Key Takeaways

- The SAS (Société par Actions Simplifiée) dominates new company registrations in France due to its flexible governance structure and absence of a minimum share capital requirement.

- Company registration in France is processed through the Guichet des formalités des entreprises, the centralized online portal introduced in 2023 that replaced the former network of Centres de Formalités des Entreprises (CFE), with filings flowing through to the Registre du Commerce et des Sociétés (RCS).

- Partners in a Société en Nom Collectif (SNC) bear unlimited joint liability, making this structure appropriate only where all partners are prepared to accept full personal exposure to business debts.

- France offers no offshore tax concessions under its standard corporate tax regime, though its extensive network of double tax treaties can moderate cross-border withholding obligations for international structures.

Introduction to Entity Types in France

France is a sovereign republic in Western Europe, bordered by Belgium, Luxembourg, Germany, Switzerland, Italy, Spain, and Andorra, with coastlines on both the Atlantic and the Mediterranean. Selecting among the available types of business entities in France requires an understanding of how each legal form interacts with French commercial law, tax obligations, and governance requirements.

Company registration is administered through the Guichet des formalités des entreprises, the centralized online portal that replaced the former network of Centres de Formalités des Entreprises (CFE) in 2023. Filings flow through to the Registre du Commerce et des Sociétés (RCS), maintained by the commercial courts (tribunaux de commerce). France operates a standard corporate tax regime with no offshore concessions, though an extensive network of double tax treaties moderates cross-border withholding obligations.

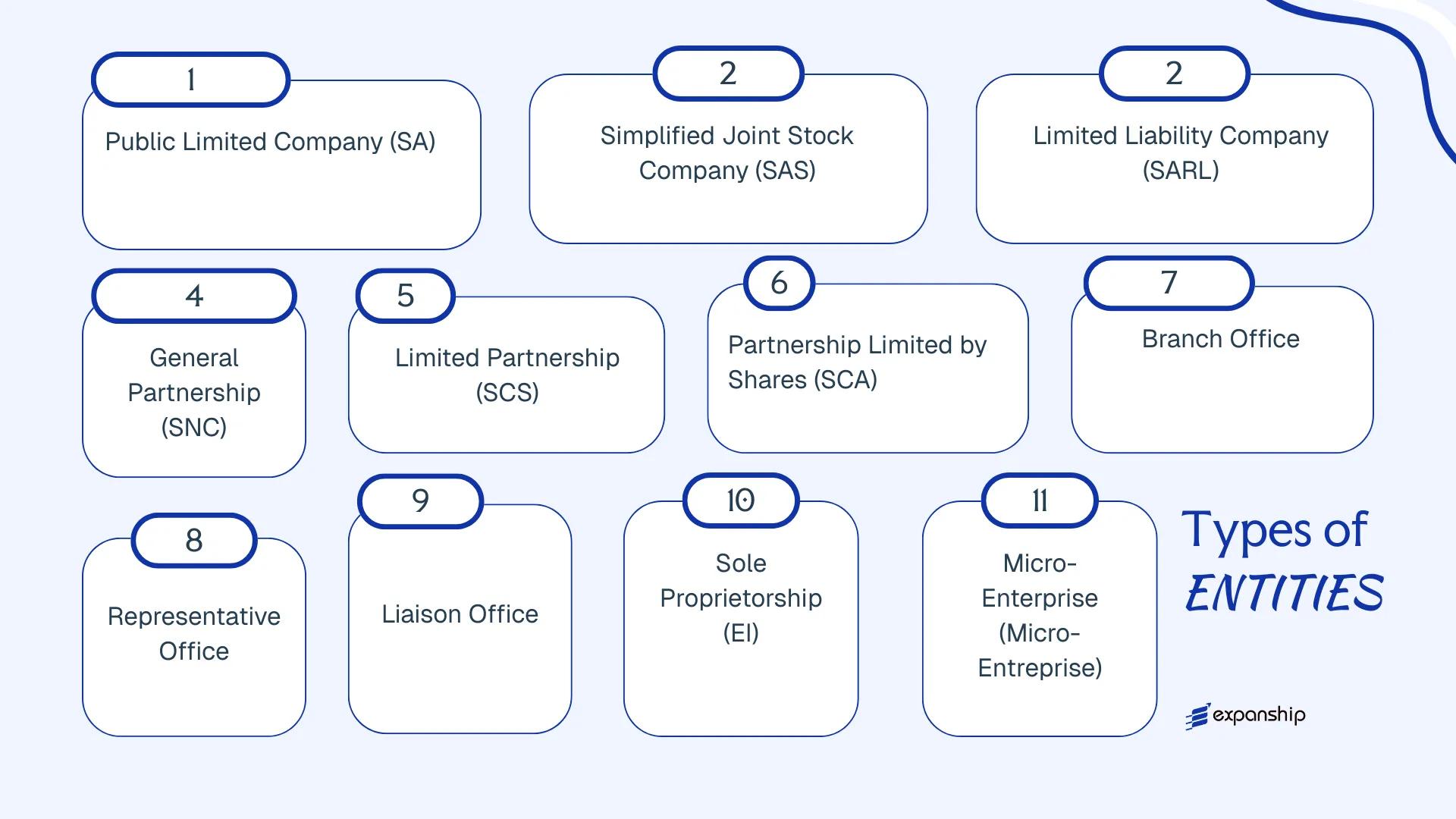

The principal legal entity types available include the Société Anonyme (SA), Société par Actions Simplifiée (SAS), Société à Responsabilité Limitée (SARL), Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA), Branch Office, Representative Office, Liaison Office, Entreprise Individuelle (EI), and Micro-Entreprise. Each structure carries distinct liability, governance, and tax treatment — this article examines each in turn.

An Overview of Business Structures in France

French company law offers several distinct entity types, each governed primarily by the Code de Commerce and supplemented by specific statutes such as the law of 24 July 1966 on commercial companies. An overview of business structures in France reveals that available forms range from single-person sole proprietorships to publicly listed joint-stock companies, with each structure carrying different rules on liability, governance, and taxation. The sections that follow examine each type in detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| SA | Share company | Limited | Corporate tax (IS) | Yes | 2 shareholders | Greffe du Tribunal de Commerce | Code de Commerce |

| SAS | Simplified share company | Limited | IS (IRPP optional) | Yes | 1 shareholder | Greffe du Tribunal de Commerce | Code de Commerce |

| SARL | Limited liability company | Limited | IS (IRPP optional) | Yes | 1–100 partners | Greffe du Tribunal de Commerce | Code de Commerce |

| SNC | General partnership | Unlimited | IRPP (IS optional) | Yes | 2 partners | Greffe du Tribunal de Commerce | Code de Commerce |

| SCS | Limited partnership | Mixed | IRPP (IS optional) | Yes | 2 partners | Greffe du Tribunal de Commerce | Code de Commerce |

| SCA | Partnership limited by shares | Mixed | Corporate tax (IS) | Yes | 4 members | Greffe du Tribunal de Commerce | Code de Commerce |

| Branch Office | Foreign extension | Parent liable | IS on French profits | Yes | N/A (parent entity) | Greffe du Tribunal de Commerce | Code de Commerce |

| Representative Office | Non-trading entity | Parent liable | No taxable activity | No | N/A (parent entity) | Greffe du Tribunal de Commerce | N/A |

| EI | Sole proprietorship | Limited (since 2022) | IRPP | Yes | 1 individual | Guichet Unique (INPI) | Loi n°2022-172 |

| Micro-Entreprise | Simplified EI regime | Limited | IRPP (flat-rate) | Yes | 1 individual | Guichet Unique (INPI) | Code de Commerce |

Each of these structures is examined in full in the sections below.

Société Anonyme (SA)

The Société Anonyme is governed primarily by the French Commercial Code (Code de Commerce), with foundational provisions dating back to the law of 24 July 1966, subsequently codified and reformed over successive decades. As a distinct legal entity with separate legal personality, it shields shareholders from personal liability beyond the value of their subscribed shares.

Structurally, the SA occupies a more regulated tier than most other French commercial forms, reflecting its suitability for larger enterprises and public capital-raising. Meeting the Société Anonyme SA France requirements involves satisfying minimum shareholder thresholds, capital rules, and governance obligations that set it apart from lighter structures.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (SA) | Joint-stock company; separate legal personality |

| Members | Minimum 2 shareholders (non-public); minimum 7 for a listed SA; no statutory maximum | Shareholders hold transferable shares (actions) |

| Governance | Board of Directors (Conseil d'Administration) with 3–18 members, or a Supervisory Board (Conseil de Surveillance) + Management Board (Directoire) | Two governance models available under the same legal form |

| Capital | Minimum €37,000 (non-listed); minimum €225,000 (listed); denominated in EUR | At least half must be paid up on registration; remainder within 5 years |

| Local Presence | Registered office (siège social) required in France | No statutory requirement for a local director, but governance obligations apply |

| Privacy | Shareholder details filed with the Registre du Commerce et des Sociétés (RCS); beneficial ownership reported to the Registre des Bénéficiaires Effectifs | Limited privacy; public filings are standard |

Focus Points

- Taxation: Subject to corporate income tax (*impôt sur les sociétés*) at the standard 25% rate; dividends distributed to non-residents attract a 30% withholding tax (reducible under applicable tax treaties); VAT registration required if turnover thresholds are met; no specific stamp duty on share transfers beyond the 0.1% flat rate applicable to listed shares.

- Annual Compliance: Mandatory statutory audit (commissaire aux comptes) required; annual accounts must be filed with the RCS; shareholder meetings (AGM) required at least once per year within six months of the financial year-end.

- Treaty Access: As a French tax-resident entity, the SA qualifies for France's extensive double tax treaty network (over 120 treaties), provided genuine economic substance exists.

- Conversion: An SA may be converted into an SAS by unanimous shareholder resolution, subject to compliance with applicable Code de Commerce provisions; the reverse conversion is also permitted.

- Restrictions: Cannot be formed as a single-member entity; regulated sectors (banking, insurance) impose additional supervisory requirements from the Autorité de Contrôle Prudentiel et de Résolution (ACPR) or Autorité des Marchés Financiers (AMF).

Sub-Types

SA with Board of Directors (Conseil d'Administration)

This is the classical governance model, where a single board oversees both management and supervision. It suits firms that prefer unified decision-making under a Chairperson-CEO (Président-Directeur Général).

SA with Supervisory Board and Management Board (Directoire / Conseil de Surveillance)

Adopted from the German two-tier model, this structure separates executive management from supervisory oversight. It is typically used by larger enterprises seeking formal segregation of governance functions, or where institutional investors require independent oversight mechanisms.

Recommendations

The SA is most appropriate for large operating companies, firms preparing for a public listing on Euronext Paris, or businesses requiring institutional investor participation. Its principal advantage is access to public equity markets; the primary drawback is the administrative and compliance burden, which is materially higher than most other French commercial entities.

The SA is best suited to established businesses with significant capital requirements, institutional shareholders, or an intent to list on a regulated market.

Company Incorporation in France

Incorporate your Société Anonyme or other French entity with full regulatory compliance support.

Société par Actions Simplifiée (SAS)

The Société par Actions Simplifiée SAS France is governed primarily by Articles L227-1 through L227-20 of the Code de commerce, introduced in 1994 and substantially reformed in 1999 to broaden access beyond large corporations. It carries separate legal personality from the moment of registration with the Registre du commerce et des sociétés (RCS), and shareholders bear liability only to the extent of their capital contributions.

Structurally, the SAS occupies a hybrid position: it combines the capital-based framework of a joint-stock company with the contractual freedom more typically associated with partnerships. The articles of association (statuts) govern most internal arrangements, giving founders wide latitude over governance, share transfer conditions, and profit distribution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société par Actions Simplifiée | Separate legal personality; limited liability |

| Members | Shareholders (actionnaires); President (Président) as mandatory officer | Minimum 1 shareholder (SASU if sole); no maximum. President need not be a shareholder |

| Capital | No statutory minimum; shares denominated in EUR | Capital must be fully defined in statuts; contributions in kind require an apport commissaire valuation above certain thresholds |

| Local Presence | Registered office (siège social) in France required | No mandatory resident director, but a legal address must be maintained |

| Share Transfers | Governed by statuts; approval clauses (agrément) are common | Transfer restrictions can be extensively customised |

| Privacy | Beneficial ownership disclosed to RCS and reported to BODACC | Shareholder identity appears in public filings |

Focus Points

- Taxation: Subject to corporate income tax (IS) at 25% standard rate; reduced 15% rate applies on the first €42,500 of profit for qualifying SMEs. VAT registration is mandatory once turnover thresholds are met. Dividends paid to non-resident shareholders are subject to a 30% withholding tax, reducible under applicable double tax treaties. No specific stamp duty on share transfers by default, though variable rates apply when real estate assets are held by the company.

- Annual Compliance: Annual accounts must be filed with the greffe du tribunal de commerce; a statutory auditor (commissaire aux comptes) is mandatory once two of three thresholds (balance sheet, turnover, headcount) are exceeded.

- Treaty Access: As a French tax resident entity, the SAS accesses France's extensive tax treaty network, covering over 120 jurisdictions.

- Conversion: An SAS can be converted into an SA, SARL, or other recognised form by shareholder resolution, subject to the conditions of the Code de commerce.

- Restrictions: Financial institutions and insurance companies are prohibited from using the SAS structure under French regulatory law.

Sub-Types

Société par Actions Simplifiée Unipersonnelle (SASU)

The SASU is the single-shareholder variant of the SAS, established under the same legislative framework. It is the preferred structure for solo founders who require limited liability and the contractual flexibility of the SAS without involving multiple shareholders. The SASU converts automatically into a standard SAS upon the admission of a second shareholder.

Closing

The SAS is widely used for holding structures, venture-backed operating companies, joint ventures, and IP-holding vehicles, largely because the statuts can be tailored to accommodate investor rights, vesting schedules, and exit mechanisms that more rigid forms do not permit. Its principal limitation is administrative cost: above the statutory auditor thresholds, ongoing compliance becomes materially more expensive.

The SAS suits founders and investors who require contractual flexibility over governance and share rights, particularly in multi-shareholder or investment-stage businesses where bespoke arrangements are a commercial necessity.

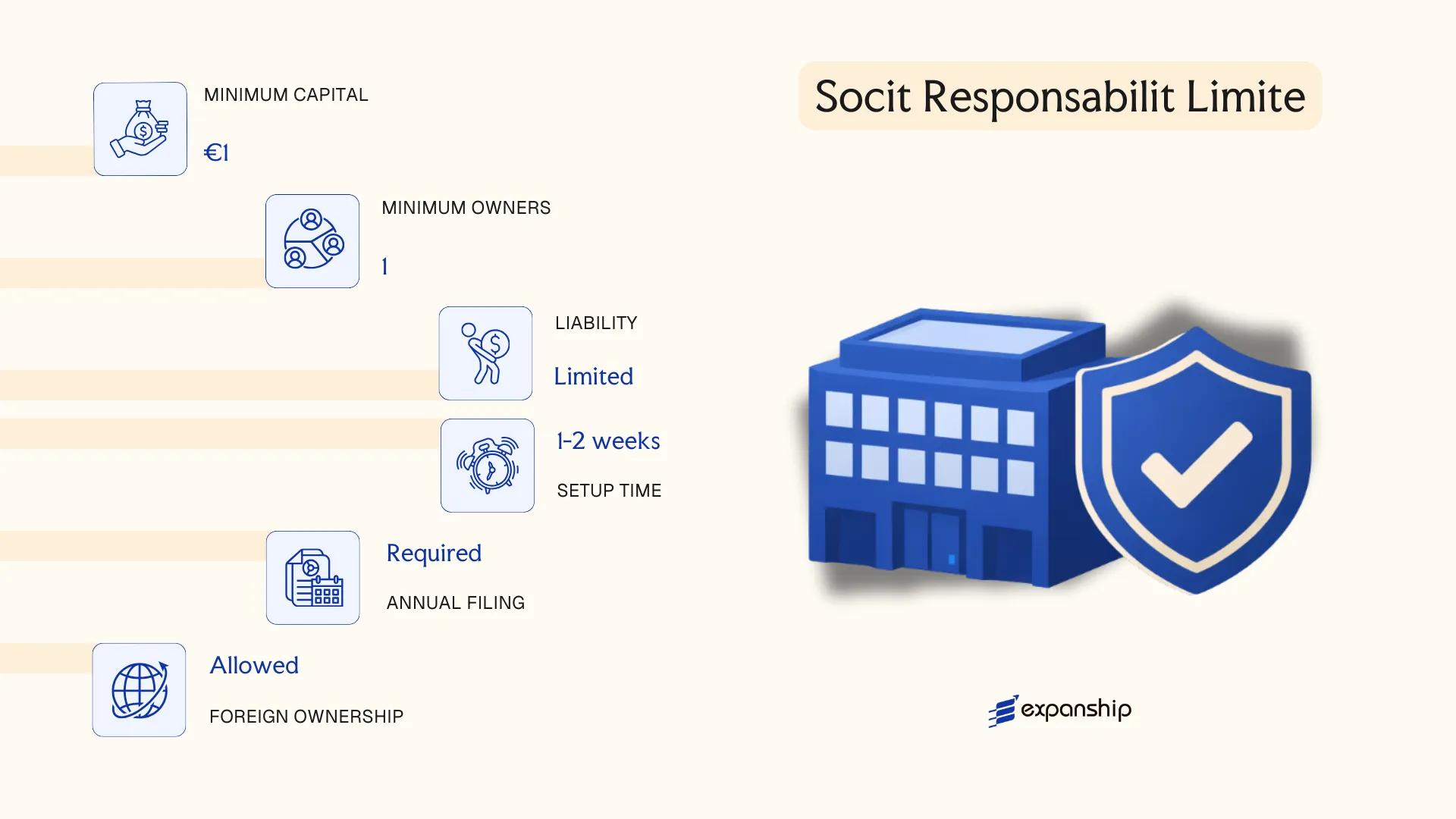

Société à Responsabilité Limitée (SARL)

The Société à Responsabilité Limitée SARL France is governed primarily by the French Commercial Code (Code de commerce), with foundational provisions established under the law of 24 July 1966, subsequently consolidated through successive reforms. It carries separate legal personality from the moment of registration with the Registre du Commerce et des Sociétés (RCS).

Liability is limited to each associate's capital contribution, making it a hybrid structure — neither purely a share-based company nor a traditional partnership. This combination has historically made it a default choice for small and medium-sized businesses established by French residents and foreign investors alike.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company | Separate legal personality upon RCS registration |

| Members | 1 to 100 associates (associés); managed by one or more gérants | Single-member variant is the EURL; gérant need not be an associate |

| Capital | No statutory minimum (nominally €1); contributions can be in cash or in kind | Cash contributions must be deposited with a bank or notary prior to registration |

| Local Presence | Registered office (siège social) required in France | No mandatory resident director, but a French address is compulsory |

| Shares | Non-freely transferable parts sociales | Transfer to third parties requires approval by associates holding a majority of shares |

| Privacy | Beneficial ownership declared to Registre des Bénéficiaires Effectifs (RBE) | Financial accounts filed with the RCS are publicly accessible |

Focus Points

- Taxation: Subject to Impôt sur les Sociétés (IS) at the standard 25% corporate rate; small eligible SARLs may opt for Impôt sur le Revenu (IR) for up to five years; VAT registration required once turnover thresholds are met; dividends paid to non-resident associates may be subject to a 12.8% or 30% withholding tax depending on applicable tax treaties.

- Annual Compliance: Annual accounts must be approved by associates and filed with the RCS within seven months of the financial year-end; statutory audit is mandatory only once two of three prescribed thresholds are exceeded.

- Economic Substance: No formal substance regime applies, though tax residency determinations follow effective management principles under the Code général des impôts.

- Treaty Access: As a French tax-resident entity, the SARL accesses France's extensive tax treaty network, covering over 120 jurisdictions.

- Conversion: A SARL may be converted into an SAS or SA by associate resolution, subject to formalities prescribed by the Code de commerce without creating a new legal entity.

Sub-Types

EURL (Entreprise Unipersonnelle à Responsabilité Limitée)

The EURL is the single-associate variant of the SARL, governed by the same statutory provisions. It is commonly used by sole operators who require limited liability without involving additional shareholders; by default it is taxed under IR when the sole associate is an individual.

SARL de Famille

This variant is available exclusively to SARLs whose associates are all members of the same family group, as defined under Article 239 bis AA of the Code général des impôts. It permits an indefinite opt-in for IR taxation, beyond the standard five-year ceiling applicable to ordinary SARLs.

The SARL suits trading operations, family businesses, and domestic holding structures where close control over ownership transfers is desirable. Its transfer restriction mechanism preserves ownership stability, though that same mechanism can complicate exit strategies or the entry of new investors.

Small to medium-sized businesses or family-owned enterprises seeking limited liability with tightly controlled ownership.

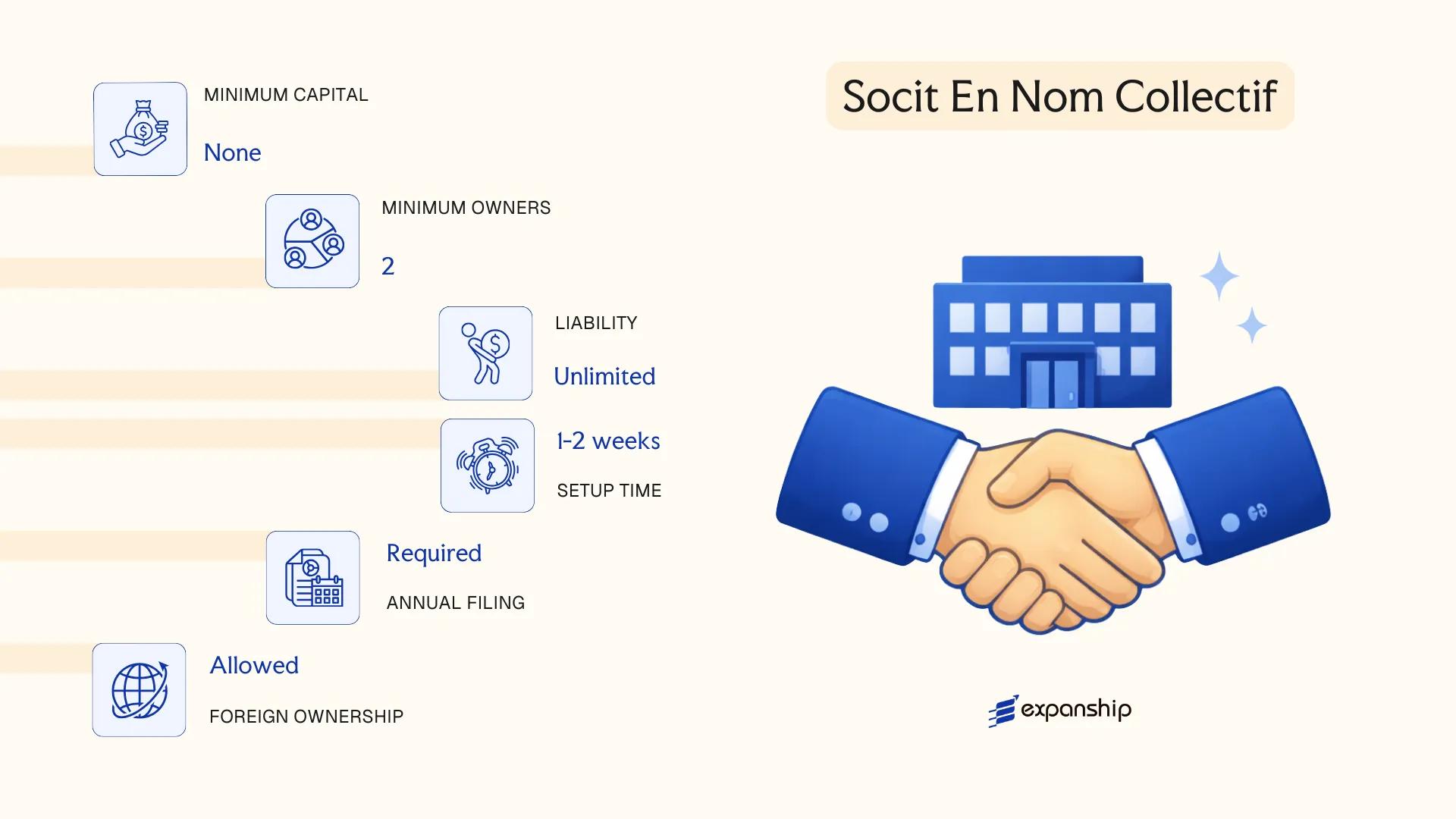

Société en Nom Collectif (SNC)

The Société en Nom Collectif SNC France represents the closest French equivalent to a general partnership under common law systems. Governed by Articles L221-1 to L221-17 of the Code de commerce, it holds separate legal personality upon registration with the Registre du commerce et des sociétés (RCS), yet this distinction offers shareholders little protection from business debts.

All associates bear joint, several, and unlimited personal liability for the firm's obligations. This structural feature, more than any other, defines how the SNC operates and who typically uses it.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société en Nom Collectif (General Partnership) | Separate legal personality; unlimited liability for all associates |

| Members | Referred to as associés; minimum 2, no maximum | All associates must hold trader status (commerçant); corporations may participate |

| Local Presence | Registered office (siège social) required in France | Must register with the RCS at the competent Greffe du tribunal de commerce |

| Capital | No statutory minimum; denominated in EUR | Capital divided into parts sociales, not shares; transfer requires unanimous consent |

| Privacy | Beneficial ownership disclosed to RCS and to the Registre des bénéficiaires effectifs | Associates' names appear in public filings |

Focus Points

- Taxation: By default, profits are taxed at the associate level under the income tax (IR) regime; unanimous election for corporate tax (IS) is possible. Standard French VAT rules apply, and no withholding tax exemption specific to the SNC form exists.

- Annual Compliance: Annual accounts must be filed with the Greffe; statutory audit is not required unless the firm crosses two of three thresholds under Article L221-9.

- Transfer Restrictions: Transfer of parts sociales requires unanimous approval from all associates, making exit difficult without prior shareholder agreement provisions.

- Treaty Access: As a fiscally transparent entity under the IR regime, treaty access depends on the tax residency of individual associates rather than the entity itself.

- Conversion: The SNC may be converted into another form, such as a SARL or SAS, subject to associate approval and compliance with formalities under the Code de commerce.

Closing

The SNC suits closely held professional or family businesses where associates prefer internal governance flexibility over liability protection, and where profit pass-through at the partner level is a deliberate tax planning choice. The absence of a minimum capital requirement lowers the entry barrier, but unlimited personal liability remains a significant structural constraint for any associate with personal assets at risk.

The SNC is best suited for small groups of trusted partners, particularly in trading or family-owned businesses, where all associates are comfortable accepting full personal liability for the firm's debts.

Partnerships [Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA)]

Both the Société en Commandite Simple and the Société en Commandite par Actions are governed by the French Commercial Code (Code de commerce), specifically the provisions regulating partnership structures. Each form of Société en Commandite France SCS SCA carries a distinct liability architecture: general partners (associés commandités) bear unlimited joint and several liability, while limited partners (associés commanditaires) are liable only up to their capital contribution.

Both entities hold separate legal personality upon registration with the Registre du Commerce et des Sociétés (RCS). This hybrid design makes them structurally distinct from purely capitalist entities like the SA or SAS, as the personal exposure of commandités introduces a meaningful governance consideration for prospective founders.

Key Characteristics

| Requirement | SCS | SCA |

|---|---|---|

| Legal Form | Limited partnership (no share capital required) | Partnership limited by shares (share capital required) |

| Members | Min. 1 commandité (general partner) + 1 commanditaire (limited partner); no maximum | Min. 1 commandité + 3 commanditaires; no maximum |

| Capital | No statutory minimum | Min. €37,000; at least 50% paid up on formation |

| Local Presence | Registered office in France required | Registered office in France required |

| Governance | No mandatory supervisory board | Supervisory board (conseil de surveillance) required |

| Privacy | Beneficial ownership disclosed in RCS; no public share register for SCS | Shareholders disclosed per standard listed/unlisted rules |

Focus Points

- Taxation: Both entities are generally treated as tax-transparent partnerships (sociétés de personnes) by default, meaning profits are taxed at partner level; however, an irrevocable election for corporate income tax (impôt sur les sociétés) is available. VAT registration obligations follow standard French rules.

- Annual Compliance: Both forms must file annual accounts with the RCS; the SCA, given its share capital structure, faces additional disclosure obligations comparable to those of a standard joint-stock company.

- Treaty Access: Tax treaty access depends on the elected tax regime and the residency of partners; treaty entitlement is not automatic for transparent entities.

- Restrictions: Commandités cannot be removed without their own consent in the SCS, which limits investor control over management.

Sub-Types

Société en Commandite Simple (SCS)

The SCS does not divide its capital into negotiable shares, making partner interests non-freely transferable without unanimous consent. It is typically used for family-held businesses or structures where founders wish to retain tight control over ownership transfers while admitting passive capital contributors.

Société en Commandite par Actions (SCA)

The SCA issues shares to commanditaires, allowing capital to be raised from a broader investor base while the commandités retain management authority. The French luxury and retail sector has historically used this structure to insulate founding families from hostile takeover attempts, since commanditaires cannot remove general partners through a shareholder vote.

Closing

The French limited partnership SCS structure suits closely held businesses prioritising transfer restrictions, while the Société en Commandite par Actions France serves capital-intensive operations where founders require durable management protection against outside shareholders. The principal drawback of both forms is the unlimited personal liability carried by all general partners.

These structures are best suited for founder-led businesses or family groups seeking to separate economic participation from management control, provided at least one partner is prepared to accept unlimited liability.

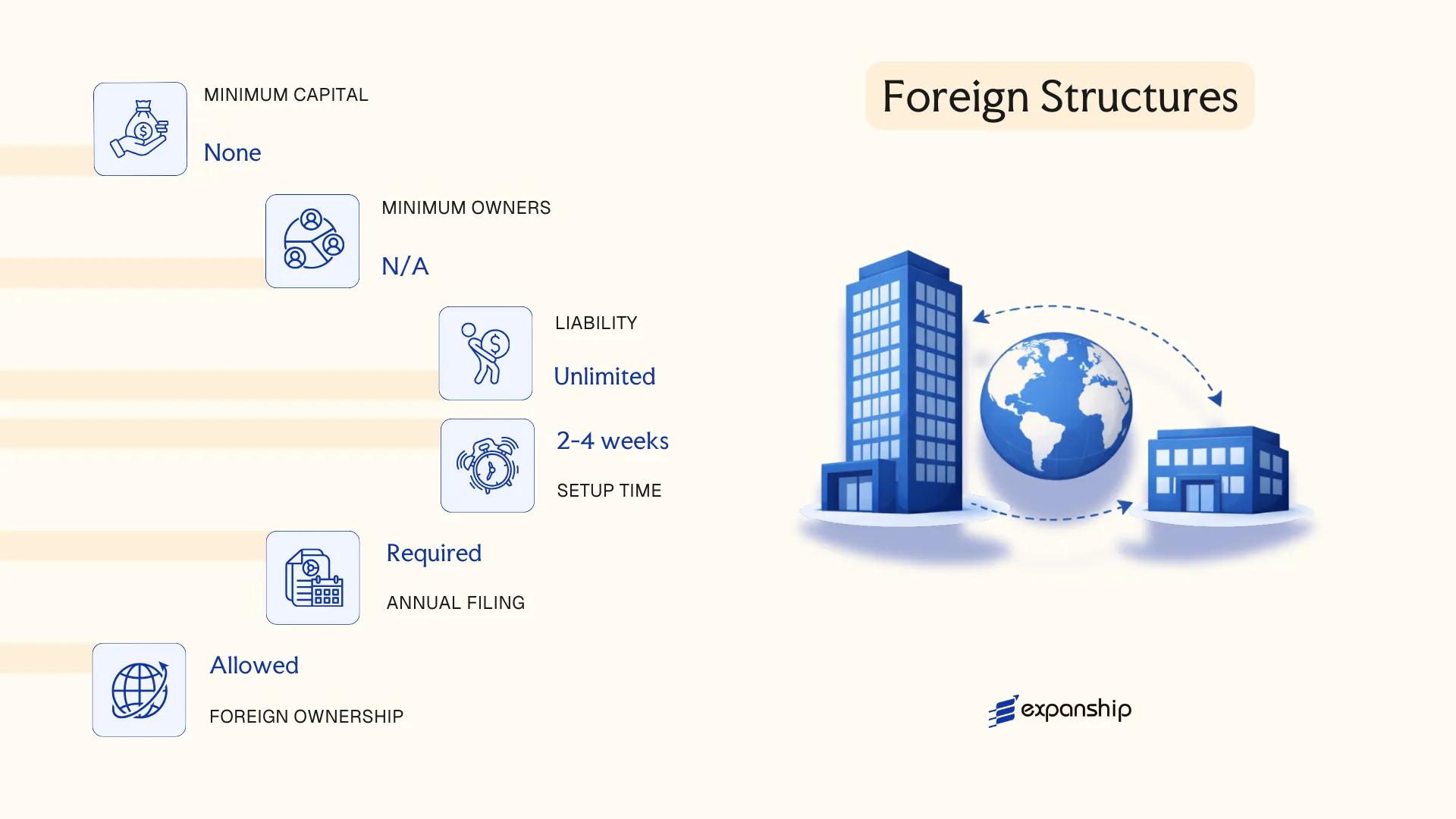

Foreign Structures [Branch Office, Representative Office, Liaison Office]

A foreign company branch office in France operates as an extension of its parent entity rather than a distinct legal person under French law. Governed by Articles L. 123-11 and related provisions of the Code de commerce, and subject to registration with the Registre du commerce et des sociétés (RCS), a branch carries no separate legal personality — the parent company bears full liability for its obligations.

Registration is handled through the relevant Greffe du Tribunal de commerce, and a legal representative domiciled in France must be appointed. Unlike a subsidiary, the branch files accounts that reflect the parent's financial position, and its activities are directly attributed to the foreign entity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch: extension of parent; Rep/Liaison Office: no distinct legal form | None hold separate legal personality |

| Representative | Permanent representative (mandataire) required | Must be resident or have a French address |

| Registration | RCS registration mandatory for branches; rep/liaison offices may register with relevant trade bodies | Liaison offices have lighter formalities |

| Capital | No minimum capital requirement | Parent's capital underpins the entity |

| Liability | Parent company bears unlimited liability | No liability ring-fencing exists |

| Privacy | Parent company accounts may be publicly linked | Financial disclosure obligations apply to branches |

Focus Points

- Taxation: Branches are subject to French corporate income tax (25% standard rate) on French-source profits; VAT obligations apply to taxable supplies; a branch profits remittance tax (retenue à la source) may apply under certain conditions, though tax treaty provisions can reduce or eliminate this.

- Economic Substance: A branch must carry out genuine commercial activity; representative and liaison offices are restricted to preparatory or auxiliary functions and cannot generate revenue directly.

- Annual Compliance: Branches must file annual accounts with the RCS and submit corporate tax returns to the Direction générale des Finances publiques (DGFiP); liaison offices face fewer filing obligations.

- Treaty Access: Branches can access France's tax treaty network as part of the parent entity, subject to permanent establishment rules under each applicable treaty.

- Conversion: A branch can be converted into a subsidiary (such as an SAS or SARL), but the process involves a fresh incorporation and transfer of assets rather than a direct structural transformation.

Sub-Types

Branch Office (Succursale)

A branch conducts full commercial operations — entering contracts, generating revenue, and employing staff — on behalf of the parent. It constitutes a permanent establishment for tax purposes and must register with the RCS.

Representative Office (Bureau de représentation)

Permitted only for preparatory and auxiliary activities such as market research or client liaison. It cannot conclude contracts or invoice clients independently, which limits its tax exposure but also its operational scope.

Liaison Office (Bureau de liaison)

Functionally similar to a representative office, a liaison office is used primarily for communication and coordination purposes. No commercial transactions may flow through it, and its administrative obligations are minimal compared to a branch.

Branches suit foreign firms that want direct operational presence without incorporating a separate entity, though the absence of liability separation is a significant structural drawback for risk management purposes.

Foreign companies testing the French market or running limited operations before committing to a full subsidiary structure.

Sole Proprietorship [Entreprise Individuelle (EI), Micro-Entreprise]

The micro-entreprise France sole proprietorship framework was significantly restructured by the loi du 14 février 2022, commonly known as the "loi en faveur de l'activité professionnelle indépendante." This reform abolished the former distinction between the Entreprise Individuelle and the auto-entrepreneur status, consolidating them under a unified EI regime while preserving the micro-entreprise as a simplified tax and social contribution track within that structure.

Under current law, the EI is not a separate legal entity. The entrepreneur and the business are legally the same person, though the 2022 reform introduced a mandatory separation between professional and personal assets, giving the proprietor de facto patrimoine protection without requiring formal incorporation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole proprietorship (no separate legal personality) | Asset separation introduced by 2022 reform provides limited personal patrimoine protection |

| Members | Single proprietor | No minimum capital; no shareholders or directors |

| Local Presence | Registered business address in France required | Registration made via the Guichet unique (INPI portal) |

| Capital | No minimum capital requirement | No paid-up or authorised capital threshold |

| Liability | Personal assets protected under patrimoine professionnel separation | Creditors can only claim against professional assets by default |

| Privacy | Proprietor's name publicly linked to the business | Listed in the Registre National des Entreprises (RNE) |

Focus Points

- Taxation: EI is subject to income tax (impôt sur le revenu) under BIC or BNC categories; micro-entreprise applies a flat abatement on turnover before tax calculation; no corporate tax applies unless an optional IS election is made; VAT exemption applies below the micro-entreprise franchise en base thresholds (currently €36,800 for services, €91,900 for goods).

- Social Contributions: Contributions are paid to the URSSAF on a percentage of turnover under the micro-entreprise regime, simplifying the standard TNS (travailleur non-salarié) calculation.

- Annual Compliance: No statutory accounts filing required for micro-entrepreneurs; EI proprietors outside the micro threshold must maintain full accounting records and file with the RNE.

- Conversion: An EI can be converted into a company (such as an EURL or SASU) through an apport de fonds de commerce procedure without triggering automatic liquidation.

- Restrictions: The micro-entreprise regime is subject to annual turnover ceilings; exceeding these thresholds automatically shifts the proprietor to the standard EI regime.

Sub-Types

Micro-Entreprise (formerly Auto-Entrepreneur)

The micro-entreprise is not a distinct legal structure but a simplified fiscal and social regime available to EI proprietors whose annual turnover remains below statutory ceilings. The French auto-entrepreneur regime uses flat-rate contribution and abatement rates, removing the need for detailed accounting, which makes it the most accessible entry point for freelancers and small-scale traders.

Entreprise Individuelle à Responsabilité (Standard EI post-2022)

The standard EI, post-reform, applies to proprietors exceeding micro thresholds or those who opt out of the simplified regime. It requires formal bookkeeping, annual declarations to tax authorities, and URSSAF registration under the standard TNS regime — while still offering the same patrimoine separation protections introduced by the 2022 law.

Closing

The EI and micro-entreprise structures suit freelancers, consultants, and sole traders operating in France with low overhead and no immediate plans to bring in co-owners or external investors. The built-in asset separation under the 2022 reform addresses the primary historical drawback of unlimited personal liability, though the absence of corporate tax optimisation tools remains a constraint for higher-earning independents.

The micro-entreprise regime is best suited for individuals testing a business concept or operating as solo service providers with annual turnover below the statutory thresholds.

How to Choose the Right Entity Type in France

Knowing how to choose a business entity in France requires more than a general preference — the structural decision carries legal, tax, and operational consequences that are difficult to reverse once registration is complete.

Why Your Entity Choice Matters

The French Commercial Code (Code de commerce) governs entity formation and sets mandatory obligations that vary by structure. Choosing the wrong form can produce concrete, costly outcomes:

- Registering as a micro-entreprise when your revenue exceeds the applicable threshold forces an automatic reclassification, which may trigger retroactive tax and social contribution adjustments.

- Selecting an entity that lacks corporate tax status can disqualify your business from benefits under France's tax treaty network, preventing withholding tax reductions on dividends or royalties paid to foreign shareholders.

- Forming an SA when your business is a single-person consultancy creates mandatory auditor (commissaire aux comptes) appointment obligations that add unnecessary annual costs.

- Choosing a general partnership structure when limited liability is operationally necessary exposes partners to unlimited personal liability for company debts.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or insurance each point toward distinct structures under French law.

- Ownership and Management: Single-founder businesses may suit an SAS unipersonnelle, while multi-investor arrangements may require a more formalized governance structure.

- Tax Objectives: Your need for IS (impôt sur les sociétés) liability, IR pass-through treatment, or treaty network access will narrow the eligible structures significantly.

- Liability Exposure: The extent to which you require separation between personal and business assets determines whether a limited-liability form is non-negotiable.

- Substance Capacity: If you cannot maintain a genuine operational presence — employees, premises, local decision-making — certain entity types may expose you to tax residency challenges.

- Exit Strategy: Not all French entities permit redomiciliation or conversion; verifying exit options before formation avoids structural lock-in.

Compliance Services for Companies in France

Ongoing compliance support for French entities, including annual filings, statutory obligations, and regulatory reporting.

Conclusion

Selecting the right structure is one of the most consequential early decisions in any setting up a company in France guide. The SAS dominates new registrations, largely due to its flexible governance and absence of a minimum share capital requirement. The SA suits larger enterprises requiring formal board structures or public capital markets access. For small, closely held businesses, the SARL offers a regulated framework with predictable liability boundaries. The SNC binds partners with unlimited joint liability, making it suitable only for businesses where partners accept full personal exposure. Commandite structures serve niche arrangements separating management from capital. Sole proprietorship regimes, including the micro-entreprise, serve individual operators with modest revenue thresholds.

France continues to modernise its corporate registry processes, including digital filings through the Guichet unique administered by the INPI. Professional guidance through entity selection and registration reduces procedural risk considerably.

How Expanship Can Assist You

Registering a business in France involves entity-specific requirements — from drafting compliant statuts for an SAS or SARL to filing with the Greffe du Tribunal de Commerce through the Guichet Unique platform. Expanship's corporate services France company registration practice covers each of these steps directly, so nothing falls through the gaps between local procedure and your business objectives.

Our France entity setup service handles the full incorporation cycle and beyond:

- Preparation and legalization of formation documents

- Registered agent and registered office provision

- Filing with the Greffe and Guichet Unique liaison

- Post-incorporation compliance management, including annual obligations

- Banking introduction assistance for your French entity

Every engagement is managed by specialists familiar with French commercial law and the Infogreffe registry system.

Ready to take the next step? Reach out to Expanship France to discuss your specific situation.

Frequently Asked Questions (FAQ)

The Société par Actions Simplifiée (SAS) is the most frequently formed entity, primarily because it allows a single shareholder, imposes no minimum share capital, and grants broad contractual freedom in drafting the company's bylaws. Its flexibility makes it the default choice for startups and foreign investors alike.

A Branch Office is not a separate legal entity; it remains an extension of the foreign parent company, which bears full liability for its operations in France. An SAS, by contrast, holds independent legal personality under French law, with liability contained at the entity level. From a tax standpoint, both are subject to corporate income tax on French-source profits, but an SAS offers greater structural autonomy and a cleaner separation of assets.

The SAS and SARL both require shareholder disclosure in the Registre du Commerce et des Sociétés (RCS), so full anonymity is not achievable under standard French corporate law. Beneficial ownership information must also be filed in the Registre des Bénéficiaires Effectifs, maintained by the Greffe du Tribunal de Commerce. Nominee arrangements exist in practice but do not override these statutory disclosure requirements.

No. The Société en Nom Collectif (SNC) and both commandite structures require at least two partners by definition. A single individual can, however, form an SAS (as a SASU), a SARL (as an EURL), or operate as an Entreprise Individuelle. The SA requires a minimum of two shareholders in the simplified form, and seven when listed.

Most entity types, including the SAS, SARL, and SA, are open to non-resident foreign founders without a requirement to hold French nationality or residency. A foreign individual intending to act as a director, however, may need to obtain a titre de séjour autorisant l'exercice d'une activité commerciale if residing in France. Non-EU nationals operating remotely as shareholders typically face no additional administrative barriers at the point of incorporation.

French law permits transformation between entity types without dissolution, provided the conversion meets the statutory requirements of the target structure. A common pathway is the transformation of an EURL into a SASU, or a SARL into an SAS, both of which are handled through shareholder resolution and re-registration with the Greffe. Transformation into an SA requires a higher share capital threshold and an auditor's report confirming the company's net assets.

No. A Branch Office and a Liaison Office do not constitute separate legal entities under French law; they are extensions of the foreign parent. By contrast, the SA, SAS, SARL, SNC, SCS, and SCA all acquire legal personality upon registration with the RCS. The Entreprise Individuelle sits in a middle position: since the 2022 reform under the loi du 14 février 2022, it benefits from a statutory separation of personal and professional assets, though it remains legally indistinct from its owner.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.