Key Takeaways

- Costa Rica's Código de Comercio provides eight distinct business entity types available to both residents and foreign investors, each carrying different implications for liability, governance, and capital structure.

- The Sociedad Anónima consistently accounts for the highest volume of registered entities in the country, making it the dominant incorporation vehicle under the Registro Nacional's records.

- Costa Rica's territorial tax system means that income generated outside the country is generally not subject to local income tax, a structurally significant feature for internationally operating businesses.

- Foreign entities can establish a market presence through a branch office or representative office without full local incorporation, offering a lower-commitment entry path governed by the Código de Comercio.

Introduction to Entity Types in Costa Rica

Costa Rica is an independent republic in Central America, bordered by Nicaragua to the north and Panama to the south. Company registration falls under the jurisdiction of the Registro Nacional, the national registry that administers the incorporation and maintenance of legal entities operating within the country.

Costa Rica operates a territorial tax system, meaning income generated outside the country is generally not subject to local income tax.

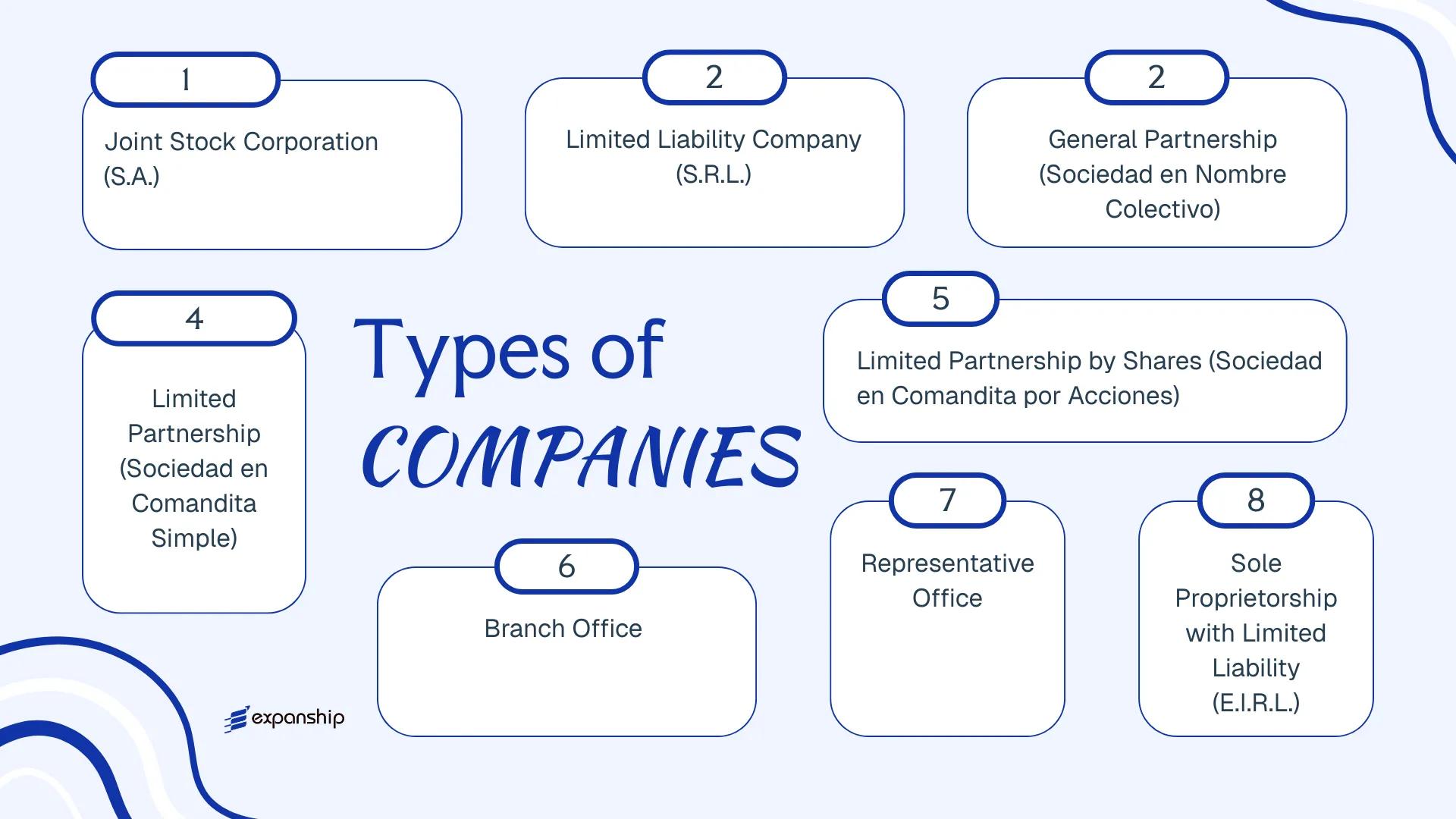

Several distinct business entity types in Costa Rica are available to both residents and foreign investors under the Código de Comercio (Commercial Code). These include the Sociedad Anónima (S.A.), Sociedad de Responsabilidad Limitada (S.R.L.), Sociedad en Nombre Colectivo, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones, Branch Office, Representative Office, and the Empresa Individual de Responsabilidad Limitada. Each structure carries different implications for liability, governance, and capital requirements.

The sections that follow examine each of these Costa Rica corporate entities in detail — covering formation requirements, ownership rules, and the practical considerations relevant to your business.

An Overview of Business Structures in Costa Rica

Costa Rica's commercial legislation recognises several distinct entity types, each governed primarily by the Código de Comercio (Commercial Code, Law No. 3284). The registry authority overseeing formation and ongoing filings is the Registro Nacional, specifically its Mercantile Registry division. Each structure carries different rules on liability, membership, and permitted commercial activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Sociedad Anónima (S.A.) | Joint Stock Corporation | Limited to share capital | Taxed | Yes | 2 shareholders | Registro Nacional | Código de Comercio |

| Sociedad de Responsabilidad Limitada (S.R.L.) | Limited Liability Company | Limited to quota capital | Taxed | Yes | 2 partners | Registro Nacional | Código de Comercio |

| Sociedad en Nombre Colectivo | General Partnership | Unlimited, joint | Taxed | Yes | 2 partners | Registro Nacional | Código de Comercio |

| Sociedad en Comandita Simple | Limited Partnership | Mixed (general/limited) | Taxed | Yes | 2 partners | Registro Nacional | Código de Comercio |

| Sociedad en Comandita por Acciones | Share-based Limited Partnership | Mixed (general/limited) | Taxed | Yes | 2 partners | Registro Nacional | Código de Comercio |

| Branch Office | Foreign entity extension | Parent bears liability | Taxed on local income | Yes | N/A | Registro Nacional | Código de Comercio |

| Representative Office | Non-trading presence | Parent bears liability | Generally exempt | No | N/A | Registro Nacional | Código de Comercio |

| Empresa Individual de Responsabilidad Limitada (E.I.R.L.) | Sole Proprietorship | Limited | Taxed | Yes | 1 individual | Registro Nacional | Law No. 9349 |

Each of these structures is examined in full in the sections below.

Sociedad Anónima (S.A.) — Costa Rica's Joint Stock Corporation

Governed by the Código de Comercio (Commercial Code, enacted in 1964 and subsequently amended), the Sociedad Anónima is the most widely used corporate structure for Costa Rica Sociedad Anónima formation. It carries separate legal personality, meaning the entity holds rights and obligations independent of its shareholders.

Liability is limited to each shareholder's subscribed capital contribution. This structure accommodates both closely held businesses and firms with broader ownership, making it a practical choice for foreign investors seeking S.A. company registration in Costa Rica.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad Anónima (S.A.) | Capital divided into transferable shares |

| Members | Shareholders: minimum 2, no maximum | Directors form a Board (Junta Directiva): minimum 3 officers (President, Secretary, Treasurer); shareholders and directors may overlap |

| Local Presence | Registered agent and registered legal address required | Registered agent must be a licensed attorney (abogado) in Costa Rica |

| Capital | No statutory minimum; denominated in Costa Rican Colones (CRC) | Shares must be subscribed at incorporation; at least 25% of subscribed capital must be paid in |

| Share Transfer | Shares are freely transferable unless restricted by the articles (pacto social) | Bearer shares are prohibited; all shares must be registered |

| Privacy | Shareholder and director information filed with the Registro Nacional | Records are publicly accessible |

Focus Points

- Taxation: Corporate income tax is applied on a territorial basis via the Dirección General de Tributación; rates are progressive for small businesses and a flat 30% for larger firms; VAT at 13% applies to taxable supplies; dividend withholding tax of 15% applies to distributions; stamp duties apply to certain notarized documents.

- Annual Compliance: Annual corporate tax returns, financial statements, and filings with the Registro Nacional are required; failure to file triggers penalties and eventual dissolution.

- Beneficial Ownership: Under Law 9416 (Ley para Mejorar la Lucha contra el Fraude Fiscal), beneficial ownership information must be reported to the Banco Central de Costa Rica annually.

- Economic Substance: No formal substance requirements exist beyond maintaining a registered address and agent, but territorial tax residency determinations may require demonstrating local management for specific income streams.

- Treaty Access: Costa Rica has a limited tax treaty network; the S.A. structure does not automatically confer treaty benefits, and treaty eligibility depends on the specific bilateral agreement.

Recommendations

The Sociedad Anónima suits trading operations, real estate holding, and joint ventures where share transferability is operationally useful. Its freely transferable share structure offers ownership flexibility, though the public nature of the Registro Nacional records limits shareholder privacy.

Foreign investors and multi-shareholder businesses seeking a structured corporate vehicle with clear governance and the ability to transfer ownership without restructuring the entity.

Company Incorporation in Costa Rica

Incorporate a Sociedad Anónima or other entity type in Costa Rica with end-to-end support from Expanship.

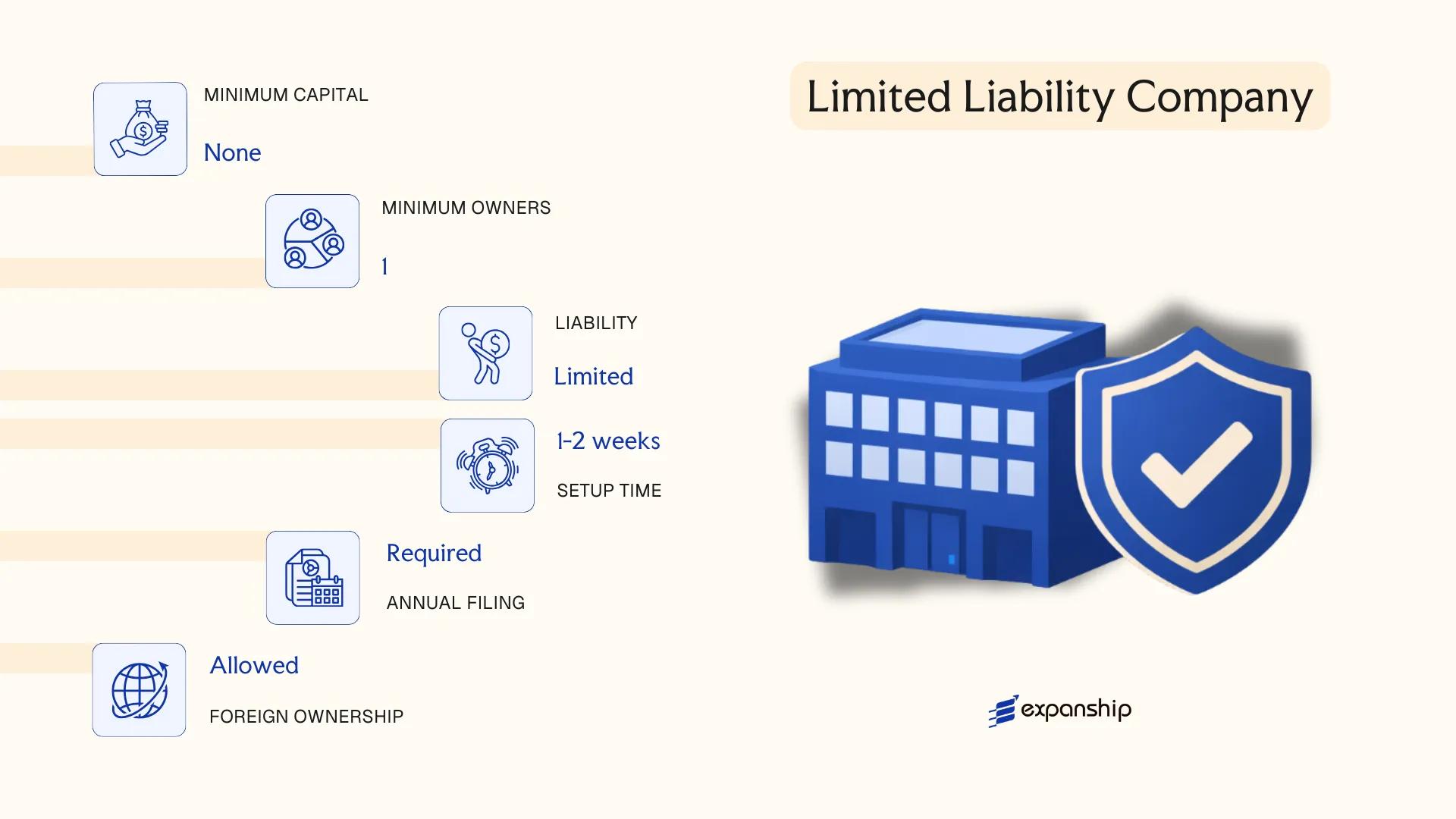

Sociedad de Responsabilidad Limitada (S.R.L.) — Limited Liability Company

The Costa Rica SRL limited liability company is governed by the Código de Comercio (Commercial Code), specifically articles 75 through 136, which have regulated this structure since the code's enactment in 1964. It carries separate legal personality, meaning the entity holds rights and obligations independently from its members.

Structurally, the Sociedad de Responsabilidad Limitada sits between a corporation and a partnership. Ownership is represented by participaciones (quotas) rather than freely transferable shares, and transfers to third parties generally require consent from the other members, making this a more closely held structure by default.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad de Responsabilidad Limitada (S.R.L.) | Registered with the Registro Nacional (National Registry) |

| Members | Referred to as socios (quota holders); minimum 2, maximum 25 | Exceeding 25 members requires conversion to an S.A. |

| Management | One or more gerentes (managers); need not be members | No board of directors required |

| Local Presence | Registered agent and registered address in Costa Rica required | Must maintain a registered office for official notifications |

| Capital | Denominated in Costa Rican Colones; no statutory minimum | Divided into quotas; each socio's liability capped at their capital contribution |

| Privacy | Beneficial ownership reported to BCCR/SUGEF under Law 9416 | Quota ownership not publicly searchable in the same manner as S.A. shares |

Focus Points

- Taxation: Subject to corporate income tax on Costa Rica-source income at progressive rates up to 30%; VAT at 13% applies to taxable supplies; withholding taxes apply to dividends and certain payments to non-residents; stamp duties apply at registration.

- Annual Compliance: Must file annual tax returns with the Ministerio de Hacienda and submit beneficial ownership declarations under Ley 9416 (Ley para Mejorar la Lucha contra el Fraude Fiscal).

- Quota Transfers: Third-party transfers require approval by socios representing at least 75% of capital unless the cuota agreement specifies otherwise, restricting liquidity.

- Treaty Access: Costa Rica has a limited tax treaty network; S.R.L. entities are generally treated as opaque for treaty purposes, but access depends on the specific bilateral agreement.

- Conversion: An S.R.L. may be converted to an S.A. through a formal notarial process and re-registration with the Registro Nacional, without dissolving the legal entity.

The S.R.L. registration in Costa Rica suits trading operations, family-held businesses, and joint ventures where partners want controlled ownership succession and simplified governance without a full board structure. The capped membership at 25 socios, however, limits scalability for businesses anticipating broader investor participation.

The S.R.L. is most appropriate for small-to-medium closely held businesses or joint ventures where ownership control and restricted transferability are deliberate priorities.

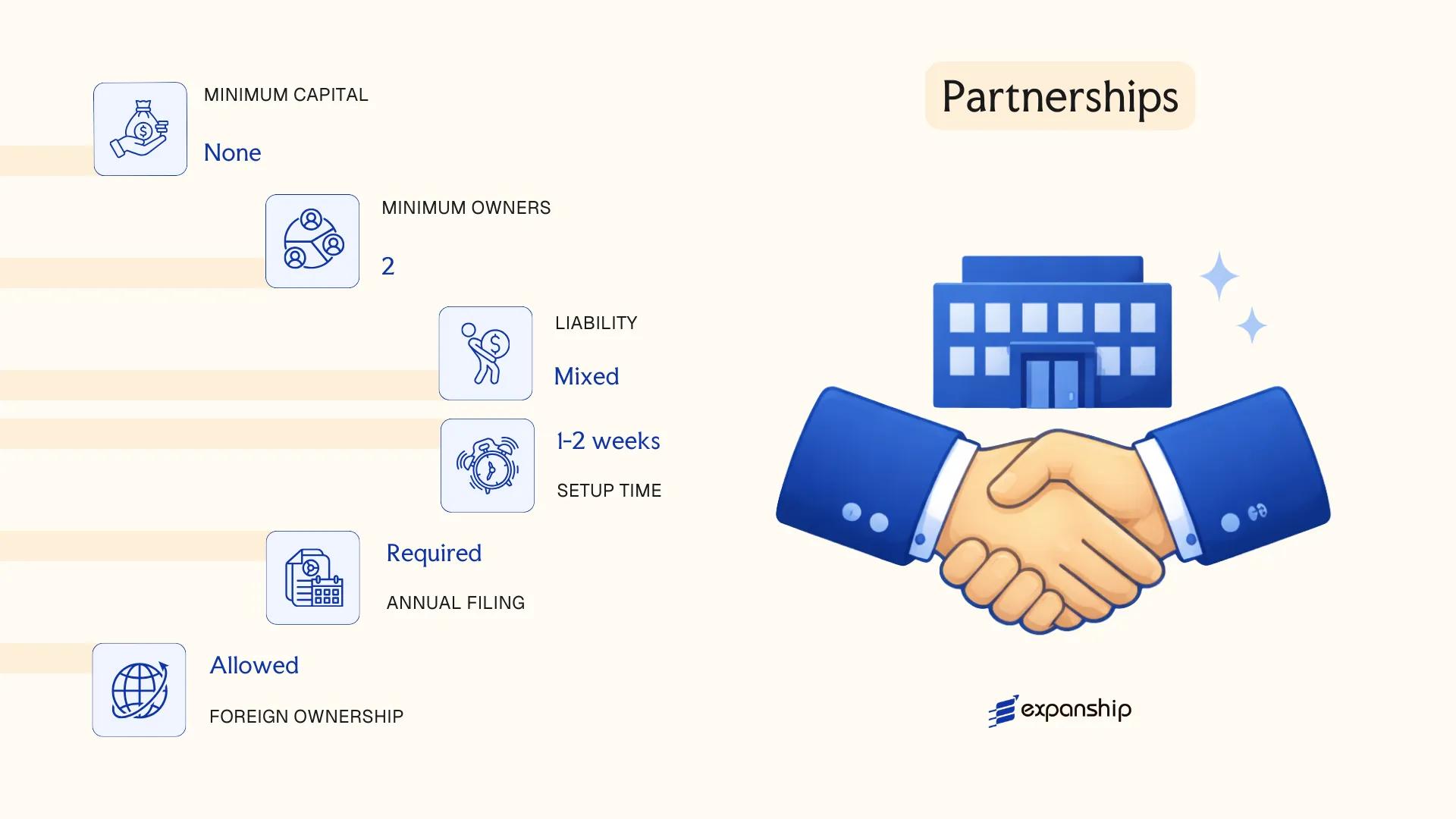

Partnerships in Costa Rica [Sociedad en Nombre Colectivo, Sociedad en Comandita Simple, Sociedad en Comandita por Acciones]

Costa Rica partnership business structures are governed by the Código de Comercio (Commercial Code), enacted in 1964, which recognises three distinct partnership forms. Each carries separate legal personality upon registration with the Registro Nacional (National Registry), though liability exposure varies significantly across the three structures.

Registration is completed through the Registro de Personas Jurídicas, a division of the National Registry. All three partnership types require the execution of a public deed before a licensed notary, followed by publication in the official gazette, La Gaceta.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sociedad en Nombre Colectivo / Sociedad en Comandita Simple / Sociedad en Comandita por Acciones | Three distinct legal entities under the Commercial Code |

| Members | Partners (socios) | Minimum 2; no statutory maximum. Comandita types require at least one general and one limited partner |

| Liability | General partners: unlimited personal liability; Limited partners: liability capped at capital contribution | Nombre Colectivo partners all bear unlimited liability |

| Local Presence | Registered legal address in Costa Rica; licensed notary required for incorporation | No mandatory resident director, but a local fiscal address is required |

| Capital | No statutory minimum; denominated in Costa Rican Colón (CRC) | Comandita por Acciones divides limited partners' capital into transferable shares |

| Privacy | Partner names appear in the public deed filed with the National Registry | Limited privacy; beneficial ownership data is subject to disclosure under AML regulations |

Focus Points

- Taxation: Partnerships are treated as transparent or opaque depending on structure; corporate income tax applies at rates between 5% and 30% on Costa Rican-source income; VAT at 13% applies to taxable supplies; withholding taxes apply to dividends and royalties paid abroad.

- Annual Compliance: Annual corporate tax declarations must be filed with the Ministerio de Hacienda; beneficial ownership registers must be updated with the National Registry annually.

- Restrictions: General partners in all three types must be individuals or legal entities capable of bearing liability; foreign nationals may participate but must comply with immigration and investment registration requirements.

- Conversion: Partnership structures can generally be converted to an S.A. or S.R.L. through a notarised deed and National Registry filing, subject to creditor notification.

Sub-Types

Sociedad en Nombre Colectivo

All partners hold unlimited, joint, and several liability for the firm's obligations. This structure is rarely used in modern commercial practice and is more common among small family-operated businesses where partners accept shared personal risk.

Sociedad en Comandita Simple

This form separates general partners, who bear unlimited liability and manage the business, from limited partners, whose exposure is capped at their capital contribution. Limited partners may not participate in management without forfeiting their liability protection.

Sociedad en Comandita por Acciones

Structurally similar to the Comandita Simple, but the limited partners' interests are represented by transferable shares rather than quota units. This allows greater flexibility in transferring ownership stakes without restructuring the entire partnership agreement.

Closing Paragraph

Partnership structures suit professional services firms, family businesses, or joint ventures where defined liability tiers are operationally practical. The Comandita por Acciones offers share transferability as a meaningful structural advantage, though the unlimited personal liability carried by general partners in all three forms represents a material drawback that limits their appeal for higher-risk commercial activities.

These structures are best suited for small family businesses or professional partnerships where all active participants accept personal liability exposure and share a long-term relationship of mutual trust.

Foreign Business Presence in Costa Rica [Branch Office, Representative Office]

Establishing a foreign company branch office in Costa Rica is governed primarily by the Código de Comercio (Commercial Code), specifically Articles 226 through 232, which regulate the registration of foreign entities operating within the country. A branch does not constitute a separate legal entity — it remains an extension of the parent company, which retains full liability for the branch's obligations.

Registration is administered through the Registro Nacional (National Registry), Mercantile Section. The process requires apostilled or legalized corporate documents from the parent company's home jurisdiction, translated into Spanish by a certified translator, and filed by a licensed Costa Rican attorney (notario público).

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Extension of foreign parent company | No separate legal personality |

| Designated Representative | Resident legal representative (apoderado) | Must hold sufficient power of attorney |

| Local Presence | Registered legal address required | Must maintain a physical or fiscal address in-country |

| Capital | No statutory minimum | Parent company's capital backs operations |

| Privacy | Director details filed with Registro Nacional | Publicly accessible records |

| Liability | Unlimited; falls on parent entity | No liability shield for the parent |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at standard territorial rates; remittances to the parent may attract withholding tax, and VAT obligations apply to taxable local activities.

- Annual Compliance: Annual declarations must be filed with the Ministerio de Hacienda; the beneficial ownership registry (ROBE) reporting obligations also apply.

- Economic Substance: No specific substance regime exists for branches, but the entity must demonstrate genuine local activity to maintain good standing.

- Treaty Access: Access to double tax treaty benefits depends on the parent company's home jurisdiction and treaty terms; Costa Rica's treaty network remains limited.

- Restrictions: Branches cannot issue shares or admit new equity partners independently of the parent structure.

Sub-Types

Representative Office

A representative office is a lighter form of foreign business presence, permitted to conduct promotional, market research, and liaison activities only. It cannot execute contracts, generate local revenue, or invoice clients directly. This structure is suited to foreign firms testing the market before committing to a full operational entity.

Closing

A branch office suits foreign companies that need direct operational presence without incorporating a separate local entity, though the unlimited liability exposure of the parent company is a material structural drawback for most multinationals.

Foreign companies seeking direct operational control in the local market that are prepared to accept parent-level liability for local activities.

Sole Proprietorship (Empresa Individual de Responsabilidad Limitada)

The Costa Rica Empresa Individual de Responsabilidad Limitada (EIRL) is governed by Law No. 9024, enacted in 2011, which introduced this entity as a formal mechanism for individual entrepreneurs to conduct business with limited personal liability.

Unlike a general sole proprietorship, the EIRL holds a separate legal personality from its owner, meaning the proprietor's personal assets are shielded from business debts and obligations up to the extent defined by the entity's registered capital.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Single-member limited liability entity | Separate legal personality from the proprietor |

| Members | One individual proprietor (minimum and maximum) | No corporate sole proprietorships permitted |

| Local Presence | Registered agent and registered address required | Must maintain a physical or legal address in Costa Rica |

| Capital | No statutory minimum; denominated in Costa Rican Colones (CRC) | Capital must be declared at registration with the National Registry |

| Privacy | Proprietor's name appears in the public registry | Beneficial ownership disclosures required under AML regulations |

Focus Points

- Taxation: Subject to territorial corporate income tax (0%–30% progressive rates on net income); VAT at 13% applies to taxable activities; standard withholding taxes apply to remittances abroad.

- Annual Compliance: Annual tax declarations must be filed with the Dirección General de Tributación; corporate books must be maintained and legalised.

- Conversion: The EIRL can be converted into an S.A. or S.R.L. through a formal notarial process and re-registration with the National Registry (Registro Nacional).

- Restrictions: Only natural persons may form an EIRL; legal entities are excluded from ownership.

Closing

The EIRL suits individual entrepreneurs operating small to medium trading or service businesses who require formal liability protection without the administrative overhead of a multi-member structure. Its single-owner constraint, however, makes it unsuitable for ventures requiring investor participation or share-based capital raising.

The EIRL is best suited for individual residents or established sole traders seeking formal liability separation under Costa Rican law without forming a multi-member company.

How to Choose the Right Entity Type in Costa Rica

Choosing the right company structure in Costa Rica affects tax exposure, liability, reporting obligations, and long-term operational flexibility. The decision is governed primarily by the Código de Comercio (Commercial Code), which defines the formation requirements and governance rules for each available structure.

Why Your Entity Choice Matters

Selecting an unsuitable structure produces concrete legal and financial consequences:

- Registering a branch or representative office without proper authorization from the Registro Nacional can result in operating illegally, exposing the business to fines or forced closure.

- Choosing a structure that lacks access to Costa Rica's tax treaty network means withholding tax reductions available under applicable bilateral agreements cannot be claimed by counterpart payers.

- Forming an S.A. when a single-person consultancy is the intended operation adds mandatory board composition requirements and associated annual compliance costs that an E.I.R.L. would not impose.

- Selecting an entity type that cannot hold licensed activities — financial services, insurance — results in rejection of the operating license application by the relevant regulatory body, such as the Superintendencia General de Entidades Financieras (SUGEF).

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each require different structures under Costa Rican commercial law.

- Ownership Structure: An S.R.L. suits closely held arrangements with few participants, while an S.A. accommodates broader share transferability and multi-party governance.

- Tax Objectives: Your eligibility for specific tax regimes under the Dirección General de Tributación depends on the entity type registered.

- Privacy Requirements: Both the S.A. and S.R.L. involve entries in the Registro Nacional's public registry; shareholder privacy requires additional structural consideration.

- Exit Strategy: Not all entity types permit redomiciliation or conversion under current Costa Rican law — confirm this before incorporating.

- Substance Capacity: If maintaining a local office and employees is not feasible, confirm whether your chosen structure carries minimum presence obligations.

Corporate Compliance Services in Costa Rica

Maintain good standing with the Registro Nacional and meet annual filing obligations across all entity types.

Conclusion

Setting up a company in Costa Rica requires matching your operational profile to a legal structure governed by the Código de Comercio. The Sociedad Anónima suits shareholders who require formal capital division and transferable shares; the Sociedad de Responsabilidad Limitada fits smaller ventures where ownership stability matters more than share liquidity. Partnership structures serve niche arrangements where partners accept shared liability. Branch offices and representative offices address foreign entities testing the market without full local incorporation. The Empresa Individual de Responsabilidad Limitada remains the narrowest option, built for sole operators.

The S.A. consistently accounts for the highest volume of registered entities in the country. Regulatory oversight from the Registro Nacional and tax administration through the Ministerio de Hacienda continue to evolve, with ongoing digitization of filing processes and incremental treaty developments shaping the compliance environment. Understanding which structure aligns with your ownership model and operational scope is where professional guidance adds measurable value.

How Expanship Can Assist You

Expanship provides Costa Rica company incorporation services covering the full range of entities discussed in this guide, from the Sociedad Anónima to the Sociedad de Responsabilidad Limitada. Every incorporation in Costa Rica runs through the Registro Nacional, and our team manages that process directly on your behalf.

From document preparation to post-registration compliance, our service scope includes:

- Drafting and legalizing articles of incorporation (pacto constitutivo)

- Registered agent and registered office provision

- Filing with the Registro Nacional and liaison with the Ministerio de Hacienda for tax registration

- Ongoing corporate maintenance, including annual Registro Nacional fees and shareholder registry updates

- Banking introduction assistance for your new entity in Costa Rica

Reach out to Expanship Costa Rica to discuss the right structure for your business.

Frequently Asked Questions (FAQ)

The Sociedad Anónima (S.A.) is the most frequently incorporated entity in the country. Its flexible share structure, broad statutory recognition, and established precedent in commercial practice make it the default choice for most local and foreign investors.

Both structures offer limited liability and full local trading rights, but they differ in governance and transferability. An S.A. issues freely transferable shares and requires a formal board of directors, while an S.R.L. uses membership quotas that require consent from existing members before transfer. Compliance obligations are broadly similar, though the S.A. carries somewhat more formal corporate governance requirements.

The S.R.L. historically offered a degree of privacy because quota holders were not always prominently featured in public records. Nominee arrangements are legally permissible for both the S.A. and S.R.L., though beneficial ownership disclosure requirements have been strengthened under Law 9416, the Law to Improve the Fight Against Tax Fraud.

Not uniformly. An S.A. requires a minimum of two shareholders at formation, and an S.R.L. requires at least two members. Partnerships, by definition, require two or more parties. Only the Empresa Individual de Responsabilidad Limitada (E.I.R.L.) is designed explicitly for a sole individual.

Yes. Foreign nationals face no nationality restrictions when incorporating an S.A. or S.R.L. under the Código de Comercio. A foreigner does not need residency to hold shares or serve as a director, though a local registered agent with a physical address in the country is required.

The Código de Comercio allows for transformation of one commercial entity type into another through a formal process involving a notarial deed and registration at the Registro Nacional. An S.A. can be converted into an S.R.L. and vice versa, provided the transformation is approved by the requisite majority of shareholders or quota holders and properly recorded.

Not all structures do. The S.A., S.R.L., Sociedad en Comandita por Acciones, and E.I.R.L. each hold distinct legal personality separate from their owners. General partnerships (Sociedad en Nombre Colectivo) also acquire legal personality upon registration, but partners retain unlimited personal liability for the entity's obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.