Key Takeaways

- The S.r.l. is Italy's most commonly registered entity type, offering single-member eligibility and accessible minimum capital requirements under the Codice Civile.

- Company registration in Italy is administered through local Chambers of Commerce (Camere di Commercio) via the Registro delle Imprese, under oversight of the Ministry of Enterprises and Made in Italy (MIMIT).

- Resident entities in Italy are subject to worldwide income taxation, governed by the Agenzia delle Entrate.

- Structures such as the S.n.c. and S.a.s. involve personal liability for at least some partners, making them best suited to closely held operations that accept that exposure in exchange for simpler administration.

Introduction to Entity Types in Italy

Italy is a founding member of the European Union and sits at the heart of southern Europe, sharing land borders with France, Switzerland, Austria, and Slovenia, with coastlines along the Mediterranean, Adriatic, and Tyrrhenian seas. Choosing among the types of business entities in Italy requires an understanding of how the Italian civil legal system classifies commercial structures — each carrying distinct liability, governance, and fiscal implications.

Company registration falls under the authority of the Registro delle Imprese (Business Register), administered through the local Chambers of Commerce (Camere di Commercio) under oversight of the Ministry of Enterprises and Made in Italy (MIMIT). Tax residency and corporate taxation are governed by the Agenzia delle Entrate, operating within a worldwide income taxation framework for resident entities.

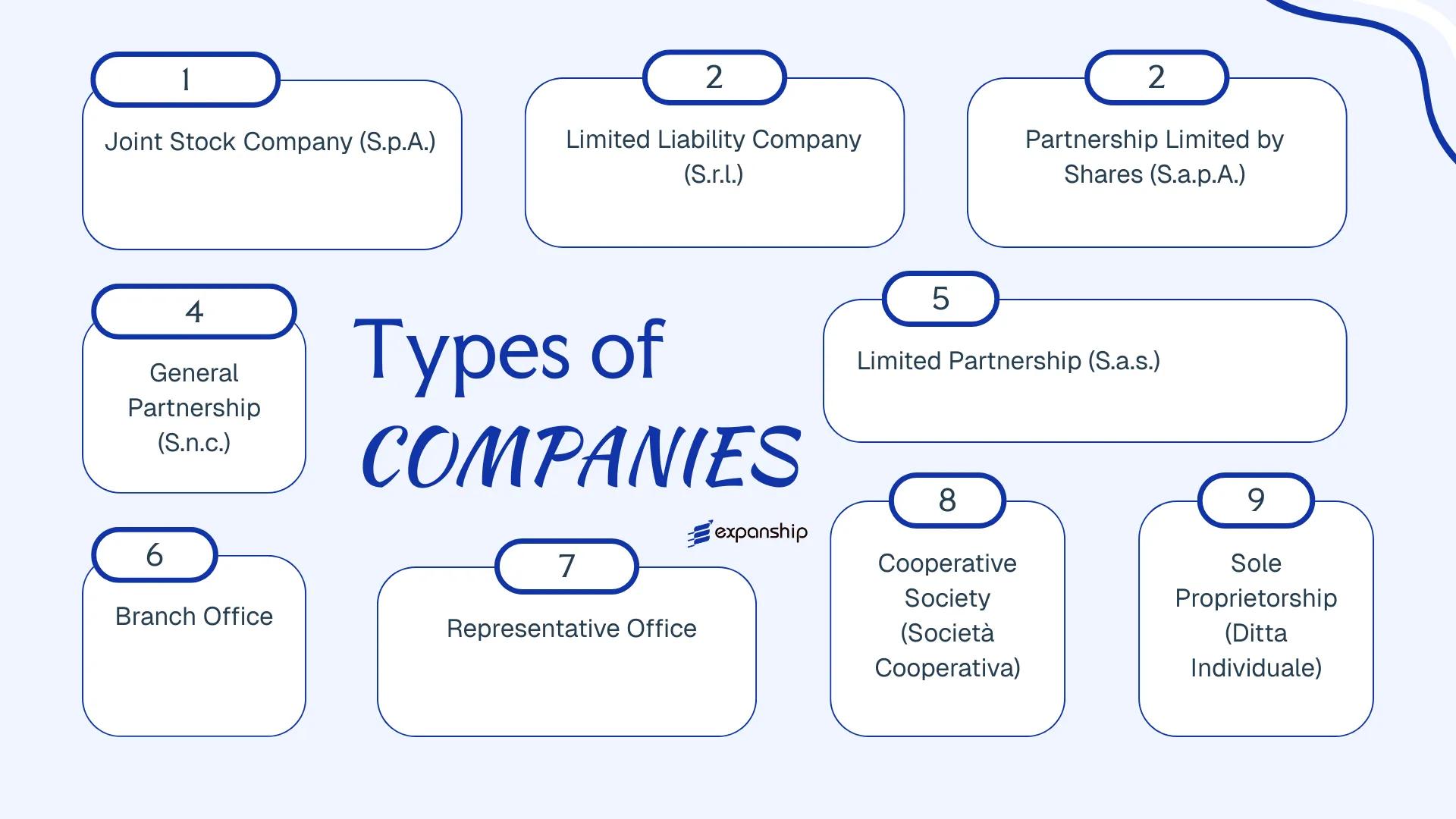

The legal structures available to foreign and domestic investors include the Società per Azioni (S.p.A.), Società a Responsabilità Limitata (S.r.l.), Società in Accomandita per Azioni (S.a.p.A.), Società in Nome Collettivo (S.n.c.), Società in Accomandita Semplice (S.a.s.), Società Cooperativa, Ditta Individuale, branch offices, and representative offices. Each of these structures is examined in detail across the sections that follow.

An Overview of Business Structures in Italy

Italian company law provides several distinct entity types, each governed primarily by the Codice Civile (Civil Code), with supplementary rules established under Legislative Decree No. 6 of 2003, which carried out a substantial reform of corporate law. The Registro delle Imprese (Business Register), maintained by the local Chambers of Commerce under the supervision of the Unioncamere, serves as the central registry for all commercial entities. Each structure carries its own liability profile, capital requirements, and governance framework.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxation | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| S.p.A. | Corporation | Limited | Corporate (IRES/IRAP) | Yes | 1 shareholder | Registro delle Imprese | Codice Civile |

| S.r.l. | LLC | Limited | Corporate (IRES/IRAP) | Yes | 1 member | Registro delle Imprese | Codice Civile |

| S.r.l.s. | Simplified LLC | Limited | Corporate (IRES/IRAP) | Yes | 1 member | Registro delle Imprese | Codice Civile |

| S.a.p.A. | Partnership/Shares | Mixed | Corporate (IRES/IRAP) | Yes | 2 partners | Registro delle Imprese | Codice Civile |

| S.n.c. | General Partnership | Unlimited | Pass-through (IRPEF) | Yes | 2 partners | Registro delle Imprese | Codice Civile |

| S.a.s. | Limited Partnership | Mixed | Pass-through (IRPEF) | Yes | 2 partners | Registro delle Imprese | Codice Civile |

| Branch Office | Foreign Entity Extension | Parent liable | Corporate (IRES/IRAP) | Yes | N/A | Registro delle Imprese | Codice Civile |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | No | N/A | Registro delle Imprese | Codice Civile |

| Società Cooperativa | Cooperative | Limited | Partial exemptions apply | Yes | 3 members minimum | Registro delle Imprese | Codice Civile |

| Ditta Individuale | Sole Proprietorship | Unlimited | Personal (IRPEF) | Yes | 1 individual | Registro delle Imprese | Codice Civile |

Each of these structures is examined in full in the sections below.

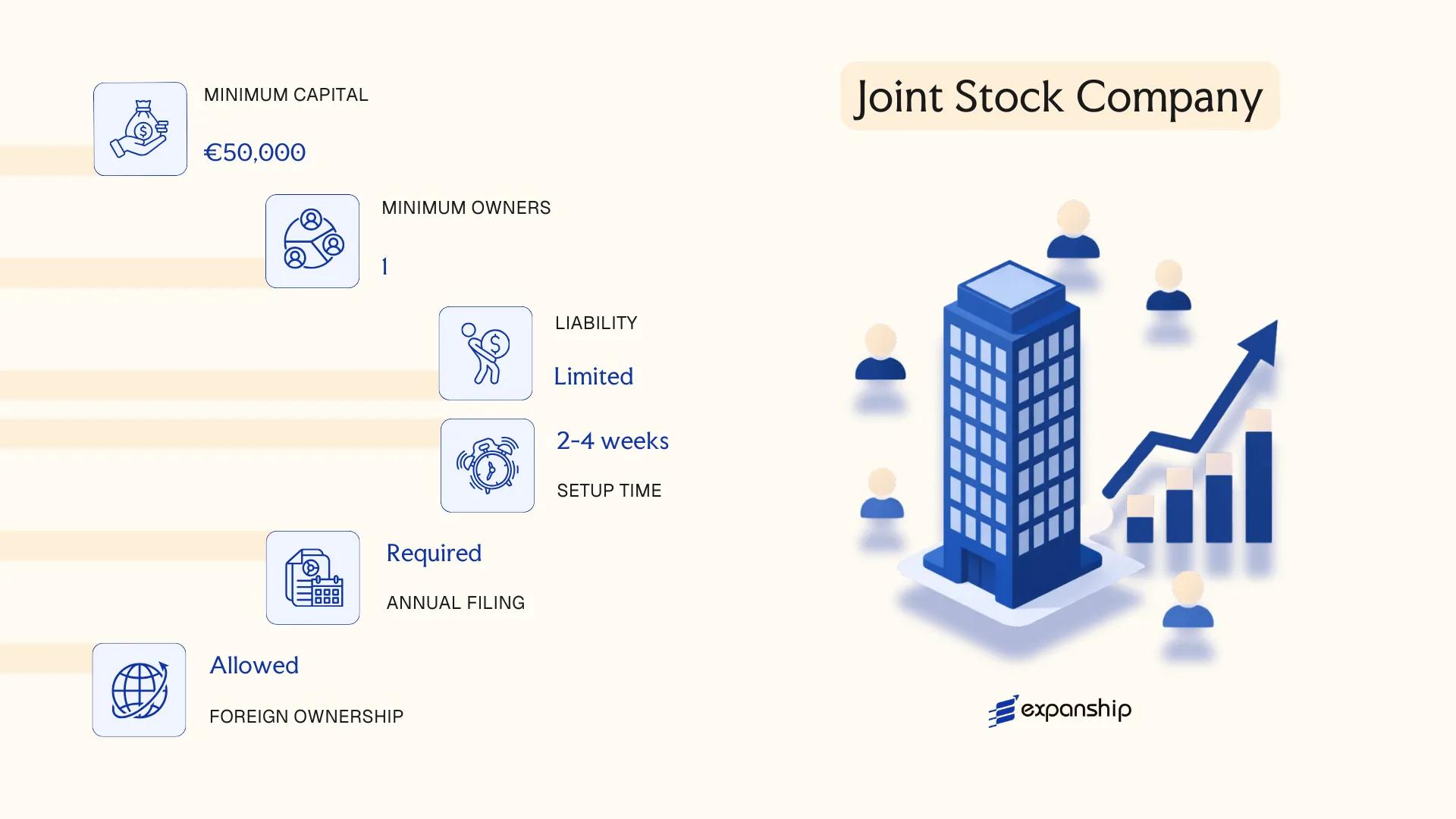

Società per Azioni (S.p.A.) — Joint Stock Company

The Società per Azioni is governed primarily by the Italian Civil Code (Codice Civile), specifically Articles 2325–2451, introduced in its modern form through legislative reform in 2003. As a distinct legal entity, the S.p.A. carries full separate legal personality, meaning the company's assets and liabilities are entirely its own.

Shareholders bear no personal liability beyond their subscribed capital. Share capital is divided into transferable shares, making this structure suitable for businesses seeking external investment or eventual public listing on regulated markets such as Euronext Milan.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company | Separate legal personality; governed by Articles 2325–2451 of the Codice Civile |

| Members | Shareholders (minimum 1; no maximum) | A sole shareholder S.p.A. is permitted; full liability applies to the sole shareholder if formalities are not observed |

| Governance | Board of Directors (Consiglio di Amministrazione) or Sole Director; Statutory Auditors (Collegio Sindacale) | A Collegio Sindacale is mandatory once certain size thresholds are met |

| Local Presence | Registered office (sede legale) in Italy required | No mandatory local director requirement, though a local registered address is compulsory |

| Capital | EUR 50,000 minimum; at least 25% paid-up at incorporation | Shares may be issued in multiple classes with different rights |

| Privacy | Shareholder and director details filed with the Registro delle Imprese | Beneficial ownership disclosed to the UBO Register (Titolari Effettivi) |

Focus Points

- Taxation: Corporate income tax (IRES) applies at 24%, a regional production tax (IRAP) at approximately 3.9% (variable by region), VAT (IVA) at a standard 22%, and withholding taxes apply to dividends, interest, and royalties paid abroad, subject to applicable EU Directives or tax treaties.

- Annual Compliance: Mandatory filing of audited financial statements with the Registro delle Imprese; statutory audit required when size thresholds under Article 2477 are exceeded.

- Treaty Access: Italy maintains an extensive double taxation treaty network; the S.p.A. qualifies as a resident entity for treaty purposes under standard residenza fiscale rules.

- Conversion: An S.p.A. may be converted into an S.r.l. or other permitted forms through a notarial deed (atto notarile) and registration with the Registro delle Imprese, subject to creditor protection rules.

- Public Offering: Only an S.p.A. (not an S.r.l.) may issue shares to the public or list on a regulated exchange under CONSOB oversight.

Sub-Types

Listed S.p.A. (Società Quotata)

A listed S.p.A. has its shares admitted to trading on a regulated market, subjecting it to additional CONSOB regulations, continuous disclosure obligations, and shareholder rights rules under the Testo Unico della Finanza (Legislative Decree 58/1998).

S.p.A. with Employee Participation (S.p.A. con Partecipazione dei Lavoratori)

Permitted under Article 2349 of the Codice Civile, this variant allows the issuance of special shares or financial instruments to employees, typically used by larger industrial groups seeking to structure profit-sharing or incentive arrangements at the equity level.

The S.p.A. is commonly used for holding structures, capital-intensive trading operations, and businesses targeting institutional investors or a public market listing. Its principal advantage is unrestricted share transferability and access to equity capital markets; the main drawback is the comparatively high administrative burden, including mandatory auditing and Collegio Sindacale requirements once size thresholds are crossed.

The S.p.A. is best suited for larger businesses, joint ventures with multiple institutional investors, or any company planning a public offering or regulated market listing in Italy.

Company Incorporation in Italy

Incorporate an S.p.A. or other Italian entity with end-to-end support from registered office setup to *Registro delle Imprese* filings.

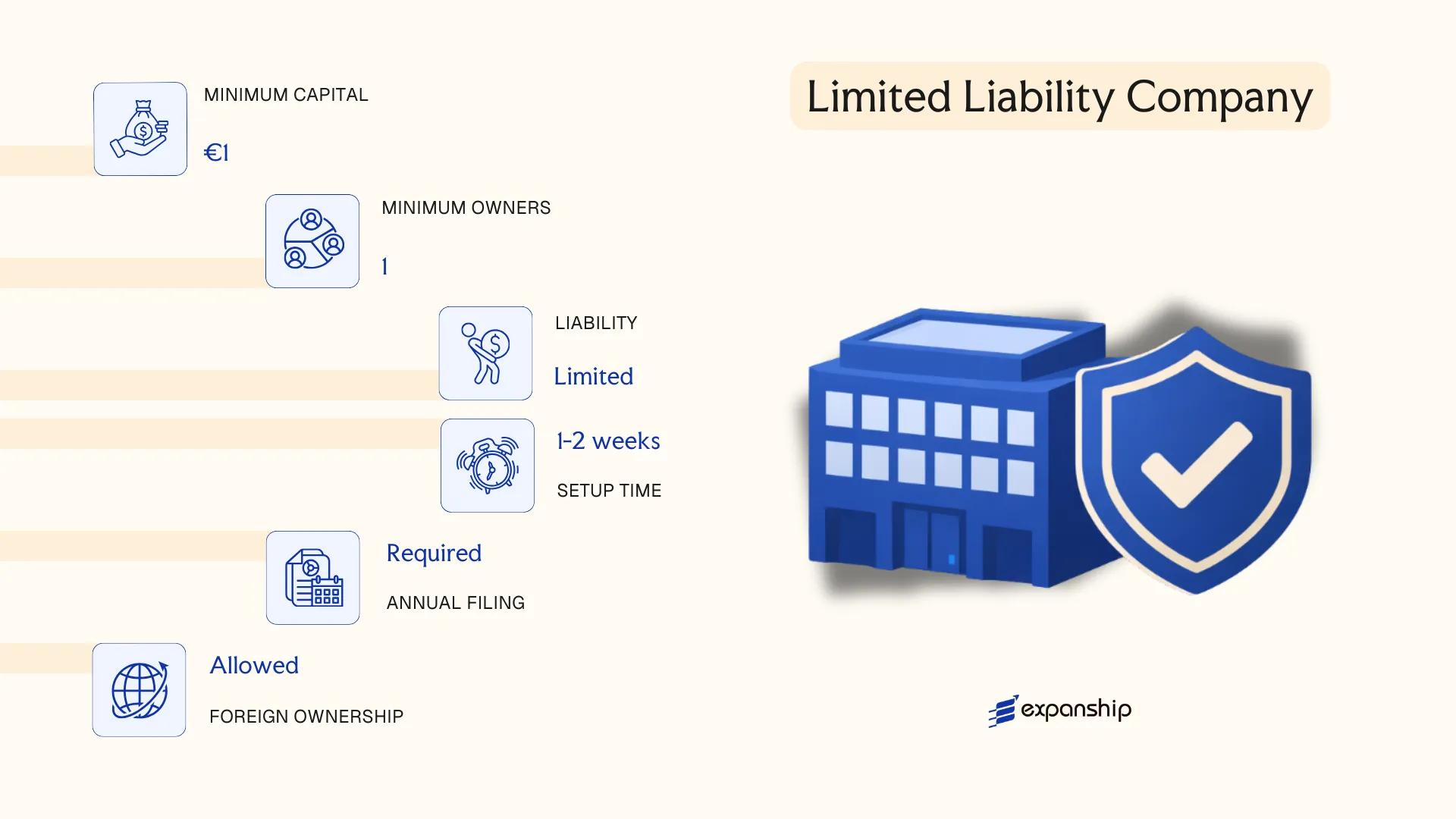

Società a Responsabilità Limitata (S.r.l.) — Limited Liability Company

The Società a Responsabilità Limitata is governed primarily by Articles 2462–2483 of the Italian Civil Code, as substantially reformed by Legislative Decree No. 6 of 2003. As a distinct legal entity, the S.r.l. separates the personal assets of its members from the company's liabilities, making it the most widely used corporate structure for small and medium-sized enterprises in the country.

Unlike the S.p.A., the S.r.l. issues quotas rather than freely transferable shares, giving members tighter control over ownership changes. Quota transfers are recorded in the Companies Register (Registro delle Imprese) held by the local Chamber of Commerce, rather than through a public market. This structural feature makes the Srl company formation Italy process more straightforward and less costly than a joint stock company.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Società a Responsabilità Limitata (S.r.l.) | Separate legal personality; limited liability |

| Members | Referred to as "Soci" (Quota Holders) | Minimum 1 (Unipersonale); no statutory maximum |

| Management | Administered by one or more "Amministratori" (Directors) | Can be members or external appointees |

| Local Presence | Registered office (sede legale) required in Italy | Must be maintained with the Registro delle Imprese |

| Capital | Minimum €1 (standard); €10,000 for S.r.l. ordinaria | Must be fully paid-up at notarial deed stage if below €10,000 |

| Privacy | Quota holdings and directors are publicly disclosed | Beneficial ownership registered in the UBO Register |

Focus Points

- Taxation: Subject to IRES (corporate income tax) at 24%, IRAP (regional production tax) at approximately 3.9%, and standard VAT at 22%; dividend distributions may attract 26% withholding tax for individual recipients.

- Annual Compliance: Must file annual financial statements with the Registro delle Imprese and hold a members' meeting to approve accounts within 120 days of year-end (or 180 days under certain conditions).

- Economic Substance: No formal economic substance law applies, but Italian tax authorities may apply anti-avoidance provisions under Article 73 of the TUIR (Presidential Decree 917/1986) to entities lacking genuine activity.

- Treaty Access: As a resident entity, the S.r.l. qualifies for Italy's extensive double tax treaty network.

- Conversion: Can be converted into an S.p.A. by notarial deed, subject to meeting the higher capital and governance requirements of that form.

Sub-Types

S.r.l. Ordinaria

The standard form, requiring a minimum share capital of €10,000. It is suited to established businesses seeking a conventional limited liability structure with full statutory governance rights.

S.r.l. Semplificata (S.r.l.s.)

Introduced by Law Decree No. 1/2012, this simplified variant allows formation with capital between €1 and €9,999. Articles of association must follow a government-prescribed template, and all quota holders must be natural persons — corporate shareholders are not permitted.

S.r.l. con Socio Unico (Unipersonale)

A single-member variant available to both natural persons and legal entities. Full limited liability is preserved provided the sole member fully pays up the subscribed capital at incorporation; failure to do so results in unlimited personal liability.

The S.r.l. suits trading operations, holding structures, and IP-owning vehicles where ownership control and formation costs matter. Its quota-based structure limits investor transferability compared to a share-issuing entity.

Best suited for small to medium-sized businesses, joint ventures, and entrepreneurs seeking limited liability without the administrative overhead of a listed or widely held company structure.

Società in Accomandita per Azioni (S.a.p.A.) — Partnership Limited by Shares

The Società in Accomandita per Azioni SapA Italy is governed by Articles 2452–2461 of the Italian Civil Code, which apply the S.p.A. regulatory framework to this hybrid structure by reference. It holds separate legal personality, meaning the entity is legally distinct from its members.

Two distinct member classes define its structure: general partners (soci accomandatari), who bear unlimited personal liability and serve as directors by operation of law, and limited partners (soci accomandanti), whose liability is capped at their share subscription. This dual-liability architecture is what distinguishes the SapA from both standard partnerships and capital companies.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Hybrid capital-partnership entity | Governed by Articles 2452–2461, Italian Civil Code |

| Members | Min. 1 general partner (accomandatario) + 1 limited partner (accomandante); no statutory maximum | General partners hold unlimited liability; limited partners are liable only to their subscribed capital |

| Management | General partners act as directors by law | Limited partners cannot perform management acts without assuming unlimited liability |

| Registered Office | Physical registered address in Italy required | Must be filed with the Registro delle Imprese (Companies Register) |

| Share Capital | Minimum €120,000, fully subscribed at incorporation; at least 25% paid up | Shares are transferable; limited partner interests take share form |

| Privacy | General partners disclosed publicly; limited partners listed in the shareholders' register | Both registers accessible via the Registro delle Imprese |

Focus Points

- Taxation: Subject to IRES (corporate income tax) at 24% on net profits; IRAP (regional production tax) at the standard 3.9% rate applies; VAT registration required for commercial activities; withholding tax applies to dividends distributed to non-resident shareholders under standard Italian rules, subject to applicable tax treaty relief.

- Annual Compliance: Annual financial statements must be filed with the Registro delle Imprese; statutory audit requirements follow S.p.A. rules where thresholds are met.

- Conversion: The S.a.p.A. may be converted into an S.p.A. or S.r.l. through a notarial deed and shareholder resolution, subject to Civil Code procedures.

- Restrictions: A limited partner who intervenes in management loses their limited liability status automatically under Article 2460 of the Civil Code.

- Treaty Access: As an Italian-resident entity, the S.a.p.A. can access Italy's tax treaty network, though treaty benefits for pass-through items may require analysis depending on the counterparty jurisdiction's classification of the entity.

General partners cannot be removed without their own consent under the default Civil Code rules, making succession and exit planning structurally complex. This entity suits family-controlled businesses or investment structures where founders wish to retain operational control while raising outside capital through transferable shares.

The S.a.p.A. is best suited for established family businesses or founder-led firms that require access to external capital while maintaining centralised management control among a defined group of principals.

Partnerships [Società in Nome Collettivo (S.n.c.), Società in Accomandita Semplice (S.a.s.)]

Both S.n.c. and S.a.s. partnerships in Italy are governed by the Italian Civil Code (Codice Civile), specifically under Articles 2291–2312 for the S.n.c. and Articles 2313–2324 for the S.a.s. Neither structure carries separate legal personality in the strict sense, though both can hold assets, enter contracts, and sue or be sued under the firm name.

The critical distinction between the two lies in liability. In a Società in Nome Collettivo Italy, all partners bear unlimited joint and several liability for the firm's obligations. The Società in Accomandita Semplice Italy introduces a two-tier membership: accomandatari (managing partners) carry unlimited liability, while accomandanti (silent partners) are liable only up to their contributed capital.

Key Characteristics

| Requirement | S.n.c. Detail | S.a.s. Detail |

|---|---|---|

| Legal Form | General partnership | Limited partnership |

| Members | Partners (soci); minimum 2, no maximum | Min. 1 accomandatario + 1 accomandante; no maximum |

| Liability | All partners: unlimited, joint and several | Accomandatari: unlimited; Accomandanti: limited to capital |

| Registered Office | Required in Italy; registered with the local Chamber of Commerce (Camera di Commercio) | Same requirement applies |

| Capital | No statutory minimum; contributions can be cash, goods, or services | No statutory minimum; accomandante contributions must be defined in the deed |

| Privacy | Partner names and capital contributions disclosed in the business register (Registro delle Imprese) | Same; accomandante names also publicly registered |

Focus Points

- Taxation: Both structures are fiscally transparent — profits pass through to partners and are taxed at the individual level under IRPEF (personal income tax) at progressive rates up to 43%; the firm itself is not subject to IRES (corporate income tax), though IRAP (regional production tax) applies at the entity level.

- Annual Compliance: Annual financial statements must be filed with the Registro delle Imprese; bookkeeping obligations apply under Italian accounting rules.

- Conversion: Either structure can be converted into a capital company (e.g., S.r.l. or S.p.A.) through a notarial deed, subject to creditor protection provisions under the Codice Civile.

- Restrictions: Accomandanti in an S.a.s. who engage in management acts risk losing their limited liability status under Article 2320 of the Codice Civile.

- Treaty Access: As fiscally transparent entities, S.n.c. and S.a.s. firms generally do not independently access Italy's tax treaty network; treaty benefits apply at the partner level based on each partner's residence.

Closing

These structures suit small, closely held businesses — particularly family firms or professional partnerships — where partners accept personal liability in exchange for administrative simplicity and pass-through taxation. The absence of a minimum capital requirement reduces the barrier to entry, though unlimited liability for managing partners represents a material financial exposure.

S.n.c. and S.a.s. partnerships are best suited for small family-owned businesses or professional operators seeking minimal formation requirements and pass-through taxation, where at least one partner is willing to accept unlimited personal liability.

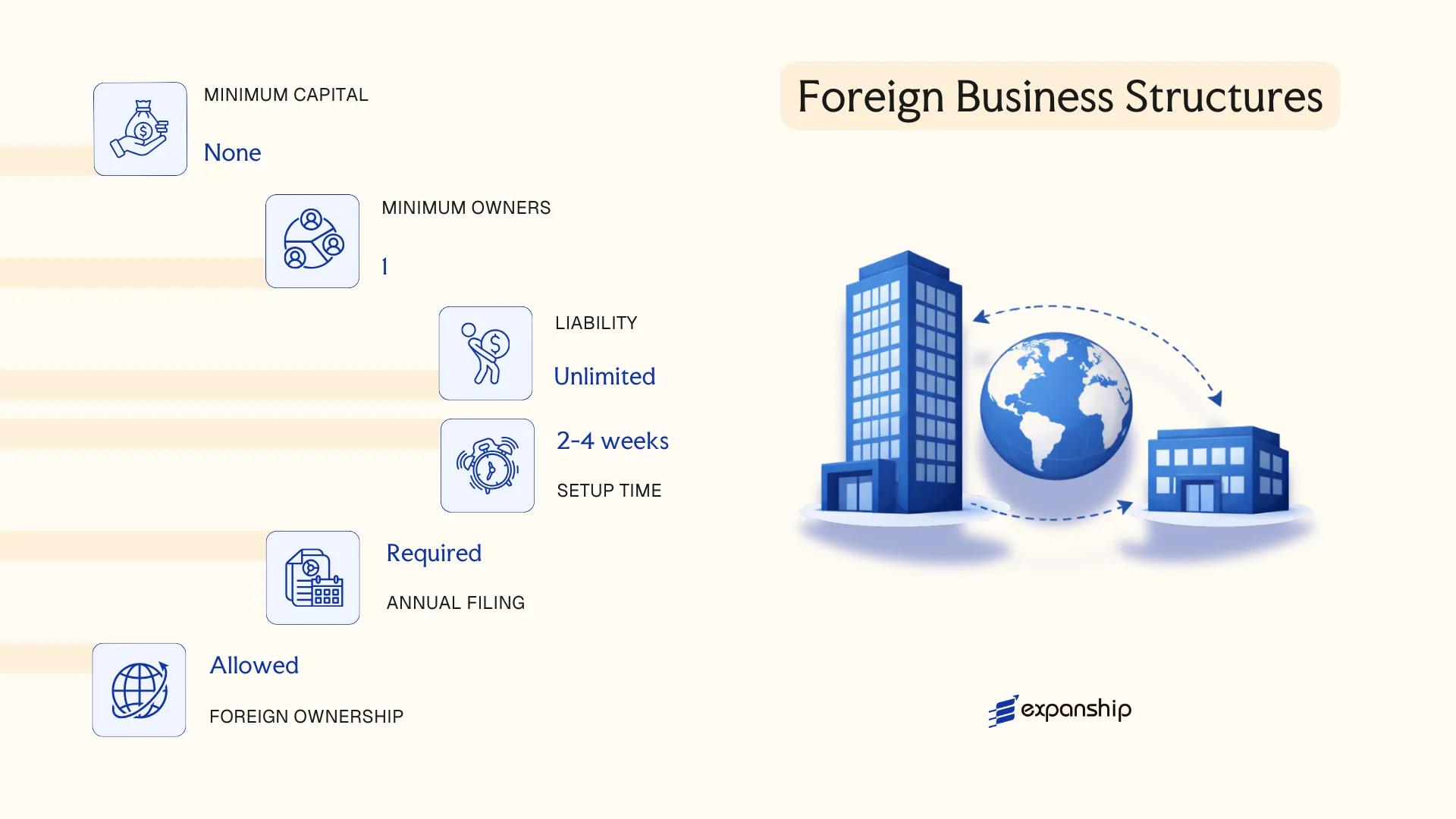

Foreign Business Structures [Branch Office, Representative Office]

Establishing a foreign company branch office in Italy is governed primarily by Articles 2506 and following of the Italian Civil Code, along with the provisions set out in Legislative Decree No. 218/2012 and related commercial registry regulations. A branch office (sede secondaria) is not a separate legal entity — it remains an extension of the foreign parent, which retains full legal personality and bears unlimited liability for the branch's obligations.

A representative office (ufficio di rappresentanza), by contrast, carries no commercial mandate. It cannot generate revenue or enter into contracts on behalf of the parent; its activity is strictly limited to market research, promotional liaison, and preparatory functions.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Designated Representative | Appointed representative (rappresentante) with power of attorney, registered locally | Designated contact person; no commercial authority |

| Local Presence | Registered with the local Chamber of Commerce (Camera di Commercio); physical address required | Physical address required; no Chamber of Commerce registration as a trading entity |

| Capital Requirement | No minimum capital; parent's capital structure applies | None |

| Liability | Parent company bears full liability | Parent company bears full liability |

| Privacy | Representative's details filed in the Business Register (Registro delle Imprese) | Lower disclosure; not registered as a commercial operator |

Focus Points

- Taxation: A branch is treated as a permanent establishment and subject to IRES (corporate income tax) at 24% on Italian-sourced profits, plus IRAP at 3.9%; VAT obligations apply to taxable supplies; a representative office, conducting no commercial activity, generally falls outside the scope of corporate tax and VAT.

- Economic Substance: The branch must maintain genuine operational activity in Italy; the appointed representative must hold documented authority and be contactable at the registered address.

- Annual Compliance: Branches must file annual financial statements with the Registro delle Imprese and submit Italian tax returns; representative offices face minimal reporting obligations.

- Treaty Access: Branch profits may benefit from Italy's double tax treaty network, though treaty entitlement depends on the parent's jurisdiction and treaty terms.

- Restrictions: A representative office cannot invoice clients, hold inventory for sale, or sign commercial contracts — any such activity reclassifies it as a permanent establishment.

Sub-Types

Sede Secondaria (Secondary Registered Office)

This is the standard branch structure used by EU and non-EU companies alike. It requires registration with the Camera di Commercio in the province where it operates and must maintain accounting records separate from the parent's, in accordance with Italian fiscal law.

Ufficio di Rappresentanza (Representative Office)

Distinct from the branch in both function and registration requirements, this structure is suited to foreign firms conducting preliminary market activity without triggering a taxable presence. No commercial transactions may flow through it.

A branch office suits foreign businesses that wish to operate commercially in the Italian market without incorporating a standalone subsidiary, accepting that the parent retains full liability exposure. The primary limitation is that the parent's financial position remains directly at risk for all branch obligations.

Foreign companies testing the Italian market or managing ongoing client relationships without committing to a locally incorporated entity.

Società Cooperativa — Cooperative Society

Governed primarily by Articles 2511–2548 of the Italian Civil Code, alongside Legislative Decree 220/2002 on supervisory oversight, the Società Cooperativa is a member-based entity structured around a principle of mutualistic purpose (scopo mutualistico) rather than profit maximisation. Società Cooperativa Italy registration requires a minimum of nine members in most cases, though a simplified variant permits as few as three.

The entity holds separate legal personality, and member liability is generally limited to the capital subscribed. Its hybrid character stems from the dual function it serves: operating commercially while distributing benefits primarily to its members in proportion to their activity with the cooperative, not solely to capital held.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Società Cooperativa | Separate legal personality; governed by the Civil Code and Legislative Decree 220/2002 |

| Members | Referred to as "soci" (members); minimum 9 (or 3 for small cooperatives); no statutory maximum | Small cooperatives (cooperativa a r.l.) require at least 3 members |

| Governing Body | Board of Directors (Consiglio di Amministrazione) or sole administrator | Supervisory board required for certain larger cooperatives |

| Local Presence | Registered office in Italy; no registered agent requirement | Must register with the Registro delle Imprese at the local Chamber of Commerce |

| Capital | No fixed statutory minimum for cooperatives; shares (azioni or quote) issued at nominal value | Capital varies based on cooperative type; contributions may be in cash or kind |

| Privacy | Member register is publicly accessible via the Registro delle Imprese | Beneficial ownership disclosure required under Legislative Decree 231/2007 |

Focus Points

- Taxation: Subject to IRES (corporate income tax) at 24%, though qualifying cooperatives may benefit from partial IRES exemptions on allocated reserves; VAT (IVA) applies at standard rates; cooperative reserves are partially exempt from taxation if reinvested under mutualistic purposes.

- Annual Compliance: Must file annual financial statements with the Registro delle Imprese; subject to periodic supervisory audits by ministerially authorised supervisory bodies (enti di revisione) such as Legacoop or Confcooperative.

- Economic Substance: Must demonstrate genuine mutualistic activity with members; cooperatives that fail to maintain this purpose risk reclassification and loss of tax benefits.

- Restrictions: At least 30% of net surplus must be allocated to a legal reserve; cooperatives must adhere to the "prevalenza mutualistica" (mutualistic prevalence) rule to retain tax-advantaged status.

Sub-Types

Cooperativa a Mutualità Prevalente (Predominantly Mutualistic Cooperative)

This classification applies when the cooperative conducts the majority of its activity directly with its own members, meeting thresholds defined under Article 2513 of the Civil Code. It qualifies for preferential tax treatment, including partial exemptions on IRES and favourable reserve rules.

Cooperativa Sociale (Social Cooperative)

Established under Law 381/1991, social cooperatives pursue general social interest objectives rather than purely member benefit. Two sub-categories exist: Type A (social and healthcare services) and Type B (work integration for disadvantaged individuals).

The Società Cooperativa suits worker-owned enterprises, agricultural producers, and social service providers where member participation outweighs investor return as the primary objective. The main structural advantage is the partial tax exemption on mutualistic reserves; the primary limitation is the administrative burden of maintaining mutualistic prevalence and mandatory supervisory audit obligations.

This structure is most appropriate for groups of workers, producers, or service users seeking to operate collectively under a formalised legal entity with shared governance and limited personal liability.

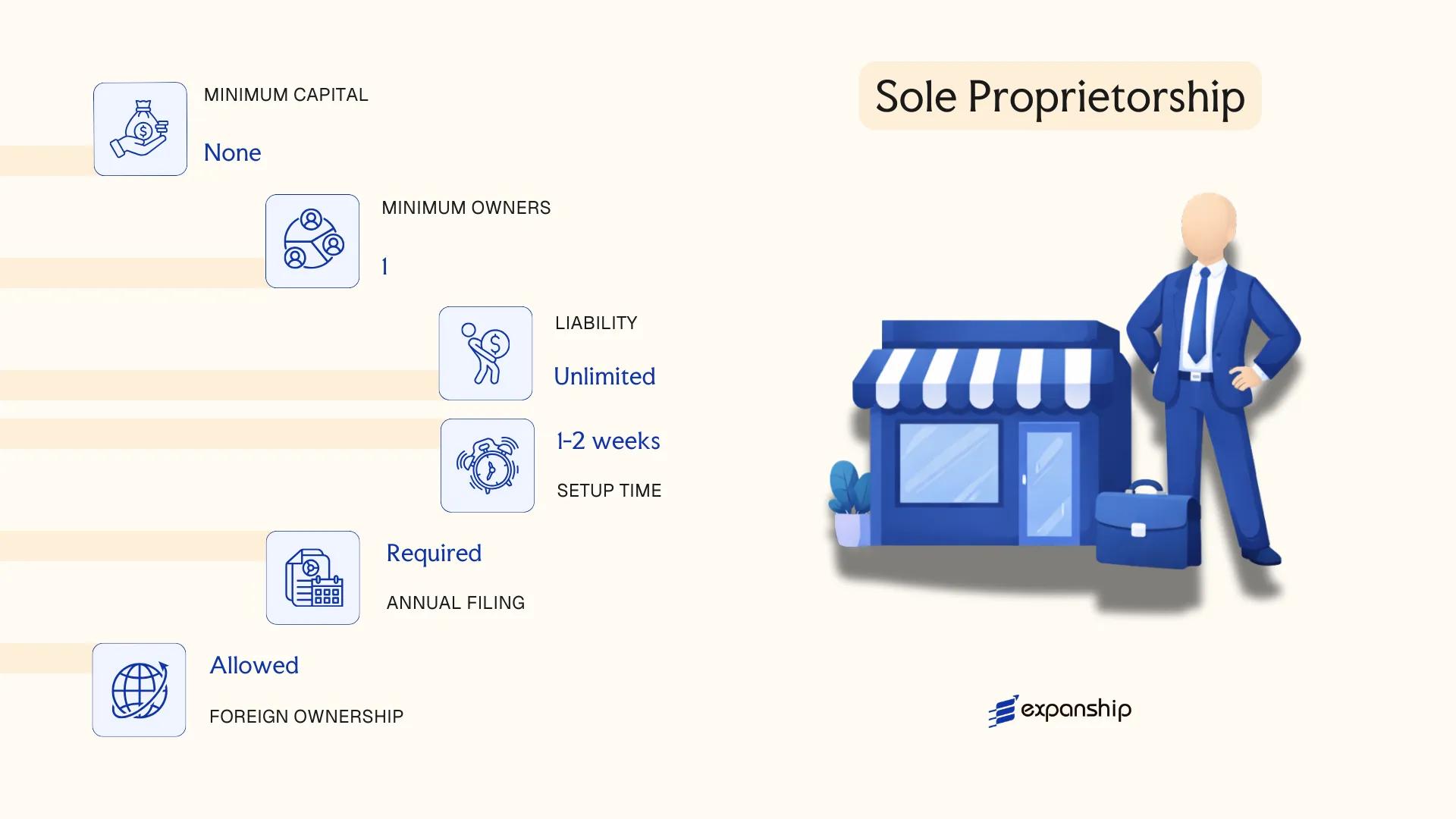

Sole Proprietorship (Ditta Individuale)

The Ditta Individuale sole proprietorship Italy represents the simplest and most accessible business structure available to self-employed individuals. Governed primarily by Articles 2082 and 2195 of the Italian Civil Code, the Ditta Individuale carries no separate legal personality — the proprietor and the business are legally the same entity, meaning personal assets are fully exposed to business liabilities.

Registration is mandatory with the local Camera di Commercio (Chamber of Commerce) through the Registro delle Imprese, and the proprietor must also register with INPS for social contributions. Artisans and craftspeople face an additional requirement to enrol with the Albo delle Imprese Artigiane.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship | No separate legal personality; unlimited personal liability |

| Members | Single proprietor only | No minimum capital requirement |

| Local Presence | Registered business address in Italy | Required for Chamber of Commerce registration |

| Capital | No statutory minimum | Proprietor's personal assets constitute the business base |

| Privacy | Proprietor's name and address publicly registered | Registro delle Imprese records are publicly accessible |

Focus Points

- Taxation: Subject to IRPEF (personal income tax) on a progressive scale up to 43%; a flat-rate regime (regime forfettario) applies at 15% (or 5% for new entrants) if annual revenues remain below set thresholds; VAT registration required unless under the forfettario exemption threshold.

- Social Contributions: Mandatory INPS contributions apply regardless of profit; artisans and merchants contribute to separate INPS gestioni.

- Compliance: Annual tax return filing via Modello Redditi PF; no obligation to file statutory accounts with the Chamber of Commerce.

- Conversion: Can be converted into a corporate entity such as an S.r.l., though the process involves establishing a new legal entity rather than a structural transformation.

- Restrictions: Cannot take on partners or investors without dissolving and re-registering under a different legal form.

Closing

The Ditta Individuale suits freelancers, sole traders, and small-scale operators who require a low-cost, administratively light structure. The principal advantage is minimal setup cost and straightforward sole trader registration in Italy; the clear limitation is unlimited personal liability, which exposes the proprietor's private assets to any business debts or legal claims.

The Ditta Individuale is best suited for individual professionals and small traders operating with limited liability exposure and no immediate need to bring in co-owners or outside capital.

How to Choose the Right Entity Type in Italy

Knowing how to choose a company type in Italy before you begin the registration process prevents structural problems that are difficult and costly to reverse once the entity is active.

Why Your Entity Choice Matters

The structure you register has binding legal and financial consequences.

- Registering a foreign branch without establishing a permanent establishment where one legally exists under Article 162 of the Consolidated Income Tax Act (TUIR) exposes the business to tax assessment, penalties, and potential forced liquidation.

- Selecting an S.r.l. semplificata when your capitalization requirements grow beyond its statutory limits forces a mandatory conversion, triggering additional notarial and registration costs.

- Choosing a partnership structure (S.n.c. or S.a.s.) when unlimited personal liability conflicts with your asset protection requirements leaves partners personally exposed to business debts with no corporate shield.

- Forming an S.p.A. as a single-person consultancy imposes statutory auditor obligations and minimum capital requirements of €50,000 that a sole proprietorship or S.r.l. would not require.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each require distinct entity forms under Italian law.

- Ownership Structure: A single-member S.r.l. suits solo operators, while multi-party ventures requiring governance formality point toward an S.p.A.

- Tax Objectives: Your eligibility for IRES rates, participation exemption, or Italy's patent box regime depends on the entity type you select.

- Liability Exposure: Whether partners or shareholders bear personal liability for company debts determines which structure adequately protects your personal assets.

- Audit and Reporting Requirements: Statutory audit thresholds under the Italian Civil Code vary by entity type and company size, affecting your ongoing compliance costs.

- Exit and Conversion: Not all Italian entities permit straightforward redomiciliation or conversion; verify this before formation under the Civil Code provisions governing transformations.

Compliance Services for Companies in Italy

Maintain statutory obligations, filing deadlines, and regulatory requirements for your Italian entity.

Conclusion

Selecting the right structure is one of the most consequential early decisions in any setting up a company in Italy guide. The S.r.l. remains the most registered entity type in the country, favored by small to mid-sized businesses for its accessible minimum capital and single-member eligibility under the Codice Civile. The S.p.A. suits firms requiring external investment or public capital markets access. Partnerships such as the S.n.c. and S.a.s. fit closely held operations where personal liability is accepted in exchange for simpler administration. The S.a.p.A. serves a narrow use case involving mixed partner structures. Branch offices address foreign firms testing the market without full incorporation.

Regulatorily, Italy continues to refine its digital incorporation procedures and expand its tax treaty network, gradually reducing friction for cross-border structures. Expanship's team works directly within this framework to support your registration from entity selection through post-incorporation compliance.

How Expanship Can Assist You

Expanship Italy company formation services cover the full scope of what this blog has addressed — from registering an S.r.l. or S.p.A. with the Registro delle Imprese to meeting the ongoing obligations overseen by the Agenzia delle Entrate and the relevant Camera di Commercio. Your specific structure determines which filings, capitalization rules, and governance requirements apply, and our team works through those distinctions with you directly.

Across each engagement, we handle the practical steps so your business can proceed without administrative delays:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Filing and liaison with the Registro delle Imprese

- Post-incorporation compliance management

- Corporate tax registration and VAT enrollment

- Banking introduction assistance

Get in touch with Expanship Italy to discuss the right structure for your business and begin the formation process.

Frequently Asked Questions (FAQ)

The Società a Responsabilità Limitata (S.r.l.) is the most frequently incorporated entity. Its relatively low minimum share capital of €10,000, single-member formation option, and limited liability make it the default choice for small and medium-sized businesses across most sectors.

Both structures offer limited liability, but the S.p.A. requires a minimum share capital of €50,000, allows share transfers on public markets, and carries heavier governance obligations, including mandatory board structures under the Italian Civil Code. The S.r.l. restricts quota transfers and cannot issue shares to the public, making it structurally closer to a private holding vehicle. Compliance costs and administrative requirements are notably higher for the S.p.A.

Among Italian structures, the S.r.l. with a sole quotaholder provides the most contained disclosure profile. Beneficial ownership information must still be filed with the Registro delle Imprese under Legislative Decree 231/2007 and anti-money laundering reforms, so complete confidentiality is not achievable. Nominee arrangements are legally permitted but do not override mandatory beneficial ownership reporting.

A sole individual can establish a Ditta Individuale or a single-member S.r.l. without partners. The S.p.A. can technically be formed by one shareholder, though its governance framework requires multiple appointed officers. Partnerships — both the S.n.c. and the S.a.s. — require a minimum of two partners by definition.

Non-Italian nationals can incorporate an S.r.l. or S.p.A. without restrictions on share ownership. A foreign individual typically requires an Italian fiscal code (codice fiscale), issued by the Agenzia delle Entrate, before completing registration at the Registro delle Imprese. Residency in Italy is not a prerequisite for ownership, though a registered office address within the country is mandatory.

Transformation between entity types is governed by Articles 2498 to 2500-novies of the Italian Civil Code. A partnership can convert into a capital company, and an S.r.l. can transform into an S.p.A., provided specific procedural and notarial requirements are met. Cross-type conversions involving cooperatives follow separate rules under the same code.

Capital companies — the S.r.l., S.p.A., and S.a.p.A. — hold full legal personality distinct from their members. General partnerships (S.n.c.) have legal subjectivity but not complete separation of liability, meaning partners remain personally exposed to firm debts. The Ditta Individuale has no separate legal personality at all.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.