Key Takeaways

- The Private Limited Company (Chevra Prutit) is the most commonly registered entity in Israel, suited to startups, SMEs, and foreign investors due to its liability protection and minimal share capital requirements.

- All company registration, ongoing compliance, and regulatory filings in Israel are administered by the Israel Corporations Authority, which operates under the Ministry of Justice.

- Branch offices and registered foreign companies allow overseas businesses to operate in Israel without forming a separate legal entity, though full liability remains with the parent company.

- Israel's available business structures span multiple legal forms governed by distinct legislation, including the Companies Law, 5759-1999, with non-profit entities such as the Amuta and Public Benefit Company falling under the oversight of the Registrar of Amutot.

Introduction to Entity Types in Israel

Located in the Middle East, bordered by Lebanon, Syria, Jordan, and Egypt, Israel is an independent state with a well-developed legal and commercial framework. Businesses registering here fall under the jurisdiction of the Israel Corporations Authority, which operates under the Ministry of Justice and administers company registration, ongoing compliance, and regulatory filings.

Israel operates a territorial-plus-residency tax system, meaning tax liability depends on both the nature of income and the residency status of the entity or its shareholders.

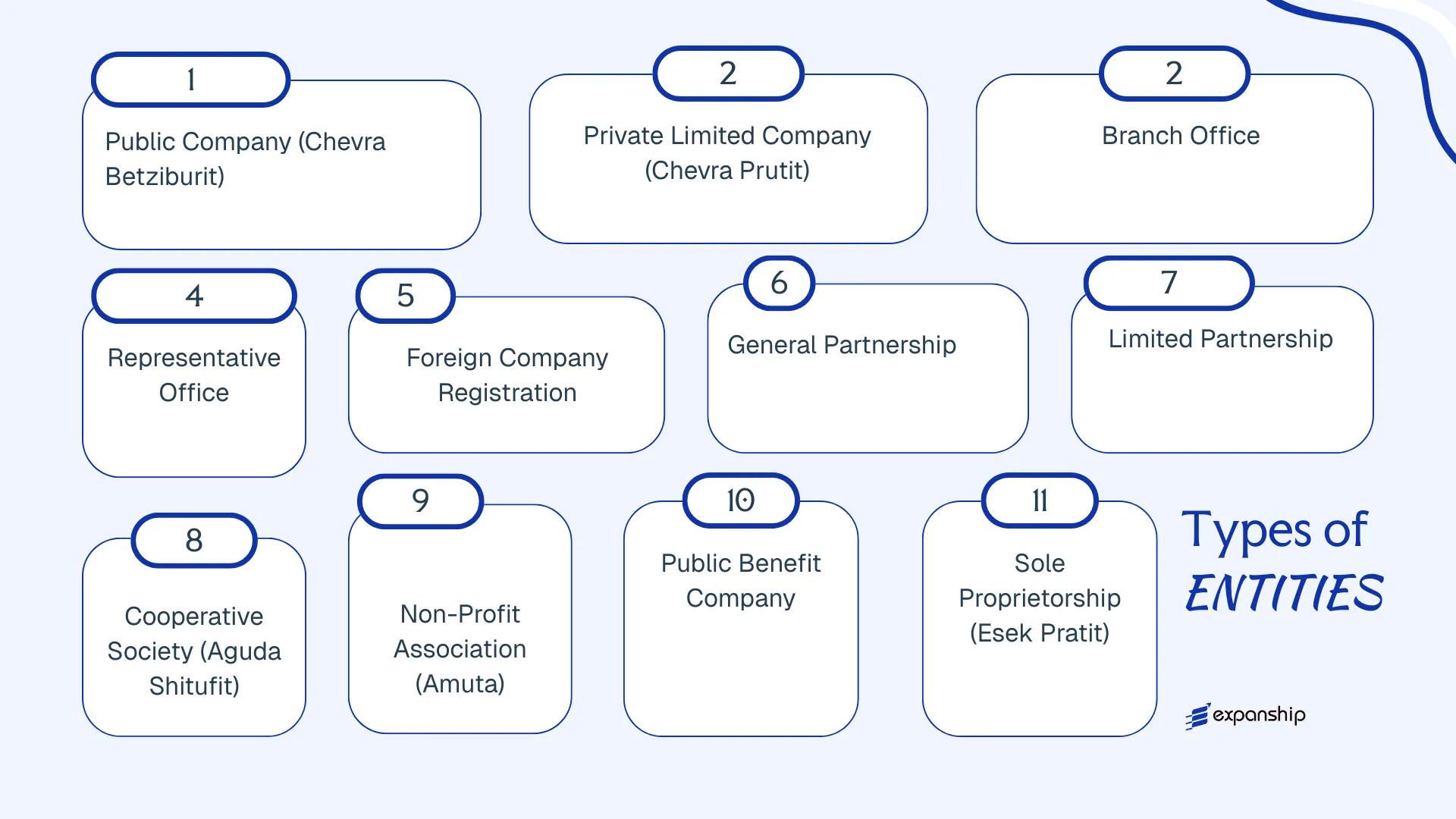

The types of business entities in Israel span several legal forms, each governed by distinct legislation. Available structures include the Public Company, Private Limited Company, Branch Office, Representative Office, Foreign Company Registration, General Partnership, Limited Partnership, Cooperative Society, Amuta, Public Benefit Company, and Sole Proprietorship. Each entity type carries specific requirements around ownership, liability, reporting, and taxation.

This article examines each structure in detail — covering formation requirements, governance rules, and practical considerations for your business.

An Overview of Business Structures in Israel

Israel business structures comparison spans several distinct entity types, each governed primarily by the Companies Law, 5759-1999 (Hok HaChevrot), with additional frameworks under the Partnerships Ordinance [New Version], 5735-1975 and the Cooperative Societies Ordinance. Each structure carries different implications for liability, taxation, and operational scope.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Company (Chevra Betziburit) | Corporation | Limited | Taxed | Yes | 2 shareholders | Israel Securities Authority / Registrar of Companies | Companies Law, 5759-1999 |

| Private Limited Company (Chevra Prutit) | Corporation | Limited | Taxed | Yes | 1 shareholder | Registrar of Companies | Companies Law, 5759-1999 |

| Branch Office | Foreign entity extension | Unlimited (parent) | Taxed on local income | Yes | N/A | Registrar of Companies | Companies Law, 5759-1999 |

| Representative Office | Non-trading presence | Unlimited (parent) | Generally exempt | No | N/A | Registrar of Companies | Companies Law, 5759-1999 |

| General Partnership (Shutafut Klalit) | Partnership | Unlimited | Partners taxed | Yes | 2 partners | Registrar of Partnerships | Partnerships Ordinance, 5735-1975 |

| Limited Partnership (Shutafut Mugbelet) | Partnership | Mixed | Partners taxed | Yes | 1 GP + 1 LP | Registrar of Partnerships | Partnerships Ordinance, 5735-1975 |

| Cooperative Society (Aguda Shitufit) | Cooperative | Limited | Taxed | Yes | 3 members | Registrar of Cooperative Societies | Cooperative Societies Ordinance |

| Amuta (Non-Profit Association) | Association | Limited | Exempt (conditions apply) | No | 7 members | Registrar of Amutot | Amutot Law, 5740-1980 |

| Public Benefit Company | Corporation | Limited | Exempt (conditions apply) | No | 1 shareholder | Registrar of Companies | Companies Law, 5759-1999 |

| Sole Proprietorship (Esek Pratit) | Unincorporated | Unlimited | Owner taxed | Yes | 1 owner | Israel Tax Authority | Income Tax Ordinance |

Each of these structures is examined in full in the sections below.

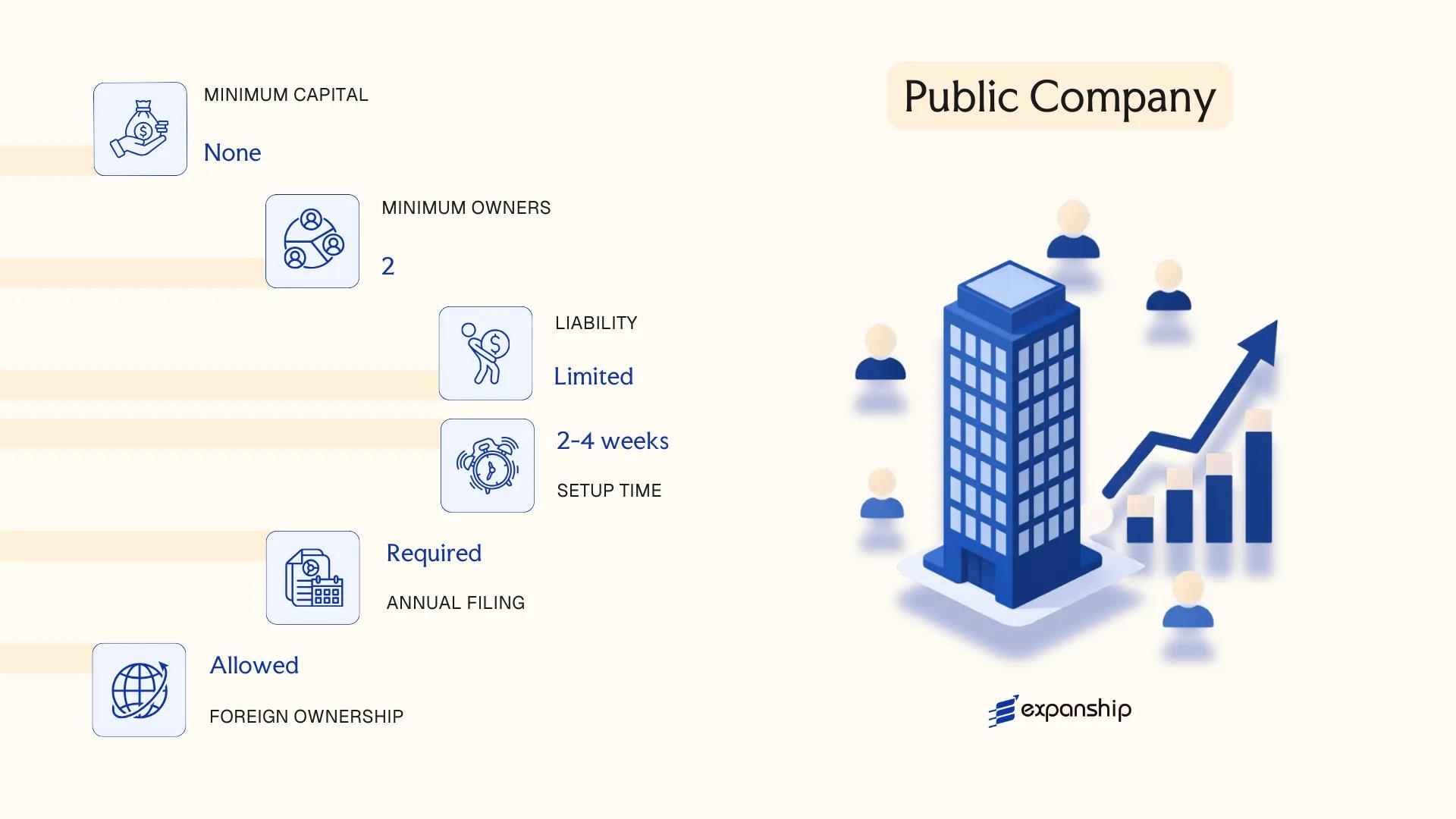

Public Company (Chevra Betziburit)

Governed by the Israeli Companies Law, 5759-1999, an Israel public company Chevra Betziburit is a corporate entity whose shares may be offered to the public and traded on a stock exchange. Like its private counterpart, it holds separate legal personality, meaning the firm exists independently of its shareholders.

Shareholders bear limited liability, capped at the value of their unpaid share capital. Public companies are subject to heightened disclosure obligations and ongoing oversight by the Israel Securities Authority (ISA), which administers the Securities Law, 5728-1968.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (Chevra Betziburit) | Separate legal personality; limited liability |

| Members | Minimum 2 shareholders; no maximum | Directors: minimum 2, at least 2 must be external (independent) directors |

| Local Presence | Registered office in Israel required | No mandatory local director, but ISA compliance officers are standard practice |

| Share Capital | No statutory minimum; denominated in NIS | Shares may be publicly traded on the Tel Aviv Stock Exchange (TASE) |

| Privacy | Full public disclosure required | Financial statements, shareholder registers, and board compositions are publicly filed |

| Auditor | Mandatory certified auditor | Required under the Companies Law; reports filed with the Registrar of Companies |

Focus Points

- Taxation: Subject to corporate income tax at 23%; VAT applies at 17%; dividend withholding tax of 25–30% for substantial shareholders; no stamp duty on share transfers.

- Annual Compliance: Mandatory annual general meeting, audited financial statements, and periodic reporting to the ISA under the Securities Regulations.

- Stock Exchange Listing: Listing on the Tel Aviv Stock Exchange requires meeting TASE prospectus, free-float, and equity threshold requirements, with ongoing quarterly and annual disclosures.

- Treaty Access: Qualifies as an Israeli resident company for purposes of Israel's tax treaty network, covering over 50 bilateral agreements.

- Restrictions: Foreign ownership is generally unrestricted, though certain regulated sectors (defence, banking, telecoms) require prior government approval.

Closing

A Chevra Betziburit suits businesses seeking access to public capital markets, particularly established firms planning a TASE listing or those requiring broad institutional investment. The primary limitation is the compliance burden: continuous disclosure requirements, mandatory external directors, and ISA oversight add significant administrative and legal costs relative to a private structure.

This entity type is most appropriate for mature businesses with the operational capacity to meet ongoing public reporting and corporate governance obligations.

Company Incorporation in Israel

Incorporate a public or private company in Israel with end-to-end support from entity selection through registration.

Private Limited Company (Chevra Prutit)

The Israel private limited company, known as a Chevra Prutit, is the most widely used business structure for foreign investors and domestic entrepreneurs alike. Governed by the Companies Law, 5759-1999, it carries a separate legal personality distinct from its shareholders, meaning the firm's obligations do not extend to its owners' personal assets.

Shares in a Chevra Prutit are not freely transferable to the public, distinguishing it structurally from a public company. This restriction makes the entity suitable for closely held business operations where ownership control is a priority.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company | Separate legal personality; liability limited to share capital |

| Members | Shareholders and Directors | Minimum 1 shareholder; maximum 50 shareholders; minimum 1 director |

| Local Presence | Registered Office in Israel | A registered address within Israel is mandatory; no statutory requirement for a local director |

| Capital | NIS; no minimum share capital | Shares can be issued at any par value; capital structure is flexible |

| Privacy | Shareholder details filed with the Israel Companies Registrar | Basic registry information is publicly accessible |

Focus Points

- Taxation: Subject to corporate income tax at 23%; VAT at 17% applies to taxable transactions; withholding tax applies to dividends, interest, and royalties paid to non-residents; no stamp duty on share transfers.

- Annual Compliance: Annual report filed with the Companies Registrar; audited financial statements required.

- Treaty Access: Qualifies for benefits under Israel's tax treaty network as a resident entity.

- Conversion: Can be converted into a public company under the Companies Law upon meeting applicable requirements.

- Restrictions: Prohibited from offering shares to the public or listing on a stock exchange without conversion.

Closing

A Chevra Prutit suits trading operations, holding structures, and IP ownership arrangements where limited liability and operational flexibility are required. The absence of a minimum share capital requirement lowers the entry threshold, though the mandatory public disclosure of shareholder information at the Companies Registrar limits confidentiality.

Best suited for foreign investors and SMEs seeking a fully operational Israeli entity with straightforward governance and access to the country's tax treaty network.

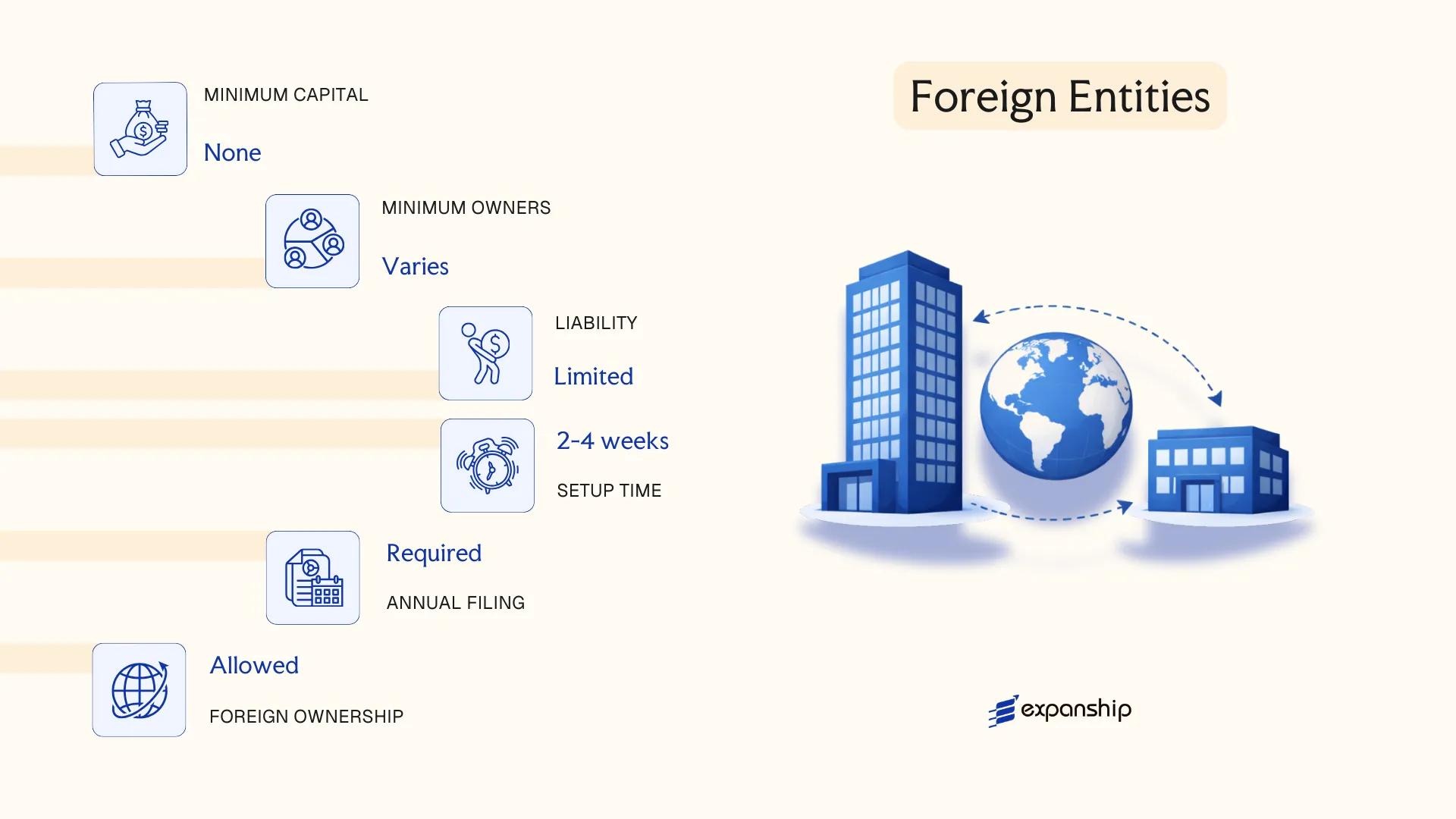

Foreign Entities in Israel [Branch Office, Representative Office, Foreign Company Registration]

Foreign companies seeking a presence in Israel must complete foreign company registration in Israel through the Israeli Registrar of Companies, operating under the Companies Law, 5759-1999. A registered foreign company does not constitute a new legal entity — it remains an extension of the parent, carrying the same legal personality and liability structure as the incorporating jurisdiction.

Registration is mandatory for any foreign company that establishes a place of business within the country. The process requires filing prescribed documents with the Registrar, including certified copies of the company's constitutional documents, translated into Hebrew where applicable.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Extension of foreign parent | No separate Israeli legal personality |

| Local Representative | Authorized representative required | Must be an Israeli resident |

| Registered Address | Local address required | Must be maintained for official correspondence |

| Capital | No minimum imposed locally | Parent's capital structure applies |

| Privacy | Parent's documents filed publicly | Accessible via Registrar of Companies |

| Governing Law | Companies Law, 5759-1999 | Specific regulations under Section 346+ |

Focus Points

- Taxation: Subject to Israeli corporate tax (currently 23%) on Israeli-sourced income; VAT registration required if conducting taxable activity; withholding tax may apply on cross-border payments.

- Treaty Access: Access to Israel's tax treaty network depends on the parent entity's jurisdiction and treaty eligibility.

- Annual Compliance: Annual report and updated particulars must be filed with the Registrar; financial reporting obligations apply.

- Restrictions: Cannot issue shares or raise capital independently; all obligations ultimately rest with the foreign parent.

Sub-Types

Branch Office

A branch conducts active business operations in Israel and is directly liable for all obligations incurred locally. It is commonly used by foreign firms entering the market operationally rather than through a subsidiary.

Representative Office

A representative office is restricted to promotional and liaison activities only — it cannot generate revenue or execute commercial contracts. This structure suits firms conducting market research or maintaining client relationships ahead of a fuller market entry.

Foreign company registration at the Registrar of Companies covers both structures under the same statutory framework, though their permitted activities differ substantially.

Closing

A registered foreign entity suits multinationals testing the Israeli market or maintaining a defined operational footprint without incorporating a standalone subsidiary, though the parent remains fully exposed to local liabilities incurred through it.

Best suited for established foreign companies requiring a direct operational or liaison presence without the administrative burden of incorporating a separate Israeli entity.

Partnerships in Israel [General Partnership, Limited Partnership]

Partnership registration in Israel is governed by the Partnerships Ordinance [New Version], 5735-1975, which consolidates earlier mandatory law and defines two distinct structural forms. Unlike a private limited company, a general partnership does not carry separate legal personality, meaning partners bear direct exposure to the firm's liabilities. A limited partnership introduces a hybrid arrangement, separating liability between general and limited partners while remaining registered under the same ordinance.

Registration is handled through the Israeli Registrar of Partnerships (Rasham HaShutafuyot), which operates under the Ministry of Justice. The Hebrew term shutafut covers both forms, and both must be registered before commencing business activity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated association (no separate legal personality) | Partners are personally liable in a general partnership |

| Members | Called "partners"; minimum 2, no statutory maximum | Limited partnership requires at least one general and one limited partner |

| Local Presence | Registered office address in Israel required | Must be maintained throughout the partnership's existence |

| Capital | No minimum capital requirement; no prescribed currency | Contributions defined by the partnership agreement |

| Privacy | Partnership deed and partner details filed with Rasham HaShutafuyot | Register is publicly accessible |

Focus Points

- Taxation: Partnerships are fiscally transparent; profits are attributed to individual partners and taxed at their applicable personal or corporate income tax rates. VAT registration obligations apply to trading partnerships once turnover thresholds are met.

- Annual Compliance: Annual reports and any changes to partner composition must be filed with the Registrar; failure to report changes carries penalties.

- Treaty Access: Because partnerships are tax-transparent, treaty benefits under Israel's double tax agreements apply at the partner level, not the entity level, which can complicate cross-border structuring.

- Restrictions: A limited partner who participates in management loses limited liability protection under the Ordinance.

Sub-Types

General Partnership (Shutafut Klalit)

All partners carry unlimited joint and several liability for the firm's obligations. This structure is common among professional service providers such as lawyers and accountants, where regulatory frameworks may require or permit this form.

Limited Partnership (Shutafut Mugbelet)

At least one general partner retains unlimited liability, while limited partners' exposure is capped at their agreed capital contribution. This structure is frequently used for private equity vehicles, real estate funds, and venture capital arrangements in Israel.

Closing Paragraph

Partnerships suit professional services, joint ventures with defined exit terms, and fund structures where pass-through taxation is commercially desirable. The absence of minimum capital and the transparent tax treatment are practical advantages, though the unlimited liability exposure for general partners represents a significant structural constraint for high-risk commercial activities.

Israeli partnerships are best suited for professional services firms, domestic joint ventures, and private fund vehicles where pass-through taxation and flexible partner arrangements are priorities.

Cooperative Society (Aguda Shitufit)

A cooperative society Israel — known locally as an Aguda Shitufit — is governed by the Cooperative Societies Ordinance, originally enacted in 1933 and subsequently updated through various regulations administered by the Registrar of Cooperative Societies within the Ministry of Economy. The entity carries separate legal personality, meaning it can hold assets, enter contracts, and bear liabilities independently of its members.

Structurally, the Aguda Shitufit is a hybrid form: it combines the mutual-benefit orientation of an association with commercial operational capacity. Members hold equal voting rights regardless of their capital contribution, which distinguishes the cooperative from standard share-based entities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Cooperative Society (body corporate) | Separate legal personality; limited liability for members |

| Members | Referred to as "members"; minimum 7 founding members | No statutory maximum; members hold equal voting rights |

| Governance | General Assembly + elected Board of Directors | Board elected by members; decisions often require majority or supermajority votes |

| Local Presence | Registered office in Israel required | Must be maintained for official correspondence with the Registrar |

| Capital | No prescribed minimum share capital; members purchase shares at fixed par value | Par value set in the cooperative's bylaws (takanon) |

| Privacy | Member register maintained by the Registrar; partially public | Annual reports filed with the Registrar are accessible |

Focus Points

- Taxation: Subject to standard Israeli corporate income tax (currently 23%); VAT registration required for commercial activity; withholding tax applies on distributions; no special cooperative tax exemption unless classified as an agricultural cooperative under specific rulings.

- Annual Compliance: Must file audited financial statements and an annual report with the Registrar of Cooperative Societies; General Assembly must convene at least once per year.

- Restrictions: Membership criteria and transfer of membership shares are governed by the takanon (bylaws); shares generally cannot be freely transferred to third parties.

- Conversion: Conversion to another entity type is not straightforward and typically requires dissolution and re-registration under a different ordinance.

- Treaty Access: As an Israeli tax resident entity, the cooperative can access Israel's network of double tax treaties, subject to treaty-specific beneficial ownership conditions.

Sub-Types

Agricultural Cooperative

Formed specifically to serve farming communities, this sub-type may benefit from preferential tax treatment and dedicated support under Ministry of Agriculture frameworks. It typically handles collective purchasing, marketing, or processing of agricultural produce.

Workers' Cooperative

Members are simultaneously employees and owners of the enterprise. Governance rules emphasize worker participation, and surplus distribution is often tied to labour contribution rather than capital held.

Consumer Cooperative

Organised to supply goods or services to its members at reduced cost, this sub-type is common in retail and housing. Surplus, if any, is returned to members proportionally based on usage rather than share ownership.

The Aguda Shitufit is suited to agricultural ventures, worker-owned businesses, and community-based commercial projects where collective governance takes priority over investor returns. Its equal-vote structure promotes democratic control, though this same feature can slow decision-making in larger organisations.

Agricultural enterprises, worker-owned ventures, or community-focused businesses where members require equal voting rights and shared operational control.

Non-Profit Organizations in Israel [Amuta, Public Benefit Company]

Two primary legal forms serve non-commercial purposes under Israeli law: the Amuta (association) and the Public Benefit Company. Non-profit organization registration Israel falls primarily under the Associations Law, 5740-1980 for the Amuta, while the Public Benefit Company is governed by the Companies Law, 5759-1999.

Both structures carry separate legal personality and limit member liability. The Amuta is the more traditional form, structured around a membership body with elected organs, while the Public Benefit Company adopts a corporate framework without distributing profits to shareholders.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Association (Amuta) / Public Benefit Company | Governed by separate legislation; both have full legal personality |

| Governing Body | Amuta: General Assembly + Management Board; Public Benefit Company: Board of Directors | Amuta requires at least 7 founding members; Public Benefit Company follows corporate governance norms |

| Members / Shareholders | Amuta: minimum 7 members, no upper limit; Public Benefit Company: no member requirement | Public Benefit Company may have a sole director structure |

| Local Presence | Registered office address in Israel required for both | Registrar of Associations or Companies Registrar, respectively |

| Capital | No minimum capital for either form | Profits must remain within the organization; distribution to members is prohibited |

| Privacy | Founding documents and officer details are publicly registered | Annual reports filed with the relevant registrar are accessible |

Focus Points

- Taxation: Both forms may qualify for tax-exempt status under Section 9(2) of the Income Tax Ordinance; approved public institutions may also issue tax-deductible donation receipts under Section 46.

- Annual Compliance: Amuta must file annual activity reports and financial statements with the Registrar of Associations; Public Benefit Companies report to the Companies Registrar.

- Fundraising Restrictions: Amuta receiving foreign government funding above a defined threshold must register and report under the Foreign Agents Law, 5777-2016.

- Conversion: An Amuta cannot convert directly into a for-profit company; structural changes require dissolution and re-incorporation.

- Treaty Access: Neither form is structured for commercial treaty benefits; tax arrangements are governed by domestic exemption provisions rather than double tax treaties.

Sub-Types

Amuta (עמותה)

Registered under the Associations Law, 5740-1980 and supervised by the Registrar of Associations within the Ministry of Justice, an Amuta is the standard vehicle for civil society, charitable, and community organizations. Membership governance distinguishes it from the corporate model.

Public Benefit Company (Chevra Le'Toelet HaTzibur)

Incorporated under the Companies Law, 5759-1999, this form suits organizations that prefer a corporate governance structure without a traditional membership body. It is commonly used by foundations and institutionalized philanthropic entities that require a board-driven framework.

Closing

Both forms are suited to charitable, educational, cultural, and social welfare activities, with the Amuta being the more widely used option for grassroots and community organizations. The primary limitation for both structures is the absolute prohibition on profit distribution, which restricts any commercial cross-subsidy to related for-profit entities.

Best suited for civil society organizations, foundations, and educational bodies seeking a recognized legal structure with potential tax-exempt status under Israeli law.

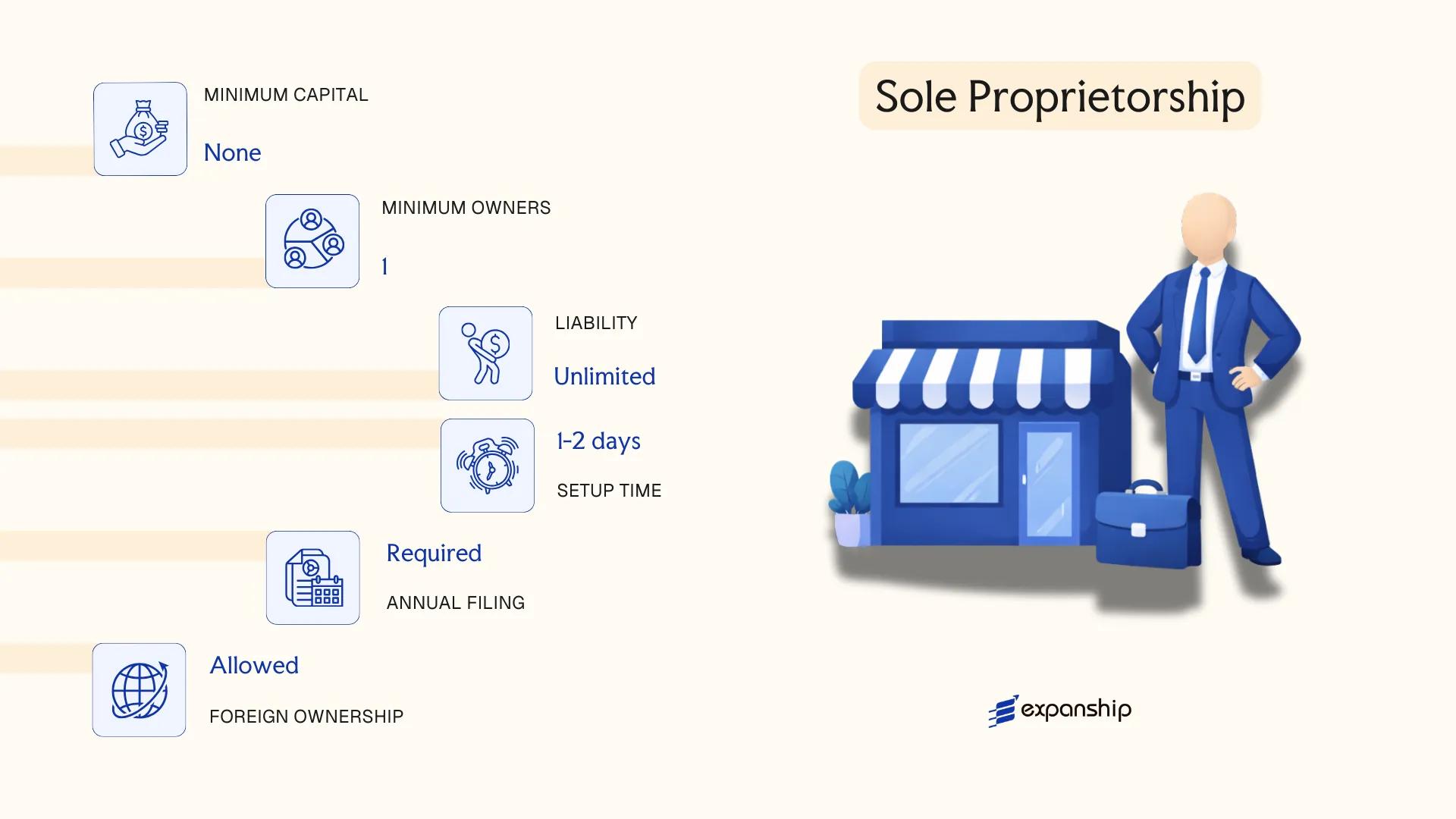

Sole Proprietorship (Esek Pratit)

A sole proprietorship Israel Esek Pratit is governed by the Business Licensing Law, 1968, alongside the Income Tax Ordinance [New Version], 1961, which establishes the tax treatment for self-employed individuals. Unlike a company, the Esek Pratit carries no separate legal personality — the proprietor and the business are the same legal entity, meaning personal assets are fully exposed to business liabilities.

Registration is handled through the Israel Tax Authority and, where applicable, the local municipality. Most self-employed individuals must also register with the Value Added Tax directorate and the National Insurance Institute (Bituach Leumi).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the proprietor |

| Member Type | Sole proprietor | One individual only; no partners or shareholders |

| Local Presence | Israeli resident proprietor; registered business address | Must register with Israel Tax Authority and municipality |

| Capital | No minimum capital requirement | No statutory threshold |

| Liability | Unlimited personal liability | Personal assets exposed to all business debts |

| Privacy | Business details partially public via tax records | No corporate registry filing equivalent to a company |

Focus Points

- Taxation: Subject to personal income tax (up to 50%), VAT registration required above the statutory turnover threshold, and Bituach Leumi contributions; no corporate tax applies.

- Annual Compliance: Annual income tax return filed with the Israel Tax Authority; periodic VAT reports (monthly or bimonthly depending on turnover).

- Treaty Access: No access to Israel's tax treaty network as a separate entity; treaty benefits flow through the individual proprietor's personal residency status.

- Conversion: Can be converted into a private company (Chevra Prutit) through a transfer of business assets, though this may trigger tax events under Israeli law.

- Restrictions: Cannot raise equity capital or issue shares; growth financing is limited to personal funds or debt instruments.

A sole proprietorship suits freelancers, consultants, and small-scale traders who operate with low overhead and limited third-party liability exposure. The absence of corporate formalities reduces administrative burden, but unlimited personal liability makes it unsuitable for businesses with significant contractual or financial risk.

Best suited for individual professionals and sole traders in Israel seeking a low-cost, low-formality structure with no partners or investors involved.

How to Choose the Right Entity Type in Israel

Selecting the correct entity structure is a foundational decision that affects your tax position, liability exposure, regulatory obligations, and long-term operational flexibility.

Why Your Entity Choice Matters

The Companies Law, 5759-1999 governs most corporate structures registered with the Israel Corporations Authority, and the consequences of misalignment between your structure and your actual operations are concrete:

- Registering a foreign company under Section 346 of the Companies Law without meeting local substance requirements can trigger reporting failures and potential administrative penalties imposed by the Registrar of Companies.

- Selecting a tax-exempt structure — such as an Amuta — when your business requires access to Israel's tax treaty network means you cannot claim withholding tax reductions available to resident companies under those treaties.

- Forming a private company when your needs center on asset protection or estate planning locks you into annual shareholder obligations, audit thresholds, and dividend distribution rules that would not apply to a foundation-type structure.

- Choosing a structure that mandates audited financial statements for a single-person consultancy adds recurring compliance costs that are disproportionate to the scale of the operation.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or insurance each correspond to distinct permissible structures under Israeli law.

- Local vs. Cross-Border Operations: Transacting with Israeli residents typically requires full local incorporation rather than a foreign company registration or representative office.

- Ownership and Management: Single-owner operations and multi-party ventures have different governance requirements — a private company accommodates flexible management, while a public company mandates a formal board structure.

- Tax Objectives: Your need for participation exemption, access to the territorial tax regime, or eligibility for approved enterprise benefits under the Law for the Encouragement of Capital Investments shapes which structure qualifies.

- Privacy Requirements: Director and shareholder details are publicly searchable through the Israel Corporations Authority register, so nominee arrangements may be necessary where confidentiality is a priority.

- Exit Strategy: Not all Israeli entities permit redomiciliation or conversion — confirm that your chosen structure allows the winding-up or transformation mechanism your business may eventually require.

Compliance Services for Companies in Israel

Ongoing compliance support for Israeli-registered entities, covering annual filings, shareholder obligations, and regulatory reporting requirements.

Conclusion

Setting up a company in Israel requires matching your operational goals with the correct legal structure under the Companies Law, 5759-1999. The Private Limited Company (Chevra Prutit) is the most commonly registered entity, suited to startups, SMEs, and foreign investors seeking liability protection with minimal share capital requirements. Public Companies serve firms pursuing capital markets access through the Tel Aviv Stock Exchange. Branches and registered foreign companies allow overseas businesses to operate without establishing a separate legal entity, though they carry full parent liability. Partnerships work for professional services firms, while the Aguda Shitufit serves member-based cooperative ventures. Non-profit structures, whether an Amuta or a Public Benefit Company, address philanthropic or social mandates governed by the Registrar of Amutot.

Israel continues expanding its tax treaty network and refining its foreign investment framework, which shapes entity selection over time. Professional guidance remains relevant as registration, tax, and compliance obligations are administered across multiple authorities, including the Companies Registrar and the Israel Tax Authority.

How Expanship Can Assist You

Expanship's corporate services Israel company formation work covers the full scope of what the Israel Companies Registrar (Rasham HaChavarot) and the Israeli Tax Authority require — from selecting between a Chevra Prutit and a foreign branch to meeting post-registration filing obligations. Your entity type determines your compliance path, and our team is structured to support both.

From initial document preparation through to ongoing regulatory maintenance, here is what we handle:

- Document preparation, apostille, and legalization

- Registered office and local agent provision

- Filing with the Companies Registrar and coordination with the Israeli Tax Authority

- VAT registration and corporate tax enrollment

- Post-incorporation compliance and annual reporting

- Banking introduction assistance for local and international accounts

Reach out to Expanship Israel to discuss your specific requirements with our incorporation team.

Frequently Asked Questions (FAQ)

The Private Limited Company (Chevra Prutit) is the most frequently incorporated entity. Its liability protection, flexible shareholding structure, and relatively straightforward registration through the Registrar of Companies make it the default choice for most commercial ventures.

A branch is not a separate legal entity; the foreign parent bears full liability for its Israeli operations. A Chevra Prutit is independently incorporated, files its own tax returns with the Israel Tax Authority, and limits shareholder exposure to their contributed capital.

A Private Limited Company does not publicly disclose beneficial ownership details beyond what is filed with the Registrar of Companies. Nominee director and shareholder arrangements are legally permissible, though ultimate beneficial ownership may be subject to reporting under anti-money laundering regulations.

A sole individual can incorporate a Chevra Prutit and register as a Sole Proprietor. General and Limited Partnerships require at least two partners, and a Cooperative Society requires a minimum group of founding members under the Cooperative Societies Ordinance.

Foreigners may incorporate a Chevra Prutit, register a branch or representative office, or form a partnership. There is no residency requirement for directors or shareholders of a Private Limited Company under the Companies Law.

Conversion from a Sole Proprietorship or partnership into a Private Limited Company is generally achievable through a restructuring process. Direct statutory conversion between all entity types is not universally available; legal reorganization or asset transfer may be required depending on the structures involved.

No. A branch office and a Sole Proprietorship lack separate legal personality, meaning the parent company or individual owner bears direct liability. The Chevra Prutit, Public Company, Cooperative Society, and Amuta each hold distinct legal standing under their respective governing legislation.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.