Key Takeaways

- The PT PMA (Perusahaan Penanaman Modal Asing) is the standard legal vehicle for foreign direct investment in Indonesia, regulated through the Investment Coordinating Board (BKPM) via the Online Single Submission (OSS) system.

- Foreign business structures such as the Representative Office (KPPA) and Foreign Representative Office (KP3A) are restricted to non-commercial activities, making them unsuitable for revenue-generating operations.

- Company registration in Indonesia falls under the Ministry of Law and Human Rights (Kementerian Hukum dan Hak Asasi Manusia) through its Directorate General of General Law Administration (AHU), which administers the country's legal entity system.

- A local PT is subject to no foreign investment restrictions and is the appropriate structure for Indonesian-resident founders seeking full domestic ownership, whereas a PT Tbk applies exclusively to companies intending to list on the Indonesia Stock Exchange.

Introduction to Entity Types in Indonesia

Indonesia is an archipelago nation in Southeast Asia, bordered by Malaysia, Papua New Guinea, and Timor-Leste, and comprising over 17,000 islands across a territory that spans from the Indian Ocean to the Pacific. Choosing among the types of business entities in Indonesia requires an understanding of local corporate law, foreign ownership restrictions, and the regulatory framework that governs commercial activity in the country.

Company registration falls under the jurisdiction of the Ministry of Law and Human Rights (Kementerian Hukum dan Hak Asasi Manusia), which administers the legal entity system through its Directorate General of General Law Administration (AHU). The Investment Coordinating Board (BKPM), now integrated into the Ministry of Investment, oversees foreign investment licensing. Indonesia operates a territorial tax system, with resident entities taxed on Indonesian-sourced and worldwide income depending on residency status.

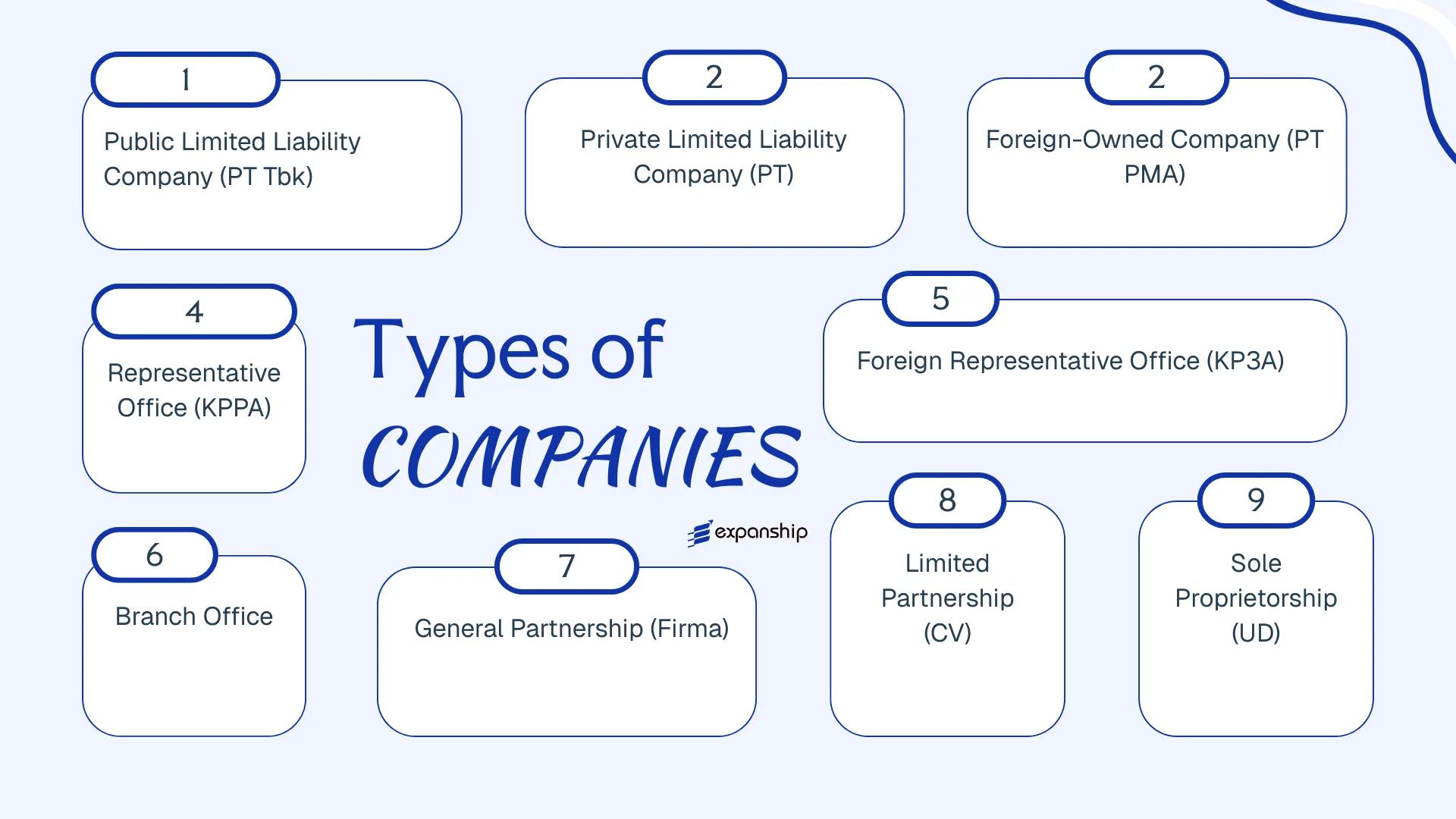

The principal business structures available include the Perseroan Terbatas (PT), Perseroan Terbuka (PT Tbk), Perusahaan Penanaman Modal Asing (PT PMA), Representative Office (KPPA), Foreign Representative Office (KP3A), Branch Office, General Partnership (Firma), Limited Partnership (CV), and Sole Proprietorship (UD). Each structure carries distinct implications for liability, foreign ownership eligibility, and permitted commercial activity — this article examines each in detail.

An Overview of Business Structures in Indonesia

Under Indonesia's company law framework, several distinct entity types are available to domestic and foreign investors, each governed primarily by Law No. 40 of 2007 on Limited Liability Companies (Undang-Undang Perseroan Terbatas), alongside sector-specific regulations and the Investment Law No. 25 of 2007. An overview of business structures in Indonesia reveals that the available forms range from fully foreign-owned companies to local partnerships and sole proprietorships. Each structure carries different implications for ownership, liability, and permitted commercial activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| PT Tbk | Public LLC | Limited | Taxed | Yes | 2 shareholders | OJK / MCI | Law No. 40/2007 |

| PT | Private LLC | Limited | Taxed | Yes | 2 shareholders | MCI (OSS) | Law No. 40/2007 |

| PT PMA | Foreign-owned LLC | Limited | Taxed | Restricted | 2 shareholders | BKPM / OSS | Law No. 25/2007 |

| KPPA | Rep. Office | N/A | Exempt | No | 1 appointee | MCI | MCI Regulation |

| KP3A | Foreign Rep. Office | N/A | Exempt | No | 1 appointee | MCI | MCI Regulation |

| Branch Office | Branch | Parent liable | Taxed | Limited | N/A | Sector regulator | Sector-specific |

| Firma | General Partnership | Unlimited | Taxed | Yes | 2 partners | MCI | Civil/Trade Code |

| CV | Limited Partnership | Mixed | Taxed | Yes | 2 partners | MCI | Civil/Trade Code |

| UD | Sole Proprietorship | Unlimited | Taxed | Yes | 1 owner | Local government | Local regulation |

Each of these structures is examined in full in the sections below.

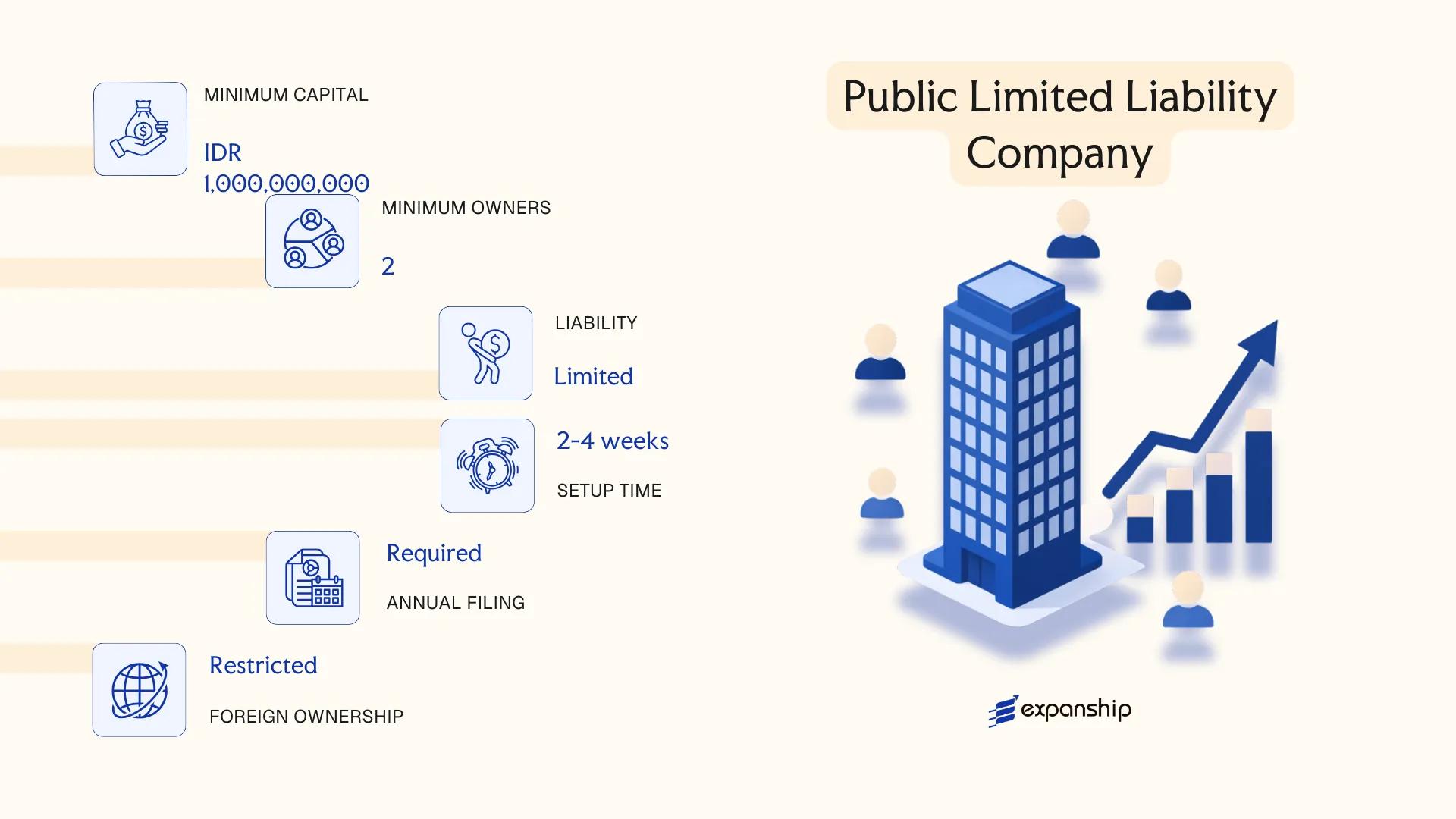

Perseroan Terbuka (PT Tbk) — Public Limited Liability Company

A PT Tbk public company Indonesia is governed by Law No. 40 of 2007 on Limited Liability Companies (Undang-Undang Perseroan Terbatas), alongside Law No. 8 of 1995 on Capital Markets and the regulations issued by the Otoritas Jasa Keuangan (OJK), the Financial Services Authority.

As a separate legal entity, the PT Tbk carries its own rights and obligations distinct from its shareholders. Liability is limited to each shareholder's subscribed capital, and shares are offered to the public through listing on the Indonesia Stock Exchange (Bursa Efek Indonesia/BEI).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Publicly listed limited liability company | Separate legal personality; shareholders not personally liable beyond their shareholding |

| Members | Minimum 2 shareholders (individuals or entities); no maximum | Board of Directors (min. 2 directors) and Board of Commissioners (min. 2 commissioners) required |

| Share Structure | Minimum 300 shareholders and minimum 30% free float post-IPO | OJK requires public ownership threshold to maintain listed status |

| Local Presence | Registered office address in Indonesia required | Physical presence mandatory; registered address must be operational |

| Capital | Minimum issued capital IDR 30 billion for main board listing (BEI rules) | Authorised capital must be at least 4x issued capital; denominated in IDR |

| Privacy | Shareholder register and financial statements publicly disclosed | Annual reports and audited financials filed with OJK and publicly available |

Focus Points

- Taxation: Subject to a standard corporate income tax rate of 22%; listed companies with at least 40% public float may qualify for a 3% reduction; VAT at 11% on taxable supplies; withholding tax applies to dividends, interest, and royalties at rates varying by tax treaty access.

- Annual Compliance: Audited financial statements must be submitted to OJK within 90 days of financial year-end; annual general meeting of shareholders (RUPS) required within 6 months of year-end.

- OJK Oversight: Ongoing reporting obligations include quarterly financials, material information disclosures, and corporate action notifications to OJK and BEI.

- Conversion: A private PT may convert to PT Tbk status through an IPO process, requiring OJK registration and BEI listing approval; the reverse process requires delisting procedures.

- Foreign Ownership: Restrictions under the Negative Investment List (now superseded by the Priority Scale List under Government Regulation No. 10 of 2021) may cap foreign shareholding in certain sectors even in publicly listed entities.

Closing

The PT Tbk structure suits large enterprises seeking access to public capital markets, institutional investors, or an exit mechanism for existing shareholders. The primary advantage is unrestricted access to equity capital through public share issuance; the principal drawback is the significant regulatory burden imposed by continuous OJK disclosure and compliance obligations.

PT Tbk is best suited for established Indonesian businesses with a proven financial track record that are seeking to raise public capital or achieve a market listing on the BEI.

Company Incorporation in Indonesia

Expanship assists with entity formation and registration across all company types in Indonesia, from private PT structures to publicly listed PT Tbk entities.

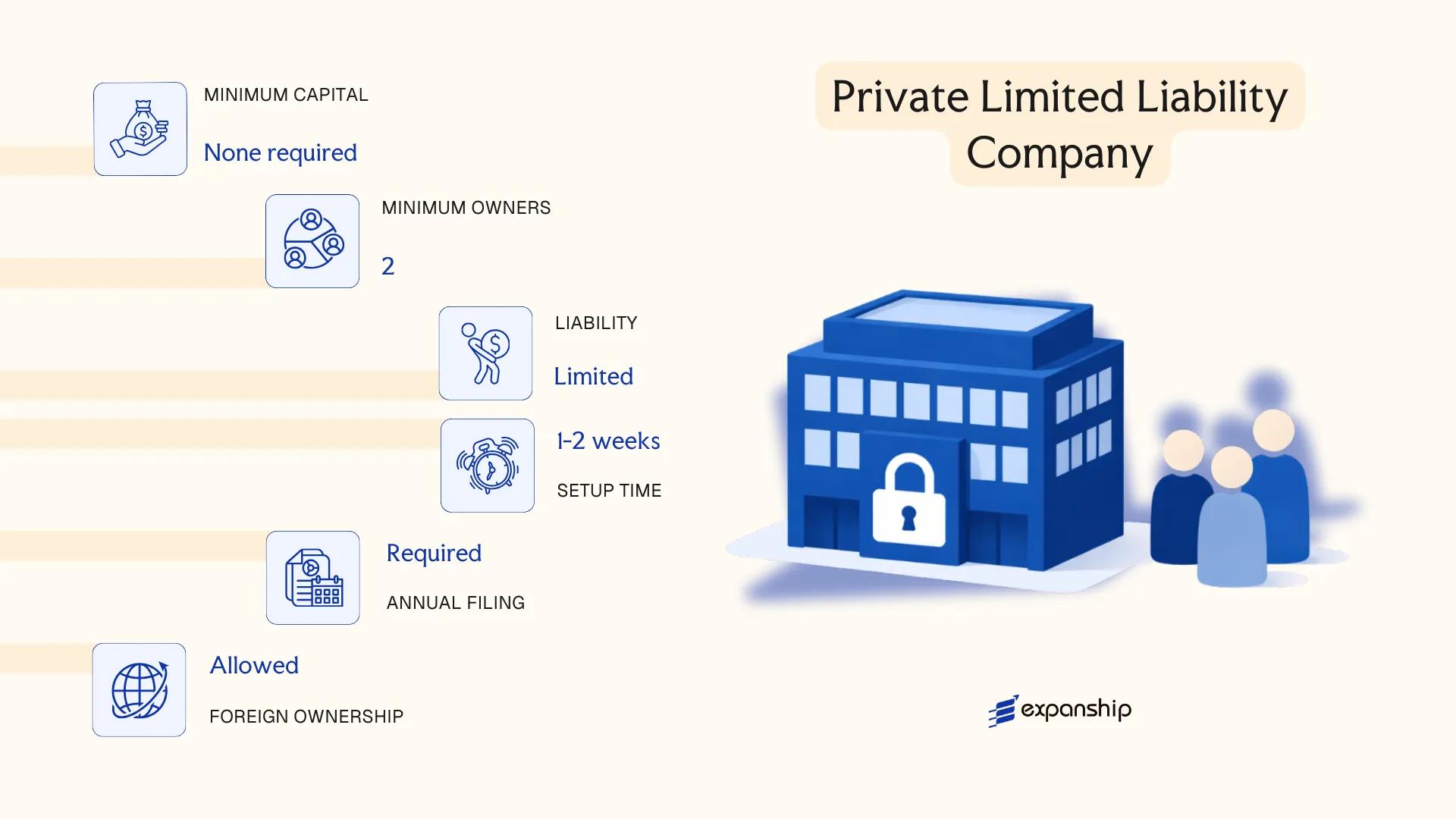

Perseroan Terbatas (PT) — Private Limited Liability Company

Governed by Law No. 40 of 2007 on Limited Liability Companies (Undang-Undang Perseroan Terbatas), the PT private limited company Indonesia is the most widely used domestic business structure for commercial activity. It carries separate legal personality, meaning the entity's assets and liabilities are distinct from those of its shareholders.

Liability exposure for shareholders is capped at their respective capital contributions. This structure suits a range of activities — from trading and manufacturing to holding and services — and forms the baseline against which other entity variants are measured.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Liability Company | Incorporated under Law No. 40 of 2007 |

| Members | Min. 2 shareholders; no statutory maximum | Shareholders may be individuals or legal entities; single-shareholder PTs are not permitted under standard rules |

| Directors & Commissioners | Min. 1 Director; min. 1 Commissioner | Both roles are mandatory; foreign nationals may hold director positions subject to manpower regulations |

| Local Presence | Registered address in Indonesia required | Must reflect actual domicile; a virtual office may be acceptable depending on the business activity |

| Capital | IDR 50 million minimum authorised capital; 25% must be issued and paid-up | Certain sectors impose higher minimum capital thresholds |

| Privacy | Shareholder and director data filed with the Ministry of Law and Human Rights (Kemenkumham) | Data is accessible via the AHU Online system; not fully private |

Focus Points

- Taxation: Subject to a standard corporate income tax rate of 22%; VAT at 11% applies to taxable goods and services; withholding tax obligations arise on dividends, royalties, and service fees; stamp duty applies to certain documents.

- Annual Compliance: Annual financial statements and GMS (General Meeting of Shareholders) are required; larger entities must have financial statements audited by a registered public accountant.

- Treaty Access: As a domestic entity, a PT can access Indonesia's tax treaty network, subject to meeting beneficial ownership and anti-avoidance requirements.

- Restrictions: Certain sectors restrict or prohibit foreign shareholding under the Negative Investment List (now governed by Government Regulation No. 10 of 2021); a domestically owned PT has no such foreign ownership ceiling.

- Conversion: A PT may be converted into a PT Tbk (public company) upon meeting the capital and shareholder thresholds prescribed by the Financial Services Authority (OJK).

A PT is suited to domestic trading, holding structures, and service businesses where full operational presence is required. Its primary advantage is straightforward access to local contracts, licences, and the banking system. The main limitation is that full foreign ownership is not available under this structure; for that, a PT PMA is required instead.

Domestically owned businesses or joint ventures where Indonesian shareholders hold the majority stake and full operational activity is intended.

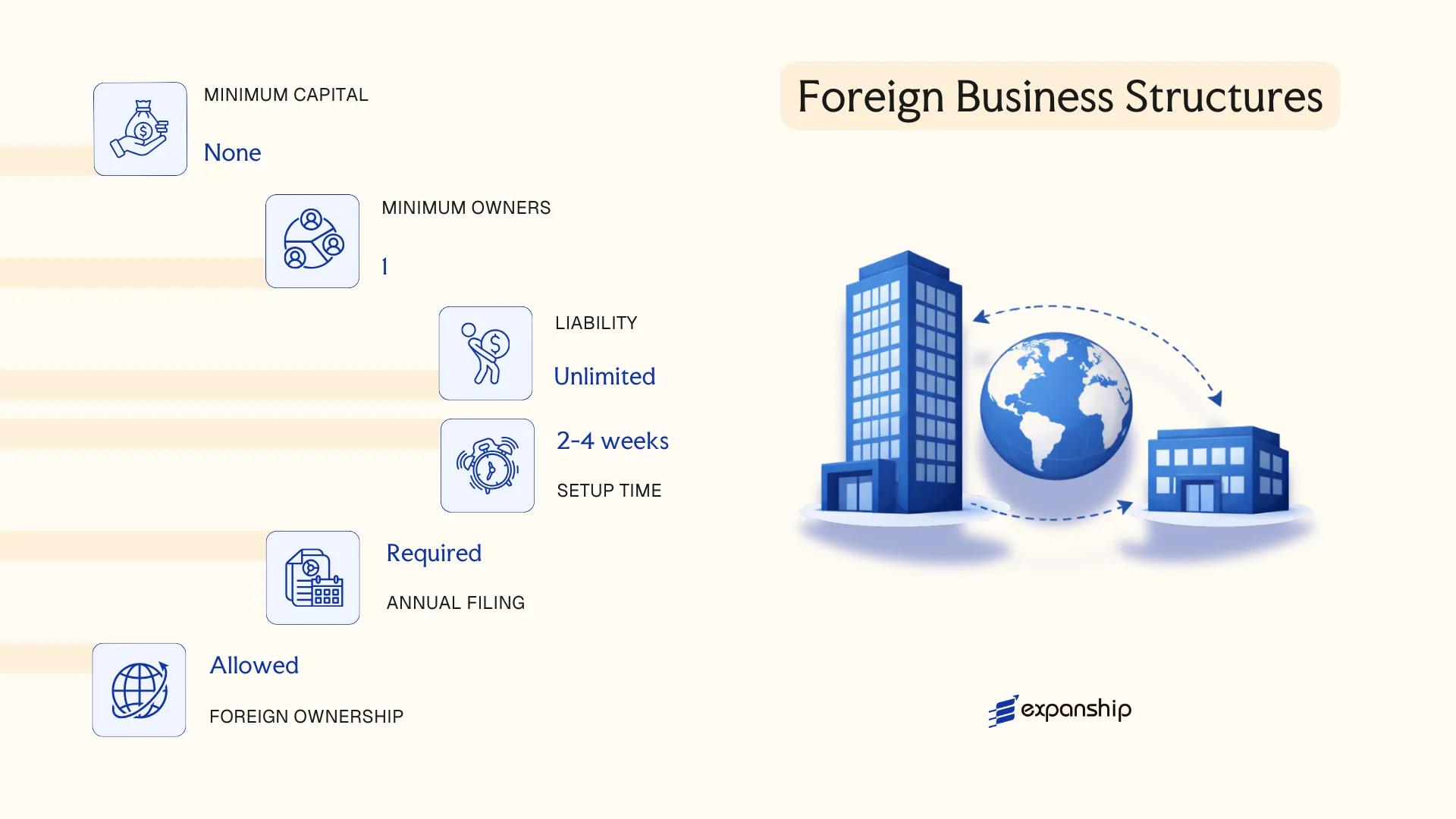

Perusahaan Penanaman Modal Asing (PT PMA) — Foreign-Owned Company

A PT PMA foreign company Indonesia is the primary vehicle through which foreign investors conduct active business operations in the country. It is governed by Law No. 25 of 2007 on Investment (the Investment Law) and regulated by the Indonesia Investment Coordinating Board, known as BKPM (Badan Koordinasi Penanaman Modal), now operating under the Ministry of Investment.

As a separate legal entity, the PT PMA carries its own rights and obligations distinct from its shareholders. Foreign ownership is permitted, though the extent of permissible ownership is determined by the Negative Investment List (Daftar Negatif Investasi), which designates sectors either closed to foreign capital or subject to ownership caps.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability company with foreign shareholding | Separate legal personality; shareholders' liability limited to share capital |

| Members | Min. 2 shareholders (individuals or entities); no maximum | At least 1 Director and 1 Commissioner required |

| Foreign Ownership | Up to 100% in open sectors; restricted or prohibited in certain sectors | Determined by the Positive Investment List under OSS (Online Single Submission) |

| Local Presence | Registered office address in Indonesia required | Virtual offices accepted in certain regions; physical presence required for operational licences |

| Capital | Minimum paid-up capital of IDR 10 billion (~USD 625,000); minimum issued capital IDR 2.5 billion | Applies per business activity; lower thresholds may apply in special economic zones |

| Privacy | Shareholder and director details recorded in company deed and BKPM registry | No public beneficial ownership register, though reporting obligations exist |

Focus Points

- Taxation: Subject to 22% corporate income tax; 11% VAT on taxable supplies; withholding tax applies to dividends, interest, and royalties at rates varying by tax treaty status; stamp duty applies to certain instruments.

- Treaty Access: Indonesia maintains an active tax treaty network; PT PMA entities may access treaty benefits subject to anti-treaty shopping provisions under Minister of Finance Regulation No. 49 of 2019.

- Annual Compliance: Annual financial statements, mandatory audit for certain thresholds, BKPM investment activity reports (LKPM) submitted quarterly, and annual tax return filing required.

- Sector Restrictions: Foreign investment company Indonesia registration is subject to the Positive Investment List (Presidential Regulation No. 10 of 2021), which restricts or conditions foreign participation in specific industries.

- Conversion: A PT PMA can be converted to a domestic PT if foreign shareholders divest, subject to notarial deed amendment and re-registration with the Ministry of Law and Human Rights.

Closing

The PT PMA structure suits foreign investors seeking to establish an operational presence for trading, manufacturing, or services. The primary advantage is the ability to repatriate profits and hold foreign equity; the principal limitation is the minimum capital threshold, which can exclude smaller ventures.

Foreign companies or investors seeking majority or full ownership of an active business operation in Indonesia across eligible sectors.

Foreign Business Structures [Representative Office (KPPA), Foreign Representative Office (KP3A), Branch Office]

Foreign entities seeking a presence in Indonesia without establishing a locally incorporated company have three primary structural options. The foreign representative office Indonesia KPPA framework, along with the KP3A and branch office models, is governed under the Investment Law (Law No. 25 of 2007) and further regulated by the Investment Coordinating Board, known as BKPM (now integrated into the Ministry of Investment).

None of these structures carry separate legal personality distinct from their foreign parent. They are extensions of the overseas entity, meaning the parent company bears full legal and financial responsibility for their activities in-country.

Key Characteristics

| Requirement | KPPA | KP3A | Branch Office |

|---|---|---|---|

| Legal Form | Representative office (non-legal entity) | Foreign trade representative office (non-legal entity) | Extension of foreign parent (non-legal entity) |

| Permitted Activities | Liaison and promotion only; no direct commercial transactions | Market research, promotion; no revenue-generating activity | Can conduct limited commercial operations depending on sector |

| Governing Authority | BKPM / Ministry of Investment | Ministry of Trade | Sector-specific regulators (e.g., OJK for financial services) |

| Local Presence | Must appoint a Chief Representative; registered office required | Representative and registered address required | Registered address; local representative required |

| Capital Requirement | None prescribed | None prescribed | None prescribed, but parent's financial standing is assessed |

| Permitted Duration | Typically 3 years, renewable | Typically 3 years, renewable | Subject to sector licence terms |

Focus Points

- Taxation: KPPA and KP3A offices are generally not subject to corporate income tax on Indonesian-sourced revenue since they cannot generate it; however, employee salaries are subject to Article 21 withholding tax, and any reimbursements from the parent may attract scrutiny under transfer pricing rules.

- Commercial Restrictions: Neither the KPPA nor KP3A may issue invoices, sign sales contracts, or receive payment for goods or services directly.

- Annual Compliance: All three structures must file activity reports with their respective governing authority and renew licences within prescribed periods.

- Conversion: Converting a representative office into a PT PMA requires a separate incorporation process; the representative office cannot be directly converted.

- Treaty Access: Since these structures are not taxpaying entities in the conventional sense, access to double tax treaty benefits is limited and depends on the parent's residency status.

Sub-Types

KPPA (Kantor Perwakilan Perusahaan Asing)

Established under BKPM regulations, the KPPA is used by foreign companies in the trade and industry sectors to conduct liaison activities, coordinate with local partners, and oversee market entry preparation. It cannot employ Indonesian nationals in senior representative roles without specific authorisation.

KP3A (Kantor Perwakilan Perusahaan Perdagangan Asing)

Regulated by the Ministry of Trade, the KP3A Indonesia foreign office setup is specific to foreign trading companies. Its permitted scope is narrower than a branch office but slightly distinct from the KPPA in that it falls under trade sector regulations rather than general investment rules.

Branch Office

Available only in select regulated sectors such as banking, insurance, and construction, a branch office may conduct limited revenue-generating activities subject to sector-specific licensing from bodies such as OJK (Otoritas Jasa Keuangan) for financial services.

Closing

These structures suit foreign firms conducting preparatory, promotional, or regulatory-mandated activities before committing to full incorporation, though their prohibition on commercial transactions is a firm ceiling on operational scope.

Foreign companies testing market conditions or fulfilling sector-specific regulatory requirements before proceeding to incorporate a PT PMA.

Partnerships [General Partnership (Firma), Limited Partnership (Commanditaire Vennootschap/CV)]

Partnerships in Indonesia are governed by the Indonesian Commercial Code (Wetboek van Koophandel, or KUHD), a body of law with Dutch colonial origins still in effect today. Two distinct forms exist: the Firma (general partnership) and the CV partnership Indonesia Commanditaire Vennootschap, the latter being the more widely used structure among small and medium-scale domestic businesses.

Neither form carries separate legal personality under Indonesian law. Partners bear personal liability for the entity's obligations, though the CV introduces a structural distinction between active and passive partners that partially limits exposure for certain members.

Key Characteristics

| Requirement | Firma | CV |

|---|---|---|

| Legal Form | General partnership; no separate legal personality | Limited partnership; no separate legal personality |

| Members | Partners (minimum 2, no statutory maximum); all hold active management roles | Active (complementary) partners and passive (sleeping) partners; minimum 1 of each |

| Liability | Unlimited personal liability for all partners | Unlimited for active partners; passive partners liable only up to their capital contribution |

| Local Presence | No registered agent requirement; a business domicile address is required | Same as Firma; registered address required for domicile purposes |

| Capital | No statutory minimum; contributions defined by partnership deed | No statutory minimum; passive partner's contribution recorded in the deed |

| Registration | Registered with the local District Court (Pengadilan Negeri) and notarised deed required | Same registration process; notarised deed filed with Pengadilan Negeri |

Focus Points

- Taxation: Both Firma and CV are treated as taxable entities subject to corporate income tax at the standard 22% rate; distributions to partners may attract dividend withholding tax, and VAT obligations apply if turnover thresholds are met.

- Foreign ownership: Neither structure is open to foreign nationals or foreign-owned entities; ownership is restricted to Indonesian citizens.

- Annual compliance: Obligations are comparatively light, but both structures must maintain updated business licences through the Online Single Submission (OSS) system under BKPM's framework.

- Conversion: A CV may be converted into a PT (Perseroan Terbatas), though this requires a full legal restructuring rather than a simple administrative amendment.

- Treaty access: As domestically restricted entities without foreign shareholding capacity, neither form is relevant for double tax treaty planning.

Closing

A CV suits domestic entrepreneurs seeking a low-cost operational structure for trading or service businesses, with the key advantage of shielding passive investors from full liability. The primary limitation is the complete exclusion of foreign ownership, making these forms irrelevant for cross-border investment purposes.

Both Firma and CV structures are suited to Indonesian nationals running small-to-medium domestic businesses where minimal compliance overhead outweighs the absence of limited liability protections.

Sole Proprietorship (Usaha Dagang/UD)

A sole proprietorship Indonesia Usaha Dagang structure is the simplest business form available to individual entrepreneurs operating under Indonesian law. Unlike a PT or CV, a UD carries no separate legal personality — the proprietor and the business are legally indistinct, meaning personal assets are directly exposed to business liabilities.

Registration is handled at the local government level and typically involves obtaining a business registration certificate (NIB) through the Online Single Submission (OSS) system administered by the Investment Coordinating Board (BKPM). Foreign nationals cannot establish a UD; ownership is restricted to Indonesian citizens.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality; owner bears full liability |

| Members | Single proprietor (Indonesian citizen only) | No minimum capital requirement under general rules |

| Local Presence | Business address required; NIB registration via OSS | Physical operational address within Indonesia |

| Capital | No statutory minimum | Determined by the proprietor |

| Privacy | Owner identity disclosed in registration documents | No shareholder registry privacy |

Focus Points

- Taxation: Subject to personal income tax under PPh (Pajak Penghasilan); VAT registration required if annual turnover exceeds IDR 4.8 billion; no corporate tax applies.

- Annual Compliance: NIB renewal and local business licence maintenance; no mandatory audit requirement.

- Treaty Access: No access to tax treaty benefits available to corporate entities.

- Conversion: Can be converted into a PT by establishing a new legal entity; no direct statutory conversion mechanism exists.

- Restrictions: Closed to foreign ownership; unsuitable for capital-intensive or regulated industries.

Recommendations

A UD suits small-scale domestic trading or service operations where simplicity and low administrative cost outweigh the need for liability protection. The absence of a minimum capital requirement reduces the barrier to entry, though unlimited personal liability remains a significant structural drawback.

Indonesian citizens running small, low-risk domestic businesses who prioritise minimal setup cost and administrative simplicity over liability protection.

How to Choose the Right Entity Type in Indonesia

Selecting the right structure before incorporation determines your tax position, liability exposure, and operational permissions for the life of the business. Getting this decision wrong has concrete consequences, not just administrative inconvenience.

Why Your Entity Choice Matters

Understanding how to choose a business structure in Indonesia requires recognising the regulatory outcomes attached to each decision.

- Registering a representative office (KPPA) while conducting revenue-generating transactions breaches its permitted scope under BKPM regulations, exposing the entity to licence revocation.

- Forming a CV when your sector appears on the Negative Investment List (DNI) under Presidential Regulation No. 10 of 2021 bars foreign participation entirely, leaving the structure legally non-compliant from inception.

- Choosing a PT when a PT PMA is required for foreign ownership means the foreign shareholder's stake lacks legal recognition under the Company Law (Law No. 40 of 2007), creating ownership disputes at exit.

- Selecting a structure without audited financial reporting capacity when your activity triggers OJK oversight results in regulatory non-compliance and potential sanctions.

Key Factors to Consider

- Business Activity: Active trading, asset holding, and regulated sectors such as banking or insurance each require distinct entity structures under Indonesian law.

- Foreign Ownership: If any foreign equity is involved, only a PT PMA provides the legal framework for foreign shareholding recognised by BKPM (now OSS/BKPM under the Ministry of Investment).

- Tax Objectives: Your eligibility for Indonesia's tax treaty network or sector-specific incentives depends on the entity type and its tax residency status.

- Liability Structure: A CV exposes general partners to unlimited personal liability, whereas a PT limits shareholder liability to subscribed capital.

- Substance Capacity: If your firm cannot maintain a physical presence and local staff, a representative office structure may be more appropriate than a full PT.

- Exit and Conversion: Indonesian law imposes procedural requirements for converting or winding up entities; your anticipated exit route should factor into the initial structure choice.

Corporate Compliance Services in Indonesia

Maintain your Indonesian entity's good standing with ongoing compliance support, from annual reporting to regulatory filings.

Conclusion

Choosing the right structure is the first binding decision in any Indonesia company formation conclusion guide, and each entity type carries a distinct legal identity under Indonesian law. The PT PMA is the standard vehicle for foreign direct investment, while the local PT suits Indonesian-resident founders who want full ownership and no foreign investment restrictions. Public companies (PT Tbk) apply only when a firm intends to list on the Indonesia Stock Exchange. Representative offices, whether KPPA or KP3A, are limited to non-commercial activities. Partnerships and sole proprietorships remain relevant primarily for smaller, domestically focused operations.

The PT PMA is consistently the most registered structure among foreign investors, tracked through the Online Single Submission (OSS) system administered by the Investment Coordinating Board (BKPM). Your choice ultimately depends on ownership structure, intended commercial activity, and the applicable Negative Investment List classifications. As Indonesia continues expanding its bilateral investment treaty network, the regulatory environment for foreign-owned entities is gradually becoming more predictable.

How Expanship Can Assist You

Expanship provides corporate services Indonesia company setup clients require across the full range of entity structures available under Indonesian law, from a PT PMA registered with the Indonesia Investment Coordinating Board (BKPM/BKPI) to a local PT governed by the Ministry of Law and Human Rights (Kemenkumham). Each structure carries distinct formation steps and ongoing obligations, and our team works directly with the relevant authorities on your behalf.

Expanship's Indonesia incorporation assistance covers every stage of the process:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Government filing and liaison with Kemenkumham and OSS (Online Single Submission)

- Post-incorporation compliance management, including annual reporting

- Director and shareholder registry maintenance

- Banking introduction assistance

Ready to take the next step? Contact Expanship Indonesia to discuss your requirements.

Frequently Asked Questions (FAQ)

The Perseroan Terbatas (PT) is the most frequently registered entity, largely because it offers limited liability protection and suits a wide range of commercial activities under Indonesian law. Domestic entrepreneurs favour it for its straightforward governance structure under Law No. 40 of 2007 on Limited Liability Companies.

A PT is restricted to Indonesian shareholders, while a PT PMA permits foreign equity participation as governed by the Investment Coordinating Board (BKPM) and the Negative Investment List. PT PMAs face additional licensing requirements and minimum investment thresholds, and their permissible business sectors depend on foreign ownership caps that do not apply to a standard PT.

Among available structures, the CV (Commanditaire Vennootschap) offers comparatively less public disclosure than a PT, as silent partners are not prominently registered with public-facing authorities. Nominee arrangements are legally permissible in Indonesia but carry regulatory scrutiny, particularly following beneficial ownership disclosure rules introduced under Government Regulation No. 13 of 2018.

No. A PT requires a minimum of two shareholders under Law No. 40 of 2007, and a Firma demands at least two partners by its legal nature. A Sole Proprietorship (Usaha Dagang) is the only structure one individual can establish independently.

Foreigners may establish a PT PMA, register a Representative Office (KPPA), or open a Foreign Representative Office (KP3A). Direct foreign participation in a standard PT, CV, or Firma is not permitted under Indonesian investment regulations, making the PT PMA the primary vehicle for foreign-owned commercial operations.

A PT can be converted into a PT Tbk upon meeting the requirements for a public offering under the Financial Services Authority (OJK) regulations. Restructuring a CV or Firma into a PT is possible but requires dissolution of the original entity and fresh incorporation rather than a statutory conversion process.

No. A PT and PT PMA hold full legal personality as distinct juridical entities. A CV, Firma, and Usaha Dagang do not enjoy separate legal personality, meaning owners bear personal exposure to business liabilities in those structures.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.