Key Takeaways

- Haiti's corporate law derives from the Code de Commerce, with business formalization coordinated through the Centre de Facilitation des Investissements (CFI), Direction Générale des Impôts (DGI), and Office National d'Assurance (ONA).

- The Société à Responsabilité Limitée (SARL) is the most commonly adopted structure for private business activity in Haiti, offering liability protection with relatively low formation complexity.

- Foreign entities can establish a direct operational presence in Haiti through a Branch Office without creating a separate legal person under Haitian law.

- Haiti operates a territorial tax system, meaning only income sourced within the country is subject to local taxation, a factor that directly influences entity selection for foreign investors.

Introduction to Entity Types in Haiti

Occupying the western third of Hispaniola in the Caribbean, Haiti shares the island with the Dominican Republic and sits within the Greater Antilles archipelago. It is an independent republic governed under a civil law tradition, with Haitian corporate law drawing from the Code de Commerce.

Company registration falls under the authority of the Office National d'Assurance (ONA) in coordination with the Direction Générale des Impôts (DGI) and the Centre de Facilitation des Investissements (CFI), which serves as the primary entry point for business formalization. Haiti operates a territorial tax system, meaning only income sourced within the country is subject to local taxation.

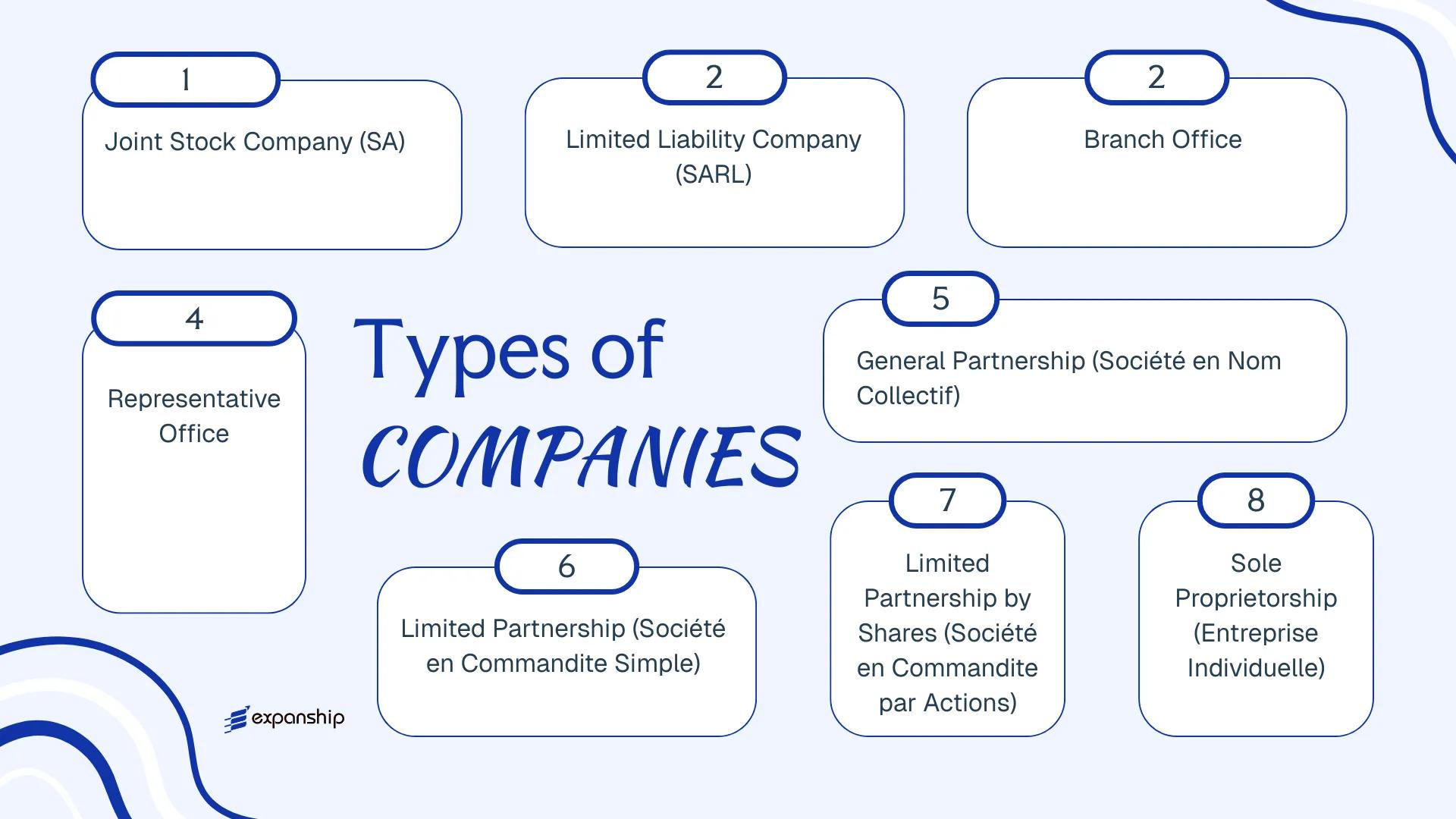

The types of business entities in Haiti available to domestic and foreign investors include the Société Anonyme (SA), Société à Responsabilité Limitée (SARL), Société en Nom Collectif, Société en Commandite Simple, Société en Commandite par Actions, Branch Office, Representative Office, and Entreprise Individuelle. Each structure carries distinct requirements regarding capital, liability, governance, and foreign ownership. This article examines each of these Haitian corporate structures in detail to help you determine which form suits your operational and legal requirements.

An Overview of Business Structures in Haiti

Haiti business structures overview begins with the country's primary commercial legislation: the Code de Commerce, supplemented by specific regulatory provisions administered through the Registre du Commerce et des Sociétés (RCS). Several distinct legal forms are available to investors and entrepreneurs, each calibrated to a different scale of operation, ownership model, or level of liability exposure. The sections that follow examine each structure in full.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Société Anonyme (SA) | Joint Stock Company | Limited to share capital | Taxed | Permitted | 7 shareholders | RCS / MEF | Code de Commerce |

| Société à Responsabilité Limitée (SARL) | Limited Liability Company | Limited to contribution | Taxed | Permitted | 2 members | RCS / MEF | Code de Commerce |

| Société en Nom Collectif (SNC) | General Partnership | Unlimited, joint | Taxed | Permitted | 2 partners | RCS | Code de Commerce |

| Société en Commandite Simple (SCS) | Limited Partnership | Mixed (general/limited) | Taxed | Permitted | 2 partners | RCS | Code de Commerce |

| Société en Commandite par Actions (SCA) | Partnership by Shares | Mixed (general/limited) | Taxed | Permitted | 2 partners | RCS | Code de Commerce |

| Branch Office | Foreign entity extension | Parent bears liability | Taxed | Permitted | N/A | RCS / MEF | Code de Commerce |

| Representative Office | Non-trading presence | Parent bears liability | Generally exempt | Not permitted | N/A | RCS | Code de Commerce |

| Entreprise Individuelle | Sole Proprietorship | Unlimited, personal | Taxed | Permitted | 1 owner | RCS | Code de Commerce |

Each of these structures is examined in full in the sections below.

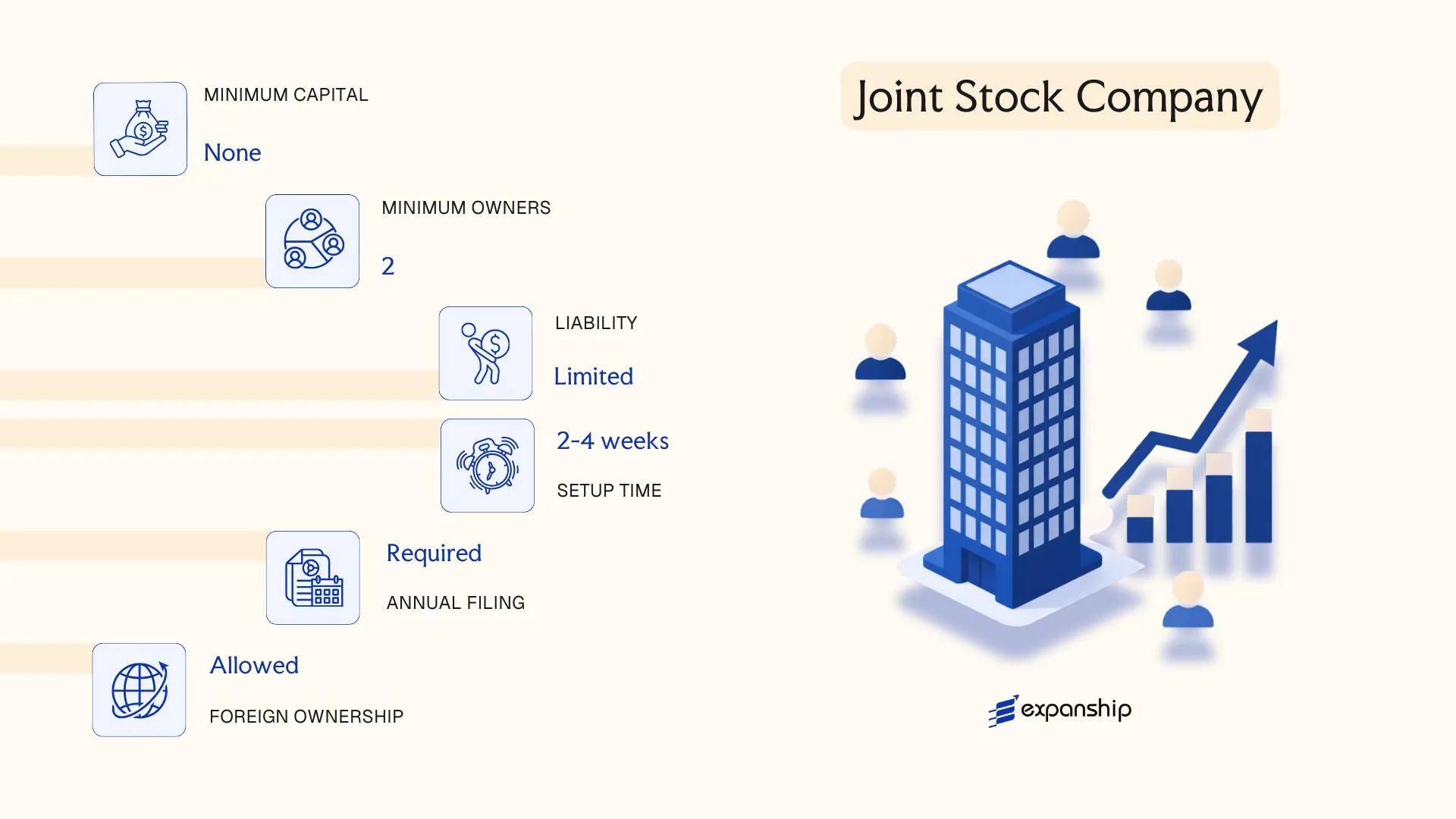

Société Anonyme (SA) – Joint Stock Company

Société Anonyme Haiti SA registration is governed primarily by the Commercial Code of Haiti, which draws from the French Napoléonic commercial law tradition. The SA constitutes a distinct legal entity, meaning its liabilities are separate from those of its shareholders.

Shareholders hold transferable shares, and their financial exposure is limited to the amount of capital they have subscribed. This structure suits firms anticipating public or private equity investment, or those requiring a formal governance framework with a board of directors.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (SA) | Separate legal personality; limited liability |

| Members | Shareholders and a Board of Directors | Minimum 7 shareholders; no statutory maximum |

| Management | Board of Directors (Conseil d'Administration) | Minimum 3 directors required |

| Local Presence | Registered office in Haiti | Physical address required; registered agent not separately mandated by statute |

| Share Capital | Minimum capital requirements apply under the Commercial Code | Denominated in Haitian Gourdes (HTG); shares must be partially paid up at incorporation |

| Privacy | Shareholder details filed with the registry | Records are generally accessible; limited privacy |

Focus Points

- Taxation: Corporate income is subject to tax administered by the Direction Générale des Impôts (DGI); applicable taxes include corporate income tax, value-added tax (TVA) at the standard rate, and withholding taxes on dividends and certain payments to non-residents.

- Annual Compliance: Annual financial statements must be filed, and general shareholder meetings are required by law.

- Transfer of Shares: Shares are freely transferable unless the articles of association impose restrictions, making the SA suitable for entities expecting ownership changes.

- Treaty Access: Haiti has a limited tax treaty network; SA entities cannot assume broad double taxation treaty coverage.

- Conversion: Conversion from an SA to another entity form is possible but requires shareholder approval and re-registration with the relevant commercial registry.

Closing

The SA is used primarily for medium-to-large trading operations, holding structures, and businesses seeking to raise capital from multiple investors. Its principal advantage is the free transferability of shares; its primary drawback is the administrative burden of maintaining a board and meeting statutory corporate governance requirements.

The SA is best suited for larger businesses or investor-backed ventures that require a formal governance structure and anticipate share transfers or future capital raising.

Company Incorporation in Haiti

Set up your Société Anonyme or other business entity in Haiti with end-to-end incorporation support.

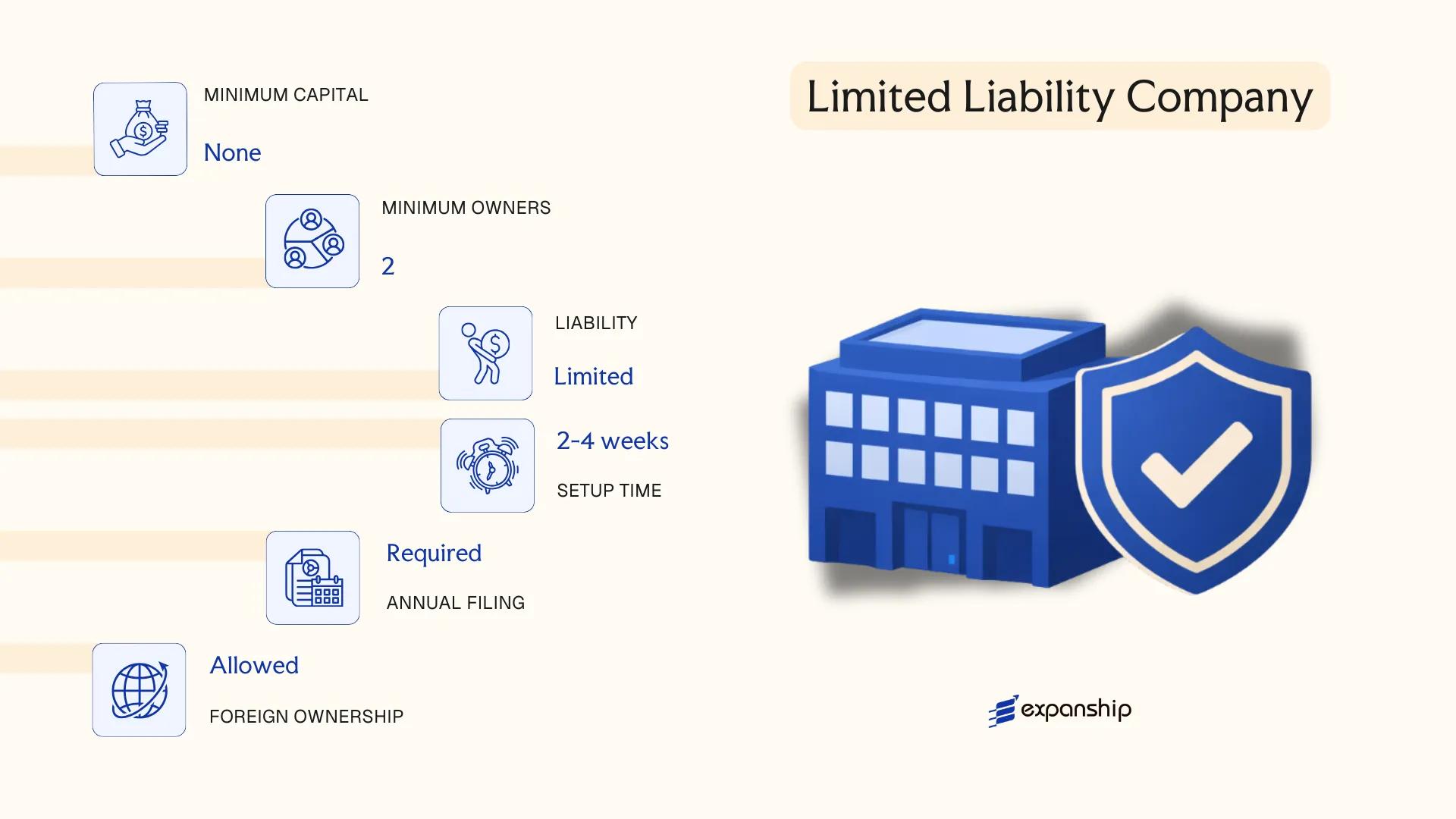

Société à Responsabilité Limitée (SARL) – Limited Liability Company

The Société à Responsabilité Limitée Haiti SARL is governed by the Haitian Commercial Code, which establishes it as a separate legal entity distinct from its members. Liability is confined to each member's capital contribution, shielding personal assets from business obligations.

This hybrid structure sits between a partnership and a joint stock company, making it accessible to small and medium enterprises without the administrative burden of a full SA. Ownership is represented by social parts rather than publicly transferable shares, which restricts free transfer and keeps control within a defined group of members.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société à Responsabilité Limitée (SARL) | Separate legal personality; civil and commercial liability limited to contributions |

| Members | 1–50 members (associés) | Sole-member SARL is permitted; exceeding 50 requires conversion to SA |

| Management | One or more gérants (managers) | Need not be a member; can be Haitian or foreign national |

| Capital | No statutory minimum under general practice | Denominated in Haitian Gourdes (HTG); capital divided into social parts, not shares |

| Local Presence | Registered office address in Haiti required | No mandatory local director, but a registered address is required for official correspondence |

| Privacy | Names of members filed with the Office National d'Assurance (ONA) and trade registry | Beneficial ownership disclosure requirements apply at registration |

Focus Points

- Taxation: Corporate income tax applies at the standard rate; the SARL is also subject to TVA (Taxe sur la Valeur Ajoutée), withholding taxes on dividends and payments to non-residents, and applicable municipal taxes.

- Annual Compliance: Annual financial statements must be filed; the entity is registered with the Centre de Facilitation des Investissements (CFI) and must maintain updated records at the Registre du Commerce.

- Transfer Restrictions: Social parts are not freely transferable; transfers to third parties require member approval, typically by a qualified majority as stipulated in the statuts.

- Conversion: An SARL that exceeds 50 members is legally required to convert into an SA under the Commercial Code.

- Treaty Access: Haiti has a limited tax treaty network; SARL entities may have restricted access to double taxation relief depending on the investor's home jurisdiction.

Closing

The SARL suits trading operations, family-held businesses, and joint ventures where the parties want limited liability without the formalities of a public company structure. The restriction on share transferability, however, can complicate exit strategies for investors seeking liquidity.

The SARL is most appropriate for small to medium enterprises and closely held ventures with a defined group of up to 50 members who do not require publicly tradeable ownership interests.

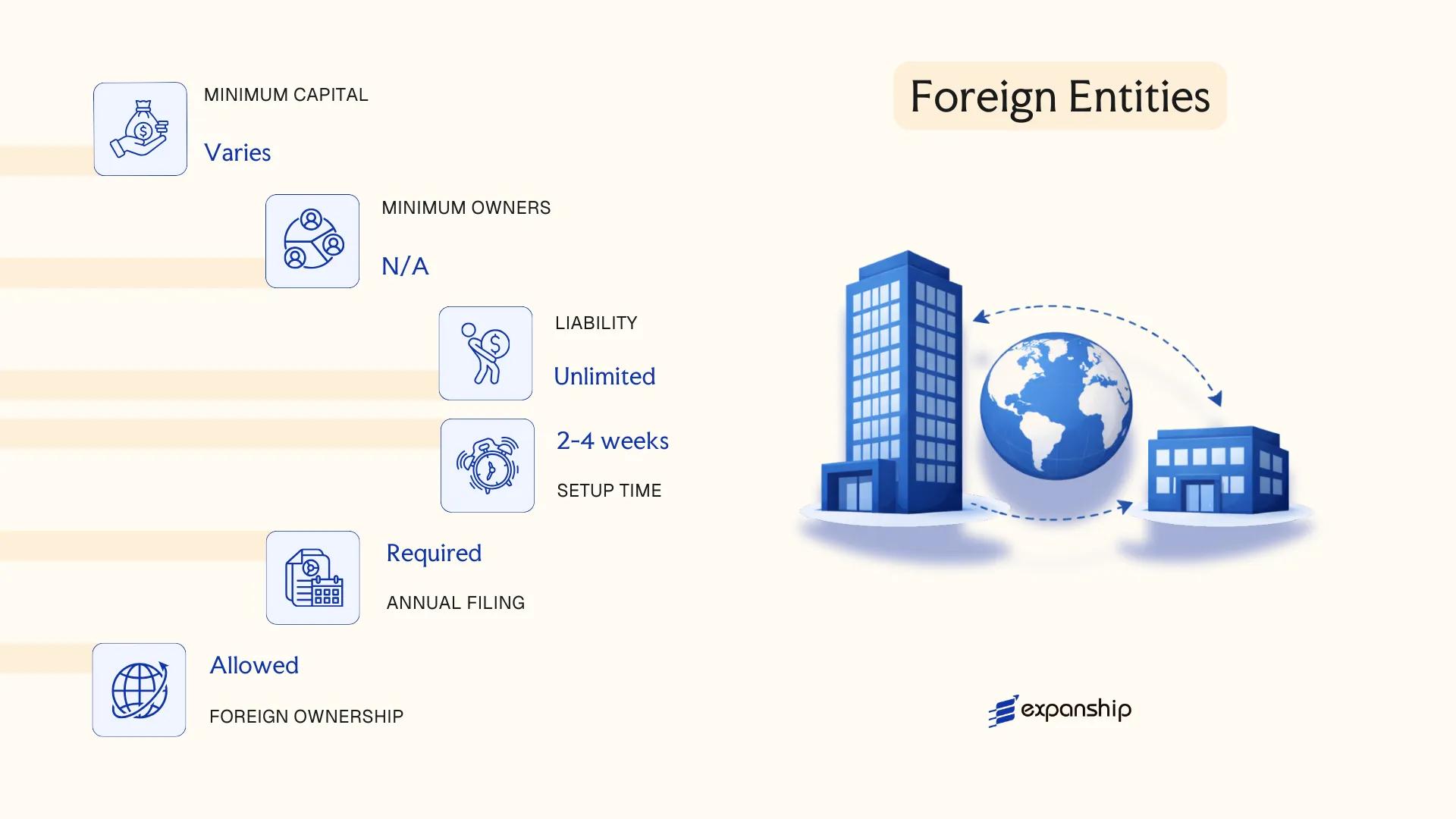

Foreign Entities in Haiti [Branch Office, Representative Office]

Registering a foreign company branch office Haiti requires compliance with the Commercial Code and relevant provisions governing foreign business activity. Under Haitian law, a branch office is not a separate legal entity — it is an extension of the parent company, which retains full legal and financial liability for the branch's obligations. Registration is administered through the Office du Registre des Entreprises et des Sociétés (ORES) under the Ministry of Commerce and Industry (MCI).

A representative office operates under a narrower mandate: it may conduct market research, promote the parent company, and facilitate liaison activities, but it cannot generate revenue locally.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None – extension of parent company | None – extension of parent company |

| Liability | Parent bears full liability | Parent bears full liability |

| Commercial Activity | Permitted | Not permitted; promotional only |

| Local Representative | Mandatory – appointed resident agent | Mandatory – appointed resident agent |

| Registered Office | Required physical address in Haiti | Required physical address |

| Capital Requirement | No statutory minimum; parent's capital applies | None |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at the standard rate; VAT obligations apply to taxable supplies; withholding tax applies to remittances to the parent; representative offices with no revenue have limited tax exposure.

- Economic Substance: No formal substance legislation exists; however, branch operations must reflect genuine local activity to avoid reclassification risk.

- Annual Compliance: Annual renewal of registration with ORES is required, along with financial reporting aligned to the parent company's accounts.

- Treaty Access: Haiti has a limited tax treaty network; treaty benefits for branches depend on the parent's home jurisdiction.

- Conversion: A branch can be converted into a locally incorporated entity, though the process requires a fresh incorporation filing with MCI.

Closing

A branch office suits foreign firms testing the Haitian market or executing defined project-based work, with the key advantage of a simpler setup relative to full incorporation; the principal drawback is unlimited parental liability exposure.

Foreign companies seeking an operational presence for a defined project or exploratory phase, without committing to full local incorporation.

Partnerships in Haiti [Société en Nom Collectif, Société en Commandite Simple, Société en Commandite par Actions]

Haiti's partnership structures are governed by the Code de Commerce (originally derived from the French commercial code and adapted over time), which recognises three distinct forms: the Société en Nom Collectif (SNC), the Société en Commandite Simple (SCS), and the Société en Commandite par Actions (SCA). Each of these partnership structures in Haiti carries different liability profiles and operational characteristics, making them relevant for different commercial arrangements.

Registration is handled through the Centre de Facilitation des Investissements (CFI) and the commercial registry, with the partnership deed required to be notarised and published in accordance with local formalities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société en Nom Collectif / Société en Commandite Simple / Société en Commandite par Actions | Three distinct but related forms under the Code de Commerce |

| Members | Partners (associés); general partners bear unlimited liability | SCA additionally issues shares to limited partners |

| Minimum Partners | Minimum 2 partners across all three forms | No statutory maximum under general principles |

| Local Presence | Registered office in Haiti required | No mandatory local agent requirement for domestic partnerships |

| Capital | No prescribed minimum capital; Haitian Gourde (HTG) | SCA requires share capital divided into negotiable shares |

| Privacy | Partnership deeds are filed and publicly accessible via the commercial registry | Limited privacy for partner identities |

Focus Points

- Taxation: Partnerships are generally subject to Haiti's corporate income tax regime at a rate of 30% on net profits; VAT obligations apply to commercial activities; withholding taxes apply to distributions and payments to non-residents.

- Liability: General partners in both the SNC and the commandite structures carry unlimited, joint and several liability for firm debts.

- Annual Compliance: Partners must file annual financial statements and tax returns with the Direction Générale des Impôts (DGI); failure to comply triggers penalties.

- Conversion: Conversion between partnership forms is permitted under commercial law but requires notarial deed, creditor notification, and re-registration.

- Restrictions: Foreign participation in partnerships is permitted, though certain regulated sectors impose nationality or residency conditions on partners.

Sub-Types

Société en Nom Collectif (SNC)

The SNC is a general partnership in which all partners bear unlimited personal liability for the firm's obligations. It is most commonly used for small family-owned commercial operations or professional firms where partners maintain close operational control.

Société en Commandite Simple (SCS)

The SCS introduces a two-tier partner structure: general partners with unlimited liability manage the business, while limited partners contribute capital without participating in management. This structure suits investment arrangements where passive investors wish to limit their exposure.

Société en Commandite par Actions (SCA)

The SCA functions similarly to the SCS but divides the limited partners' interests into transferable shares, making it closer in structure to a joint stock company for the limited partner class. It is typically used for larger ventures requiring external capital while preserving management control among general partners.

Partnerships in Practice

Partnership structures are suitable for joint ventures, family enterprises, and investment vehicles where partners accept defined liability roles. The ability to separate management from capital contribution in commandite forms provides structural flexibility, though the unlimited liability carried by general partners remains a significant exposure for those in management roles.

Société en Commandite structures are best suited for investors or sponsors seeking passive participation with limited liability alongside a managing general partner willing to accept personal liability.

Sole Proprietorship [Entreprise Individuelle]

The sole proprietorship Haiti Entreprise Individuelle is the simplest business structure available to individual operators under the Haitian Commercial Code. Unlike corporate forms, it carries no separate legal personality — the proprietor and the business are treated as a single legal and financial unit.

Registration requires filing with the Registre du Commerce et des Sociétés (RCS) and obtaining a patent (patente) from the Direction Générale des Impôts (DGI). For self-employed business setup in Haiti, this structure involves minimal formation requirements and no mandatory minimum capital.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Owner Title | Proprietor (Propriétaire) | Single individual only; no co-owners |

| Liability | Unlimited personal liability | Personal assets are exposed to business debts |

| Local Presence | Registered business address in Haiti | Filing made at the RCS |

| Capital | No statutory minimum | Declared at registration for patent purposes |

| Privacy | Owner's name publicly associated with the business | No confidentiality mechanisms available |

Focus Points

- Taxation: Business income taxed as personal income under the DGI's general income tax (impôt sur le revenu); VAT registration required if annual turnover exceeds the applicable threshold; no separate corporate tax applies.

- Annual Compliance: Patent renewal required annually with the DGI; bookkeeping obligations apply even at the individual level.

- Treaty Access: As an unincorporated entity, access to Haiti's bilateral tax treaties is limited and generally not available.

- Conversion: Can be converted to an SARL or SA, though this requires a full new incorporation process rather than a structural amendment.

- Restrictions: Foreign nationals face practical and legal constraints when registering as a sole proprietor; local residency is generally expected.

Closing

The Entreprise Individuelle suits Haitian residents operating small-scale trading or service businesses where minimal administrative overhead is the primary consideration. The absence of liability protection is a significant constraint for anyone conducting activities that carry financial or legal risk.

Local individual operators running low-risk, small-scale businesses who do not require liability separation or external investors.

How to Choose the Right Entity Type in Haiti

Selecting how to choose a business entity in Haiti is a structural decision with direct legal and financial consequences — the wrong choice can expose your business to compliance failures, unnecessary costs, or restricted operational capacity.

Why Your Entity Choice Matters

- Registering a foreign branch under the wrong classification can result in operating outside the scope of your approved activities, triggering penalties under the regulatory oversight of Haiti's Ministry of Commerce and Industry (MCI).

- Choosing an entity form that lacks legal capacity to hold local contracts means any agreements your firm enters may be unenforceable before Haitian courts.

- Selecting a SARL when your activity requires a licensed financial or insurance structure results in an entity that cannot obtain the required sectoral authorisation.

- Forming a general partnership when limited liability is needed leaves all partners personally exposed to the full debts of the business, with no structural separation between personal and commercial assets.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each require a different legal form under Haiti's Commercial Code.

- Ownership Structure: A single-member operation points toward an Entreprise Individuelle or SARL, while multi-party ventures may require an SA with a defined board structure.

- Liability Exposure: Your tolerance for personal liability directly determines whether a corporate structure or a partnership form is appropriate.

- Local vs. Cross-Border Operations: Entities intending to transact with Haitian residents must be registered locally; representative offices carry restrictions on revenue-generating activity.

- Exit Strategy: Not all entity forms permit redomiciliation or conversion, so your anticipated exit path should influence your formation choice from the outset.

- Regulatory Compliance Capacity: If your business cannot maintain a physical presence or local management, certain entity forms will be difficult to sustain under MCI requirements.

Compliance Services for Companies in Haiti

Maintain your entity's good standing with ongoing compliance support across registration, filings, and regulatory obligations in Haiti.

Conclusion

Selecting the right structure is a foundational decision in any Haiti company incorporation, and this guide has mapped the primary options available under Haitian commercial law. The Société Anonyme suits larger operations requiring capital markets access or institutional investment. A Société à Responsabilité Limitée serves closely held businesses where liability protection matters but formation complexity should remain low. Branch offices give foreign entities a direct operational presence without creating a separate legal person. Partnerships, including the Société en Nom Collectif and Société en Commandite forms, work for ventures where partners accept defined liability arrangements. The Entreprise Individuelle fits sole operators with limited exposure.

Among registered entities, the SARL is the most commonly adopted structure for private business activity. Regulatory oversight through the Office National d'Assurance Vieillesse and relevant fiscal authorities continues to evolve, and your chosen entity type will determine how compliance obligations take shape going forward.

How Expanship Can Assist You

Expanship Haiti company formation services cover the full process of registering your entity with the Centre de Facilitation des Investissements (CFI) and the Registre du Commerce et des Sociétés, from initial structure selection to final certificate issuance. Our team works directly with the entities and registration processes outlined in this guide — whether you are forming a Société Anonyme, a SARL, or establishing a branch of a foreign company.

From document preparation to post-registration obligations, your business has a single point of contact throughout.

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Government filing and registrar liaison

- Post-incorporation compliance management

- Corporate secretarial support

- Banking introduction assistance

Reach out directly through our Expanship Haiti contact page to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The Société à Responsabilité Limitée (SARL) is the most frequently formed entity, largely because it combines limited liability protection with a relatively straightforward registration process under the Commercial Code. Its flexible capital and management requirements make it accessible to both local entrepreneurs and foreign investors entering the Haitian market.

A SARL is designed for smaller, closely held operations, whereas an SA is structured for larger enterprises that may seek to raise capital through share issuance. The SA carries heavier compliance obligations, including mandatory auditor appointments and more formal governance requirements. Tax treatment under Haitian law does not differ fundamentally between the two, but the administrative burden of maintaining an SA is considerably higher.

The SARL generally affords greater confidentiality relative to the SA, as shareholder disclosure requirements are less extensive in practice. Nominee arrangements are not formally prohibited, though their legal standing depends on the underlying contractual structure. Beneficial ownership transparency is an evolving area of Haitian regulatory policy.

No. A Société en Nom Collectif and a Société en Commandite Simple each require at least two partners by definition. The SARL and SA can theoretically be formed with a single founding shareholder under certain interpretations of the Commercial Code, while a Sole Proprietorship (Entreprise Individuelle) is inherently a single-person structure.

Foreign nationals may form a SARL, SA, or establish a Branch Office in Haiti. Registration of foreign-owned entities typically requires approval from the Centre de Facilitation des Investissements (CFI) and compliance with sectoral restrictions that may apply in specific industries. A Representative Office is available for liaison activities but cannot generate revenue locally.

Conversion between entity types is not comprehensively codified in Haitian corporate law, though restructuring through dissolution and re-registration is a recognized practice. Transforming a SARL into an SA, for example, generally requires shareholder resolution, updated statutes, and re-registration with the relevant commercial registry. Legal counsel familiar with the Commercial Code should be engaged before initiating any conversion.

Not all do. The Entreprise Individuelle does not constitute a separate legal person; the owner and the business are treated as one for liability and tax purposes. The SARL, SA, Société en Commandite par Actions, and Branch Offices registered under a foreign parent do carry distinct legal personality, though a Branch's juridical independence is limited by its relationship to the parent entity.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.