Key Takeaways

- The Kosovo Business Registration Agency (KBRA) is the central authority for formalizing all business structures, from the SH.P.K. to branch offices, before operations can commence.

- Kosovo's most widely registered entity, the Shoqëria me Përgjegjësi të Kufizuar (SH.P.K.), provides limited liability without requiring public disclosure of share capital, making it the default choice for small to mid-sized businesses.

- All legal entities in Kosovo are governed under the Law on Business Organizations, which defines distinct liability, governance, and capital requirements for each structure.

- Foreign companies seeking a controlled presence in Kosovo without establishing a separate legal person may do so through a branch office or representative office rather than incorporating a standalone entity.

Introduction to Entity Types in Kosovo

Kosovo is a landlocked country in the Western Balkans, bordered by Serbia, North Macedonia, Albania, and Montenegro. It declared independence in 2008 and is recognized as a sovereign state by over 100 countries, though its international legal status remains contested in some forums. The country operates under a civil law framework influenced by European Union legislative models.

Company registration is administered by the Kosovo Business Registration Agency (KBRA), which operates under the Ministry of Industry, Entrepreneurship, and Trade. All legal entities conducting business in the territory must register with the KBRA before commencing operations.

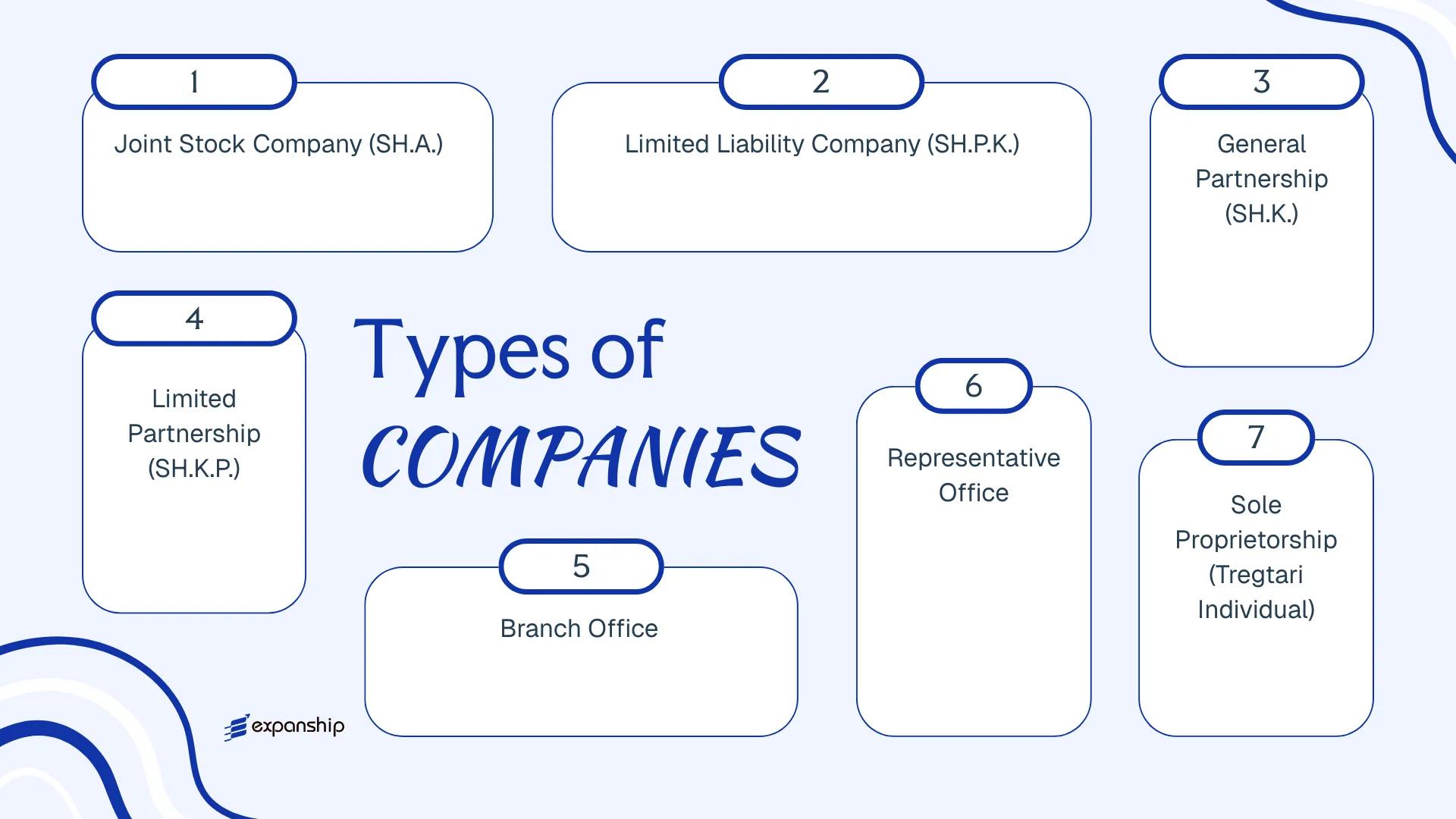

Kosovo applies a low-tax regime, with a flat corporate income tax rate and no capital gains tax on certain categories of assets. The types of business entities in Kosovo available to both domestic and foreign investors include the Shoqëria Aksionare (SH.A.), the Shoqëria me Përgjegjësi të Kufizuar (SH.P.K.), the General Partnership (SH.K.), the Limited Partnership (SH.K.P.), the Sole Proprietorship (Tregtari Individual), Branch Offices, and Representative Offices. Each structure carries distinct liability, governance, and capital requirements that this article examines in detail.

An Overview of Business Structures in Kosovo

Under the Law on Business Organizations (Law No. 02/L-123, as amended), Kosovo recognizes five principal legal forms through which commercial activity can be conducted. The Business Registration Agency (BRA), operating under the Ministry of Industry, Entrepreneurship and Trade, serves as the primary registration authority for all domestic entities. Each legal form carries distinct implications for liability, governance, and capital requirements.

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| SH.A. | Joint Stock Company | Limited to shares | Taxed | Yes | 1 shareholder | BRA | Law No. 02/L-123 |

| SH.P.K. | Limited Liability Company | Limited to capital | Taxed | Yes | 1 member | BRA | Law No. 02/L-123 |

| SH.K. | General Partnership | Unlimited, joint | Taxed | Yes | 2 partners | BRA | Law No. 02/L-123 |

| SH.K.P. | Limited Partnership | Mixed liability | Taxed | Yes | 2 partners | BRA | Law No. 02/L-123 |

| Branch Office | Foreign branch | Parent liability | Taxed | Yes | N/A | BRA | Law No. 02/L-123 |

| Representative Office | Non-trading presence | Parent liability | Exempt | No | N/A | BRA | Law No. 02/L-123 |

| Tregtari Individual | Sole Proprietorship | Unlimited, personal | Taxed | Yes | 1 owner | BRA | Law No. 02/L-123 |

Each of these structures is examined in full in the sections below.

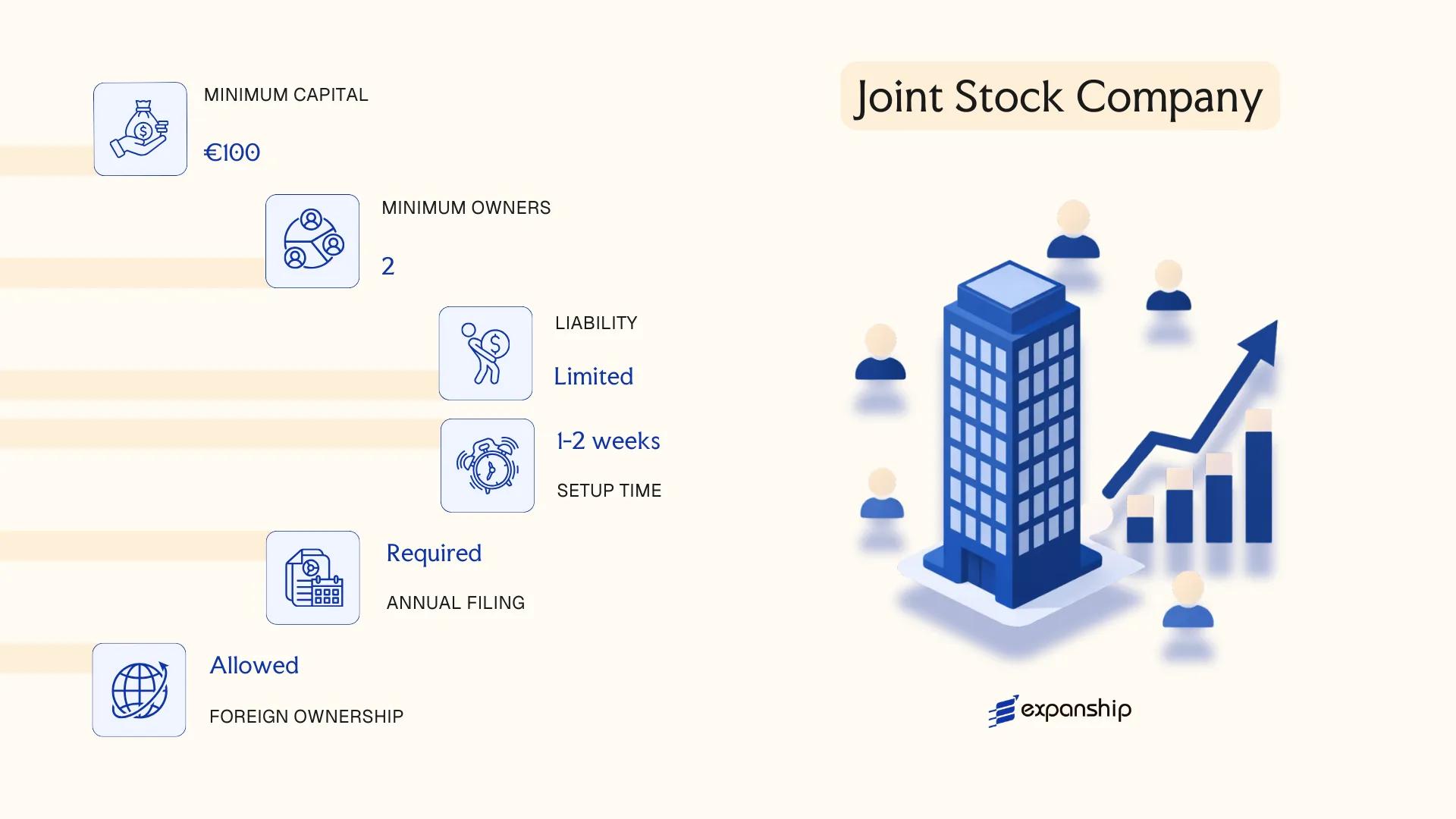

Shoqëria Aksionare (SH.A.) – Joint Stock Company

The Kosovo SHA joint stock company is governed by Law No. 02/L-123 on Business Organizations, which establishes it as a separate legal entity with limited liability for its shareholders. Capital is divided into transferable shares, making it the structure of choice for businesses that anticipate external investment or eventual public listing.

Structurally, this entity sits at the more formal end of the spectrum. Shareholders are liable only to the extent of their share contributions, and the firm can issue multiple classes of shares with varying rights.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Joint Stock Company (Shoqëria Aksionare) | Separate legal personality; shares freely transferable |

| Governing Bodies | Shareholders, Board of Directors, Executive Officers | A supervisory board may also be required above certain thresholds |

| Members | Minimum 1 shareholder; no maximum | Single-founder SH.A. permitted; public companies face additional disclosure rules |

| Local Presence | Registered office address in Kosovo required | No mandatory resident director requirement under general rules |

| Share Capital | Minimum €10,000 (private); €25,000 (public) | Must be denominated in EUR; at least 25% paid up at registration |

| Privacy | Shareholder register maintained; beneficial ownership disclosure required | Filed with the Kosovo Business Registration Agency (KBRA) |

Focus Points

- Taxation: Corporate income tax applies at 10% on net profit; VAT standard rate is 18%; dividends distributed to non-residents are subject to a 10% withholding tax; no stamp duty on share transfers under general rules.

- Annual Compliance: Audited financial statements required; annual report filed with KBRA; public SH.A. entities fall under Kosovo Financial Supervisory Authority (FSA) oversight.

- Treaty Access: Kosovo has a limited but growing double tax treaty network; treaty eligibility depends on the beneficial owner's residence and substance maintained in Kosovo.

- Conversion: An SH.A. may be converted into an SH.P.K. or another recognized business form through a shareholder resolution and KBRA re-registration procedure.

- Restrictions: Foreign ownership is permitted without restriction; however, certain regulated sectors (banking, insurance) require additional licensing from the relevant supervisory authority.

Closing

The SH.A. is suited to capital-intensive ventures, holding structures, and businesses targeting institutional investors or a public market. Its share transferability is a clear operational advantage, though the mandatory audit requirement and higher minimum capital make it disproportionate for small or early-stage operations.

Best suited for businesses planning to raise external capital, operate across multiple jurisdictions, or seek eventual public listing on a regulated exchange.

Company Incorporation in Kosovo

Incorporate a Joint Stock Company or other business structure in Kosovo with end-to-end support from Expanship.

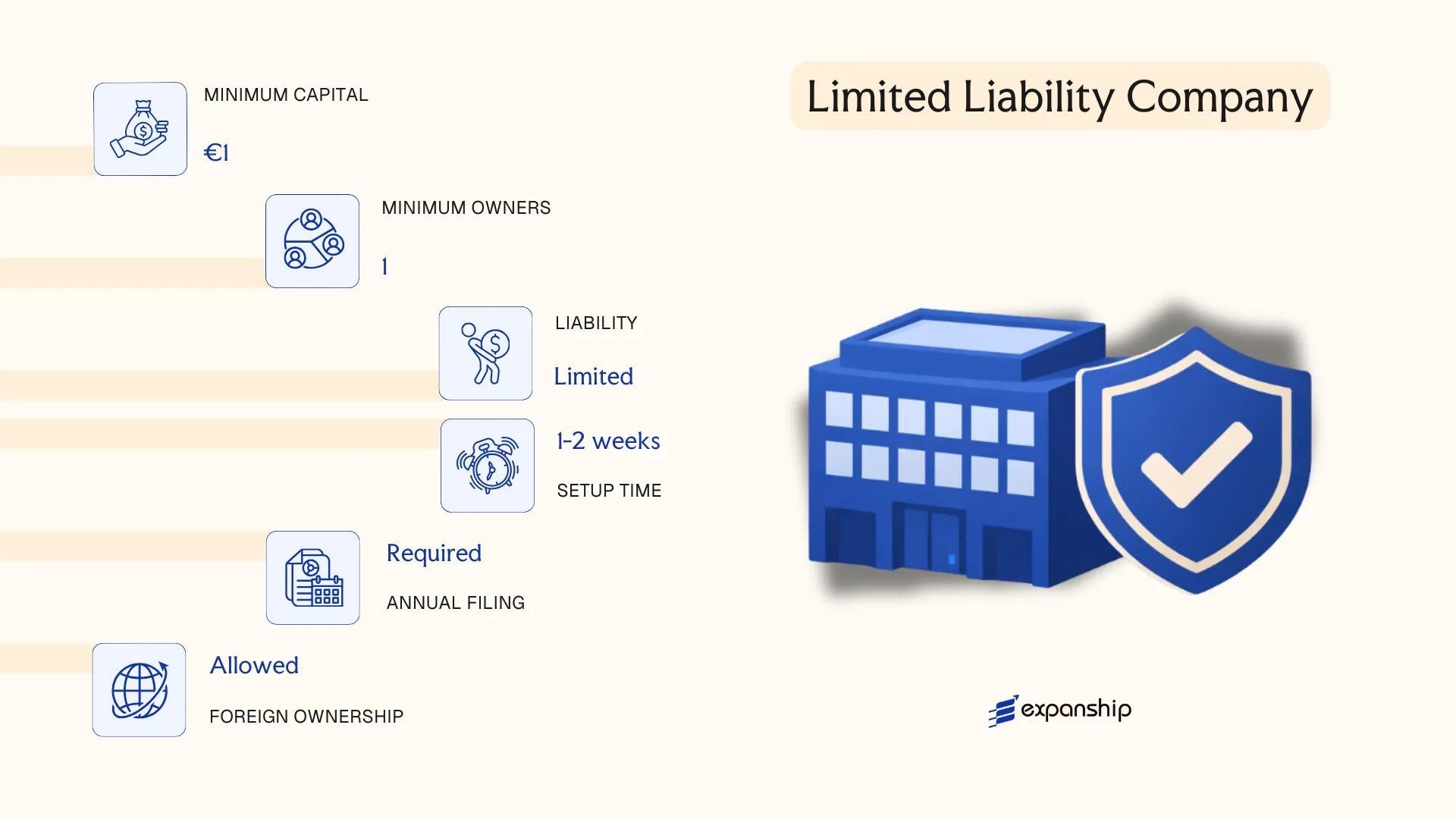

Shoqëria me Përgjegjësi të Kufizuar (SH.P.K.) – Limited Liability Company

The Kosovo SHPK limited liability company is the most widely used business structure in the country, governed primarily by the Law on Business Organizations No. 02/L-123 and its subsequent amendments. It carries separate legal personality, meaning the entity holds rights and obligations in its own name, distinct from its members.

Liability of each member is capped at their capital contribution. This hybrid nature — combining corporate-style liability protection with relatively flexible internal governance — makes the SH.P.K. accessible to a broad range of investors and operators.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (Shoqëria me Përgjegjësi të Kufizuar) | Registered with the Kosovo Business Registration Agency (KBRA) |

| Members & Management | 1–50 members; managed by one or more Directors | Members hold ownership shares; Directors handle day-to-day management |

| Local Presence | Registered office address in Kosovo required | No mandatory resident director, but a local registered address must be maintained |

| Share Capital | Minimum EUR 1; no maximum cap | Capital divided into ownership shares, not publicly tradeable |

| Privacy | Member and director details filed with KBRA; publicly accessible | No bearer shares permitted |

Focus Points

- Taxation: Corporate income tax at 10%; VAT registration required once annual turnover exceeds EUR 30,000; withholding tax of 10% applies to dividends, interest, and royalties paid to non-residents; no stamp duty on share transfers.

- Annual Compliance: Annual financial statements must be filed with the Kosovo Tax Administration (ATK) and the KBRA; audit requirements depend on company size thresholds.

- Economic Substance: No formal economic substance regime currently in force, though tax residency is determined by place of effective management.

- Treaty Access: Kosovo has a limited but growing tax treaty network; treaty eligibility depends on the residency status of the entity and its beneficial owners.

- Conversion: An SH.P.K. may be converted into a Joint Stock Company (SH.A.) through a formal restructuring process under the Law on Business Organizations.

Closing

The SH.P.K. suits trading operations, holding structures, and service businesses requiring a straightforward corporate vehicle with capped member liability. Its low capital threshold and single-member option lower the barrier to entry, though the 50-member ceiling restricts scalability for businesses anticipating broad equity distribution.

Small to mid-sized businesses, foreign investors entering the market with a wholly-owned subsidiary, or entrepreneurs seeking a cost-effective structure with limited personal liability.

Partnerships in Kosovo [General Partnership (SH.K.), Limited Partnership (SH.K.P.)]

Kosovo general and limited partnership registration is governed by the Law on Business Organizations No. 02/L-123, which regulates both the Shoqëria Kolektive (SH.K.) and the Shoqëria Komandite me Pjesëmarrje (SH.K.P.) as distinct legal forms. Both structures carry separate legal personality once registered with the Business Registration Agency (BRA).

Unlike capital-based entities, partnerships are defined primarily by the relationships between their members. The general partnership holds all partners jointly and severally liable for obligations of the firm, while the limited partnership introduces a two-tier membership model separating active management from passive investment.

Key Characteristics

| Requirement | SH.K. (General Partnership) | SH.K.P. (Limited Partnership) | Notes |

|---|---|---|---|

| Legal Form | General Partnership | Limited Partnership | Both have separate legal personality |

| Members | Partners (minimum 2, no statutory maximum) | General Partners (min. 1) + Limited Partners (min. 1) | No upper cap specified under general statute |

| Liability | Unlimited, joint and several for all partners | Unlimited for general partners; limited to capital contribution for limited partners | Limited partners must not engage in management |

| Registered Office | Required in Kosovo | Required in Kosovo | Must maintain a physical registered address with BRA |

| Minimum Capital | No statutory minimum | No statutory minimum | Contributions may be in cash or in kind |

| Privacy | Partner names disclosed in public register | Both general and limited partner names disclosed | BRA register is publicly accessible |

Focus Points

- Taxation: Partnerships are treated as transparent entities for Corporate Income Tax purposes — income is attributed to and taxed at the partner level at the applicable personal or corporate rate; VAT registration is required once the turnover threshold is met; withholding tax applies to distributions to non-resident partners at the standard rate.

- Annual Compliance: Partners must file annual financial statements with the Tax Administration of Kosovo (TAK) and maintain up-to-date BRA registration records.

- Economic Substance: No formal substance regime equivalent to offshore jurisdictions; however, active business presence is expected given the domestic legal framework.

- Conversion: A general partnership may be converted to a limited partnership or another recognized form through a formal amendment process at the BRA.

- Restrictions: Limited partners lose liability protection if they participate in management decisions, which can expose them to unlimited personal liability.

Sub-Types

Shoqëria Kolektive – SH.K. (General Partnership)

All partners carry equal management rights and unlimited liability. This structure is typically used by small professional firms or family-owned businesses where partners are closely involved in day-to-day operations.

Shoqëria Komandite me Pjesëmarrje – SH.K.P. (Limited Partnership)

The distinguishing feature is the separation of general partners, who manage the business and bear unlimited liability, from limited partners, whose exposure is capped at their agreed capital contribution. This form suits arrangements where passive investors wish to participate financially without assuming management responsibility.

Closing

Partnerships in Kosovo are best suited to small-scale trading operations, professional service arrangements, or domestic joint ventures where the partners have an established working relationship and shared operational involvement. The absence of a minimum capital requirement lowers the entry barrier, though the unlimited liability exposure for general partners represents a significant structural risk for any business with substantial third-party obligations.

This structure is most appropriate for small domestic businesses or professional partnerships where all active partners accept personal liability and formal capital requirements are a constraint.

Foreign Business Presence in Kosovo [Branch Office, Representative Office]

Establishing a foreign company branch office in Kosovo is governed by the Law on Business Organizations (Law No. 02/L-123, as amended), which treats a branch as an extension of the foreign parent rather than a separate legal entity. This distinction carries direct consequences: the parent company bears full liability for the branch's obligations incurred within the territory.

A representative office operates under similar registration requirements but is restricted to non-commercial activities such as market research, liaison, and promotion. Neither structure acquires independent legal personality under Kosovo law.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None – extension of parent | None – extension of parent |

| Commercial Activity | Permitted | Not permitted |

| Liability | Parent company bears full liability | Parent company bears full liability |

| Registration Body | Kosovo Business Registration Agency (KBRA) | Kosovo Business Registration Agency (KBRA) |

| Local Representative | Mandatory – resident authorised representative required | Mandatory – resident authorised representative required |

| Registered Address | Physical address in Kosovo required | Physical address in Kosovo required |

| Capital Requirement | None prescribed | None prescribed |

| Privacy | Parent company details filed on public record | Parent company details filed on public record |

Focus Points

- Taxation: Branch profits are subject to corporate income tax at 10%; VAT registration is required once turnover exceeds the statutory threshold; withholding tax applies to payments remitted abroad, including dividends and royalties to the parent.

- Economic Substance: A branch must maintain genuine operational activity in Kosovo; purely passive or administrative presences risk reclassification by the Tax Administration of Kosovo (TAK).

- Annual Compliance: Annual financial statements must be filed with the Kosovo Tax Administration; the branch must also renew its registration details if any parent-level structural changes occur.

- Treaty Access: Kosovo has a limited tax treaty network; confirm whether the parent's jurisdiction has a double taxation agreement in force before structuring profit repatriation.

- Restrictions: A representative office may not conclude commercial contracts, generate revenue, or invoice clients — any deviation from this scope triggers an obligation to convert to a branch or incorporate a standalone entity.

Sub-Types

Branch Office

Registered with the KBRA, the branch may conduct full commercial and trading operations in Kosovo under the parent's name. It files its own tax returns locally while remaining legally inseparable from the foreign parent.

Representative Office

Limited strictly to promotional and liaison functions, the representative office cannot generate income or enter into binding commercial agreements on behalf of the parent. It suits businesses conducting preliminary market assessments before committing to a full operational structure.

Closing

Both structures suit foreign firms that want operational or market presence without the administrative overhead of incorporating a separate local entity, though the absence of limited liability protection for the parent is a clear structural drawback.

Foreign companies seeking a low-commitment entry point into the Kosovo market, particularly for trade representation or pre-incorporation market testing.

Sole Proprietorship (Tregtari Individual)

The Kosovo sole proprietorship, known locally as the Tregtari Individual, is governed by Law No. 02/L-123 on Business Organizations and subsequent amendments administered by the Kosovo Business Registration Agency (KBRA). Unlike corporate forms, this structure carries no separate legal personality — the proprietor and the business are legally the same entity, meaning personal assets are fully exposed to business liabilities.

Registration is handled directly through the KBRA, with a relatively straightforward sole trader Kosovo setup process. Because there is no capital requirement and no board structure, the Tregtari Individual suits early-stage or low-risk commercial activity where administrative simplicity is a priority.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Member Designation | Proprietor | Single individual only; no co-ownership structure |

| Ownership | 1 proprietor (natural person) | Foreign nationals may register subject to residency or permit conditions |

| Local Presence | Registered address in Kosovo required | No mandatory registered agent requirement |

| Minimum Capital | None | No paid-up or share capital required |

| Liability | Unlimited personal liability | All personal assets are at risk for business debts |

Focus Points

- Taxation: Subject to personal income tax on business profit; VAT registration is mandatory once annual turnover exceeds the statutory threshold; no corporate income tax applies.

- Annual Compliance: Annual declaration must be filed with the Kosovo Tax Administration (ATK); bookkeeping obligations apply based on turnover level.

- Treaty Access: As an unincorporated structure, access to Kosovo's double tax treaties is limited compared to corporate entities.

- Conversion: Can be converted into a SH.P.K. or other corporate form through KBRA procedures as the business grows.

- Restrictions: Cannot issue shares, take on partners, or raise equity capital; restricted to individual ownership throughout its existence.

Closing

The Tregtari Individual suits freelancers, small traders, and individual service providers seeking a low-cost entry point into commercial activity, though the unlimited liability exposure makes it unsuitable for ventures carrying significant financial or legal risk.

Resident individuals conducting small-scale trade or services who require minimal administrative overhead and do not anticipate significant liability exposure.

How to Choose the Right Entity Type in Kosovo

Choosing the right business entity in Kosovo affects your tax exposure, liability, compliance obligations, and operational capacity from day one.

Why Your Entity Choice Matters

The consequences of an unsuitable structure are concrete, not theoretical:

- Registering a branch or representative office when you intend to conduct full commercial activity can result in operating outside the scope permitted under the Law on Business Organizations No. 06/L-016, exposing the business to penalties or forced deregistration.

- Selecting an entity that lacks a tax residency certificate under Kosovo's corporate tax framework means you cannot access withholding tax reductions available under applicable double taxation agreements.

- Choosing a SH.P.K. when a sole proprietorship would serve a single-person consultancy adds mandatory bookkeeping, annual reporting, and registration fees that a Tregtari Individual does not require.

- Forming a general partnership without understanding joint and several liability locks all partners into unlimited personal exposure for the firm's obligations.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each correspond to distinct structures under Kosovo company law.

- Ownership and Management: Multi-party ownership with formal governance requirements points toward a SH.A., while single or small-group ownership suits a SH.P.K.

- Tax Objectives: Your eligibility for Kosovo's flat 10% corporate income tax rate, or any sector-specific regime, depends on the registered entity type.

- Substance Capacity: If you cannot maintain a physical presence or local decision-making, certain structures will create compliance exposure with the Kosovo Tax Administration.

- Exit Strategy: Not all entity types permit redomiciliation or conversion; verify this before registration.

Compliance Services for Companies in Kosovo

Ongoing compliance support for Kosovo-registered entities, including annual reporting, tax filings, and regulatory obligations.

Conclusion

Choosing the right structure is the first substantive decision in any incorporating a company in Kosovo guide. Each entity type registered under the Law on Business Organizations serves a distinct purpose: the SH.P.K. is the most widely registered form and suits small to mid-sized firms requiring limited liability without public disclosure of share capital; the SH.A. is structured for businesses seeking external investment or eventual public listing; partnerships carry personal liability and are typically used within specific trades or professions; and branch or representative offices serve foreign companies establishing a controlled presence without forming a separate legal person.

Kosovo's regulatory environment has been gradually aligning with EU standards, and continued progress on bilateral investment treaty expansion may broaden its appeal to foreign investors. Registration through the Kosovo Business Registration Agency remains the central process for formalizing any business structure. Expanship's team has direct experience with that process across all entity types.

How Expanship Can Assist You

Expanship provides corporate services for Kosovo company formation, working directly with the structures and requirements covered in this guide. From registering a Shoqëria me Përgjegjësi të Kufizuar (SH.P.K.) to establishing a branch office for a foreign parent entity, our team handles each step through the Kosovo Business Registration Agency (KBRA), the authority responsible for entity registration and commercial record-keeping.

Our service scope covers the full formation and post-incorporation cycle:

- Document preparation and notarization

- Registered agent and registered office provision

- Filing and liaison with the KBRA on your behalf

- Tax registration with the Tax Administration of Kosovo

- Ongoing compliance management, including annual reporting obligations

- Banking introduction assistance for newly incorporated entities

For questions about your specific situation, contact Expanship Kosovo directly.

Frequently Asked Questions (FAQ)

The Shoqëria me Përgjegjësi të Kufizuar (SH.P.K.) is the most frequently registered structure. Its combination of limited liability, a single-shareholder minimum, and relatively low capital threshold makes it practical for both small domestic firms and foreign investors entering the market.

Foreign nationals face no ownership restrictions under Business Organizations Law No. 02/L-123 and may register a SH.P.K., SH.A., branch office, or sole proprietorship. A branch office does not create a separate legal entity, meaning the parent company retains full liability for its Kosovo operations.

No. A Shoqëria Kolektive (SH.K.) general partnership requires at least two partners, and a limited partnership (SH.K.P.) requires at least one general and one limited partner. A SH.P.K. and SH.A., however, can each be formed by a single shareholder.

A SH.P.K. and SH.A. each hold full legal personality distinct from their owners. Branch offices and representative offices do not — they remain extensions of the foreign parent. General and limited partnerships occupy an intermediate position; they may enter contracts but partner liability is not fully ring-fenced.

A sole proprietorship (Tregtari Individual) carries the lightest compliance burden, with no audit requirement and simplified bookkeeping obligations. That simplicity comes with the trade-off of unlimited personal liability, which makes it unsuitable for operations carrying significant financial or contractual risk.

Conversion between entity types is permitted under Kosovo's Business Organizations Law, most commonly from a SH.P.K. to a SH.A. as a business scales and seeks external capital. The process requires KBRA filings, updated founding documents, and, where applicable, revised shareholder agreements.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.