Key Takeaways

- Dominican Republic commercial entities are governed primarily by Law No. 479-08 on Commercial Companies and Individual Limited Liability Enterprises, as amended by Law No. 31-11, with registration administered through the Mercantile Registry via the Chamber of Commerce and Production network.

- The Sociedad Anónima Simplificada (S.A.S.) provides the most flexible governance framework among Dominican Republic entity types, making it the preferred structure for startups and mid-sized ventures.

- Partnership structures such as the Sociedad en Nombre Colectivo and Sociedad en Comandita Simple impose unlimited personal liability on partners, which limits their practical use in commercial settings.

- Among small and medium enterprises, the Sociedad de Responsabilidad Limitada (S.R.L.) is the most frequently registered entity type in the Dominican Republic.

Introduction to Entity Types in Dominican Republic

Occupying the eastern two-thirds of Hispaniola in the Caribbean, the Dominican Republic shares its island with Haiti and sits between Cuba to the west and Puerto Rico to the east. It is an independent sovereign nation and a member of CARICOM as an observer state, operating under a civil law system derived largely from the Napoleonic Code.

Company registration falls under the jurisdiction of the Registro Mercantil, administered through the Chamber of Commerce and Production network. Incorporation filings are governed primarily by Law No. 479-08 on Commercial Companies and Individual Limited Liability Enterprises, as amended by Law No. 31-11. The Dominican Republic operates a territorial tax system, meaning resident companies are taxed on domestically sourced income.

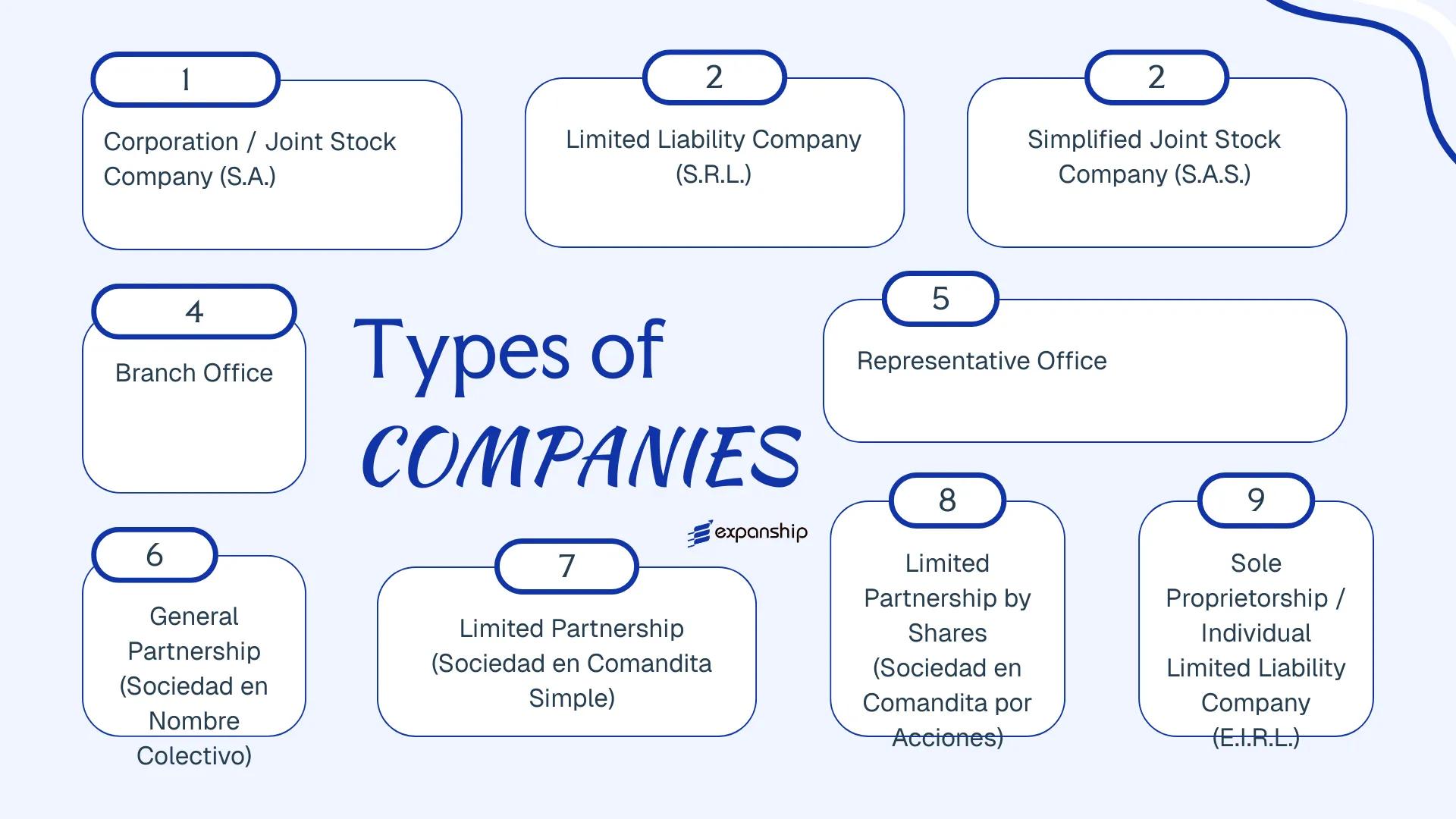

Several business entity types Dominican Republic law recognizes are available to local and foreign investors alike:

- Sociedad Anónima (S.A.)

- Sociedad de Responsabilidad Limitada (S.R.L.)

- Sociedad Anónima Simplificada (S.A.S.)

- Sociedad en Nombre Colectivo

- Sociedad en Comandita Simple

- Sociedad en Comandita por Acciones

- Empresa Individual de Responsabilidad Limitada (E.I.R.L.)

- Branch Office

- Representative Office

Each of these Dominican Republic company structures carries distinct legal, liability, and operational implications, which the sections below examine in full detail.

An Overview of Business Structures in Dominican Republic

Dominican corporate law recognizes several distinct entity types, each governed primarily by Law No. 479-08 on Commercial Companies and Individual Limited Liability Enterprises, as amended by Law No. 31-11. Each structure carries different implications for liability, governance, and ownership — the sections that follow examine each one in full.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima (S.A.) | Corporation | Limited | Taxed | Yes | 2 shareholders | Registro Mercantil | Law 479-08 |

| Sociedad de Responsabilidad Limitada (S.R.L.) | LLC | Limited | Taxed | Yes | 2 partners | Registro Mercantil | Law 479-08 |

| Sociedad Anónima Simplificada (S.A.S.) | Simplified corporation | Limited | Taxed | Yes | 1 shareholder | Registro Mercantil | Law 479-08 |

| Branch Office | Foreign branch | Parent liable | Taxed | Yes | N/A | Registro Mercantil | Law 479-08 |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | No | N/A | Registro Mercantil | Law 479-08 |

| Sociedad en Nombre Colectivo | General partnership | Unlimited | Taxed | Yes | 2 partners | Registro Mercantil | Law 479-08 |

| Sociedad en Comandita Simple | Limited partnership | Mixed | Taxed | Yes | 2 partners | Registro Mercantil | Law 479-08 |

| Sociedad en Comandita por Acciones | Share-based partnership | Mixed | Taxed | Yes | 2 partners | Registro Mercantil | Law 479-08 |

| Empresa Individual de Responsabilidad Limitada (E.I.R.L.) | Sole proprietorship | Limited | Taxed | Yes | 1 owner | Registro Mercantil | Law 479-08 |

Each of these structures is examined in full in the sections below.

Sociedad Anónima (S.A.)

The Sociedad Anónima Dominican Republic S.A. structure is governed primarily by the General Commercial Companies and Individual Limited Liability Enterprises Law (Law No. 479-08), as amended by Law No. 31-11. The entity carries separate legal personality distinct from its shareholders, meaning the firm's obligations do not extend to the personal assets of its owners.

Capital is divided into transferable shares, making this structure suitable for businesses that anticipate bringing in investors or eventually listing on a regulated exchange. Shareholder liability is capped at the value of their subscribed shares.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima (S.A.) | Joint stock company with transferable shares |

| Members | Minimum 2 shareholders; no statutory maximum | Shareholders may be individuals or legal entities; foreign nationals permitted |

| Directors | Minimum 3 directors if no supervisory board; or minimum 1 if a supervisory board is established | Directors need not be Dominican residents |

| Local Presence | Registered office in the Dominican Republic required | No mandatory resident director, but a local registered address must be maintained |

| Share Capital | Minimum RD$30,000,000 (approx. USD 500,000) for publicly traded; general minimum DOP 100,000 for private S.A. | Capital divided into nominative or bearer shares (bearer shares now restricted) |

| Privacy | Shareholder register maintained internally; not fully public | Beneficial ownership disclosure required under AML regulations |

Focus Points

- Taxation: Corporate income tax is levied at 20% on net taxable income; VAT (ITBIS) applies at 18% on goods and services; dividends distributed to non-residents are subject to a 10% withholding tax; no stamp duty on standard share transfers.

- Annual Compliance: Audited financial statements required annually; annual shareholders' meeting mandatory; tax returns filed with the DGII (Dirección General de Impuestos Internos).

- Treaty Access: The Dominican Republic has a limited tax treaty network; S.A. entities may access agreements where in force, subject to beneficial ownership conditions.

- Share Transferability: Shares are freely transferable by default, though the bylaws may impose restrictions on private S.A. entities.

- Conversion: An S.A. may be converted into another commercial form, including an S.R.L. or S.A.S., by shareholder resolution and formal registration with the Mercantile Registry.

Closing

The S.A. is used primarily for large-scale trading operations, holding structures, and ventures requiring equity participation from multiple investors. Its transferable share structure supports capital-raising activity, though the higher minimum capital threshold and mandatory multi-director governance add administrative weight relative to simpler forms.

The S.A. is best suited for medium-to-large businesses, joint ventures, or investor-backed companies where share transferability and formal governance are operational priorities.

Company Incorporation in the Dominican Republic

Expanship assists with the full S.A. formation process, from name registration to Mercantile Registry filing.

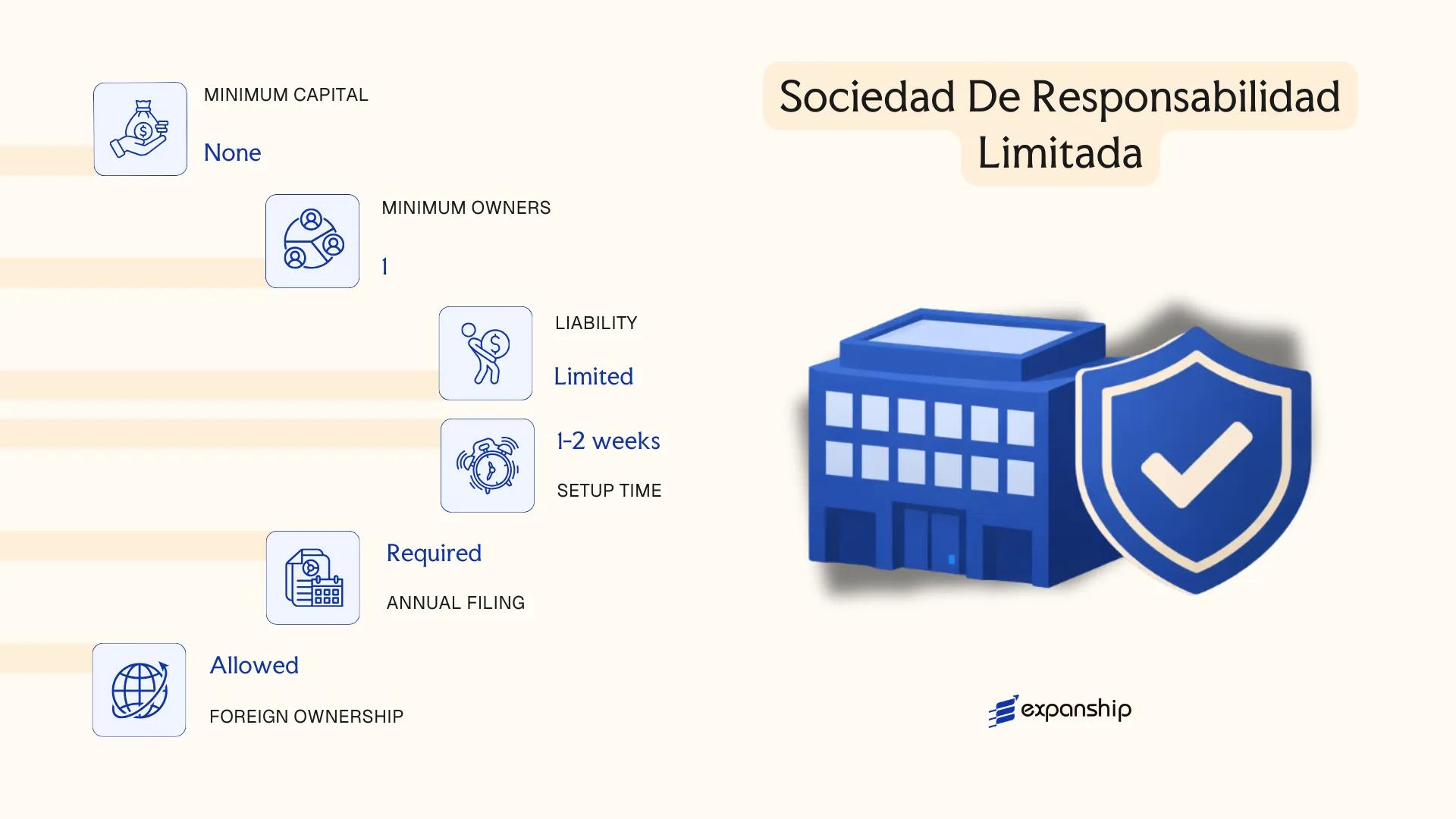

Sociedad de Responsabilidad Limitada (S.R.L.)

The Sociedad de Responsabilidad Limitada Dominican Republic framework is governed by Law No. 479-08 on Commercial Companies and Individual Limited Liability Enterprises, as amended by Law No. 31-11. Under this statute, the S.R.L. carries separate legal personality, meaning the entity holds rights and obligations distinct from its members.

Liability exposure for each member is capped at the value of their capital contribution. This structure makes the S.R.L. a hybrid form — combining corporate-style liability protection with a more flexible, privately held ownership arrangement that does not issue publicly tradeable shares.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad de Responsabilidad Limitada | Governed by Law No. 479-08 as amended |

| Members | 2 to 50 members (socios) | Cannot issue shares to the general public |

| Management | One or more managers (gerentes) | Need not be members or residents |

| Local Presence | Registered address in Dominican Republic required | Registered agent not mandated by statute but advisable in practice |

| Capital | No statutory minimum; denominated in Dominican Pesos (DOP) | Divided into quotas (cuotas), not shares |

| Privacy | Member details filed with the Mercantile Registry | Not publicly searchable in a centralised online database |

Focus Points

- Taxation: Subject to 27% corporate income tax on net profits; VAT (ITBIS) applies at 18% on applicable transactions; dividend withholding tax of 10% on distributions to non-residents; no stamp duty on routine commercial transactions.

- Annual Compliance: Annual financial statements must be filed; the entity must maintain accounting records in accordance with local standards.

- Transfer Restrictions: Quota transfers to third parties require prior consent from the majority of existing members, as established under Law No. 479-08.

- Treaty Access: The Dominican Republic has a limited double taxation treaty network; S.R.L. entities are generally treated as tax residents and may access applicable treaties subject to substance requirements.

- Conversion: An S.R.L. may be converted into an S.A. or S.A.S. through a formal restructuring process filed before the Mercantile Registry.

Closing

The S.R.L. suits small to mid-sized trading operations and family-owned businesses where ownership is closely held and public capital markets are not required. The quota-based structure simplifies ownership management, though the 50-member cap and transfer consent requirement can constrain growth or investor entry.

Best suited for closely held businesses with a defined group of founders or partners who do not anticipate requiring external equity investment or public shareholding.

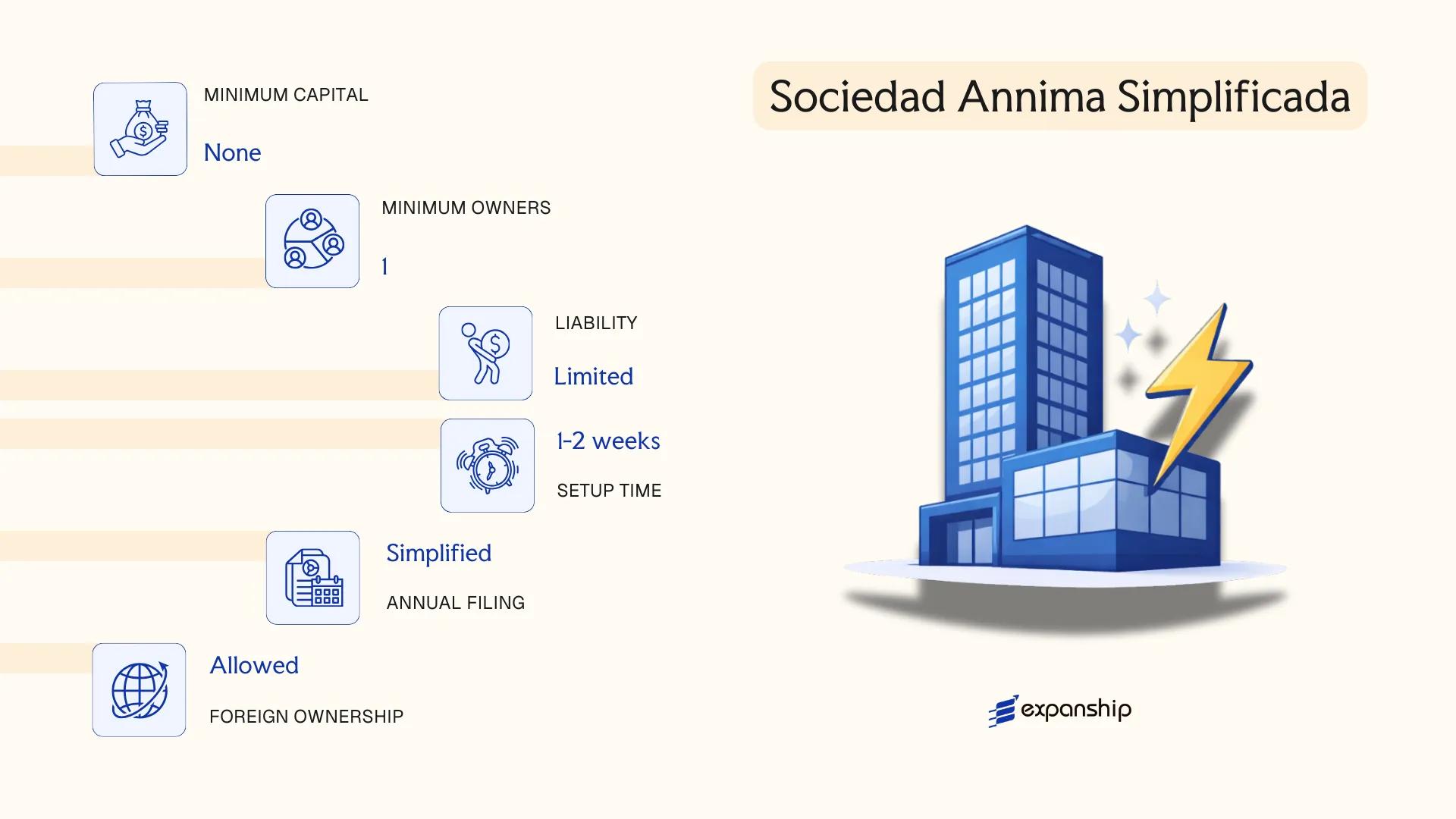

Sociedad Anónima Simplificada (S.A.S.)

The Sociedad Anónima Simplificada Dominican Republic framework was introduced under Law No. 31-11 of 2011, which amended the Commercial Companies Law to create a more accessible corporate structure for small and medium-sized businesses. The S.A.S. carries full legal personality, separate from its shareholders, with liability limited to each member's capital contribution.

Structurally, this entity functions as a hybrid: it borrows the limited liability protections of the S.A. while permitting considerably more contractual freedom in its governance documents. Shareholders of an S.A.S. company in the Dominican Republic can define many internal rules through the company's statutes rather than relying solely on statutory defaults.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima Simplificada | Hybrid structure with flexible governance |

| Members | Shareholders; minimum 1, maximum not prescribed by law | Can be 100% foreign-owned |

| Management | Designated by statutes; no mandatory board structure | Greater flexibility than the S.A. |

| Local Presence | Registered address in Dominican Republic required | No mandatory resident director |

| Share Capital | No statutory minimum; denominated in Dominican pesos | Freely determined in statutes |

| Privacy | Shareholder registry not publicly disclosed | Beneficial ownership rules may apply |

Focus Points

- Taxation: Subject to standard corporate income tax at 27%, ITBIS (VAT) at 18%, dividend withholding tax at 10%, and applicable stamp duties on registered documents.

- Annual Compliance: Annual financial statements and tax filings required with the DGII (Dirección General de Impuestos Internos); mercantile registry renewal with the CCPSD.

- Treaty Access: Eligible to access the Dominican Republic's limited tax treaty network, subject to substance requirements.

- Conversion: Can be converted into another recognized commercial form through a shareholder resolution and re-registration with the Registro Mercantil.

Closing

The S.A.S. suits trading operations, startup ventures, and holding structures where governance flexibility matters more than the formality of a full S.A. Its primary constraint is limited public market access — shares cannot be offered to the general public.

Best suited for entrepreneurs, SMEs, and foreign investors seeking a single-shareholder or closely held structure with minimal governance formality.

Foreign Entities in the Dominican Republic [Branch Office, Representative Office]

Foreign companies seeking a physical presence without incorporating a local entity have two primary options: the branch office and the representative office. Establishing a foreign company branch office Dominican Republic is governed by Law 479-08 on Commercial Companies and Individual Limited Liability Enterprises, which sets out the registration requirements for foreign entities operating within the territory.

A branch (Sucursal) is not a separate legal entity — it is an extension of its parent company, which bears full liability for the branch's obligations. A representative office, by contrast, is restricted to promotional and liaison activities and cannot generate local revenue.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Liability | Parent company bears unlimited liability | Parent company bears unlimited liability |

| Local Presence | Registered agent and local address required | Registered agent and local address required |

| Capital | No statutory minimum; parent's capital is referenced | No statutory minimum |

| Revenue Generation | Permitted | Not permitted |

| Registry | Mercantile Registry (Registro Mercantil) | Mercantile Registry |

Focus Points

- Taxation: Branch profits are subject to the standard 27% corporate income tax; VAT (ITBIS) at 18% applies to taxable transactions; withholding taxes apply to remittances to the parent company.

- Economic Substance: No formal substance regime, but the branch must maintain demonstrable local operations to support its registered activities.

- Annual Compliance: Annual renewal with the Mercantile Registry and filing of audited financial statements reflecting the branch's Dominican operations are required.

- Treaty Access: Access to tax treaties depends on whether the parent's home jurisdiction has a treaty with the Dominican Republic; the branch itself does not independently qualify.

- Restrictions: Representative offices are legally prohibited from signing commercial contracts or invoicing clients directly.

Sub-Types

Branch Office (Sucursal)

A Sucursal is the standard operational structure for a foreign company conducting active business locally. It must register with the Mercantile Registry and appoint a local legal representative with authority to act on the parent's behalf.

Representative Office (Oficina de Representación)

This structure is limited to market research, promotion, and liaison functions. It cannot execute contracts or generate taxable income, making it unsuitable for firms requiring local sales or service delivery.

Both structures suit foreign firms testing the market or managing regional operations without committing to full local incorporation. The branch offers operational flexibility, while the absence of a liability shield for the parent company is a significant exposure to weigh carefully.

Foreign companies seeking operational presence or market entry without incorporating a new local entity — particularly multinationals managing Latin American operations from a single parent structure.

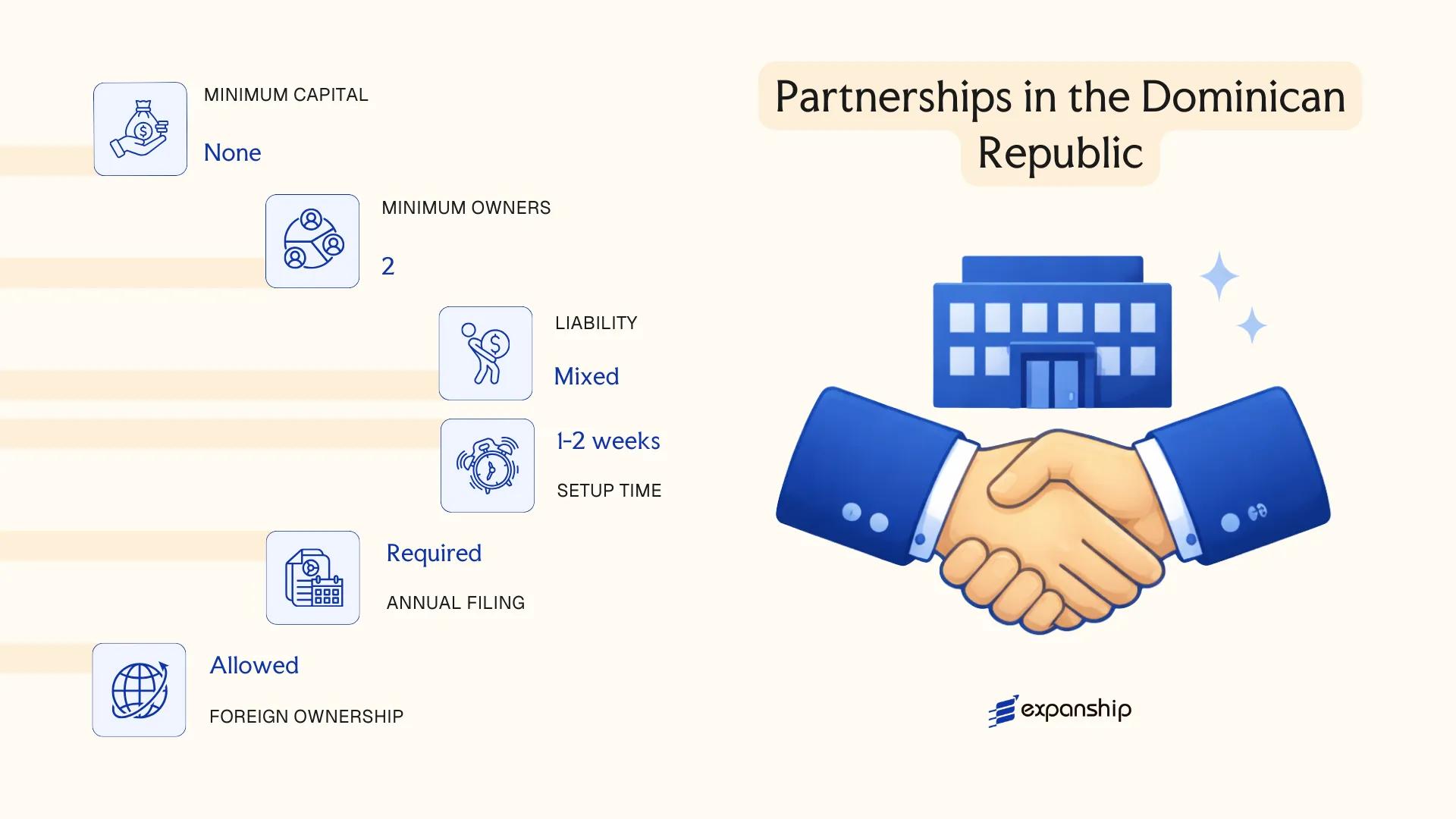

Partnerships in the Dominican Republic [Sociedad en Nombre Colectivo, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones]

Three partnership structures are available under the Dominican Commercial Code and Law 479-08 on Commercial Companies: the Sociedad en Nombre Colectivo (general partnership), the Sociedad en Comandita Simple (limited partnership), and the Sociedad en Comandita por Acciones (limited partnership by shares). Each carries distinct liability profiles. Partnerships in the Dominican Republic Sociedad en Comandita formations are less common than capital-based structures, largely because general partners in these forms bear unlimited personal liability for company debts.

Unlike the S.A. or S.R.L., these entities are not routinely used for standard commercial activity. Their structures suit specific arrangements where personal accountability or hybrid capital mechanisms are intentional design features rather than incidental ones.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Partnership (Sociedad en Nombre Colectivo / Sociedad en Comandita Simple / Sociedad en Comandita por Acciones) | Governed by Law 479-08 and the Commercial Code |

| Members | Referred to as socios (partners); general partners bear unlimited liability | Sociedad en Comandita structures include both general (gestores) and limited (comanditarios) partners |

| Minimum Partners | 2 partners minimum across all three types | No statutory maximum specified under general rules |

| Local Presence | Registered office in the Dominican Republic required; registration with the Mercantile Registry (Registro Mercantil) mandatory | Sociedad en Comandita por Acciones must also register with the Superintendencia de Valores if shares are publicly offered |

| Capital | No statutory minimum capital for Sociedad en Nombre Colectivo or Sociedad en Comandita Simple; Sociedad en Comandita por Acciones issues shares | Denominated in Dominican Pesos (DOP) |

| Privacy | Partner names appear in public registry filings | No beneficial ownership confidentiality available |

Focus Points

- Taxation: Subject to corporate income tax at 27%, VAT (ITBIS) at 18% on applicable transactions, and withholding taxes on dividends (10%) and interest paid abroad; no partnership-level tax transparency applies.

- Annual Compliance: Annual renewal of Mercantile Registry registration required; financial statements must be maintained in accordance with Dominican accounting standards.

- Treaty Access: The Dominican Republic has a limited tax treaty network; partnership structures do not inherently confer additional treaty benefits.

- Restrictions: General partners in a Sociedad en Nombre Colectivo cannot transfer their interest without unanimous partner consent.

- Conversion: Conversion to an S.R.L. or S.A. is possible but requires a formal restructuring process before the Registro Mercantil.

Sub-Types

Sociedad en Nombre Colectivo

All partners carry joint and unlimited personal liability for the firm's obligations. This structure is primarily used by professional service providers or family-owned businesses where partners accept mutual accountability as a deliberate arrangement.

Sociedad en Comandita Simple

This form separates active management (general partners with unlimited liability) from passive investors (limited partners whose liability is capped at their capital contribution). It suits arrangements where outside investors wish to participate financially without taking on operational responsibility.

Sociedad en Comandita por Acciones

The Sociedad en Comandita por Acciones DR structure introduces share capital into the limited partnership framework, allowing the limited partners' interests to be represented by transferable shares. This makes it marginally more flexible for capital-raising than the Sociedad en Comandita Simple, though it remains rarely used in practice.

Closing

Partnership structures in the Dominican Republic are most relevant to professional practices, family businesses, and arrangements requiring a clear separation between active managers and passive capital contributors. The primary limitation across all three forms is the unlimited personal liability carried by at least one class of partner, which makes them unsuitable where liability protection is a priority.

These structures are best suited to closely-held family businesses or professional partnerships where the partners involved are willing to accept personal liability as part of the arrangement.

Sole Proprietorship (Empresa Individual de Responsabilidad Limitada)

The Empresa Individual de Responsabilidad Limitada (EIRL) is the Dominican Republic's statutory sole proprietorship structure, governed by Law No. 479-08 on Commercial Companies and Individual Limited Liability Enterprises, as amended by Law No. 31-11. Unlike a general sole proprietorship, the EIRL holds separate legal personality from its owner, which means the individual's personal assets are shielded from business liabilities up to the limits prescribed by law.

Registration is filed with the Registro Mercantil through the Cámara de Comercio y Producción of the relevant province. This structure suits individuals operating independently who require legal separation between personal and commercial patrimony without forming a multi-member company.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Individual Limited Liability Enterprise | Separate legal personality from owner |

| Members | Single proprietor (natural person only) | Legal entities cannot be the sole proprietor of an EIRL |

| Local Presence | Registered commercial address required | Must be registered with the provincial Cámara de Comercio |

| Capital | Denominated in Dominican Pesos (DOP); no statutory minimum specified under Law 479-08 | Capital must be declared at registration |

| Privacy | Proprietor's name and capital appear in public Registro Mercantil records | Limited confidentiality |

Focus Points

- Taxation: Subject to corporate income tax at 27%, ITBIS (VAT) at 18% on applicable goods and services, and withholding tax obligations on payments to third parties; no special tax regime applies by virtue of the EIRL form alone.

- Annual Compliance: Must file annual tax returns with the Dirección General de Impuestos Internos (DGII) and renew the Registro Mercantil annually.

- Conversion: An EIRL can be converted into a multi-member company (such as an SRL or SAS) through a formal notarial deed and re-registration process.

- Restrictions: Only natural persons may establish an EIRL; the structure cannot be used by foreign legal entities as a direct operating vehicle.

- Treaty Access: Access to Dominican Republic tax treaties depends on residency and activity, not the entity form itself.

Closing

The EIRL suits resident individuals running small to medium commercial or service operations who need liability separation without a partnership structure. The key advantage is personal asset protection within a single-owner framework; the primary limitation is that only natural persons qualify, excluding corporate shareholders entirely.

Best suited for Dominican-resident individuals seeking formal liability separation for a sole-operated business, particularly in trading or professional services.

How to Choose the Right Entity Type in Dominican Republic

Selecting how to choose a business entity in the Dominican Republic requires more than comparing registration fees — the structural decision has direct legal, tax, and operational consequences that are difficult to reverse once the company is active.

Why Your Entity Choice Matters

Choosing the wrong structure produces concrete problems, not abstract ones:

- A branch office operating beyond the scope of its registered activities under Law 479-08 can face administrative sanctions from the Registro Mercantil.

- Selecting a tax-exempt entity without access to the Dominican Republic's bilateral tax treaty network means withholding tax reductions available under those treaties cannot be claimed in the counterpart country.

- Forming an S.A. when a sole-owner consultancy structure would suffice imposes mandatory board requirements and annual shareholder obligations that increase compliance overhead unnecessarily.

- Choosing an entity that requires audited financial statements when your business does not meet the thresholds that justify that cost adds recurring professional fees without regulatory benefit.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors such as banking or insurance each require different entity types under Dominican law.

- Ownership Structure: Single-owner operations may suit an S.R.L. or S.A.S., while multi-party arrangements with complex governance needs point toward an S.A.

- Tax Objectives: Your need for treaty access, standard corporate tax treatment, or a specific incentive regime under laws such as Law 16-95 on Foreign Investment shapes which structure applies.

- Privacy Requirements: Public disclosure requirements at the Registro Mercantil vary by entity type and affect whether nominee arrangements are necessary.

- Exit Strategy: Not all Dominican entity types permit redomiciliation or conversion — confirm these options before incorporating if restructuring is anticipated.

The full text of Law 479-08 on Commercial Companies and Individual Limited Liability Enterprises governs formation requirements across all principal entity types and should be reviewed alongside professional legal advice.

Compliance Services for Companies in the Dominican Republic

Maintain good standing with annual filing obligations, registered agent requirements, and regulatory reporting under Dominican law.

Conclusion

Setting up a company in Dominican Republic means selecting from a well-defined set of structures governed primarily by Law No. 479-08 and its amendments. Each entity carries a distinct legal profile: the S.A. suits larger operations requiring capital market access; the S.R.L. fits closely held businesses with a fixed shareholder group; the S.A.S. offers the most flexible governance terms for startups and mid-sized ventures; branch offices serve foreign firms testing the market without establishing a separate legal person; and partnerships carry unlimited liability, making them uncommon in commercial practice.

The S.R.L. remains the most frequently registered structure among small and medium enterprises. Regulatory oversight from institutions such as the Mercantile Registry and the DGII continues to move toward digital processing, reflecting a broader modernization of corporate administration. Your choice of entity will shape everything from tax filing obligations to how profits are distributed and how future investors may participate.

How Expanship Can Assist You

Expanship's corporate services in the Dominican Republic cover the full incorporation process, from selecting the right entity structure to meeting the registration requirements set by the Registro Mercantil and the Cámara de Comercio y Producción. Whether your business suits an S.A.S. for its flexible governance or an S.R.L. for its shareholder protections, our team handles the procedural requirements specific to each structure.

From document preparation to post-incorporation obligations, Expanship supports your business at every stage:

- Document preparation, notarization, and legalization

- Registered agent and local office provision

- Filing with the Registro Mercantil and relevant government bodies

- Ongoing compliance management, including annual renewals

- Tax registration with the Dirección General de Impuestos Internos (DGII)

- Banking introduction assistance

Reach out to Expanship Dominican Republic to discuss your incorporation requirements directly.

Frequently Asked Questions (FAQ)

The Sociedad Anónima Simplificada (S.A.S.) has become the most frequently chosen structure since its introduction, primarily because it allows formation by a single shareholder and carries fewer administrative formalities than the traditional S.A. Its flexibility in governance and reduced capital requirements make it the default choice for small to mid-sized ventures.

Both structures offer limited liability and separate legal personality, but the S.A. requires a minimum of two shareholders and a more formal board structure, while the S.A.S. can be formed by one person with simplified statutes. Tax treatment under the Dirección General de Impuestos Internos (DGII) applies equally to both. The S.A. carries heavier ongoing compliance obligations, including mandatory auditor appointments at certain thresholds.

The S.R.L. and S.A.S. both offer relatively limited public disclosure compared to the S.A., as shareholder registers are maintained internally rather than filed in full public detail with the Registro Mercantil. Beneficial ownership information is, however, subject to reporting obligations under anti-money laundering regulations. Nominee arrangements are legally permissible but do not override disclosure requirements to regulatory authorities.

No. The Sociedad en Nombre Colectivo and both Comandita structures require at least two partners by their legal definition under Law 479-08. The S.A. also requires a minimum of two shareholders. The S.A.S. and the Empresa Individual de Responsabilidad Limitada (EIRL) are the only structures explicitly designed for sole formation.

Foreign nationals face no legal restriction on forming or owning a Dominican entity. An S.A.S. or S.R.L. can be incorporated with 100% foreign ownership, and there is no residency requirement for shareholders. A local registered address is required, and certain regulated sectors may impose additional conditions through sector-specific legislation.

Conversion between entity types is permitted under Dominican corporate law, most commonly from an S.R.L. to an S.A. or S.A.S. as a business scales. The process requires shareholder approval, updated statutes, and re-registration with the Registro Mercantil. Not all conversions follow a simplified path; some require full dissolution and reconstitution depending on the structures involved.

Not all. The Sociedad en Nombre Colectivo and Sociedad en Comandita Simple do not provide full separation between the entity and its general partners, who remain personally liable for business debts. The S.A., S.A.S., S.R.L., and EIRL are each recognized as distinct legal persons under Law 479-08, meaning their obligations do not automatically extend to their owners.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.