Key Takeaways

- Czechia's 19% corporate income tax rate under Act No. 586/1992 Coll. provides a measurable cost advantage for businesses structuring cross-border operations within the EU.

- Because the S.R.O. carries no statutory minimum share capital requirement, founders retain full use of their capital for operational purposes from the moment the entity is registered.

- An extensive bilateral double tax treaty network reduces withholding tax exposure on cross-border income flows, making Czechia a practical base for businesses with clients or counterparties across multiple jurisdictions.

- EU membership gives a Czech-registered entity direct access to the single market's unified rules on goods, services, and capital movement, removing the legal friction that would otherwise apply to cross-border commercial relationships across member states.

Czechia is a landlocked EU member state in Central Europe, bordering Germany, Austria, Slovakia, and Poland. As a sovereign republic, it operates under a stable constitutional framework with company registration overseen by the Ministry of Justice, which maintains the public Commercial Register. Foreign businesses looking to establish a local presence most commonly do so through an s.r.o. The country's tax posture is treaty-based, with an extensive network of bilateral agreements that shapes how cross-border income is treated. Foreign ownership of Czech entities faces no general statutory restrictions, and the government maintains an open stance toward inbound foreign direct investment across most sectors.

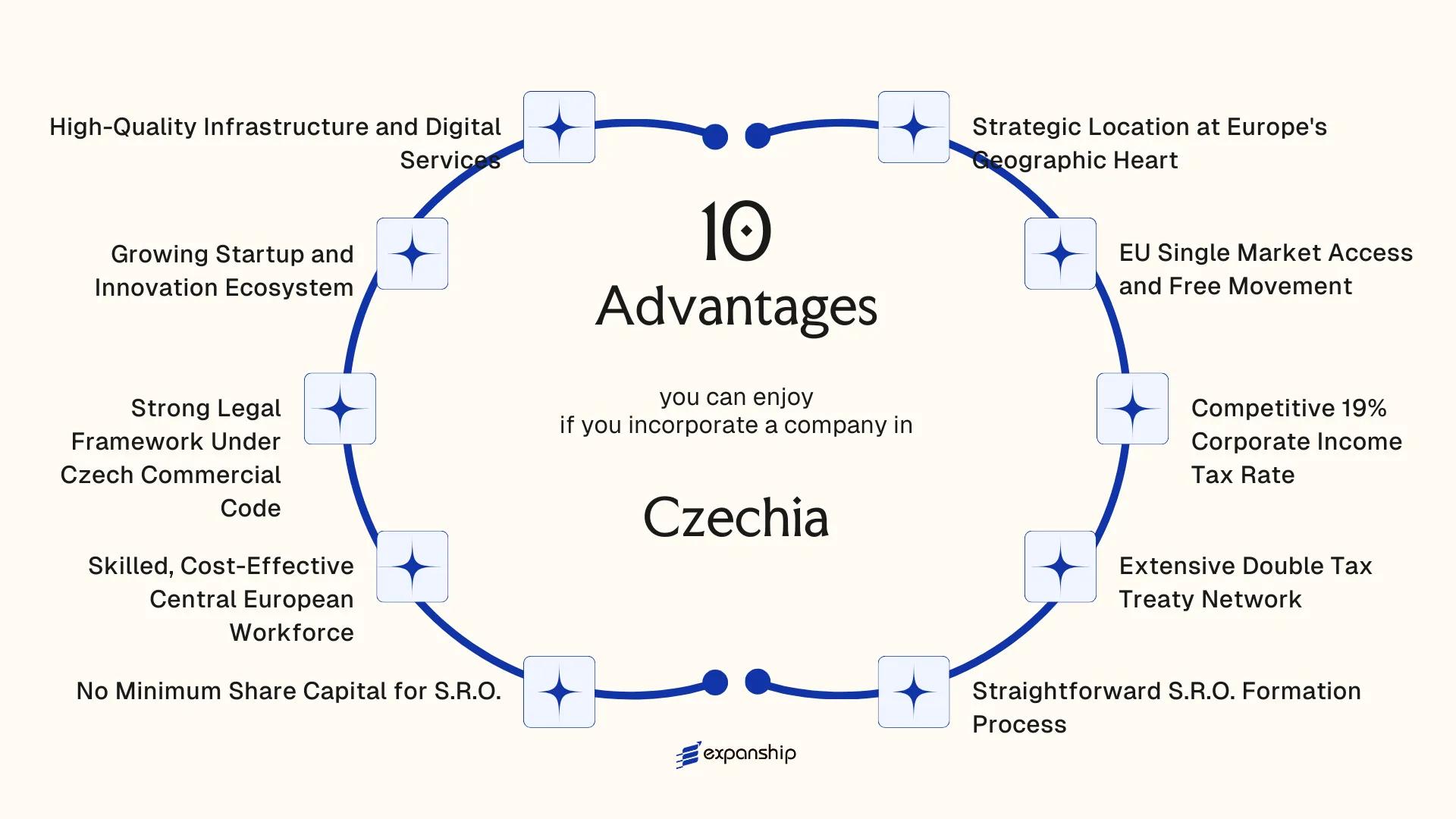

The benefits of incorporating in Czechia extend across legal, fiscal, and operational dimensions. Advantages of Czech company formation draw interest from businesses across Europe, Asia, and North America — reflecting the country's position as a credible commercial jurisdiction within the EU. This article examines the key factors that make why incorporate in Czech Republic a question worth answering for businesses at various stages of international expansion.

Strategic Location at Europe's Geographic Heart

Czechia's central Europe location advantages for business are, in large part, geographical. Sitting at the physical centre of the continent, the country shares borders with Germany, Austria, Poland, and Slovakia — placing your operations within a day's drive of the majority of European economic output.

Proximity to Major European Markets

Prague sits roughly 280 kilometres from Vienna, 350 kilometres from Berlin, and under 500 kilometres from Warsaw. For manufacturers, distributors, and logistics operators, that proximity means shorter lead times and reduced freight costs compared to businesses based on the Atlantic or Balkan periphery.

A Natural Hub for Regional Operations

Central European time alignment means your team in Prague can hold working hours with counterparts in both London and Kyiv simultaneously. Multinational firms frequently structure their regional headquarters here precisely because the Czech Republic's geographic position for companies reduces the operational friction of managing offices across multiple time zones.

Your Czech entity can serve as a distribution or coordination hub for both Western and Eastern European operations without requiring a secondary regional office.

EU Single Market Access and Free Movement

As a Czech-registered entity, your business operates under EU law with full access to the single market — a trading area covering over 450 million consumers across 27 member states. Czechia's accession to the EU in 2004 brought Czech companies under the Treaty on the Functioning of the European Union (TFEU), which enshrines the four fundamental freedoms: free movement of goods, services, capital, and persons.

For a foreign business owner, this translates directly into commercial reach. A Czech s.r.o. can sell goods into Germany, provide services in France, or hire employees from any EU member state without facing customs duties, import quotas, or work permit requirements that would otherwise apply to third-country entities.

Practical advantages that follow from EU membership include:

- Goods produced or cleared through Czech customs can circulate freely across the entire single market without re-inspection

- EU passporting rules allow certain regulated activities to operate across member states under a single authorization

- Freedom of capital movement permits unrestricted cross-border transfers within the EU, simplifying treasury and investment structures

- EU public procurement directives give Czech-registered firms equal standing to bid on government contracts across member states

Non-EU shareholders can fully own a Czech entity and still access these rights, provided the company itself is validly incorporated under Czech law.

Incorporate a Company in Czechia

Register your Czech s.r.o. and access the EU single market through one of Central Europe's most established business jurisdictions.

Competitive 19% Corporate Income Tax Rate

At 19%, the Czech Republic 19% corporate tax rate advantage is one of the more tangible financial reasons to establish an entity here. The rate applies to the taxable base of a Czech legal entity, calculated under the Income Taxes Act (Act No. 586/1992 Coll.) after allowable deductions. For foreign investors accustomed to jurisdictions where headline rates exceed 25%, the difference in retained earnings compounds meaningfully over time.

| Parameter | Detail |

|---|---|

| Standard CIT Rate | 19% |

| Governing Legislation | Act No. 586/1992 Coll. on Income Taxes |

| Tax Year | Calendar year or approved fiscal year |

| Investment Fund Rate | 5% (qualifying funds) |

| Witholding Tax on Dividends | 15% (resident), subject to treaty reduction |

Qualifying investment funds face a reduced 5% rate, and dividend distributions to EU parent companies may fall under the Parent-Subsidiary Directive, potentially eliminating withholding tax altogether where the parent holds at least a 10% stake for a minimum 12-month period. Your business structure determines which of these provisions applies.

The tax base itself is calculated from accounting profit, adjusted under Czech tax rules. Deductible items include depreciation under statutory asset categories, research and development cost deductions, and loss carry-forwards of up to five years. These mechanics allow your firm to reduce its effective tax burden below the 19% headline figure in capital-intensive or R&D-active operations.

Extensive Double Tax Treaty Network

Czech Republic double tax treaty network benefits are material rather than theoretical. The country has concluded over 90 bilateral tax treaties, covering most major economies across Europe, Asia, North America, and the Middle East. For a foreign investor routing income through a Czech entity, this reach significantly reduces the risk of the same profit being taxed twice.

Under these treaties, withholding tax rates on dividends, interest, and royalties paid from a Czech company to a foreign parent or shareholder are often reduced below the domestic statutory rate. Treaty eligibility is governed by the residence of the beneficial owner, so the structure of your shareholding directly determines which rate applies.

Practically, this means a business using a Czech s.r.o. as an operating or holding entity can distribute profits to a treaty-partner jurisdiction at a reduced withholding rate, governed by the specific treaty text published by the Ministry of Finance.

Keep these points in mind:

- Confirm the treaty is in force, not merely signed

- Verify that your entity qualifies as a tax resident under Czech law (place of management matters)

- Check the specific article covering the income type, as rates differ by category

- Beneficial ownership requirements must be satisfied, not merely formal ownership

- Some treaties include limitation-on-benefits or principal purpose test clauses

Czechia's treaty with South Korea predates many comparable Central European economies' agreements, giving Czech-resident entities an earlier and often more favorable withholding rate framework for income flows to and from Seoul.

Straightforward S.R.O. Formation Process

Registering an s.r.o. under Czech law does not require a drawn-out bureaucratic process. The Czech S.R.O. formation benefits for investors stem partly from a legal framework that has been progressively simplified, making entry into the Czech market faster than in many comparable EU jurisdictions.

Single Founder, Online Registration

An s.r.o. can be established by a single natural or legal person, including a foreign national or foreign corporate entity. Registration is handled through the Commercial Register maintained by the Regional Courts, and since amendments to the Business Corporations Act (zákon č. 90/2012 Sb.), notarial deeds for founding documents can be executed before a Czech notary without requiring the founder to be physically present through a valid power of attorney. That procedural flexibility reduces both travel costs and lead time for foreign incorporators.

Speed as a Structural Feature

The statutory timeframe for court registration, once all documents are submitted correctly, is five business days. For a foreign investor structuring an entry into the EU, that predictability means operational timelines can be planned with a degree of certainty that longer, more variable registration processes elsewhere cannot offer. The Trade Licensing Office (Živnostenský úřad) issues the necessary trade license in parallel, so both authorizations can be secured within a tight window rather than sequentially.

Start Your Czech S.R.O. Formation with Expanship

Get guidance on incorporating your s.r.o. in Czechia, from document preparation through Commercial Register filing.

No Minimum Share Capital for S.R.O.

Under Czech law, a společnost s ručením omezeným can be formed with a minimum registered share capital of just CZK 1 per member, down from the previous CZK 200,000 threshold following amendments to Act No. 90/2012 Coll., the Act on Business Corporations (ZOK). The Czech S.R.O. no minimum share capital advantage is straightforward: you are not required to lock up significant capital before your business generates any revenue.

- Capital efficiency from day one: You can incorporate with a nominal amount and direct available funds toward operations, hiring, or market entry instead of satisfying a statutory deposit requirement.

- Reduced formation cost: Since no substantial paid-in capital is mandated at registration, your upfront financial commitment is limited to notarial fees, court registration costs, and professional service charges.

- Accessible structure for lean business models: Startups, consultancies, and holding entities that do not require large asset bases can adopt the S.R.O. without overcapitalizing the entity relative to its actual needs.

- Flexibility under ZOK: The same legislation permits capital increases post-incorporation through standard member resolutions, so the structure can scale as your business grows without requiring a different legal form.

Each member's liability remains limited to their unpaid contribution, so the low capital threshold does not alter the core liability protection the entity form provides.

Skilled, Cost-Effective Central European Workforce

Czech Republic skilled workforce advantages for companies stem from a combination of technical education depth and wage levels that remain significantly below Western European averages. Average gross monthly wages in Czechia sit around CZK 43,000–45,000 (approximately EUR 1,750–1,850), compared to EUR 3,500–4,000 in Germany or Austria for comparable roles. For a foreign-owned s.r.o. employing technical staff, that differential directly reduces operating costs without sacrificing output quality.

Czech universities, including the Czech Technical University in Prague and Brno University of Technology, produce a steady supply of engineers, software developers, and applied scientists. The country has a long industrial heritage in manufacturing and precision engineering, which means experienced mid-career talent is available across sectors, not just entry-level graduates.

Employment relationships are governed by Act No. 262/2006 Coll., the Labour Code, which sets out clear frameworks for contracts, working hours, and termination. That predictability matters when structuring a workforce from abroad.

A foreign-owned s.r.o. hiring 10 mid-level software engineers in Prague at an average gross salary of CZK 70,000/month would incur approximately CZK 700,000 monthly in gross payroll. An equivalent team in Munich at EUR 5,500/month gross would cost roughly EUR 55,000 — nearly three times more at current exchange rates.

Strong Legal Framework Under Czech Commercial Code

The Czech Commercial Code legal framework benefits foreign business owners through a codified, predictable legal environment. The primary legislation governing companies, the Act on Business Corporations (Zákon o obchodních korporacích, No. 90/2012 Coll.), defines the rights and obligations of shareholders, directors, and corporate structures with precision. For foreign investors, this predictability reduces legal uncertainty when structuring ownership, profit distribution, or management authority.

Czech contract law and corporate disputes fall under the jurisdiction of general civil courts, with the Prague Municipal Court maintaining a dedicated commercial register. Entities registered there have their corporate documents publicly accessible, which supports due diligence for international partners and creditors.

The legal system draws from continental European tradition, meaning your firm's legal counsel in Germany, Austria, or France will find the framework broadly familiar. This compatibility lowers the cost of cross-border legal advisory work.

- Czech corporate law aligns with EU directives on company law, shareholder rights, and financial reporting

- The Civil Code (No. 89/2012 Coll.) governs contractual relationships with clear rules on liability and enforcement

- Intellectual property protections operate under both national law and EU regulations, with the Industrial Property Office (Úřad průmyslového vlastnictví) as the competent authority

The Act on Business Corporations applies by default, but certain provisions can be modified by the company's articles of association, so the specific protections available to your business depend on how the founding document is drafted.

Growing Startup and Innovation Ecosystem

Czech Republic startup ecosystem advantages are increasingly visible through concrete government programs and institutional infrastructure, not just informal networks. Prague, in particular, has become a recognized Central European base for early-stage technology firms and venture-backed businesses.

State-Backed Funding Through CzechInvest

CzechInvest, the government investment and business development agency operating under the Ministry of Industry and Trade, actively channels EU structural funds and national grants toward qualifying startups and innovative SMEs. Access to this funding does not require Czech citizenship, meaning foreign-owned entities registered in the country can apply on equal footing. For a firm entering European markets, this reduces early-stage capital pressure without diluting equity.

R&D Tax Incentives Under the Income Tax Act

Under Act No. 586/1992 Coll. (the Income Tax Act), businesses can claim a deduction of 100% of qualifying research and development expenditures on top of the standard cost deduction. This super-deduction effectively doubles the tax value of R&D spending for eligible activities. Technology firms allocating budgets to product development can reduce taxable income more aggressively than in many peer EU jurisdictions.

Talent Pipeline from Technical Universities

- Czech Technical University in Prague (CTU) and Brno University of Technology produce thousands of engineering and computer science graduates annually.

- Several universities run accelerator programs with direct links to commercial startups.

- The concentration of technical graduates keeps recruitment costs lower than in Western Europe while maintaining output quality.

This talent supply reduces hiring friction for foreign tech businesses establishing development or engineering teams locally.

High-Quality Infrastructure and Digital Services

Czech Republic digital infrastructure advantages for business extend well beyond basic connectivity. The country ranks among the top performers in the EU for fixed broadband penetration, and its mobile network coverage reaches the vast majority of the population. For a foreign-owned s.r.o., this means reliable day-to-day operations without dependence on costly private infrastructure.

The Czech government has invested significantly in digitalising public administration under the framework of the Digital Czechia strategy, which aligns with the EU's Digital Decade targets. Businesses registered in the country can interact with most public authorities through the CZECHPOINT network and the government's datové schránky (data boxes) system. Every legal entity is assigned a data box upon registration, enabling legally binding electronic communication with courts, tax authorities, and state bodies without physical presence.

Key infrastructure advantages relevant to foreign-owned entities include:

- The datové schránky system eliminates the need to appear in person for most official correspondence, reducing administrative overhead for non-resident directors

- Prague's data centre density supports hosting, fintech, and IT service operations with low-latency access to Western European markets

- The country's road and rail freight network, including its position on Trans-European Transport Network (TEN-T) corridors, supports manufacturing and logistics companies with direct connections to Germany, Austria, and Slovakia

- Electronic filing with the Czech Tax Administration (Finanční správa) and the Czech Social Security Administration (ČSSZ) is standard, not optional

Czechia's integration of e-government tools into mandatory business processes means your firm can meet statutory obligations remotely, which is a practical consideration for internationally mobile owners.

Why Czechia Stands Out Among European Business Destinations

Comparing the Czech Republic against other European business destinations reveals a consistent pattern: the combination of a moderate flat corporate tax rate, zero minimum share capital for the s.r.o., and full EU market membership positions the country competitively against jurisdictions that offer only one or two of these features simultaneously. The competitors most relevant to this comparison are Poland, Slovakia, and Austria — each geographically proximate, each targeting broadly similar foreign investors, and each frequently appearing in the same due-diligence shortlists.

Slovakia shares the same legal tradition and similar incorporation costs, yet its corporate tax rate sits at 21% for entities above a defined profit threshold, compared to the flat 19% rate applicable in Czechia. Austria offers exceptional legal stability and EU access but carries a minimum share capital requirement of €35,000 for a GmbH, which places an immediate capital burden on early-stage foreign entrants. Poland presents a large domestic market advantage but involves a more layered compliance structure under the Krajowy Rejestr Sądowy system. Across these parameters, the Czech s.r.o. framework under the Zákon o obchodních korporacích holds a measurably favourable position for cost-conscious foreign incorporations.

| Parameter | Czechia | Slovakia | Austria | Poland |

|---|---|---|---|---|

| Corporate Tax Rate | 19% (flat) | 21% (above threshold) | 25% | 19% (standard) |

| Minimum Share Capital (private entity) | CZK 1 (~€0.04) | €1 | €35,000 | PLN 5,000 (~€1,150) |

| EU Member State | Yes | Yes | Yes | Yes |

| Double Tax Treaties | 90+ | 70+ | 90+ | 90+ |

| Standard VAT Rate | 21% | 20% | 20% | 23% |

Compliance Services for Czech Companies

Maintain your Czech s.r.o. in good standing with ongoing statutory filings, registered office support, and regulatory reporting under Czech law.

Conclusion

The benefits of incorporating in Czech Republic rest on a coherent combination of structural and regulatory factors rather than any single feature. A 19% corporate income tax rate applied under Act No. 586/1992 Coll., combined with one of Europe's more extensive double tax treaty networks, reduces the cost of cross-border operations in a measurable way. The S.R.O. structure, with no statutory minimum share capital requirement, means capital that might otherwise be tied up in paid-in requirements remains available for operational use from day one.

EU membership translates directly into legal certainty for your business. Goods, services, and capital move across member state borders under unified rules, which matters when your clients or suppliers are distributed across Europe. The Czech Commercial Code provides a codified framework that foreign directors and shareholders can rely on without navigating parallel or conflicting legal systems.

Whether this structure suits your business depends on your industry, the location of your customers, and how your holding or operating entities are arranged. A technology firm with European clients faces different considerations than a manufacturing operation or a financial services entity. The case for a Czech entity is strongest when EU market access, workforce access, and tax treaty coverage align with your existing or planned commercial relationships. For businesses where those factors apply, formation through the Czech trade licensing system and Commercial Register provides a defined, documented path to an operational EU entity.

Start Your Czech S.R.O. with Expanship Today

Expanship supports foreign business owners through the full cycle of forming and maintaining a Czech s.r.o., from preparing founding documents in line with the requirements of the Czech Commercial Code (zákon č. 90/2012 Sb.) to filing with the Municipal Court in Prague or the relevant regional court acting as the commercial register authority. The firm's work spans the entity types, share capital rules, tax registration obligations, and compliance obligations discussed across this blog.

Expanship Czech Republic company formation services cover the practical steps that foreign founders typically find difficult to execute remotely:

- Preparation and legalization of founding documents, including the memorandum of association

- Registered agent and registered office provision at a Czech address

- Filing with the commercial register and liaison with the Trade Licensing Office (Živnostenský úřad)

- Post-incorporation compliance management, including annual filing obligations

- Tax registration support with the Financial Administration of the Czech Republic (Finanční správa)

- Banking introduction assistance to support corporate account opening

To start your Czech s.r.o. with Expanship or discuss your specific requirements, contact Expanship Czech Republic.

Frequently Asked Questions (FAQ)

Once all formation documents are submitted to the relevant regional court maintaining the Commercial Register, registration is typically completed within five business days under Czech procedural rules. Preparation of the memorandum of association, notarisation, and obtaining a trade licence beforehand can add one to three weeks to the overall timeline. The total process from document preparation to active registration generally runs three to six weeks for foreign applicants.

The standard corporate income tax rate is 19% under the Czech Income Tax Act (Act No. 586/1992 Coll.). No general solidarity surcharge or municipal profit tax applies at the company level, so the statutory rate reflects the effective rate in most standard trading structures. Certain investment funds and pension funds are taxed at reduced rates, but these apply to specific regulated vehicles rather than standard trading companies.

Czech tax treaties frequently reduce or eliminate withholding tax on dividends, though the specific rate depends on the treaty with the shareholder's country of residence. Under domestic law, the standard withholding rate on dividends paid to non-resident shareholders is 15%. Where an applicable treaty or the EU Parent-Subsidiary Directive applies, this rate may be reduced to zero or a lower percentage, subject to minimum shareholding and holding period conditions.

A registered office address within Czech territory is a statutory requirement for s.r.o. registration under Act No. 90/2012 Coll. This address appears in the Commercial Register and serves as the official address for legal correspondence and regulatory notices. A virtual or serviced office address is permissible, provided the address provider confirms consent to its use as a registered seat.

Failure to deposit financial statements in the Collection of Deeds within the statutory deadline can result in fines imposed by the court maintaining the Commercial Register, or by the Czech Trade Inspection Authority in applicable cases. Persistent non-compliance may lead the court to initiate dissolution proceedings under Section 93 of Act No. 304/2013 Coll. on Public Registers. Directors also carry personal liability exposure where non-filing causes harm to creditors or third parties.

At 19%, the Czech corporate income tax rate is materially lower than Austria's 24% and Germany's combined federal and trade tax burden, which typically ranges between 28% and 33% depending on the municipality. Both Austria and Germany also impose more complex thin-capitalisation and controlled foreign corporation rules than those currently applied under Czech domestic law. For holding structures, the participation exemption under Czech law exempts qualifying dividend income and capital gains from subsidiaries, subject to minimum ownership thresholds.

Since an amendment to the Business Corporations Act took effect, the minimum share capital for an s.r.o. is CZK 1, effectively removing any meaningful capital barrier to formation. Each founder's contribution must be at least CZK 1, and the full amount of monetary contributions does not need to be paid up before registration, provided the memorandum of association specifies a payment schedule. The administrator of contributions, typically one of the founders, confirms the paid-up amount in a declaration submitted as part of the registration filing.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.