Key Takeaways

- The Dominican Republic's 27% corporate income tax rate sits above the regional average, creating a recurring cost burden that compounds for foreign-owned operational subsidiaries with limited treaty relief options.

- Registration of an SRL or SA requires navigating multi-step procedures across the Commercial Registry and DGII, adding time and administrative cost before a company can legally operate.

- Foreign investors face sector-specific ownership restrictions that cannot be resolved through structural planning alone, as the restrictions are imposed by Dominican law rather than by regulatory discretion.

- Weak contract enforcement through the Dominican judicial system introduces operational risk that is difficult to price or mitigate without heavy reliance on arbitration clauses and cross-border dispute mechanisms.

The Dominican Republic operates under an evolving regulatory framework, with corporate governance requirements governed primarily by the Commercial Code and supplemented by sector-specific legislation. Understanding the disadvantages of incorporating in Dominican Republic is relevant before committing to a structure, particularly given the range of compliance, tax, and institutional factors that affect day-to-day operations.

This article examines several categories of disadvantages — spanning registration procedures, tax obligations, banking access, and legal enforcement — without addressing each in isolation at this stage.

The cons of setting up a company in Dominican Republic do not apply uniformly. Risks and friction points vary considerably depending on whether your business is structured as an SRL or SA, the industry you operate in, and whether you involve foreign capital.

Foreign investors establishing an operational subsidiary, rather than a holding or trading entity, are most likely to encounter the full range of drawbacks discussed here.

Complex SRL and SA Registration Process

Dominican Republic SRL and SA registration challenges begin at the structural level. Both entity types require a notarized incorporation deed, and the documentation burden alone delays the formation timeline significantly.

Multiple Notarial and Authentication Requirements

Forming an SRL or SA requires a public deed executed before a Dominican notary, which must then be registered with the Cámara de Comercio y Producción. Foreign-sourced documents require apostille certification or consular legalization before they are accepted, adding weeks to the process. If your founding shareholders are non-residents, coordinating notarized identity documents across multiple countries compounds the delay.

Capital and Statutory Filing Obligations

An SA requires a minimum authorized capital, and at least ten percent must be paid in at the time of incorporation, a requirement that demands advance capital commitment before the entity can operate. The Registro Mercantil also mandates publication of the incorporation notice in a nationally circulated newspaper, an obligation that adds cost and time with no operational benefit to the foreign investor.

Foreign founders who underestimate the notarial and authentication requirements for SRL incorporation problems Dominican Republic often face formation delays of two to three months before the entity is legally operational.

Mandatory Local Registered Agent Requirement

One of the less visible but persistent Dominican Republic registered agent requirement drawbacks is the obligation to maintain a locally present representative for your company's legal correspondence and official filings. This requirement is not optional and applies throughout the life of the entity, not just at incorporation.

Under Dominican corporate law, both the SRL and SA structures require a designated local contact point accessible to regulatory bodies, including the Cámara de Comercio and the DGII. For a foreign founder who does not live in the country, this creates a dependency on a third party whose reliability directly affects your company's standing.

The mandatory local agent restrictions in the Dominican Republic generate specific friction points for foreign operators:

- Your agent's unavailability or negligence can result in missed DGII notifications, triggering penalties that fall on your company regardless of fault.

- Replacing an underperforming agent requires formal legal steps, creating delays in compliance coverage.

- Agent fees are a recurring operational cost with no regulatory cap, leaving pricing entirely at the provider's discretion.

- Any mismatch between the agent's registered address and actual correspondence routing can cause documents to go unacknowledged during audits or legal proceedings.

Company Incorporation in the Dominican Republic

Expanship manages the full incorporation process for SRL and SA structures in the Dominican Republic, including local registered agent coordination and DGII registration.

Slow Commercial Registry Processing Times

Dominican Republic commercial registry delays represent one of the more disruptive operational risks for foreign-owned businesses attempting to establish a legal presence there. Registration is handled through the Registro Mercantil, administered by the Cámaras de Comercio y Producción at the provincial level. Processing times are inconsistent and can extend well beyond published guidelines, depending on the chamber's workload and the completeness of submitted documentation.

Even when all documents are in order, approvals for an SRL or SA can take several weeks. Your business cannot legally operate, open a corporate bank account, or obtain a Registro Nacional del Contribuyente (RNC) number from the DGII until registration is confirmed, creating a direct delay in generating revenue.

| Stage | Estimated Delay | Business Impact |

|---|---|---|

| Initial document review | 5–15 business days | Operations legally blocked |

| Corrections or re-submissions | Additional 5–10 business days per round | Timeline extends unpredictably |

| Certificate of Incorporation issuance | 3–7 additional business days | Required before RNC application |

| RNC registration via DGII | Up to 15 additional business days | No tax compliance possible without it |

Errors in notarized documents, which must meet specific formatting standards under Dominican commercial law, trigger re-submission cycles that compound delays significantly. Each correction round resets portions of the review queue.

Provincial chambers vary in administrative capacity, so registration timelines in Santo Domingo differ from those in Santiago or smaller provinces. This inconsistency makes project timelines genuinely difficult to forecast.

Restricted Foreign Ownership in Certain Sectors

Foreign ownership restrictions in the Dominican Republic are defined by a combination of constitutional provisions and sector-specific legislation rather than a single unified foreign investment law. While Law No. 16-95 on Foreign Investment generally permits full foreign ownership in most sectors, several industries impose binding caps or outright exclusions that directly affect how your business can be structured.

Media and broadcasting represent one of the clearest examples. Under the Broadcasting Law, foreign nationals face ownership limitations on television and radio concessions, requiring majority Dominican ownership. This means a foreign media group cannot hold a controlling stake without a local partner, limiting operational and editorial control.

Real estate near border zones and coastlines carries constitutional restrictions under Article 11 that affect how foreign entities can hold title, adding legal complexity to property-backed business models.

- Majority local ownership is mandatory for broadcast media concessions

- Border zone and coastal real estate ownership restrictions apply to foreign-registered entities

- Sector-specific rules exist independently of the general foreign investment framework under Law No. 16-95

- Structuring around ownership caps requires a qualifying Dominican partner, which creates dependency

- Non-compliant ownership structures can result in license denial or concession revocation

These restrictions force foreign investors into co-ownership arrangements they may not have anticipated, with legal and governance consequences that go beyond simple equity splitting.

The Dominican Republic's general foreign investment law permits 100% foreign ownership in most sectors, yet sector-specific laws can contradict this at the licensing stage, catching investors off guard after incorporation.

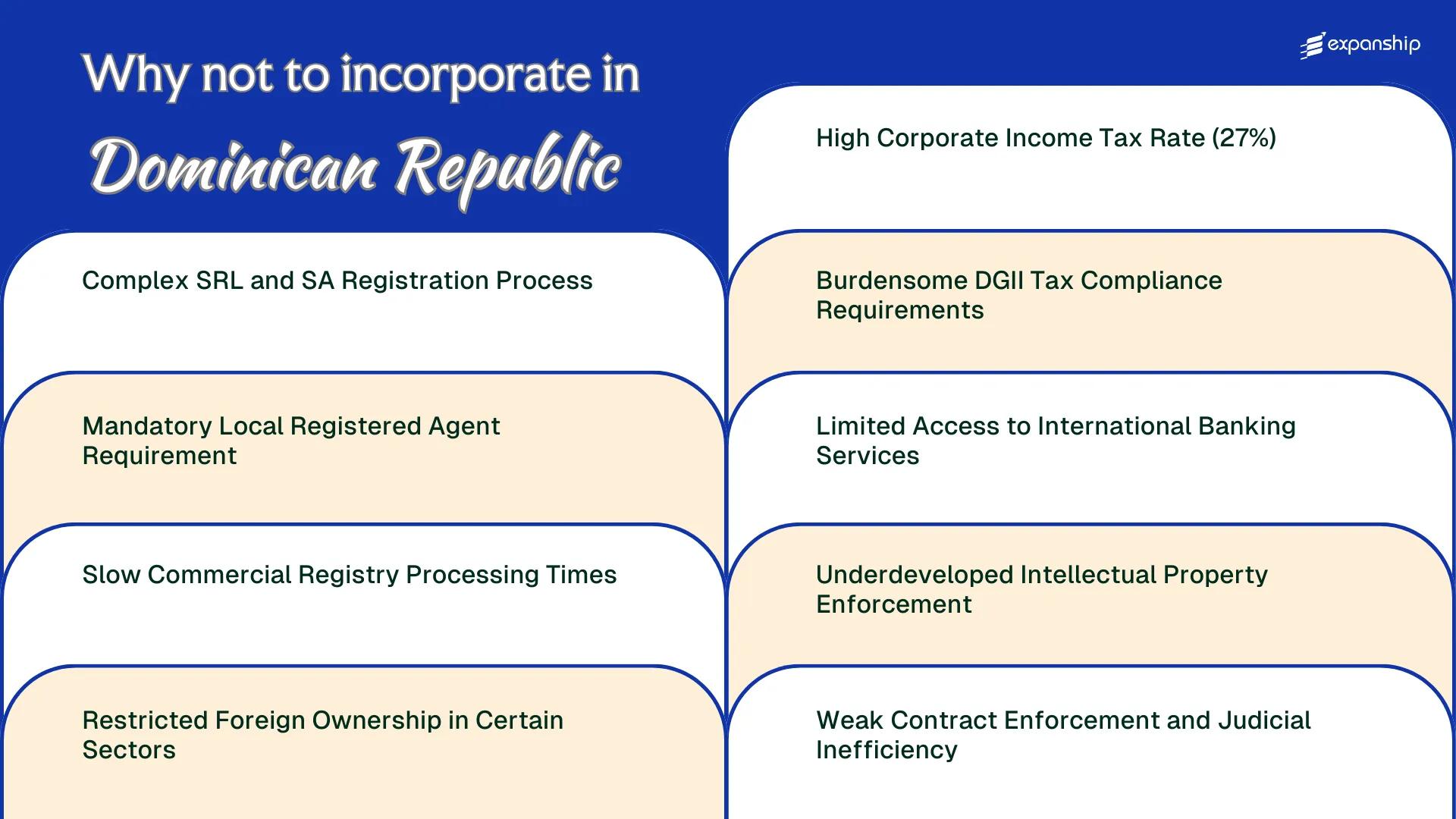

High Corporate Income Tax Rate (27%)

At 27%, the Dominican Republic corporate tax rate disadvantages foreign-owned businesses in ways that extend well beyond the headline figure. That rate, applied under the Ley de Impuesto sobre la Renta, places the country above many competing jurisdictions in Latin America and the Caribbean.

A Rate That Erodes Profit Margins

Panama applies a 25% rate, while several Caribbean jurisdictions sit considerably lower, making the 27 percent corporate income tax in the Dominican Republic a real cost differential for internationally mobile businesses. Profits distributed to foreign shareholders may then face additional withholding tax obligations under domestic rules administered by the Dirección General de Impuestos Internos (DGII), compounding the effective tax burden.

How This Affects Foreign Business Owners Specifically

For a foreign entity with no offsetting tax treaty benefits — the Dominican Republic has a limited treaty network — the combined statutory and withholding exposure can materially reduce after-tax returns compared to what the same structure would yield elsewhere. Free zone entities operating under Law 8-90 carry a separate tax regime, but that exemption applies only to qualifying export-oriented activities and is unavailable to most general commercial businesses.

Get Guidance on Managing Tax Exposure in the Dominican Republic

Understand how the 27% corporate income tax rate and DGII obligations affect your structure before you commit to incorporating.

Burdensome DGII Tax Compliance Requirements

DGII tax compliance burdens in the Dominican Republic add a recurring administrative cost layer that many foreign-owned entities underestimate before incorporating.

- Your company must file monthly returns with the Dirección General de Impuestos Internos (DGII) for ITBIS (value-added tax), meaning compliance obligations arise every single month regardless of revenue activity.

- Advance income tax payments (pagos a cuenta) are required throughout the fiscal year, forcing your business to commit cash before actual annual liability is confirmed.

- Withholding tax declarations on payments to suppliers and contractors must be submitted separately, multiplying the number of filings your firm manages each period.

- The DGII mandates electronic fiscal invoicing (e-CF) through its comprobantes fiscales system, requiring technical integration that generates upfront setup costs for newly registered entities.

- Failure to meet filing deadlines triggers automatic penalties and interest charges under the Código Tributario Dominicano, with limited tolerance for administrative errors during the early operational phase.

Limited Access to International Banking Services

Dominican Republic banking access limitations for foreign companies begin before operations even start. Local banks, including Banco Popular Dominicano and Banreservas, apply stringent due diligence requirements to foreign-owned entities that routinely extend the account-opening process by several weeks or months.

Correspondent banking restrictions compound this problem. Many Dominican banks maintain limited correspondent relationships with North American and European institutions, which means international wire transfers can face delays, additional fees, or outright rejection depending on the counterparty bank's compliance thresholds.

Foreign directors who are non-residents face the steepest barriers. Most banks require in-person visits for account authorization, which forces non-resident shareholders to make a dedicated trip to Santo Domingo solely for banking setup, adding travel costs and time before the business generates a single peso.

Even once an account is opened, foreign currency transactions are subject to oversight by the Banco Central de la República Dominicana under the Monetary and Financial Law No. 183-02, which regulates foreign exchange operations and can slow cross-border fund movements.

A foreign-owned SRL incorporated in Santo Domingo requiring regular USD wire transfers to European suppliers could realistically face per-transfer fees of $25-$45 at the domestic bank level, plus potential intermediary bank charges of $15-$30 per transaction, accumulating to over $800 annually on modest monthly transfer volumes.

Underdeveloped Intellectual Property Enforcement

Dominican Republic intellectual property enforcement problems present a concrete operational risk for any foreign business holding trademarks, patents, or proprietary content. While the country is a signatory to TRIPS and the Berne Convention, and Law No. 20-00 on Industrial Property provides a formal registration framework administered by ONAPI (Oficina Nacional de la Propiedad Industrial), registration alone does not guarantee protection in practice.

Counterfeit goods and trademark infringement are documented concerns, and civil enforcement through Dominican courts tends to be slow. This delay means that by the time a court order is obtained, commercial damage to your brand may already be substantial.

Customs-level IP enforcement, while technically available under the framework, operates inconsistently. For digital assets and software, weak IP protection risks are compounded by limited specialized enforcement capacity.

Criminal prosecution for IP violations exists under Law No. 20-00, but successful prosecutions are infrequent. A foreign firm relying on litigation as its primary enforcement mechanism will face both cost and time exposure that makes deterrence difficult.

If your business model depends on proprietary technology, brand exclusivity, or licensed content, the practical gap between ONAPI registration and actual market enforcement in the Dominican Republic means your intellectual property rights may be difficult to defend without significant legal expenditure.

Weak Contract Enforcement and Judicial Inefficiency

Dominican Republic contract enforcement risks are a documented concern for foreign investors, stemming from structural inefficiencies within the civil court system rather than an absence of commercial law.

The country's commercial disputes are governed by the Code of Commerce and adjudicated through ordinary civil chambers, as a dedicated commercial court system remains limited in reach. Cases involving breach of contract can take several years to resolve, which exposes your business to prolonged uncertainty and accumulating legal costs.

Judicial outcomes can also be inconsistent, with enforcement of foreign judgments requiring a separate recognition procedure under Dominican civil procedure rules. This adds another procedural layer before any award becomes executable.

Arbitration clauses offer a contractual workaround, but only if your counterparty has agreed to them in advance. Without such provisions embedded in your agreements, you default into a court process that offers little predictability on timelines or outcomes.

Strategies to Overcome These Challenges

Overcoming Dominican Republic incorporation challenges requires structural preparation rather than reactive adjustments. Foreign businesses that plan entity type, tax position, and sector exposure before filing with the Cámara de Comercio y Producción tend to encounter fewer material delays.

- Register as an SRL or SA with a certified local agent listed on the Registro Mercantil before initiating any commercial activity.

- Apply for a Registro Nacional de Contribuyentes (RNC) number with the DGII early in the formation process to avoid tax compliance backlogs.

- Conduct a pre-entry sector review against Law 16-95 on Foreign Investment to identify any restricted ownership thresholds.

- File trademark registrations with ONAPI promptly, as administrative IP protection precedes any enforcement options.

- Structure dispute resolution clauses in commercial contracts to reference international arbitration, given documented judicial processing delays.

Mitigating risks of business setup in the Dominican Republic depends heavily on sequencing these steps correctly within the existing regulatory framework. None of these measures eliminate the underlying structural constraints; they reduce exposure to the most common procedural and compliance failures.

Dominican Republic Still Worth Considering

Despite the documented drawbacks, the Dominican Republic remains a credible destination for foreign business incorporation, particularly given its geographic position as a gateway to Caribbean and Latin American markets and the legal framework established under Laws 479-08 and 31-11. Answering whether the Dominican Republic is worth incorporating despite drawbacks requires an honest reading of both sides.

| Pros | Cons |

|---|---|

| Strategic location with access to Caribbean and Latin American markets | SRL and SA registration involves multi-step bureaucratic procedures with no guarantee of processing speed |

| Free Trade Zone regimes offer significant tax incentives for qualifying businesses | The 27% corporate income tax rate is high relative to comparable jurisdictions in the region |

| CAFTA-DR membership provides preferential trade access to the United States market | DGII compliance requirements impose recurring administrative burdens on foreign-owned entities |

| A growing consumer base supports domestic market entry strategies | Foreign ownership is restricted in sectors such as media, coastal land, and certain utilities |

| The SRL structure allows incorporation with relatively modest capital requirements | Intellectual property enforcement remains inconsistent despite ratification of international treaties |

Contract enforcement timelines through the Dominican court system add operational uncertainty for foreign firms. Banking access for non-resident entities remains constrained by due diligence requirements that can delay account opening by months.

Compliance Services for Companies in the Dominican Republic

Maintain your Dominican entity in good standing with DGII filings, annual obligations, and registry requirements.

Conclusion

A Dominican Republic company incorporation cons summary reflects a consistent pattern: structural friction at multiple points in the formation and operating cycle. The 27% corporate income tax rate, combined with DGII's detailed compliance obligations, creates a sustained administrative burden. Judicial inefficiency under the civil law system further compounds operational risk, particularly when contractual disputes arise. These are not isolated concerns. Businesses entering this market with a clear understanding of the regulatory and tax environment, and with qualified local support in place, are better positioned to manage what the setup process demands.

Expanship's Support for Your Dominican Republic Expansion

Expanship's Dominican Republic company formation support is structured around the specific friction points this jurisdiction creates: from preparing notarized formation documents for the Cámara de Comercio y Producción to managing ongoing DGII tax filings and sector-specific ownership compliance. Your operational burden doesn't disappear, but having experienced support means fewer delays, errors, and missed obligations along the way.

Expanship provides practical assistance across the full incorporation and compliance cycle.

- Your company registration and all required formation documents are prepared to meet local legal standards.

- A local registered agent and domicile address are provided to satisfy Dominican legal requirements.

- All government filings and liaison with regulatory bodies, including the DGII and commercial registry, are handled on your behalf.

- Post-incorporation compliance obligations are managed to keep your entity in good standing.

- Banking introduction assistance is available to support your access to local financial institutions.

- Tax registration and coordination with local authorities are completed as part of the setup process.

Reach out to Expanship Dominican Republic to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

Yes, the Dirección General de Impuestos Internos applies its filing and reporting obligations regardless of company size or ownership structure. Both an SRL with a single foreign shareholder and a large SA face the same mandatory monthly VAT filings, annual income tax returns, and withholding tax reporting cycles. There is no simplified regime for newly incorporated foreign-owned entities that reduces this administrative load during the early operational period.

The DGII imposes surcharges of 10% of unpaid tax for the first month of non-compliance, rising by an additional 4% for each subsequent month, plus annual interest charges. Repeated non-compliance can trigger audits, account freezes, or cancellation of your tax registration number (RNC), which effectively halts your ability to operate legally. These penalties accumulate quickly and can become disproportionate relative to the original tax liability for smaller businesses.

Contract enforcement through Dominican courts is slow and procedurally complex, making litigation a poor primary remedy for foreign firms. The judicial process can extend for several years, and decisions are not always predictable when one party has stronger local ties. Many foreign businesses operating in the Dominican Republic mitigate this by including international arbitration clauses in commercial contracts, typically referencing ICC or UNCITRAL rules, rather than relying on domestic courts.

Foreign investors can hold 100% ownership in most sectors under the Foreign Investment Law No. 16-95, but specific industries are subject to ownership caps or require prior government authorization. Media companies, for instance, face restrictions tied to Dominican nationality requirements, and certain natural resource concessions involve state participation conditions. Before incorporating, you need to verify whether your intended activity falls under a restricted category, as proceeding without clearance exposes the entity to regulatory sanctions.

The Dominican Republic has intellectual property legislation in place, including Law No. 20-00 on Industrial Property, but enforcement through administrative and judicial channels is inconsistent. Infringement cases move slowly, and injunctive relief is difficult to obtain quickly enough to prevent market damage. For businesses whose value depends on brand integrity, proprietary technology, or licensed content, this creates a real commercial risk that registration alone does not adequately address.

Processing delays at the Registro Mercantil are common and can extend your incorporation timeline by several weeks beyond the official estimates. During this period your entity has no legal standing, meaning you cannot open a corporate bank account, sign contracts in the company's name, or apply for a tax identification number with the DGII. There is no formal escalation mechanism that guarantees faster processing, so operational planning needs to account for this uncertainty from the outset.

Yes, Dominican-registered entities face above-average difficulty accessing correspondent banking and multi-currency accounts with international banks. Global banks apply enhanced due diligence to companies from jurisdictions on certain FATF or OECD monitoring lists, and the Dominican Republic's historical inclusion on such watchlists has contributed to a cautious banking posture from foreign institutions. This affects your ability to receive international wire transfers and hold foreign currency reserves efficiently, which is a practical constraint that companies incorporated in, say, Chile or Colombia are less likely to encounter at the same severity.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.