisha (General Partnership) | Goshi Kaisha (Limited Partnership) | LLP |

|---|---|---|---|

| Legal Form | Unincorporated; no separate legal personality | Unincorporated; no separate legal personality | Contractual entity; limited separate standing |

| Members | Partners (all with unlimited liability); min. 1 | General partners (unlimited) + limited partners; min. 1 of each | Members; min. 2, no statutory maximum |

| Liability | Unlimited for all partners | Unlimited for general partners; limited for limited partners | Limited to capital contribution for all members |

| Local Presence | Registered address in Japan required | Registered address in Japan required | Registered address in Japan required |

| Capital | No statutory minimum; denominated in JPY | No statutory minimum; denominated in JPY | No statutory minimum; denominated in JPY |

| Privacy | Partner names filed publicly in commercial registry | Partner names filed publicly in commercial registry | Member details filed with Legal Affairs Bureau |

Focus Points

- Taxation: All three structures are pass-through by default; profits are taxed at the partner or member level under individual or corporate income tax rates, with no entity-level corporate tax; consumption tax (JCT) registration obligations apply if annual taxable sales exceed JPY 10 million.

- Annual Compliance: Gomei Kaisha and Goshi Kaisha must file changes with the Legal Affairs Bureau; LLPs file annual reports under the LLP Act but face lighter disclosure requirements than incorporated entities.

- Treaty Access: Pass-through treatment may restrict access to Japan's tax treaty network, as treaty benefits typically attach to tax-resident corporations, not transparent entities.

- Restrictions: LLPs cannot list publicly or issue equity securities; Gomei Kaisha structures are rarely used in foreign-investment contexts due to unlimited liability exposure.

Sub-Types

Gomei Kaisha (General Partnership Company)

All partners hold unlimited, joint liability for the firm's obligations. This structure is uncommon in commercial practice and is generally used only for family-run or professional businesses where all participants actively manage operations.

Goshi Kaisha (Limited Partnership Company)

Goshi Kaisha registration in Japan requires at least one general partner bearing unlimited liability alongside one or more limited partners whose exposure is capped at their capital contribution. Limited partners are prohibited from participating in management.

Limited Liability Partnership (LLP)

Distinct from the Goshi Kaisha, the LLP grants limited liability to all members while permitting flexible profit allocation in the partnership agreement. It is commonly used for joint ventures and professional collaborations between corporate entities.

These structures suit professional services firms, joint ventures, or domestic family businesses where management participation and flexible profit distribution outweigh the absence of full corporate liability protection. Pass-through taxation is the key operational advantage, though unlimited liability in general and limited partnership forms poses a material risk for foreign investors.

Japanese partnerships are most appropriate for domestic joint ventures between corporate entities or professional firms seeking pass-through tax treatment, provided all parties have a clear understanding of their respective liability exposure.

Sole Proprietorship (Kojin Jigyo)

A sole proprietorship Japan residents and foreign nationals can register is known as a Kojin Jigyo. Unlike a Kabushiki Kaisha or Godo Kaisha, it carries no separate legal personality — the business and its owner are treated as a single legal entity under Japanese law.

Because there is no corporate shield, the proprietor bears unlimited personal liability for all business debts and obligations. Registration is filed with the local tax office (zeimusho) under the Act on Special Measures Concerning Taxation and related administrative guidance, rather than through the Legal Affairs Bureau.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality; owner and business are one |

| Members | Single proprietor | No minimum capital or co-owners; foreign nationals may register with valid residency status in Japan |

| Local Presence | Business address required | Must file with the jurisdictionally competent zeimusho (tax office) |

| Capital | No minimum | Owner funds business from personal assets |

| Privacy | Proprietor's name is public | Business name (ya-go) may differ from proprietor's name but is not a separate legal identity |

| Liability | Unlimited personal liability | All personal assets are exposed to business creditors |

Focus Points

- Taxation: Income is reported as personal income tax (shotokuzei) under a self-assessment system; consumption tax (8% or 10%) applies once annual taxable sales exceed JPY 10 million; no corporate tax applies; proprietors may deduct business expenses against gross income.

- Annual Compliance: A Blue Form (Aoiro Shinkoku) tax return must be filed annually by March 15 for the prior calendar year; Blue Form status, applied for through the zeimusho, unlocks additional deduction allowances.

- Treaty Access: Kojin Jigyo does not qualify for corporate tax treaty benefits; personal income tax treaties may apply depending on the proprietor's country of residence.

- Conversion: A sole proprietorship can be converted into a GK or KK, but assets must be formally transferred; there is no automatic structural carry-over.

- Restrictions: Foreign nationals without a qualifying residency status or work visa cannot register a Kojin Jigyo.

Closing

Kojin Jigyo suits freelancers, consultants, and small-scale traders operating with low overheads and no need for investor capital. The primary advantage is administrative simplicity — setup requires minimal paperwork and no incorporation fees. The central drawback is unlimited personal liability, which makes this structure unsuitable for businesses carrying significant financial or legal risk.

Kojin Jigyo is best suited for individual professionals and sole traders already resident in Japan who want a low-cost, low-formality structure for small-scale business activity.

How to Choose the Right Entity Type in Japan

Choosing the right company structure in Japan requires matching your operational profile, tax position, and governance needs to the specific legal characteristics of each available form. No single structure suits every situation.

Why Your Entity Choice Matters

The consequences of an ill-fitted entity selection are concrete and measurable:

- A foreign company conducting continuous business transactions in Japan without registering a branch under the Companies Act (Kaisha-hō, Act No. 86 of 2005) violates Article 818, exposing the entity to injunctions and potential deregistration.

- Selecting a structure that lacks legal personality — such as a Nin-i Kumiai — disqualifies your business from claiming benefits under Japan's tax treaty network, leaving withholding taxes unreduced at source.

- Registering as a Representative Office when your activities cross into commercial operations triggers reclassification risk by the National Tax Agency, with back-tax assessments applied retroactively.

- Forming a KK when a single-member GK would suffice imposes mandatory statutory auditor requirements above certain thresholds, generating recurring compliance costs with no corresponding operational benefit.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors such as financial instruments under the Financial Instruments and Exchange Act, and passive asset holding each correspond to distinct entity types.

- Ownership Structure: A GK suits single-owner or small multi-party arrangements with flexible capital rules, while a KK is required where share transferability or institutional investment is anticipated.

- Tax Objectives: Your entity's residency status and legal form determine eligibility for Japan's participation exemption on foreign dividends and access to its treaty network.

- Public Disclosure Tolerance: KK director and capital details appear in the Commercial Register; if shareholder-level privacy is a priority, structure accordingly from the outset.

- Substance Capacity: If you cannot maintain a physical office and resident representative in Japan, a Representative Office is the only form that avoids full corporate registration obligations.

- Exit and Conversion: Japanese law permits conversion between a KK and GK under Articles 743–747 of the Companies Act, but dissolution procedures differ materially — factor this into your initial decision.

Corporate Compliance Services in Japan

Maintain good standing with Japan's regulatory requirements, including annual filings, registered agent obligations, and statutory recordkeeping.

Conclusion

Selecting the right structure is one of the most consequential decisions in any incorporating a company in Japan guide. The Kabushiki Kaisha suits businesses seeking credibility with Japanese partners and institutional investors, while the Godo Kaisha offers a lower-cost, more flexible alternative for smaller operations and foreign entrepreneurs. Branch offices carry parent company liability; representative offices cannot conduct revenue-generating activities at all. Partnerships serve niche operational needs.

The KK remains the most registered corporate form in Japan, reflecting its deep familiarity among local counterparties and financial institutions.

Regulatory oversight from the Ministry of Justice and the Legal Affairs Bureau continues to evolve, with Japan actively expanding its network of tax treaties and updating compliance expectations for foreign-owned entities. For your business, understanding which structure aligns with your ownership, liability, and commercial objectives is a foundational step before engaging any formal registration process.

How Expanship Can Assist You

Expanship's Japan company formation services cover the full arc of establishment — from choosing between a Kabushiki Kaisha and a Godo Kaisha to filing incorporation documents with the Legal Affairs Bureau (Homukyoku). Every engagement is grounded in the actual regulatory requirements of Japanese corporate law, not generic templates applied across jurisdictions.

From the paperwork stage through to ongoing compliance, Expanship's corporate services in Japan include:

- Articles of incorporation drafting and notarization

- Registered agent and registered office provision

- Filing with the Legal Affairs Bureau and company seal registration

- Post-incorporation tax and social insurance enrollment

- Annual compliance and corporate secretarial support

- Banking introduction assistance for resident and non-resident directors

For a detailed discussion of your specific situation, reach out to Expanship Japan directly.

Frequently Asked Questions (FAQ)

The Kabushiki Kaisha (KK) remains the most frequently registered structure. Its recognition among Japanese clients, financial institutions, and government bodies makes it the default choice for businesses planning sustained domestic operations.

Both structures carry separate legal personality and limit member liability, but their compliance obligations diverge significantly. A KK must hold annual general meetings, prepare audited financial statements under the Companies Act, and maintain a publicly accessible register of directors. A GK carries lighter ongoing requirements and no mandatory share structure, though it is sometimes viewed with less institutional familiarity.

The Godo Kaisha discloses less information publicly than a KK. Member names are not always prominently listed in commercial registry extracts in the same way that KK directors are. Nominee arrangements are legally permissible under Japanese law for both structures, though actual beneficial ownership obligations apply.

A KK and GK can each be formed by a single individual acting as sole shareholder or member. Gomei Kaisha and Goshi Kaisha require at least two partners by definition under the Companies Act. A branch office requires no separate shareholder but must have an appointed representative in Japan.

Foreign nationals face no statutory prohibition on forming a KK, GK, or branch office. The Companies Act imposes no nationality requirement on shareholders, directors, or members. One practical requirement is that a KK must have at least one representative director with a registered address in Japan, which non-residents typically satisfy through a registered agent or by appointing a local representative.

The Companies Act permits organisational conversion between a KK and a GK through a formal resolution and registration procedure at the Legal Affairs Bureau. Conversion to or from a partnership structure is not directly provided for under the same framework and would generally require dissolution and re-incorporation.

The Godo Kaisha has the lightest statutory maintenance burden among incorporated structures. There is no mandatory annual general meeting, no statutory audit requirement for smaller firms, and no prescribed share issuance process. A representative office carries even fewer obligations but cannot conduct revenue-generating activity.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.