Key Takeaways

- The Anpartsselskab (ApS) is the most commonly registered business structure in Greenland, favoured for its lower capital threshold and simpler governance requirements compared to the Aktieselskab (A/S).

- Company registration in Greenland is administered by the Danish Business Authority (Erhvervsstyrelsen) through the central business register at virk.dk, despite Greenland's autonomous status under the 2009 Act on Greenland Self-Government.

- Foreign firms can establish a presence in Greenland without incorporating a separate legal entity by operating through either a branch office or a representative office.

- Greenland maintains its own territorial tax administration, separate from Denmark, which applies to residents and businesses with a local presence in the territory.

Introduction to Entity Types in Greenland

Greenland is a self-governing territory within the Kingdom of Denmark, situated between the Arctic and Atlantic Oceans, northeast of Canada and northwest of Iceland. Despite its autonomous status under the 2009 Act on Greenland Self-Government, the territory maintains close constitutional ties with Denmark, which continues to oversee certain areas of foreign policy and defence. Business entity types in Greenland are registered through the Danish Business Authority (Erhvervsstyrelsen), which administers the central business register and governs company formation across the territory.

Greenland operates its own tax administration separately from Denmark, with a territorial income tax system that applies to residents and businesses with a local presence.

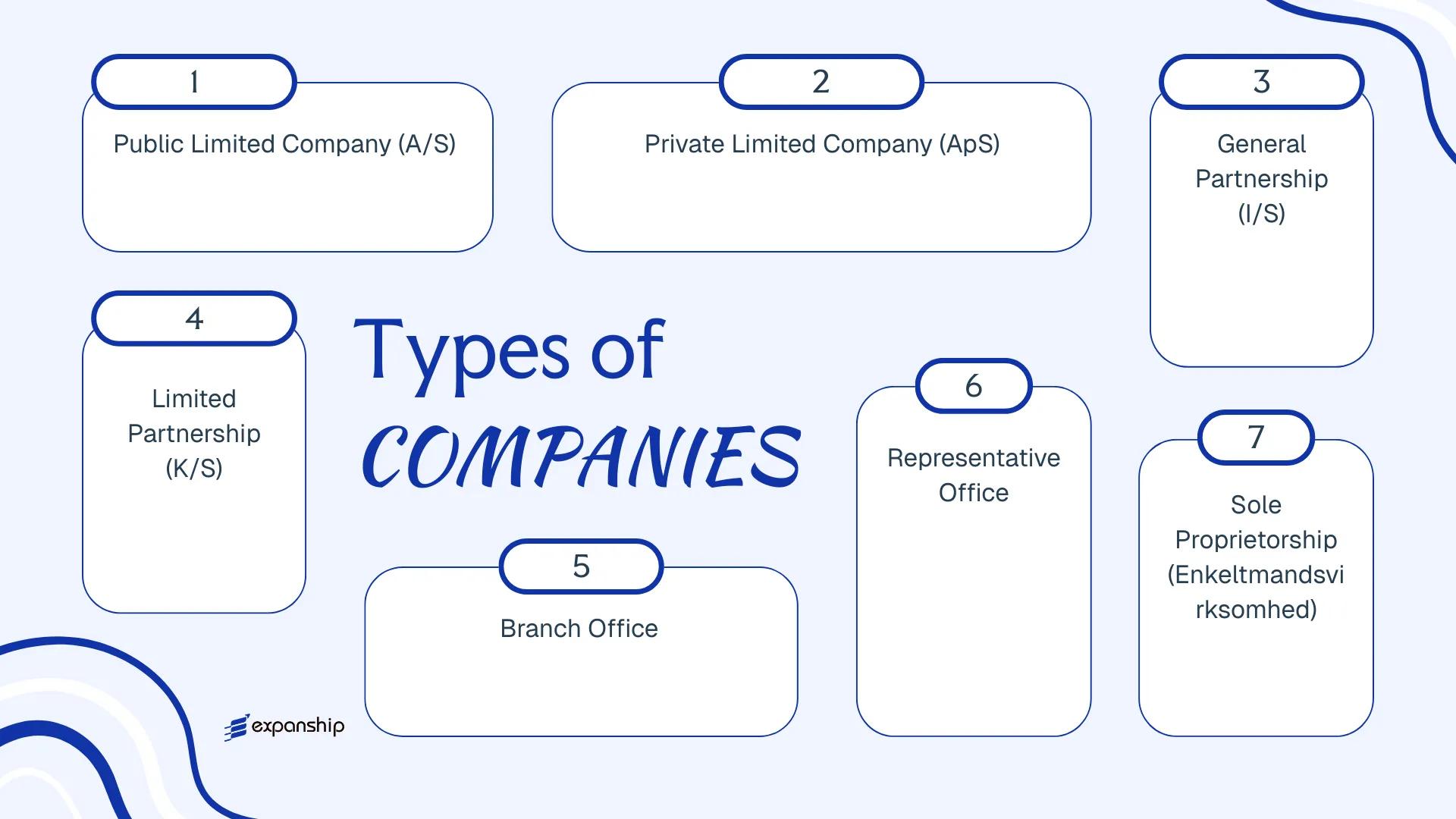

The principal business structures available include the Aktieselskab (A/S), Anpartsselskab (ApS), Interessentskab (I/S), Kommanditselskab (K/S), Enkeltmandsvirksomhed, branch office, and representative office. Each carries distinct liability, capital, and governance implications. This article examines each structure in detail to help you assess which formation best suits your commercial objectives in the territory.

An Overview of Business Structures in Greenland

Greenland's company law framework provides several distinct legal forms for conducting business, each governed primarily by the Selskabsloven (the Danish Companies Act) as applied through Greenlandic legislation. The territory's regulatory authority for company registration is the Danish Business Authority (Erhvervsstyrelsen), which oversees filings for entities operating under its jurisdiction. Each legal form carries different implications for liability, taxation, and operational scope.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Aktieselskab (A/S) | Public Limited Company | Limited | Taxed | Yes | 1 shareholder | Erhvervsstyrelsen | Selskabsloven |

| Anpartsselskab (ApS) | Private Limited Company | Limited | Taxed | Yes | 1 shareholder | Erhvervsstyrelsen | Selskabsloven |

| Interessentskab (I/S) | General Partnership | Unlimited | Taxed at partner level | Yes | 2 partners | Erhvervsstyrelsen | Partnership rules |

| Kommanditselskab (K/S) | Limited Partnership | Mixed | Taxed at partner level | Yes | 1 general, 1 limited | Erhvervsstyrelsen | Partnership rules |

| Branch Office | Foreign Branch | Parent liability | Taxed on local income | Yes | N/A | Erhvervsstyrelsen | Selskabsloven |

| Representative Office | Non-trading presence | Parent liability | Generally exempt | No | N/A | Erhvervsstyrelsen | General regulations |

| Enkeltmandsvirksomhed | Sole Proprietorship | Unlimited | Personal income tax | Yes | 1 individual | Erhvervsstyrelsen | Business registration rules |

Each of these structures is examined in full in the sections below.

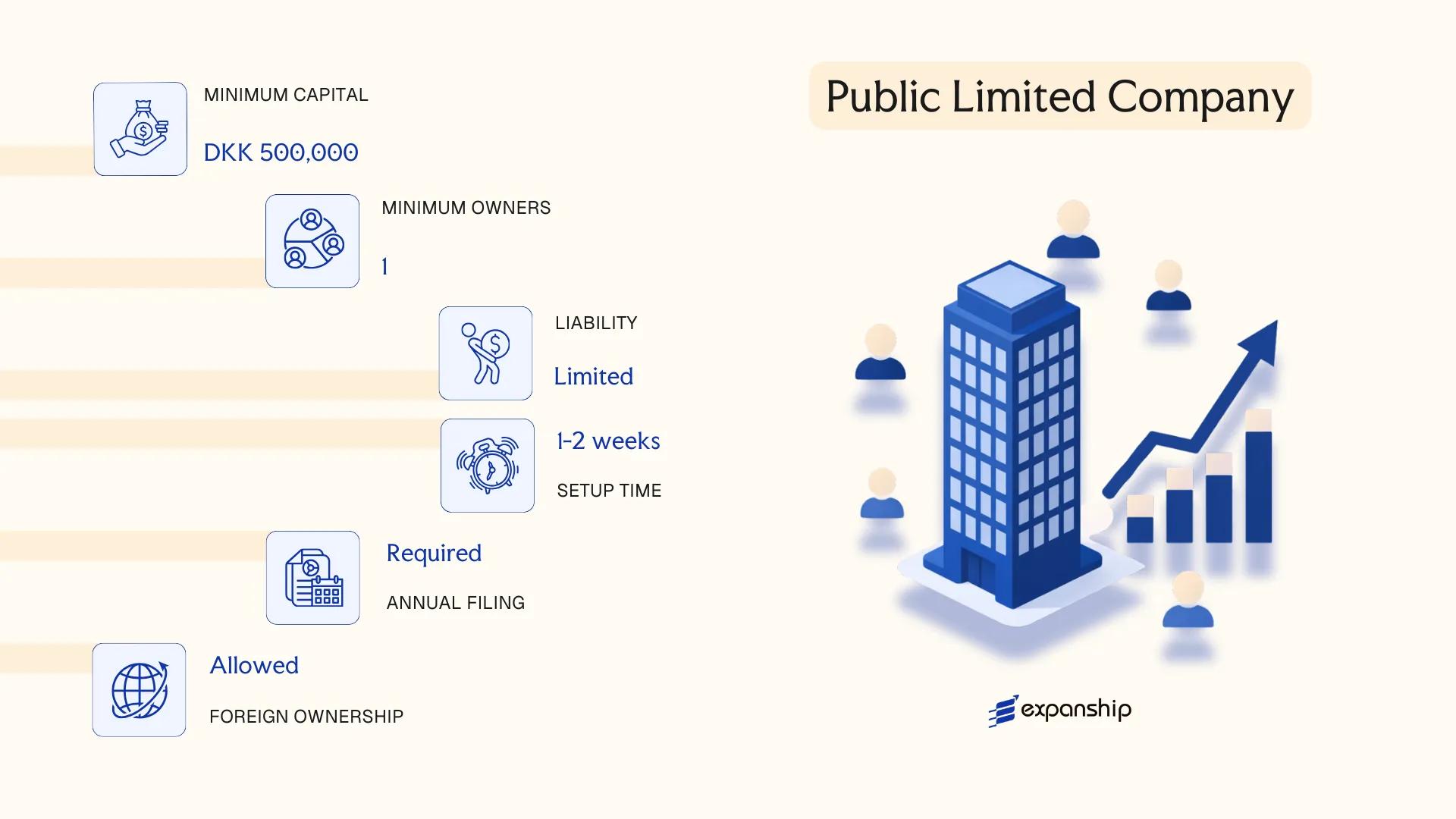

Aktieselskab (A/S) — Public Limited Company

Governed by the Selskabsloven (Companies Act), which Greenland applies through its administrative relationship with Denmark, the Aktieselskab A/S Greenland structure carries full separate legal personality. Shareholders bear no personal liability beyond their capital contribution.

Shares in an A/S can be offered to the public, distinguishing it structurally from its private counterpart. This makes the form suitable for larger enterprises, institutional investors, or businesses anticipating external capital raises.

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company | Separate legal personality; limited liability |

| Members | Shareholders (min. 1); Board of Directors (min. 3 members) | Supervisory board required for larger entities |

| Local Presence | Registered address in Greenland required | No statutory requirement for a local resident director under general rules |

| Capital | DKK 400,000 minimum share capital | Must be fully subscribed at formation |

| Share Transferability | Shares freely transferable unless articles restrict | Public offering permissible |

| Privacy | Shareholder register filed; directors publicly recorded | Limited confidentiality |

Focus Points

- Taxation: Corporate income tax applies at the standard Greenlandic rate; VAT obligations apply to taxable supplies; withholding tax may apply to dividends distributed to non-residents.

- Annual Compliance: Audited financial statements and annual return filing are mandatory.

- Economic Substance: No specific substance regime, but genuine business activity is expected for tax residency purposes.

- Treaty Access: Greenland maintains limited double taxation arrangements; treaty benefits are not automatically equivalent to Danish coverage.

- Conversion: An A/S may be converted to an ApS subject to satisfying the target entity's requirements.

Closing

The A/S suits capital-intensive operations, holding structures, and businesses seeking investor participation through tradeable shares. The mandatory DKK 400,000 minimum capital and three-member board requirement represent meaningful entry thresholds that smaller ventures may find disproportionate.

Best suited for large trading companies, institutional joint ventures, or businesses planning public capital raises in or through Greenland.

Company Incorporation in Greenland

Incorporate an Aktieselskab or other entity type in Greenland with end-to-end support from Expanship.

Anpartsselskab (ApS) — Private Limited Company

The Anpartsselskab ApS Greenland private company structure is governed by Greenlandic corporate legislation derived from Danish law, as Greenland operates within the Danish Realm and applies adapted versions of Danish statutes. The ApS carries separate legal personality, meaning its liabilities are distinct from those of its owners, and member liability is capped at the amount contributed to the share capital.

Structurally, this entity sits between a sole proprietorship and a publicly traded company, making it a common choice for closely held businesses and subsidiaries of foreign groups operating in Greenland.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company | Separate legal personality; not publicly tradeable |

| Members | Shareholders: 1 minimum, no statutory maximum | Single-shareholder structure permitted |

| Management | Board of Directors optional; at least 1 manager required | Manager need not be a shareholder |

| Local Presence | Registered address in Greenland required | Registered agent not mandated but a local address is obligatory |

| Share Capital | DKK 40,000 minimum | Must be fully paid up at registration |

| Privacy | Shareholder register filed with authorities | Beneficial ownership disclosure required |

Focus Points

- Taxation: Subject to Greenlandic corporate income tax; VAT obligations apply to taxable supplies; withholding tax may apply to dividends paid to non-residents under applicable rules.

- Annual Compliance: Annual accounts must be prepared and submitted; audit requirements depend on company size thresholds.

- Economic Substance: No formal substance regime equivalent to offshore jurisdictions, but genuine local activity is expected for tax residency purposes.

- Conversion: An ApS may be converted to an A/S provided capital and procedural requirements of the relevant legislation are satisfied.

- Restrictions: Shares in an ApS cannot be offered to the general public; transfer of shares may be subject to pre-emption rights set out in the articles of association.

Closing

Greenland private limited company formation via the ApS structure suits trading operations, subsidiaries, and holding arrangements where share transferability to the public is not required. The capped liability is a functional advantage; however, the DKK 40,000 minimum capital requirement and mandatory registered address add upfront cost relative to simpler structures.

The ApS is best suited for foreign investors and SMEs seeking a structured, liability-limited presence in Greenland without the compliance burden associated with a publicly listed entity.

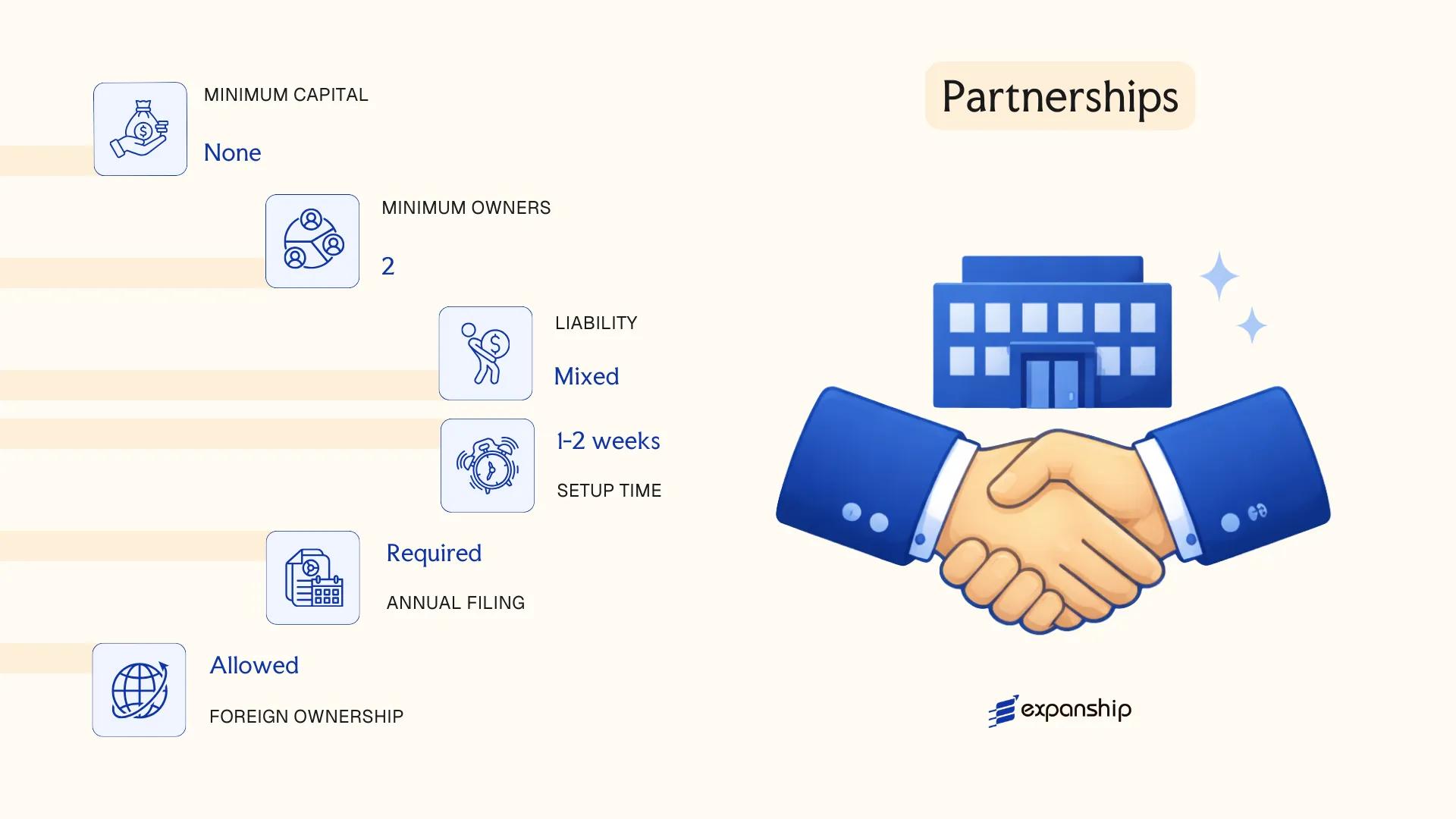

Partnerships [Interessentskab (I/S), Kommanditselskab (K/S)]

Greenland's partnership structures — the Interessentskab (I/S) and the Kommanditselskab (K/S) — are governed primarily by Danish commercial law principles, which Greenland has adopted through its Home Rule and subsequent Self-Rule arrangements. Neither the I/S nor the K/S carries separate legal personality in the conventional corporate sense, meaning partners remain personally exposed to the entity's obligations to varying degrees.

Registration for both forms is handled through the Danish Business Authority (Erhvervsstyrelsen), which maintains jurisdiction over Greenlandic commercial registrations. The I/S requires all partners to bear unlimited, joint and several liability, while the K/S introduces a hybrid liability model — at least one general partner holds unlimited liability, and limited partners are liable only up to their contributed capital.

Key Characteristics

| Requirement | I/S (Interessentskab) | K/S (Kommanditselskab) |

|---|---|---|

| Legal Form | General partnership; no separate legal personality | Limited partnership; no separate legal personality |

| Members | Partners (minimum 2, no statutory maximum) | At least 1 general partner + at least 1 limited partner |

| Liability | All partners: unlimited and joint | General partner: unlimited; limited partners: capped at contribution |

| Local Presence | Registered address in Greenland required | Registered address in Greenland required |

| Capital | No statutory minimum; contributions defined by partnership agreement | No statutory minimum; limited partner's liability tied to committed capital |

| Privacy | Partner details filed with Erhvervsstyrelsen; publicly accessible | Same public disclosure obligations apply |

Focus Points

- Taxation: Partnerships are fiscally transparent — profits are allocated to and taxed at the partner level under Greenlandic income tax rules; no separate corporate tax applies to the entity itself, and VAT registration obligations depend on turnover thresholds.

- Annual Compliance: Both forms must maintain updated registrations with Erhvervsstyrelsen; annual accounts may be required depending on size and activity.

- Treaty Access: Because partnerships lack separate legal personality, access to double tax treaty benefits is determined at the partner level, not the entity level.

- Restrictions: A general partner in a K/S cannot simultaneously limit their own liability; appointing a corporate general partner is a common structural workaround.

- Conversion: Conversion to a capital company such as an ApS is possible but requires formal restructuring and re-registration.

Sub-Types

Interessentskab (I/S)

The I/S is a general partnership where every partner carries equal, unlimited liability unless the partnership agreement stipulates otherwise. It is commonly used by professional firms and small joint ventures where partners have mutual trust and shared operational involvement.

Kommanditselskab (K/S)

The K/S separates management authority and liability exposure between its general and limited partners. This structure is frequently used in investment funds, real estate holding arrangements, and project finance vehicles where passive investors require defined liability caps.

Closing

Both structures suit joint ventures, professional practices, and investment arrangements where pass-through taxation is preferred over corporate-level tax. The primary advantage is fiscal transparency; the principal drawback is the unlimited personal liability carried by at least one partner in every case.

These structures are best suited for two or more parties seeking pass-through tax treatment and are prepared to accept — or contractually manage — the liability exposure that comes with partnership form.

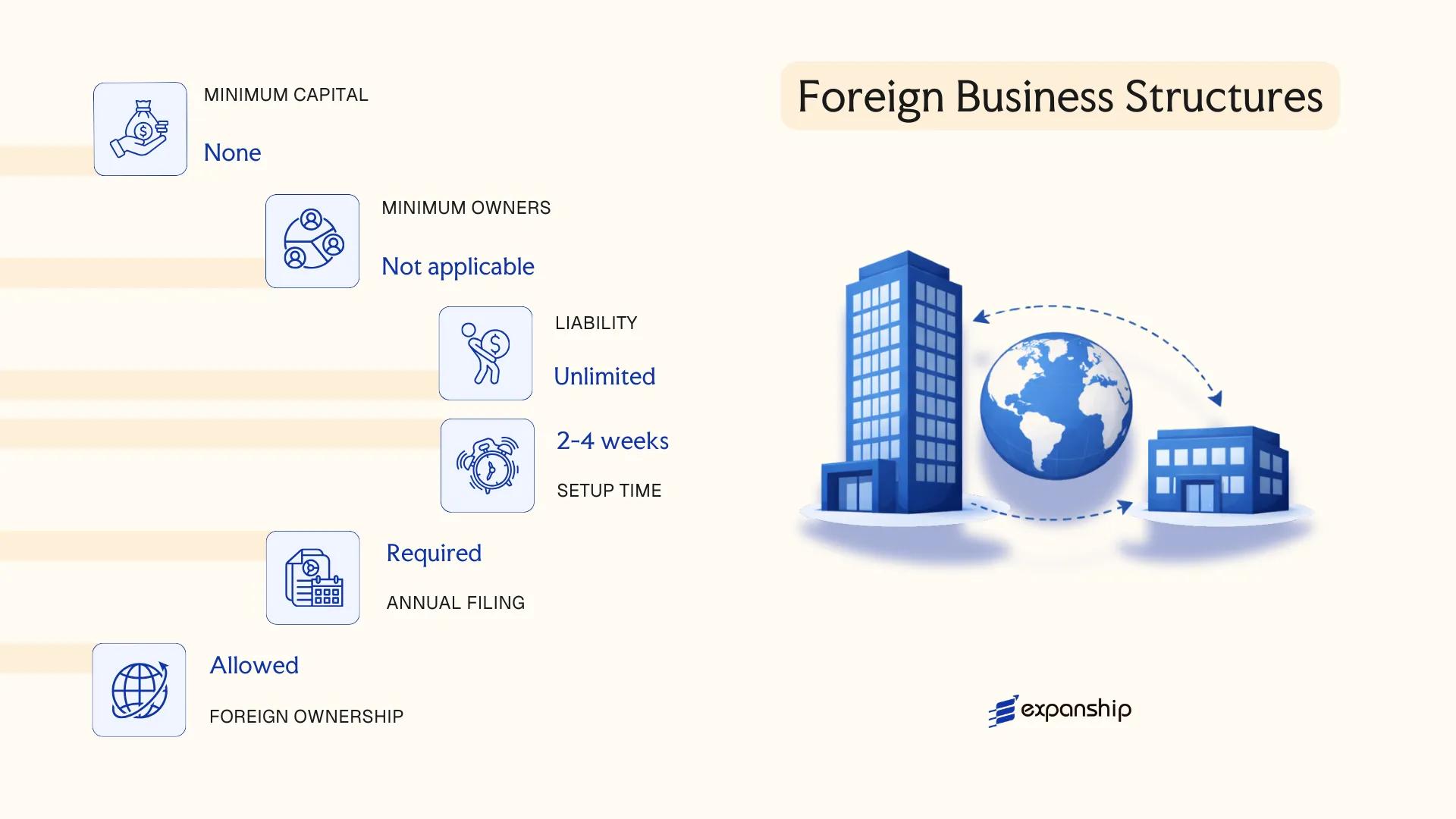

Foreign Business Structures [Branch Office, Representative Office]

Foreign companies seeking a presence in Greenland without forming a separate local entity typically do so through a branch office or a representative office. A foreign branch office setup in Greenland is governed by Danish corporate law as extended to Greenland, primarily the Danish Companies Act (Selskabsloven), since Greenland has not enacted independent company legislation in this domain. A branch is not a legally separate entity from its parent — the foreign firm bears full liability for the branch's obligations.

Registration is handled through the Danish Business Authority (Erhvervsstyrelsen), which maintains jurisdiction over business registrations applicable to Greenland. The branch must be registered before commencing operations, and registration requires submission of the parent company's constitutional documents, a designated local representative, and a registered address.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent | None — extension of parent |

| Liability | Parent bears full liability | Parent bears full liability |

| Commercial Activity | Permitted | Not permitted — liaison only |

| Local Representative | Mandatory | Mandatory |

| Registered Address | Required in Greenland | Required |

| Registration Body | Danish Business Authority | Danish Business Authority |

Focus Points

- Taxation: Branch profits are subject to Greenlandic corporate income tax; withholding tax may apply to profit remittances depending on treaty status, and VAT obligations arise if commercial activity thresholds are met.

- Treaty Access: Access to Denmark's tax treaty network is not automatic for Greenland; separate treaty coverage must be confirmed for the specific jurisdiction.

- Annual Compliance: Annual accounts of the parent must generally be filed, along with any local financial reporting obligations applicable to the branch.

- Restrictions: A representative office cannot generate revenue, enter contracts commercially, or invoice clients — its role is limited to market research and liaison activities.

- Conversion: Converting a branch to a fully incorporated local entity requires a separate incorporation process; there is no statutory conversion mechanism.

Closing

A branch office suits foreign firms testing commercial viability in the territory or executing specific projects, while a representative office is appropriate for market research or pre-sales functions. The principal advantage of a branch is operational speed without a separate capitalisation requirement; the principal limitation is unlimited parental liability exposure.

Best suited for established foreign companies with defined revenue-generating operations or preliminary market assessment needs, where full local incorporation is premature.

Enkeltmandsvirksomhed — Sole Proprietorship

An Enkeltmandsvirksomhed sole proprietorship in Greenland is the simplest form of business registration available to individuals. It carries no separate legal personality — the proprietor and the business are treated as one and the same under the law, meaning personal assets are fully exposed to business liabilities.

Registration is handled through the Greenlandic business register, Sullissivik, which administers commercial registrations under the authority of the Naalakkersuisut (Government of Greenland). No minimum capital is required to establish the entity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Enkeltmandsvirksomhed) | No separate legal personality from the owner |

| Members | One proprietor | Single individual only; no co-owners permitted under this structure |

| Liability | Unlimited personal liability | Personal assets are fully exposed to business debts |

| Local Presence | Registered address in Greenland required | Proprietor must be resident or have a local contact address |

| Capital | No minimum capital requirement | No paid-in capital obligations |

| Privacy | Name and registration details publicly recorded | Beneficial ownership disclosure applies |

Focus Points

- Taxation: Business income is taxed as personal income under Greenlandic income tax rules; no separate corporate tax applies, and VAT registration is required once turnover exceeds the applicable threshold.

- Annual Compliance: Annual tax filing is required; accounting records must be maintained but full statutory audit requirements do not generally apply at this level.

- Conversion: The structure can be converted into a capital company (ApS or A/S) as the business grows, though the process involves formal legal steps and asset transfer.

- Treaty Access: As a self-employed business in Greenland operating under personal income rules, access to double tax treaty benefits is limited compared to corporate structures.

- Restrictions: Non-resident individuals face practical barriers to registration, as local presence and residency are generally expected.

A sole proprietorship suits local self-employed professionals, sole traders, and small individual businesses with limited liability exposure. The absence of capital requirements and administrative simplicity make it straightforward to establish, but unlimited personal liability is a significant structural constraint that makes it unsuitable for ventures carrying financial or legal risk.

Best suited for resident individuals operating a small, low-risk self-employed business in Greenland who do not require structural separation between personal and business assets.

How to Choose the Right Entity Type in Greenland

Choosing the right company structure in Greenland affects your legal standing, tax position, and administrative obligations from the moment of registration.

Why Your Entity Choice Matters

The structure you register determines concrete legal and financial outcomes — not just theoretical risks.

- Registering a branch or representative office when you intend to conduct independent local trade places you in breach of the applicable provisions under Greenlandic company law, which can result in deregistration or administrative penalties.

- Selecting an entity without the capacity to maintain genuine economic substance, where substance rules apply, can trigger reporting failures and associated fines under Danish-derived tax administration rules applied in Greenland.

- Forming an Anpartsselskab (ApS) when a partnership structure would suit a small professional practice locks you into annual filing obligations and capital maintenance requirements that general partnerships do not carry.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as financial services each point toward a different legal form under Greenlandic business regulation.

- Ownership Structure: Single-owner operations may be served by a sole proprietorship or ApS, while multi-party arrangements with differing liability needs point toward a K/S or A/S.

- Tax Objectives: Your need for treaty access, full exemption, or a specific tax regime determines which entity qualifies.

- Substance Capacity: If you cannot maintain a physical presence, your chosen structure must reflect that operational reality.

- Exit Strategy: Not all entity types in Greenland permit redomiciliation or straightforward conversion, so your long-term plans should inform the initial choice.

The primary legislation governing company formation is the Greenlandic Companies Act (Selskabsloven as applied in Greenland), which should be reviewed alongside any sector-specific licensing requirements before registration.

Corporate Compliance Services in Greenland

Ongoing compliance support for companies registered in Greenland, including annual filing, reporting obligations, and regulatory maintenance.

Conclusion

Greenland company incorporation involves a defined set of entity types, each suited to specific operational and ownership profiles. The Anpartsselskab (ApS) is the most commonly registered structure, favoured by small to mid-sized businesses due to its lower capital threshold and simpler governance. The Aktieselskab (A/S) suits larger enterprises requiring access to external capital or multiple shareholder classes. Partnerships under the Interessentskab and Kommanditselskab frameworks serve those prioritising pass-through treatment over liability separation. Branch offices and representative offices allow foreign firms to establish a presence without forming a separate legal entity. The Enkeltmandsvirksomhed remains the most accessible structure for individual operators, though it carries unlimited personal liability.

Greenland's corporate framework continues to develop within the broader Danish legal tradition, with the Erhvervsstyrelsen maintaining oversight of registration and compliance. Expanship's team works directly with these structures across all formation stages.

How Expanship Can Assist You

Expanship company formation services Greenland cover the full process of registering an entity with the Danish Business Authority (Erhvervsstyrelsen), which oversees business registration in Greenland. From selecting between an Anpartsselskab and an Aktieselskab to satisfying the capital requirements and filing obligations specific to each structure, your formation is handled with direct knowledge of local requirements.

Expanship supports your business across every stage of establishment and ongoing compliance:

- Document preparation and notarization

- Registered address and local agent provision

- Filing with Erhvervsstyrelsen and government liaison

- Post-incorporation compliance management

- Corporate tax registration and regulatory filings

- Banking introduction assistance

Ready to incorporate in Greenland? Contact Expanship Greenland to discuss your specific structure and requirements.

Frequently Asked Questions (FAQ)

The Anpartsselskab (ApS) is the most frequently registered entity. Its lower minimum capital requirement and simpler governance structure make it the practical default for small to mid-sized businesses.

An A/S is subject to stricter disclosure requirements and higher minimum share capital, while an ApS imposes fewer formalities on shareholder meetings and reporting. Both entity types are treated as resident taxpayers under Greenlandic income tax rules, but the A/S is the appropriate vehicle when public share issuance or institutional investment is involved.

Among registered structures, the Interessentskab (I/S) involves relatively limited public filing requirements compared to capital companies. Beneficial ownership disclosure obligations, however, apply broadly across entity types, and nominee arrangements do not eliminate those reporting duties.

No. A sole proprietorship (Enkeltmandsvirksomhed) requires only one individual. An ApS can be formed by a single shareholder, and an A/S similarly permits sole ownership. Partnerships, whether an I/S or Kommanditselskab (K/S), require a minimum of two partners by their legal definition.

Foreign nationals can register an ApS, A/S, or a branch office (filial) without a residency requirement applying at the entity level, though directors may need to meet specific conditions. A branch office under a foreign parent company is also a common entry point, as it avoids creating a separate legal entity while permitting commercial operations.

Conversion from an ApS to an A/S is generally permissible, subject to meeting the capital and governance thresholds of the target form. Restructuring in the opposite direction follows a similar principle, though the process requires updated registration with the Greenlandic Business Authority and revised constitutional documents.

No. An Enkeltmandsvirksomhed has no legal personality distinct from its owner, meaning personal assets remain exposed to business liabilities. An I/S similarly does not separate partners from the firm's obligations, while an ApS, A/S, and K/S (for limited partners) do provide that separation.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.