Key Takeaways

- Under Japan's Companies Act (Kaisha-ho), all incorporating entities must register with the Legal Affairs Bureau under the Ministry of Justice before commencing operations, with unregistered business activity exposing founders to legal liability.

- Foreign investors establishing a Kabushiki Kaisha or Godo Kaisha must appoint at least one representative director who is resident in Japan, making this the most structurally significant compliance requirement for non-resident founders.

- Share capital in Japan carries no statutory minimum for most entity types, but the amount declared at incorporation has direct practical implications for corporate credibility and banking relationships.

- Entity type selection — whether a Kabushiki Kaisha or Godo Kaisha — determines the applicable structural, documentary, and director requirements that must be satisfied before the Legal Affairs Bureau will approve a registration application.

Entity formation in Japan is governed by the Companies Act (Kaisha-ho), administered through the Legal Affairs Bureau under the Ministry of Justice, which maintains the commercial register for all incorporated entities. Japan business formation compliance requires meeting a defined set of structural, documentary, and legal conditions before registration is approved.

Failure to satisfy these conditions results in rejection of the incorporation application by the relevant Legal Affairs Bureau, and operating without proper registration exposes a business to legal liability under Japanese law.

Specific requirements vary depending on the entity type selected, such as a Kabushiki Kaisha (KK) or Godo Kaisha (GK), as well as the industry sector and whether the founders are resident or non-resident.

This article is most relevant to foreign investors and overseas business owners evaluating the Japan company registration requirements before establishing a local presence.

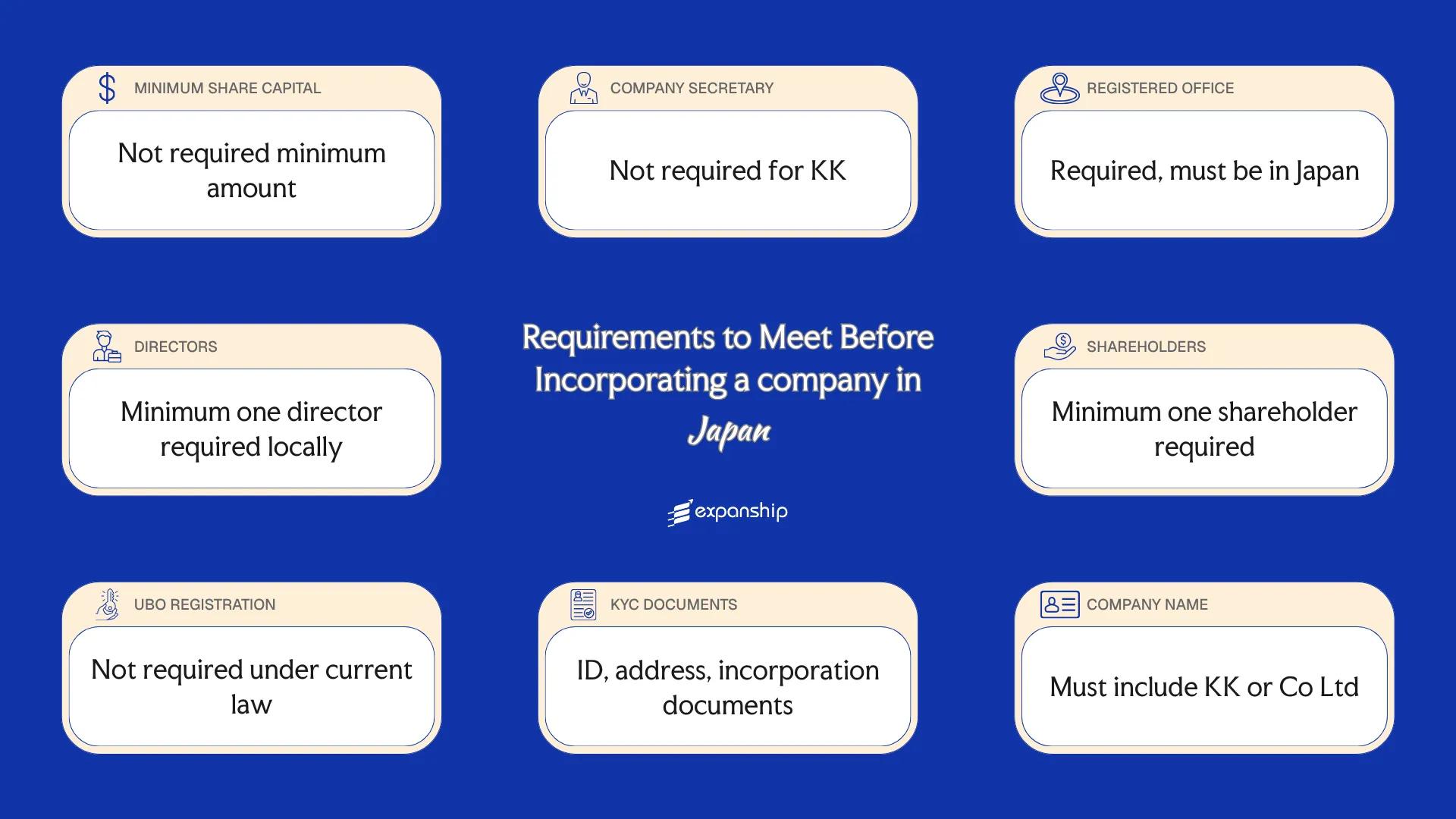

Minimum Share Capital Requirements in Japan

Under Japan's Companies Act (Kaisha-ho), there is no statutory minimum share capital for a Kabushiki Kaisha (KK) or Godo Kaisha (GK). A KK can be incorporated with as little as JPY 1 in authorized and paid-up capital, though the required capital amount must be stated in the articles of incorporation (teikan) filed with the Legal Affairs Bureau (Homukyoku).

Capital deposit must be verified before registration is completed. The incorporator deposits the subscribed capital into a personal or corporate bank account, and the bank issues a confirmation document that is submitted as part of the registration package to the Legal Affairs Bureau.

| Parameter | Detail |

|---|---|

| Minimum Authorized Share Capital | No statutory minimum |

| Maximum Authorized Share Capital | No statutory maximum |

| Minimum Paid-Up Capital | No statutory minimum (JPY 1 technically permissible) |

| Paid-Up Requirement at Incorporation | Full payment of subscribed shares required before registration |

| Accepted Currency | Japanese Yen (JPY); foreign currency permissible if converted |

| Accepted Forms of Contribution | Cash; non-cash contributions (property, IP) permitted subject to valuation rules under the Companies Act |

| Timeframe to Deposit Capital | Prior to filing registration with the Legal Affairs Bureau |

No statutory minimum does not mean capital structure is optional. The authorized share capital and issued shares must still be defined in the teikan, and the paid-up amount must be documented through a bank deposit confirmation before the Legal Affairs Bureau will process the incorporation filing.

Company Secretary Requirements in Japan

Under the Companies Act of Japan, a company secretary in the Western corporate sense is not a statutory requirement for a Kabushiki Kaisha (KK) or a Godo Kaisha (GK). Japan company secretary requirements differ from common law jurisdictions; the compliance and administrative functions typically assigned to a corporate secretary are instead distributed among directors and statutory auditors (kansayaku).

Certain larger KK entities, particularly those with a board of directors and a statutory audit structure, must appoint kansayaku to oversee director conduct and financial reporting. For your business, understanding who may fill supervisory and representative roles is relevant to Japan KK secretary compliance.

Qualification criteria for individuals or entities serving in a supervisory or representative capacity:

- Must be a natural person; corporations cannot serve as a statutory auditor (kansayaku)

- No Japanese residency requirement applies specifically to statutory auditors

- Cannot simultaneously serve as a director, employee, or accounting advisor of the same entity

- Must not fall within the disqualification grounds listed under the Companies Act, including prior bankruptcy or criminal convictions

- No mandatory professional licensing is required to serve as a statutory auditor

Incorporate a Company in Japan

Set up your Kabushiki Kaisha or Godo Kaisha in Japan with end-to-end support across registration, documentation, and statutory compliance.

Registered Office Requirements in Japan

Japan registered office requirements mandate that every Kabushiki Kaisha (KK) or Godo Kaisha (GK) maintain a honsha, or principal office address, within the country, which serves as the entity's official point of contact for all legal and regulatory correspondence.

- A physical address in Japan is required; P.O. boxes are not accepted as a registered office.

- Virtual office addresses are permitted, provided they correspond to a real, identifiable location.

- The address must be situated within Japan; foreign addresses do not satisfy the honsha requirement.

- Proof of occupancy, such as a lease agreement or property ownership document, is typically required to support the registered address.

- The registered address is publicly listed on the Commercial Register maintained by the Legal Affairs Bureau under the Ministry of Justice.

- Any change to the registered address must be formally reported to the relevant Legal Affairs Bureau within two weeks, as required under the Companies Act.

- Failure to maintain a valid registered address or to update it within the prescribed period can result in administrative penalties under the Companies Act, including fines of up to JPY 1,000,000 for non-compliant filings.

Director Requirements in Japan

Upon appointment, directors of a Kabushiki Kaisha (KK) assume statutory duties under the Companies Act (Kaisha-ho), including the duty of care of a prudent manager and a duty of loyalty to the company. Breach of these obligations can result in personal liability for damages caused to the entity or third parties.

| Parameter | Detail |

|---|---|

| Minimum Number of Directors | One director is required for a KK without a Board of Directors; three directors are required if a Board of Directors is established. |

| Maximum Number of Directors | No statutory maximum is prescribed under the Companies Act. |

| Local/Resident Director Required | No statutory residency requirement exists, though a representative director must have a registered address in Japan for service of process purposes in practice. |

| Nationality Restrictions | No nationality restrictions apply to directors under Japanese corporate law. |

| Minimum Age Requirement | Directors must be at least 18 years of age under the Companies Act. |

| Corporate Directors Permitted | Corporate directors are not permitted; only natural persons may serve as directors of a KK. |

| Director Must Be a Shareholder | No requirement exists for directors to hold shares in the company. |

| Publicly Listed on Registry | Directors' names and representative director details are recorded in the Commercial Registry (Shogyou Touki) and are publicly accessible. |

| Disqualification Conditions | Persons who have been sentenced to imprisonment for violations of the Companies Act, or who have been declared bankrupt without reinstatement, are disqualified from serving as directors. |

Unlike many jurisdictions, Japan does not require even one locally resident director by statute — yet foreign-only director structures can create significant practical barriers with banks and local authorities during account opening and licensing procedures.

Shareholder Requirements in Japan

Under the Companies Act (Kaisha-ho), a Kabushiki Kaisha (KK) requires at least one shareholder, with no statutory maximum. A sole shareholder structure is fully permitted, allowing a single individual or entity to hold all issued shares.

Nationality and Residency Restrictions

Japan imposes no nationality or residency requirements on shareholders. Foreign individuals and foreign-incorporated entities may hold shares without restriction on ownership percentage, subject to sector-specific foreign investment rules under the Foreign Exchange and Foreign Trade Act (FEFTA).

Corporate Shareholders

Corporate entities are permitted to act as shareholders in a KK. No additional conditions are attached solely on the basis of the shareholder being a legal entity rather than a natural person.

Shareholder Liability

Shareholder liability is limited to the amount of each shareholder's capital contribution. The Kaisha-ho does not generally extend personal liability beyond that subscribed amount except in cases of abuse of the corporate form.

Register of Shareholders

A KK must maintain a register of shareholders (kabunushi meibo) at its registered office. This register is not publicly accessible, though shareholders and creditors may inspect it under prescribed conditions set out in the Companies Act.

Guidance on Shareholder Structuring for Your Japan Incorporation

Get clarity on how shareholder rules under the Companies Act apply to your specific structure, whether you are setting up as a sole shareholder or with multiple corporate investors.

UBO / Beneficial Ownership Disclosure Requirements in Japan

Japan beneficial ownership disclosure requirements are governed primarily by the Act on Prevention of Transfer of Criminal Proceeds and supplemented by guidance from the Financial Services Agency (FSA) and the National Tax Agency (NTA). A beneficial owner is generally defined as a natural person holding 25% or more of the voting rights in a corporation.

- Identify all natural persons who directly or indirectly hold 25% or more of the voting rights in the entity.

- Record beneficial ownership information in the corporate register maintained internally by the company.

- Submit beneficial ownership details to the Japan Legal Affairs Bureau at the time of incorporation via the commercial registration process.

- Report any subsequent changes to the Legal Affairs Bureau within the applicable statutory timeframe.

| Parameter | Detail |

|---|---|

| Ownership Threshold for UBO Status | 25% of voting rights |

| Filing Authority | Japan Legal Affairs Bureau |

| Disclosure Deadline at Incorporation | At time of commercial registration |

| Publicly Accessible Register | No statutory public register |

| Penalties for Non-Disclosure | Administrative penalties may apply under the Act on Prevention of Transfer of Criminal Proceeds |

| Ongoing Update Obligation | Required upon material changes to ownership structure |

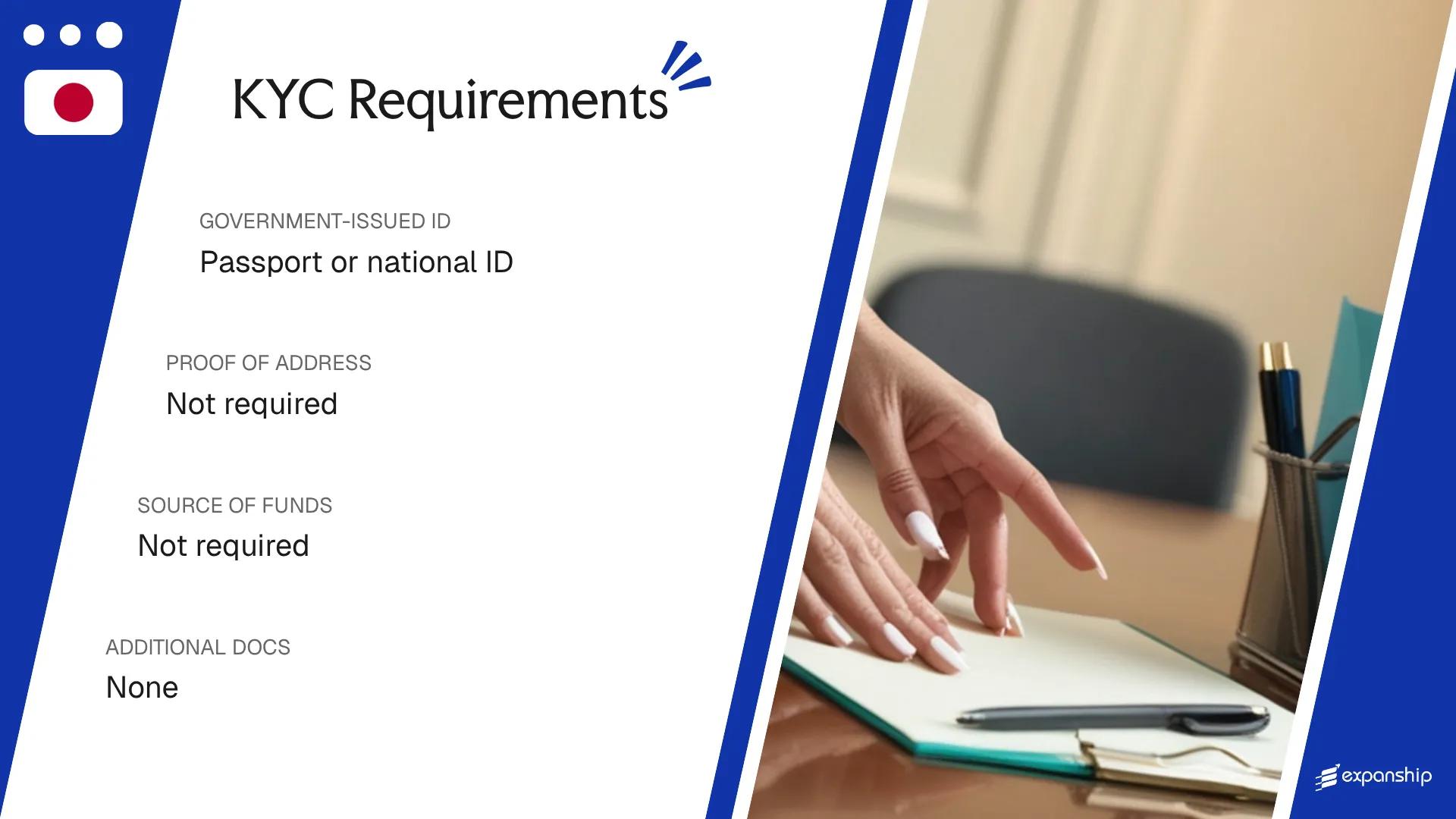

KYC / Document Requirements in Japan

Japan KYC document requirements for incorporation are governed by the Act on Prevention of Transfer of Criminal Proceeds, administered by the Financial Intelligence Unit under the National Police Agency. Notaries and registered agents involved in company formation are subject to due diligence obligations under this framework before a Kabushiki Kaisha or Godo Kaisha can be established.

Individual / Personal Documents

- Valid government-issued photo identification, such as a passport or My Number card, for each director and shareholder

- Proof of residential address dated within three months, such as a utility bill or resident certificate (juminhyo)

- In the case of foreign nationals, a copy of their residence card if residing in Japan

Corporate Documents

- Certificate of incorporation or equivalent constitutional document for any corporate shareholder or director

- Register of directors or equivalent officer list from the corporate entity's home jurisdiction

- Proof of the corporate entity's registered address, such as an official registration extract

Source of Funds Documentation

- Bank statements covering a minimum of three to six months evidencing the origin of contributed capital

- Audited financial statements where the subscribing entity is a corporate body

- A written declaration of the source of funds may be required where bank records are insufficient

Notarisation and Apostille Requirements

- Foreign public documents must be apostilled under the Hague Convention, which Japan acceded to in 2023

- Documents not in Japanese require a certified translation prepared by a sworn translator

- Notarisation by a Japanese notary (koshonin) is required for the articles of incorporation of a Kabushiki Kaisha prior to registration

Incorporation filings are commonly delayed when foreign-issued identity documents are submitted without a certified Japanese translation.

Company Name Requirements in Japan

Japan company name requirements are assessed at the point of registration through the Legal Affairs Bureau, which examines proposed names against existing registrations in the same municipality and business category. Names that are identical or closely similar to an already-registered entity in the same locality may be rejected.

All Kabushiki Kaisha must include the suffix "株式会社" (Kabushiki Kaisha) either preceding or following the trade name. The name must be written in kanji, hiragana, katakana, or Roman letters, and certain symbols are permitted within defined parameters.

Certain words are restricted or require regulatory pre-approval before the Legal Affairs Bureau will accept the registration. Terms implying a government affiliation, financial licensing, or a regulated profession fall into this category.

Formal name reservation is not a standard feature of the Japanese corporate registration process. Applicants generally proceed directly to incorporation filing, meaning the name is secured only upon successful registration with the Legal Affairs Bureau.

Corporate Compliance Services in Japan

Maintain good standing with Japanese regulatory requirements, from annual filings to ongoing statutory obligations.

Conclusion

Japan company incorporation requirements span several distinct legal obligations, from the structure of a Kabushiki Kaisha or Godo Kaisha to director residency rules and registered office provisions under the Companies Act. The requirement for at least one resident representative director remains one of the most consequential constraints for foreign investors. Share capital, while technically flexible, still carries practical implications for corporate credibility. Once these requirements are understood, the operational work of entity setup, document notarisation, and filing with the Legal Affairs Bureau can proceed in a structured sequence.

Expanship's Corporate Formation Services in Japan

Japan's incorporation framework, from the Kabushiki Kaisha structure to beneficial ownership registration under the amended Companies Act, involves specific procedural steps that require careful coordination with the Legal Affairs Bureau and relevant local authorities. Expanship's Japan corporate formation services are structured to help your business meet these requirements without absorbing the full administrative burden in-house. Our team manages the process methodically, so your entity reaches operational status on schedule.

Beyond initial registration, Expanship supports your business across the full incorporation lifecycle:

- We prepare and file all company registration documents with the Legal Affairs Bureau on your behalf.

- Our team provides a registered agent and compliant office address in Japan.

- We handle all government filings and liaise directly with relevant regulatory bodies.

- Post-incorporation compliance obligations are managed on an ongoing basis.

- We facilitate introductions to banking partners suited to your business type.

- Tax registration and liaison with local tax authorities are coordinated as part of your setup.

To discuss your requirements, contact Expanship Japan.

Frequently Asked Questions (FAQ)

A foreign non-resident can serve as a representative director of a KK following a 2015 amendment that removed the earlier requirement for at least one representative director to be a Japan resident. The change does not eliminate practical complications: executing the required personal seal registration (inkan tōroku) and obtaining a certificate of registered seal (inkan shōmeisho) from outside Japan involves consular procedures that add time to the incorporation process. Corporate bank account opening may also be more difficult when no director holds Japanese residency.

Any change to a KK's registered office address must be filed with the Legal Affairs Bureau (Hōmu-kyoku) within two weeks of the change under the Companies Act. Failure to update the register on time exposes the company to a non-compliance fine of up to ¥1 million under Article 976. Prolonged non-compliance can also affect the entity's good standing, which is a requirement for contract execution and regulatory filings with bodies such as the National Tax Agency.

Japan introduced beneficial ownership disclosure obligations primarily through anti-money laundering frameworks rather than a centralised public UBO register. Financial institutions are required under the Act on Prevention of Transfer of Criminal Proceeds to verify and record the beneficial owners of corporate customers, and non-compliance by those institutions carries regulatory sanctions. For the company itself, providing false ownership information during customer due diligence processes can constitute a criminal offence under the same Act.

The Companies Act prohibits names that suggest a different type of entity — for example, a KK cannot include terms implying it is a Godo Kaisha (GK) or a bank without the appropriate licence. Names must be registered in characters compatible with the Commercial Register, meaning kanji, hiragana, katakana, or accepted Roman alphabet characters. Using a purely foreign-language name that cannot be rendered in these scripts is not permissible for registration purposes, though a trade name used in commerce can differ from the registered legal name.

Yes, the documentary requirements differ materially. Individual shareholders must provide identity documents such as a passport and proof of address, whereas corporate shareholders must supply certified copies of their constitutional documents — typically articles of incorporation or equivalent — along with evidence of the authorised signatory's identity. Where a corporate shareholder is incorporated outside Japan, documents generally require apostille certification or notarisation, and Japanese-language translations prepared by a certified translator are required for submission to the Legal Affairs Bureau.

A single-shareholder KK is permitted under the Companies Act, and there is no legal requirement for that shareholder to also act as director. The roles can be separated, with a third party appointed as director, provided the minimum director requirements for the chosen governance structure are met. For a non-publicly traded KK, a single director is sufficient, so a sole shareholder could appoint one unrelated individual to fulfil that requirement without taking on any directorial responsibility personally.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.