Key Takeaways

- The Private Limited Company is the most commonly registered entity for both foreign and domestic investors in Ethiopia, offering closed membership and defined liability limits under the Commercial Code of Ethiopia.

- Company registration in Ethiopia falls under the joint authority of the Ethiopian Investment Commission and the Ministry of Trade and Regional Integration, which administers the Commercial Registration and Business Licensing Proclamation.

- Foreign firms requiring an in-country presence without establishing a separate legal entity can operate through a Branch Office, Representative Office, or Liaison Office under Ethiopian commercial law.

- Sole proprietorships and general partnerships are suited to small-scale domestic trade rather than cross-border operations, while Share Companies are reserved for larger ventures that require access to public capital.

Introduction to Entity Types in Ethiopia

Ethiopia sits in the Horn of Africa, bordered by Eritrea, Djibouti, Somalia, Kenya, South Sudan, and Sudan. It is an independent federal republic and one of the most populous countries on the African continent. For investors and business owners, understanding the types of business entities in Ethiopia is a necessary first step before committing to any structure.

Company registration falls under the authority of the Ethiopian Investment Commission (EIC) and the Ministry of Trade and Regional Integration, which oversees the Commercial Registration and Business Licensing Proclamation. The country operates a residence-based tax system, with corporate income subject to domestic rates rather than a zero-tax or purely territorial framework.

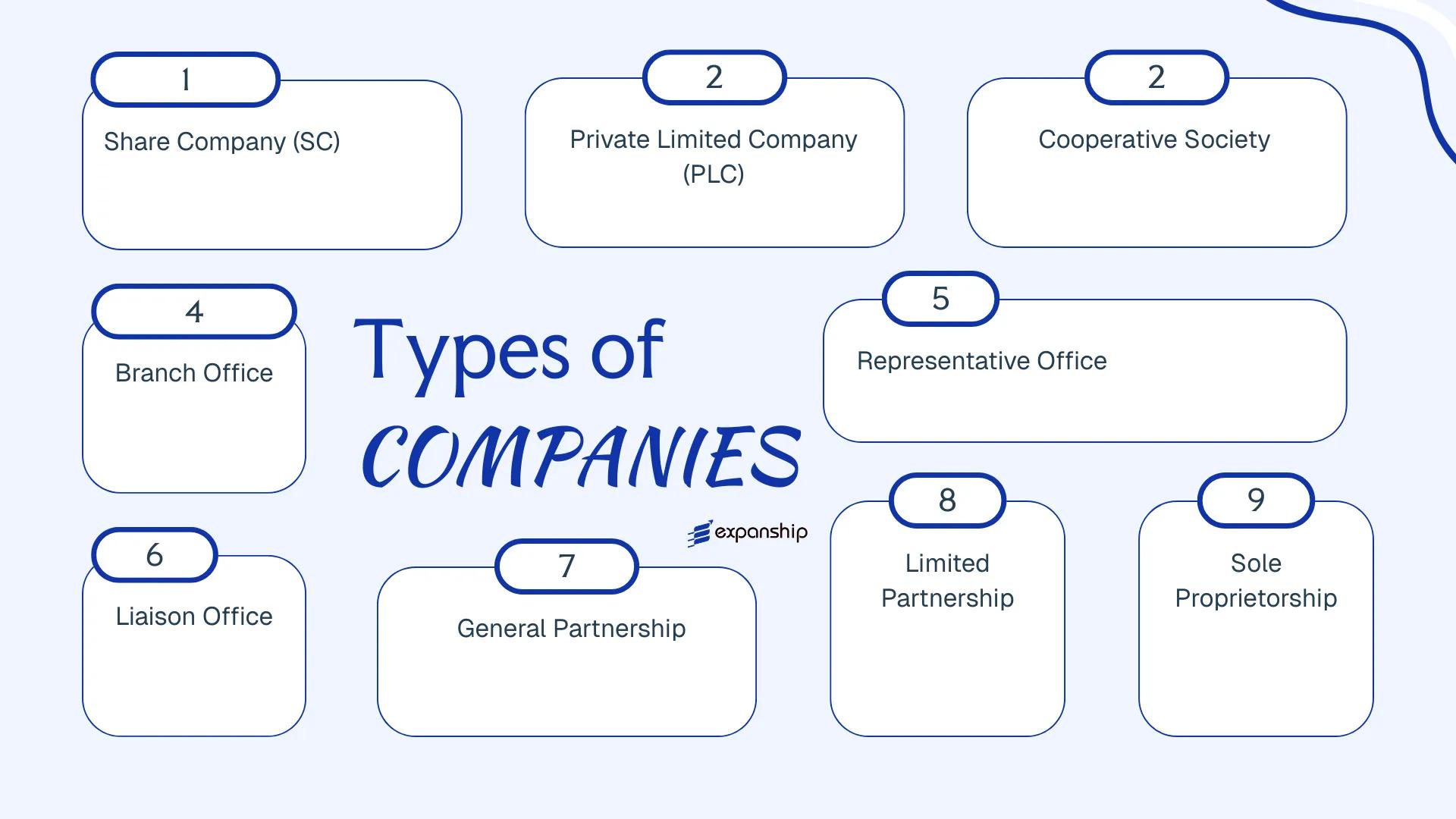

Available legal structures include the Share Company, Private Limited Company, General Partnership, Limited Partnership, Cooperative Society, Sole Proprietorship, Branch Office, Representative Office, and Liaison Office. Each carries distinct formation requirements, liability rules, and ownership conditions under Ethiopian commercial law. This article examines each structure in detail — covering its legal basis, minimum capital thresholds, governance requirements, and practical suitability for different types of investors.

An Overview of Business Structures in Ethiopia

Ethiopia's commercial law recognises several distinct entity types, each governed primarily by the Commercial Code of Ethiopia — most recently revised through Proclamation No. 1243/2021, which replaced the original 1960 Code. Every structure carries different implications for liability, ownership, and regulatory treatment, and the sections below examine each one in full detail.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Share Company (SC) | Public joint stock company | Limited to shares | Taxed | Yes | 5 shareholders | Ethiopian Investment Holdings / MoT | Commercial Code 1243/2021 |

| Private Limited Company (PLC) | Closed company | Limited to capital | Taxed | Yes | 2 members | Ministry of Trade (MoT) | Commercial Code 1243/2021 |

| General Partnership | Unincorporated firm | Unlimited, joint | Taxed | Yes | 2 partners | Ministry of Trade (MoT) | Commercial Code 1243/2021 |

| Limited Partnership | Hybrid partnership | Mixed liability | Taxed | Yes | 2 partners (1 general) | Ministry of Trade (MoT) | Commercial Code 1243/2021 |

| Sole Proprietorship | Individual trader | Unlimited | Taxed | Yes | 1 owner | Ministry of Trade (MoT) | Commercial Code 1243/2021 |

| Branch Office | Foreign entity extension | Parent liable | Taxed | Restricted | N/A | Ethiopian Investment Commission | Investment Proclamation 1180/2020 |

| Representative Office | Non-trading presence | Parent liable | Exempt | No | N/A | Ethiopian Investment Commission | Investment Proclamation 1180/2020 |

| Cooperative Society | Member-owned body | Limited | Taxed / Partial | Yes | Varies by type | Federal Cooperative Agency | Cooperative Societies Proclamation 985/2016 |

Each of these structures is examined in full in the sections below.

Share Company (SC) — Ethiopia's Public Joint Stock Company

Governed by the Commercial Code of Ethiopia (2021), Share Company SC formation Ethiopia follows the structure of a public joint stock company, where capital is divided into transferable shares and ownership can be held by a broad group of shareholders. The entity carries separate legal personality, meaning the company itself bears rights and obligations distinct from those of its shareholders.

Liability of each shareholder is capped at the value of their subscribed shares. This structure suits businesses seeking to raise capital from the public or institutional investors, and it is subject to oversight by the Ethiopian Investment Commission and relevant sectoral regulators.

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Share Company (SC) | Equivalent to a public joint stock company |

| Members | Shareholders; minimum 5 founders | No statutory maximum on shareholders |

| Directors | Board of Directors required | Minimum 3 board members |

| Local Presence | Registered office in Ethiopia required | Must maintain a physical address on record |

| Capital | Minimum ETB 50,000 (subscribed); 25% paid up at incorporation | Capital divided into shares of equal par value |

| Privacy | Shareholder register is maintained; public filings required | Lower privacy relative to a PLC |

Focus Points

- Taxation: Corporate income tax at 30%; VAT at 15% if turnover exceeds the registration threshold; dividend withholding tax applies; stamp duty on share transfers and instruments. See Ethiopian Revenue and Customs Authority (ERCA) for current rates.

- Annual Compliance: Audited financial statements required annually; general shareholder meetings must be held as prescribed by the Commercial Code.

- Treaty Access: Ethiopia has a limited network of double taxation agreements; treaty benefits depend on shareholder residency and structure.

- Conversion: An SC may be converted to another business form subject to shareholder resolution and re-registration with the relevant authority.

- Restrictions: Certain sectors restrict or prohibit foreign participation; the Ethiopian Investment Commission maintains a list of reserved activities.

Closing

An SC suits large-scale enterprises, joint ventures with institutional partners, or businesses intending to raise capital publicly, though the administrative and compliance burden is considerably higher than that of a PLC.

Share Companies are most appropriate for large enterprises or investor groups seeking broad share ownership, public capital raising, or eventual listing on the Ethiopian Securities Exchange.

Company Incorporation in Ethiopia

Incorporate a Share Company or other business structure in Ethiopia with end-to-end support from Expanship.

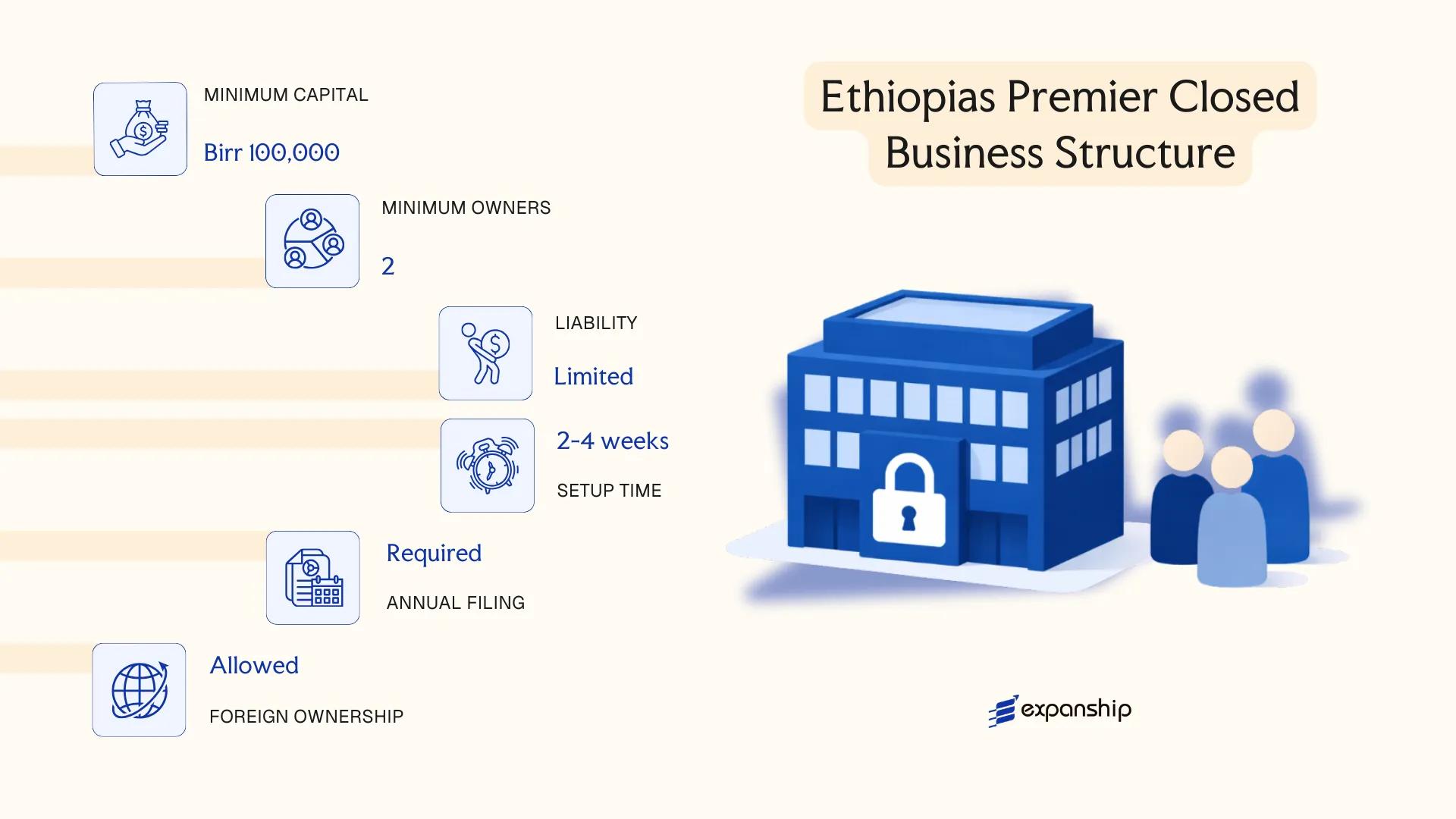

Private Limited Company (PLC) — Ethiopia's Premier Closed Business Structure

A Private Limited Company (PLC) in Ethiopia is governed by the Commercial Code of Ethiopia, which was substantially revised through Proclamation No. 1243/2021. The entity carries separate legal personality, meaning its debts and obligations are distinct from those of its members.

Liability is capped at each member's capital contribution, creating a structure that suits both domestic operators and foreign investors seeking a locally incorporated presence.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company (PLC) | Closed share structure; shares cannot be offered to the public |

| Members | Members (shareholders); 2 minimum, 50 maximum | Referred to as "members"; 100% foreign ownership permitted in most sectors |

| Management | Manager(s) appointed by members | No board requirement for smaller PLCs; at least one manager must be designated |

| Local Presence | Registered office address in Ethiopia required | A physical or legally registered address; no mandatory resident agent under general company law |

| Capital | ETB 15,000 minimum paid-up capital (general rule) | Sector-specific investment thresholds set by the Ethiopian Investment Commission may apply |

| Privacy | Member details filed with the Ethiopian Registrar of Companies | Register is not fully public in the manner of common law jurisdictions, but disclosures are made on registration |

Focus Points

- Taxation: Corporate income tax applies at 30% on net profit; VAT at 15% applies once turnover exceeds the registration threshold; withholding tax obligations arise on dividends, service payments, and imports; stamp duty applies to certain instruments including the memorandum of association.

- Annual Compliance: Annual financial statements must be filed; audit requirements apply where thresholds are met under the Commercial Code.

- Restrictions: Shares may not be transferred without member consent as prescribed in the memorandum; public offering is prohibited.

- Treaty Access: Ethiopia has a limited but growing double taxation agreement network; treaty access depends on beneficial ownership and residency of the member.

- Conversion: A PLC may convert to a Share Company if it meets the relevant capital and membership thresholds under Proclamation No. 1243/2021.

Closing

The PLC is the standard vehicle for trading, service, and holding operations in Ethiopia, offering defined liability protection within a privately held structure. Its restriction on public share issuance limits capital-raising options for businesses anticipating significant external investment rounds.

A PLC suits foreign investors and joint venture partners establishing a locally incorporated operational or holding entity in Ethiopia with a defined, closed membership.

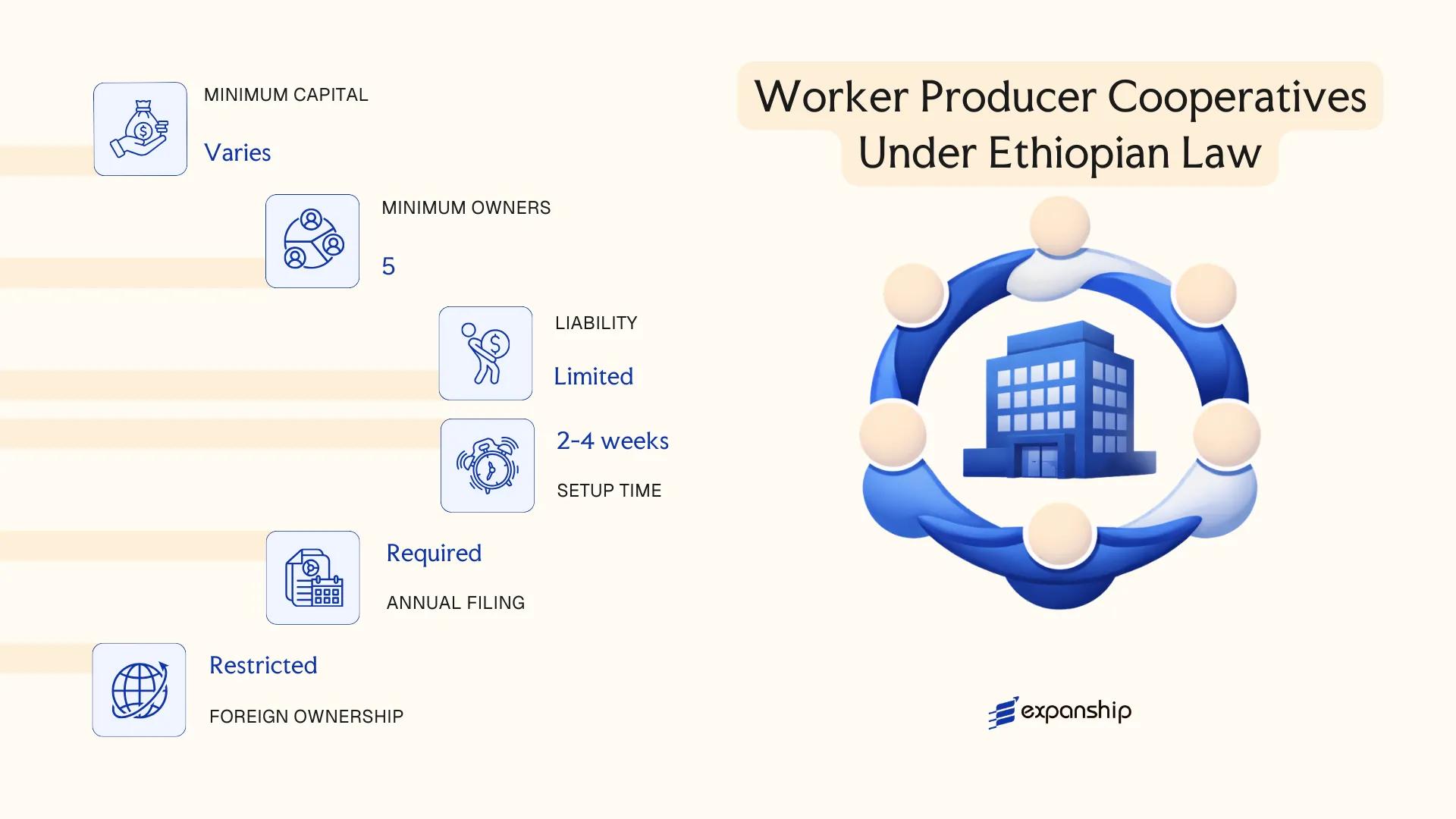

Cooperative Society — Worker & Producer Cooperatives Under Ethiopian Law

Cooperative society registration Ethiopia is governed primarily by the Federal Cooperative Societies Proclamation No. 985/2016, which repealed the earlier Proclamation No. 147/1998 and substantially updated the regulatory framework. A cooperative society registered under this law acquires separate legal personality upon registration, with liability of members generally limited to their share contributions.

Registration and oversight fall under the Federal Cooperative Commission (FCC) for federally registered cooperatives, while regional cooperatives bureaus administer entities operating within a single region.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Cooperative Society (incorporated body) | Separate legal personality upon registration with FCC or regional bureau |

| Members | Referred to as members; minimum 10 natural persons for a primary cooperative | Secondary (union) cooperatives require at least 2 primary cooperatives; tertiary (federation) requires at least 2 unions |

| Local Presence | Registered office within Ethiopia required | Must maintain a physical operational address in the area of registration |

| Capital | No statutory minimum capital prescribed by federal proclamation; members contribute shares as defined in bylaws | Share value and contribution schedules set in the cooperative's own bylaws |

| Privacy | Member register maintained internally; financial statements subject to audit and reporting to the FCC or regional bureau | Not publicly listed; limited public disclosure compared to a Share Company |

Focus Points

- Taxation: Cooperative societies are generally subject to corporate income tax at standard rates on business income; agricultural cooperatives may benefit from specific exemptions or reductions under Ethiopian tax law, and standard VAT registration thresholds apply to taxable supplies.

- Annual Compliance: Cooperatives must hold a general assembly at least once per year, submit audited financial statements to the relevant authority, and renew their business licence periodically.

- Restrictions: Membership is restricted to persons sharing a common economic interest; a cooperative cannot distribute profits in the same manner as a company — surplus is distributed as patronage refunds proportional to member transactions.

- Conversion: Proclamation No. 985/2016 does not provide a straightforward mechanism to convert a cooperative into a PLC or SC; restructuring would require dissolution and fresh incorporation.

- Foreign Participation: Foreign nationals are generally not permitted to form or join domestic cooperatives as members, limiting this structure to Ethiopian nationals or resident communities.

Sub-Types

Primary Cooperative

A primary cooperative is the base-level entity formed directly by individual members to pursue a shared economic activity such as agricultural production, savings and credit, or consumer supply. This is the most commonly formed cooperative type under Ethiopian law.

Cooperative Union (Secondary Cooperative)

Formed by at least two primary cooperatives, a union operates at a higher organisational tier to provide services — such as bulk marketing or input supply — to its member cooperatives rather than to individuals directly.

Cooperative Federation (Tertiary Cooperative)

A federation sits above unions and is formed by at least two cooperative unions, typically to coordinate sector-wide activities at a regional or national level. It does not engage directly with individual members.

Closing

Cooperative societies are suited to community-based productive activities, agricultural marketing, and savings-and-credit schemes where collective ownership and profit-sharing among members is the primary objective. The structure provides a legal framework for collective enterprise, though the restriction on profit distribution and the bar on foreign membership make it unsuitable for conventional commercial investment.

Worker cooperative Ethiopia law and producer cooperative Ethiopia formation structures are best suited for Ethiopian nationals forming agricultural, artisan, or savings-and-credit groups with a shared economic purpose.

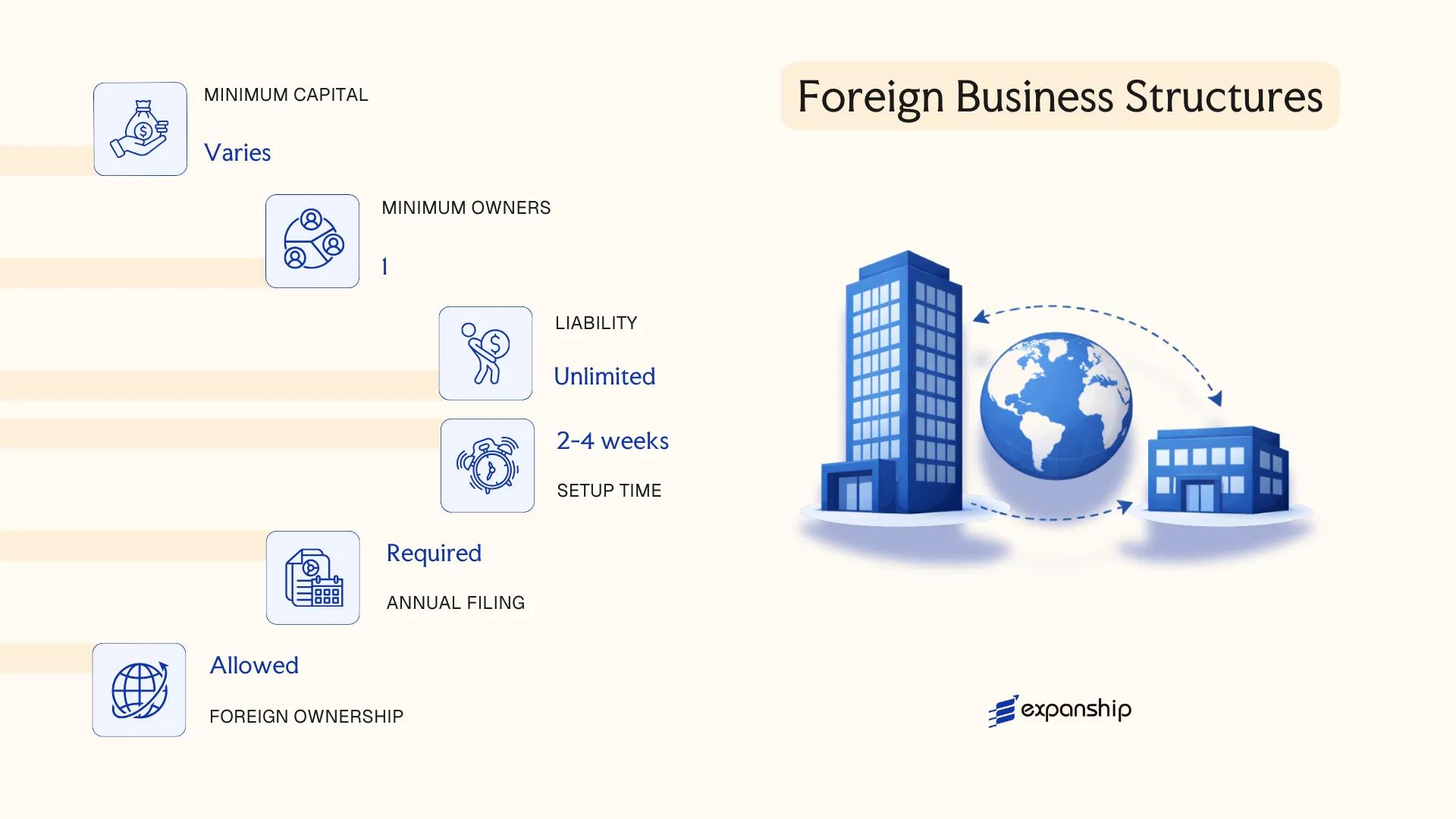

Foreign Business Structures [Branch Office, Representative Office, Liaison Office]

Foreign companies seeking to operate in Ethiopia without incorporating a locally registered entity have three structural options, each governed primarily by the Commercial Registration and Business Licensing Proclamation No. 980/2016 and further regulated by the Ethiopian Investment Commission (EIC) under the Investment Proclamation No. 1180/2020. None of these structures carry separate legal personality; the parent company retains full liability for their activities.

Completing a foreign branch office registration Ethiopia requires submission of the parent company's constitutive documents, audited financials, and a board resolution authorising the establishment, all filed with the EIC or the relevant regional bureau depending on sector.

Key Characteristics

| Requirement | Branch Office | Representative / Liaison Office |

|---|---|---|

| Legal Form | Extension of parent company; no separate legal personality | Extension of parent; non-commercial presence |

| Authorised Activities | Commercial operations, contracts, revenue generation | Promotion, research, coordination only — no revenue |

| Registered Agent | Not mandatory, but local contact address required | Local contact address required |

| Capital Requirement | No statutory minimum prescribed for branches | None |

| Privacy | Parent company documents become part of public registration file | Same |

| Governing Body | Parent company directors govern; local manager appointed | Local representative appointed by parent |

Focus Points

- Taxation: Branch profits are subject to 30% corporate income tax; VAT registration required if turnover exceeds the statutory threshold; withholding tax applies to remittances to the parent; representative offices with no taxable income generally fall outside the corporate tax net.

- Economic Substance: The appointed local manager must maintain a physical office address; purely postal registrations are not accepted.

- Annual Compliance: Annual renewal of the commercial registration certificate is required; audited accounts of the branch must be filed with the relevant authority.

- Treaty Access: Ethiopia has a limited network of double tax treaties; branch structures may not access treaty benefits as readily as locally incorporated subsidiaries.

- Restrictions: Foreign branches are barred from sectors reserved for domestic investors under the Investment Regulation No. 474/2020.

Sub-Types

Branch Office

A branch conducts full commercial activities, enters contracts, and generates revenue in its own operational capacity while remaining legally inseparable from the parent entity. It is the standard structure for foreign firms actively trading or delivering services.

Representative Office / Liaison Office

Both terms are used interchangeably in Ethiopian practice and refer to a non-revenue-generating presence used for market research, promotion, or coordination with local partners. No commercial transactions may be concluded through this structure.

Closing

Branch offices suit foreign firms requiring an operational footprint for service delivery or contract execution, with the key advantage of simpler setup compared to full incorporation; the primary limitation is unlimited parental liability for all branch obligations.

Foreign companies testing the Ethiopian market or executing a defined project contract without committing to a locally incorporated subsidiary.

Partnership-Based Structures [General Partnership, Limited Partnership]

Governed by the Commercial Code of Ethiopia (Proclamation No. 1243/2021), partnerships are recognised as distinct legal entities separate from their members. General partnership formation Ethiopia follows a contractual model where all partners bear unlimited joint liability for the firm's obligations.

Unlike capital-heavy corporate structures, partnerships suit smaller operations or professional ventures where personal accountability is accepted as a trade-off for operational simplicity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Commercial partnership with separate legal personality | Registered under the Commercial Code 2021 |

| Members | General Partnership: minimum 2 partners, all with unlimited liability; Limited Partnership: minimum 1 general partner (unlimited liability) + 1 limited partner (liability capped at contribution) | No statutory maximum on partner count |

| Local Presence | Registered office address in Ethiopia required | Must be maintained for service of legal notices |

| Capital | No statutory minimum capital prescribed | Contributions defined by partnership agreement |

| Governing Document | Partnership agreement (contract of association) | Must be in writing and registered with the relevant trade bureau |

| Privacy | Partner names are disclosed in registration records | No confidentiality provisions under current law |

Focus Points

- Taxation: Partners are taxed individually on their share of profits under Schedule B or Schedule C income tax rules; the partnership itself is not subject to corporate income tax, though VAT registration applies if turnover exceeds the statutory threshold.

- Annual Compliance: Filing of annual accounts with the relevant regional trade bureau is required; failure to file can result in administrative penalties.

- Conversion: A partnership may be converted into a PLC or Share Company through a formal restructuring process under the Commercial Code.

- Restrictions: Foreign nationals may face sectoral restrictions on participation in partnerships operating in areas reserved for Ethiopian investors under the Investment Proclamation No. 1180/2020.

- Treaty Access: Partnerships generally do not independently access Ethiopia's double taxation agreements; treaty benefits flow through to individual partners based on their residence status.

Sub-Types

General Partnership (Ye-Wend Serategnoch Serat)

All partners hold equal management rights and bear unlimited personal liability for the partnership's debts. This structure is typically used by small trading firms or professional service providers where partners maintain active operational roles.

Limited Partnership (Ye-Limit Serat)

At least one general partner retains unlimited liability while one or more limited partners contribute capital without participating in management. Limited partners' exposure is confined to their agreed contribution, making this form suitable for investment arrangements where silent capital participation is preferred.

Closing

Partnerships under Ethiopian law are most appropriate for small domestic trading operations or professional service arrangements where the partners are known to each other and actively involved. The absence of a minimum capital requirement is a practical advantage, though unlimited personal liability for general partners remains a significant structural risk.

Best suited for small domestic businesses or professional ventures where two or more known individuals seek a simple, low-cost structure and are prepared to accept personal liability exposure.

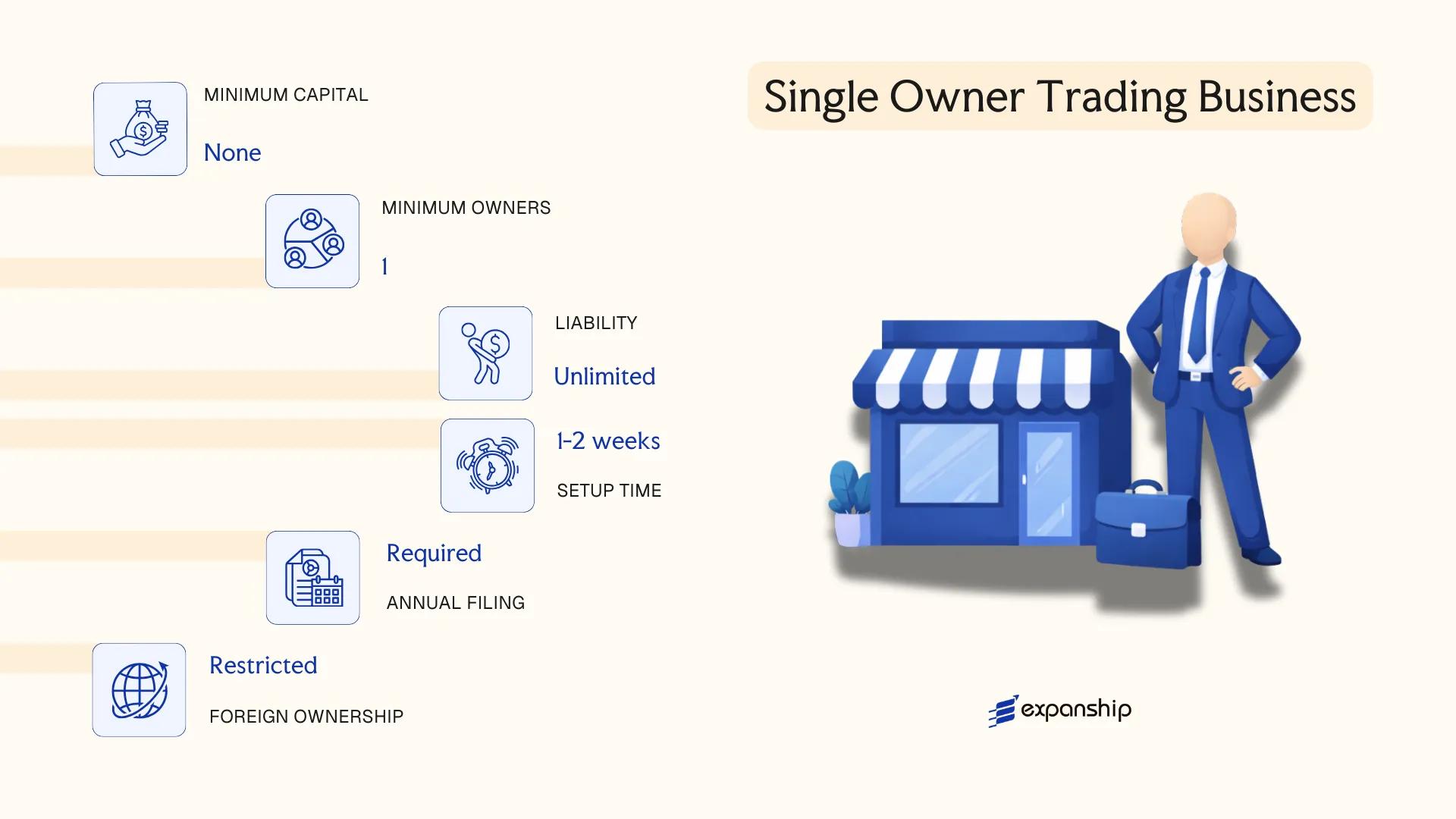

Sole Proprietorship — Single-Owner Trading Business in Ethiopia

Sole proprietorship registration Ethiopia follows the framework established under the Commercial Code of Ethiopia (Proclamation No. 1243/2021), which replaced the earlier 1960 Commercial Code. Under this structure, the business and its owner are legally the same entity — there is no separate legal personality, and the proprietor bears unlimited personal liability for all business obligations.

Registration is handled through the Ethiopian Investment Commission for foreign-involved activities, or through regional trade bureaus for domestic operators, depending on the nature of the business.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole trader | No separate legal personality from the owner |

| Members | Single proprietor | No minimum capital partners; one individual only |

| Local Presence | Registered business address required | Physical address within the operating region |

| Capital | No statutory minimum (ETB) | Capital adequacy may vary by sector license |

| Liability | Unlimited personal liability | Personal assets exposed to business debts |

| Privacy | Owner name appears on public trade register | No confidentiality of ownership |

Focus Points

- Taxation: Subject to personal income tax on business profit under a progressive schedule (up to 35%); VAT registration required if annual turnover exceeds ETB 1,000,000; withholding tax obligations apply on qualifying payments.

- Annual Compliance: Must renew the individual business license annually through the relevant trade bureau; bookkeeping records are required.

- Restrictions: Certain regulated sectors (banking, insurance, large-scale investment) are closed to sole traders; foreign nationals face additional restrictions on permitted activities.

- Conversion: Can be converted into a PLC or other registered entity as the business grows, subject to fresh registration requirements.

A sole proprietorship suits small-scale domestic trading, artisan services, and individual consultancy work where administrative simplicity outweighs the need for liability protection. The main advantage is the low setup burden; the principal drawback is full personal exposure to business liabilities.

Individual Ethiopian nationals operating small trading or service businesses who do not require external investment or liability separation.

How to Choose the Right Entity Type in Ethiopia

Understanding how to choose a business structure in Ethiopia requires more than matching a company type to a general description. The structure you register determines your liability exposure, tax treatment, foreign ownership eligibility, and ongoing compliance obligations under the Commercial Registration and Business Licensing Proclamation No. 980/2016.

Why Your Entity Choice Matters

Selecting the wrong structure carries concrete legal and financial consequences:

- Registering a representative office to conduct direct commercial transactions violates its permitted scope under Ethiopian law, which restricts such offices to promotional activities only — this can result in license cancellation.

- Choosing a structure ineligible under the Investment Proclamation for the sector you intend to enter means your business cannot lawfully operate in that sector, regardless of registration status.

- Forming a Share Company when your ownership group is small and closed adds mandatory audit requirements and minimum capital thresholds that a Private Limited Company would not impose.

- Selecting a general partnership when your business carries significant liability risk exposes all partners to unlimited personal liability for firm debts.

Key Factors to Consider

- Business Activity: Regulated sectors such as banking, insurance, and telecommunications require specific entity forms under sector-specific proclamations, which override general commercial law.

- Ownership Structure: A PLC caps shareholders at 50, making it unsuitable for businesses anticipating broad investor participation or eventual public capital raising.

- Foreign Ownership: Your eligibility to hold equity depends on whether your sector appears on the investment reservations list administered by the Ethiopian Investment Commission.

- Minimum Capital Requirements: Different structures carry different paid-up capital thresholds, which directly affect how much capital must be committed at registration.

- Liability Exposure: Whether your principals can tolerate unlimited personal liability determines whether a partnership structure is viable or a limited liability entity is necessary.

- Exit and Conversion: Not all Ethiopian entity types permit straightforward conversion or redomiciliation, so your anticipated exit path should inform the initial structure chosen.

Compliance Services for Companies in Ethiopia

Maintain your legal standing in Ethiopia with ongoing compliance support, including annual filings, license renewals, and regulatory reporting.

Conclusion

Selecting the right structure is the first substantive decision in any Ethiopia company incorporation process. The Private Limited Company remains the most commonly registered entity among foreign investors and domestic operators alike, given its closed membership structure and defined liability limits under the Commercial Code of Ethiopia. Share Companies suit larger ventures requiring public capital access. Branch and liaison offices serve foreign firms that need a presence without establishing a separate legal entity. Sole proprietorships and general partnerships fit small-scale domestic trade rather than cross-border operations.

Regulated by the Ethiopian Investment Commission and the Ministry of Trade and Regional Integration, the registration framework has undergone notable procedural reform in recent years, with ongoing efforts toward treaty expansion and digitized compliance systems. Your choice of entity will carry direct consequences for ownership rights, tax exposure, and operational scope throughout the life of the business. Expanship's team works with each of these structures across the full formation and compliance cycle.

How Expanship Can Assist You

Expanship Ethiopia company registration services cover the full range of entities discussed in this blog — from Private Limited Companies and Share Companies to Branch Offices and Representative Offices. Each structure carries distinct registration requirements under the Commercial Registration and Business Licensing Proclamation, and filings are processed through the Ethiopian Investment Commission or the relevant regional trade bureau, depending on your business type.

Across those processes, Expanship handles the operational and administrative side on your behalf:

- Document preparation and notarization for submission to Ethiopian authorities

- Registered agent and local office address provision

- Government filing and liaison with the Commercial Registration office

- Post-incorporation compliance, including annual renewal and statutory reporting

- Banking introduction assistance for corporate account opening in Ethiopia

- Ongoing registered office maintenance

Ready to move forward? Contact [Expanship Ethiopia](et/contact-us) to discuss your specific structure and timeline.

Frequently Asked Questions (FAQ)

The Private Limited Company (PLC) is the most frequently registered entity structure, primarily because it permits as few as two shareholders while capping liability at each member's capital contribution. Its relatively straightforward registration process through the Ethiopian Investment Commission or regional trade bureaus makes it the default choice for small to mid-sized domestic ventures.

A foreign company's branch office operates as an extension of its parent and does not constitute a separate legal entity under Ethiopian law, whereas a PLC is an independently incorporated firm with its own legal personality. Both are subject to corporate income tax at the standard rate, but a branch has no local shareholders and cannot independently own assets in its own name.

The Private Limited Company does not require public disclosure of shareholder details in a searchable public registry in the same manner that a Share Company's prospectus-related documents may be reviewed. Nominee arrangements are not formally codified under the Commercial Code of Ethiopia, so privacy levels remain limited across all structures.

No. A Sole Proprietorship and a one-person structure are possible for individual traders, but a PLC requires a minimum of two shareholders, and a Share Company requires at least five. General and Limited Partnerships require at least two partners by definition under the Commercial Code.

Foreigners may establish a PLC, Share Company, Branch Office, or Representative Office, subject to sector restrictions under the Investment Proclamation No. 1180/2020. Certain sectors remain reserved for Ethiopian nationals, so the permitted activities must be verified against the current investment schedule before incorporation proceeds.

Conversion between entity types is not explicitly prohibited, though the Commercial Code of Ethiopia does not provide a streamlined statutory conversion mechanism equivalent to those in some other jurisdictions. In practice, restructuring typically involves dissolving the existing entity and re-registering under the target structure, with all associated regulatory filings completed afresh.

No. Sole Proprietorships and General Partnerships do not confer separate legal personality, meaning owners bear personal liability for business obligations. A PLC, Share Company, and Cooperative Society each carry distinct legal personality under the Commercial Code, insulating members from direct liability beyond their stated contributions.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.