Key Takeaways

- The Companies Act, 2013 and the Limited Liability Partnership Act, 2008 form the two primary legislative frameworks governing business entities in India, administered centrally by the Ministry of Corporate Affairs (MCA).

- Among all available structures, the Private Limited Company remains the most commonly incorporated form in India due to its liability protection and compatibility with external investment.

- Foreign entities entering India typically do so through a Wholly Owned Subsidiary or, where operational restrictions apply, a Branch Office registered with the Reserve Bank of India.

- Single-founder businesses in India can incorporate as a One Person Company (OPC), a structure distinct from a sole proprietorship that offers limited liability under the Companies Act, 2013.

Introduction to Entity Types in India

India is a federal republic in South Asia, sharing borders with Pakistan, China, Nepal, Bhutan, Bangladesh, and Myanmar. Structuring a business here means engaging directly with the Ministry of Corporate Affairs (MCA), the central authority responsible for company registration, incorporation filings, and statutory compliance. The MCA administers the Companies Act, 2013, which governs most corporate entities, while the Limited Liability Partnership Act, 2008 covers LLPs separately.

India operates a residence-based tax system with treaty obligations under an extensive network of Double Taxation Avoidance Agreements (DTAAs).

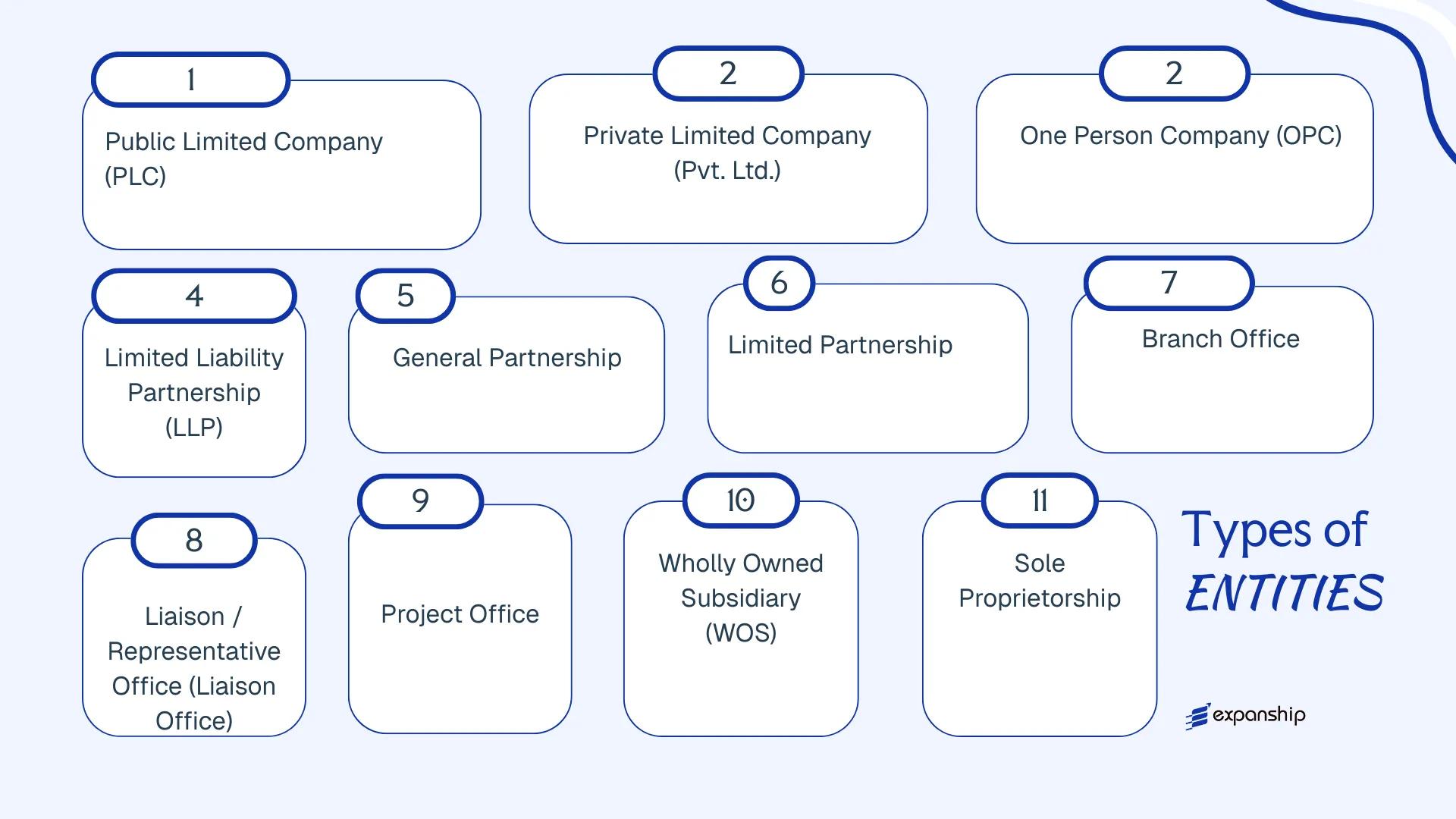

Depending on your objectives, ownership structure, and operational scope, the available entity types are: Private Limited Company, Public Limited Company, One Person Company, Limited Liability Partnership, General Partnership, Limited Partnership, Branch Office, Liaison Office, Project Office, Wholly Owned Subsidiary, and Sole Proprietorship.

Each of the types of business entities in India carries distinct compliance obligations, liability exposure, and capital requirements. This article examines each structure in detail so your business can assess which formation aligns with its legal and commercial requirements.

An Overview of Business Structures in India

Several distinct business structures are available in India, each governed primarily by the Companies Act, 2013, with additional frameworks under the Limited Liability Partnership Act, 2008, the Partnership Act, 1932, and the Foreign Exchange Management Act, 1999 for foreign entities. The Ministry of Corporate Affairs (MCA) administers registration and ongoing compliance for most of these structures. Each entity type carries a different legal form, liability profile, and regulatory obligation.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company | Separate legal entity | Limited | Taxed | Permitted | 7 shareholders | MCA / ROC | Companies Act, 2013 |

| Private Limited Company | Separate legal entity | Limited | Taxed | Permitted | 2 shareholders | MCA / ROC | Companies Act, 2013 |

| One Person Company | Separate legal entity | Limited | Taxed | Permitted | 1 shareholder | MCA / ROC | Companies Act, 2013 |

| Limited Liability Partnership | Hybrid entity | Limited | Taxed | Permitted | 2 partners | MCA / ROC | LLP Act, 2008 |

| General Partnership | Unincorporated firm | Unlimited | Taxed | Permitted | 2 partners | Registrar of Firms | Partnership Act, 1932 |

| Limited Partnership | Unincorporated firm | Mixed | Taxed | Permitted | 2 partners | Registrar of Firms | Partnership Act, 1932 |

| Sole Proprietorship | Unincorporated | Unlimited | Taxed as individual | Permitted | 1 person | No central authority | No single statute |

| Branch Office | Extension of foreign parent | Parent liable | Taxed | Restricted | N/A | RBI / MCA | FEMA, 1999 |

| Liaison Office | Extension of foreign parent | Parent liable | Exempt (no revenue) | Not permitted | N/A | RBI | FEMA, 1999 |

| Project Office | Extension of foreign parent | Parent liable | Taxed | Project-specific | N/A | RBI | FEMA, 1999 |

| Wholly Owned Subsidiary | Separate legal entity | Limited | Taxed | Permitted | 1 shareholder (foreign) | MCA / ROC | Companies Act, 2013 |

Each of these structures is examined in full in the sections below.

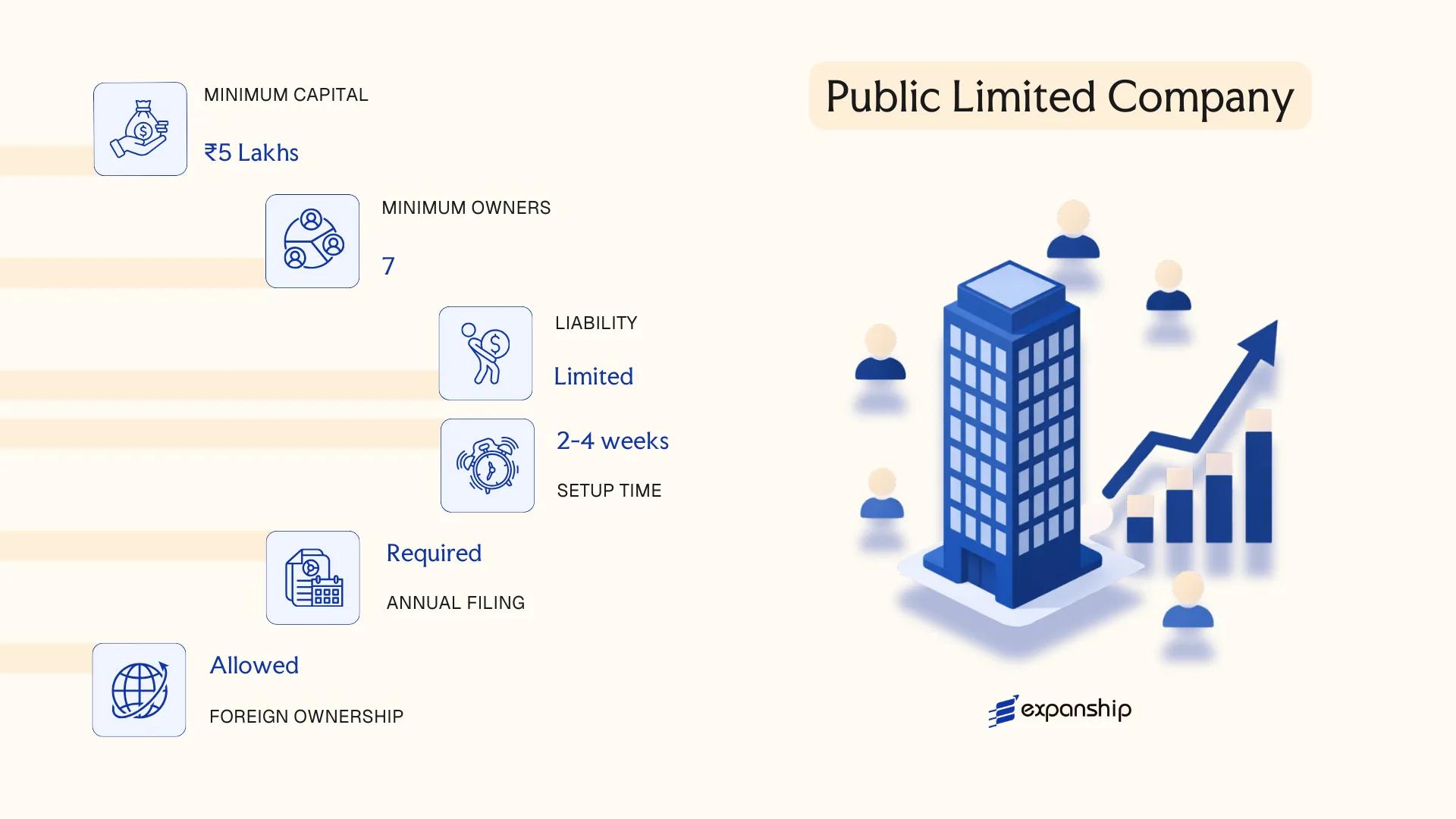

Public Limited Company (PLC)

A public limited company India (PLC) is governed by the Companies Act, 2013, administered by the Ministry of Corporate Affairs (MCA). The entity carries a separate legal personality, meaning its existence is distinct from its shareholders, and liability is limited to each member's unpaid share capital.

Shares in a PLC can be offered to the general public and, subject to Securities and Exchange Board of India (SEBI) regulations, listed on a recognised stock exchange. This makes PLC registration India the preferred route for businesses seeking access to public capital markets.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Company limited by shares | Separate legal entity under the Companies Act, 2013 |

| Members | Shareholders (directors manage; shareholders own) | Minimum 7 shareholders; no maximum. Minimum 3 directors; at least 1 must be a resident director |

| Local Presence | Registered office in India required | Must be maintained throughout the company's existence |

| Share Capital | INR; no statutory minimum paid-up capital | Authorised capital must be stated in the Memorandum of Association |

| Privacy | Financial statements and annual returns are publicly filed with the MCA | Beneficial ownership disclosures required above certain thresholds |

| Listing | Optional; listing requires SEBI compliance | Unlisted PLCs exist and are not subject to full SEBI disclosure requirements |

Focus Points

- Taxation: Subject to corporate income tax (currently 30% for domestic companies, or 22% under the concessional regime under Section 115BAA); GST applies to goods and services; dividend distribution no longer taxed at the company level but taxable in shareholders' hands; withholding tax applies on dividends, interest, and royalties paid to non-residents.

- Annual Compliance: Mandatory filing of financial statements (Form AOC-4) and annual return (Form MGT-7) with the MCA; statutory audit required; AGM must be held within six months of the financial year-end.

- SEBI Obligations: Listed PLCs are subject to SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, including quarterly reporting and corporate governance norms.

- Conversion: A private limited company can convert to a PLC under Section 14 of the Companies Act, 2013 by altering its Articles of Association and meeting the membership thresholds.

- Treaty Access: As a domestic company, a PLC can access India's tax treaty network, subject to principal purpose and beneficial ownership tests.

A PLC suits large enterprises, family conglomerates seeking public listing, or businesses requiring broad equity participation. The primary advantage is unrestricted access to public capital; the primary limitation is the significant ongoing regulatory burden, particularly under SEBI if listed.

Public limited companies are best suited for established businesses targeting public equity markets or those anticipating a large and diverse shareholder base.

Company Incorporation in India

Incorporate a public limited company or any other business structure in India with end-to-end support from Expanship.

Private Limited Company (Pvt. Ltd.)

Governed by the Companies Act, 2013, and administered by the Ministry of Corporate Affairs (MCA), a private limited company India Pvt Ltd structure is one of the most widely used corporate forms for domestic and foreign-owned businesses. The entity holds a separate legal personality from its shareholders, meaning it can own property, enter contracts, and incur liabilities in its own name.

Liability exposure for shareholders is capped at the amount unpaid on their shares. This separation between personal and business assets makes the structure a practical choice for ventures requiring third-party investment or scalable ownership.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate | Incorporated under the Companies Act, 2013 |

| Members | Min. 2 shareholders, max. 200; min. 2 directors, max. 15 | At least one director must be an Indian resident |

| Local Presence | Registered office address required in India | Must be a physical address; P.O. boxes not permitted |

| Share Capital | INR denomination; no statutory minimum paid-up capital | Authorised capital attracts stamp duty on incorporation |

| Share Transferability | Restricted by Articles of Association | Shares cannot be offered to the public |

| Privacy | Financials filed with MCA; publicly accessible via MCA21 portal | Beneficial ownership disclosures required |

Focus Points

- Taxation: Subject to corporate income tax (base rate 22% for domestic companies, 15% for new manufacturing entities under certain conditions); GST applies to taxable supplies; dividend distribution taxed in shareholders' hands; withholding tax applies to payments to non-residents under domestic law or applicable DTAA rates.

- Annual Compliance: Mandatory filing of financial statements (Form AOC-4) and annual return (Form MGT-7) with the Registrar of Companies; statutory audit required each financial year.

- Treaty Access: As a tax resident entity, qualifies for benefits under India's double taxation avoidance agreements (DTAAs), subject to Principal Purpose Test provisions under BEPS-aligned domestic rules.

- Conversion: Can be converted to a public limited company or LLP subject to MCA procedural requirements and creditor/shareholder approvals.

- Foreign Ownership: 100% foreign direct investment permitted in most sectors under the automatic route; certain sectors require prior government approval.

A private limited company suits trading operations, technology ventures, joint ventures, and businesses seeking equity investment. The structure offers credibility with lenders and investors, though it carries ongoing statutory obligations — including mandatory audits and MCA filings — that add administrative overhead compared to lighter structures.

Foreign investors and growth-oriented domestic businesses that require a formal corporate structure capable of accepting equity capital and scaling operations.

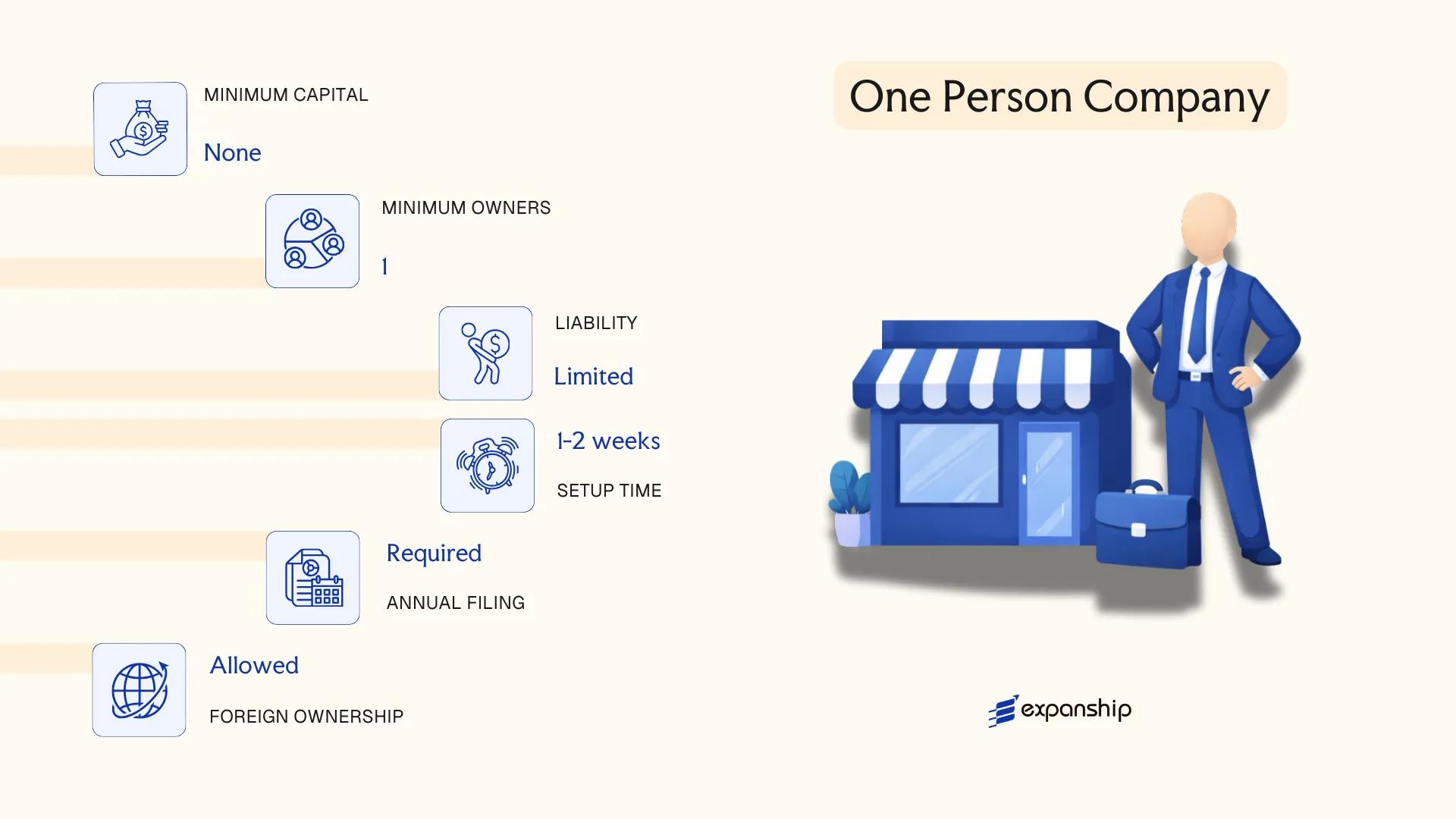

One Person Company (OPC)

Introduced under the Companies Act, 2013, the One Person Company is a distinct legal structure designed for solo entrepreneurs who require a corporate form without partners or co-shareholders. As with a private limited company, an OPC carries separate legal personality, meaning the entity's liabilities do not extend to the personal assets of its sole member beyond unpaid share capital.

One person company India OPC registration is governed by Section 2(62) and Sections 3–11 of the Companies Act, 2013, with the Ministry of Corporate Affairs (MCA) serving as the primary regulatory authority. The structure functions as a hybrid: it combines the operational simplicity associated with sole proprietorship with the liability protection of a corporate entity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Incorporated Company | Separate legal entity under the Companies Act, 2013 |

| Members | 1 Shareholder (nominee required) | Shareholder must be a natural person, Indian resident; nominee activates upon death or incapacity |

| Directors | Minimum 1, Maximum 15 | Sole member may also serve as the sole director |

| Local Presence | Registered office address in India | Required at incorporation; must be maintained throughout |

| Capital | INR; no statutory minimum paid-up capital | Authorised capital governs stamp duty calculations |

| Residency Restriction | Sole member must be an Indian resident | Non-resident Indians and foreign nationals are ineligible to form an OPC |

Focus Points

- Taxation: Subject to corporate income tax at 22% (existing companies under Section 115BAA) or 15% for eligible new manufacturing entities; dividend distribution taxable in the hands of the member; GST applies to applicable supplies; stamp duty on share issuance varies by state.

- Annual Compliance: Mandatory filing of financial statements (Form AOC-4) and annual return (Form MGT-7A) with the MCA; statutory audit required regardless of turnover.

- Conversion: An OPC must mandatorily convert to a private limited company once paid-up capital exceeds INR 50 lakh or average annual turnover exceeds INR 2 crore over three consecutive years.

- Restrictions: Cannot carry out non-banking financial investment activities or issue securities to the public.

- Treaty Access: As a domestic Indian company, an OPC is eligible for benefits under India's tax treaties, subject to beneficial ownership and substance conditions.

Closing

An OPC suits a single founder operating a service, consulting, or small trading business who requires limited liability without bringing in additional shareholders. The structure's primary advantage is enabling full ownership and control within a corporate wrapper; its principal drawback is the mandatory conversion threshold, which limits scalability without a structural change.

An OPC is most appropriate for a resident Indian individual running a small-to-medium business who wants corporate liability protection without the requirement of a second shareholder.

Limited Liability Partnership (LLP)

Governed by the Limited Liability Partnership Act, 2008, an LLP is a distinct legal entity separate from its partners, capable of owning property, entering contracts, and initiating legal proceedings in its own name. The structure combines elements of a traditional partnership with corporate-style limited liability, making it a hybrid form under Indian law.

Registration is handled through the Ministry of Corporate Affairs (MCA) via the MCA21 portal, and the entity receives a unique LLP Identification Number (LLPIN) upon incorporation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate with separate legal personality | Governed by the LLP Act, 2008 |

| Members | Designated Partners and Partners; minimum 2 Designated Partners, no upper limit on total partners | At least 2 Designated Partners must be individuals; one must be an Indian resident |

| Local Presence | Registered office address in India required | Must be capable of receiving official correspondence |

| Capital | No minimum capital requirement; contributions in cash, kind, or intangibles | Contributions defined in the LLP Agreement |

| Privacy | LLP Agreement and financials filed with MCA; publicly accessible | Less privacy than a private company in practice |

Focus Points

- Taxation: Subject to corporate income tax at 30% (plus applicable surcharge and cess); no dividend distribution tax, but distributions may attract tax in partners' hands; subject to Alternate Minimum Tax (AMT) at 18.5%; GST applies to taxable supplies; stamp duty on LLP Agreement varies by state.

- Annual Compliance: Annual return (Form 11) and Statement of Accounts (Form 8) must be filed with the MCA each year; audit required if turnover exceeds ₹40 lakh or contribution exceeds ₹25 lakh.

- Conversion: An LLP can be converted into a private limited company under the Companies Act, 2013, subject to prescribed conditions; a firm or private company can also convert into an LLP.

- Restrictions: Foreign nationals can be partners, but FDI into LLPs is permitted only in sectors where 100% FDI is allowed under the automatic route; LLPs cannot issue equity shares or access public capital markets.

An LLP suits professional services firms, consultancies, and small-to-mid-sized businesses seeking operational flexibility without a complex corporate structure. The absence of a minimum capital requirement and the pass-through-friendly profit distribution are practical advantages; however, the inability to raise equity funding limits growth financing options.

LLPs are best suited for professional partnerships, service-based businesses, and ventures where partners want limited liability without the compliance burden of a full corporate structure.

Partnership Structures [General Partnership, Limited Partnership]

Governed by the Indian Partnership Act 1932, a partnership firm is one of the older business structures available in the country. Crucially, a partnership does not have a separate legal personality — partners are collectively and individually liable for the firm's obligations. Partnership firm registration in India is handled at the state level through the Registrar of Firms, and while registration is technically optional, an unregistered firm cannot file suits to enforce contractual rights.

The firm's existence is tied directly to its partners; dissolution can occur upon the death, insolvency, or exit of a partner unless the partnership deed states otherwise.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated firm | No separate legal personality; partners bear unlimited liability |

| Members | Partners; minimum 2, maximum 20 (general); maximum 10 for banking business | Designated as "Partners" |

| Local Presence | Registered office address within the state of registration | Registration with State Registrar of Firms |

| Capital | No statutory minimum; in INR | Defined in the partnership deed |

| Privacy | Partnership deed filed with Registrar is not publicly accessible | Limited public disclosure compared to companies |

Focus Points

- Taxation: Partnership firms are taxed at a flat 30% plus applicable surcharge and cess; partners' share of profit is exempt from further income tax, but remuneration and interest paid to partners are separately taxable in their hands. Stamp duty applies on the partnership deed.

- Annual Compliance: No mandatory annual filing with the Registrar of Firms post-registration; however, income tax returns must be filed annually.

- Conversion: A partnership firm can be converted into an LLP or a Private Limited Company under prescribed procedures, though the process involves regulatory filings and potential tax implications.

- Restrictions: Foreign nationals cannot ordinarily be partners in a general partnership without prior RBI approval under FEMA regulations.

Sub-Types

General Partnership

All partners share management responsibilities and carry unlimited personal liability for the firm's debts. This structure operates entirely under the Indian Partnership Act 1932 with no distinction between managing and contributing partners.

Limited Partnership

India does not have a formal statutory framework for limited partnerships equivalent to those in common law jurisdictions such as the UK or Singapore. The LLP Act 2008 effectively fills this role, meaning traditional limited partnerships with a mix of general and limited partners have no dedicated legislation in India.

Closing

A general partnership suits small domestic businesses, professional practices, or family-run operations where formality and compliance overhead must be kept low. The absence of separate legal personality is a significant structural limitation for any business expecting third-party investment or contractual exposure.

Small professional practices or family businesses with known, trusted partners operating primarily in a single Indian state.

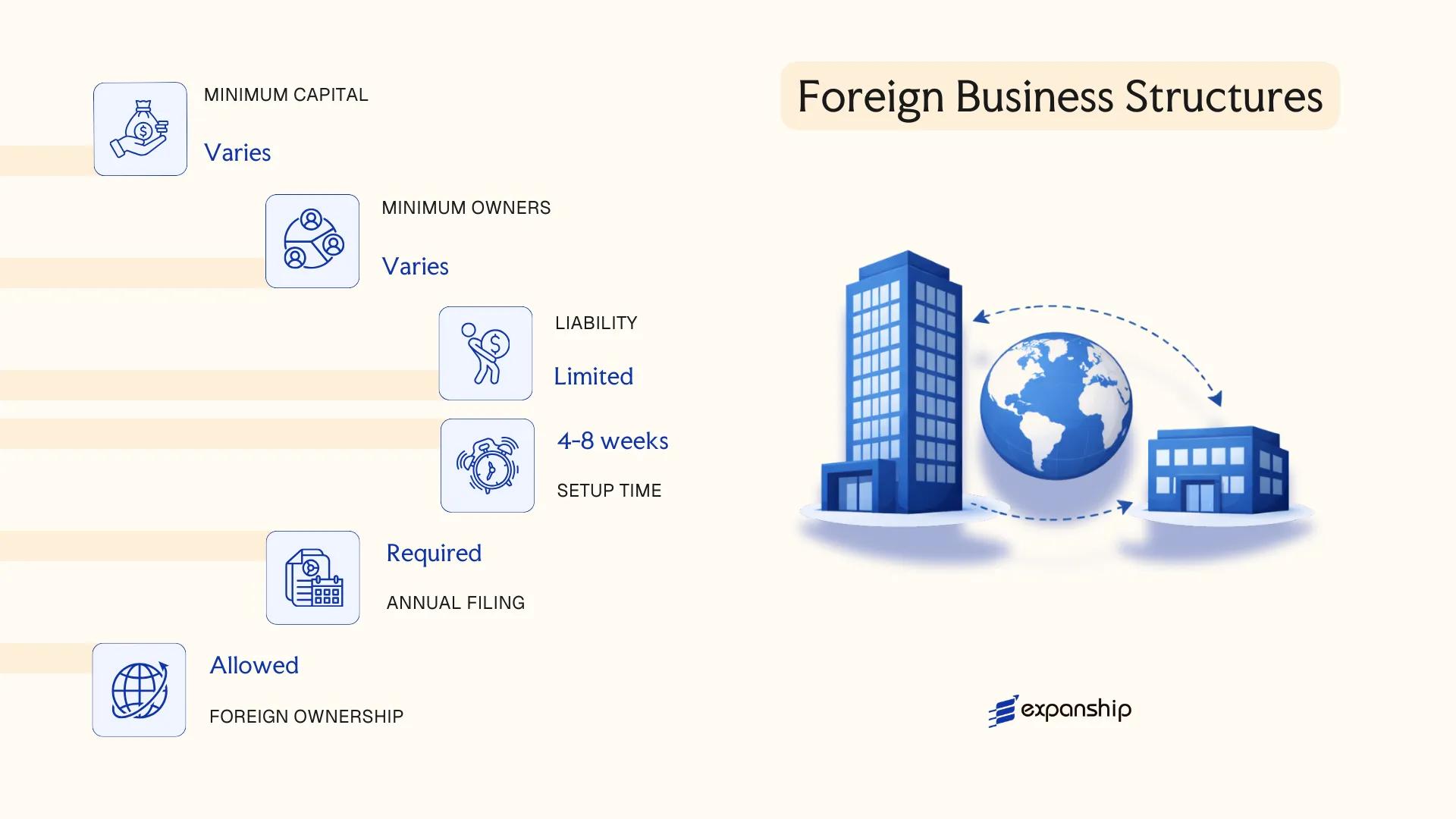

Foreign Business Structures [Branch Office, Liaison / Representative Office, Project Office, Wholly Owned Subsidiary]

Foreign companies entering the Indian market operate under the Foreign Exchange Management Act, 1999 (FEMA) and the Companies Act, 2013, with the Reserve Bank of India (RBI) and the Ministry of Corporate Affairs (MCA) serving as the primary regulators. Each foreign company structure options in India carries a distinct legal character — none of these forms create a separate legal entity independent of the parent, except the wholly owned subsidiary.

Registering under Section 380 of the Companies Act, 2013 is mandatory for branch offices, liaison offices, and project offices. Approvals are routed through the RBI's Foreign Exchange Department under the Foreign Exchange Management (Establishment in India of a branch office or a liaison office or a project office) Regulations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Extension of foreign parent (except WOS, which is a Pvt. Ltd.) | Branch, liaison, and project offices are not separate legal entities |

| Regulatory Approval | RBI via AD Category-I Bank; MCA for WOS | Project office may qualify for automatic route under specific conditions |

| Permitted Activities | Varies by structure type | Liaison: no commercial activity; Branch: limited commercial; WOS: full business operations |

| Local Office | Mandatory registered address in India | Required for all four structures |

| Capital | No minimum for offices; WOS subject to FDI sectoral caps | Remittances governed by FEMA |

| Liability | Parent liable for branch/liaison/project obligations; WOS offers limited liability | WOS liability is ring-fenced to the Indian entity |

Focus Points

- Taxation: Branch offices are taxed at 40% corporate tax rate (plus surcharge and cess) on India-sourced income; a WOS is taxed at the standard domestic rate of 22% (base) under Section 115BAA of the Income Tax Act, 1961; transfer pricing rules apply to all inter-company transactions.

- Permitted activities: Liaison offices are restricted to representational and information-gathering functions; no revenue generation is permitted.

- Compliance: All structures must file annual activity certificates; a WOS follows full Companies Act compliance including annual returns with the MCA.

- RBI reporting: Remittances abroad require prior RBI/AD bank approval; annual reporting obligations apply to all foreign entity forms.

- Conversion: A branch or liaison office cannot convert directly into a WOS; a fresh incorporation process is required.

Sub-Types

Branch Office

A branch office in India may conduct limited commercial operations, including import/export, professional services, and research, but cannot engage in manufacturing or retail directly. It suits foreign firms testing revenue-generating activity before full incorporation.

Liaison / Representative Office

This structure is restricted entirely to non-commercial functions: market research, promotion of the parent company's products, and acting as a communication channel. No invoicing or income generation is permitted from Indian operations.

Project Office

A project office is established for executing a specific project in India, typically in infrastructure, construction, or defence. RBI approval India for a project office may be granted automatically if the project is funded by inward remittance or awarded by a government entity under a specified bilateral arrangement.

Wholly Owned Subsidiary (WOS)

A wholly owned subsidiary India foreign company establishes is incorporated as a private limited company under the Companies Act, 2013, with 100% foreign shareholding where sectoral FDI policy permits. This is the only structure that creates a distinct legal person separate from the parent.

Closing

Foreign firms requiring full operational scope and liability separation typically incorporate a WOS, while project-specific or exploratory activities are handled through the office structures. The branch office vs liaison office India distinction is critical — misclassifying permitted activities can trigger FEMA violations.

Foreign companies seeking to conduct substantive, ongoing business in India with limited parent liability should establish a wholly owned subsidiary rather than a branch or office structure.

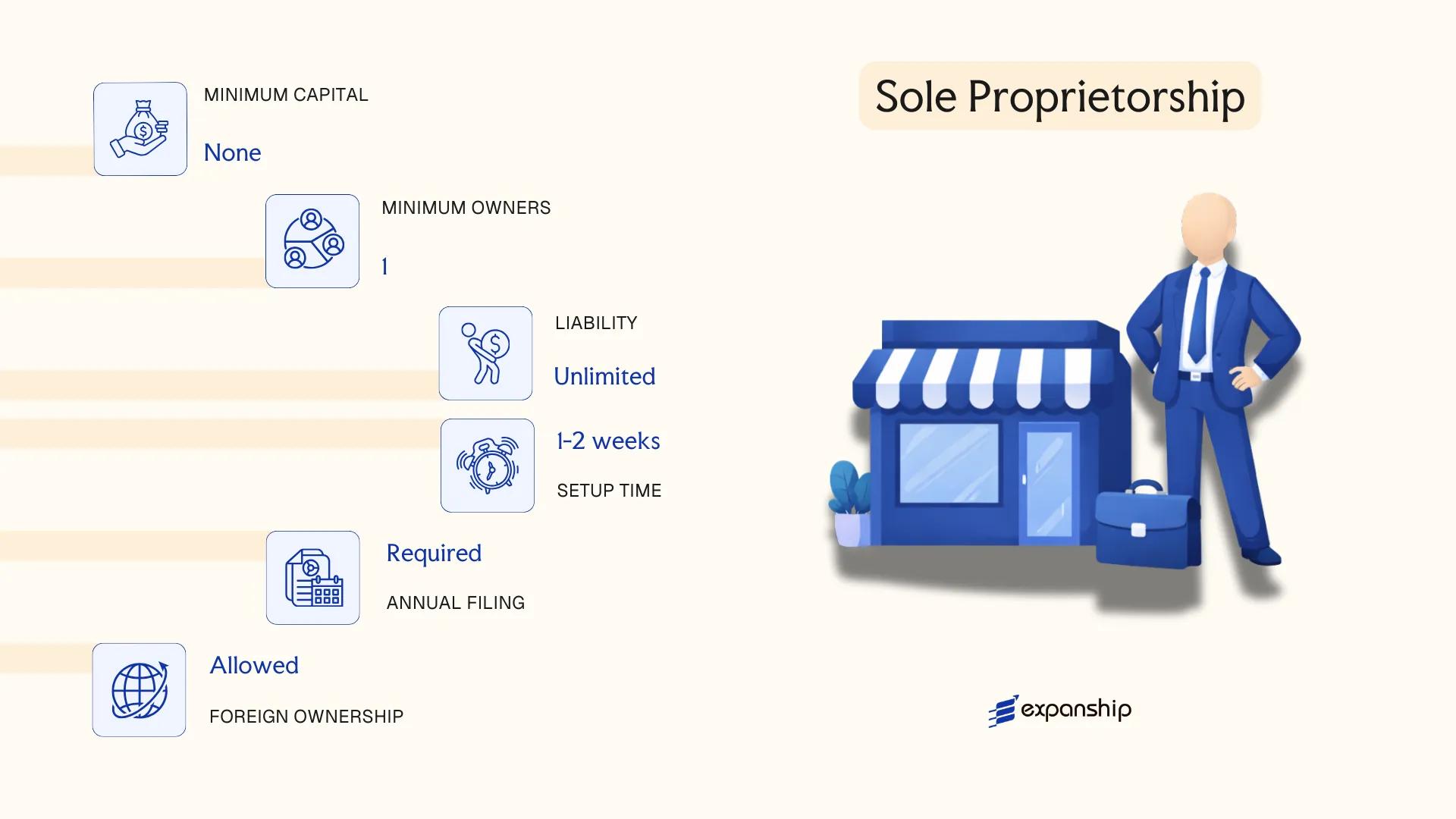

Sole Proprietorship

A sole proprietorship business in India is the simplest form of commercial operation, with no dedicated statute governing its formation. Unlike registered entities under the Companies Act, 2013, or the LLP Act, 2008, a sole proprietorship carries no separate legal identity from its owner. The business and the individual are treated as one and the same in law.

Because no distinct legal personality exists, the proprietor bears unlimited personal liability for all debts and obligations of the business. Registration is not mandatory at the central level, though obtaining a Goods and Services Tax (GST) registration, Shops and Establishments registration under the applicable state legislation, or an MSME/Udyam registration effectively formalises the business in practice.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unregistered / informally recognised business | No governing central incorporation statute |

| Members | Single proprietor | No distinction between owner and business |

| Local Presence | Business address in the state of operation | Required for GST and Shops & Establishments registration |

| Capital | No statutory minimum; in INR | Funded entirely by the proprietor |

| Liability | Unlimited personal liability | Personal assets are exposed to business debts |

| Privacy | No public filings required | No mandatory disclosure to MCA or equivalent |

Focus Points

- Taxation: Business income is taxed as personal income under the Income Tax Act, 1961, at individual slab rates (up to 30%); GST applies if turnover exceeds the applicable threshold (currently ₹20–40 lakh depending on the state and nature of supply); no separate corporate tax liability arises.

- Annual Compliance: Filing of personal income tax returns (ITR-3 or ITR-4) is required; GST returns apply if registered; no annual ROC filings or board resolutions are mandated.

- Conversion: A sole proprietorship can be converted into a Private Limited Company or an OPC under the Companies Act, 2013, though this requires fresh incorporation and transfer of assets and liabilities.

- Restrictions: Cannot raise equity capital from investors; the business ceases to exist upon the death or incapacity of the proprietor.

Closing

A sole proprietorship suits very small, low-risk domestic businesses where simplicity and minimal compliance overhead are the primary considerations; however, the absence of limited liability protection makes it unsuitable for any operation carrying meaningful financial or legal exposure.

Sole proprietorships are best suited for individual freelancers, local traders, and micro-enterprises operating in a single state with no plans to raise external capital or scale significantly.

How to Choose the Right Entity Type in India

Selecting how to choose the right business structure in India is a decision with direct legal, tax, and operational consequences — getting it wrong creates problems that can take years and significant cost to undo.

Why Your Entity Choice Matters

The structure you register shapes every aspect of how your business operates, is taxed, and can be dissolved.

- A foreign company operating through an entity not permitted for active trading under the Foreign Exchange Management Act, 1999 (FEMA) risks penalties and compulsory winding up by the Registrar of Companies.

- Forming a Liaison Office when your actual activity generates revenue violates Reserve Bank of India approval conditions, exposing the business to cancellation of registration.

- Registering an LLP when your investors require a structured equity cap table and board governance adds friction to funding rounds, as LLPs cannot issue shares or debentures.

- Selecting an entity without the capacity to maintain a registered office, resident directors, and local compliance filings under the Companies Act, 2013 triggers default notices from the Ministry of Corporate Affairs.

Key Factors to Consider

- Business Activity: Passive asset holding, active trading, and regulated sectors each require a structurally different entity under Indian law.

- Ownership Configuration: Single-founder operations may suit an OPC, while multi-party ventures require a private limited company or LLP to accommodate governance and profit-sharing arrangements.

- Tax Objectives: Your eligibility for treaty benefits under India's Double Taxation Avoidance Agreements depends on the entity type and its residency status.

- Foreign Ownership Rules: Certain sectors carry FDI restrictions under the Consolidated FDI Policy, and your chosen structure must be compatible with the applicable entry route.

- Compliance Capacity: Each structure carries distinct annual obligations — ROC filings, audits, board meetings — and your operational resources must match those requirements.

- Exit and Conversion: Not all entities permit conversion; an OPC can be converted to a private limited company, but an LLP conversion to a company involves a separate procedure under the Companies Act.

Corporate Compliance Services for Companies in India

Ongoing compliance support for Indian entities, including ROC filings, annual returns, and statutory audit coordination.

Conclusion

Setting up a company in India requires matching the structure to your ownership profile, operational scope, and compliance capacity. Among all registered entity types, the Private Limited Company remains the most incorporated form, favored for its balance of liability protection and investor readiness under the Companies Act, 2013. The One Person Company suits single founders with limited scale ambitions. An LLP works for professionals and service-oriented firms where partner flexibility outweighs the need for equity capital. Foreign entities typically enter through a Wholly Owned Subsidiary or, where restrictions apply, a Branch Office registered with the Reserve Bank of India.

Regulatory oversight under the Ministry of Corporate Affairs continues to digitize and tighten disclosure norms, reflecting a broader shift toward formal compliance frameworks. Your choice of structure will shape tax treatment, repatriation rights, and reporting obligations from day one. Expanship's team works directly with these structures across all stages of the incorporation process.

How Expanship Can Assist You

Expanship provides corporate services for India company formation across the full range of structures discussed in this blog, from Private Limited Companies registered under the Companies Act, 2013 to LLPs governed by the Limited Liability Partnership Act, 2008. Our team works directly with the Ministry of Corporate Affairs (MCA) and manages filings through the MCA21 portal on your behalf.

From initial structure selection to post-incorporation obligations, our India company registration assistance covers each stage of the process:

- Document preparation, notarization, and apostille legalization

- Registered office address provision

- MCA and Registrar of Companies (RoC) filing liaison

- Director Identification Number (DIN) and Digital Signature Certificate (DSC) procurement

- Ongoing compliance management, including annual returns and statutory filings

- Banking introduction support for opening corporate accounts in India

Reach out to Expanship India to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The Private Limited Company (Pvt. Ltd.) is the most frequently incorporated structure, registered through the MCA's SPICe+ portal. Its combination of limited liability, the ability to raise external funding, and a defined compliance framework under the Companies Act, 2013 makes it the default choice for startups and established businesses alike.

A Branch Office is an extension of the foreign parent and is restricted from engaging in manufacturing or retail trading; its profits are taxed in India at the applicable corporate rate without the benefit of the lower domestic company rate. A Private Limited Company incorporated as a Wholly Owned Subsidiary is treated as an Indian resident entity for tax purposes, qualifying for the standard 22% base corporate tax rate under Section 115BAA of the Income Tax Act, 1961. The subsidiary structure also carries fewer operational restrictions and greater flexibility in repatriating dividends.

Among registered structures, the Limited Liability Partnership (LLP) offers comparatively greater privacy than a company, as it is not required to file financial statements that are publicly accessible in the same manner as those of companies under the Companies Act, 2013. Beneficial ownership disclosures are still required under the Prevention of Money Laundering Act, 2002. Nominee arrangements are not a standard feature of Indian corporate law.

A One Person Company (OPC) is the only structure under the Companies Act, 2013 explicitly designed for a sole incorporator, who must be an Indian resident. A Private Limited Company requires a minimum of two directors and two shareholders, while an LLP requires at least two designated partners. General and limited partnerships similarly require more than one participant, making the OPC the sole option for individual incorporation.

Foreign nationals and non-resident entities may establish a Wholly Owned Subsidiary, Joint Venture, Branch Office, Liaison Office, or Project Office, subject to Foreign Direct Investment (FDI) policy and Reserve Bank of India (RBI) approval where applicable. An OPC is not available to foreign nationals, as the sole member must be an Indian citizen resident in India. For most foreign investors, the Wholly Owned Subsidiary is the accessible entry point that permits commercial operations without the restrictions that apply to Branch and Liaison Offices.

Conversion is permitted in several defined directions under Indian law. An OPC may be converted into a Private Limited Company once its paid-up capital exceeds Rs. 50 lakh or its average annual turnover exceeds Rs. 2 crore over three consecutive years. A Private Limited Company may also be converted into a Public Limited Company or an LLP under the procedures set out in the Companies Act, 2013 and the LLP Act, 2008, respectively, provided the requisite shareholder approvals and MCA filings are completed.

Private Limited Companies, Public Limited Companies, OPCs, and LLPs all possess separate legal personality, meaning the entity can own assets, enter contracts, and incur liabilities independently of its members. A general partnership and a sole proprietorship do not have separate legal standing; the individual partners or proprietor remain personally liable for business obligations. This distinction is a primary reason many operators transition from informal structures to registered entities.

A sole proprietorship has no statutory annual filings with the MCA, though it remains subject to GST registration, income tax returns, and applicable professional licensing. Among registered entities, an LLP with a turnover below Rs. 40 lakh and capital contribution below Rs. 25 lakh is exempt from mandatory audit under the LLP Act, 2008, reducing its annual compliance burden relative to a Private Limited Company.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.