Key Takeaways

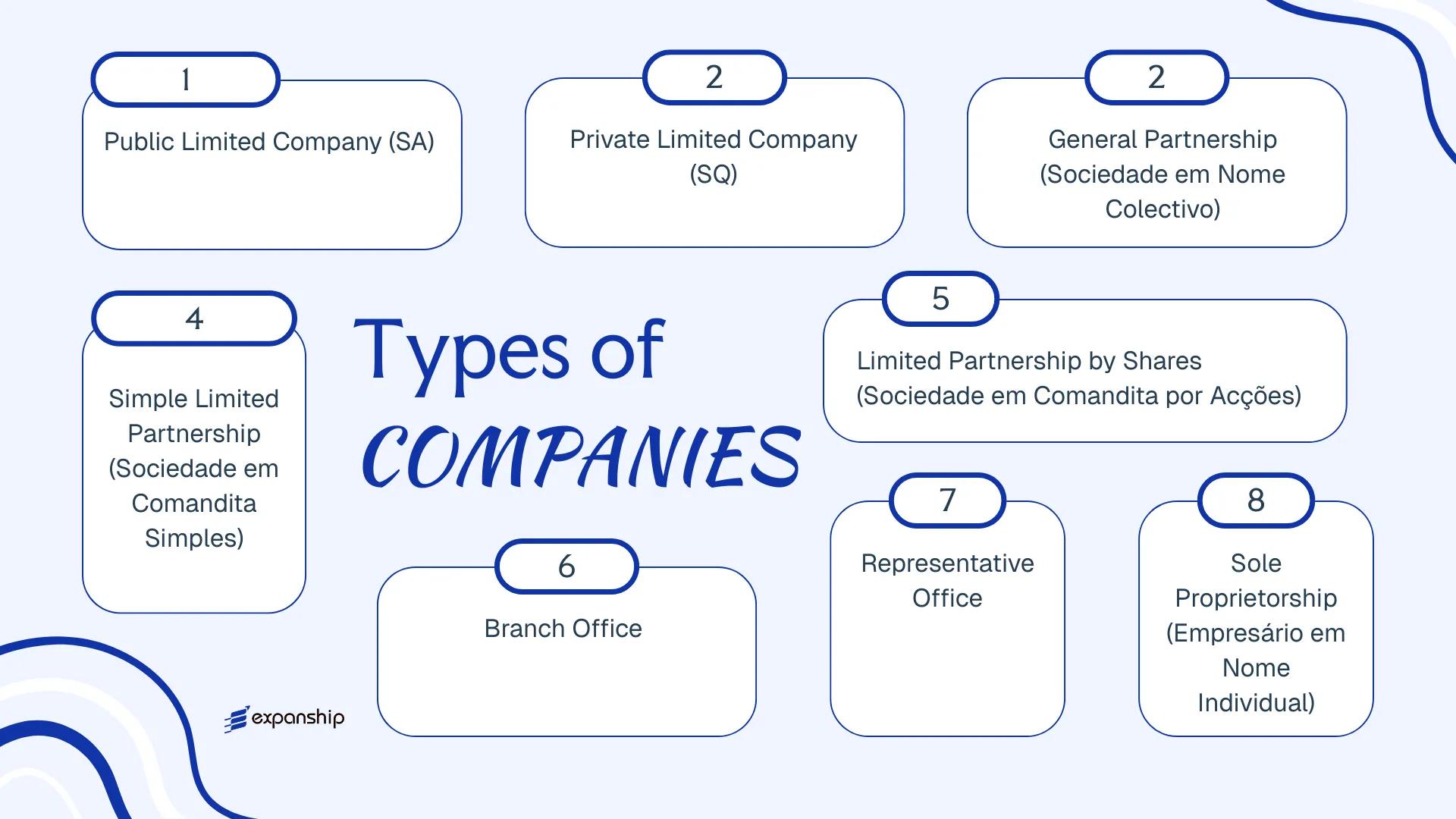

- Guinea-Bissau recognizes eight distinct business entity types under its commercial law, ranging from the Sociedade Anónima to the Empresário em Nome Individual, each with different liability, capital, and governance requirements.

- The Sociedade por Quotas is the most commonly registered entity in Guinea-Bissau, favored by small and medium-sized businesses for its quota-based ownership structure and lower capital threshold relative to the SA.

- Business registration in Guinea-Bissau falls under the Conservatória do Registo Comercial, which operates within the country's Ministry of Justice framework.

- Since adopting the OHADA framework in 2015, Guinea-Bissau's commercial law has been progressively aligning with regional standards, which may improve legal predictability for foreign investors over time.

Introduction to Entity Types in Guinea-Bissau

Located on the West African coast and bordered by Senegal to the north and Guinea to the south and east, Guinea-Bissau is an independent republic that also includes the Bijagós Archipelago. Business registration falls under the jurisdiction of the Conservatória do Registo Comercial, the commercial registry operating within the country's Ministry of Justice framework. The tax regime is territorial in orientation, with corporate tax obligations generally applying to income sourced within the country.

Several business entity types Guinea-Bissau recognizes under its commercial law are available to both resident and foreign investors:

- Sociedade Anónima (SA)

- Sociedade por Quotas (SQ)

- Sociedade em Nome Colectivo

- Sociedade em Comandita Simples

- Sociedade em Comandita por Acções

- Branch Office

- Representative Office

- Empresário em Nome Individual

Each of these Guinea-Bissau corporate structures carries distinct requirements around minimum capital, liability, governance, and foreign ownership. This article examines each legal entity in detail to help your business determine which structure fits your operational and legal objectives.

An Overview of Business Structures in Guinea-Bissau

Guinea-Bissau recognises several distinct legal entity types under its commercial law framework, which draws from the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, adopted following the country's accession to the OHADA treaty. Each structure carries different implications for liability, capital requirements, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedade Anónima (SA) | Public Limited Company | Limited to share capital | Taxed | Yes | 1 shareholder | Ministry of Commerce | OHADA Uniform Act |

| Sociedade por Quotas (SQ) | Private Limited Company | Limited to quota value | Taxed | Yes | 1 member | Ministry of Commerce | OHADA Uniform Act |

| Sociedade em Nome Colectivo | General Partnership | Unlimited, joint | Taxed | Yes | 2 partners | Ministry of Commerce | OHADA Uniform Act |

| Sociedade em Comandita Simples | Limited Partnership | Mixed liability | Taxed | Yes | 2 partners | Ministry of Commerce | OHADA Uniform Act |

| Sociedade em Comandita por Acções | Partnership with Shares | Mixed liability | Taxed | Yes | 2 partners | Ministry of Commerce | OHADA Uniform Act |

| Branch Office | Foreign Entity Extension | Parent liable | Taxed | Yes | 1 parent company | Ministry of Commerce | OHADA Uniform Act |

| Representative Office | Non-trading Presence | Parent liable | Generally exempt | No | 1 parent company | Ministry of Commerce | OHADA Uniform Act |

| Empresário em Nome Individual | Sole Proprietorship | Unlimited, personal | Taxed | Yes | 1 individual | Ministry of Commerce | OHADA Uniform Act |

Each of these structures is examined in full in the sections below.

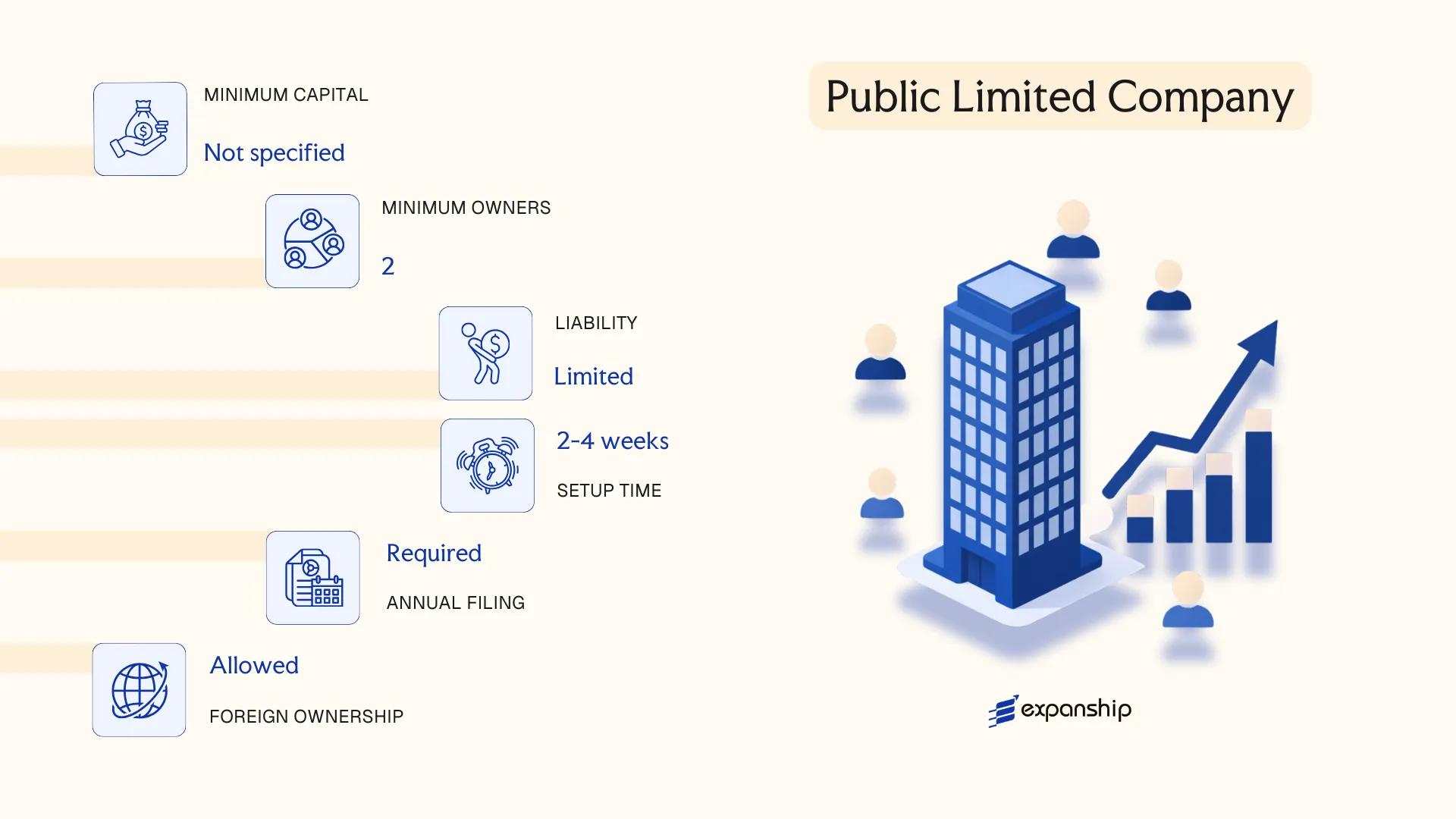

Sociedade Anónima (SA) — Public Limited Company

The Sociedade Anónima Guinea-Bissau SA structure derives from the commercial law framework inherited from Portugal and subsequently adapted under Guinea-Bissau's national legislation. It carries full separate legal personality, meaning the entity itself holds rights and obligations independently of its shareholders.

Shareholders bear no personal liability beyond their subscribed capital contributions. This structure suits businesses seeking to raise capital from multiple investors or establish a formalized corporate presence.

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (Joint Stock Company) | Separate legal personality; liability limited to subscribed capital |

| Members | Shareholders — minimum 5 | No statutory maximum; shares freely transferable in principle |

| Governing Body | Board of Directors (Conselho de Administração) + Supervisory Board or Fiscal Council | Dual-tier governance structure required for larger entities |

| Local Presence | Registered office in Guinea-Bissau required | No statutory registered agent requirement confirmed under general practice |

| Share Capital | Minimum FCFA 1,000,000 (XOF) | Must be fully subscribed at incorporation; partial paid-up permitted under general OHADA-influenced practice |

| Privacy | Shareholder register maintained; publicly filed documents include incorporation deed | Beneficial ownership disclosure subject to applicable AML regulations |

Focus Points

- Taxation: Corporate income tax applies to net profits; VAT applies to qualifying transactions; withholding taxes apply to dividends, interest, and royalties paid to non-residents — consult the Ministério das Finanças for current rates.

- Annual Compliance: Financial statements must be prepared annually; audit obligations apply above prescribed thresholds.

- Economic Substance: No formalized substance regime confirmed, but a registered office and operational presence are standard requirements.

- Treaty Access: Guinea-Bissau's tax treaty network is limited; verify bilateral arrangements before relying on reduced withholding rates.

- Conversion: An SA may generally be converted to another corporate form through shareholder resolution and regulatory filing, subject to procedural requirements.

Closing

The SA suits larger trading operations, joint ventures, or entities planning to bring in multiple institutional investors, though the minimum five-shareholder requirement and governance obligations make it administratively heavier than smaller structures. For businesses that anticipate growth but carry fewer initial stakeholders, the compliance burden warrants careful evaluation before incorporation.

The SA is best suited for mid-to-large enterprises, joint ventures, or investor-backed businesses requiring a formalized share capital structure with freely transferable ownership interests.

Company Incorporation in Guinea-Bissau

Incorporate a Sociedade Anónima or other business entity in Guinea-Bissau with end-to-end support from Expanship.

Sociedade por Quotas (SQ) — Private Limited Company

The Sociedade por Quotas Guinea-Bissau framework is governed by the OHADA Uniform Act on Commercial Companies and Economic Interest Groups, adopted under Guinea-Bissau's membership in the Organisation for the Harmonisation of Business Law in Africa. The SQ carries separate legal personality from its members and confers limited liability, meaning each member's exposure is capped at the value of their subscribed quota.

Capital is divided into quotas rather than shares, which restricts free transferability and keeps ownership within a defined group. This structural feature makes the SQ private limited company Guinea-Bissau framework more suited to closely held businesses than to entities seeking open capital markets.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedade por Quotas (SQ) | Separate legal personality; limited liability |

| Members | Minimum 1, maximum 50 | Members are referred to as "associados" (quota holders); single-member SQ is permitted |

| Management | One or more gérants (managers) | Managers need not be members; no nationality requirement under OHADA rules |

| Registered Office | Physical address in Guinea-Bissau required | A registered office address must be maintained locally |

| Share Capital | Minimum 1,000,000 XOF | Divided into quotas; no par value floor per quota specified under general OHADA rules |

| Privacy | Member names filed with RCCM | The Registre du Commerce et du Crédit Mobilier (RCCM) maintains public records |

Focus Points

- Taxation: Corporate income tax applies at the standard rate; VAT obligations arise on taxable supplies; withholding taxes apply to dividends, interest, and service fees paid to non-residents; stamp duty may apply to certain instruments.

- Annual Compliance: Annual financial statements must be filed; general meetings of members are required per the OHADA Uniform Act calendar.

- Treaty Access: Guinea-Bissau's tax treaty network is limited; verify applicability before relying on reduced withholding rates.

- Quota Transfer: Transfers to third parties outside the existing membership require member consent, governed by the articles of association and OHADA transfer rules.

- Conversion: An SQ may be converted into a Sociedade Anónima once it meets the statutory thresholds for that form under the OHADA Uniform Act.

The SQ suits trading operations, Guinea-Bissau limited liability company formation for SMEs, and holding structures where concentrated ownership is intended. Its principal advantage is straightforward formation with a relatively low capital threshold; the key limitation is that quota transferability is restricted, which can complicate exits or investor onboarding.

The SQ is most appropriate for small-to-medium enterprises, family-owned businesses, and foreign investors establishing a locally incorporated operational subsidiary with a defined ownership group.

Partnerships in Guinea-Bissau [Sociedade em Nome Colectivo, Sociedade em Comandita Simples, Sociedade em Comandita por Acções]

Partnership structures in Guinea-Bissau are governed by the country's commercial code, which draws substantially from the Portuguese Código Comercial tradition, reflecting the jurisdiction's civil law heritage. Three recognised forms exist: the Sociedade em Nome Colectivo (general partnership), the Sociedade em Comandita Simples (simple limited partnership), and the Sociedade em Comandita por Acções (partnership limited by shares).

Each form carries distinct liability profiles. General partners bear unlimited personal liability for firm obligations, while limited partnership structures introduce a tiered membership model separating active management from passive capital contribution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedade em Nome Colectivo / Sociedade em Comandita Simples / Sociedade em Comandita por Acções | Separate legal personality upon registration |

| Members | Partners (general and, where applicable, limited/commanditaire) | Minimum 2 partners; no statutory maximum specified |

| Liability | General partners: unlimited; Limited partners: capped at contribution | Comandita structures separate these roles formally |

| Registered Office | Physical address in Guinea-Bissau required | Must be maintained for official correspondence |

| Capital | No statutory minimum for SNC or Comandita Simples; Comandita por Acções requires share capital | Denominated in West African CFA franc (XOF) |

| Privacy | Partner names typically appear in the commercial register | Public disclosure applies to general partners |

Focus Points

- Taxation: Partnerships are generally subject to corporate income tax (Imposto Industrial) on profits; VAT obligations apply to taxable activities; withholding tax may apply to distributions depending on partner residency.

- Annual Compliance: Financial statements must be filed with the Conservatória do Registo Comercial; accounting records are required to be maintained locally.

- Treaty Access: Guinea-Bissau has a limited tax treaty network; access to treaty benefits for partnership income should be assessed on a case-by-case basis.

- Restrictions: Foreign nationals may face additional approval requirements when registering as general partners with unlimited liability exposure.

Sub-Types

Sociedade em Nome Colectivo (SNC)

All partners hold general status and carry unlimited, joint liability for the firm's debts. This structure is typically used by small professional or family-run businesses where partners are actively involved in management.

Sociedade em Comandita Simples

Two partner classes co-exist: general partners with unlimited liability who manage the business, and limited (commanditaire) partners whose liability is confined to their agreed capital contribution. This form suits arrangements where passive investors participate alongside active operators.

Sociedade em Comandita por Acções

Limited partners hold transferable shares rather than fixed quotas, introducing a capital-market element to the partnership structure. This hybrid form is less common and typically used for larger enterprises seeking flexible capital admission without full conversion to a Sociedade Anónima.

Closing

Partnership structures in Guinea-Bissau are most applicable to closely held businesses, family enterprises, or arrangements where at least one party accepts unlimited liability in exchange for operational control. The principal limitation is that general partners remain personally exposed to all firm liabilities, which constrains the risk appetite required to use these structures.

These structures are best suited to small domestic businesses or joint ventures where partners have an established relationship and accept the liability implications of the chosen form.

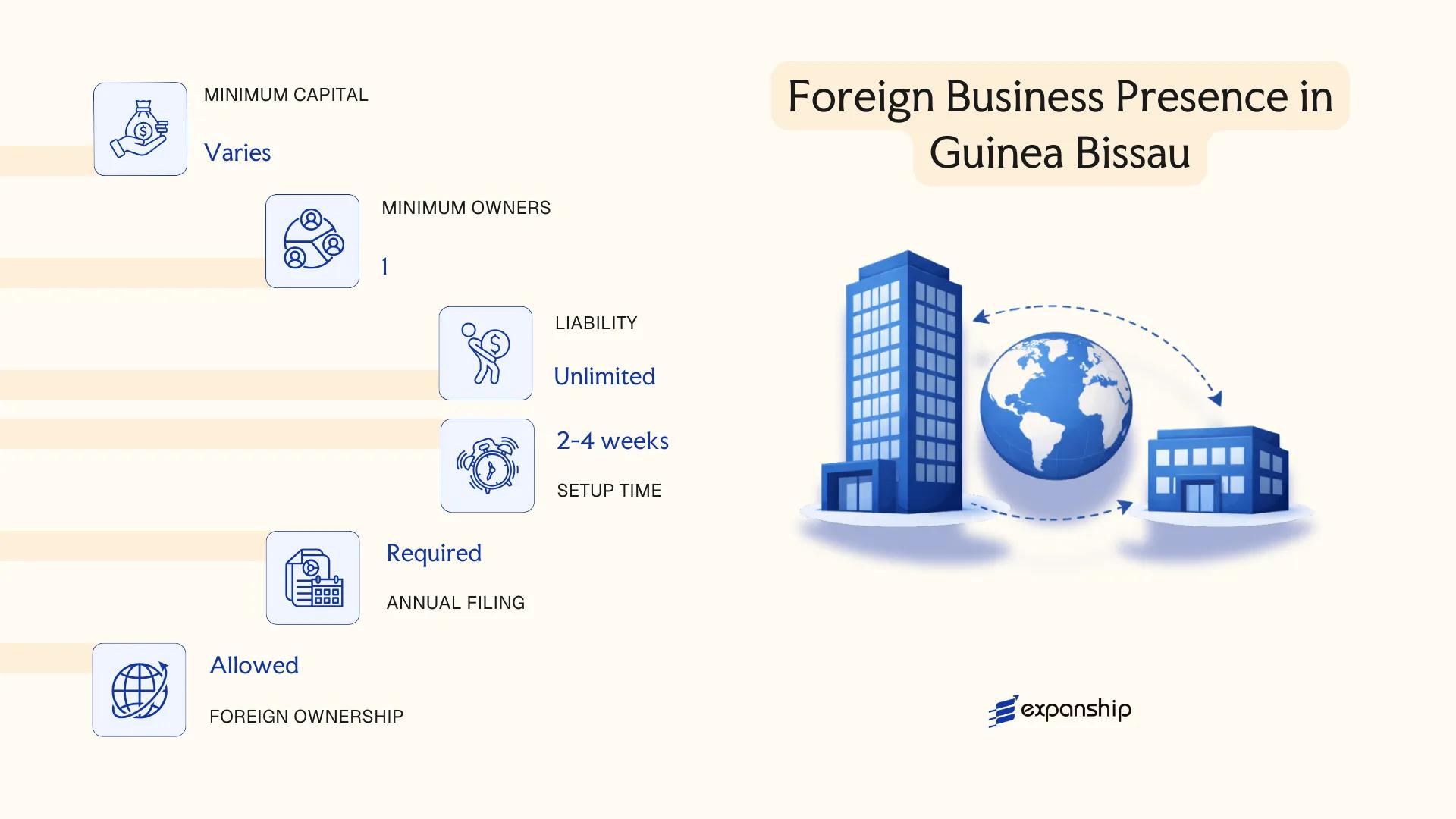

Foreign Business Presence in Guinea-Bissau [Branch Office, Representative Office]

A foreign company branch in Guinea-Bissau operates under the country's Commercial Code, which draws heavily from the OHADA Uniform Act on Commercial Companies and Economic Interest Groups. A branch does not constitute a separate legal entity — it remains an extension of the parent company, meaning the parent bears unlimited liability for the branch's obligations. A representative office, by contrast, is restricted to non-commercial activities such as market research and liaison functions.

Registering either structure requires filing with the Conservatória do Registo Comercial. The branch must submit authenticated copies of the parent company's constitutive documents, proof of legal existence in the home jurisdiction, and a power of attorney designating a local representative. Representative office setup in Guinea-Bissau follows a similar administrative process but operates under more restricted authorizations.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Permitted Activities | Full commercial operations | Non-commercial only (liaison, research) |

| Local Representative | Mandatory | Mandatory |

| Registered Address | Required in-country | Required in-country |

| Capital Requirement | No statutory minimum | No statutory minimum |

| Liability | Parent bears full liability | Parent bears full liability |

Focus Points

- Taxation: Branches are subject to corporate income tax on Guinea-Bissau-sourced profits; VAT and withholding tax obligations mirror those of locally incorporated entities.

- Economic Substance: No formal substance regime exists, but the branch must maintain a genuine operational presence to conduct commercial activity.

- Annual Compliance: Annual accounts must be filed reflecting the branch's local operations, separate from the parent's consolidated accounts.

- Treaty Access: Access to double tax treaties depends on the parent entity's residence jurisdiction; Guinea-Bissau's treaty network is limited.

- Restrictions: Representative offices cannot invoice, generate revenue, or enter into commercial contracts in their own name.

Closing

A branch suits foreign firms testing the local market or executing specific contracts without incorporating a new entity, though the parent's unlimited exposure to local liabilities is a significant structural drawback.

Best suited for established foreign companies seeking direct commercial operations in Guinea-Bissau without the administrative burden of incorporating a separate subsidiary.

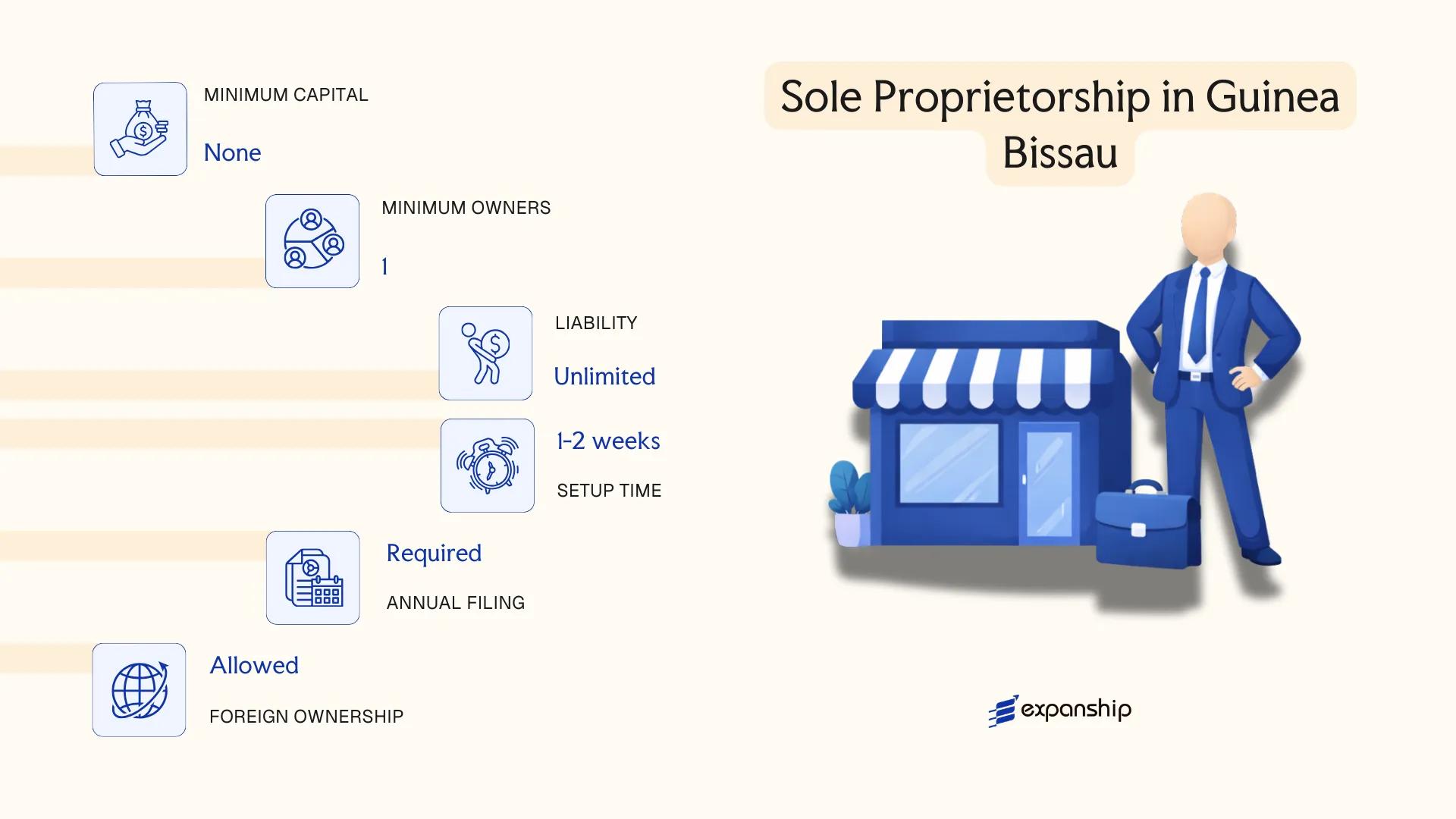

Sole Proprietorship in Guinea-Bissau [Empresário em Nome Individual]

The Empresário em Nome Individual is the simplest business form available under Guinea-Bissau's commercial law, which draws from the OHADA Uniform Act on General Commercial Law (Acte Uniforme relatif au Droit Commercial Général), to which Guinea-Bissau acceded. Registration is handled through the Conservatória do Registo Comercial (Commercial Registry).

There is no separation between the proprietor and the business — the individual and the enterprise are legally one. This means your personal assets remain exposed to all business liabilities, with no liability shield of any kind.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Unincorporated) | No separate legal personality |

| Referred To As | Proprietor / Entrepreneur | Single individual only |

| Members | 1 individual (minimum and maximum) | Must be a natural person |

| Local Presence | Registered business address required | No registered agent requirement specified under OHADA |

| Capital | No statutory minimum; XOF (West African CFA Franc) | Capital reflects proprietor's own contribution |

| Liability | Unlimited personal liability | Personal estate fully exposed to business debts |

Focus Points

- Taxation: Subject to personal income tax (Imposto sobre o Rendimento das Pessoas Singulares) on business profits; VAT registration applies if turnover thresholds are met; no separate corporate tax layer.

- Annual Compliance: Annual tax declaration required; no separate financial statements filing obligation comparable to incorporated entities.

- Conversion: Can be converted into an incorporated structure, though the process requires fresh registration rather than a simple transformation.

- Treaty Access: As an unincorporated individual trader, access to double tax treaty benefits depends on the proprietor's personal tax residency status, not a corporate entity status.

- Restrictions: Foreign nationals may face additional licensing or residency conditions before registering as an individual entrepreneur.

Closing

This structure suits Guinea-Bissau-based individuals conducting small-scale, low-risk trading or service activities where administrative simplicity outweighs the need for liability protection.

Local individual traders or artisans operating at small scale who do not require a liability shield and want minimal administrative overhead.

How to Choose the Right Entity Type in Guinea-Bissau

Choosing the right company type in Guinea-Bissau is not a formality — the structure you register determines your tax exposure, liability, reporting obligations, and operational flexibility from day one.

Why Your Entity Choice Matters

Selecting the wrong structure carries concrete legal and financial consequences:

- Registering a branch or representative office when your business model requires local contracting may result in the arrangement being treated as an undisclosed permanent establishment, exposing the parent entity to local tax liability.

- Forming a Sociedade Anónima when your firm is a single-person operation subjects you to statutory audit requirements and minimum capital thresholds that do not apply to a Sociedade por Quotas or sole proprietorship.

- Choosing a structure without the legal capacity to hold property or employ staff directly creates compliance gaps that regulators may treat as a registration violation under applicable commercial law.

- Selecting a partnership form when limited liability is a priority leaves partners personally exposed to business debts with no corporate shield.

Key Factors to Consider

- Business Activity: Active trading, regulated sectors such as banking, and passive asset holding each correspond to different permitted structures under Guinea-Bissau's commercial framework.

- Ownership Structure: A single founder operating independently points toward an Empresário em Nome Individual or SQ, while multi-investor arrangements with transferable equity require an SA.

- Liability Exposure: If personal asset protection is a priority, structures with unlimited liability — such as general partnerships — are unsuitable.

- Statutory Obligations: The reporting and capital requirements attached to each entity type vary; your administrative capacity should match those obligations.

- Exit and Restructuring: Some structures permit conversion or dissolution more straightforwardly than others — confirm this before incorporating.

Guinea-Bissau's primary company formation legislation, the Commercial Code, governs these structural requirements in full.

Compliance Services for Companies in Guinea-Bissau

Ongoing compliance support for Guinea-Bissau registered entities, including annual filings, statutory record maintenance, and regulatory reporting.

Conclusion

Incorporating a company in Guinea-Bissau requires selecting a legal structure that matches your operational scope, ownership preferences, and liability tolerance. The Sociedade por Quotas remains the most commonly registered entity, favored by small and medium-sized businesses for its flexible quota-based ownership and lower capital threshold. The Sociedade Anónima suits larger ventures requiring share transferability and capital market access. Partnerships carry unlimited or mixed liability, making them appropriate only where partners accept personal exposure. Branch and representative offices serve foreign firms testing market presence without establishing a separate legal person. The Empresário em Nome Individual fits sole operators running low-risk, low-capital activities.

Guinea-Bissau's regulatory environment, administered under the OHADA framework adopted in 2015, continues to align with regional commercial law standards, which may progressively improve legal predictability for foreign investors. Professional guidance through the formation process remains advisable given the administrative requirements at the Conservatória do Registo Comercial.

How Expanship Can Assist You

Providing corporate services in Guinea-Bissau, Expanship works directly with businesses forming entities under the OHADA Uniform Act on Commercial Companies, which governs Sociedades Anónimas, Sociedades por Quotas, and partnership structures in the country. From initial registration with the Centro de Formalização de Empresas (CFE) through to ongoing compliance obligations, your business has a single point of contact throughout the entire process.

Expanship's Guinea-Bissau company formation assistance covers the full operational setup of your entity:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Government filing and CFE liaison

- Post-incorporation compliance management, including annual obligations

- Banking introduction assistance for newly incorporated entities

Our business incorporation support in Guinea-Bissau also extends to foreign businesses establishing branch offices or representative presences under local regulatory requirements.

Reach out to Expanship Guinea-Bissau to discuss your specific requirements.

Frequently Asked Questions (FAQ)

The Sociedade por Quotas (SQ) is the most frequently registered entity. Its lower capital threshold and simplified governance structure make it the default choice for small to mid-sized commercial operations.

Both structures permit local trading and are subject to corporate tax under Guinea-Bissau's fiscal framework, but the SA carries heavier ongoing obligations, including mandatory auditing once share capital or turnover crosses statutory thresholds. The SQ suits closely held businesses, while the SA is structured for entities anticipating broader shareholder bases or external investment.

The SQ generally affords more privacy than the SA, as public share issuance is not permitted and ownership is recorded through quota certificates rather than a publicly traded register. Nominee arrangements may be available through licensed service providers, though their legal effect depends on the underlying agreement.

No. Partnerships, including the Sociedade em Nome Colectivo and both forms of Sociedade em Comandita, require at least two partners by definition. The SQ and SA can be formed with a single founding member in some configurations, though minimum capital and directorship requirements still apply.

Foreign investors may register an SA, SQ, branch office, or representative office. Branch offices operate as extensions of the parent company without separate legal personality, while an SQ or SA constitutes an independent legal entity subject to local corporate law.

Conversion between entity types is permissible under general company law principles derived from the OHADA Uniform Act on Commercial Companies, which Guinea-Bissau applies. An SQ may be converted to an SA, provided the conditions for the target structure, including minimum capital and shareholder count, are met at the time of conversion.

Not all do. The Sociedade em Nome Colectivo and Sociedade em Comandita Simples operate with partners who bear personal liability, and while these structures hold legal personality as firms, the liability shield is substantially weaker than that afforded by the SQ or SA. Representative offices have no independent legal personality whatsoever.

The Empresário em Nome Individual (sole proprietorship) has the lightest administrative burden, with no board requirements, no minimum capital, and simplified tax filing. That simplicity comes with full personal liability for all business obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.