Key Takeaways

- Hungary's corporate framework is governed primarily by Act V of 2013 on the Civil Code, with business registration processed by the Court of Registration operating within the county-level court system.

- The Korlátolt Felelősségű Társaság (Kft.) is the most commonly registered entity type in Hungary, favored by small and mid-sized businesses for its accessible minimum capital requirements and straightforward governance structure.

- At 9%, Hungary applies one of the lowest flat corporate income tax rates within the European Union, reinforcing its appeal as a structured entry point into Central Europe.

- Foreign entities seeking a limited operational presence in Hungary may establish either a branch office or a representative office, each carrying distinct scope and compliance obligations.

Introduction to Entity Types in Hungary

Hungary is a landlocked Central European country bordered by Austria, Slovakia, Ukraine, Romania, Serbia, Croatia, and Slovenia. An independent republic and EU member state, it operates under a civil law system with company law governed primarily by Act V of 2013 on the Civil Code and Act V of 2006 on Company Registration. Business registration falls under the jurisdiction of the Court of Registration, which operates within the county-level court system and processes incorporation filings.

On tax posture, Hungary applies a flat corporate income tax rate of 9%, making it one of the lower-rate regimes within the European Union.

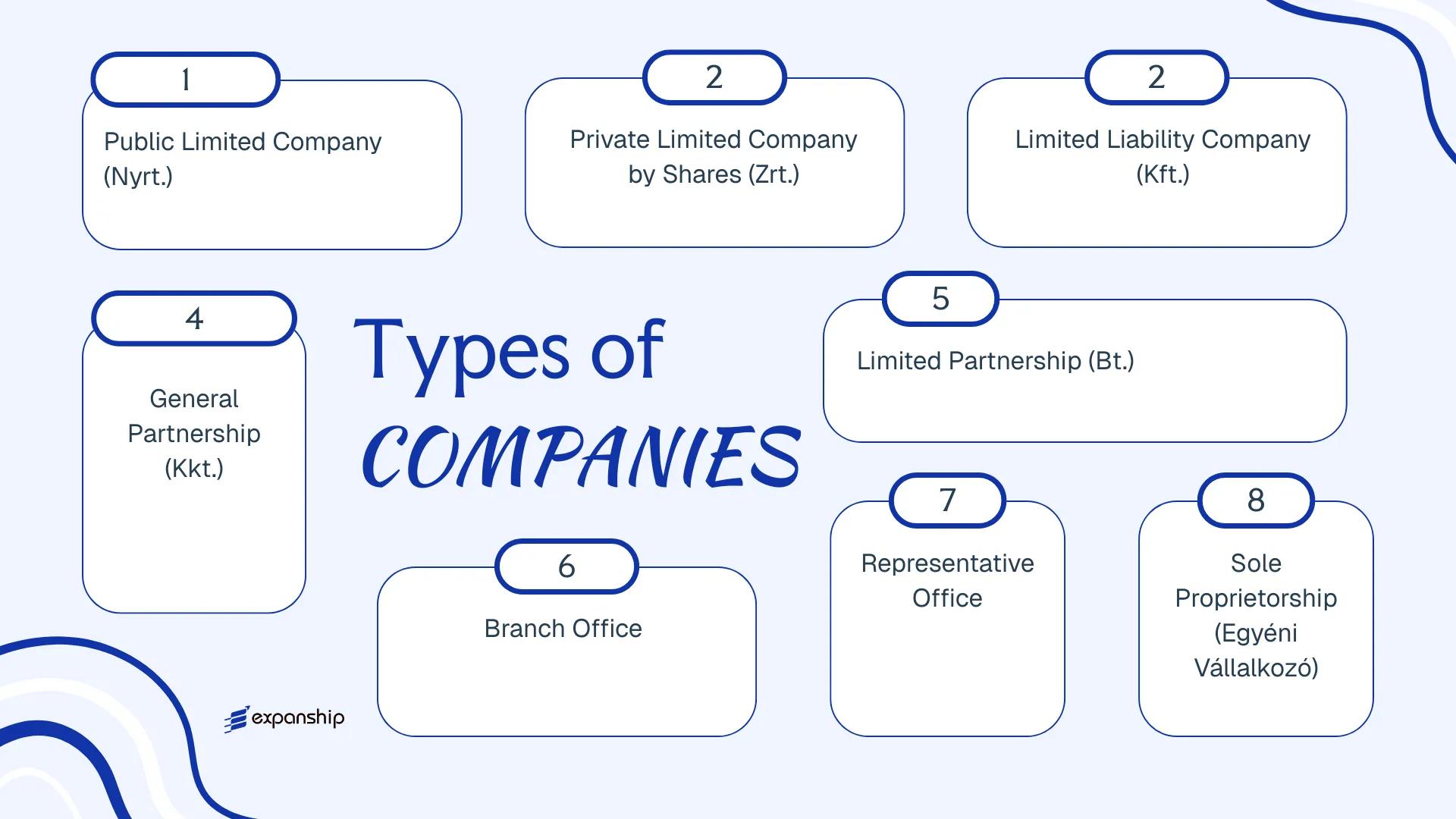

Businesses structuring operations here can choose from several legal entity types: Nyilvánosan Működő Részvénytársaság (Nyrt.), Zártkörűen Működő Részvénytársaság (Zrt.), Korlátolt Felelősségű Társaság (Kft.), Közkereseti Társaság (Kkt.), Betéti Társaság (Bt.), branch offices, representative offices, and Egyéni Vállalkozó. Each carries distinct liability, governance, and capital requirements.

This article examines each structure in detail — covering formation requirements, ownership rules, and tax treatment — so your business can make an informed decision about the most appropriate vehicle for operating in the Hungarian market.

An Overview of Business Structures in Hungary

Hungarian company law recognises several distinct legal forms, each governed primarily by Act V of 2013 on the Civil Code (Polgári Törvénykönyv, or Ptk.), which consolidated and replaced the earlier Companies Act. A separate commercial framework for certain registration and court procedures is maintained under Act V of 2006 on Public Company Information, Company Registration, and Winding-up Proceedings. Each legal form carries different implications for liability, taxation, governance, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Status | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Nyrt. | Public limited company | Limited to shares | Corporate tax applies | Permitted | 1 shareholder | Company Court (Cégbíróság) | Ptk. (Act V of 2013) |

| Zrt. | Private limited by shares | Limited to shares | Corporate tax applies | Permitted | 1 shareholder | Company Court (Cégbíróság) | Ptk. (Act V of 2013) |

| Kft. | Limited liability company | Limited to quota | Corporate tax applies | Permitted | 1 member | Company Court (Cégbíróság) | Ptk. (Act V of 2013) |

| Kkt. | General partnership | Unlimited, joint | Corporate tax applies | Permitted | 2 partners | Company Court (Cégbíróság) | Ptk. (Act V of 2013) |

| Bt. | Limited partnership | Mixed liability | Corporate tax applies | Permitted | 2 partners | Company Court (Cégbíróság) | Ptk. (Act V of 2013) |

| Branch Office | Branch of foreign entity | Parent liable | Corporate tax applies | Permitted | 1 (parent company) | Company Court (Cégbíróság) | Act CXXXII of 1997 |

| Representative Office | Non-trading presence | Parent liable | No trading income | Not permitted | 1 (parent company) | Company Court (Cégbíróság) | Act CXXXII of 1997 |

| Egyéni Vállalkozó | Sole proprietorship | Unlimited personal | Personal income tax | Permitted | 1 individual | NISZ / Government Window | Act CX of 2010 |

Each of these structures is examined in full in the sections below.

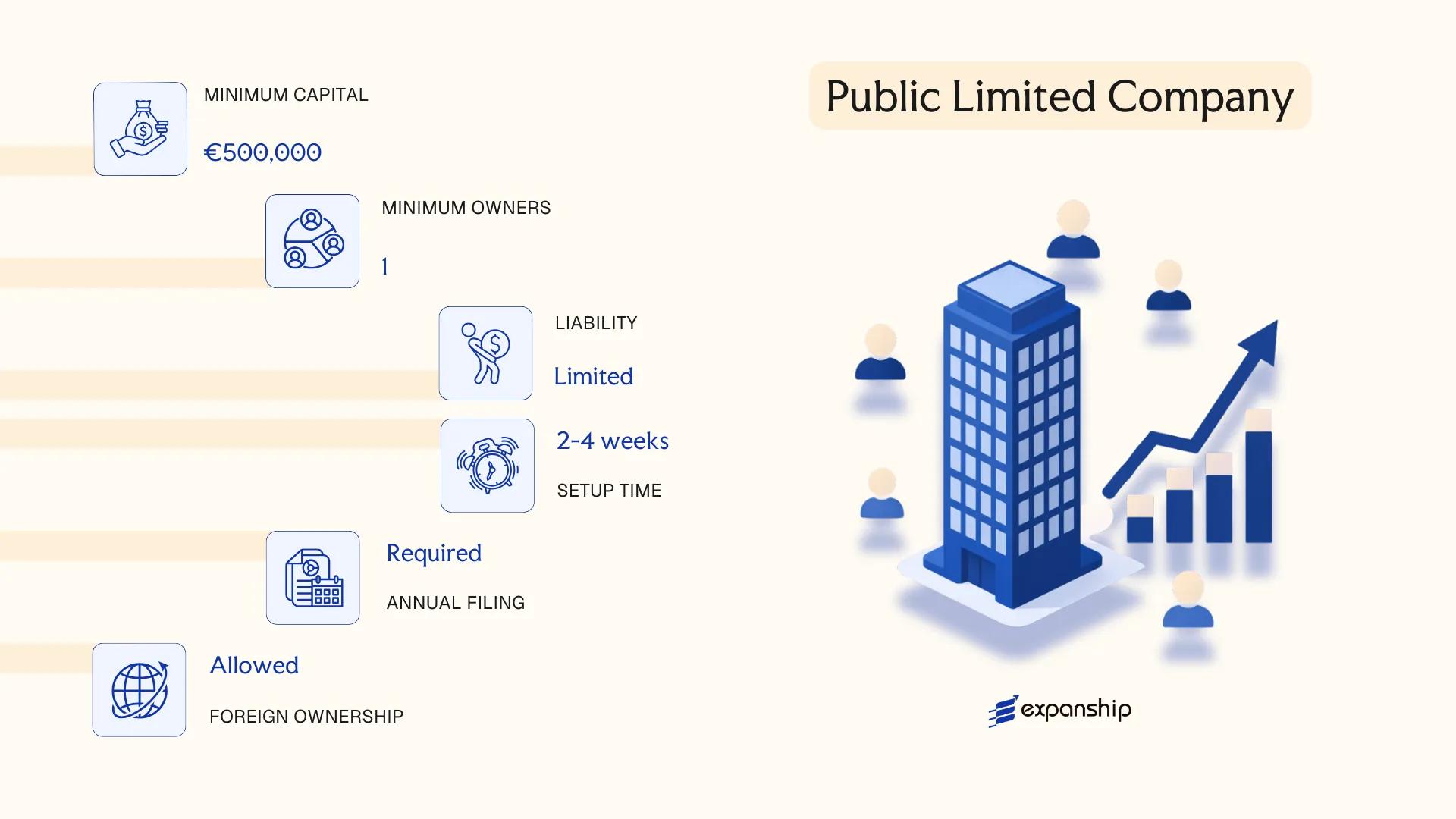

Nyilvánosan Működő Részvénytársaság (Nyrt.) — Public Limited Company

The Nyrt public limited company Hungary recognises is governed by Act V of 2013 on the Civil Code (Polgári Törvénykönyv, Ptk.), which consolidated the earlier company law framework. As a distinct legal entity, the Nyrt. carries separate legal personality and confers limited liability on its shareholders, meaning personal assets remain insulated from corporate obligations.

Shares in an Nyrt. are freely transferable and must be admitted to a regulated market, typically the Budapest Stock Exchange (Budapesti Értéktőzsde, BÉT). This public trading requirement is the defining structural feature that separates this form from its private counterpart.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company by Shares (Nyrt.) | Governed by Ptk., Act V of 2013 |

| Members | Shareholders; no minimum shareholder count, but shares must be publicly offered | Board of Directors (minimum 3 members) required; Supervisory Board mandatory above statutory thresholds |

| Local Presence | Registered seat in Hungary required | A registered address is mandatory; a local representative is not legally required but practically necessary |

| Share Capital | Minimum HUF 20,000,000 (approx. EUR 50,000) | At least 30% of subscribed capital must be paid up at registration |

| Share Transferability | Freely transferable; no restrictions permitted | Shares must be admitted to a regulated market or multilateral trading facility |

| Privacy | Shareholder register is publicly accessible | Beneficial ownership disclosed to the Company Register and the Hungarian National Bank (MNB) |

Focus Points

- Taxation: Corporate income tax applies at a flat 15% rate on profits, with a 5% rate available for certain qualifying SME thresholds; standard VAT at 27% applies to taxable supplies; withholding tax on dividends paid to non-residents is generally 15%, subject to reduction under applicable double tax treaties.

- Regulatory oversight: The Magyar Nemzeti Bank (MNB) supervises listed entities; ongoing disclosure obligations under EU Market Abuse Regulation (MAR) and the Transparency Directive apply.

- Annual compliance: Mandatory annual general meeting (AGM), audited financial statements, and continuous stock exchange reporting obligations.

- Treaty access: Hungary's extensive double tax treaty network (70+ treaties) is accessible to Nyrt. entities; EU Parent-Subsidiary and Interest-Royalties Directives also apply.

- Conversion: An Nyrt. may be converted into a Zrt. (private limited company) by resolution, subject to delisting and statutory procedures under the Ptk.

Closing

The Nyrt. structure suits large-scale enterprises seeking access to public capital markets, institutional investment, or cross-border listings. The primary advantage is unrestricted share transferability and access to equity financing; the principal limitation is the substantial ongoing regulatory burden imposed by both the MNB and stock exchange rules, making it impractical for most closely held or mid-market businesses.

The Nyrt. is best suited for established enterprises with significant capital requirements that intend to list on the Budapest Stock Exchange or another regulated European market.

Company Incorporation in Hungary

Expanship assists with the full incorporation process for Hungarian entities, including Nyrt. formation, registered seat arrangements, and ongoing compliance support.

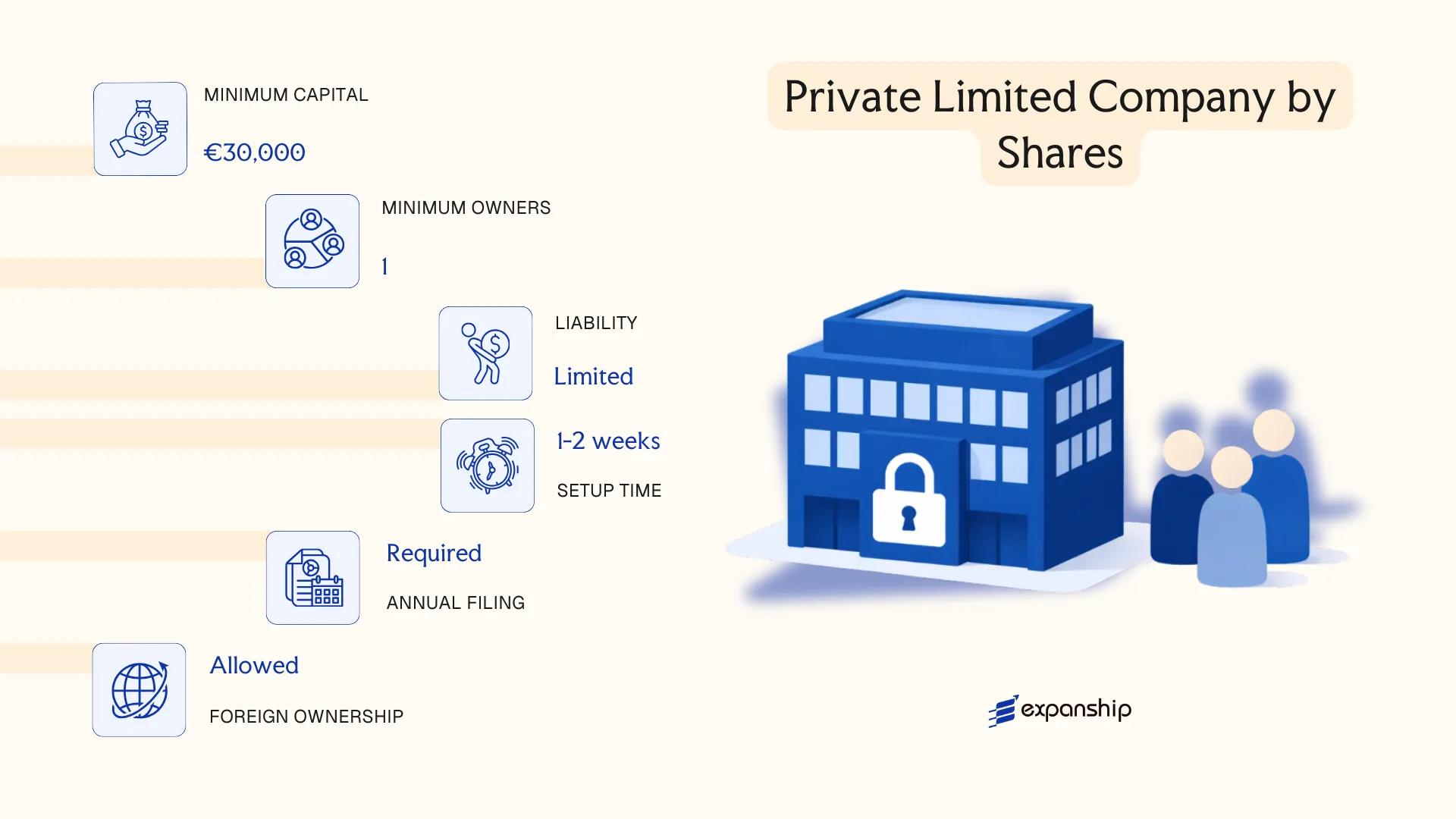

Zártkörűen Működő Részvénytársaság (Zrt.) — Private Limited Company by Shares

The Zrt private limited company Hungary recognises as its primary share-based closed structure is governed by Act V of 2013 on the Civil Code (Polgári Törvénykönyv), which consolidated and replaced the earlier company law framework. As a distinct legal entity, the Zrt carries its own rights and obligations separately from its shareholders.

Shares in a Zrt cannot be offered to the public or traded on a regulated market — this closed nature distinguishes it from its publicly listed counterpart. The structure suits businesses that require share capital mechanics, such as tiered share classes or employee share schemes, while retaining full control over ownership transfers.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Joint Stock Company | Separate legal personality; shareholders not personally liable beyond their capital contribution |

| Members | Shareholders: minimum 1, no statutory maximum | Single-shareholder Zrt is permitted |

| Management | Board of Directors or sole Executive Director | Supervisory Board mandatory if certain employee thresholds are met |

| Local Presence | Registered seat in Hungary required | A registered address service may satisfy this requirement |

| Share Capital | Minimum HUF 5,000,000 | At least 25% must be paid up at incorporation; remainder within one year |

| Share Transferability | Restricted; articles may impose pre-emption rights | Shares are not publicly tradeable |

| Privacy | Shareholders listed in company registry (Cégbíróság) | Registry is publicly searchable |

Focus Points

- Taxation: Subject to 9% corporate income tax; standard VAT rate of 27% applies to taxable supplies; dividend withholding tax is 15% unless reduced by a tax treaty; no stamp duty on share transfers in most cases.

- Annual Compliance: Mandatory filing of audited financial statements with the Company Court; annual general meeting required unless waived by unanimous shareholder consent.

- Treaty Access: Qualifies as a Hungarian tax resident entity, granting access to Hungary's extensive double tax treaty network covering 80+ countries.

- Conversion: A Zrt may convert into a Nyrt. by meeting public company requirements, or downward into a Kft., subject to court registration.

- Restrictions: Foreign nationals may hold shares without restriction, but regulated sectors may impose additional licensing or ownership conditions.

Closing

The Zrt suits mid-to-large enterprises, holding structures, and businesses anticipating future capital raises or investor participation that require a share-based framework without public market exposure. The ability to issue multiple share classes is a structural advantage; the higher minimum capital and more complex governance obligations relative to a Kft. represent meaningful operational costs.

The Zrt is most appropriate for established businesses or investment holding vehicles where share capital structuring, multiple share classes, or eventual transition to a public listing are relevant considerations.

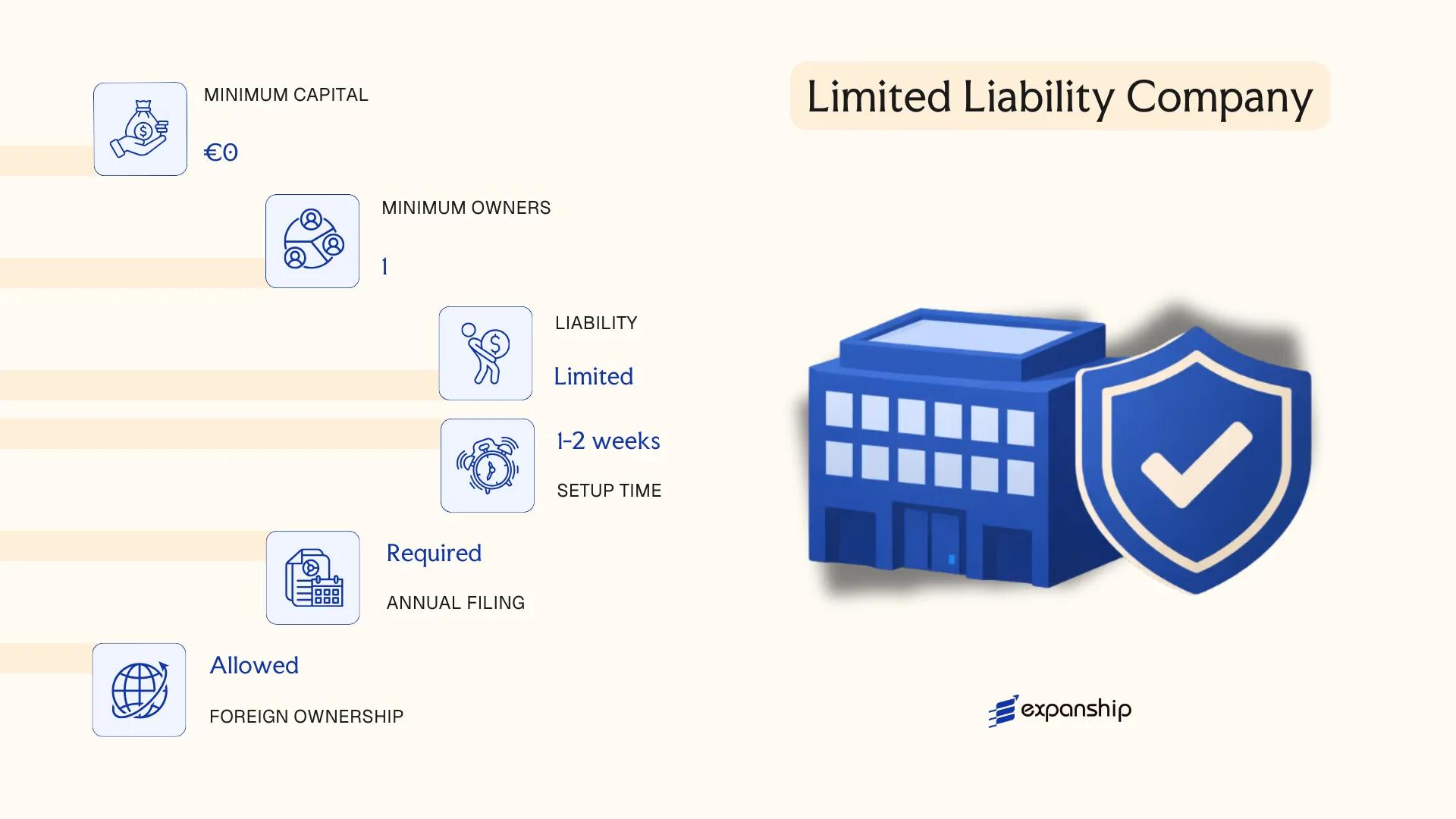

Korlátolt Felelősségű Társaság (Kft.) — Limited Liability Company

The Kft. is governed by Act V of 2013 on the Civil Code (Polgári Törvénykönyv), which consolidated Hungarian company law and replaced the earlier Act IV of 2006. As a Kft. limited liability company Hungary, the entity carries its own separate legal personality, meaning its members bear no personal liability for corporate debts beyond their contributed capital.

Structurally, the Kft. sits between a pure partnership and a share-based company. Ownership is divided into business quotas rather than transferable shares, and quota transfers to third parties may be subject to pre-emption rights held by existing members, making it a closer-held form by default.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (Kft.) | Separate legal personality; quota-based ownership |

| Members | 1–50 members (natural persons or legal entities) | Single-member Kft. is permitted |

| Management | Executive officer (ügyvezető); supervisory board required above 200 employees | Ügyvezető need not be a member |

| Local Presence | Registered seat (székhely) in Hungary required | A registered address service is acceptable |

| Minimum Capital | HUF 3,000,000 (approx. EUR 8,000) | Must be fully subscribed at formation; contributions may be in cash or in kind |

| Privacy | Members listed in the Company Registry (Cégbíróság) | Registry is publicly accessible |

Focus Points

- Taxation: Subject to 9% corporate income tax; standard VAT rate of 27% applies; dividend withholding tax is 15% unless reduced by treaty; small business tax (KATA or KIVA) regimes may be available as alternatives depending on size and structure.

- Annual Compliance: Annual financial statements must be filed with the Court of Registration; a statutory audit is required once the entity exceeds defined thresholds under the Accounting Act (Act C of 2000).

- Treaty Access: As an EU member state, Hungary's extensive double tax treaty network is accessible to Kft. entities, subject to beneficial ownership requirements.

- Quota Transfers: Transfers to non-members require a written agreement and are subject to a 30-day pre-emption right held by existing members and the company itself.

- Conversion: A Kft. may be converted into a Zrt. or other corporate form through a transformation procedure under the Civil Code without dissolution.

Closing

The Kft. is used across trading, holding, and IP-holding structures, and its low minimum capital threshold makes Korlátolt Felelősségű Társaság registration accessible for small to mid-sized operations. The primary drawback is that quota transferability is more restricted than shares in a Zrt., limiting flexibility in secondary transactions.

The Kft. suits foreign investors and SMEs seeking a cost-effective, EU-based entity with limited liability, without the regulatory overhead of a public company.

Partnerships in Hungary [Közkereseti Társaság (Kkt.) — General Partnership, Betéti Társaság (Bt.) — Limited Partnership]

Both partnership forms in Hungary are governed by Act V of 2013 on the Civil Code (Polgári Törvénykönyv, Ptk.), which unified the regulation of business associations under a single legislative framework. Each structure carries distinct liability implications that directly affect how risk is distributed among members.

Under Hungarian law, neither the Közkereseti Társaság (Kkt.) nor the Betéti Társaság (Bt.) is a purely limited liability vehicle. Both possess separate legal personality, yet at least some members bear unlimited, joint, and several liability for the obligations of the firm.

Key Characteristics

| Requirement | Kkt. (General Partnership) | Bt. (Limited Partnership) |

|---|---|---|

| Legal Form | Separate legal personality; unlimited liability for all members | Separate legal personality; dual-class liability structure |

| Members | Minimum 2 members (referred to as tagok); no statutory maximum; all carry unlimited liability | Minimum 2 members: at least 1 beltag (general partner, unlimited liability) and at least 1 kültag (limited partner, liability capped at contribution) |

| Registered Office | Local registered address in Hungary required | Local registered address in Hungary required |

| Share Capital | No statutory minimum capital requirement | No statutory minimum capital requirement; kültag contribution must be defined in the articles |

| Privacy | Member names filed in the Company Register (Cégbíróság); publicly accessible | Same public filing requirement; both partner classes disclosed |

Focus Points

- Taxation: Both Kkt. and Bt. are subject to corporate income tax at 9% on profits; VAT registration applies at the standard 27% rate where thresholds are met; no withholding tax specific to partnerships at the entity level, though profit distributions to members may attract personal income tax obligations depending on residency.

- Annual Compliance: Annual financial statements must be filed with the Company Register; accounting obligations apply under Act C of 2000 on Accounting.

- Treaty Access: As Hungarian-registered entities with separate legal personality, both forms can potentially access Hungary's double tax treaty network, subject to the treaty's definition of "resident" and "person."

- Restrictions: Neither form is permitted to carry out activities reserved for specific licensed entities without the appropriate regulatory authorisation from the relevant sectoral authority.

- Conversion: Both structures can be converted into other business association forms (e.g., Kft. or Zrt.) through a transformation procedure under the Ptk. and Act CLXXXI of 2011 on Cross-Border Transformations and Mergers.

Sub-Types

Közkereseti Társaság (Kkt.) — General Partnership

All members of a Kkt. act as general partners, each bearing unlimited personal liability for the entity's debts. This structure is typically chosen for small professional practices or family-run businesses where all participants are actively involved in management.

Betéti Társaság (Bt.) — Limited Partnership

The Bt. introduces a two-tier membership structure: the beltag manages the business and carries unlimited liability, while the kültag contributes capital but is excluded from management and assumes liability only to the extent of their declared contribution. This separation makes the Bt. a functional vehicle for arrangements where a passive investor co-operates with an active operator.

Closing Remarks

Partnership structures suit closely held businesses, professional services arrangements, and ventures where operational control is concentrated among a small group of known participants. The absence of a minimum capital requirement lowers the barrier to formation, though the unlimited liability exposure of general partners represents a material structural risk.

Kkt. and Bt. structures are best suited for small, domestically focused businesses or professional partnerships where the members have an established trust relationship and accept personal liability as part of the operating arrangement.

Foreign Business Presence in Hungary [Branch Office, Representative Office]

Registering a foreign company branch office Hungary is governed primarily by Act V of 2013 on the Civil Code, alongside Act XLIV of 1997 on Foreign Branches and Representative Offices, which sets out the specific rules for foreign entities operating within the country. A branch office is not a separate legal entity — it remains part of the parent company and carries no independent limited liability, meaning creditors can pursue the foreign parent directly.

Registration takes place at the competent Court of Registration, and the branch must be entered into the Hungarian Company Registry. Unlike a subsidiary, the branch operates under the parent company's name and is bound by its constitutional documents.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None (extension of parent) | None (extension of parent) |

| Commercial Activity | Permitted | Not permitted — preparatory and auxiliary activities only |

| Registration Body | Court of Registration | Court of Registration |

| Registered Address | Mandatory Hungarian address | Mandatory Hungarian address |

| Minimum Capital | No statutory minimum, but parent's capital must meet HUF 2 million equivalent | No statutory minimum |

| Head of Office | Designated representative (natural person) required | Designated representative required |

| Parent Liability | Unlimited — parent is fully liable | Unlimited — parent is fully liable |

Focus Points

- Taxation: Branch profits are subject to 9% corporate income tax on Hungarian-sourced income; VAT obligations apply if the branch conducts taxable supplies; withholding tax may apply to profit transfers depending on the applicable double tax treaty between Hungary and the parent's home jurisdiction.

- Economic Substance: The branch must maintain a genuine operational presence; a letterbox arrangement without actual activity risks deregistration.

- Annual Compliance: Branches must file standalone financial statements in Hungarian under local accounting rules (Act C of 2000 on Accounting) and submit annual tax returns independently.

- Treaty Access: Access to Hungary's double tax treaty network depends on the parent's tax residency, not the branch itself.

- Restrictions: A representative office cannot generate revenue or enter into commercial contracts on behalf of the parent — its scope is strictly limited to market research, liaison, and promotion.

Sub-Types

Branch Office (Fióktelep)

A Fióktelep is the standard vehicle for a foreign entity wishing to conduct revenue-generating operations without incorporating a separate Hungarian entity. It must carry the parent company's name with the addition of "magyarországi fióktelepe."

Representative Office (Képviseleti Iroda)

A Képviseleti Iroda suits foreign businesses that need a physical presence for non-commercial purposes — such as coordinating with local partners or conducting preliminary market assessments — without triggering full corporate registration obligations.

Closing

Both structures are used by foreign firms testing the Hungarian market or managing regional operations without committing to a full subsidiary. The branch office offers operational flexibility, but the absence of liability separation is a meaningful exposure for the parent entity.

A branch office suits foreign companies that require an operational foothold in Hungary without incorporating a new entity, while a representative office fits those with purely preparatory or liaison-based activities.

Egyéni Vállalkozó — Sole Proprietorship

The Egyéni Vállalkozó sole proprietorship Hungary is governed primarily by Act CXV of 2009 on Individual Entrepreneurs, which established a simplified registration framework through the central government portal. Unlike corporate entities, this structure carries no separate legal personality — the proprietor and the business are legally identical, meaning personal assets are fully exposed to business liabilities.

Registration is handled electronically via the Ügyfélkapu (Client Gateway) portal and requires a Hungarian tax identification number, making this form accessible only to individuals with established Hungarian self-employment registration status. Foreign nationals may register if they hold a valid residence permit authorising economic activity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole proprietorship (unincorporated) | No separate legal personality; proprietor bears unlimited personal liability |

| Member Type | Sole proprietor (egyéni vállalkozó) | One individual only; no co-ownership structure permitted |

| Local Presence | Registered business address in Hungary | Must be a valid Hungarian address; home address is permissible |

| Capital | No minimum capital requirement | No share capital; business assets are personal assets |

| Privacy | Name and address on public register | NISZ National Infocommunications register is publicly searchable |

| Eligibility | Natural persons only | Hungarian tax ID (adóazonosító jel) required; suspended or banned individuals are ineligible |

Focus Points

- Taxation: Subject to personal income tax under Act CXVII of 1995; eligible for the KATA flat-rate tax regime (with eligibility restrictions post-2022 reforms) or itemised deduction method; VAT registration threshold applies under Act CXXVII of 2007; no corporate tax exposure; social contribution obligations apply.

- Annual Compliance: Annual personal income tax return required; VAT returns filed monthly or quarterly depending on turnover; no separate audited accounts required.

- Economic Substance: The proprietor must personally conduct the registered activity; delegating operations entirely to third parties is inconsistent with this structure.

- Conversion: An Egyéni Vállalkozó cannot convert directly into a Kft. through a statutory merger process; a new entity must be incorporated separately and assets transferred.

- Restrictions: A single individual may hold only one sole proprietorship registration at a time; certain regulated professions require additional licensing regardless of business form.

Closing

This structure suits resident freelancers, tradespeople, and individual consultants operating domestically with low liability exposure. The absence of minimum capital and streamlined Ügyfélkapu registration are practical advantages, though unlimited personal liability makes it unsuitable for activities carrying significant financial or legal risk.

Resident individuals conducting low-risk, single-person service or trade activities who require minimal administrative overhead and do not need liability separation.

How to Choose the Right Entity Type in Hungary

Selecting how to choose a business entity in Hungary determines more than your registration cost — it shapes your tax exposure, liability profile, and operational capacity for the life of the business.

Why Your Entity Choice Matters

The legal form you register under the Act V of 2013 on the Civil Code has direct, measurable consequences if mismatched to your actual operations.

- Selecting a structure without the capacity to maintain local substance when substance rules apply triggers reporting failures under Hungarian tax authority (NAV) review and potential penalties.

- Choosing a form that mandates statutory audit when your firm operates as a single-person consultancy below the audit threshold adds avoidable annual costs.

- Forming a share-based company when your objectives are asset protection or succession planning locks you into annual shareholder meeting obligations that do not apply to foundations.

- Registering a representative office when you intend to conclude contracts locally places you in breach of the permitted activity scope, which can result in forced closure by the Court of Registration.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each require a distinct legal form under Hungarian law.

- Ownership Structure: Single-owner setups and multi-party arrangements carry different governance obligations across entity types.

- Tax Objectives: Your need for treaty access, participation exemption eligibility, or small taxpayer status (KATA/KIVA) directly narrows your options.

- Liability Exposure: The degree of personal liability you can accept determines whether a partnership structure is viable.

- Exit Strategy: Not all Hungarian entity types permit redomiciliation or conversion without dissolution and re-registration.

- Public Disclosure: Director and member data appears on the Company Register; nominee structures can address disclosure concerns within permitted limits.

Compliance Services for Companies in Hungary

Ongoing compliance support for Hungarian entities, covering filing deadlines, statutory obligations, and NAV reporting requirements.

Conclusion

A Hungary company incorporation summary is, at its core, a question of liability structure, ownership preferences, and operational scale. The Kft. remains the most registered entity type in the country, favored by small and mid-sized businesses for its accessible minimum capital and straightforward governance under the Civil Code (Act V of 2013). The Zrt. suits businesses requiring share-based ownership without public listing obligations, while the Nyrt. applies exclusively to firms seeking access to public capital markets. General and limited partnerships carry personal liability implications that make them appropriate for smaller, domestically focused operations. Branch offices and representative offices serve foreign entities testing the market or maintaining a limited operational footprint.

Registered under the supervision of the Court of Registration, Hungary's corporate framework continues to align with EU directives, and its expanding double tax treaty network reinforces its position as a structured entry point into Central Europe. Professional guidance remains relevant at every stage of the setup process.

How Expanship Can Assist You

Expanship Hungary company formation services cover the full process of registering a business with the Hungarian Court Registration System (Cégbíróság), from selecting the right entity structure — a Kft., Zrt., or branch office — through to ongoing compliance with Hungary's Act V of 2013 on the Civil Code and the related company law provisions.

Expanship's corporate services in Hungary span every stage of the process:

- Preparation and legalization of founding documents

- Registered agent and registered office provision

- Filing and liaison with the relevant Company Registry Court

- Post-incorporation compliance management, including annual reporting obligations

- Corporate bank account introduction assistance

Our team coordinates directly with local notaries and the Company Court to keep your registration on track and your entity in good standing after formation.

Get in touch with Expanship Hungary to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The Korlátolt Felelősségű Társaság (Kft.) is the most frequently registered business form in Hungary. Its relatively low minimum share capital of HUF 3,000,000, single-member eligibility, and limited liability make it the default choice for small and medium-sized enterprises.

A Kft. transfers ownership through quota assignments subject to member approval, while a Zrt. issues transferable shares, making equity structuring more flexible for investor-backed businesses. Both are subject to Hungarian corporate income tax at the standard rate, but a Zrt. carries higher formation costs and more rigorous ongoing governance requirements under Act V of 2013.

Among Hungarian structures, the Kft. offers a comparatively lower public profile, though ultimate beneficial owners must still be disclosed in the company register maintained by the regional courts of registration. Nominee arrangements are legally permissible but do not override beneficial ownership disclosure obligations under Act LIII of 2017 on anti-money laundering.

A sole individual can form a Kft. or Zrt. as the sole member or shareholder. Közkereseti Társaság (Kkt.) and Betéti Társaság (Bt.) each require at least two founding members by statute, as partnerships are inherently multi-party structures.

Non-Hungarian nationals may establish a Kft., Zrt., or register a branch of a foreign entity without restrictions tied to nationality. However, appointing a local registered address is mandatory, and a foreign individual acting as a director must obtain a Hungarian tax identification number from the National Tax and Customs Administration (NAV).

Act V of 2013 permits transformation, merger, and demerger of companies, including conversion from a Kft. to a Zrt. Continuity of legal personality is preserved through the process, and creditors retain protection rights during the transformation procedure.

The Kft., Zrt., Nyrt., Kkt., and Bt. all possess separate legal personality under Hungarian law. The Egyéni Vállalkozó (sole proprietorship) does not — the individual and the business remain legally indistinguishable, meaning personal assets are exposed to business liabilities without limitation.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.