Key Takeaways

- Business entities in Mayotte are registered through the Greffe du Tribunal de Commerce and governed by the French Code de commerce, reflecting the territory's status as a French overseas department.

- The SARL is the most frequently registered entity among both local and foreign entrepreneurs in Mayotte, valued for its limited liability structure and modest capital requirements.

- The SAS provides the greatest contractual flexibility for investor-backed ventures, while partnerships such as the SNC expose associates to unlimited personal liability, limiting their practical appeal.

- Mayotte's ongoing institutional integration with metropolitan France means compliance standards and reporting obligations for established firms are expected to tighten as alignment with mainland French fiscal rules progresses.

Introduction to Entity Types in Mayotte

Mayotte is a French overseas department and region situated in the Indian Ocean, positioned between the northern tip of Madagascar and the eastern coast of Mozambique. It forms part of the Comoro archipelago and operates under French law, making it subject to the same legal and regulatory framework applied in metropolitan France.

Business entity types in Mayotte are registered through the Greffe du Tribunal de Commerce (Commercial Court Registry), which serves as the primary company registration authority. The tax posture follows the French territorial system, with specific transitional arrangements that have historically applied to Mayotte as its alignment with mainland French fiscal rules has progressed.

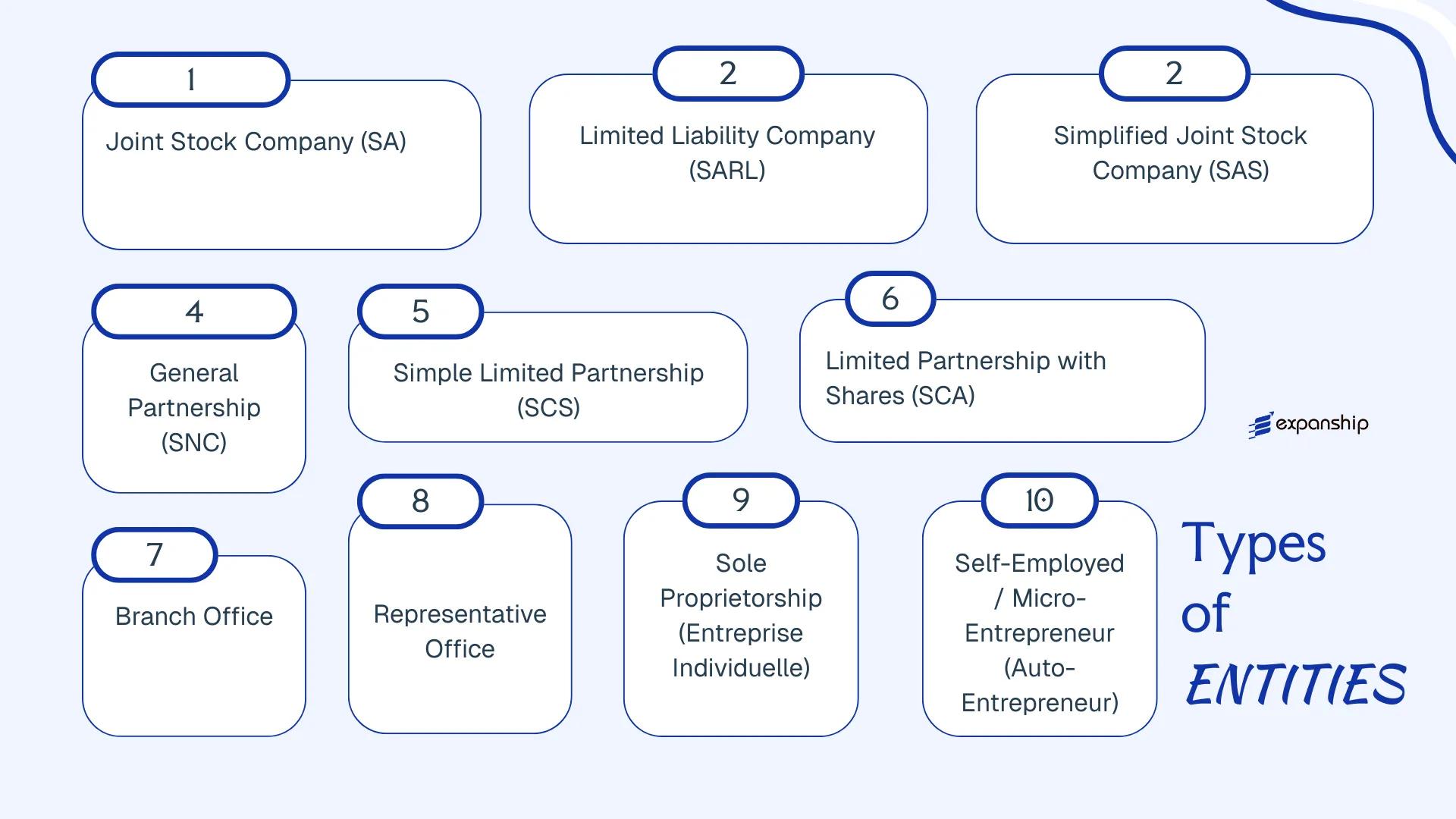

Firms operating in the territory may establish themselves under several recognized legal structures: Société Anonyme (SA), Société à Responsabilité Limitée (SARL), Société par Actions Simplifiée (SAS), Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA), Branch Office, Representative Office, Entreprise Individuelle, and Auto-Entrepreneur.

Each of these Mayotte company structures carries distinct formation requirements, liability rules, and governance obligations, all of which are examined in the sections that follow.

An Overview of Business Structures in Mayotte

French corporate law, applied through Mayotte's status as a French overseas department, provides several distinct legal forms for conducting commercial activity. The principal legislation governing these entities is the French Code de commerce, supplemented by local administrative provisions enforced through the Greffe du Tribunal de Commerce de Mayotte. Each legal form carries different implications for liability, governance, and taxation.

| Entity Type | Legal Form | Liability | Tax Treatment | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Société Anonyme (SA) | Corporation | Limited to share capital | Corporate tax (IS) | Permitted | 2 shareholders | Greffe du Tribunal de Commerce | Code de commerce |

| Société à Responsabilité Limitée (SARL) | Private limited | Limited to contribution | Corporate tax (IS) | Permitted | 1 shareholder | Greffe du Tribunal de Commerce | Code de commerce |

| Société par Actions Simplifiée (SAS) | Simplified joint-stock | Limited to share capital | Corporate tax (IS) | Permitted | 1 shareholder | Greffe du Tribunal de Commerce | Code de commerce |

| Société en Nom Collectif (SNC) | General partnership | Unlimited, joint | Income tax (IR) | Permitted | 2 partners | Greffe du Tribunal de Commerce | Code de commerce |

| Société en Commandite Simple (SCS) | Limited partnership | Mixed | IR or IS | Permitted | 2 partners | Greffe du Tribunal de Commerce | Code de commerce |

| Société en Commandite par Actions (SCA) | Partnership limited by shares | Mixed | Corporate tax (IS) | Permitted | 4 members | Greffe du Tribunal de Commerce | Code de commerce |

| Branch Office | Non-incorporated | Parent liability | Parent entity taxed | Permitted | 1 parent company | Greffe du Tribunal de Commerce | Code de commerce |

| Representative Office | Non-incorporated | Parent liability | Generally non-taxable | No commercial activity | 1 parent company | Greffe du Tribunal de Commerce | Code de commerce |

| Entreprise Individuelle | Sole proprietorship | Unlimited (default) | Income tax (IR) | Permitted | 1 individual | Greffe du Tribunal de Commerce | Code de commerce |

| Auto-Entrepreneur | Micro-enterprise | Limited (protected assets) | Micro-fiscal regime | Permitted | 1 individual | URSSAF / Greffe | Code de commerce |

Each of these structures is examined in full in the sections below.

Société Anonyme (SA)

The Société Anonyme (SA) in Mayotte operates under French corporate law, specifically the provisions of the Code de commerce as extended to the territory. As a French collectivity, Mayotte applies metropolitan French commercial legislation, meaning the SA functions as a public limited company with full separate legal personality and shareholder liability capped at the amount of their respective capital contributions.

Structurally, the SA is the most governance-intensive company form available. It supports both a one-tier board structure (conseil d'administration) and a two-tier structure comprising a directoire and a conseil de surveillance, giving shareholders flexibility in how management and oversight functions are separated.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (SA) | Separate legal personality; limited liability |

| Members | Shareholders (actionnaires) | Minimum 2 shareholders; no statutory maximum |

| Management | Board of Directors (CA) or Directoire + Supervisory Board | Minimum 3, maximum 18 directors under the CA structure |

| Local Presence | Registered office (siège social) required in Mayotte | No mandatory resident director under French law |

| Share Capital | EUR 37,000 minimum | Fully subscribed at formation; at least half paid up on registration |

| Privacy | Shareholder register maintained; beneficial ownership disclosed to BODACC and RCS | Limited public privacy |

Focus Points

- Taxation: Subject to French corporate income tax (impôt sur les sociétés) at the standard 25% rate; standard French VAT rules apply, along with withholding taxes on dividends, interest, and royalties at rates governed by applicable tax treaties.

- Treaty Access: As a French collectivity, Mayotte-registered SAs may access France's network of bilateral tax treaties, though treaty eligibility should be confirmed on a case-by-case basis.

- Annual Compliance: Mandatory annual accounts, statutory audit (commissaire aux comptes required once certain thresholds are met), and filing with the Registre du Commerce et des Sociétés (RCS).

- Conversion: An SA can be converted into an SAS or SARL by shareholders' resolution, subject to compliance with applicable capital and procedural requirements under the Code de commerce.

- Restrictions: Public share offerings are subject to regulatory requirements; the governance structure makes the SA disproportionately complex for small or closely-held businesses.

Closing

The SA suits larger enterprises, joint ventures requiring institutional governance structures, or businesses anticipating capital raises from multiple investors. The principal advantage is the ability to issue freely transferable shares and accommodate a broad shareholder base; the main drawback is the administrative overhead, including mandatory auditor appointment and multi-layer governance obligations.

Best suited for large-scale commercial operations, institutional joint ventures, or businesses in Mayotte planning structured equity investment.

Company Incorporation in Mayotte

Incorporate an SA or other entity type in Mayotte with end-to-end support from Expanship.

Société à Responsabilité Limitée (SARL)

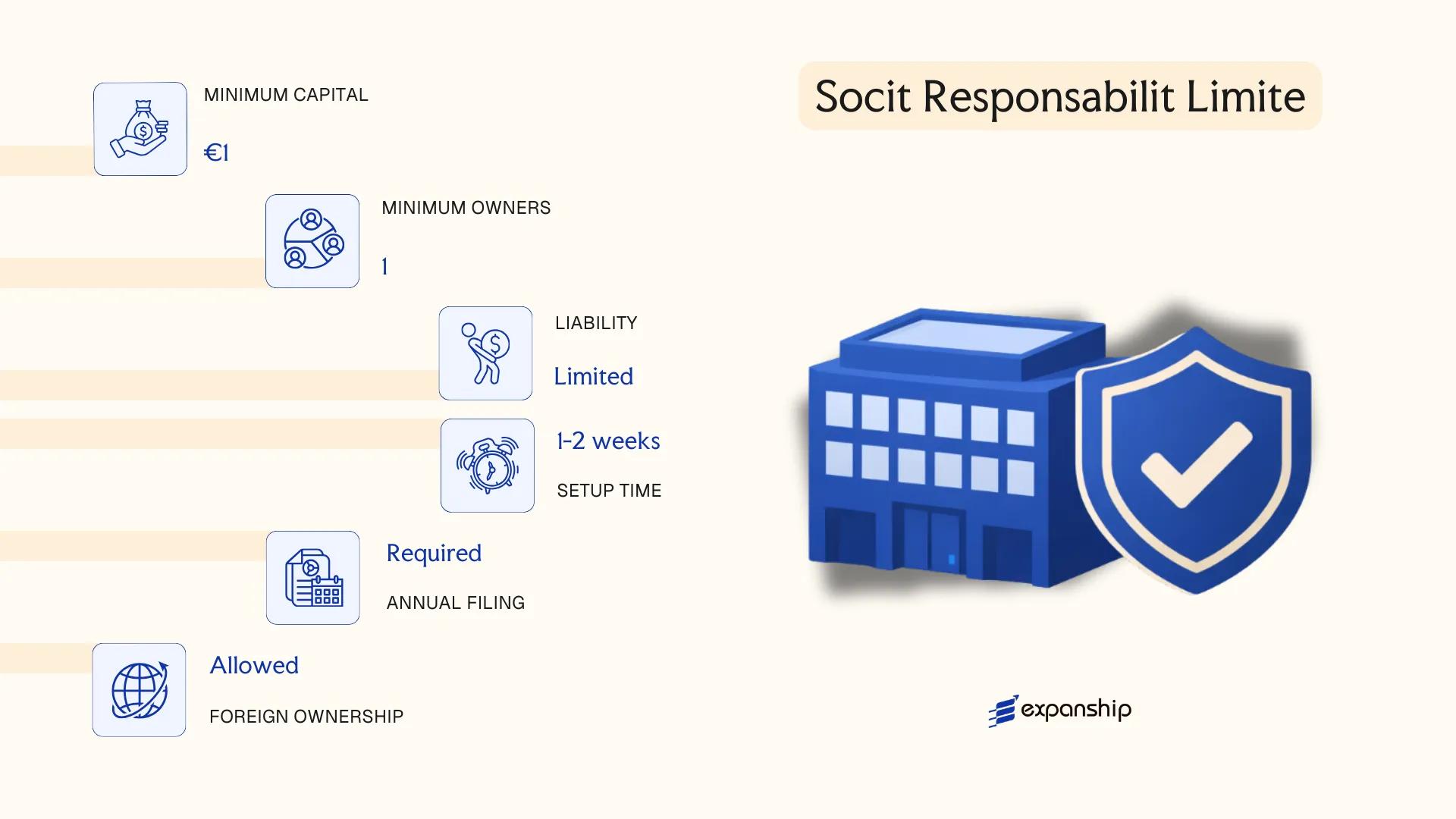

The Société à Responsabilité Limitée SARL Mayotte businesses most commonly adopt is governed by French commercial law, specifically the provisions of the Code de commerce applicable to Mayotte as a French overseas department. The SARL carries separate legal personality from the moment of registration with the Greffe du Tribunal de Commerce de Mayotte, and each associate's liability is capped at the value of their capital contribution.

Structurally, the SARL occupies a middle ground between a fully private closely-held entity and a more formally governed capital company. It suits small to medium-sized operations where ownership and management are held by a limited group with no intention of listing shares publicly.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited liability company | Carries separate legal personality upon registration |

| Members | 1 to 100 associés | Single-member variant is the EURL; multi-member capped at 100 |

| Management | One or more gérants (managers) | Gérant need not be an associé; can be a natural person only |

| Local Presence | Registered office in Mayotte required | No mandatory local resident gérant under general rules |

| Share Capital | No statutory minimum | Capital divided into parts sociales; not freely transferable without associé approval |

| Privacy | Beneficial ownership disclosure required | Filed with the Registre des bénéficiaires effectifs |

Focus Points

- Taxation: Subject to corporate income tax (impôt sur les sociétés) at standard French rates; VAT applies under French rules; withholding tax on dividends distributed to non-residents follows French domestic rates, reduced under applicable tax treaties.

- Annual Compliance: Annual accounts must be filed with the Greffe; approval by associés required within six months of the financial year-end.

- Treaty Access: Mayotte's status as a French overseas department grants access to France's extensive tax treaty network.

- Transfer Restrictions: Parts sociales transfers to third parties require approval by associés holding at least half the share capital.

- Conversion: An SARL may be converted into an SAS or SA by decision of the associés, subject to statutory conditions under the Code de commerce.

Sub-Types

Entreprise Unipersonnelle à Responsabilité Limitée (EURL)

The EURL is the single-member variant of the SARL, structurally identical except that ownership rests with one associé. It is commonly used for solo ventures where the founder requires limited liability without the administrative requirements of a multi-shareholder structure. Tax treatment defaults to personal income tax unless the sole associé opts for corporate tax.

Closing

The SARL is suited to family businesses, joint ventures, and small trading or service companies where the partners wish to retain direct management control without exposing personal assets beyond their contributed capital. A key constraint is that parts sociales cannot be freely sold or pledged, which limits the entity's capacity to attract outside investment at scale.

The SARL is best suited for small to medium enterprises, family-owned businesses, or joint ventures where a closed ownership structure and direct managerial control are priorities.

Société par Actions Simplifiée (SAS)

The Société par Actions Simplifiée SAS Mayotte framework derives from French commercial law, specifically the provisions introduced by the Law of 3 January 1994 and subsequently codified in the French Code de Commerce, which applies in Mayotte as a French overseas department. The SAS carries separate legal personality and confers limited liability on its shareholders, meaning personal assets remain protected from company debts. Its defining characteristic is contractual flexibility: the articles of association (statuts) govern internal management to a significant degree, rather than rigid statutory rules.

As a hybrid structure, the SAS combines corporate characteristics with considerable organizational freedom. Shareholders define management arrangements, voting thresholds, and share transfer conditions through the statuts, subject to mandatory provisions of the Code de Commerce.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société par Actions Simplifiée (SAS) | Separate legal personality; limited liability |

| Members | Shareholders (associés): minimum 1, no maximum | A single-shareholder variant is the SASU |

| Management | President (Président): minimum 1, no nationality restriction | The Président is the sole mandatory officer; additional managers optional |

| Registered Office | Physical address in Mayotte required | Must be maintained for official correspondence and service of legal documents |

| Share Capital | No statutory minimum (€1 permissible) | Capital divided into shares; contributions in cash or kind permitted |

| Privacy | Shareholder identity filed with the Registre du Commerce et des Sociétés (RCS) | Beneficial ownership disclosure required under French anti-money laundering rules |

Focus Points

- Taxation: Subject to French corporate income tax (impôt sur les sociétés) at the standard rate applicable in France; VAT applies under French rules; dividends paid to non-resident shareholders may attract French withholding tax, subject to applicable tax treaty relief.

- Annual Compliance: Annual accounts must be filed with the RCS; a statutory auditor (commissaire aux comptes) is mandatory once two of three legal thresholds (balance sheet, turnover, headcount) are exceeded.

- Economic Substance: No separate economic substance legislation beyond standard French commercial and tax residency requirements.

- Treaty Access: As part of France, Mayotte entities access France's extensive double tax treaty network.

- Conversion: An SAS may be converted into an SA or SARL by shareholder resolution, subject to compliance with the relevant provisions of the Code de Commerce.

Closing

An SAS suits trading companies, joint ventures, and holding structures where shareholders require flexibility in governance design. The absence of a minimum capital requirement lowers the entry threshold, though the obligation to appoint a statutory auditor at scale adds ongoing compliance cost.

The SAS structure is well suited to multi-shareholder ventures and subsidiaries of foreign groups seeking flexible governance under a familiar French legal framework.

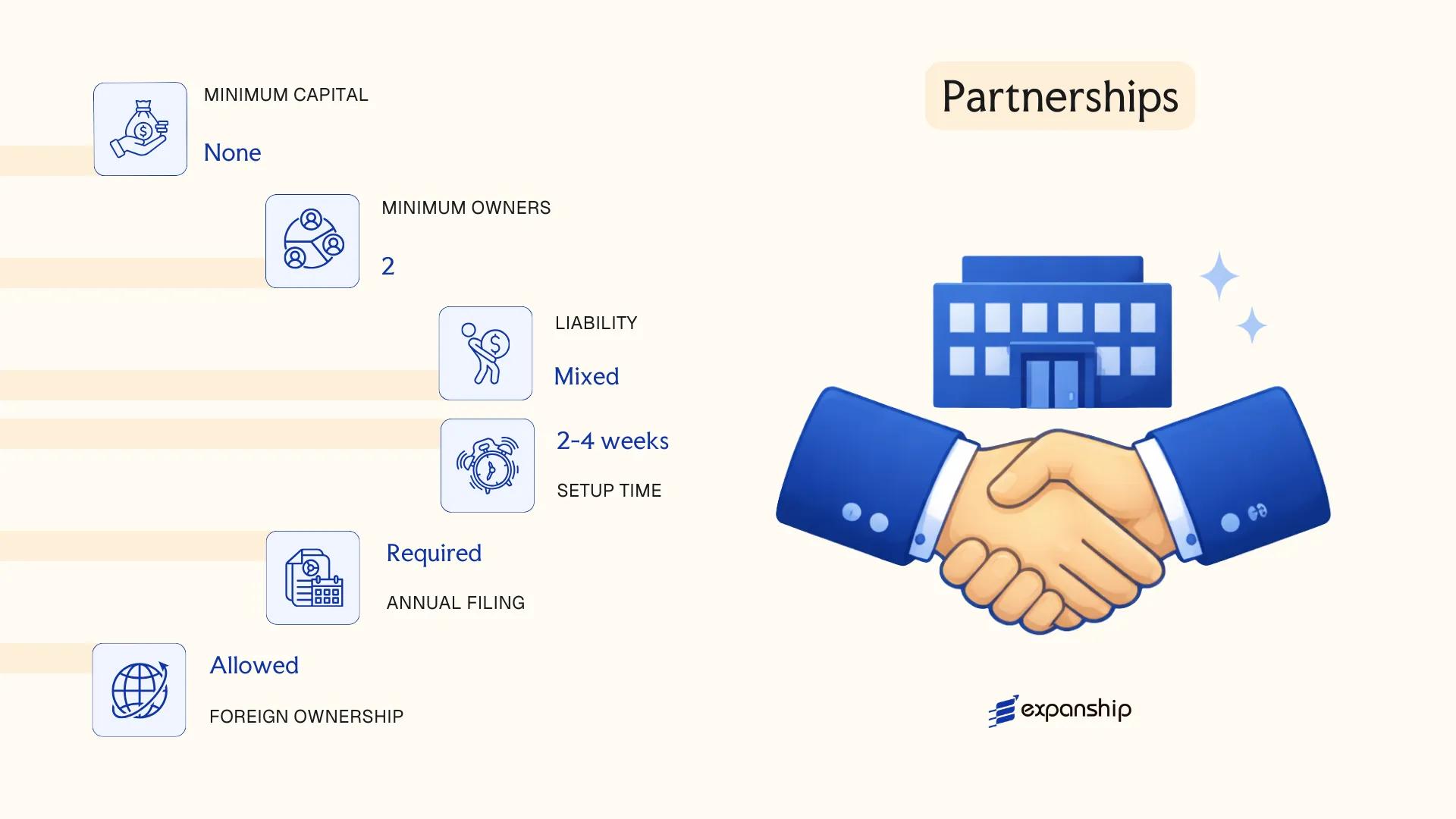

Partnerships in Mayotte [Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA)]

Partnership structures in Mayotte — SNC, SCS, and SCA — are governed by French commercial law as extended to the territory, principally through the Code de commerce. Because Mayotte became a French Overseas Department (Département d'outre-mer) in 2011, metropolitan French corporate legislation applies directly, administered locally through the Tribunal de commerce de Mayotte and the Greffe du tribunal.

Each of these three forms carries separate legal personality upon registration with the registre du commerce et des sociétés (RCS). Their liability profiles differ significantly: the SNC imposes unlimited joint and several liability on all partners, while the SCS and SCA introduce a two-tier membership structure that separates unlimited general partners from limited silent partners.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Commercial partnerships with separate legal personality | All three registered at RCS Mayotte |

| Members | SNC: minimum 2 associés (unlimited liability); SCS: minimum 1 gérant associé commandité + 1 commanditaire; SCA: minimum 1 commandité + 3 commanditaires actionnaires | SCA shares are publicly transferable; SNC/SCS interests require partner consent |

| Local Presence | Registered office (siège social) in Mayotte required | No mandatory resident agent, but a local address is compulsory |

| Capital | No statutory minimum for SNC or SCS; SCA requires minimum EUR 37,000 | SCA capital divided into shares (actions) |

| Privacy | Partners' identities disclosed at RCS; beneficial ownership reported to registre des bénéficiaires effectifs | No anonymity for SNC/SCS partners |

Focus Points

- Taxation: All three entities are generally subject to impôt sur les sociétés (corporate tax) at the standard French rate, though SNC partners may elect transparent (pass-through) taxation under certain conditions; VAT, withholding tax on dividends, and droits d'enregistrement (registration duties) apply under French fiscal rules extended to Mayotte.

- Annual Compliance: Annual accounts must be filed with the Greffe du tribunal de commerce; SCA is additionally subject to statutory audit requirements above certain thresholds.

- Treaty Access: As a French DOM, Mayotte benefits from France's tax treaty network, though treaty application to DOM entities requires case-by-case verification.

- Transfer Restrictions: SNC and SCS partner interests are non-freely transferable without unanimous or qualified partner consent; SCA shares transfer freely unless articles restrict this.

- Conversion: An SNC may be converted into an SARL or SAS by unanimous partner decision, subject to RCS formalities.

Sub-Types

Société en Nom Collectif (SNC)

The SNC is the base unlimited partnership form, where every associé bears joint and several liability for company debts. It is used primarily by professional firms or family-held trading operations where partners accept full personal exposure in exchange for simplified governance.

Société en Commandite Simple (SCS)

The SCS distinguishes between commandités (general partners with unlimited liability who manage the business) and commanditaires (silent partners whose liability is capped at their contribution). This structure suits investment arrangements where passive investors require liability protection but the entity need not issue publicly tradeable shares.

Société en Commandite par Actions (SCA)

The SCA functions as a hybrid between a partnership and a joint-stock company: commandités retain unlimited liability and management control, while commanditaires hold transferable shares (actions). It is used for structures where founders wish to maintain operational control while accessing external equity capital.

Closing

These partnership forms are most commonly used for family business succession, professional services, and controlled investment vehicles where governance concentration matters. The tiered liability structure of the SCS and SCA can be a structural advantage, but unlimited personal liability for general partners in all three forms is a material risk that limits their appeal for most commercial ventures.

Partnership structures in Mayotte are best suited for closely held family enterprises, professional partnerships, or investment vehicles where at least one party is prepared to accept unlimited liability in exchange for retained management control.

Foreign Business Establishments in Mayotte [Branch Office, Representative Office]

As an overseas department of France, Mayotte applies French commercial law, meaning any foreign company establishing a presence there operates under the same framework governing établissements secondaires on metropolitan French territory. A foreign business establishment in Mayotte does not constitute a separate legal entity — it remains an extension of the parent company, which retains full legal personality and bears unlimited liability for the establishment's obligations.

Registration is handled through the Tribunal de Commerce de Mayotte, and the establishment must be entered in the Registre du Commerce et des Sociétés (RCS). The parent company's founding documents, translated into French by a certified translator, are required at the time of filing.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Parent bears full liability |

| Designated Representative | Locally appointed permanent representative (représentant permanent) | Must be resident in France/Mayotte |

| Local Presence | Registered address in Mayotte; RCS filing mandatory | Physical office address required |

| Share Capital | No separate capital requirement | Parent's capital governs |

| Privacy | Parent company's details appear in public RCS records | No confidentiality of ownership |

Focus Points

- Taxation: Subject to French corporate income tax (25% standard rate) on locally sourced profits; VAT applies at standard French rates; withholding tax may apply to profit remittances depending on the parent's home jurisdiction and applicable tax treaties.

- Treaty Access: France's tax treaty network may extend to the establishment, but treaty eligibility depends on the parent entity's residence and treaty terms.

- Annual Compliance: Annual accounts of the establishment must be filed; the parent's financial statements may also require submission to the greffe.

- Restrictions: Cannot issue shares or raise equity independently; all contractual obligations bind the parent directly.

- Closure: Deregistration requires formal notification to the RCS and settlement of all local liabilities before the establishment is struck off.

Sub-Types

Branch Office (Succursale)

A branch operates commercially — it can conclude contracts, generate revenue, and employ staff under the parent's name. Registration with the RCS is compulsory, and it is subject to local tax on profits attributable to its activities in Mayotte. This structure suits foreign firms seeking an active trading presence without incorporating a separate subsidiary.

Representative Office (Bureau de Représentation)

A representative office is restricted to non-commercial activities such as market research, liaison, and promotion. It cannot generate revenue or enter into binding commercial contracts on behalf of the parent. This structure is used for exploratory or preparatory purposes before committing to a full commercial establishment.

Closing

Foreign business establishments are most commonly used by firms testing market entry or maintaining a coordinated operational base linked directly to the parent entity; the primary advantage is avoiding the cost and complexity of local incorporation, though the significant drawback is that the parent company assumes unlimited exposure for all local liabilities.

Foreign companies seeking a low-commitment operational foothold in Mayotte before deciding whether to incorporate a standalone French-law entity.

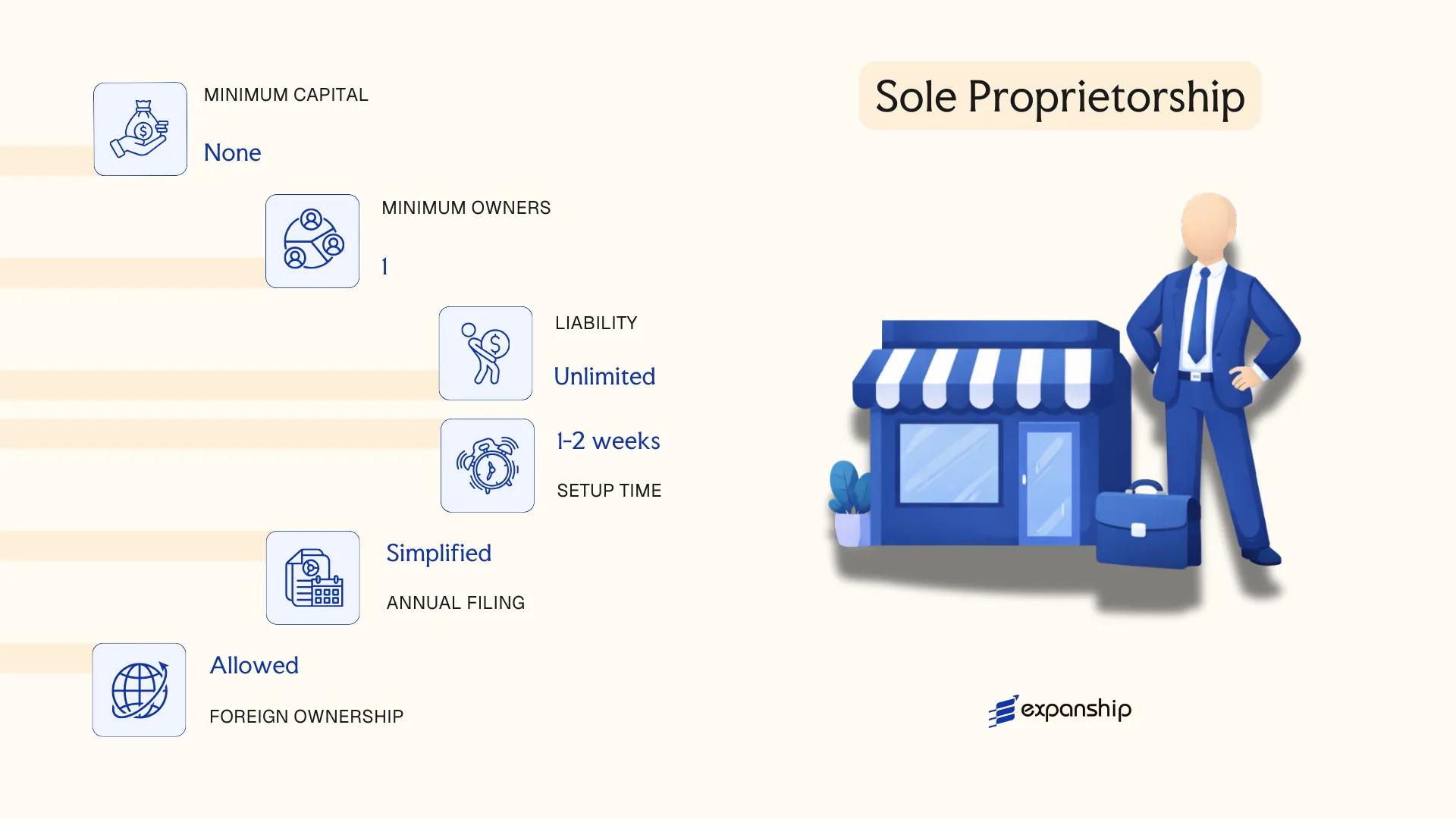

Sole Proprietorship in Mayotte [Entreprise Individuelle, Auto-Entrepreneur]

As an overseas department of France, Mayotte applies French commercial law to sole proprietorship structures. The two principal forms are the Entreprise Individuelle (EI) and the Auto-Entrepreneur (micro-entrepreneur) regime, both governed under French law — notably the Law of 14 February 2022 (loi en faveur de l'activité professionnelle indépendante), which introduced automatic asset separation between personal and professional estates for the EI, without requiring a formal declaration.

Registration for both forms is handled through the Centre de Formalités des Entreprises (CFE) or directly via the guichet unique électronique administered by the Institut National de la Propriété Industrielle (INPI). Neither structure carries separate legal personality; the sole proprietorship Mayotte auto-entrepreneur regime and the EI are extensions of the individual proprietor, not distinct legal entities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (non-corporate) | No separate legal personality; owner and business are the same legal person |

| Members | Single proprietor | One individual only; no partners, shareholders, or co-owners permitted |

| Liability | Limited to professional assets (EI) | Since 2022 reform, personal assets are protected by default unless waived |

| Registered Office | Required in Mayotte | A local business address must be declared at registration |

| Capital | No minimum | No paid-up capital requirement for either form |

| Privacy | Name and address publicly registered | INPI registry is publicly accessible |

Focus Points

- Taxation: Subject to income tax (impôt sur le revenu) under the BIC or BNC regime; the Auto-Entrepreneur benefits from a flat micro-fiscal rate applied to gross turnover; VAT exemption applies below the micro-enterprise threshold; no corporate tax applies.

- Revenue Thresholds: The Auto-Entrepreneur regime is capped at annual turnover limits set under French micro-enterprise rules (periodically revised); exceeding these thresholds triggers mandatory transition to the standard EI or a corporate form.

- Annual Compliance: Turnover declarations are submitted quarterly or monthly to URSSAF; the standard EI requires standard accounting records, while the Auto-Entrepreneur regime requires only a simplified revenue register.

- Conversion: An EI can be converted into a sole-member EURL (Entreprise Unipersonnelle à Responsabilité Limitée) without triggering a taxable asset transfer, under applicable French provisions.

- Treaty Access: As an overseas department, Mayotte falls within the French tax framework, but access to France's bilateral tax treaty network for sole traders is limited and activity-dependent.

Sub-Types

Entreprise Individuelle (EI)

The standard EI suits proprietors who exceed micro-enterprise thresholds or require full deductibility of actual business expenses. Since the 2022 reform, professional assets are automatically ring-fenced from personal assets by default, removing the need for a separate EIRL declaration.

Auto-Entrepreneur (Micro-Entrepreneur)

This simplified registration and tax regime targets low-turnover independent activity. Social contributions and income tax are calculated as a fixed percentage of gross receipts, eliminating the need for complex accounting. It is particularly suited to freelancers, artisans, and service providers testing a new activity.

Closing

Both forms are suited to individual consultants, freelancers, and small-scale traders operating with low overhead and limited capital requirements. The principal advantage is minimal administrative burden at setup; the key limitation is that business scale is structurally constrained by turnover ceilings and the absence of equity capital mechanisms.

Individuals testing a new service-based or freelance activity with low initial turnover, who do not require external investors or partners.

How to Choose the Right Entity Type in Mayotte

Selecting how to choose your business entity in Mayotte requires more than comparing registration fees — the structural decision carries legal, fiscal, and operational consequences that compound over time.

Why Your Entity Choice Matters

The wrong structure creates concrete legal and financial problems:

- Choosing a legal structure without the capacity to maintain local substance when substance requirements apply triggers reporting failures and potential regulatory penalties under French commercial law as extended to Mayotte.

- Selecting an entity with audited financial statement requirements for a single-person consultancy introduces annual compliance costs that have no proportional business justification.

- Forming a capital company when asset-holding or succession planning is the primary objective locks the business into annual shareholder obligations and governance requirements that do not serve that purpose.

- Registering an entity type that excludes you from applicable tax treaty benefits means withholding tax reductions available under France's treaty network cannot be claimed by that entity.

Key Factors to Consider

- Business Activity: Active trading, passive asset-holding, and regulated sectors each point toward distinct structures under French commercial law as applied in Mayotte.

- Ownership and Management: Single-owner operations and multi-party arrangements have different governance requirements that determine whether an SAS, SARL, or partnership fits.

- Tax Objectives: Your need for a specific tax regime or treaty eligibility will restrict or expand which entity types are viable.

- Substance Capacity: If you cannot realistically maintain local employees and decision-making, your structure must reflect that limitation.

- Exit Strategy: Some structures permit redomiciliation or conversion; others require full dissolution and re-registration.

Consult the applicable provisions under the Code de commerce before finalising any registration decision.

Corporate Compliance Services for Companies in Mayotte

Maintain your legal standing with ongoing compliance support tailored to entities registered under French commercial law in Mayotte.

Conclusion

Incorporating a company in Mayotte means operating within a French legal framework governed by the Code de commerce, administered locally through the Tribunal mixte de commerce and registered via the Centre de Formalités des Entreprises. Each structure carries a distinct profile: the SA fits larger enterprises requiring formal governance, the SARL suits closely held businesses with limited liability at modest capital thresholds, and the SAS offers the greatest contractual flexibility for investor-backed ventures. Partnerships such as the SNC expose associates to unlimited liability, making them less common in practice. The SARL remains the most frequently registered entity among local and foreign entrepreneurs.

Your choice of structure will also intersect with Mayotte's status as a French overseas department, meaning EU regulatory alignment and French tax treaties apply. As the territory continues institutional integration with mainland France, its compliance standards are expected to align further with metropolitan norms, affecting reporting obligations for established firms.

How Expanship Can Assist You

Expanship provides corporate services Mayotte company formation clients rely on across the full lifecycle of a business — from initial entity selection through to ongoing compliance. Whether you're incorporating a SARL, registering an SAS, or filing branch office documents with the Greffe du Tribunal de Commerce de Mayotte, our team handles the procedural requirements on your behalf.

From a single point of contact, you can access:

- Preparation and legalization of constitutional documents

- Registered agent and local office address provision

- Filing and liaison with the relevant commercial registry

- Post-incorporation compliance management, including annual reporting obligations

- Corporate bank account introduction assistance

Our support covers each stage without gaps, so your entity remains in good standing under French law as it applies in Mayotte.

Reach out directly to discuss your incorporation requirements with Expanship Mayotte.

Frequently Asked Questions (FAQ)

The SARL (Société à Responsabilité Limitée) is the most frequently registered structure. Its single-shareholder variant, the EURL, makes it accessible to solo founders, and its flexible governance rules suit small to mid-sized operations without the formality requirements of an SA.

Both structures carry limited liability, but the SAS allows greater contractual freedom in drafting governance arrangements through its statuts. The SARL imposes more statutory rigidity around shareholder decisions and profit distribution, while an SAS faces no cap on share capital contributions and no ceiling on the number of shareholders.

Among capital companies, the SAS discloses less mandatory information about shareholder arrangements than the SA, which requires more formal publication of governance decisions. Nominee arrangements are not prohibited under French corporate law, though beneficial ownership disclosure requirements apply under anti-money laundering regulations transposed into French law.

No. Partnerships — the SNC, SCS, and SCA — each require a minimum of two partners or shareholders by definition. A sole founder can establish an EURL, a SASU (single-shareholder SAS), or an Entreprise Individuelle, but cannot form a partnership structure alone.

Foreign nationals can establish an SARL, SAS, or SA without a French citizenship requirement, though non-EU residents may need to obtain a carte de commerçant étranger before conducting commercial activity. This requirement stems from French commercial law applicable across all overseas departments, including Mayotte. Foreigners frequently use the SAS structure due to its flexible shareholder arrangements.

French corporate law, applicable in Mayotte, permits transformation of one entity type into another — for example, converting an SARL into an SAS — provided shareholders vote in favour and specific statutory conditions are met. Transformation does not create a new legal entity; the existing firm retains its SIREN registration number and contractual obligations throughout the process.

The SA, SARL, SAS, SNC, SCS, and SCA all hold separate legal personality upon registration with the Greffe. The auto-entrepreneur regime and the Entreprise Individuelle do not create a separate legal entity — the individual and the business remain legally the same person, meaning personal assets carry greater exposure to commercial liabilities.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.