Key Takeaways

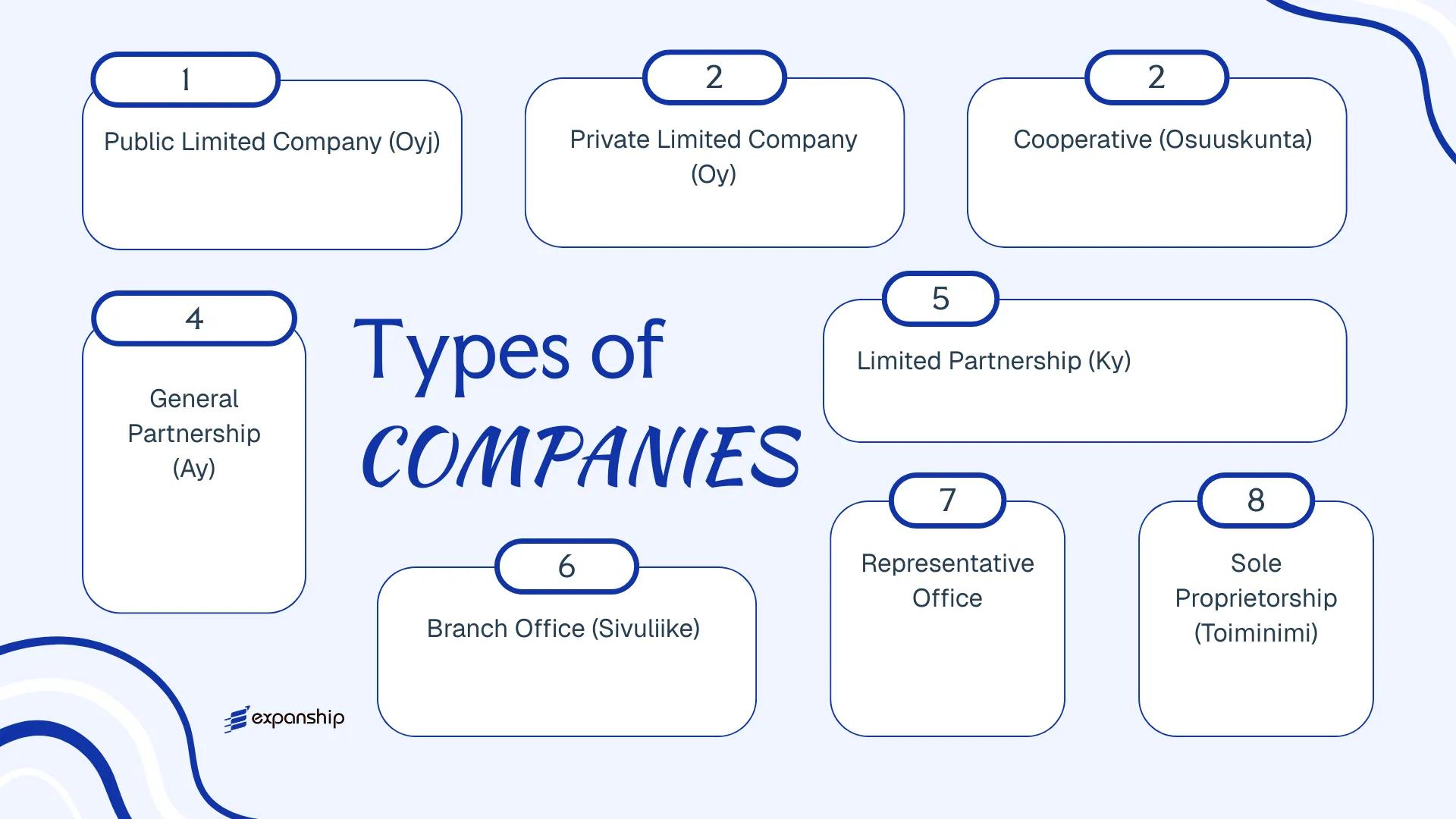

- Finland recognizes eight distinct business structures governed primarily by the Finnish Companies Act (Osakeyhtiölaki 624/2006), with all entities registered through the Finnish Patent and Registration Office (PRH).

- The Private Limited Company (Osakeyhtiö / Oy) is the most commonly registered entity form in Finland, offering liability separation and a straightforward capital structure for both resident and foreign entrepreneurs.

- Foreign companies can enter the Finnish market without establishing a local subsidiary by registering either a Branch Office (Sivuliike) or a Representative Office through the PRH.

- General Partnerships (Avoin yhtiö / Ay) and Limited Partnerships (Kommandiittiyhtiö / Ky) remain available options for smaller domestic ventures where partners are prepared to accept personal liability.

Introduction to Entity Types in Finland

Finland is a Nordic nation bordered by Sweden, Norway, and Russia, with a coastline along the Baltic Sea. As an independent republic and European Union member state, it operates a transparent, rules-based legal environment for business formation. Companies are registered through the Finnish Patent and Registration Office (PRH), which maintains the Trade Register and governs the incorporation process for all legal structures.

The country applies a territorial corporate tax system with an active network of double tax treaties, making the choice of legal structure a material decision for both domestic operators and foreign investors.

Depending on your objectives, the types of business entities in Finland available to you include the Private Limited Company (Osakeyhtiö / Oy), Public Limited Company (Julkinen osakeyhtiö / Oyj), General Partnership (Avoin yhtiö / Ay), Limited Partnership (Kommandiittiyhtiö / Ky), Cooperative (Osuuskunta), Sole Proprietorship (Toiminimi), Branch Office (Sivuliike), and Representative Office. Each structure carries distinct requirements under the Finnish Companies Act (Osakeyhtiölaki 624/2006) and related legislation. This article examines each legal structure for business in Finland in detail — covering formation requirements, liability, governance, and taxation.

An Overview of Business Structures in Finland

Finnish company law recognises six primary business structures, each governed principally by its own statute or by the Companies Act (Osakeyhtiölaki 624/2006) and the Act on Cooperative Societies (Osuuskuntalaki 421/2013). A Finland business structures comparison shows that the range spans from sole proprietorships to publicly listed corporations, with partnerships and foreign entity forms occupying the middle ground. Each structure carries distinct rules on liability, taxation, governance, and minimum membership that reflect different commercial purposes.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxation | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (Oyj) | Corporate | Limited | Corporate tax | Yes | 1 shareholder | PRH | Osakeyhtiölaki 624/2006 |

| Private Limited Company (Oy) | Corporate | Limited | Corporate tax | Yes | 1 shareholder | PRH | Osakeyhtiölaki 624/2006 |

| Cooperative (Osuuskunta) | Corporate | Limited | Corporate tax | Yes | 1 member | PRH | Osuuskuntalaki 421/2013 |

| General Partnership (Ay) | Partnership | Unlimited | Partner level | Yes | 2 partners | PRH | Laki avoimesta yhtiöstä 389/1988 |

| Limited Partnership (Ky) | Partnership | Mixed | Partner level | Yes | 1 general, 1 limited | PRH | Laki avoimesta yhtiöstä 389/1988 |

| Branch Office (Sivuliike) | Foreign entity | Parent liable | Corporate tax | Yes | Parent company | PRH | Laki elinkeinon harjoittamisesta 122/1919 |

| Representative Office | Foreign entity | Parent liable | Generally exempt | Restricted | Parent company | PRH | No specific statute |

| Sole Proprietorship (Toiminimi) | Individual | Unlimited | Personal income tax | Yes | 1 person | PRH | Laki elinkeinon harjoittamisesta 122/1919 |

Each of these structures is examined in full in the sections below.

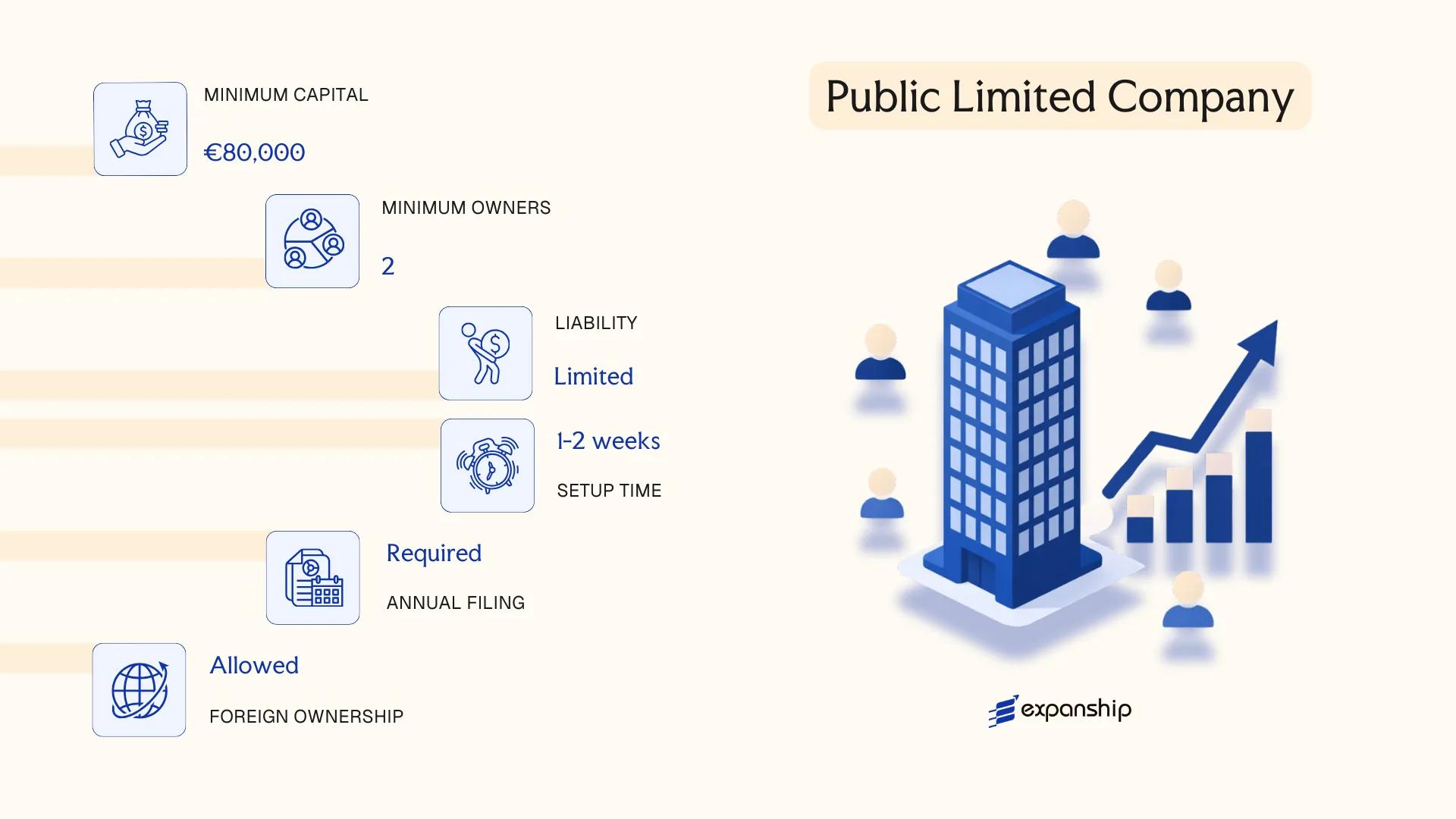

Public Limited Company (Julkinen osakeyhtiö / Oyj)

A Finland public limited company — the julkinen osakeyhtiö, abbreviated as Oyj — is governed by the Finnish Companies Act (Osakeyhtiölaki, 624/2006). It carries separate legal personality, meaning the entity itself holds rights and obligations distinct from its shareholders.

Shares in an Oyj may be offered to the public and listed on a regulated market, such as Nasdaq Helsinki. This makes the structure suited to large-scale capital raises, but it also triggers disclosure and governance requirements that do not apply to private companies.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Public Limited Company (Julkinen osakeyhtiö / Oyj) | Separate legal personality; limited liability |

| Members | Shareholders (no maximum); minimum 1 shareholder | Shareholders can be natural persons or legal entities |

| Governing Bodies | Board of Directors (min. 3 members) + Supervisory Board (optional) + General Meeting | A Managing Director is mandatory |

| Local Presence | Registered office in Finland required | No statutory resident director requirement, but practical presence is expected |

| Share Capital | Minimum EUR 80,000 | Must be fully subscribed at registration; shares may be publicly traded |

| Auditor | Statutory audit mandatory | Must appoint a KHT-certified (authorised) auditor |

| Privacy | Shareholder register is public via the Trade Register | Financial statements filed with the Finnish Patent and Registration Office (PRH) are publicly accessible |

Focus Points

- Taxation: Corporate income tax at 20% on worldwide profits; VAT standard rate of 25.5% (from September 2024); withholding tax of 20% on dividends to non-treaty residents — Finnish Tax Administration (Vero) administers all filings.

- Annual Compliance: Annual accounts, board report, and auditor's report must be filed with the PRH; listed Oyjs also report under Nasdaq Helsinki rules and the EU Market Abuse Regulation.

- Treaty Access: Finland's tax treaty network covers 70+ countries; Oyj structures are generally eligible for reduced withholding rates where treaties apply.

- Conversion: An Oyj may convert to a private limited company (Oy) by shareholder resolution, subject to creditor protection procedures under the Companies Act.

- Restrictions: Regulated sectors (banking, insurance, investment services) require separate licensing from the Finnish Financial Supervisory Authority (Finanssivalvonta / FIN-FSA).

Closing

The Oyj is used primarily for businesses seeking access to public equity markets, large institutional investors, or cross-border listings. The mandatory EUR 80,000 minimum capital and statutory audit requirement make it operationally heavier than a private structure.

Established businesses and institutional ventures planning a public listing on Nasdaq Helsinki or requiring publicly tradeable share capital.

Company Incorporation in Finland

Set up your Finnish entity with end-to-end registration support, PRH filings, and compliance onboarding.

Private Limited Company (Osakeyhtiö / Oy)

The Finland private limited company, known as the osakeyhtiö (Oy), is governed by the Companies Act (Osakeyhtiölaki, 624/2006). It carries separate legal personality, meaning the entity's obligations are distinct from those of its shareholders.

Liability is capped at each shareholder's capital contribution. This structure accommodates a single founder acting simultaneously as director and sole shareholder, making it accessible for small businesses and larger ventures alike.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company | Shares cannot be publicly traded |

| Members | Shareholders: min. 1, no maximum; Directors: min. 1, no maximum | A single individual may hold all roles |

| Local Presence | Registered office in Finland required; no mandatory local director | Registered address must be a physical Finnish address |

| Share Capital | EUR 0 minimum (as of 2019 reform) | Capital must be recorded in articles of association |

| Privacy | Shareholder register is public via PRH; beneficial ownership filed with PRH | Ultimate beneficial owners disclosed to the Trade Register |

Focus Points

- Taxation: Subject to 20% corporate income tax; VAT standard rate 25.5% (from 2024); dividend withholding tax applies to non-resident shareholders, typically 15–20% subject to tax treaty; no stamp duty on share transfers.

- Annual compliance: Financial statements filed with the Finnish Patent and Registration Office (PRH); audit required once thresholds are exceeded.

- Economic substance: No statutory substance requirements, though genuine business activity affects treaty eligibility.

- Treaty access: Finland's tax treaty network covers 70+ countries; Oy qualifies as a resident company for treaty purposes.

- Conversion: An Oy can convert to a public limited company (Oyj) by meeting capital and governance thresholds under the same Act.

Closing

The Oy suits trading operations, holding structures, IP ownership, and professional services firms where limited liability and retained earnings reinvestment are priorities. Its zero minimum capital requirement lowers the entry barrier, though the mandatory public disclosure of the shareholder register reduces structural privacy.

Best suited for entrepreneurs, SMEs, and foreign investors establishing an operational or holding presence who require limited liability without the governance burden of a public company.

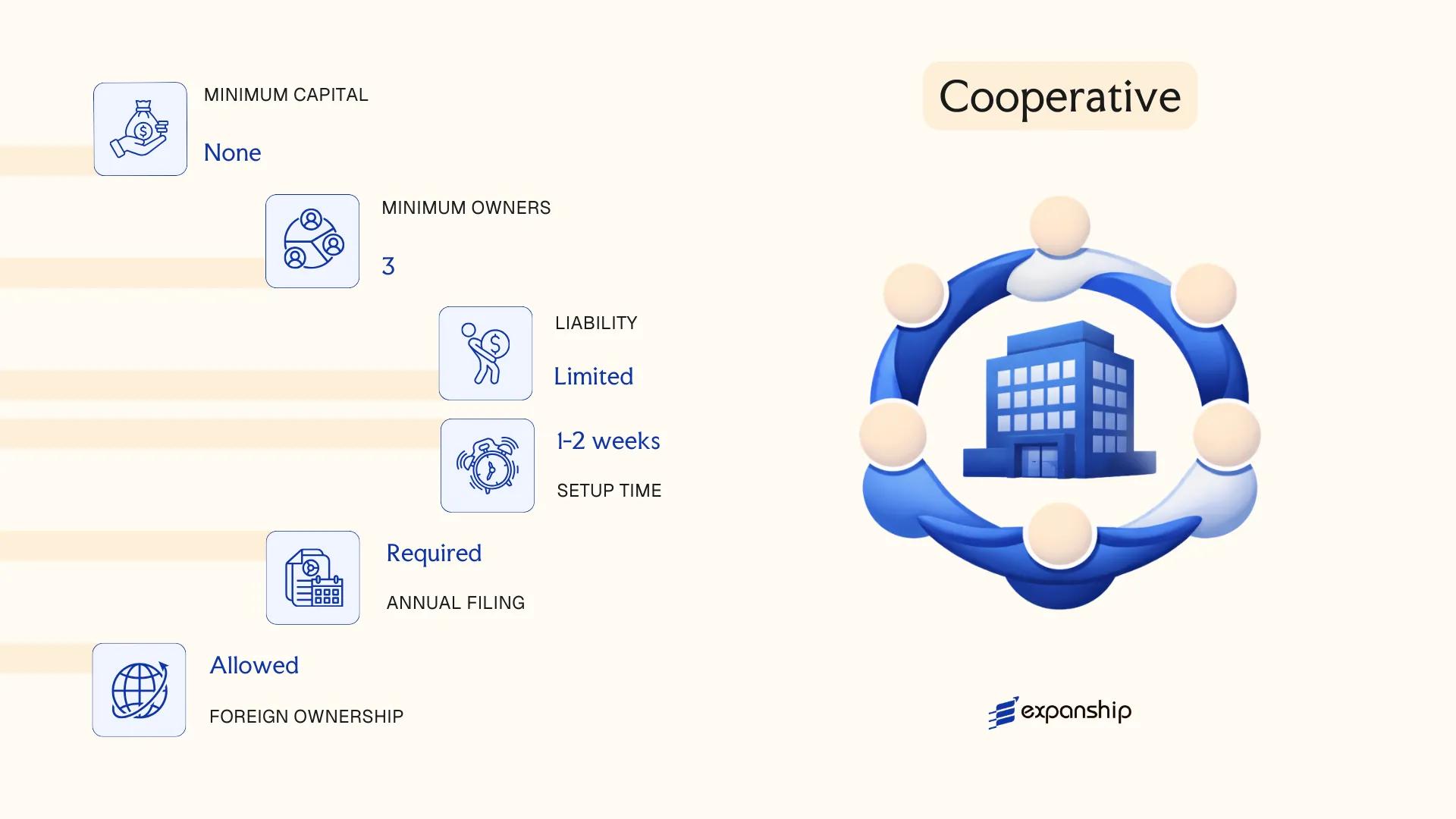

Cooperative (Osuuskunta)

Governed by the Co-operatives Act (Osuuskuntalaki 421/2013), a cooperative — or osuuskunta — is a separate legal entity in which members share economic activity for mutual benefit. To register a cooperative in Finland, at least three founding members are required, and the entity must be registered with the Finnish Trade Register maintained by the Patent and Registration Office (PRH).

Liability is limited to each member's subscription, meaning personal assets are not exposed to the cooperative's debts. This structure occupies a middle ground between a company and an association, making it common in sectors such as agriculture, retail, housing, and professional services.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Cooperative (Osuuskunta) | Separate legal personality; registered with PRH |

| Members | Minimum 3; no statutory maximum | Natural persons or legal entities; referred to as "members" (jäsenet) |

| Governing Bodies | Board of Directors + General Meeting; Supervisory Board optional | Large cooperatives may require an auditor |

| Registered Office | Must maintain a registered address in Finland | No requirement for a local resident director under the Co-operatives Act |

| Share Capital | No minimum capital requirement | Members pay a membership fee defined in the cooperative's rules (säännöt) |

| Privacy | Member register not publicly disclosed in full | Board member names are publicly available via PRH |

Focus Points

- Taxation: Subject to 20% corporate income tax; VAT applies at standard Finnish rates; withholding tax on surplus distributions (ylijäämänpalautus) follows general dividend rules where applicable.

- Annual Compliance: Annual financial statements must be filed with PRH; audit obligations apply once the entity exceeds statutory thresholds under the Auditing Act (1141/2015).

- Economic Substance: No specific economic substance regime applies, but the entity must carry on genuine cooperative activity aligned with its stated purpose.

- Conversion: A cooperative may be converted into a limited company (Oy) under Chapter 19 of the Co-operatives Act, subject to member approval.

- Treaty Access: As a Finnish tax-resident entity, an osuuskunta has access to Finland's tax treaty network, though treaty eligibility depends on the specific treaty and income type.

Closing

The osuuskunta structure suits businesses built around shared ownership and member-driven operations, such as worker cooperatives, agricultural producers, and multi-stakeholder service ventures. The absence of a minimum capital requirement lowers the formation barrier, though the governance model — requiring member consensus — can slow decision-making as the entity grows.

Best suited for groups of professionals, farmers, or community-oriented businesses seeking collective ownership without significant upfront capital.

Partnerships [General Partnership (Avoin yhtiö / Ay), Limited Partnership (Kommandiittiyhtiö / Ky)]

Both the Finland general and limited partnership are governed by the Act on General Partnerships and Limited Partnerships (Laki avoimesta yhtiöstä ja kommandiittiyhtiöstä, 389/1988). Each structure carries full legal personality, meaning the firm can own assets, enter contracts, and sue or be sued in its own name.

Unlike a limited liability company, partners in an Ay bear unlimited personal liability for the firm's obligations. In a Ky, this liability is split: at least one general partner (vastuunalainen yhtiömies) carries unlimited exposure, while silent partners (äänettömät yhtiömiehet) are liable only up to their agreed capital contribution.

Key Characteristics

| Requirement | Avoin yhtiö (Ay) | Kommandiittiyhtiö (Ky) |

|---|---|---|

| Legal Form | General Partnership | Limited Partnership |

| Partners | Minimum 2 general partners; no maximum | Minimum 1 general partner + 1 silent partner; no maximum |

| Liability | All partners: unlimited | General partner(s): unlimited; silent partner(s): limited to contribution |

| Local Presence | Registered address in Finland required | Registered address in Finland required |

| Capital | No statutory minimum | No statutory minimum for general partner; silent partner must make a defined contribution |

| Registration | Must register with Finnish Patent and Registration Office (PRH) | Must register with PRH; silent partner's contribution recorded |

| Privacy | Partner details filed in the Trade Register and publicly accessible | Same; silent partner identity is also publicly disclosed |

Focus Points

- Taxation: Partnerships are fiscally transparent — profits flow through to partners and are taxed as their personal income or, if a corporate entity is a partner, as corporate income; no separate entity-level corporate tax applies, though VAT registration obligations follow standard Finnish thresholds.

- Annual Compliance: Annual financial statements must be filed with the PRH; auditor requirements depend on the firm's size thresholds under the Auditing Act (1141/2015).

- Conversion: An Ay or Ky can be converted into an Osakeyhtiö (Oy) without dissolution, subject to PRH registration and compliance with the Limited Liability Companies Act (624/2006).

- Restrictions: Non-EU/EEA general partners may require a Finnish-resident representative or applicable permit under Finnish trade legislation.

Sub-Types

Avoin yhtiö (Ay) — General Partnership

All partners hold equal management rights and unlimited liability unless the partnership agreement specifies otherwise. Commonly used by small professional firms or family-run businesses where partners operate actively in the business.

Kommandiittiyhtiö (Ky) — Limited Partnership

The Ky separates active management from passive investment: silent partners contribute capital but hold no management rights and bear no liability beyond their contribution. This structure suits arrangements where one party funds operations without operational involvement.

Closing

Both structures suit small-scale domestic operations where founders prefer simplicity over liability protection, though the absence of limited liability for general partners remains a material exposure for any business facing contractual or financial risk.

Finnish partnerships are best suited for small professional practices, family businesses, or domestic joint ventures where all active partners accept personal liability.

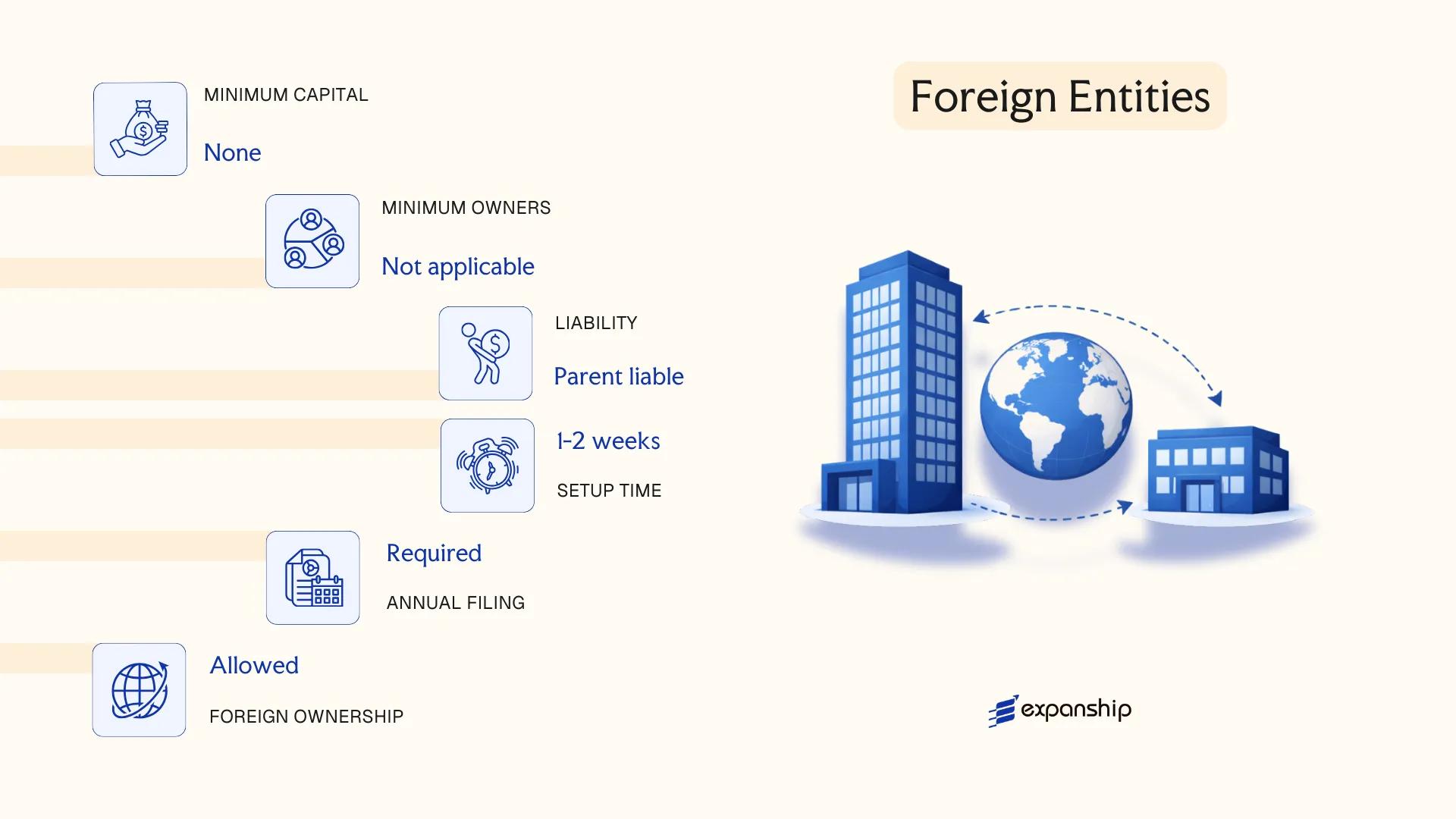

Foreign Entities [Branch Office (Sivuliike), Representative Office]

Foreign companies seeking a presence without incorporating a separate legal entity have two structural options. To open a branch office in Finland, the foreign parent must register a sivuliike with the Finnish Trade Register (Kaupparekisteri) under the Act on the Right to Carry on Trade (Laki elinkeinon harjoittamisen oikeudesta). A branch carries no separate legal personality — the parent company remains fully liable for all obligations incurred through it.

A representative office carries no formal registration requirement under Finnish law and cannot conduct revenue-generating activities. It serves solely for market research, liaison, or promotional functions, meaning it operates outside the Trade Register framework entirely.

Key Characteristics

| Requirement | Branch Office (Sivuliike) | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Informal presence; no legal standing in Finland |

| Liability | Parent bears unlimited liability | Parent bears unlimited liability |

| Local Presence | Registered address in Finland; appointed local representative mandatory | No formal requirement |

| Registration | Finnish Trade Register (PRH) | None required |

| Capital Requirement | None | None |

| Revenue Generation | Permitted | Not permitted |

Focus Points

- Taxation: A registered branch is subject to Finnish corporate income tax (20%) on Finnish-sourced profits; VAT registration is required if taxable turnover exceeds the statutory threshold; no withholding tax applies on profit remittances to the parent.

- Treaty Access: Branch offices may access Finland's tax treaties depending on the parent's residency and treaty provisions, but access is not automatic.

- Annual Compliance: Branches must file financial statements with PRH annually, mirroring the parent's accounting period.

- Restrictions: Representative offices cannot sign contracts, invoice clients, or generate income — any commercial activity triggers the obligation to register a branch or subsidiary.

Closing

A branch suits foreign firms testing the Finnish market or executing project-based contracts without committing to full incorporation. The key limitation is full parental liability exposure with no liability shield between the Finnish operations and the parent entity.

Best suited for established foreign companies with existing Finnish client contracts who require an operational presence without a standalone legal entity.

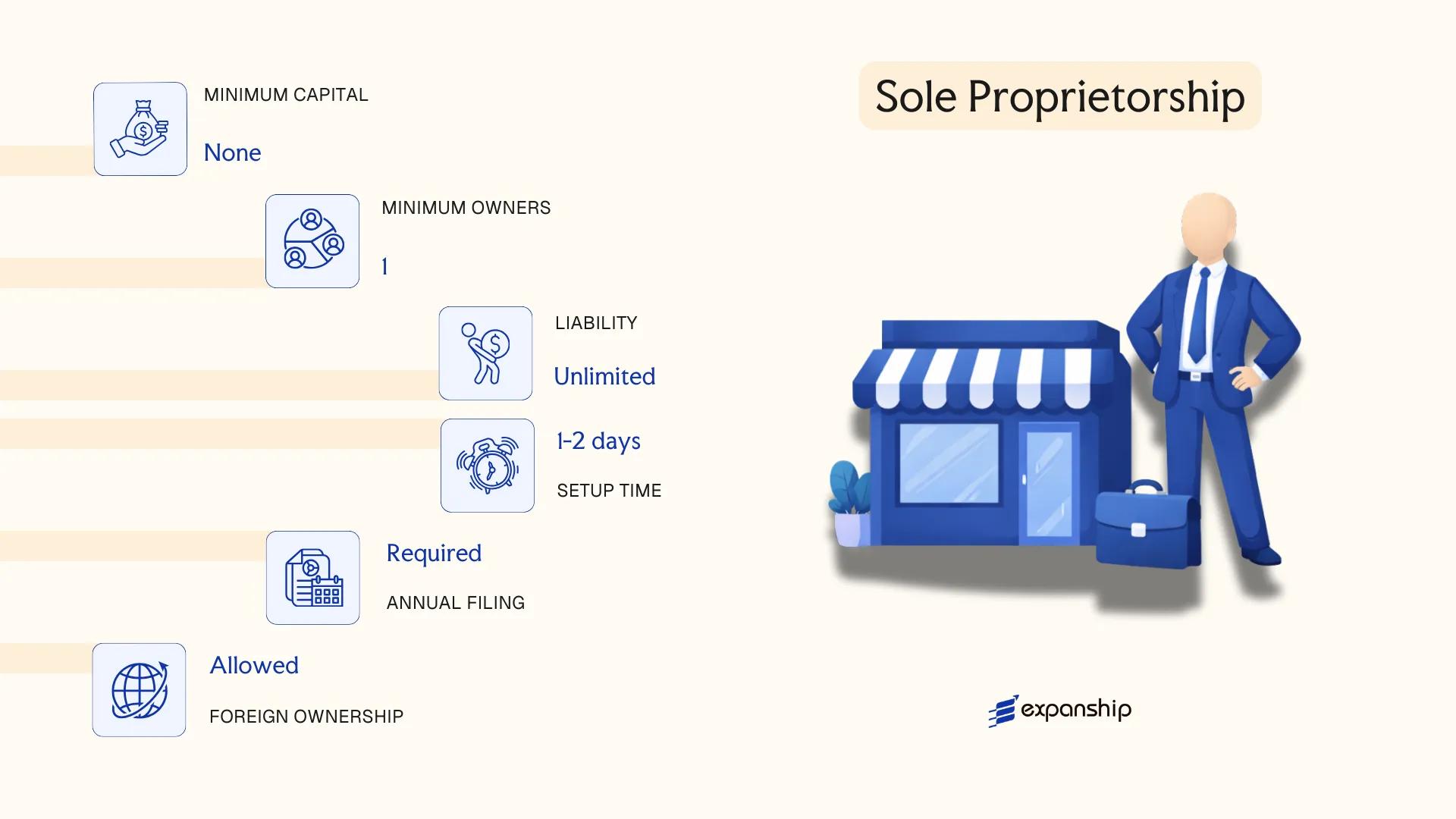

Sole Proprietorship (Yksityinen elinkeinonharjoittaja / Toiminimi)

A sole proprietorship Finland toiminimi is the simplest business form available to natural persons operating on their own account. It is governed by the Act on the Right to Carry on a Trade (Laki elinkeinon harjoittamisen oikeudesta, 122/1919) and subsequent amendments, along with general provisions under Finnish tax law.

The entity carries no separate legal personality. The proprietor and the business are legally one and the same, meaning personal assets are fully exposed to business liabilities. Registration is handled through the Finnish Patent and Registration Office (PRH) via the Business Information System (YTJ).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Toiminimi) | No separate legal personality; proprietor is personally liable |

| Members | Single natural person (proprietor) | Must be an EEA resident; non-EEA nationals require a PRH exemption permit |

| Local Presence | Finnish residential address required | No registered agent requirement, but a domicile address must be on file with PRH |

| Capital | No minimum capital requirement | No share capital structure exists |

| Privacy | Proprietor's name and business address are publicly registered via YTJ | Limited privacy compared to corporate forms |

Focus Points

- Taxation: Business income is taxed as the proprietor's personal income under progressive rates; a portion may be split into capital income taxed at 30–34%. VAT registration is mandatory once annual turnover exceeds €15,000. No withholding tax or corporate tax applies.

- Annual Compliance: Must file an annual tax return with the Finnish Tax Administration (Vero); no separate corporate financial statements required, though accounting records must be maintained.

- Conversion: Can be converted into a private limited company (Oy) with business continuity, subject to PRH notification and tax authority filings.

- Restrictions: Cannot have employees under a separate legal employer entity; the proprietor bears unlimited personal liability with no statutory liability cap.

- Treaty Access: As a pass-through structure with no separate legal personality, access to Finland's tax treaty network flows through the individual, not the business name.

Closing

A toiminimi suits low-risk, single-person service or trade operations where administrative simplicity outweighs the need for liability protection. The absence of minimum capital is a practical advantage, but unlimited personal liability makes it unsuitable for activities carrying significant financial or legal exposure.

Freelancers, consultants, and sole traders operating under their own name with limited financial risk and no immediate plans to scale or bring in partners.

How to Choose the Right Entity Type in Finland

Selecting the correct structure from the outset shapes your tax position, liability exposure, and administrative burden for the entire life of your business. Understanding how to choose a business structure in Finland means weighing concrete legal and operational factors — not just cost.

Why Your Entity Choice Matters

The structure you register has binding consequences under Finnish law:

- Choosing an Osakeyhtiö (Oy) subject to mandatory audit thresholds when your firm is a single-person consultancy generates statutory audit costs that do not apply to a sole trader (toiminimi) registration.

- Selecting a branch office (sivuliike) when you intend to conduct independent local trade may trigger reclassification as a permanent establishment under the Finnish Income Tax Act, with retroactive tax liability.

- Forming a general partnership (Avoin yhtiö) when your structure later requires outside equity investment locks you into unlimited joint liability without the capital-raising mechanism available to a limited company.

- Registering an entity without reviewing Finland's treaty network eligibility means the structure may not qualify for reduced withholding tax rates under applicable double tax agreements.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each point toward a different entity under the Finnish Companies Act (624/2006).

- Ownership and Management: Single-owner operations suit a toiminimi or Oy, while multi-party ventures may require the governance framework of a cooperative or limited company.

- Tax Objectives: Your need for treaty access, dividend distribution, or pass-through taxation should drive entity selection before any other consideration.

- Substance Capacity: If you cannot maintain a registered office, local management, or employees in Finland, certain structures will not satisfy operational requirements under Finnish tax authority (Verohallinto) guidance.

- Liability Exposure: Personal liability is unlimited in a general partnership and for a sole proprietor; an Oy limits liability to subscribed capital.

- Exit Strategy: Not all Finnish entity types permit conversion or redomiciliation — verify whether your chosen structure supports wind-up, merger, or transformation under the Companies Act before registering.

Compliance Services for Companies in Finland

Ongoing compliance support for Finnish entities, covering annual filings, Trade Register obligations, and Verohallinto reporting requirements.

Conclusion

Choosing the right structure is one of the foundational decisions in any incorporating a company in Finland guide. The Osakeyhtiö (Oy) is the most registered entity form in the country, favored by resident and foreign entrepreneurs alike for its liability separation and straightforward capital structure. The Oyj suits firms seeking public capital markets access; the Osuuskunta fits member-driven economic models. Partnerships under the Avoin yhtiö and Kommandiittiyhtiö frameworks work for smaller domestic ventures where personal liability is acceptable. Branch offices and representative offices serve foreign companies testing the market before committing to a local subsidiary.

Finland's regulatory environment, overseen by the Finnish Patent and Registration Office (PRH), continues to move toward digital-first registration processes. The country's expanding tax treaty network and its standing within the EU single market reinforce its position as a credible base for European operations. Expanship's team works directly within these frameworks to support your setup.

How Expanship Can Assist You

Expanship's Finland company incorporation services cover the full process of forming and maintaining a business entity under Finnish law. From registering a private limited company (Oy) or cooperative (Osuuskunta) to establishing a branch of a foreign firm, our team handles filings directly with the Finnish Trade Register (Kaupparekisteri), administered by the Finnish Patent and Registration Office (PRH).

Setting up your entity is only part of the picture. Ongoing compliance obligations require consistent attention after registration.

- Document preparation and notarization

- Registered address and local agent provision in Finland

- PRH filing and Trade Register liaison

- Post-incorporation compliance management, including annual reporting

- Corporate bank account introduction assistance

- Support with Business ID (Y-tunnus) registration

Reach out to our team at Expanship Finland to discuss your structure.

Frequently Asked Questions (FAQ)

The private limited company (Osakeyhtiö / Oy) is the dominant corporate form, primarily because it combines limited liability with a single-shareholder minimum and a relatively straightforward registration process through the PRH. Its structural flexibility makes it suitable for businesses ranging from early-stage startups to established domestic trading firms.

A branch (Sivuliike) has no separate legal personality — the foreign parent bears full liability for its obligations — whereas an Oy is an independent legal entity subject to Finnish corporate income tax at 20%. Compliance requirements for a branch are lighter in terms of share capital, but the parent company's financial statements must also be filed with the PRH.

Among registered structures, the general partnership (Avoin yhtiö / Ay) discloses partner identities through the Trade Register, as does every other Finnish entity — public disclosure of beneficial owners is required under the Act on the Register of Beneficial Owners (758/2019). Nominee arrangements do not eliminate disclosure obligations under Finnish law.

A sole proprietorship (Toiminimi) and an Oy can both be established by one individual. General and limited partnerships, by contrast, require at least two partners under the Act on Partnerships (389/1988), making them structurally unavailable to a sole founder.

All entity types are open to non-residents, but foreigners establishing an Oy or a branch must appoint at least one resident representative within the European Economic Area, unless the PRH grants a specific exemption. A foreign national can serve as the sole shareholder and director of an Oy without holding Finnish residency, subject to that representative requirement.

Finnish law allows conversion of an Oy into a public limited company (Oyj) and vice versa under the Companies Act, without dissolving the entity. Conversion from a partnership into a limited company is also possible through a formal transformation process, though it requires re-registration with the PRH and settlement of outstanding partnership liabilities.

The Oy, Oyj, and cooperative (Osuuskunta) each hold separate legal personality, meaning they can contract, own assets, and incur liabilities independently of their members. General and limited partnerships, along with the sole proprietorship, do not form a distinct legal person — the founders remain personally liable to varying degrees.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.