Key Takeaways

- Business formations in Guam are administered by the Department of Revenue and Taxation (DRT), which operates under a hybrid framework where federal U.S. law coexists with local statutes governed by Title 18 of the Guam Code Annotated.

- The LLC is the most widely registered entity type in Guam, favored for its combination of limited liability protection and pass-through taxation under the territory's mirrored U.S. income tax system.

- Foreign corporations, LLCs, and partnerships must qualify through the Department of Revenue and Taxation before conducting business in Guam, operating under a parallel registration framework distinct from domestic entity formation.

- Sole proprietorships in Guam provide no liability separation between the owner and the business, making them suitable only for low-risk, single-operator activities.

Introduction to Entity Types in Guam

Guam is an island territory in the western Pacific Ocean, situated at the southern end of the Mariana Islands chain and approximately 2,500 kilometers east of the Philippines. As an unincorporated territory of the United States, it operates under a hybrid legal framework — federal U.S. law applies in many respects, while local statutes govern areas including business registration and corporate governance.

Business formations are administered by the Department of Revenue and Taxation (DRT), which serves as the primary regulatory body for entity registration on the island. Guam applies a territorial-style tax system, with businesses subject to a local income tax structure that mirrors the U.S. Internal Revenue Code but is administered independently by the DRT.

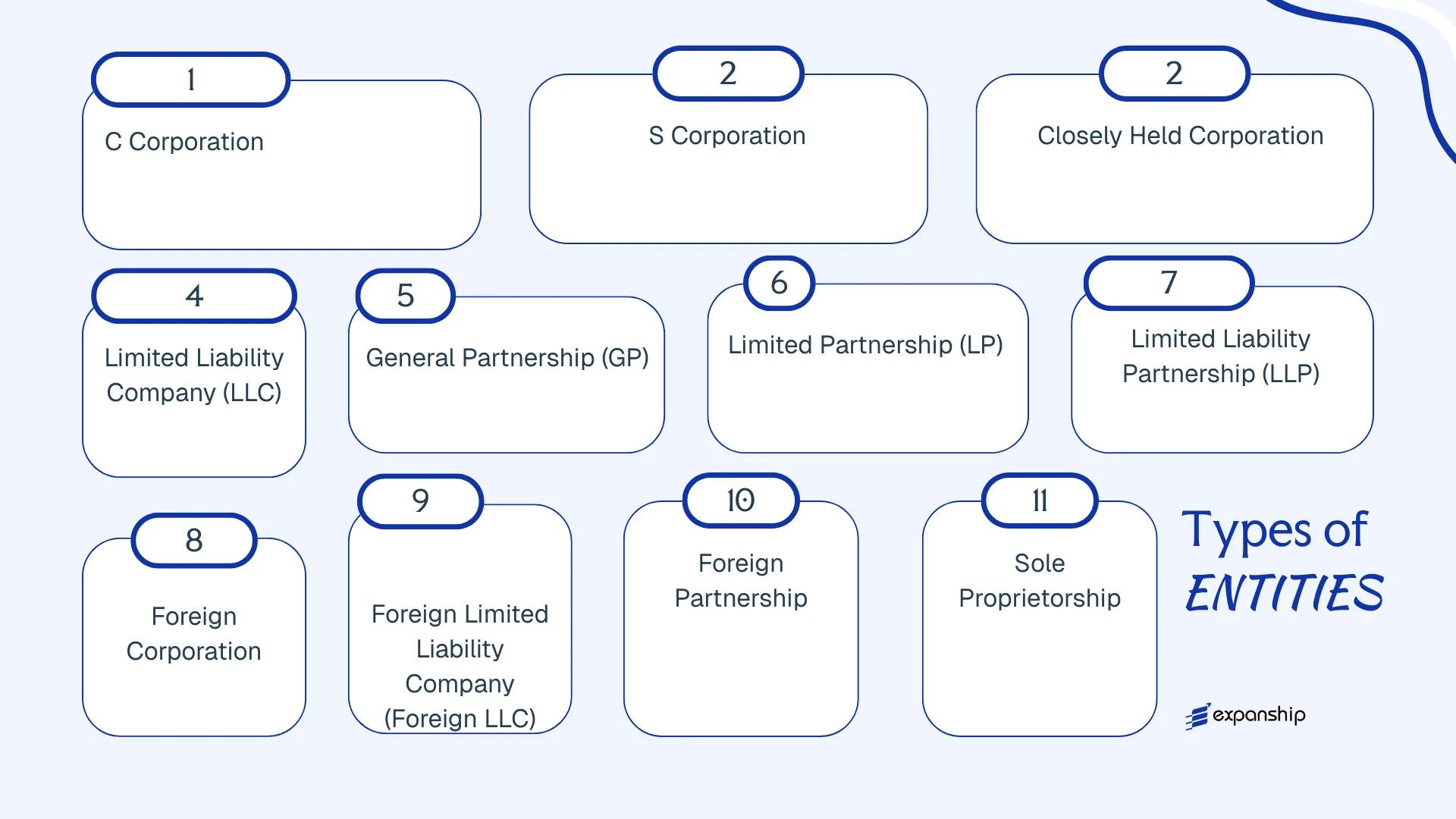

The available business entity types in Guam include corporations (C Corporation, S Corporation, and Closely Held Corporation), limited liability companies, general partnerships, limited partnerships, limited liability partnerships, foreign entities, and sole proprietorships. This article examines each structure across the Guam business structures overview — covering formation requirements, governance rules, liability treatment, and tax classification to help you assess which structure fits your business objectives.

An Overview of Business Structures in Guam

Guam recognizes several distinct business structures under its local company law framework, with the primary legislation governing these entities being Title 18 of the Guam Code Annotated, which addresses corporations, partnerships, and related commercial organizations. An overview of business structures in Guam shows that available options range from sole proprietorships to foreign entity registrations, each designed to meet different operational, liability, and tax requirements. The sections that follow examine each structure in full detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| C Corporation | Separate legal entity | Limited to investment | Corporate-level tax applies | Permitted | 1 incorporator | Guam Department of Revenue & Taxation | Title 18 GCA |

| S Corporation | Separate legal entity | Limited to investment | Pass-through taxation | Permitted | 1–100 shareholders | Guam Department of Revenue & Taxation | Title 18 GCA |

| Closely Held Corporation | Separate legal entity | Limited to investment | Corporate or pass-through | Permitted | Few shareholders | Guam Department of Revenue & Taxation | Title 18 GCA |

| LLC | Hybrid legal entity | Members generally protected | Pass-through by default | Permitted | 1 member | Guam Department of Revenue & Taxation | Title 18 GCA |

| General Partnership | Unincorporated association | Unlimited personal liability | Pass-through taxation | Permitted | 2 partners | Guam Department of Revenue & Taxation | Title 18 GCA |

| Limited Partnership | Unincorporated association | Mixed: general/limited | Pass-through taxation | Permitted | 2 partners | Guam Department of Revenue & Taxation | Title 18 GCA |

| Limited Liability Partnership | Unincorporated association | Partners generally protected | Pass-through taxation | Permitted | 2 partners | Guam Department of Revenue & Taxation | Title 18 GCA |

| Foreign Corporation | Registered foreign entity | Limited to investment | Subject to local tax | Permitted | 1 (existing entity) | Guam Department of Revenue & Taxation | Title 18 GCA |

| Foreign LLC | Registered foreign entity | Members generally protected | Subject to local tax | Permitted | 1 (existing entity) | Guam Department of Revenue & Taxation | Title 18 GCA |

| Foreign Partnership | Registered foreign entity | Varies by structure | Subject to local tax | Permitted | 2 (existing entity) | Guam Department of Revenue & Taxation | Title 18 GCA |

| Sole Proprietorship | Unincorporated individual | Unlimited personal liability | Personal income tax | Permitted | 1 owner | Guam Department of Revenue & Taxation | Local licensing rules |

Each of these structures is examined in full in the sections below.

Corporation (C Corporation, S Corporation, Closely Held Corporation)

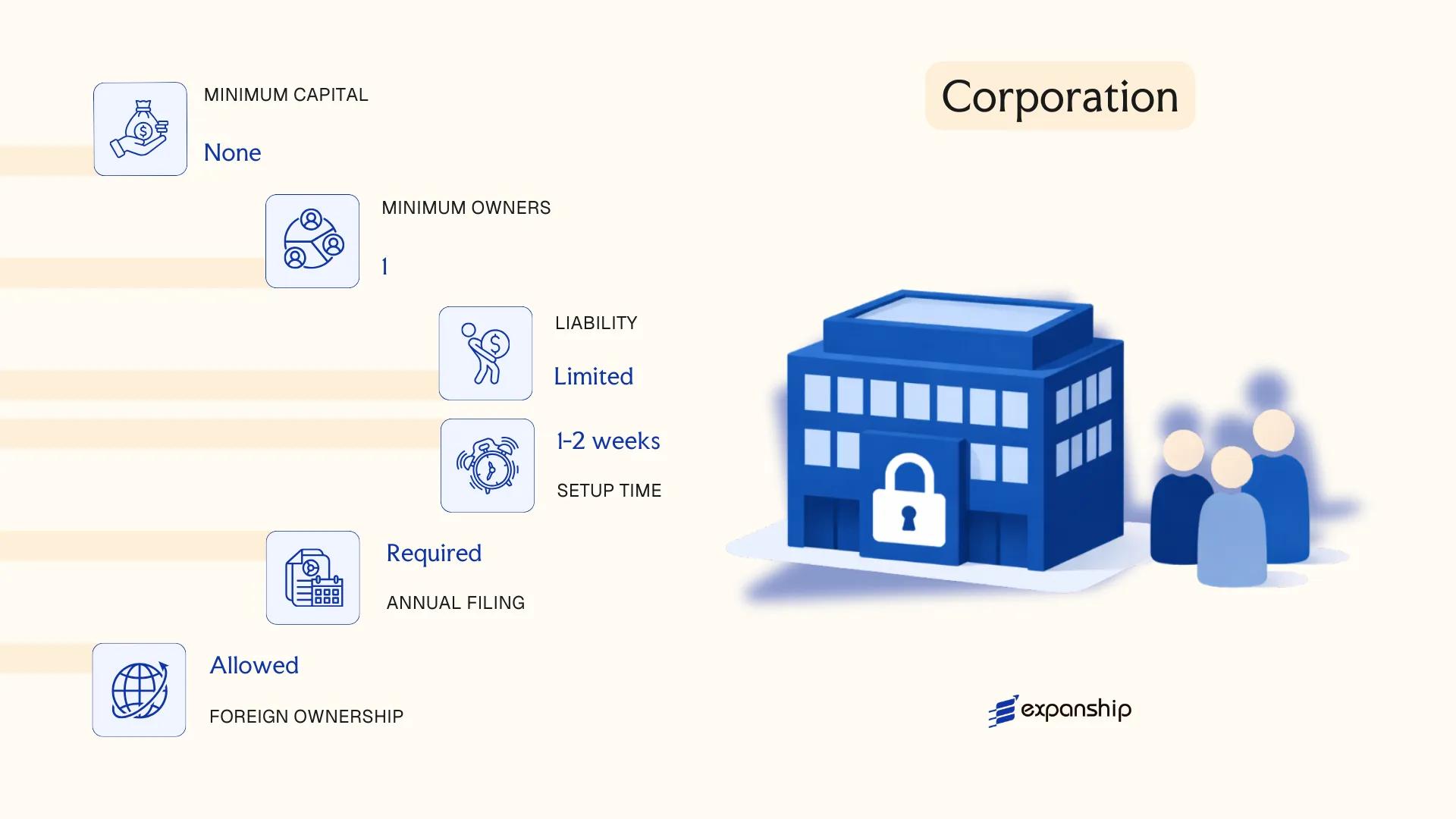

Guam corporation formation types are governed by the Guam Corporations Act, codified under Title 18 of the Guam Code Annotated. A corporation formed under this statute exists as a separate legal entity from its shareholders, meaning the business can own property, enter contracts, and incur liabilities independently.

Shareholders' personal assets are generally shielded from corporate debts. The structure suits businesses seeking defined governance, transferable ownership, and a recognized form for external investment or public filings.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | For-profit corporation | Separate legal personality under Title 18, Guam Code Annotated |

| Members | Shareholders (owners); Directors (governance); Officers (management) | Minimum 1 shareholder; no maximum. Minimum 1 director |

| Local Presence | Registered Agent with a Guam address required | Registered office address must be maintained in Guam |

| Capital | USD; no statutory minimum paid-up capital | Authorized share capital defined in articles of incorporation |

| Privacy | Director and officer names filed with the Department of Revenue and Taxation | Shareholder information not publicly disclosed in standard filings |

Focus Points

- Taxation: Corporations are subject to Guam's income tax under the Guam Territorial Income Tax (GTIT), which mirrors the U.S. Internal Revenue Code; no separate VAT applies, though a 4% Business Privilege Tax (BPT) applies to gross receipts; withholding taxes apply to dividends paid to non-resident shareholders.

- Annual Compliance: Annual report and franchise fee filing required with the Department of Revenue and Taxation; failure to file can result in administrative dissolution.

- Treaty Access: Guam is a U.S. territory and does not independently access U.S. tax treaties; treaty eligibility depends on specific provisions and entity classification.

- Conversion: A corporation may convert to an LLC under Guam law, subject to filing requirements and shareholder approval.

- Restrictions: Certain regulated industries require additional licensing beyond standard incorporation.

Sub-Types

C Corporation

A standard Guam corporation taxed at the entity level under the GTIT, with shareholders also taxed on dividends received — producing a double taxation effect. This structure is commonly used by businesses anticipating external investment, multiple share classes, or eventual public offerings.

S Corporation

An S corporation elects pass-through taxation under the U.S. Internal Revenue Code, meaning income and losses flow directly to shareholders' personal returns without entity-level tax. Eligibility is limited to a maximum of 100 shareholders, all of whom must be U.S. citizens or resident individuals — a restriction that limits its utility for international ownership structures.

Closely Held Corporation

A closely held corporation Guam recognizes is one with a small number of shareholders, often operating under a shareholder agreement that restricts share transfers. It is typically used by family-owned businesses or small professional groups that want corporate liability protection without wide share distribution.

When to Use This Structure

Corporations are well-suited for operating businesses, holding structures, and entities seeking access to formal capital markets or U.S.-aligned governance frameworks. The defined liability separation is a clear structural advantage; the compliance burden — including annual reporting, board formalities, and potential double taxation in the C corporation variant — adds ongoing administrative cost.

Businesses with multiple investors, those planning structured ownership transfers, or operations requiring a formally recognized U.S.-territorial corporate entity.

Company Incorporation in Guam

Incorporate a corporation or other business entity in Guam with end-to-end support from document preparation to registered agent services.

Limited Liability Company (LLC)

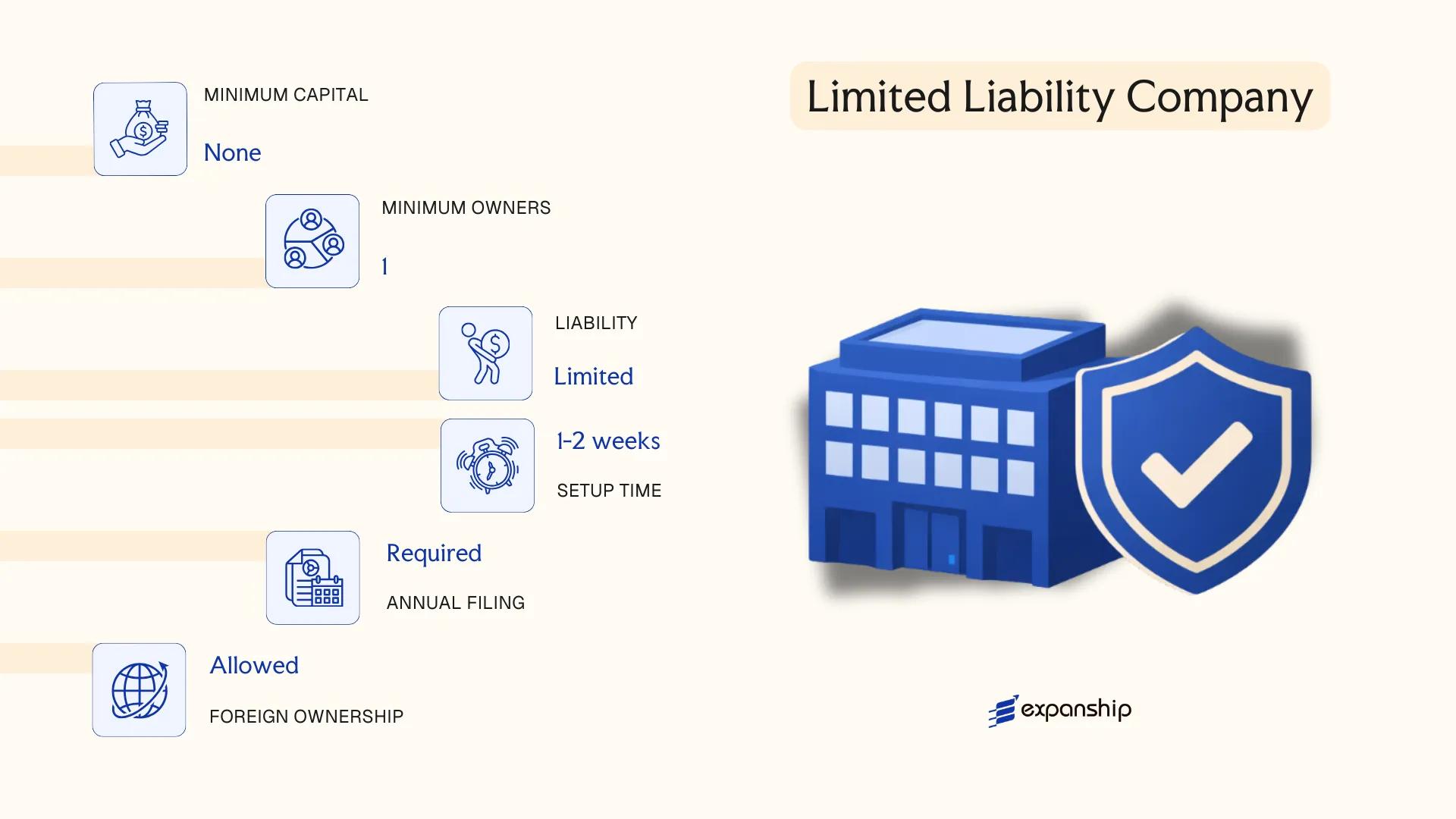

Guam LLC formation requirements are governed by the Guam Limited Liability Company Act, codified under Title 18 of the Guam Code Annotated. The LLC is a hybrid structure that combines corporate-style limited liability with pass-through taxation and partnership-like operational flexibility.

Organized as a separate legal entity, the LLC shields its members from personal liability for the debts and obligations of the business. A Guam LLC operating agreement, while not always statutorily mandated, is strongly advisable as it governs internal management, profit allocation, and member rights.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Separate legal personality; hybrid structure |

| Members | One or more members; no maximum | Single-member LLCs are permitted |

| Management | Member-managed or manager-managed | Defined in the operating agreement |

| Local Presence | Registered agent with a physical Guam address required | Registered office must be maintained on-island |

| Capital | No statutory minimum; USD denomination | Contributions may be cash, property, or services |

| Privacy | Member names filed with the Department of Revenue and Taxation | No public register equivalent to some offshore jurisdictions |

Focus Points

- Taxation: LLCs are treated as pass-through entities by default; members report income on personal returns. Guam imposes a mirror income tax system, and a 4% gross receipts tax (GRT) applies to business revenues. No separate VAT or withholding tax regime applies at the entity level.

- Annual Compliance: Annual reports and fees are due to the Department of Revenue and Taxation; failure to file can result in dissolution.

- Economic Substance: No formal economic substance regime analogous to certain offshore jurisdictions currently applies to Guam LLCs.

- Conversion: Guam law permits conversion from other entity types into an LLC through a formal statutory process.

- Restrictions: Certain licensed professions may be restricted from operating through a standard LLC and may require a professional LLC (PLLC) structure.

Sub-Types

Professional Limited Liability Company (PLLC)

A PLLC is available to licensed professionals — such as attorneys, physicians, and accountants — who are otherwise restricted from sheltering professional malpractice liability through a standard LLC. All members of a PLLC must hold the relevant professional license.

Closing

Forming an LLC in Guam suits trading operations, holding structures, and small-to-mid-sized businesses seeking liability protection without the administrative burden of a full corporate structure. The pass-through tax treatment is a functional advantage, though the requirement to file member information with the Department of Revenue and Taxation limits confidentiality compared to some alternative jurisdictions.

The Guam LLC is best suited for small business owners, professional service providers, and investors seeking a flexible, liability-protected structure within a U.S.-affiliated jurisdiction.

Partnerships [General Partnership, Limited Partnership, Limited Liability Partnership]

Partnerships in Guam are governed by the Guam Uniform Partnership Act and related statutes codified under Title 18 of the Guam Code Annotated. Guam limited liability partnership registration, along with filings for limited and general partnerships, is processed through the Department of Revenue and Taxation (DRT).

A general partnership does not confer limited liability on its partners, meaning personal assets remain exposed to business obligations. Limited partnerships and LLPs address this differently — an LLP shields all partners from personal liability for the firm's debts, while a limited partnership protects only the limited partners, leaving at least one general partner with unlimited exposure.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (contractual entity) | Not a separate legal person in the same sense as a corporation |

| Members | Partners (General / Limited) | GP: min. 2 general partners; LP: min. 1 GP + 1 LP; LLP: min. 2 partners |

| Local Presence | Registered Agent + Principal Office in Guam | Registered agent with a Guam street address is mandatory |

| Capital | USD; no statutory minimum | Contributions defined by partnership agreement |

| Privacy | Partner names disclosed in public filings | No equivalent of a register of beneficial owners for small partnerships |

| Governing Document | Partnership Agreement | Not required to be filed publicly, but strongly recommended in writing |

Focus Points

- Taxation: Partnerships are pass-through entities for Guam tax purposes; income is reported on each partner's individual Guam income tax return, with no entity-level income tax, though Guam's gross receipts tax (currently 4%) may apply to business revenues.

- Annual Compliance: Annual reports and applicable fees are due to the DRT; failure to file can result in administrative dissolution.

- Conversion: A general partnership may convert to an LLP by filing a statement of qualification with the DRT, without necessarily dissolving the underlying business.

- Restrictions: Foreign nationals may face additional considerations under federal law given Guam's status as a U.S. territory.

Sub-Types

General Partnership

All partners share management authority and bear unlimited joint and several liability. No formation filing is strictly required, though the business name may need registration with the DRT.

Limited Partnership (LP)

Limited partners contribute capital and receive liability protection proportional to their investment, while at least one general partner retains full management control and unlimited liability. This structure suits investment vehicles and project-specific ventures.

Limited Liability Partnership (LLP)

An LLP requires a formal statement of qualification filed with the DRT. Unlike an LP, every partner in an LLP receives liability protection from the firm's obligations, making it a common choice for professional service firms.

Closing

Partnerships suit joint ventures, professional practices, and real estate arrangements where pass-through taxation is preferred, though the exposure of general partners to unlimited liability remains a material structural drawback for high-risk operations.

Partnerships are best suited for professional service providers or two-party joint ventures seeking pass-through tax treatment with a defined, contractual governance structure.

Foreign Business Entities [Foreign Corporation, Foreign LLC, Foreign Partnership]

Foreign business entities operating in Guam are governed by Title 18 of the Guam Code Annotated, which requires any out-of-jurisdiction corporation, LLC, or partnership conducting business on the island to register with the Department of Revenue and Taxation (DRT). Foreign business entity registration in Guam is not optional — transacting business without qualification exposes the entity to civil penalties and bars it from maintaining legal proceedings in Guam courts.

Registration does not create a new domestic entity. The foreign firm retains its original legal structure, liability characteristics, and governing law from its home jurisdiction while gaining the legal authority to operate locally.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Foreign entity registered to do business | Retains home-jurisdiction legal structure |

| Members / Officers | Varies by entity type (directors, members, partners) | Home-jurisdiction designations are preserved |

| Local Presence | Registered Agent with a physical Guam address required | Agent must be continuously maintained |

| Capital | No separate minimum capital requirement for registration | Home-jurisdiction capital rules apply |

| Filing | Certificate of Authority (corporations); Application for Registration (LLCs, partnerships) | Filed with the DRT |

| Privacy | Officer/member details disclosed in registration filings | Public record with DRT |

Focus Points

- Taxation: Foreign entities are subject to Guam's territorial income tax on Guam-sourced income; no separate VAT applies, but gross receipts tax may apply depending on business activity.

- Annual Compliance: Registered foreign entities must file annual reports with the DRT and maintain a continuously appointed registered agent.

- Penalties for Non-Compliance: Operating without a valid Certificate of Authority can result in monetary fines and loss of standing to sue in Guam courts.

- Conversion: A foreign entity cannot convert directly to a domestic Guam entity without dissolving the foreign registration and forming a new domestic entity separately.

Sub-Types

Foreign Corporation

A foreign corporation seeking foreign corporation Guam qualification must file a Certificate of Authority with the DRT, submit a certified copy of its articles of incorporation, and designate a local registered agent. S corporation elections made in the home jurisdiction are generally not recognized under Guam's separate tax framework.

Foreign LLC

Foreign LLC Guam registration follows a similar process, requiring an Application for Registration, a certificate of good standing from the home jurisdiction, and appointment of a registered agent. The LLC's operating agreement and member structure remain governed by its formation jurisdiction.

Foreign Partnership

Both general and limited partnerships must register if conducting business in Guam, filing applicable registration documents and designating a local agent. Limited liability partnerships registered elsewhere must similarly qualify before transacting business locally.

Closing

Registering a foreign company in Guam is most commonly used by U.S. mainland businesses expanding operations to the Pacific or by firms seeking to serve Guam's federal contracting market. The process is relatively straightforward for entities already in good standing at home, though the requirement to maintain a permanent registered agent represents an ongoing administrative obligation.

U.S. mainland corporations and LLCs with existing operations that need a formal presence in Guam to enter government contracts or serve local commercial markets.

Sole Proprietorship

A sole proprietorship is the simplest business structure available under Guam law. Sole proprietorship Guam registration does not create a separate legal entity — the owner and the business are one and the same for all legal and financial purposes. This means personal assets are exposed to business liabilities without limitation.

Under Guam's business registration framework administered by the Department of Revenue and Taxation (DRT), sole proprietors operating under a name other than their own legal name must file a "Doing Business As" (DBA) trade name registration. No articles of incorporation or organization are required.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality |

| Owner Title | Sole Proprietor | Single individual only; no co-owners |

| Membership | 1 (natural person) | Cannot have multiple owners |

| Local Presence | Business License (DRT); DBA filing if trading under a trade name | Business License issued by DRT |

| Capital | No minimum; USD | No statutory capital requirement |

| Privacy | Owner name publicly linked to DBA filing | Limited privacy protection |

Focus Points

- Taxation: Subject to Guam's mirrored federal income tax system under the Guam Territorial Income Tax; no separate corporate tax; self-employment income reported on individual returns; no VAT, though a 4% Gross Receipts Tax (GRT) applies to business revenue.

- Annual Compliance: Business license renewal required annually with the DRT; no separate annual report filing obligation.

- Conversion: Can be converted into an LLC or corporation by forming the new entity and transferring assets; no statutory conversion mechanism exists for this structure.

- Treaty Access: No access to tax treaty benefits; the owner files under individual status.

- Restrictions: Not suitable for raising external investment or issuing equity.

Closing

Starting a sole proprietorship in Guam suits service-based or low-revenue operations where administrative simplicity outweighs the need for liability protection. The primary limitation is unlimited personal liability — there is no structural separation between personal and business obligations.

This structure fits individual freelancers, consultants, or micro-businesses testing a local market before committing to a formal entity.

How to Choose the Right Entity Type in Guam

Selecting how to choose a business entity in Guam is not a procedural formality — the structure you register has direct legal, tax, and operational consequences that can be difficult to reverse.

Why Your Entity Choice Matters

- Registering a foreign entity when your business will actively transact with Guam residents places you in breach of the Guam Business Corporation Act, potentially resulting in administrative penalties or loss of standing to sue in local courts.

- Choosing an entity structured for tax exemption when you require access to U.S. federal tax treaty positions may disqualify your business from applicable withholding reductions.

- Forming a corporation when a single-member LLC would suffice imposes board governance requirements, mandatory annual meetings, and shareholder record obligations that generate unnecessary compliance costs for a one-person operation.

- Selecting a general partnership without limited liability protection exposes each partner to personal liability for the debts and obligations of the firm, which is an avoidable risk in most trading scenarios.

Key Factors to Consider

- Business Activity: Whether your firm will hold assets, trade actively, or operate in a regulated sector directly determines which structures are legally permissible.

- Local vs. Offshore Operations: Businesses transacting with Guam residents must register as a domestic or qualified foreign entity under Title 18 of the Guam Code Annotated.

- Ownership and Management: Single-owner operations benefit from LLC flexibility, while multi-investor structures may require the governance framework of a corporation.

- Tax Objectives: Your eligibility for Guam's 90% income tax rebate under the Qualifying Certificate program varies by entity type and activity.

- Liability Exposure: The degree of personal liability you can accept influences whether a sole proprietorship, partnership, or limited liability structure is appropriate.

- Exit Strategy: Not all Guam entities permit redomiciliation or conversion; confirm whether your chosen structure allows for these mechanisms before formation.

Compliance Services for Companies in Guam

Maintain your Guam entity in good standing with registered agent support, annual report filings, and ongoing regulatory compliance.

Conclusion

Guam business incorporation summary points to a jurisdiction governed by Title 18 of the Guam Code Annotated, where entity selection carries direct consequences for liability exposure, tax treatment, and operational structure. The LLC remains the most widely registered entity type, favored for its combination of limited liability and pass-through taxation under Guam's income tax mirroring system. Corporations suit businesses planning external investment or structured equity arrangements, while partnerships serve closely held ventures where profit-sharing flexibility takes priority. Sole proprietorships carry no liability separation, making them appropriate only for low-risk, single-operator activities.

Registered foreign entities operate under a parallel framework requiring qualification through the Department of Revenue and Taxation before conducting business locally. Guam's existing tax treaties and its status as a U.S. territory continue to shape its appeal for businesses seeking a regulated Pacific jurisdiction. Engaging qualified legal and tax counsel familiar with Guam's mirrored federal framework remains a practical starting point before any registration decision is made.

How Expanship Can Assist You

Expanship's Guam company formation services cover the full process of registering and maintaining a business entity under the jurisdiction's specific legal framework. From selecting between a domestic LLC, a C corporation, or a limited partnership, to filing with the Guam Department of Revenue and Taxation and the Department of Revenue and Taxation's business license division, each step is managed with attention to local requirements.

Expanship handles the full scope of corporate services in Guam:

- Preparation and legalization of formation documents

- Registered agent and registered office provision in Guam

- Government filings and liaison with relevant Guam authorities

- Post-incorporation compliance, including annual report obligations

- Banking introduction assistance for newly formed entities

Reach out to Expanship Guam to discuss your specific business setup requirements.

Frequently Asked Questions (FAQ)

The LLC is the most frequently formed entity on the island. Its combination of pass-through taxation and statutory liability protection makes it practical for both resident entrepreneurs and foreign investors operating in the U.S. territory.

A corporation is subject to federal corporate income tax at the entity level, while an LLC's income flows directly to members' personal returns. Corporations carry heavier ongoing compliance requirements, including board meetings and formal resolutions, whereas LLCs operate under a more flexible management structure.

Among registered entities, the LLC generally discloses the least. Member names are not required on the public Articles of Organization, and nominee arrangements are permissible under applicable statutes.

A sole proprietorship and a single-member LLC can each be formed by one individual. Partnerships, by definition, require a minimum of two partners, so a general partnership, limited partnership, or LLP cannot be established by one person alone.

Corporations, LLCs, and registered foreign entities are all available to non-U.S. residents. Foreign nationals must designate a registered agent with a physical address in the territory and comply with any applicable federal ownership regulations.

GUBOC permits statutory conversion between entity types, including from an LLC to a corporation or vice versa. The process requires filing a plan of conversion with the Department of Revenue and Taxation and meeting applicable notice requirements.

Corporations and LLCs are legally distinct from their owners. General partnerships do not carry separate legal personality under Guam law, meaning partners bear direct personal liability for the firm's obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.