Key Takeaways

- Ireland's Companies Registration Office (CRO) administers all company formations under the Companies Act 2014, which governs the full range of incorporated structures available in the jurisdiction.

- The Private Limited Company (Ltd) is the most registered structure in Ireland, valued for its flexible constitution and suitability across general commercial use cases.

- Businesses requiring a defined and restricted operational scope are better served by a Designated Activity Company (DAC) than by the standard Ltd structure.

- Foreign companies seeking an Irish presence without local incorporation can register as a branch or external company rather than establishing a new legal entity.

Introduction to Entity Types in Ireland

Ireland is an independent republic located on the western edge of Europe, sharing the North Atlantic with Great Britain to its east and positioned at the edge of the EU's single market. Company registration is administered by the Companies Registration Office (CRO), which operates under the Companies Act 2014 — the primary legislation governing corporate formation and compliance in the country. Ireland maintains a low-tax regime, most notably through its 12.5% corporate tax rate on trading income, making it a frequently used jurisdiction for European holding and operational structures.

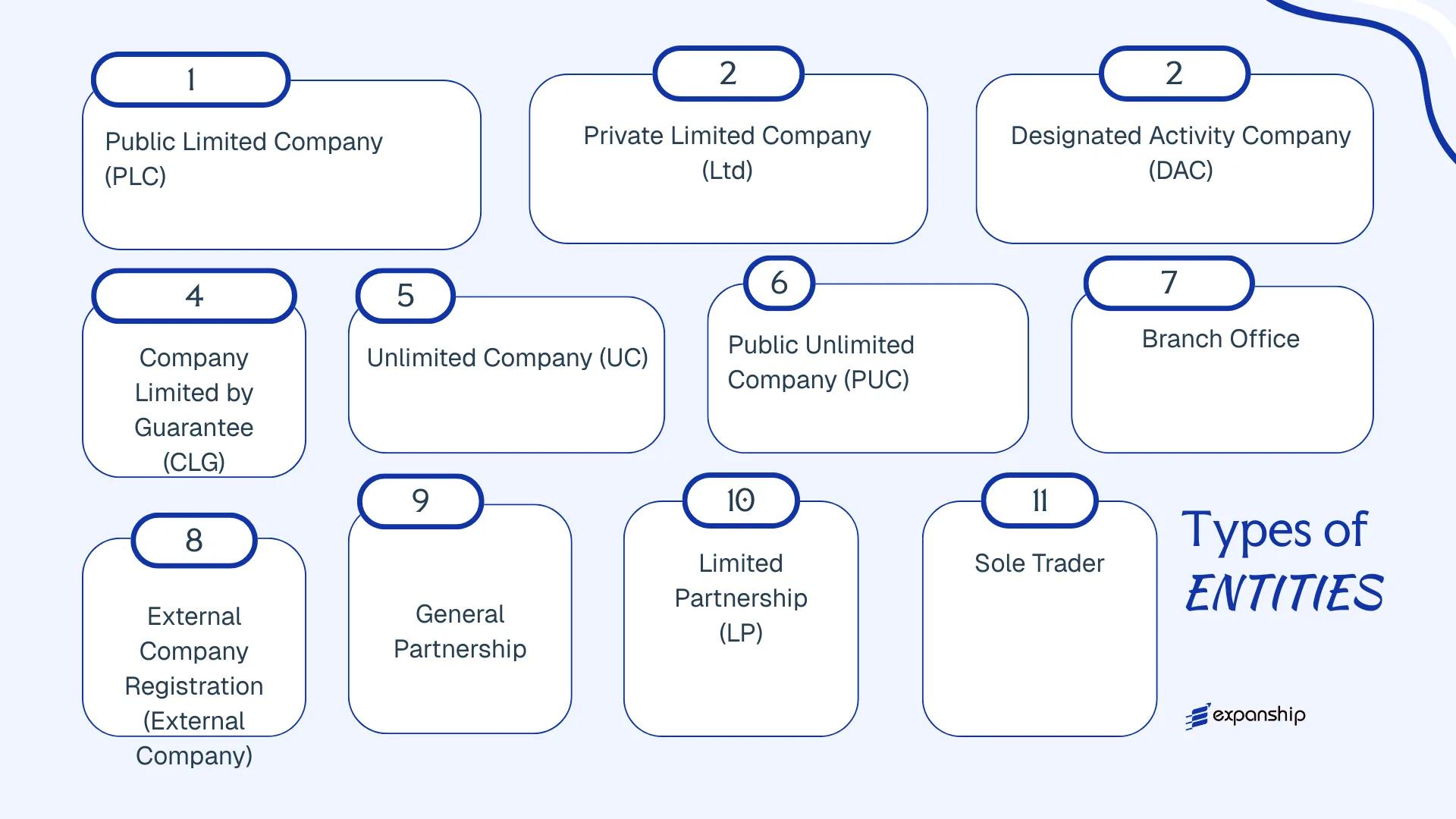

Several distinct legal structures are available to businesses registering here. These include the Private Limited Company (Ltd), Designated Activity Company (DAC), Public Limited Company (PLC), Company Limited by Guarantee (CLG), Unlimited Company (UC), and its public equivalent (PUC). Beyond incorporated entities, you can also establish a General Partnership, Limited Partnership, Investment Limited Partnership, or register as a Sole Trader. Foreign businesses may operate through a branch or external company registration.

Each structure carries specific liability, governance, and filing obligations under the Companies Act 2014. This article examines each option in detail to help you identify which entity aligns with your operational and regulatory requirements.

An Overview of Business Structures in Ireland

Under the Companies Act 2014, six distinct company types are available for incorporation, each with its own liability profile, membership requirements, and permitted activities. That legislation, consolidated and modernised from earlier company law, remains the primary statutory framework governing corporate formation and compliance. Each structure serves a different commercial purpose, from large public fundraising to charitable operations and private trading.

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Private Limited Company (Ltd) | Incorporated company | Limited by shares | Taxed | Permitted | 1 | CRO | Companies Act 2014 |

| Designated Activity Company (DAC) | Incorporated company | Limited by shares or guarantee | Taxed | Permitted | 2 | CRO | Companies Act 2014 |

| Public Limited Company (PLC) | Incorporated company | Limited by shares | Taxed | Permitted | 7 | CRO | Companies Act 2014 |

| Company Limited by Guarantee (CLG) | Incorporated company | Limited by guarantee | Often exempt | Permitted | 1 | CRO | Companies Act 2014 |

| Unlimited Company (UC / PUC) | Incorporated company | Unlimited | Taxed | Permitted | 1 | CRO | Companies Act 2014 |

| Branch / External Company | Registered presence | Per parent entity | Taxed | Permitted | N/A | CRO | Companies Act 2014, Part 21 |

| General Partnership | Unincorporated | Unlimited | Taxed (partners) | Permitted | 2 | Revenue Commissioners | Partnership Act 1890 |

| Limited Partnership | Unincorporated | Mixed | Taxed (partners) | Permitted | 2 | CRO | Limited Partnerships Act 1907 |

| Investment Limited Partnership | Unincorporated | Mixed | Taxed (partners) | Permitted | 2 | Central Bank of Ireland | Investment Limited Partnerships Act 1994 |

| Sole Trader | Unincorporated | Unlimited | Taxed (individual) | Permitted | 1 | Revenue Commissioners | N/A |

Each of these structures is examined in full in the sections below.

Public Limited Company (PLC)

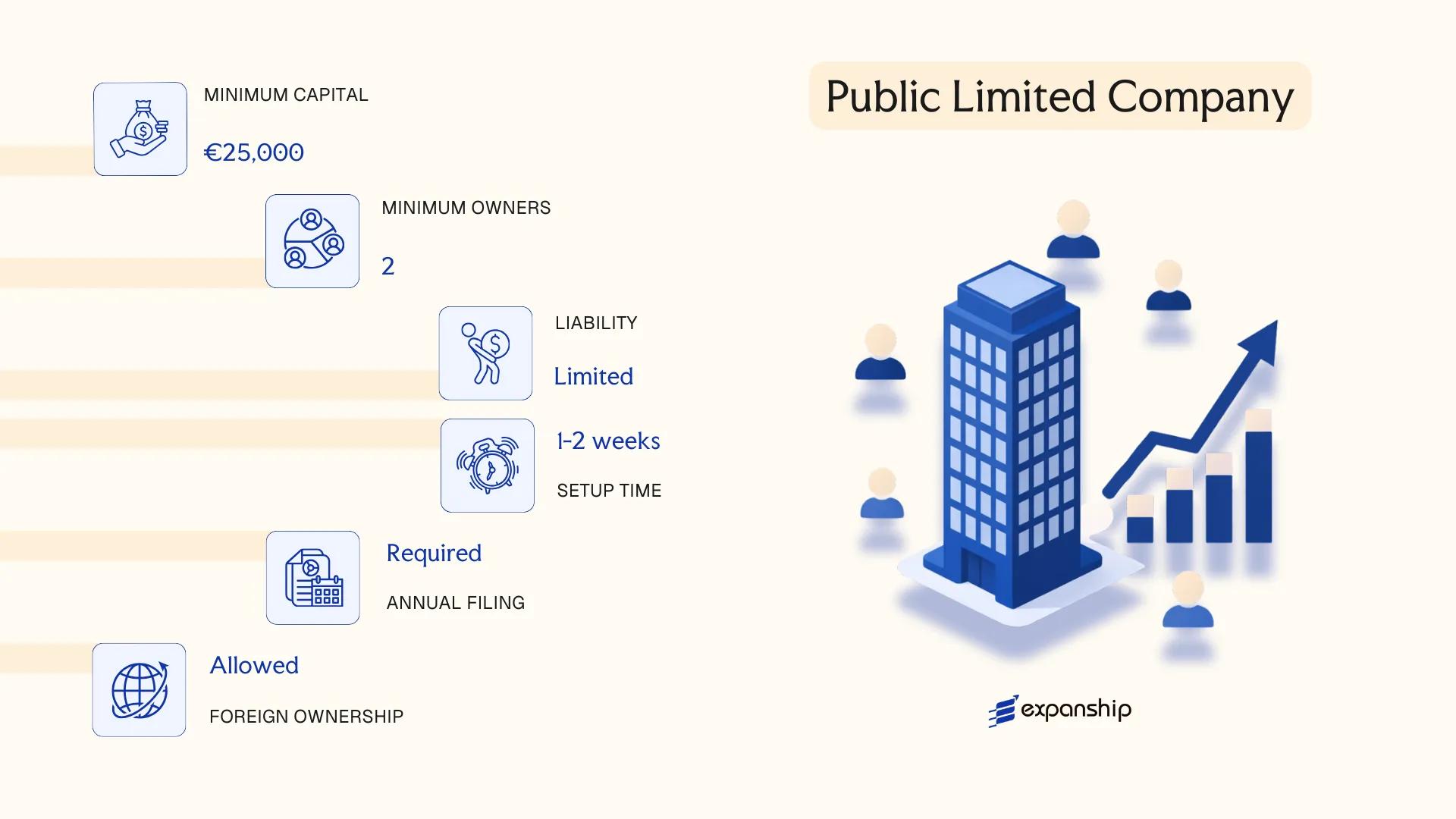

Governed by the Companies Act 2014, an Ireland Public Limited Company PLC is a distinct legal entity with separate legal personality and limited liability for its shareholders. It occupies a hybrid position in Irish company law — capable of offering shares to the public while also being used as a private holding structure where no public listing is intended.

Minimum share capital requirements and the ability to list on a recognised stock exchange distinguish this structure from most other Irish company forms. Registered with the Companies Registration Office (CRO), a PLC must have at least seven members and two directors, with no upper limit on shareholders.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (PLC) | Separate legal personality; governed by Companies Act 2014 |

| Members | Shareholders; minimum 7, no maximum | At least 2 directors required; 1 must be EEA-resident |

| Local Presence | Registered office in Ireland | Must maintain a CRO-registered address at all times |

| Capital | EUR 25,000 minimum authorised share capital; at least 25% paid up before trading | Shares may be offered to the public |

| Privacy | Accounts and shareholder details publicly filed with the CRO | Lower privacy than private structures |

Focus Points

- Taxation: Subject to corporation tax at 12.5% on trading income and 25% on passive income; standard VAT rate of 23% applies; dividend withholding tax at 25% (subject to exemptions); stamp duty on share transfers at 1%.

- Annual Compliance: Annual return and audited financial statements must be filed with the CRO; audit cannot be waived for a PLC.

- Treaty Access: Qualifies as an Irish tax resident entity and can access Ireland's extensive double tax treaty network (over 70 treaties in force).

- Listing Requirement: No obligation to list on a stock exchange; however, if listed, Euronext Dublin rules and additional regulatory obligations apply.

- Conversion: A PLC may re-register as a private limited company or DAC under Part 20 of the Companies Act 2014, subject to shareholder approval.

Closing

A PLC suits large-scale trading operations, cross-border group structures requiring public capital raising, or entities seeking a listed vehicle on Euronext Dublin. The ability to offer shares publicly is a clear structural advantage, though mandatory audits, a minimum of seven shareholders, and full public disclosure of financial accounts represent material administrative and compliance burdens.

Best suited for established businesses seeking public capital markets access or large multinational groups requiring a publicly accountable Irish entity.

Company Incorporation in Ireland

Incorporate your Irish PLC or other entity type with end-to-end support from Expanship's corporate services team.

Private Limited Company (Ltd)

Governed by the Companies Act 2014, the Ireland Private Limited Company (Ltd) is the most widely used corporate structure in the country. It carries separate legal personality, meaning the company exists as a distinct legal entity from its shareholders, and members' liability is limited to the amount unpaid on their shares.

Unlike most company forms, an Ltd under the 2014 Act does not require a constitution that specifies objects clauses — it has full unlimited capacity to carry on any lawful business activity by default.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private company limited by shares | Incorporated under Companies Act 2014 |

| Members | 1–149 shareholders | Shares cannot be offered to the general public |

| Directors | Minimum 1 director; at least one must be EEA-resident | A non-EEA resident sole director requires a Section 137 bond |

| Registered Office | Must maintain a registered address in Ireland | Used for official CRO and Revenue correspondence |

| Share Capital | No minimum capital requirement; denominated in any currency | Shares must be fully or partly paid |

| Company Secretary | 1 required; cannot be the sole director | Can be an individual or a body corporate |

Focus Points

- Taxation: Subject to 12.5% corporation tax on trading income; 25% on passive income; standard VAT rate of 23%; dividend withholding tax at 25% applies unless an exemption applies; stamp duty on share transfers at 1%.

- Annual Compliance: Must file an Annual Return with the Companies Registration Office (CRO) and financial statements with Revenue; audit exemption available for qualifying small companies.

- Tax Treaties: Ireland's extensive double taxation treaty network is accessible to Irish Ltd companies that establish tax residency through central management and control.

- Conversion: An Ltd can be re-registered as a DAC, PLC, or other permitted form under Part 20 of the Companies Act 2014.

- Restrictions: Shares may not be offered to the public; any such offering triggers mandatory conversion to a PLC.

Closing

The Ltd structure suits trading operations, holding arrangements, and IP-holding entities that require operational flexibility without the formalities attached to more regulated corporate forms. Its principal advantage is structural simplicity; the main limitation is the 149-shareholder cap, which restricts large-scale private equity structures.

Irish Ltd registration is most appropriate for SMEs, foreign subsidiaries, and entrepreneur-led businesses seeking limited liability with minimal constitutional constraints.

Designated Activity Company (DAC)

The Designated Activity Company is a distinct corporate form introduced under the Companies Act 2014, which consolidated and replaced much of Ireland's earlier company law. A DAC Ireland incorporation is defined primarily by its objects clause — a provision in the constitution that restricts the company to carrying out only the activities expressly stated within it.

As a body corporate, the DAC carries separate legal personality and offers limited liability to its members. This structure sits between a fully flexible private limited company and more restricted entities, making it a deliberate choice rather than a default registration form.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Designated Activity Company (DAC) | Governed by Part 16 of the Companies Act 2014 |

| Members | Minimum 1, maximum 149 | Referred to as shareholders; shares may or may not be issued depending on sub-type |

| Directors | Minimum 2 | At least one director must be EEA-resident, or a bond must be held |

| Registered Office | Required in Ireland | Must be a physical address; PO boxes are not accepted |

| Share Capital | No statutory minimum | Denominated in any currency; structure depends on sub-type |

| Objects Clause | Mandatory, restricted | Activities outside stated objects are ultra vires |

| Privacy | Beneficial ownership disclosed to the RBO | Register of members is not publicly accessible |

Focus Points

- Taxation: Subject to Ireland's 12.5% corporate tax rate on trading income and 25% on passive income; standard VAT registration thresholds apply; withholding tax on dividends applies at 25% unless treaty relief or exemptions are claimed; stamp duty of 1% applies on share transfers.

- Annual Compliance: Must file annual returns and financial statements with the Companies Registration Office (CRO); audit requirements depend on size thresholds.

- Economic Substance: No specific substance regime, but genuine trading activity is expected to support the 12.5% rate.

- Conversion: A DAC can convert to a private limited company (Ltd) or other permitted form by special resolution and CRO filing.

- Restrictions: Activities undertaken outside the stated objects clause carry legal risk; amending the objects requires a special resolution.

Sub-Types

DAC Limited by Shares

The standard form, where member liability is limited to the amount unpaid on their shares. Most commonly used for regulated financial vehicles, joint ventures, and structured finance arrangements where activity scope must be contractually or regulatorily defined.

DAC Limited by Guarantee (with share capital)

Member liability is limited by a guarantee amount rather than share value alone, though share capital is also present. This structure is less common and typically used where both equity participation and capped guarantee obligations are needed.

Closing

A designated activity company Ireland suits regulated financial entities, special purpose vehicles (SPVs), and joint ventures where restricting the company's scope by constitution is a commercial or compliance requirement. The defined objects clause provides contractual clarity to counterparties but reduces operational flexibility if the business evolves beyond its original purpose.

The DAC is best suited for structured finance vehicles, regulated entities, and joint ventures where limiting the company's activities by constitution is a legal, contractual, or regulatory necessity.

Company Limited by Guarantee (CLG)

A Company Limited by Guarantee CLG Ireland is governed by Part 18 of the Companies Act 2014. Unlike share-based structures, it has no share capital; instead, members guarantee a nominal amount — typically €1 — toward the company's debts in the event of winding up. The entity carries full separate legal personality and limited liability, making it a structurally distinct option for organisations that do not distribute profits to members.

Registered with the Companies Registration Office (CRO), a CLG must also comply with reporting obligations under the Companies Act 2014 and, where charitable status is sought, with the Charities Regulator under the Charities Act 2009.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate with separate legal personality | No share capital issued |

| Members | Minimum 1, no statutory maximum | Members replace shareholders; each provides a guarantee |

| Directors | Minimum 1 director; at least one must be EEA-resident or a Section 137 bond must be in place | A company secretary is also required |

| Registered Office | Physical address in Ireland | Must be maintained at all times |

| Capital | No share capital; member guarantee typically €1 | Not a fundraising mechanism |

| Privacy | Director names filed publicly at CRO; member details not publicly disclosed | Financial statements filed if above certain thresholds |

Focus Points

- Taxation: Subject to Irish corporation tax (12.5% on trading income, 25% on passive income); VAT registration required if turnover thresholds are met; charitable bodies may qualify for tax exemption under section 207 of the Taxes Consolidation Act 1997, removing corporation tax and income tax liability on qualifying income.

- Annual Compliance: Annual return and financial statements must be filed with the CRO; charitable CLGs file separately with the Charities Regulator.

- Profit Distribution: Profits must be applied to the entity's stated objects; distribution to members is prohibited.

- Conversion: A CLG may convert to another company type under Part 20 of the Companies Act 2014, subject to member approval and CRO filing.

- Treaty Access: As an Irish-resident entity, a CLG may access Ireland's tax treaty network, though treaty benefits on passive income depend on the entity's specific activities and tax-exempt status.

Closing

A CLG is the standard non-profit company structure in Ireland, used by charities, sporting bodies, professional associations, and membership organisations. The absence of share capital keeps ownership simple, though the prohibition on profit distribution makes it unsuitable for any venture with commercial return objectives.

This structure suits non-profit organisations, charities, and member-led associations that require limited liability without distributing profits.

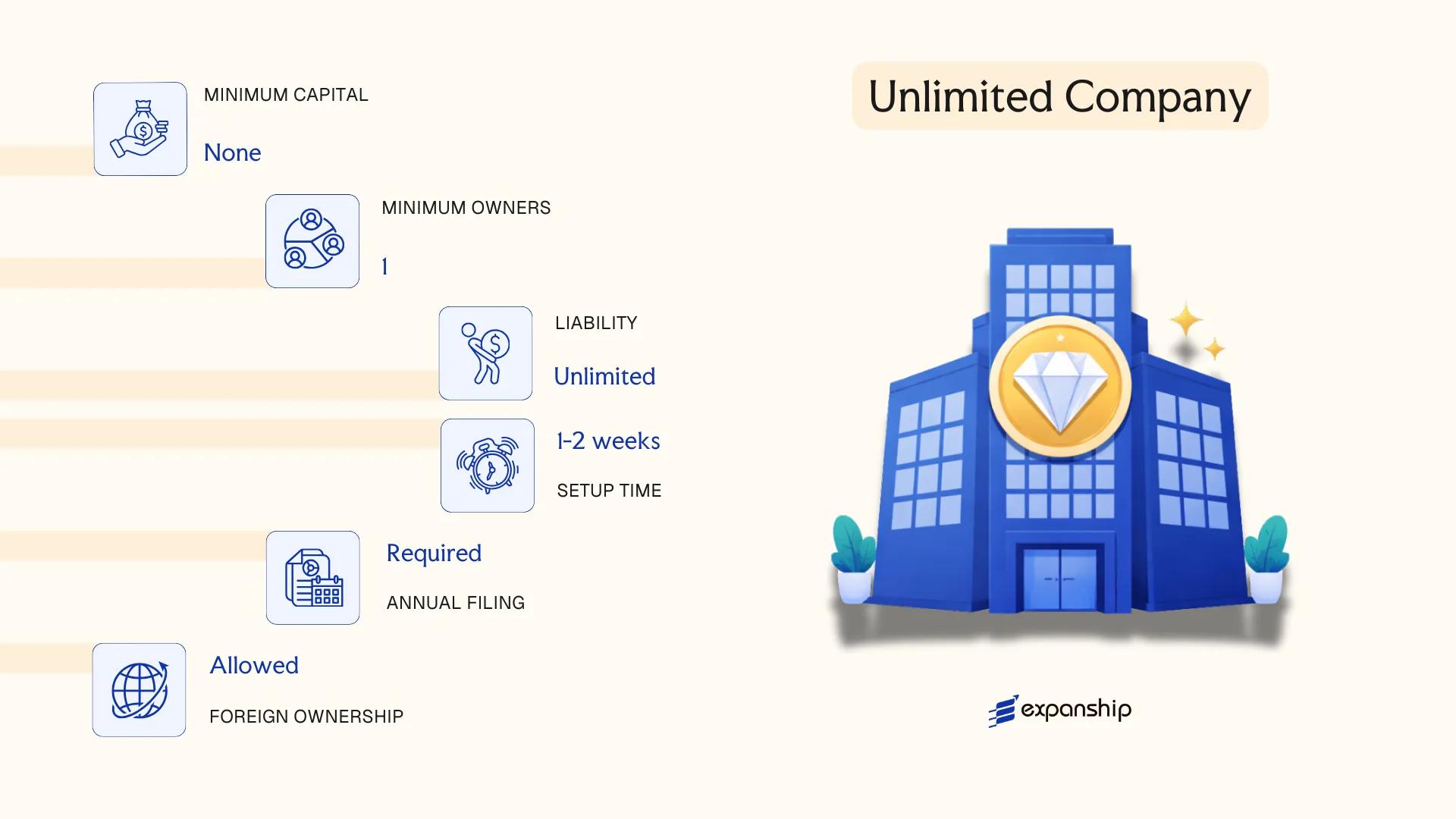

Unlimited Company (UC / PUC)

An unlimited company in Ireland — governed by the Companies Act 2014 — holds separate legal personality but imposes unlimited liability on its members. This means member assets can be called upon to meet company debts if the business is wound up. The structure is less common than limited-liability vehicles, yet it serves specific purposes where financial privacy outweighs the protection a liability cap provides.

Under the 2014 Act, two distinct forms exist: the private unlimited company (UC) and the public unlimited company (PUC). Both share the core characteristic of unlimited member liability while differing primarily in membership thresholds and public filing obligations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate with separate legal personality | Members bear unlimited personal liability on winding up |

| Members | UC: 1–149 members; PUC: minimum 2, no upper cap | Members are referred to as shareholders |

| Directors | Minimum 1 director; at least 1 must be EEA-resident (or bond posted) | A company secretary is also required |

| Registered Office | Physical address in Ireland required | Cannot be a PO box |

| Share Capital | No statutory minimum; denominated in any currency | Shares can be issued without par value |

| Financial Statements | UC: exempt from filing accounts at the CRO under certain conditions | PUC must file; the filing exemption is the primary draw of the UC structure |

Focus Points

- Taxation: Subject to Irish corporation tax (12.5% on trading income, 25% on passive income); standard VAT rules apply; withholding tax on dividends, interest, and royalties follows domestic rates unless treaty relief applies; stamp duty at 1% applies on share transfers.

- Annual Compliance: Annual return must be filed with the Companies Registration Office (CRO); UC may qualify for an exemption from attaching financial statements, subject to meeting specific ownership and structural conditions.

- Treaty Access: Qualifies as an Irish tax-resident entity for double tax treaty purposes, provided central management and control is exercised in Ireland.

- Conversion: A UC can be converted to a limited company under Part 20 of the Companies Act 2014, subject to shareholder resolution and CRO filings.

Sub-Types

Private Unlimited Company (UC)

The UC restricts membership to 149 and prohibits any invitation to the public to subscribe for shares or debentures. Its principal attraction is the potential exemption from publicly filing financial statements at the CRO, making it a preferred holding structure where balance sheet confidentiality is a priority.

Public Unlimited Company (PUC)

A PUC places no ceiling on the number of members and may offer securities to the public, though it does not benefit from the same financial-statement filing exemption available to the UC. This form is rarely chosen as a primary operating vehicle.

Unlimited companies are used primarily as holding entities, intra-group financing vehicles, and structures for asset holding where owners accept personal liability exposure in exchange for financial privacy. The filing exemption available to the UC is its most commercially significant feature; however, unlimited personal liability remains a material risk that makes this structure unsuitable for businesses carrying significant operational or debt exposure.

The UC structure is most appropriate for wholly owned subsidiaries within multinational groups where the parent entity is prepared to accept unlimited liability and values confidentiality over the statutory protection of a liability cap.

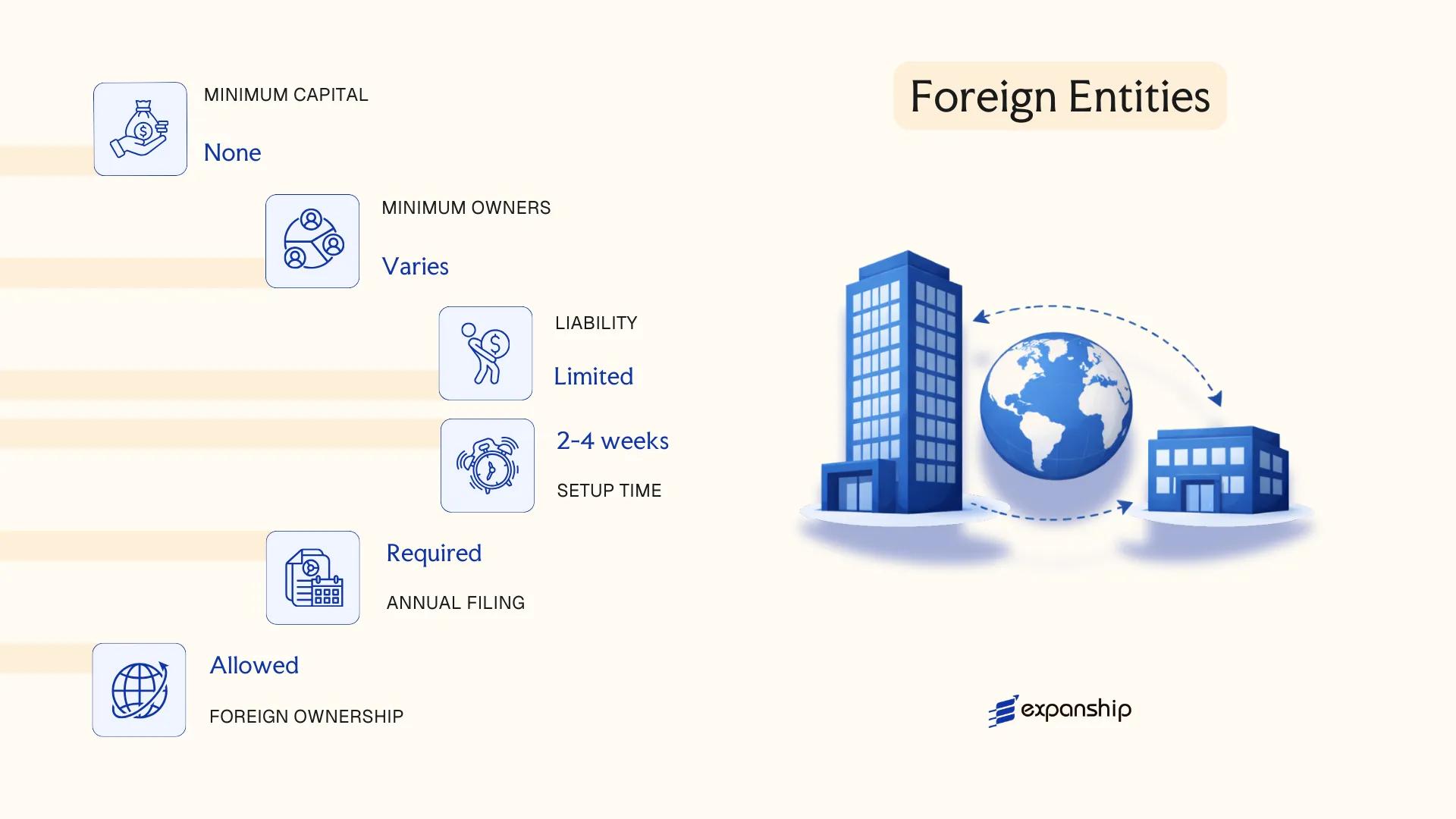

Foreign Entities in Ireland [Branch Office, External Company Registration]

Registering a foreign branch in Ireland is governed by Part 21 of the Companies Act 2014, which applies to external companies establishing a physical presence within the state. A branch does not constitute a separate legal entity; it remains an extension of the parent company, which retains full liability for the branch's obligations.

External company registration Ireland requires filing with the Companies Registration Office (CRO). Non-EEA companies face additional disclosure requirements compared to EEA-incorporated entities, including certified constitutional documents and details of persons authorised to represent the firm.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch of a foreign parent company | Not a separate legal entity; parent bears full liability |

| Registered Persons | Authorised representative(s) in Ireland | Must be named in CRO filings; at least one required |

| Local Presence | Registered address and authorised agent in Ireland | Physical place of business required for registration |

| Capital | No minimum capital requirement | Parent company's capital structure applies |

| Disclosure | Parent company accounts must be filed annually with the CRO | EEA companies have lighter filing obligations than non-EEA firms |

| Privacy | Parent financials become publicly accessible via CRO | Less privacy than a separately incorporated subsidiary |

Focus Points

- Taxation: Branches are subject to 12.5% corporation tax on Irish-source trading profits; transfer pricing rules apply to transactions with the parent; VAT registration required if turnover exceeds the applicable threshold.

- Economic Substance: The branch must demonstrate genuine activity in Ireland; a purely administrative presence may attract scrutiny from Revenue.

- Annual Compliance: Audited parent accounts and an annual return must be filed with the CRO; deadlines depend on the parent's own financial year.

- Treaty Access: Access to Ireland's double taxation treaty network depends on the parent entity's residence; treaty benefits are not automatically conferred on the branch itself.

- Restrictions: Banks and regulated sectors may require a separately incorporated subsidiary rather than accepting a branch structure.

Sub-Types

EEA Branch

An EEA branch, where the parent is incorporated within the European Economic Area, benefits from reduced CRO disclosure requirements under Schedule 21A of the Companies Act 2014. Documentation requirements are lighter, and the registration process is generally more straightforward.

Non-EEA Branch

A non-EEA branch is subject to stricter filing obligations, including certified and translated constitutional documents, full parent company accounts, and a list of all directors of the parent entity. This structure is typically used by multinational firms testing the Irish market before committing to a full subsidiary incorporation.

Closing Paragraph

A branch structure suits foreign businesses that need a market presence without incorporating a new legal entity, though the lack of liability separation between the parent and the branch remains a material commercial consideration.

Foreign companies seeking a low-cost, temporary, or exploratory presence in Ireland before committing to full subsidiary incorporation.

Partnerships in Ireland [General Partnership, Limited Partnership, Investment Limited Partnership]

Partnership structures in Ireland are governed primarily by the Partnership Act 1890 for general partnerships, the Limited Partnerships Act 1907 for limited partnerships, and the Investment Limited Partnerships Act 1994 (as significantly amended in 2020) for investment limited partnerships. None of these structures carry separate legal personality, meaning partners bear direct legal exposure to the entity's obligations.

Registration requirements and compliance obligations vary considerably across the three forms. General partnerships may operate without formal registration, while limited partnerships must register with the Companies Registration Office (CRO), and investment limited partnerships require authorisation from the Central Bank of Ireland.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated association | No separate legal personality across all three types |

| Members | Partners (general and/or limited) | GP: min. 2, no statutory maximum; LP: min. 1 general + 1 limited partner; ILP: min. 1 general partner |

| Local Presence | Registered address in Ireland required for LP and ILP | GP has no mandatory registration; ILP must have a CBI-authorised manager |

| Capital | No prescribed minimum; denominated in any currency | ILP capital is typically held in fund-grade structures |

| Privacy | Partner details filed with CRO for LP and ILP | GP partners are not publicly registered |

Focus Points

- Taxation: Partnerships are tax-transparent; each partner is taxed on their share of income at their applicable rate. No entity-level corporation tax applies, though VAT registration may be required depending on activity. Stamp duty applies to transfers of partnership interests in certain circumstances.

- Annual Compliance: LPs must file annual returns with the CRO; ILPs are subject to ongoing Central Bank regulatory reporting.

- Treaty Access: Tax treaty access depends on the partner's residence, not the partnership itself, as the structure is fiscally transparent.

- Restrictions: Limited partners in an LP lose liability protection if they participate in management; ILPs are restricted to collective investment purposes.

Sub-Types

General Partnership

Partners share unlimited joint and several liability. No registration is required, making this the least formal structure available, though it offers no liability protection.

Limited Partnership

Registered with the CRO under the Limited Partnerships Act 1907, this structure allows limited partners to cap liability to their capital contribution, provided they take no active role in management. Ireland limited partnership registration is straightforward but carries ongoing filing obligations.

Investment Limited Partnership (ILP)

Authorised and supervised by the Central Bank of Ireland, the Irish Investment Limited Partnership ILP is used exclusively for collective investment schemes, including private equity, venture capital, and alternative fund structures. The 2020 amendments aligned it with international fund structuring standards.

Closing

Partnerships suit joint ventures, professional services firms, and regulated fund structures depending on the variant chosen. The tax transparency of all three forms is a notable structural advantage, but the absence of limited liability in a general partnership and the management restrictions in a limited partnership require careful structural planning.

Investment limited partnerships are best suited to fund managers and institutional investors structuring regulated alternative investment vehicles under Central Bank oversight.

Sole Trader

Sole trader registration in Ireland does not create a separate legal entity. You and your business are treated as one and the same in law, meaning personal assets are exposed to any debts or liabilities incurred through trading. There is no governing incorporation statute — instead, the framework is established through Revenue registration and, where a trading name differs from your own name, the Registration of Business Names Act 1963.

Operating as a self-employed sole trader in Ireland requires registration with Revenue through the eRegistration system or by submitting a TR1 form. If your turnover exceeds, or is likely to exceed, the VAT registration thresholds (currently €40,000 for services and €80,000 for goods), VAT registration is also required.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality; owner and business are legally identical |

| Referred To As | Sole trader / proprietor | No shareholders, directors, or members |

| Membership | Single individual only | Cannot have co-owners; a second owner requires a partnership structure |

| Local Presence | Irish-resident individual | Must be personally based or operating in the jurisdiction |

| Capital | No minimum | No share capital required; fully funded by the proprietor |

| Business Name | Optional registration | Required under the Registration of Business Names Act 1963 if trading under a name other than your own |

Focus Points

- Taxation: Income taxed under personal income tax (up to 40%), USC, and PRSI as a self-assessed individual; VAT registration required above statutory thresholds; no corporate tax, withholding tax obligations, or stamp duty on formation.

- Annual Compliance: Self-assessment income tax return (Form 11) filed annually with Revenue by 31 October (or mid-November via ROS).

- Conversion: Can convert to a private limited company at any time, though the process involves incorporation, asset transfer, and potential tax implications.

- Restrictions: Cannot raise equity investment or issue shares; unsuitable for businesses seeking external capital or limiting personal liability.

- Treaty Access: As an individual, you may access Ireland's tax treaty network for personal income, but treaty benefits applicable to companies do not apply.

Closing Paragraph

A sole trader structure suits low-risk, owner-operated businesses where simplicity and low administrative cost outweigh the need for liability protection. The primary drawback is unlimited personal liability — all business debts are recoverable against your personal assets.

Freelancers, consultants, and early-stage sole operators testing a business concept before committing to a formal corporate structure.

How to Choose the Right Entity Type in Ireland

Selecting how to structure a business in Ireland determines not just administrative overhead, but legal exposure, tax treatment, and long-term operational flexibility.

Why Your Entity Choice Matters

Registering the wrong structure carries concrete consequences:

- Operating as a branch without registering as an external company under Part 21 of the Companies Act 2014 can result in regulatory penalties or striking off by the Companies Registration Office.

- Choosing a tax-exempt entity, such as a CLG, means your business cannot access Ireland's double taxation treaty network, blocking withholding tax reductions in counterpart countries.

- Selecting a structure without genuine substance capacity when transfer pricing or anti-avoidance rules apply triggers reporting failures under Revenue Commissioners guidelines and potential financial penalties.

- Forming a limited company when asset protection or estate planning is the primary goal locks your business into annual shareholder obligations, AGM requirements, and CRO filings that would not apply under a trust or foundation arrangement.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as investment funds each point toward a different structure under Irish law.

- Ownership and Management: A single-director, single-shareholder firm has different governance needs than a multi-party venture requiring a formal board structure.

- Tax Objectives: Your need for treaty access, the 12.5% trading rate, or full exemption will eliminate certain entity types from consideration.

- Liability Exposure: Whether unlimited liability is acceptable determines whether a UC or PUC is viable for your circumstances.

- Substance Capacity: If you cannot maintain directors, staff, or decision-making functions in Ireland, certain structures carry greater compliance risk than others.

- Exit Strategy: Not all Irish entities permit redomiciliation or conversion; confirm that the chosen structure supports your intended exit mechanism before incorporating.

Compliance Services for Companies in Ireland

Ongoing compliance support for Irish-registered entities, including annual returns, CRO filings, and statutory obligations.

Conclusion

Each entity type governed under the Companies Act 2014 serves a distinct purpose. The Private Limited Company (Ltd) remains the most registered structure in Ireland, favoured for its flexible constitution and general commercial use. Designated Activity Companies suit businesses requiring a defined, restricted object clause. Public Limited Companies apply where public capital-raising is the objective. Companies Limited by Guarantee serve membership-based or non-profit organisations. Unlimited Companies offer structural privacy at the cost of member liability. Branches and external company registrations give foreign firms a foothold without local incorporation. Partnerships and sole trader arrangements cover smaller or professionally structured operations.

Incorporating in Ireland key takeaways point toward a jurisdiction that continues to attract international holding and trading structures, supported by an expanding tax treaty network and sustained engagement with OECD frameworks. Expanship's team works directly with these structures across formation, compliance, and ongoing maintenance.

How Expanship Can Assist You

Expanship provides end-to-end corporate services for Ireland company setup, covering every structure examined in this guide — from a Private Limited Company (Ltd) to a Designated Activity Company (DAC) or a foreign branch registration. Our team works directly within the framework set by the Companies Registration Office (CRO) and ensures your chosen structure is formed correctly from the outset.

From document preparation through to post-incorporation maintenance, our Ireland incorporation services cover what your business actually needs:

- Preparation and legalization of incorporation documents

- Registered office and company secretary provision (mandatory under Irish law)

- CRO filings and government liaison

- Ongoing annual return and compliance management

- Banking introduction assistance

Your dedicated point of contact handles each step directly, so nothing falls between the cracks after registration.

Reach out to Expanship Ireland to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Private Limited Company (Ltd) is the most frequently incorporated structure, registered under the Companies Act 2014. It requires only one director and one shareholder, imposes no minimum share capital, and limits member liability to their subscribed shares.

Both structures offer limited liability, but a DAC must have a defined objects clause restricting its permitted activities, while a Ltd operates with unrestricted capacity. The compliance burden is broadly similar, though a DAC is better suited for entities that require contractual or regulatory certainty around their business scope.

No Irish structure eliminates public disclosure entirely, as the Companies Registration Office (CRO) maintains publicly searchable registers of directors and beneficial owners. An Unlimited Company (UC) is exempt from filing financial statements publicly, which provides a degree of financial privacy not available to limited companies.

A sole trader arrangement involves only one individual by definition. A General Partnership requires at least two partners, while a Private Limited Company can be formed with one director and one shareholder, who may be the same person.

Yes. There is no nationality or residency requirement for shareholders. However, under the Companies Act 2014, at least one director must be a resident of an EEA state, or the company must hold a Section 137 bond as a non-EEA director surety.

The Companies Act 2014 provides formal re-registration procedures allowing conversion between several entity types, including from a Private Limited Company to a DAC or PLC, and vice versa. Not all conversions are available in every direction, and specific conditions, including member resolutions and CRO filings, must be met.

Limited companies, DACs, PLCs, CLGs, and Unlimited Companies all possess separate legal personality under the Companies Act 2014. General Partnerships do not have separate legal personality, meaning partners remain personally liable for partnership obligations.

The Investment Limited Partnership (ILP), governed by the Investment Limited Partnerships Act 1994 as amended, is specifically designed for regulated fund vehicles. It is commonly used for private equity and alternative asset structures authorised by the Central Bank of Ireland.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.