Key Takeaways

- Czechia's Business Corporations Act (Act No. 90/2012 Coll.) governs the formation and operation of all major commercial entities, with the Czech Commercial Register administered by regional courts serving as the central repository for filings, ownership records, and financial statements.

- The Společnost s Ručením Omezeným (s.r.o.) is the most commonly registered entity in Czechia, distinguished by its relatively low capital requirement and limited personal liability for its members.

- Branch offices (Odštěpný Závod) expose the foreign parent company to full liability for Czech operations, whereas representative offices are legally restricted to non-revenue-generating activities.

- General Commercial Partnerships (Veřejná Obchodní Společnost, v.o.s.) and Limited Partnerships (Komanditní Společnost, k.s.) both place personal liability on at least some partners, making liability separation unavailable to all participants in these structures.

Introduction to Entity Types in Czechia

Czechia is a landlocked Central European country bordering Germany, Austria, Slovakia, and Poland. An independent republic and EU member state, it operates under a civil law system codified primarily through Act No. 90/2012 Coll., the Business Corporations Act, which governs the formation and operation of most commercial entities.

Company registration falls under the jurisdiction of the Czech Commercial Register, administered by the regional courts. Filings, ownership records, and annual financial statements are publicly accessible through this registry. The country operates a standard EU-aligned tax framework — corporate income is taxed at a flat rate, with no territorial or zero-tax exemptions applicable to domestic entities.

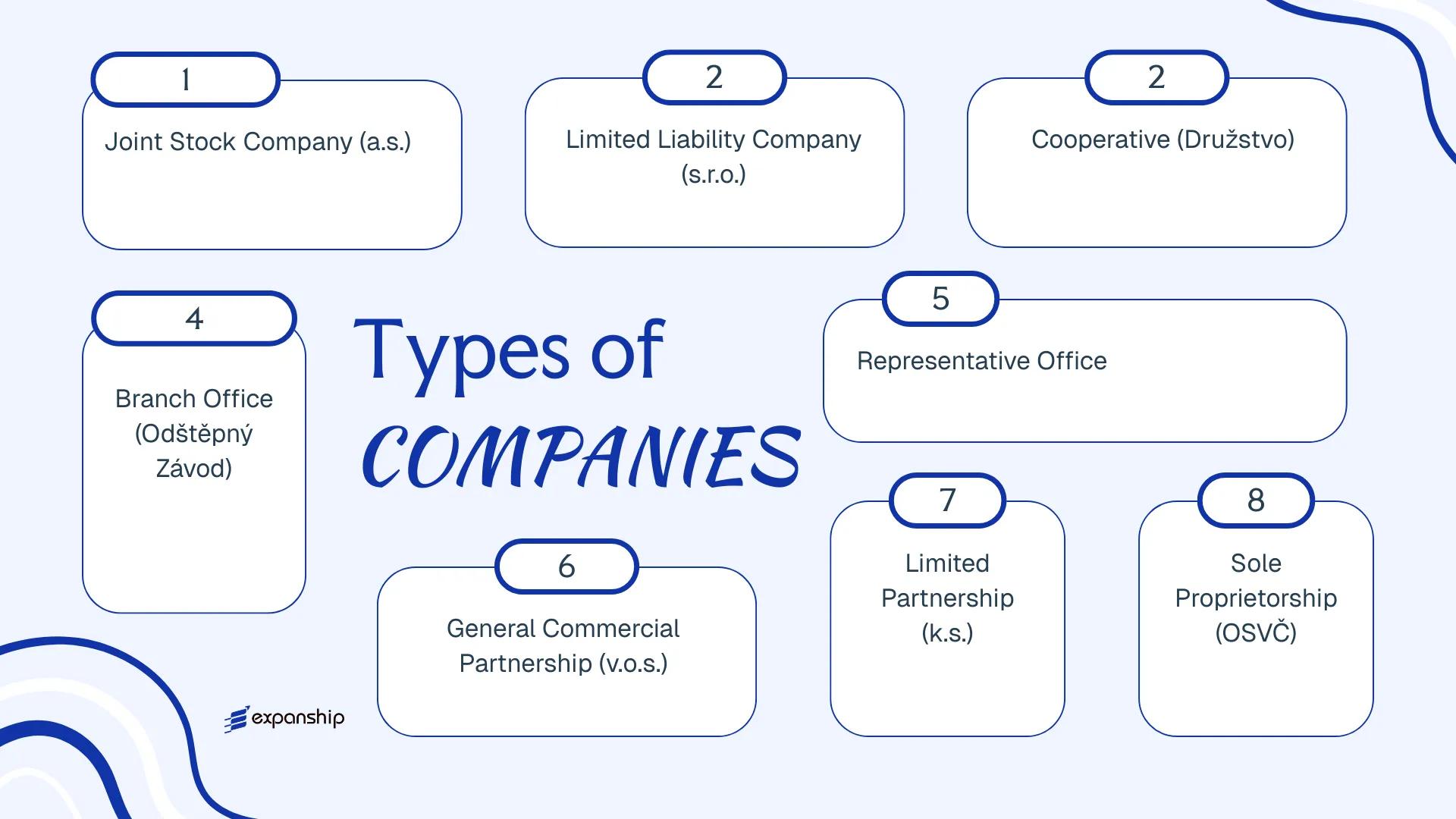

Available types of business entities in Czechia span both incorporated and unincorporated forms:

- Joint Stock Company (Akciová Společnost, a.s.)

- Limited Liability Company (Společnost s Ručením Omezeným, s.r.o.)

- Cooperative (Družstvo)

- General Commercial Partnership (Veřejná Obchodní Společnost, v.o.s.)

- Limited Partnership (Komanditní Společnost, k.s.)

- Branch Office (Odštěpný Závod)

- Representative Office

- Sole Proprietorship (Živnostník / OSVČ)

Each of these Czech legal entity types carries distinct liability, governance, and compliance obligations, all of which the sections below examine in detail.

An Overview of Business Structures in Czechia

Governed by the Act on Business Corporations (Zákon o obchodních korporacích, No. 90/2012 Coll.) and supplemented by the Civil Code (No. 89/2012 Coll.), Czech corporate law recognises several distinct legal forms available to domestic and foreign entities. An overview of company structures in Czech Republic spans capital companies, personal companies, cooperatives, sole proprietorships, and foreign entity structures. Each form carries different implications for liability, governance, and permitted activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Joint Stock Company (a.s.) | Capital company | Limited to shares | Taxable | Yes | 1 founder | Commercial Register, CNB (if listed) | ZOK No. 90/2012 Coll. |

| Limited Liability Company (s.r.o.) | Capital company | Limited to contribution | Taxable | Yes | 1 member | Commercial Register | ZOK No. 90/2012 Coll. |

| Cooperative (Družstvo) | Cooperative entity | Limited | Taxable | Yes | 3 members | Commercial Register | ZOK No. 90/2012 Coll. |

| Branch Office | Foreign entity form | Parent bears full liability | Taxable (Czech-source) | Yes | 1 parent entity | Commercial Register | Civil Code No. 89/2012 Coll. |

| Representative Office | Foreign entity form | Parent bears full liability | Generally non-taxable | No | 1 parent entity | Trade Licensing Office | Civil Code No. 89/2012 Coll. |

| General Commercial Partnership (v.o.s.) | Personal company | Unlimited, joint | Taxable at partner level | Yes | 2 partners | Commercial Register | ZOK No. 90/2012 Coll. |

| Limited Partnership (k.s.) | Personal company | Mixed | Taxable at partner level | Yes | 2 partners (1 general, 1 limited) | Commercial Register | ZOK No. 90/2012 Coll. |

| Sole Proprietorship (OSVČ) | Individual business | Unlimited, personal | Taxable (personal income) | Yes | 1 individual | Trade Licensing Office | Trade Licensing Act No. 455/1991 Coll. |

Each of these structures is examined in full in the sections below.

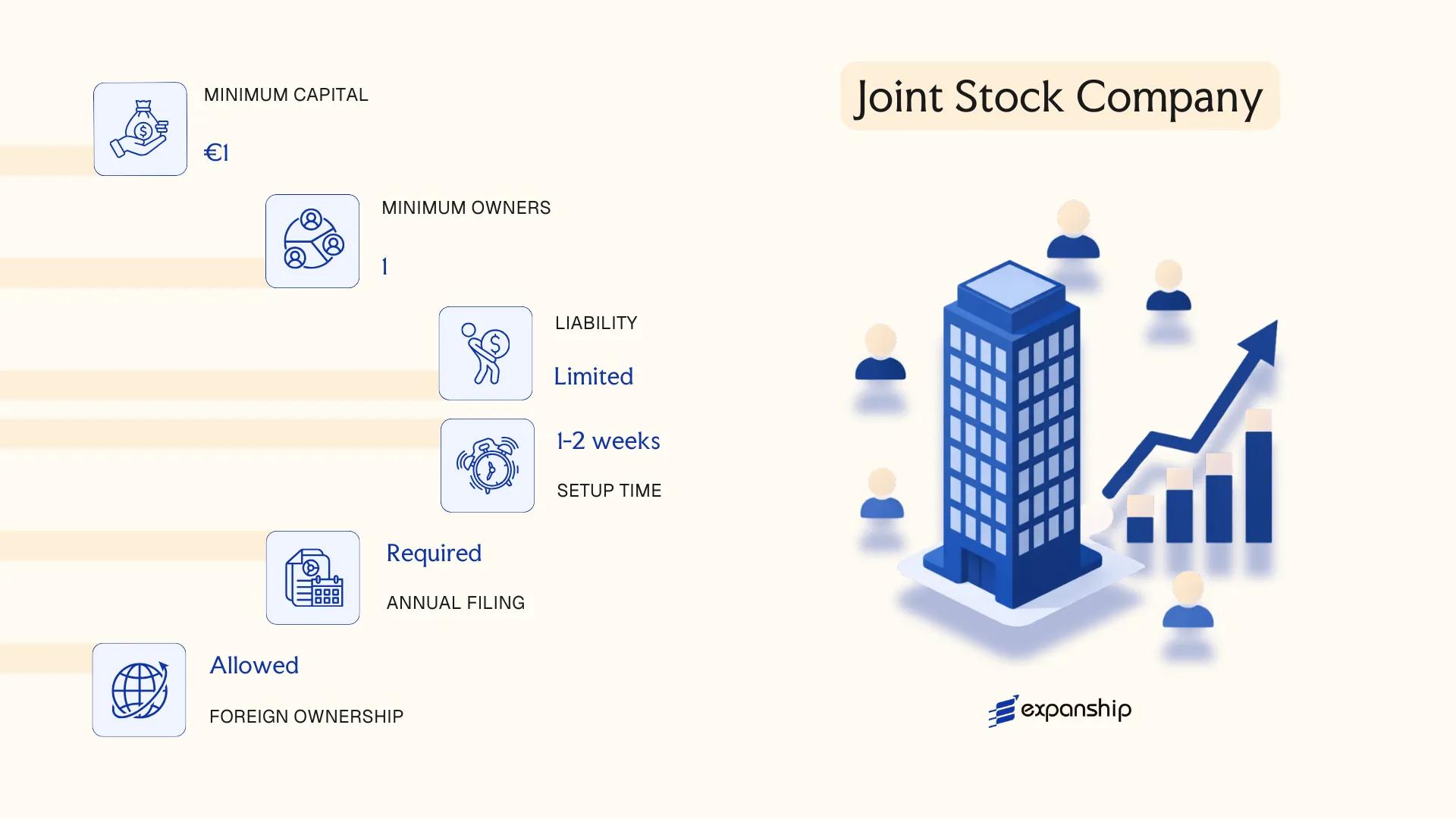

Joint Stock Company (Akciová Společnost, a.s.)

Governed by the Czech Business Corporations Act (Zákon o obchodních korporacích, Act No. 90/2012 Coll.), the akciová společnost a.s. registration process establishes an entity with full legal personality, entirely separate from its shareholders. Liability is limited to the value of subscribed shares, making this structure suitable for larger commercial operations or businesses intending to raise capital from external investors.

Share capital is divided into transferable shares, which may be issued as registered or bearer shares, subject to conditions under the Act. The entity can be formed by a single founder — whether a natural or legal person — without an upper limit on the number of shareholders.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company (a.s.) | Separate legal personality; shareholders not personally liable |

| Governing Body Members | Shareholders, Board of Directors, Supervisory Board (or monistic: Administrative Board + Statutory Director) | Two structural models available under Act No. 90/2012 Coll. |

| Members | Minimum 1 shareholder; no maximum | Single-founder formation permitted |

| Local Presence | Registered office address in Czech Republic required | Physical or c/o address acceptable; no mandatory local director |

| Share Capital | Minimum CZK 2,000,000 (approx. EUR 80,000) | At least 30% of each cash contribution must be paid up at incorporation |

| Privacy | Shareholders disclosed in the Commercial Register (Obchodní rejstřík) | Publicly searchable |

Focus Points

- Taxation: Subject to Czech corporate income tax at 21%; dividends distributed to foreign shareholders may attract 15% withholding tax, reduced under applicable double tax treaties; standard VAT rate of 21% applies to taxable supplies; no stamp duty on share transfers.

- Annual Compliance: Mandatory filing of audited financial statements with the Obchodní rejstřík; audit required when statutory thresholds on turnover, assets, or headcount are met.

- Treaty Access: Czechia's extensive double tax treaty network is accessible to a.s. entities, subject to beneficial ownership conditions.

- Conversion: An a.s. may be transformed into an s.r.o. or other legal form through a statutory transformation process under Act No. 125/2008 Coll.

Sub-Types

Monistic Structure (Monistická Struktura)

Rather than a separate Board of Directors and Supervisory Board, a monistic a.s. operates with a single Administrative Board and a Statutory Director. This model reduces governance overhead and is often used by closely held firms or single-shareholder entities.

Public Company (Veřejná a.s.)

A public a.s. may offer shares to the public and list on a regulated market. Additional obligations under capital markets regulation and Czech National Bank (ČNB) oversight apply, distinguishing it from the standard private a.s.

When to Use an a.s.

The a.s. suits businesses seeking external investment, planning a public offering, or operating as a holding vehicle where share transferability and investor structuring flexibility are priorities. The minimum capital requirement of CZK 2,000,000 is the primary practical barrier for smaller ventures.

The a.s. is best suited for large-scale commercial operations, institutional investors, and businesses with plans for structured equity financing or eventual public listing.

Company Incorporation in Czechia

Incorporate a Czech joint stock company or other legal entity with end-to-end support from Expanship.

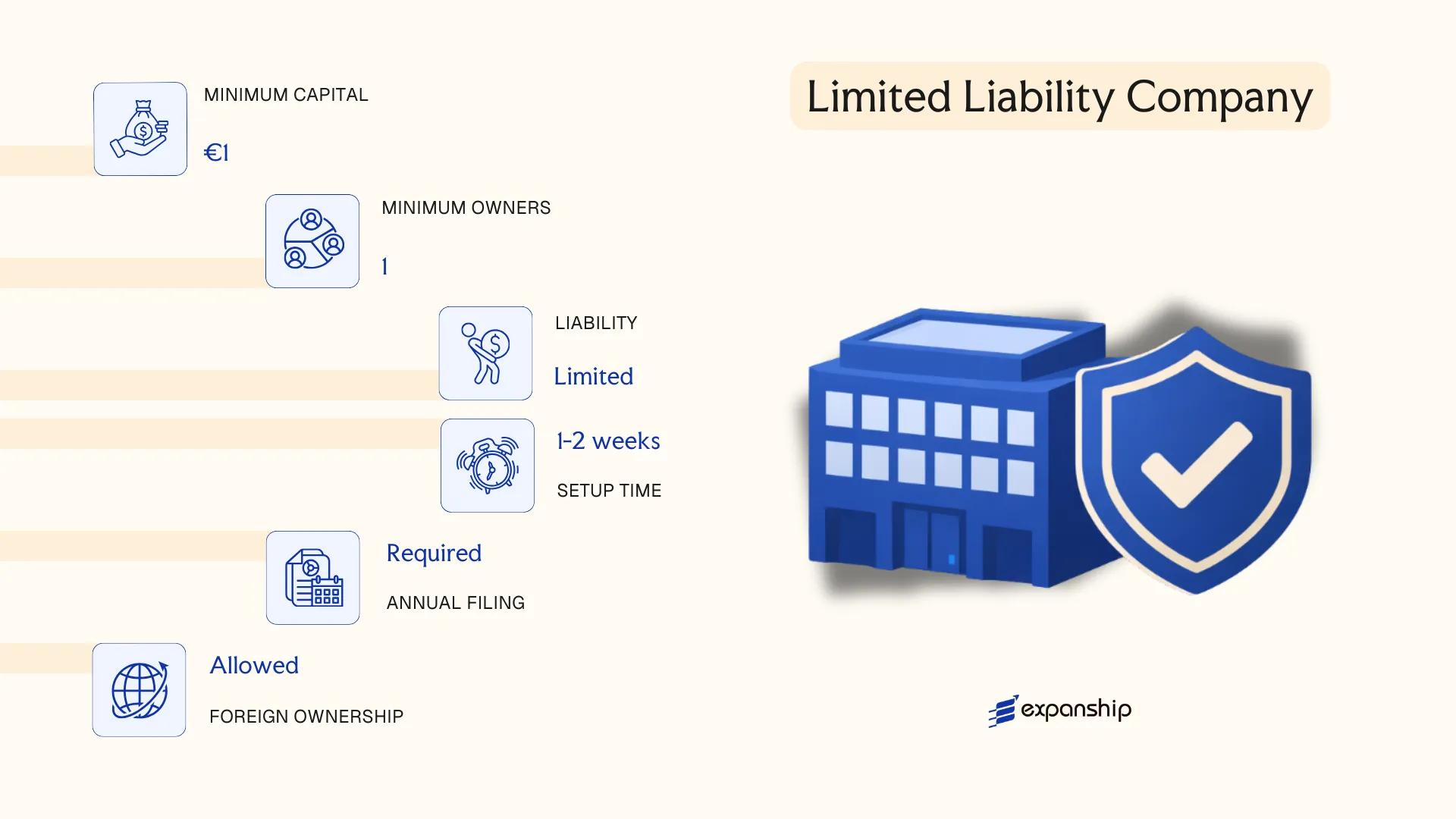

Limited Liability Company (Společnost s Ručením Omezeným, s.r.o.)

The s.r.o. company formation Czech Republic process is governed by Act No. 90/2012 Coll., the Business Corporations Act (Zákon o obchodních korporacích), which came into force on 1 January 2014. The entity carries separate legal personality, meaning it holds rights and obligations in its own name, distinct from its members.

Liability is capped at each member's unpaid capital contribution. This hybrid structure — combining corporate limited liability with comparatively flexible governance — makes the společnost s ručením omezeným setup accessible to a wide range of business models.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private limited liability company | Registered in the Commercial Register (Obchodní rejstřík) maintained by the regional courts |

| Members | 1–50 members (natural persons or legal entities) | Members hold business shares (obchodní podíl); a single-member s.r.o. is permitted |

| Management | Minimum one executive director (jednatel) | Directors need not be Czech residents; corporate directors are not permitted |

| Local Presence | Registered office address in Czechia required | A physical or virtual address is acceptable; no mandatory resident agent |

| Share Capital | Minimum CZK 1 per member contribution; no prescribed total minimum | Each contribution must be at least CZK 1; total capital reflects sum of contributions |

| Privacy | Members and directors disclosed in the Commercial Register | Register is publicly searchable; nominee arrangements are legally permissible but must reflect true economic ownership |

Focus Points

- Taxation: Subject to 21% corporate income tax; standard VAT rate of 21% applies once registration thresholds are met; withholding tax of 15% applies to profit distributions to non-resident members, subject to applicable double tax treaty reductions; no stamp duty on share transfers.

- Annual Compliance: Financial statements must be filed with the Commercial Register annually; an ordinary general meeting is required at least once per year.

- Economic Substance: No statutory substance requirement beyond the registered office, though tax residency rules under Czech law and EU anti-avoidance directives may require genuine local management.

- Treaty Access: As a Czech tax resident entity, the s.r.o. can access Czechia's network of double tax treaties, including EU Parent-Subsidiary Directive benefits.

- Conversion: An s.r.o. may be converted into a joint stock company (a.s.) or other recognised corporate forms through a statutory transformation process under Act No. 125/2008 Coll.

Registering a Czech limited liability company s.r.o. suits trading operations, holding structures, and IP ownership vehicles where full corporate liability protection is required without the administrative burden of a joint stock company. The minimal share capital threshold is a practical advantage; the public disclosure of members and directors limits structural confidentiality.

Best suited for foreign entrepreneurs and SMEs seeking a straightforward corporate presence in Czechia with full limited liability and access to EU treaty benefits.

Cooperative (Družstvo)

Governed by the Czech Corporations Act (Zákon o obchodních korporacích, Act No. 90/2012 Coll.), the cooperative is a member-owned legal entity with separate legal personality and limited liability for its members. Czech cooperative (družstvo) formation follows a distinct path from capital companies: the entity exists primarily to serve the economic, social, or cultural interests of its members rather than to generate profit for external shareholders.

Liability exposure is capped at each member's membership contribution, making this structure a hybrid between a mutual association and a conventional commercial entity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Cooperative (Družstvo) | Separate legal personality; governed by Act No. 90/2012 Coll. |

| Members | Minimum 3 members; no maximum | Members hold membership interests, not shares; referred to as "members" (členové) |

| Governing Bodies | Members' Meeting, Board of Directors (představenstvo), Supervisory Board (kontrolní komise) | Supervisory Board mandatory when member count exceeds 50 |

| Registered Office | Physical address in Czechia required | Must be maintained for the duration of the cooperative's existence |

| Capital | Minimum registered capital CZK 1; cooperative fund contributions set in statutes | Member contributions defined in the founding statutes (stanovy) |

| Privacy | Members' register not publicly filed | Board members are recorded in the Commercial Register (Obchodní rejstřík) |

Focus Points

- Taxation: Subject to 21% corporate income tax; VAT registration required above the CZK 2,000,000 threshold; member profit distributions may attract withholding tax under applicable rules.

- Annual Compliance: Annual financial statements must be filed with the Commercial Register; members' meeting must convene at least once per year.

- Economic Substance: The cooperative must conduct genuine activity aligned with its stated purpose as defined in its statutes.

- Conversion: A cooperative may be converted into a capital company (s.r.o. or a.s.) through a statutory transformation process under Act No. 125/2008 Coll.

- Restrictions: The cooperative structure cannot be used solely as a holding or investment vehicle; its purpose must demonstrably serve member interests.

Sub-Types

Housing Cooperative (Bytové Družstvo)

Established specifically for the purpose of managing, maintaining, or acquiring residential property for the benefit of its members. Membership is tied to tenancy rights over a specific residential unit rather than a general economic interest.

Social Cooperative (Sociální Družstvo)

Defined under Act No. 90/2012 Coll. as a cooperative whose activities promote social cohesion, employment of disadvantaged persons, or community development. At least 10% of profit must be reinvested into the cooperative's public benefit activities rather than distributed to members.

Closing

The cooperative structure suits member-based ventures such as agricultural operations, worker-owned enterprises, or housing projects where collective governance takes precedence over investor returns. Its accessible minimum capital requirement is a practical advantage, though the mandatory governance structure and member-service obligation add administrative weight that purely commercial entities do not carry.

Best suited for groups of three or more individuals or entities seeking a collectively governed structure aligned with shared economic, housing, or social objectives rather than external profit distribution.

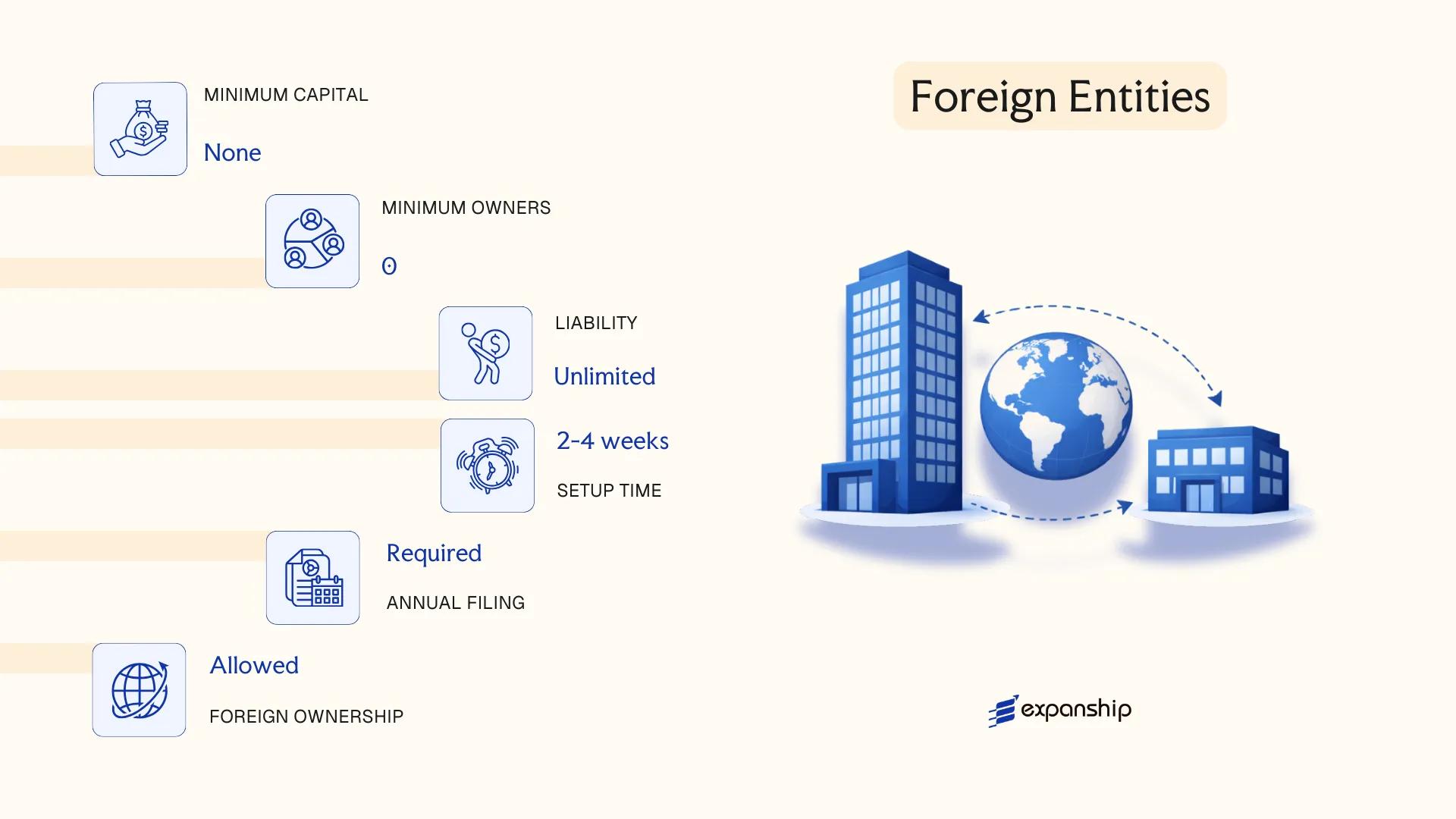

Foreign Entities in Czechia [Branch Office (Odštěpný Závod), Representative Office]

A foreign company branch office Czech Republic can be established under the Act on Business Corporations (Zákon o obchodních korporacích, No. 90/2012 Coll.) and the Civil Code (No. 89/2012 Coll.). Neither a branch office (odštěpný závod) nor a representative office carries separate legal personality — both remain organisational units of the foreign parent.

Registration is handled through the Commercial Register (Obchodní rejstřík) administered by the relevant regional court. A branch must be registered before commencing any commercial activity, while a representative office is typically used for non-commercial functions such as market research or liaison activities and does not require the same registration formality.

Key Characteristics

| Requirement | Branch Office (Odštěpný Závod) | Representative Office |

|---|---|---|

| Legal Form | Organisational unit of foreign entity; no separate legal personality | Non-commercial unit of foreign entity; no separate legal personality |

| Manager | Appointed representative (vedoucí odštěpného závodu) registered in Commercial Register | Appointed representative; no Commercial Register entry required |

| Local Presence | Registered address in Czech Republic; registered manager required | Operational address required |

| Capital | No minimum capital requirement; parent's capital applies | No capital requirement |

| Liability | Parent company bears full liability | Parent company bears full liability |

| Privacy | Manager's name and address publicly listed in Commercial Register | Not publicly registered |

Focus Points

- Taxation: Branch profits are subject to 21% corporate income tax; VAT registration required if turnover exceeds CZK 2 million; no separate withholding tax on branch profit remittances, though treaty provisions may apply to specific payments.

- Economic substance: The branch must maintain a genuine operational presence; the registered manager must be identifiable and reachable at the Czech address.

- Annual compliance: Branches must file annual financial statements derived from the parent's accounts with the Commercial Register; representative offices have no equivalent filing obligation.

- Treaty access: As an extension of the foreign parent, a branch may access double tax treaty benefits applicable to the parent's country of residence, subject to treaty terms.

- Restrictions: A representative office cannot generate revenue or enter into commercial contracts in its own name; doing so effectively requires conversion to a registered branch or a locally incorporated entity.

Sub-Types

Branch Office (Odštěpný Závod)

Registered in the Commercial Register and authorised to conduct commercial operations, the branch office is the standard structure for foreign firms seeking operational activity without incorporating a separate Czech legal entity. All contractual obligations bind the foreign parent directly.

Representative Office

Used exclusively for preparatory and auxiliary activities — such as advertising, information gathering, or liaison — this form carries no commercial mandate. No odštěpný závod registration in Czechia is required, but the firm should maintain documented evidence that activities remain non-commercial to avoid reclassification.

Closing

Both structures suit foreign firms testing the Czech market or maintaining a limited operational presence before committing to full incorporation. The branch offers operational flexibility without a separate capitalisation requirement, though the parent's unlimited exposure to Czech liabilities is a material constraint.

Foreign companies seeking a low-commitment operational or liaison presence in the Czech market before committing to a locally incorporated entity.

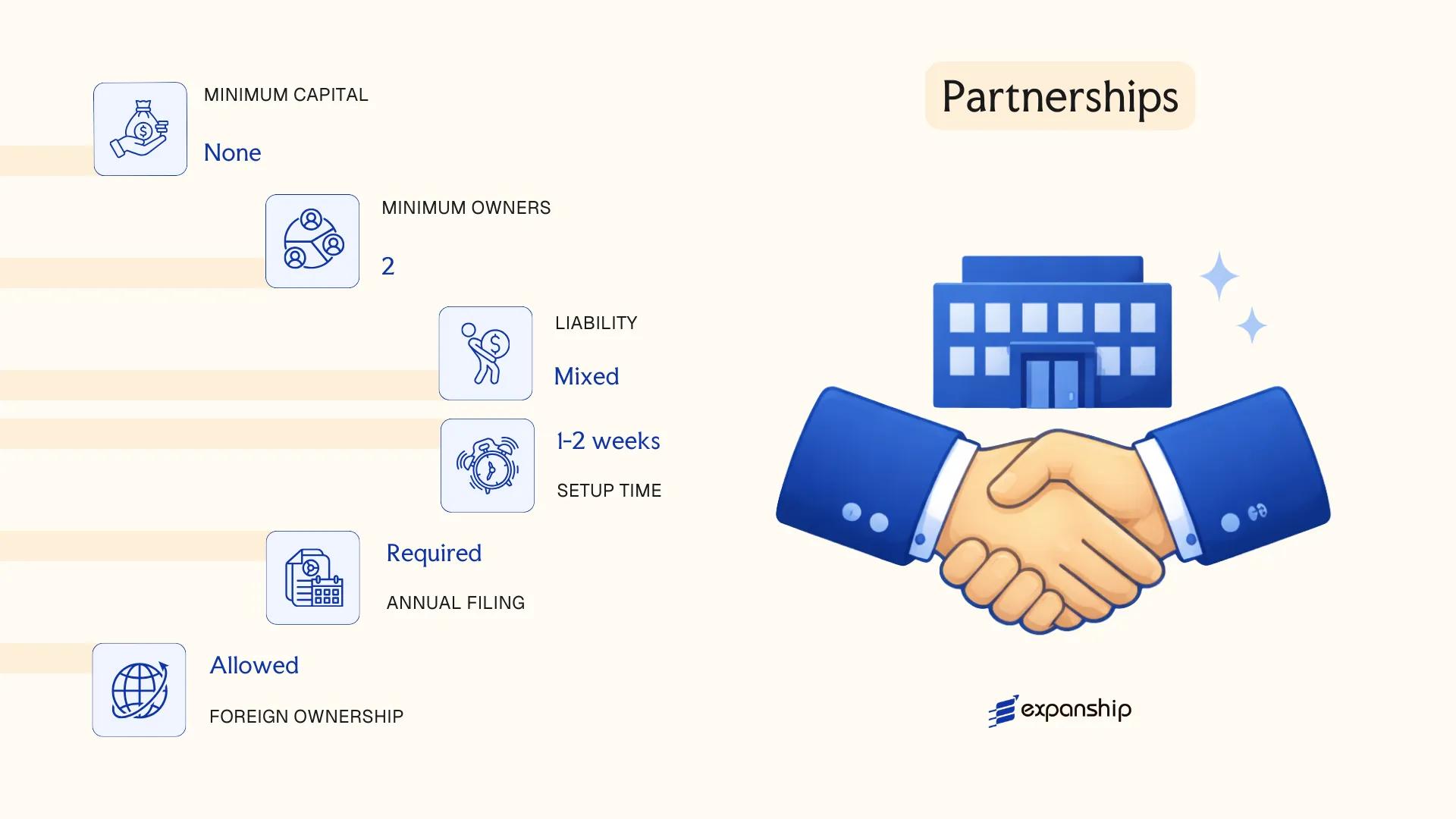

Partnerships in Czechia [General Commercial Partnership (Veřejná Obchodní Společnost, v.o.s.), Limited Partnership (Komanditní Společnost, k.s.)]

Both partnership structures available under Czech law are governed by Act No. 90/2012 Coll., the Business Corporations Act (Zákon o obchodních korporacích), which replaced the former Commercial Code in 2014. Unlike capital companies, partnerships in Czech law place greater emphasis on the personal involvement and liability of their members.

A general commercial partnership v.o.s. (veřejná obchodní společnost) carries unlimited joint and several liability for all partners, while a limited partnership (komanditní společnost, k.s.) creates a two-tier membership structure with differing liability profiles for each partner category.

Key Characteristics

| Requirement | v.o.s. | k.s. |

|---|---|---|

| Legal Form | General Commercial Partnership | Limited Partnership |

| Members | Partners (společníci); minimum 2, no maximum; all bear unlimited liability | General partners (komplementáři, min. 1) bear unlimited liability; limited partners (komanditisté, min. 1) bear liability up to their contribution |

| Capital | No minimum capital requirement | Limited partners must make a contribution as defined in the articles; no statutory minimum |

| Local Presence | Registered address in Czech Republic required | Registered address in Czech Republic required |

| Privacy | Partner names filed in the Commercial Register (Obchodní rejstřík); publicly accessible | Both komplementáři and komanditisté names appear in the Commercial Register |

Focus Points

- Taxation: Both structures are fiscally transparent at entity level; profits are allocated to individual partners and taxed under personal income tax at 15% (or 23% above a threshold), with corporate tax applying only to komplementáři who are legal entities. Standard VAT rules apply if turnover exceeds CZK 2 million.

- Annual Compliance: Financial statements must be filed with the Commercial Register; audit requirements depend on size thresholds.

- Conversion: Either structure may be converted into a capital company (s.r.o. or a.s.) under the Business Transformations Act (Act No. 125/2008 Coll.).

- Restrictions: Neither structure is permitted for regulated financial or banking activities without specific licensing.

Closing

Both structures suit domestic professional services firms or family-operated businesses where personal accountability among partners is acceptable. The pass-through taxation is a functional advantage, but unlimited liability for general partners represents a significant exposure that limits suitability for higher-risk commercial activities.

Czech partnership structures are best suited for small professional firms or family businesses where partners actively manage operations and are comfortable with personal liability.

Sole Proprietorship (Živnostník / OSVČ)

The živnostník OSVČ sole proprietorship in Czechia is governed primarily by the Trade Licensing Act (Act No. 455/1991 Coll.), with supplementary provisions under the Civil Code (Act No. 89/2012 Coll.). Unlike capital companies, this form carries no separate legal personality — the individual and the business are treated as a single legal subject.

Registration is handled through the Trade Licensing Office (Živnostenský úřad), and the proprietor is simultaneously required to register with the Czech Social Security Administration (ČSSZ) and a health insurance provider. There is no minimum capital requirement, and the setup process is relatively straightforward administratively.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Natural person (fyzická osoba) | No separate legal entity; business and individual are one |

| Members | Single proprietor | No partners, shareholders, or co-owners within this structure |

| Liability | Unlimited personal liability | All personal assets are exposed to business obligations |

| Local Presence | Registered address in Czechia required | Must correspond with a valid trade licence |

| Capital | No minimum capital | No paid-in capital obligation |

| Privacy | Name appears on public trade register | Business identity is publicly linked to the individual |

Focus Points

- Taxation: Subject to personal income tax at a flat rate of 15% (23% above the 48× average wage threshold); VAT registration mandatory once turnover exceeds CZK 2,000,000 annually; no corporate tax, withholding tax, or stamp duty applies at entity level.

- Social contributions: Mandatory contributions to state pension and health insurance, calculated as a percentage of the profit tax base.

- Annual compliance: Annual income tax return filed with the Financial Administration of the Czech Republic (Finanční správa); no statutory audit requirement.

- Conversion: Can convert into an s.r.o. by transferring the business as a going concern, though this requires a new incorporation process rather than a statutory conversion.

- Treaty access: As a natural person, the proprietor may access Czech double tax treaty benefits directly under individual residency status.

Closing

This structure suits freelancers, consultants, and sole traders conducting low-risk activity with limited transaction volume. The absence of capital requirements makes entry accessible, but unlimited personal liability is a significant structural exposure for anyone operating in sectors with material financial risk.

Individuals providing services or conducting small-scale trade who prioritise low administrative overhead over liability protection.

How to Choose the Right Entity Type in Czechia

Selecting the correct structure before registration is one of the most consequential decisions in the formation process. Understanding how to choose a business structure in Czech Republic requires mapping your operational, tax, and governance requirements against what each entity legally permits.

Why Your Entity Choice Matters

The wrong structure creates concrete, correctable-but-costly problems:

- If you register a branch office but conduct independent commercial activity, the branch lacks separate legal personality under Czech law, exposing the parent to unlimited liability for local obligations.

- Choosing an s.r.o. when your intended activity requires public share issuance forces a costly conversion to an a.s. under Act No. 90/2012 Coll. (the Business Corporations Act).

- Selecting a cooperative when capital investment and investor exit flexibility are priorities locks your business into membership-based governance rules that restrict share transferability.

- Forming an a.s. when your firm is a single-person consultancy triggers mandatory supervisory board thresholds and statutory audit obligations that add significant annual compliance costs.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each correspond to distinct structures under Act No. 90/2012 Coll..

- Ownership and Management: Single-member ownership suits an s.r.o., while multi-investor structures with public capital-raising require an a.s.

- Liability Exposure: Your tolerance for personal liability distinguishes limited structures from general partnerships, where partners remain jointly and severally liable.

- Tax Objectives: Treaty access, dividend withholding rates, and participation exemption eligibility differ across entity types and affect your effective tax position.

- Substance Capacity: If you cannot maintain a physical presence, a representative office or branch may be more appropriate than a standalone Czech entity.

- Exit Strategy: Conversion between entity types is possible but administratively burdensome; structures that permit redomiciliation or straightforward wind-up proceedings offer greater long-term flexibility.

Compliance Services for Companies in Czechia

Ongoing compliance support for Czech entities, including annual filings, registered agent services, and statutory obligation management.

Conclusion

Czechia offers a defined set of legal structures under the Business Corporations Act (Act No. 90/2012 Coll.), each suited to distinct operational profiles. The s.r.o. remains the most registered entity in the country, favored for its relatively low capital threshold and contained personal liability. The a.s. serves capital-intensive ventures requiring shareholder anonymity or public market access. Cooperatives fit member-owned, collectively managed operations rather than standard commercial activity. Branch offices carry the full liability of their foreign parent, while representative offices are limited to non-revenue functions. Partnerships place personal liability on at least some partners, making them less common for incorporating a business in Czechia guide contexts where liability separation is a priority.

Regulatory direction has trended toward greater digitalization, with the Business Register (Obchodní Rejstřík) increasingly handling filings electronically. This trajectory, alongside Czechia's expanding tax treaty network, continues to shape how foreign investors assess the jurisdiction for holding and operational structures.

How Expanship Can Assist You

Expanship's company formation services Czech Republic covers every entity type discussed in this guide — from registering an s.r.o. with the Commercial Register (Obchodní rejstřík) maintained by the regional courts, to establishing an a.s. or filing a branch office through the Czech Trade Authority (Živnostenský úřad). Our team works directly within the Czech regulatory framework so your entity is structured and registered correctly from the outset.

Here is what our corporate services cover:

- Document preparation, notarization, and apostille legalization

- Registered agent and registered office provision in Czechia

- Filing with the Commercial Register and relevant authorities

- Trade license applications through the Živnostenský úřad

- Post-incorporation compliance management, including annual obligations

- Banking introduction assistance for newly incorporated entities

Reach out to Expanship Czechia to discuss your specific requirements with our team.

Frequently Asked Questions (FAQ)

The s.r.o. (Společnost s Ručením Omezeným) is the dominant choice for new registrations. Its minimum share capital requirement of CZK 1, combined with limited liability protection, makes it accessible to small businesses and international investors alike.

A branch office (Odštěpný Závod) is not a separate legal entity — it remains an extension of the foreign parent, which bears full liability for its Czech operations. An s.r.o. holds its own legal personality, files independently with the Commercial Register, and is taxed as a Czech resident entity under the Income Taxes Act (Act No. 586/1992 Coll.). Compliance obligations are generally heavier for an s.r.o., but the liability separation is correspondingly stronger.

Among Czech structures, the s.r.o. historically offered more discretion, though the Beneficial Ownership Register (introduced under Act No. 37/2021 Coll.) now requires disclosure of ultimate beneficial owners across all entity types. Nominee arrangements are legally permissible but do not exempt a firm from UBO registration requirements.

A sole proprietor (OSVČ) and an s.r.o. can each be established by one individual. General commercial partnerships (v.o.s.) require a minimum of two partners, and a limited partnership (k.s.) requires at least one general and one limited partner, so those structures cannot be formed by a single founder.

Foreign nationals face no nationality restrictions when forming an s.r.o. or a.s. under the Czech Business Corporations Act (Act No. 90/2012 Coll.). A foreign individual may serve as the sole shareholder and director of an s.r.o., though a registered Czech address and, in some cases, a trade licence (živnostenské oprávnění) issued by the relevant Trade Licensing Authority will be required.

Czech law permits transformation between entity types, governed by Act No. 125/2008 Coll. on Transformations of Commercial Companies and Cooperatives. An s.r.o. can be converted into an a.s., and vice versa, through a formal transformation process that includes a notarial deed and re-registration in the Commercial Register.

No. A branch office (Odštěpný Závod) and a representative office do not possess legal personality independent of their parent. By contrast, the s.r.o., a.s., v.o.s., k.s., and Družstvo are each recognised as separate legal persons under Czech private law.

The OSVČ (sole proprietor) has the lightest ongoing compliance burden: no annual financial statements are filed with the Commercial Register, and accounting requirements are simplified compared to capital companies. An s.r.o. or a.s., by contrast, must deposit annual financial statements in the Collection of Documents maintained by the Commercial Register.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.