Key Takeaways

- Entities operating under Dominican Republic Free Zone Law 8-90 can eliminate corporate income tax entirely, making the jurisdiction structurally competitive for manufacturing and export-oriented businesses.

- The territorial tax system means foreign-sourced income is generally outside the scope of Dominican taxation, reducing the compliance burden for internationally operating holding and services companies.

- Access to CAFTA-DR provides Dominican-registered businesses with preferential entry to the United States market through a codified trade framework rather than discretionary arrangements.

- Sector-specific incentive regimes under Law 158-01 for tourism and Law 57-07 for renewable energy create defined, statutory pathways to reduced tax liability for qualifying investment activity.

The benefits of incorporating in the Dominican Republic draw interest from businesses seeking a regulated, mid-sized economy with direct access to both Caribbean and North American commercial channels. Situated on the island of Hispaniola, the country is an independent sovereign nation and a member of the Caribbean Community's broader trade architecture. Company registration falls under the oversight of the Registro Mercantil, the official body responsible for the incorporation and maintenance of commercial entities. Foreign businesses most commonly establish a presence through the Sociedad de Responsabilidad Limitada.

The country operates a territorial-based tax system, meaning income sourced outside its borders is generally not subject to local taxation. Foreign ownership of Dominican-registered entities is broadly permitted across most sectors, and the government has maintained a consistent policy framework encouraging foreign direct investment. This article examines the principal advantages that the Dominican Republic's corporate and regulatory environment offers to internationally operating businesses and investors.

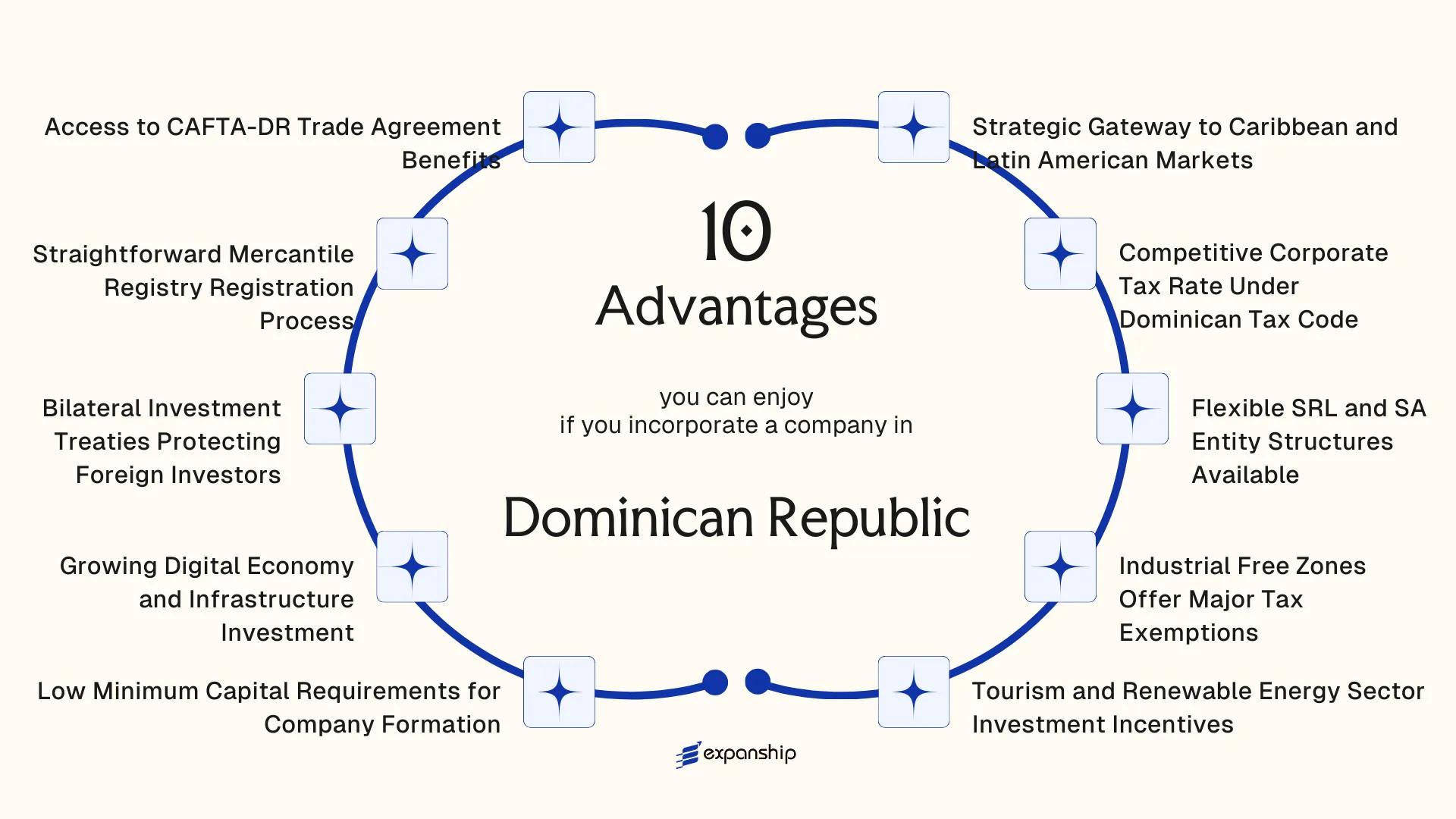

Strategic Gateway to Caribbean and Latin American Markets

Situated on Hispaniola, the Dominican Republic occupies a central position in the Caribbean Basin that translates directly into Dominican Republic Caribbean market access advantages for internationally oriented businesses. Proximity to major shipping lanes and air corridors connecting North America, South America, and Europe makes the country a functional distribution and operations hub.

Regional Connectivity With Commercial Consequence

The Port of Caucedo and Las Américas International Airport handle substantial cargo volumes, giving companies incorporated locally direct access to regional freight networks. Your business gains physical infrastructure that supports trade across the Caribbean and into Central America without requiring additional operational bases.

Trade Architecture That Extends Market Reach

Membership in CARICOM as an observer and bilateral trade arrangements with several Latin American economies extend the commercial reach of a Dominican-registered entity beyond its borders. These agreements mean a firm operating locally can engage regional markets under preferential conditions that would not apply to an offshore holding structure.

A Dominican-incorporated entity positions you at the intersection of Caribbean and Latin American trade routes, with port and airport infrastructure already in place to support cross-regional operations.

Competitive Corporate Tax Rate Under Dominican Tax Code

The standard corporate income tax rate under Dominican Tax Code (Código Tributario, Law 11-92) sits at 27%. While that figure alone carries weight, the practical advantage lies in how that rate interacts with deductible expenses, depreciation allowances, and sector-specific exemptions administered by the Dirección General de Impuestos Internos (DGII), which can meaningfully reduce your effective tax burden below the nominal rate.

Dividend distributions to non-resident shareholders are subject to a 10% withholding tax, a rate that remains fixed regardless of the distributing entity's size. For foreign investors structuring profit repatriation, predictability at that level simplifies financial modelling considerably.

Corporate capital gains are generally taxed as ordinary income under Law 11-92, but the indexed cost basis adjustment available for asset calculations limits the taxable gain to real, inflation-adjusted appreciation rather than nominal figures. That distinction matters when holding long-term business assets.

Among the structural features that make the Dominican Republic corporate tax rate advantages concrete for foreign-owned entities:

- Allowable deductions include interest on business loans, reducing taxable income for leveraged investment structures

- Depreciation schedules are defined in law, providing certainty during multi-year capital planning

- Tax losses may be carried forward for up to five fiscal years, offering relief during early-stage operations

- Transfer pricing rules follow OECD guidelines, reducing exposure to double taxation with treaty partners

Incorporate a Company in the Dominican Republic

Set up your Dominican business entity with full DGII registration support and ongoing compliance management.

Flexible SRL and SA Entity Structures Available

Two principal corporate forms are available under the Dominican Republic's Ley No. 479-08 (General Commercial Companies and Individual Limited Liability Enterprises Act): the Sociedad de Responsabilidad Limitada (SRL) and the Sociedad Anónima (SA). Each serves a distinct operational profile, and the choice between them directly shapes governance flexibility, shareholder privacy, and capital structure.

The SRL suits closely held businesses. Ownership is divided into quotas rather than publicly transferable shares, which restricts entry to new partners and preserves control among existing members. For a foreign investor who wants to maintain a defined ownership circle, this structure prevents unwanted dilution without requiring complex contractual arrangements.

| Feature | SRL | SA |

|---|---|---|

| Ownership instrument | Quotas | Shares |

| Shareholder transferability | Restricted by partner consent | Freely transferable |

| Minimum shareholders | 2 | 2 |

| Maximum shareholders | 50 | Unlimited |

| Board requirement | Not required | Required |

The SA accommodates growth-oriented businesses that anticipate bringing in outside investors or eventually accessing capital markets. Shares transfer freely unless the articles of incorporation impose restrictions, which gives your firm structural flexibility as its financing needs evolve.

Both entity types benefit from limited liability protection, meaning personal assets of shareholders remain separate from corporate obligations. Governance documents filed with the Registro Mercantil can be tailored to reflect the specific operational needs of foreign-owned businesses, including provisions on profit distribution and management authority.

Industrial Free Zones Offer Major Tax Exemptions

Dominican Republic free zone tax exemption benefits are governed by Law 8-90 on the Promotion of Free Export Zones, which grants qualifying companies operating within designated zones an extensive package of fiscal relief. Businesses established under this regime are fully exempt from corporate income tax, import and export duties, VAT, municipal taxes, and taxes on dividend remittances. For export-oriented manufacturers, distributors, or service providers, this means operating with a tax base that is structurally different from the standard Dominican Tax Code regime.

The National Free Zones Council (CNZFE) oversees the administration, approval, and compliance requirements for zona franca operators. Your business must operate within an approved free zone park and primarily conduct export-oriented activities to qualify.

Key conditions to keep in mind:

- Operations must be physically located within a CNZFE-authorized zone

- The exemption package applies for an initial period of 20 years, renewable under the law

- Sales into the domestic Dominican market are subject to standard import duties and taxes

- Annual reporting to CNZFE is required to maintain active status

- Reclassification of activities after approval can trigger a compliance review

Service companies, including call centers and software firms, are eligible for free zone status under Law 8-90, not just industrial manufacturers.

Tourism and Renewable Energy Sector Investment Incentives

Two of the most tax-advantaged sectors for foreign business owners are tourism and renewable energy, where Dominican Republic tourism investment incentives deliver structured, legislated relief rather than discretionary concessions. These incentives reduce effective costs substantially, which directly improves project viability for qualifying foreign entities.

Tourism Incentives Under Law 158-01

Law 158-01 on Tourism Promotion grants approved tourism enterprises a 10-year exemption from income tax, ITBIS (the local VAT), import duties on equipment, and taxes on property transfers related to the project. Your business qualifies if it operates within a designated tourism development pole, which includes specific provinces such as Pedernales, Barahona, and Samaná, among others. That geographic targeting means underdeveloped coastal regions offer the most extensive incentive packages, lowering entry costs for firms willing to establish in areas the government has prioritized.

Renewable Energy Benefits Under Law 57-07

Law 57-07 on Incentives for the Development of Renewable Energy Sources extends comparable fiscal treatment to firms investing in solar, wind, biomass, and hydroelectric projects. Qualified businesses receive exemptions from import tariffs on renewable energy equipment and from income taxes during the productive phase of the investment. Given that equipment importation often represents the largest capital outlay in early-stage energy projects, this exemption materially reduces the initial investment threshold. Certifications are administered through the National Energy Commission (CNE), which functions as the technical and regulatory body for qualifying approvals.

Unlock Tourism and Energy Incentives in the Dominican Republic

Speak with an Expanship specialist to confirm eligibility under Law 158-01 or Law 57-07 and structure your entry for maximum fiscal benefit.

Low Minimum Capital Requirements for Company Formation

Under Dominican Republic law, the Sociedad de Responsabilidad Limitada (SRL) carries no statutory minimum capital requirement under Law 479-08 on Commercial Companies. This Dominican Republic low minimum capital requirements benefit means you can incorporate without committing a fixed sum to a paid-in capital threshold, preserving working capital for actual operational use from day one.

- For early-stage ventures or foreign subsidiaries in a testing phase, the absence of a mandatory capital floor removes a common financial barrier present in many civil law jurisdictions, where minimums can range from several thousand to tens of thousands of dollars.

- Capital contributions to an SRL can be made in cash or in kind, giving your business flexibility in how initial resources are structured without triggering additional licensing hurdles solely on account of capitalization levels.

- This structure is particularly practical for holding companies, consulting firms, or service-oriented entities where physical asset investment is limited and operational costs are covered through revenue rather than registered capital.

- The Sociedad Anónima (SA) does carry a statutory minimum capital requirement under Law 479-08, so entity selection directly affects your initial financial obligations at incorporation.

Growing Digital Economy and Infrastructure Investment

Dominican Republic digital economy investment advantages have become increasingly concrete, backed by government policy and physical infrastructure expansion rather than aspiration alone.

The government established the Dominican Information and Communication Technology Institute (INDOTEL) as the regulatory body overseeing the country's telecommunications sector. Broadband penetration has expanded steadily, and submarine cable connections to North America and Latin America give businesses operating here reliable international connectivity. For e-commerce firms or tech companies, this translates into functional infrastructure rather than a dependency on underdeveloped networks.

Law No. 126-02 on Electronic Commerce, Documents, and Digital Signatures provides a legal framework that recognizes electronic contracts and digital signatures, giving your business a legally sound basis for operating digital transactions locally.

- Santo Domingo and Santiago host a growing cluster of technology firms and shared office infrastructure supporting digital startups and international operators.

- The government's National Digital Strategy targets expanded public digital services, which increases the addressable market for private technology and e-commerce companies.

A firm processing 10,000 monthly digital transactions under Law No. 126-02 operates with the same legal enforceability as paper-based contracts, eliminating the need for costly notarization on routine commercial agreements and reducing administrative overhead on recurring digital operations.

Bilateral Investment Treaties Protecting Foreign Investors

Dominican Republic bilateral investment treaty protections give foreign investors a formal legal shield that goes beyond domestic law. The country has signed BITs with multiple nations, including the United States, Spain, France, Germany, and several other European and Latin American states. Under these agreements, your investment cannot be expropriated without prompt, adequate, and effective compensation.

Each treaty typically guarantees:

- Fair and equitable treatment for foreign-owned entities

- Protection against arbitrary or discriminatory measures by the state

- Free transfer of returns, capital, and liquidation proceeds

- Access to international arbitration (commonly ICSID) if a dispute arises

Access to international arbitration is particularly significant. Rather than resolving disputes exclusively through Dominican courts, covered investors can submit claims to neutral international tribunals, which removes a material source of jurisdictional uncertainty.

The underlying authority comes from Law No. 16-95 on Foreign Investment, which formally recognizes and incorporates the protections negotiated under these bilateral instruments. Eligibility depends on the nationality of the investor and the specific treaty in force between the Dominican Republic and your home country.

Verify that your home country has a ratified and currently active BIT with the Dominican Republic, as treaty coverage is not universal and inactive or unsigned agreements confer no protections.

Straightforward Mercantile Registry Registration Process

Dominican Republic Mercantile Registry registration benefits begin at the structural level: the registration process is administered by the Cámara de Comercio y Producción, and completing it is a condition for legal commercial operation. Because the registry functions as a unified entry point for establishing legal existence, your business gains recognized standing with tax authorities, financial institutions, and government agencies through a single filing.

Registration at the Registro Mercantil also establishes the foundation for obtaining your Registro Nacional de Contribuyentes (RNC) number, which the Dirección General de Impuestos Internos (DGII) requires before a company can issue invoices or file tax returns. Without this sequence, no legitimate commercial activity is possible, so completing it quickly reduces the window during which your entity exists legally but cannot yet operate or contract.

Processing timelines at the Cámara are defined by established procedures rather than discretionary review, which gives you a predictable window for planning operational launch dates.

Required documentation for Mercantile Registry filing typically includes:

- Notarized articles of incorporation

- Proof of capital deposit

- Identification documents for shareholders and directors

- Publication in a newspaper of general circulation, as required under the Commercial Companies Law No. 479-08

Each requirement serves a verification purpose tied to existing law, rather than reflecting bureaucratic discretion. That legal grounding means conditions are consistent and predictable across filings.

ONAPI business registration for intellectual property protection runs separately but can proceed in parallel once your Registro Mercantil filing is underway, allowing you to protect trade names and trademarks without delaying commercial launch.

Access to CAFTA-DR Trade Agreement Benefits

The Dominican Republic CAFTA-DR trade agreement benefits extend to companies incorporated locally, giving qualifying businesses preferential access to the United States market under the Dominican Republic-Central America-United States Free Trade Agreement, which entered into force for the country in March 2007.

Under CAFTA-DR, goods produced or substantially transformed within the country can enter the U.S. market at reduced or zero tariff rates, depending on the product category and applicable rules of origin. For a manufacturer or exporter, this directly reduces the cost of reaching one of the world's largest consumer markets without the tariff burden faced by competitors operating outside the agreement.

Rules of origin under CAFTA-DR are product-specific and generally require that goods meet minimum regional content thresholds to qualify for preferential treatment. A company must structure its sourcing and production processes to satisfy these requirements, which makes local incorporation and genuine operational presence in the jurisdiction a practical necessity rather than a formality.

The agreement also covers services trade and investment protections, not just goods. Foreign firms incorporated locally can benefit from national treatment provisions, meaning U.S.-based investors receive treatment no less favorable than that accorded to domestic investors under the framework.

Key trade advantages available through CAFTA-DR membership include:

- Duty-free or reduced tariff access on a wide range of goods exported to the United States

- Transparent dispute resolution mechanisms applicable to cross-border investment conflicts

- Protections against performance requirements that might otherwise restrict how a foreign-owned entity operates

- Market access commitments covering certain financial and professional services sectors

Why the Dominican Republic Stands Out Among Caribbean Business Destinations

Positioned against its Caribbean peers, the Dominican Republic presents a distinct profile for foreign investors evaluating incorporation options in the region. Jurisdictions such as Jamaica, Trinidad and Tobago, and Panama are frequently considered alongside it, each targeting similar investor profiles through trade access, sectoral incentives, and corporate structures. What the comparison reveals is that the Dominican Republic's combination of CAFTA-DR trade access, Industrial Free Zone exemptions under Law No. 8-90, and bilateral investment treaty coverage creates a cumulative advantage that few Caribbean alternatives replicate within a single framework.

Across several measurable parameters, the Dominican Republic holds a position that warrants direct comparison. Panama offers a territorial tax system, but lacks the CAFTA-DR trade relationship with the United States. Jamaica provides English-language incorporation processes, yet its free zone regime operates under different sectoral constraints. Trinidad and Tobago carries hydrocarbon-sector depth but narrower incentive structures for manufacturing and export-oriented businesses. The table below compares these jurisdictions against criteria directly relevant to a foreign business owner assessing the region.

| Parameter | Dominican Republic | Jamaica | Panama | Trinidad and Tobago |

|---|---|---|---|---|

| CAFTA-DR Trade Access | Yes | No | No | No |

| Industrial Free Zone Tax Exemption | Yes (Law No. 8-90) | Limited | Yes (Panama Pacifico) | Limited |

| Bilateral Investment Treaties | 10+ active BITs | Fewer than 10 | 25+ BITs | Fewer than 10 |

| Standard Corporate Tax Rate | 27% | 25% | 25% | 30% |

| Minimum Share Capital (SRL) | No statutory minimum | No statutory minimum | No statutory minimum | No statutory minimum |

| Renewable Energy Investment Incentives | Yes (Law No. 57-07) | Yes | Limited | Limited |

| Access to Latin American Markets | Direct via geography and treaties | Indirect | Direct via geography | Indirect |

Compliance Services for Companies in the Dominican Republic

Maintain good standing with the Mercantile Registry, the DGII, and other Dominican regulatory bodies through structured compliance support.

Conclusion

The benefits of incorporating in the Dominican Republic rest on a combination of structural tax advantages, legal protections for foreign capital, and preferential trade access that few Caribbean jurisdictions can match at the same level. Free zone operators under Law 8-90 can eliminate corporate income tax entirely, while the CAFTA-DR agreement opens preferential access to the United States market without additional negotiation. These are not incidental features; they are codified frameworks that directly reduce the cost and risk of operating internationally.

Your business structure and industry will determine how much of this framework applies. A firm established as an SRL for holding or services will experience the tax code differently than a manufacturing entity inside a free zone. Investment incentives under Law 158-01 for tourism or Law 57-07 for renewable energy create sector-specific advantages that only activate under defined conditions.

Taken together, the Dominican Republic presents a legally grounded case for foreign incorporation, one built on treaty protections, a functioning Mercantile Registry, and statutory incentive regimes with real economic consequence. The next step is matching that framework to your specific operational model, entity type, and target market, a process that requires jurisdiction-specific structuring rather than a generic approach.

Start Your Dominican Republic Company Formation With Expanship Today

Expanship assists foreign investors in structuring their Dominican Republic company formation correctly from the outset, handling entity selection between the SRL and SA, preparing documentation in accordance with Dominican commercial law, and filing with the Mercantile Registry (Registro Mercantil) under the oversight of the Cámara de Comercio y Producción. The firm's work spans the full formation cycle, from initial structuring through to ongoing compliance under the Dirección General de Impuestos Internos (DGII).

Incorporating in the Dominican Republic through Expanship covers the following service areas:

- Document preparation, notarization, and legalization for submission to local authorities

- Registered agent and registered office provision throughout the company's operational life

- Government filing and liaison with the Mercantile Registry and relevant sectoral regulators

- Post-incorporation compliance management, including annual reporting and tax registration obligations

- Support with corporate bank account introductions through locally licensed financial institutions

- Guidance on free zone operator approvals or sector-specific incentive applications where applicable

To begin the process, contact Expanship Dominican Republic.

Frequently Asked Questions (FAQ)

Yes, foreign nationals can hold 100% ownership of both an SRL (Sociedad de Responsabilidad Limitada) and an SA (Sociedad Anónima) under Dominican corporate law. There is no statutory requirement for a local partner or nominee shareholder in standard commercial entities. Certain regulated sectors, such as specific media or land ownership near border zones, may carry separate restrictions under sector-specific legislation.

The standard corporate income tax rate is 27% under the Dominican Tax Code (Código Tributario), applicable to net taxable income. Companies operating within Industrial Free Zones are exempt from this tax entirely for the duration of their approved zone license. The rate applies to resident entities on Dominican-source income, making the sourcing of income a relevant planning consideration for foreign-owned firms.

Registration with the Mercantile Registry (Registro Mercantil) under the Chamber of Commerce generally takes between five and fifteen business days once all documentation is correctly submitted. Incomplete filings or notarization errors are the most common causes of delay. The process involves submitting the company's constitutive act, shareholder details, and registered address, among other required documents.

Companies operating under the Industrial Free Zones regime are exempt from import duties on raw materials, equipment, and other inputs used in production. This exemption is governed by Law 8-90 on Industrial Free Zones, which also covers exemptions from VAT and municipal taxes for qualifying entities. The exemptions apply for the period the company holds active free zone status, subject to renewal and compliance conditions set by the National Free Zones Council (CNZF).

The Dominican Republic has signed bilateral investment treaties (BITs) with several countries that include protections against unlawful expropriation and guarantee access to international arbitration in the event of an investment dispute. The specific protections available to your business depend on your country of incorporation or the nationality of the investor, as treaty coverage varies by signatory. Where a BIT applies, investors generally have the right to seek compensation through ICSID or other agreed arbitral forums rather than relying solely on domestic courts.

Minimum capital requirements for both the SRL and SA structures are relatively low by regional standards, making entry accessible for small and mid-sized foreign businesses. An SA requires a minimum authorized capital of RD$30,000,000, while SRL formation does not carry a fixed statutory minimum capital under the General Companies Law (Ley General de las Sociedades Comerciales y Empresas Individuales de Responsabilidad Limitada, Law 479-08). Capital requirements in regulated industries, such as banking or insurance, are set separately by the relevant sectoral regulator.

A company incorporated and operating in the Dominican Republic can access CAFTA-DR preferential tariffs on eligible goods exported to the United States and other signatory countries, provided it meets the agreement's rules of origin requirements. CAFTA-DR does not confer automatic trade benefits simply by virtue of incorporation; the goods or services must meet defined origin thresholds. Businesses in manufacturing or agro-industrial sectors tend to benefit most directly, given the agreement's structure around physical goods and tariff classification.

Failure to meet compliance obligations under Law 8-90 can result in suspension or revocation of free zone status by the National Free Zones Council (CNZF). If status is revoked, the company loses its exemptions from corporate income tax, import duties, and other fiscal benefits retroactively or prospectively, depending on the nature of the violation. Maintaining accurate production records, employment thresholds, and export documentation is typically required to sustain an active free zone license.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.