Key Takeaways

- The Securities and Exchange Commission of Pakistan (SECP) administers all company registrations under the Companies Act, 2017, while partnerships and sole proprietorships fall under the separate Partnership Act, 1932.

- Private Limited Companies remain the most registered entity type under SECP, offering liability protection and operational flexibility for both resident entrepreneurs and foreign investors.

- Foreign entities seeking a non-trading presence in Pakistan can register a Liaison Office, whereas those conducting active operations may establish a Branch Office instead.

- Partnerships and sole proprietorships carry unlimited liability and are registered at the provincial level, outside SECP's jurisdiction.

Introduction to Entity Types in Pakistan

Pakistan is a sovereign republic in South Asia, sharing borders with India, Afghanistan, Iran, and China. As a common-law jurisdiction with a codified corporate framework, it offers a defined set of business entity types in Pakistan that suit both domestic operators and foreign investors.

Company registration falls under the authority of the Securities and Exchange Commission of Pakistan (SECP), which administers the Companies Act, 2017 — the primary legislation governing corporate formation, governance, and dissolution. Partnerships and sole proprietorships operate under separate statutes, including the Partnership Act, 1932.

Pakistan follows a residence-based tax system, with corporate income subject to tax under the Income Tax Ordinance, 2001, and an active treaty network covering numerous jurisdictions.

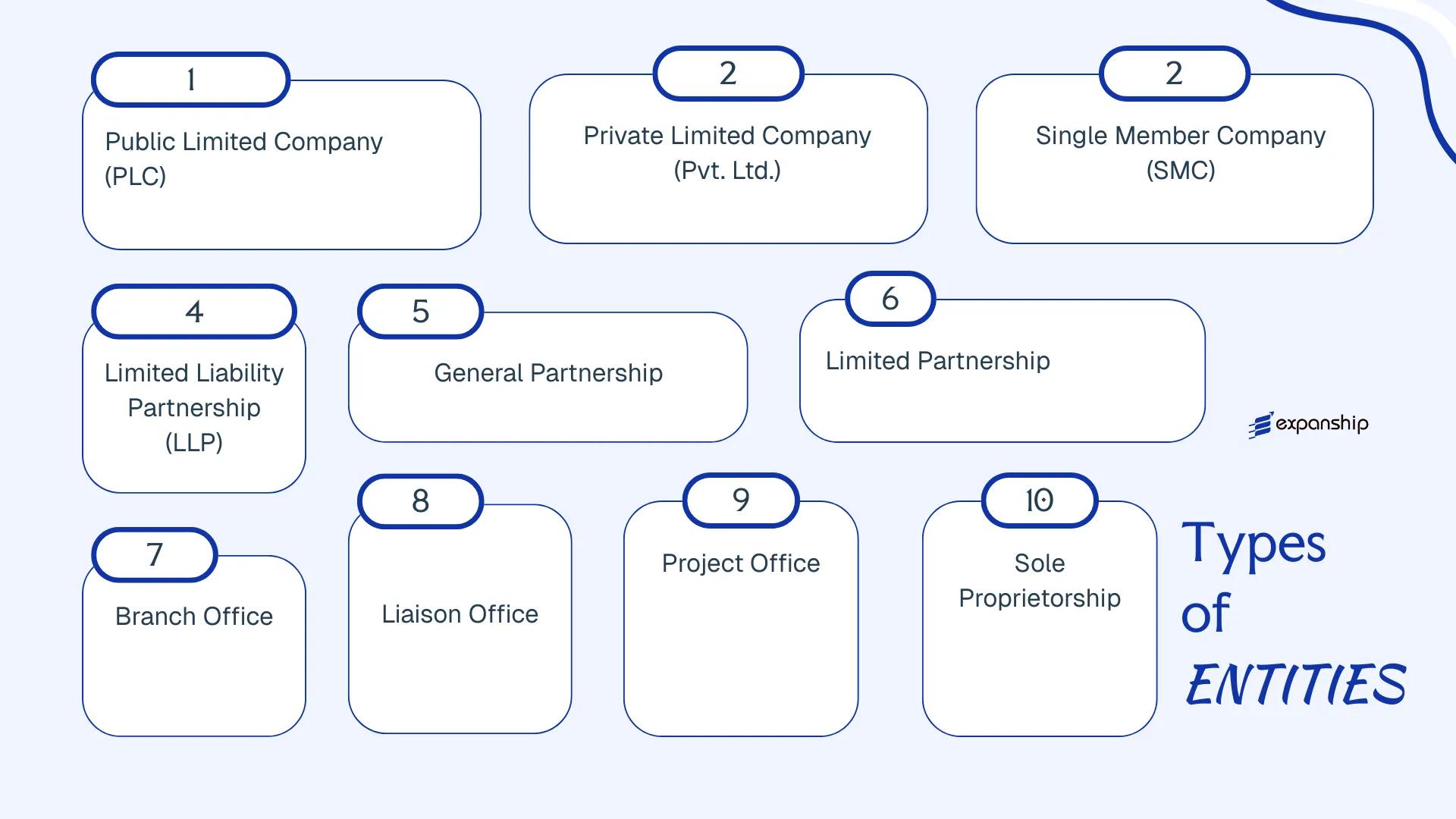

Businesses operating here may register as one of the following structures:

- Public Limited Company

- Private Limited Company

- Single Member Company

- Limited Liability Partnership

- General Partnership

- Limited Partnership

- Branch Office

- Liaison Office

- Project Office

- Sole Proprietorship

Each structure carries distinct requirements around ownership, liability, governance, and regulatory compliance — all of which this article examines in detail.

An Overview of Business Structures in Pakistan

Pakistan's company law framework provides several distinct forms of business organization, each governed primarily by the Companies Act, 2017, administered by the Securities and Exchange Commission of Pakistan (SECP). The Limited Liability Partnership Act, 2017 governs LLPs as a separate category, while sole proprietorships and general partnerships fall under provincial and federal registration requirements outside SECP's direct remit. Each structure carries different implications for ownership, liability, and regulatory obligations.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Public Limited Company (PLC) | Incorporated company | Limited | Taxed | Yes | 3 directors, 7 members | SECP | Companies Act, 2017 |

| Private Limited Company (Pvt. Ltd.) | Incorporated company | Limited | Taxed | Yes | 2 members | SECP | Companies Act, 2017 |

| Single Member Company (SMC) | Incorporated company | Limited | Taxed | Yes | 1 member | SECP | Companies Act, 2017 |

| Limited Liability Partnership (LLP) | Hybrid entity | Limited | Taxed | Yes | 2 partners | SECP | LLP Act, 2017 |

| General Partnership | Unincorporated firm | Unlimited | Taxed | Yes | 2–20 partners | FBR / Provincial | Partnership Act, 1932 |

| Limited Partnership | Unincorporated firm | Mixed | Taxed | Yes | Min. 1 general partner | Provincial | Partnership Act, 1932 |

| Branch Office | Foreign entity extension | Parent liable | Taxed | Restricted | N/A | SECP / BOI | Companies Act, 2017 |

| Liaison Office | Foreign entity extension | Parent liable | Exempt | No | N/A | SECP / BOI | Companies Act, 2017 |

| Project Office | Foreign entity extension | Parent liable | Taxed | Project-specific | N/A | SECP / BOI | Companies Act, 2017 |

| Sole Proprietorship | Unincorporated individual | Unlimited | Taxed | Yes | 1 owner | FBR / Provincial | N/A (registration-based) |

Each of these structures is examined in full in the sections below.

Public Limited Company (PLC)

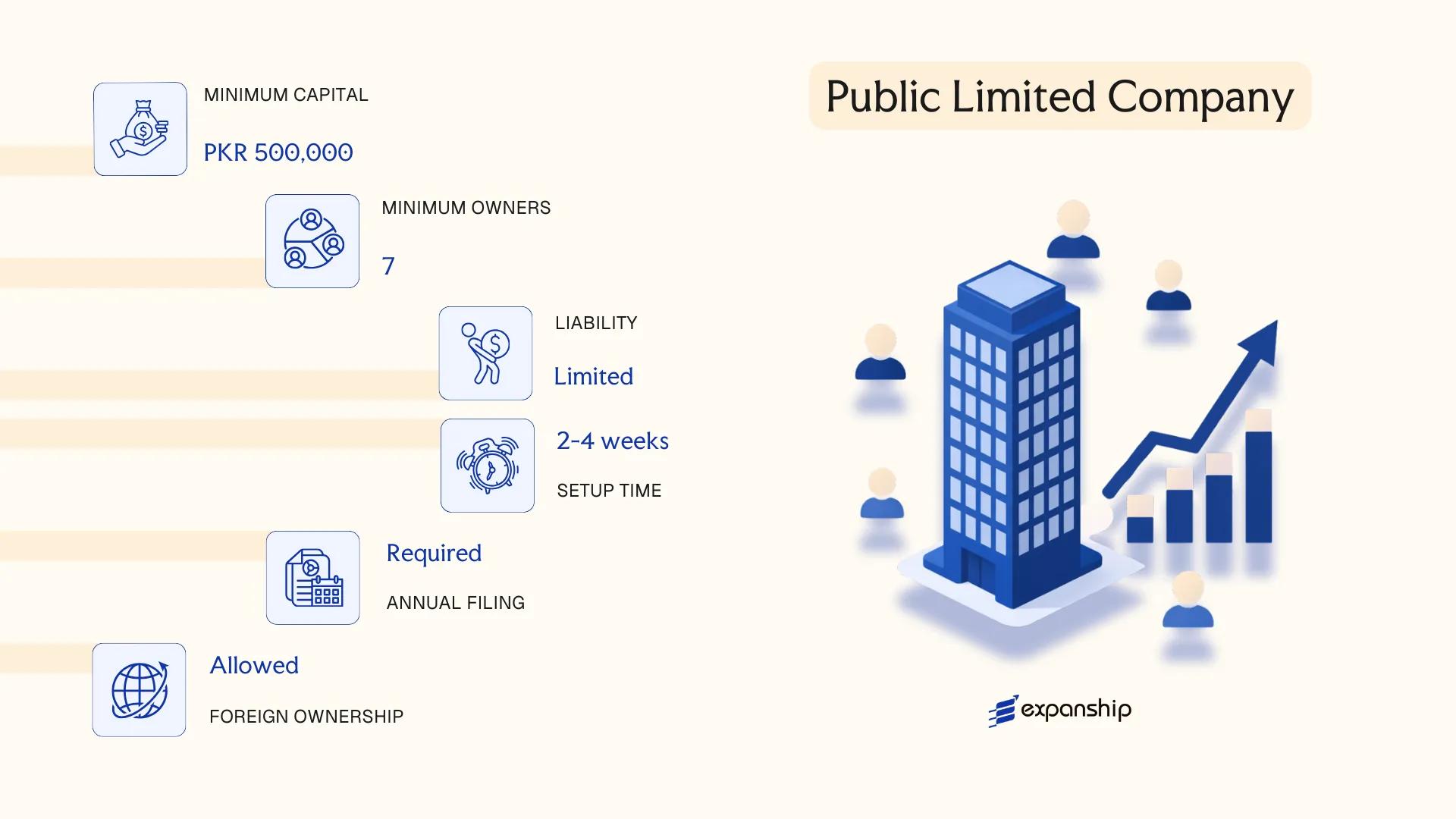

A public limited company Pakistan PLC structure is governed by the Companies Act, 2017, administered by the Securities and Exchange Commission of Pakistan (SECP). The entity carries separate legal personality, meaning its rights and obligations are distinct from those of its shareholders. Liability is limited to the amount unpaid on shares held.

Listing on a stock exchange is not mandatory for a public limited company, though any firm intending to offer shares to the general public must be registered as one. Unlisted PLCs exist and operate without exchange admission, but listed company formation in Pakistan requires additional compliance under the Pakistan Stock Exchange (PSX) rulebook and relevant SECP regulations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate | Separate legal personality; perpetual succession |

| Members | Minimum 3 directors; minimum 3 shareholders; no upper limit on shareholders | Directors and shareholders may overlap |

| Capital | PKR; no statutory minimum for unlisted PLCs; listed PLCs subject to PSX minimum capital requirements | Shares may be offered to the public |

| Local Presence | Registered office in Pakistan required | Must be maintainable and accessible to SECP |

| Privacy | Financials and shareholder register are publicly accessible via SECP's Company Registration Office (CRO) | Lower privacy than private entities |

Focus Points

- Taxation: Subject to corporate income tax at rates set by the Federal Board of Revenue (FBR); listed companies historically receive a reduced rate versus unlisted ones; withholding tax, sales tax, and super tax obligations may also apply depending on sector and turnover.

- Annual Compliance: Audited financial statements, annual general meeting (AGM), and annual return filing with SECP are mandatory.

- Treaty Access: Pakistan maintains a network of double taxation treaties; a locally incorporated PLC qualifies as a tax resident entity for treaty purposes.

- Conversion: A private limited company may convert to a public limited company under the Companies Act, 2017, subject to SECP approval and structural adjustments.

- Restrictions: Public companies face stricter disclosure requirements and cannot restrict share transferability as private entities can.

Closing

A public limited company suits businesses seeking broad capital access — particularly those planning an eventual PSX listing or requiring a shareholder base beyond the caps applicable to private structures. The primary advantage is unrestricted share issuance to the public; the principal drawback is the significant ongoing compliance burden relative to smaller entity forms.

PLCs are most appropriate for large-scale enterprises, joint ventures with public participation, or businesses with structured plans to list on the Pakistan Stock Exchange.

Company Incorporation in Pakistan

Incorporate a public limited company or any other business structure in Pakistan with Expanship's end-to-end support.

Private Limited Company (Pvt. Ltd.)

The private limited company is the most widely used corporate structure for foreign and domestic investors operating in Pakistan. Governed by the Companies Act, 2017, and regulated by the Securities and Exchange Commission of Pakistan (SECP), a private limited company Pakistan Pvt Ltd structure carries separate legal personality, meaning the company itself holds rights, obligations, and assets distinct from its shareholders.

Liability of shareholders is capped at their subscribed share capital. This combination of limited liability and operational flexibility makes the Pvt. Ltd. a practical choice across a broad range of commercial activities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private Limited Company | Incorporated under Companies Act, 2017 |

| Members | Directors: min. 1, max. 7; Shareholders: min. 1, max. 50 | Transfer of shares is restricted by default |

| Local Presence | Registered office address required in Pakistan | Must be maintained at all times with SECP |

| Share Capital | PKR; no statutory minimum capital requirement | Authorized and paid-up capital disclosed at incorporation |

| Privacy | Beneficial ownership disclosure required to SECP | Not publicly searchable in full detail |

Focus Points

- Taxation: Subject to corporate income tax (standard rate 29% for non-small companies); sales tax, withholding tax obligations, and advance tax provisions apply under the Income Tax Ordinance, 2001.

- Annual Compliance: Annual returns, audited financial statements, and statutory filings due with SECP; audit is mandatory regardless of size.

- Treaty Access: Pakistan maintains a network of double taxation treaties; a locally incorporated entity qualifies for resident status and treaty benefits.

- Conversion: Can be converted to a public limited company or single member company under the Companies Act, 2017, subject to SECP approval.

- Restrictions: Cannot invite public subscription for shares or list on a stock exchange while retaining private status.

Closing

A private limited company suits trading operations, subsidiary structures, joint ventures, and market-entry vehicles where liability protection and operational continuity are priorities. The absence of a minimum capital threshold lowers the barrier to Pakistan private company incorporation, though mandatory annual audits add a recurring compliance cost that smaller businesses should factor into their planning.

Best suited for foreign investors establishing a subsidiary, mid-sized domestic businesses, and joint venture partners seeking a structured, legally distinct operating entity in Pakistan.

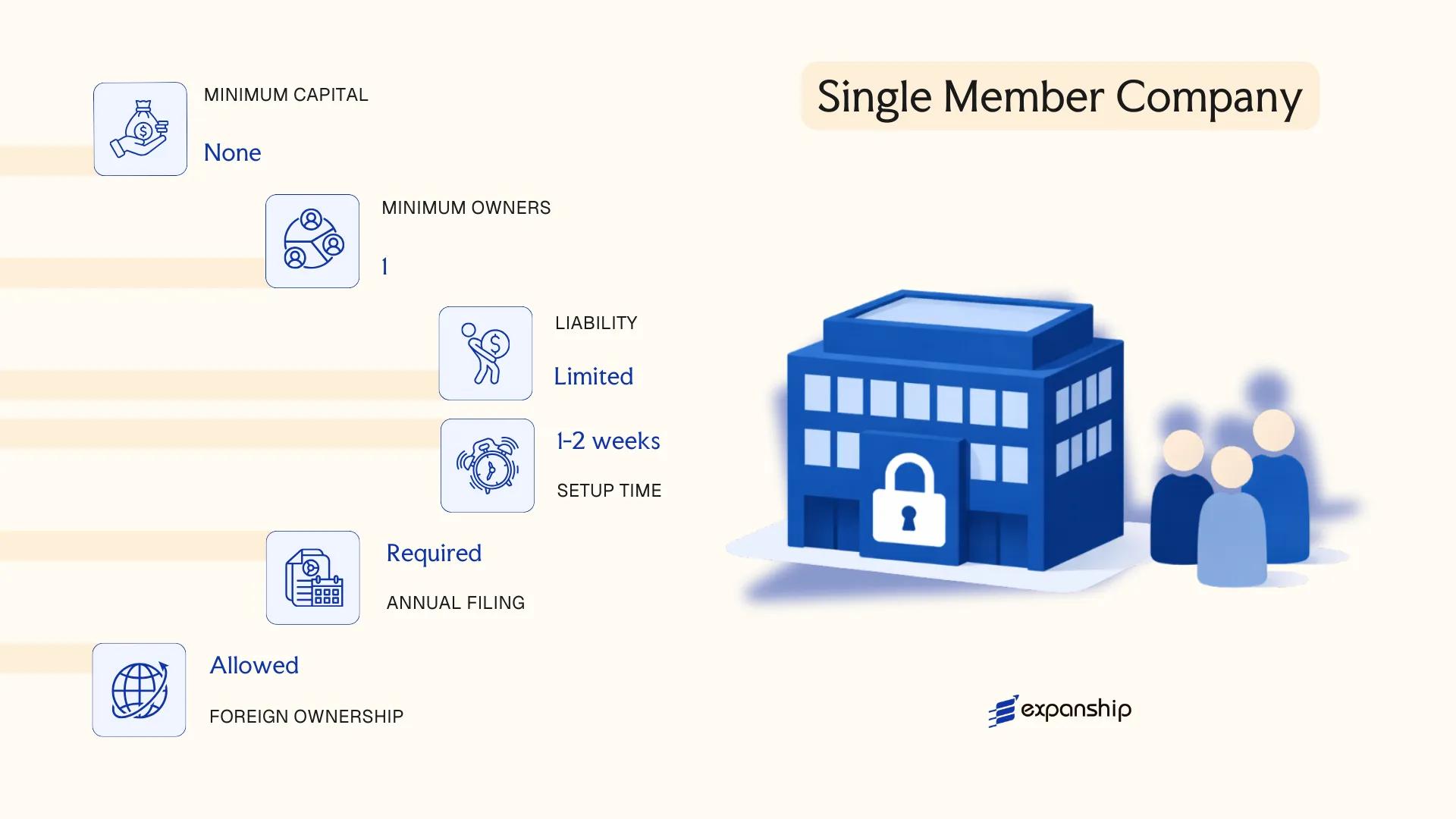

Single Member Company (SMC)

A single member company Pakistan SMC is governed by the Companies Act, 2017, administered by the Securities and Exchange Commission of Pakistan (SECP). This structure carries full separate legal personality, meaning the sole shareholder's personal assets remain insulated from the company's liabilities.

Introduced as a distinct category under Schedule II of the Companies Act, 2017, this one person company Pakistan allows an individual to own and operate a limited liability entity without requiring additional shareholders. The SECP maintains a dedicated registration pathway for this structure.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Private company with single shareholding | Carries separate legal personality; not a sole proprietorship |

| Members | 1 shareholder (minimum and maximum) | Nominee shareholder details must be filed with SECP |

| Directors | Minimum 1 director | Director and shareholder may be the same individual |

| Local Presence | Registered office address in Pakistan required | Must be maintained at all times; no registered agent requirement |

| Share Capital | PKR; no statutory minimum | Authorised and paid-up capital declared at incorporation |

| Privacy | Beneficial ownership disclosures required | Filed with SECP; not fully public but accessible to regulators |

Focus Points

- Taxation: Subject to standard corporate income tax (29% for tax year 2024); withholding tax obligations apply on payments; sales tax registration required if turnover threshold is met; stamp duty applies on instrument of transfer.

- Annual Compliance: Annual return and audited financial statements filed with SECP; statutory audit mandatory regardless of size.

- Conversion: Can be converted to a private limited company if membership expands beyond one shareholder.

- Nominee Requirement: A nominee must be designated at incorporation to assume ownership upon the member's death or incapacity.

- Restrictions: Cannot invite the public to subscribe to its shares or debentures.

Closing

An SMC suits freelancers, solo founders, and consultants seeking limited liability without a multi-shareholder structure, though the mandatory nominee filing and full audit requirement add administrative obligations that an unincorporated sole proprietorship does not carry.

Best suited for individual entrepreneurs and professionals in Pakistan who require a legally distinct entity with liability protection but have no immediate need for co-ownership.

Limited Liability Partnership (LLP)

Governed by the Limited Liability Partnership Act, 2017, a limited liability partnership Pakistan LLP is a distinct legal entity separate from its partners. This structure combines partnership flexibility with the liability protection typically associated with incorporated companies — partners are not personally liable for the firm's debts beyond their agreed contribution.

Unlike a conventional partnership, an LLP holds assets, enters contracts, and initiates legal proceedings in its own name. SECP limited liability partnership registration is handled through the Securities and Exchange Commission of Pakistan (SECP), which maintains the central register under this legislation.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Body corporate with separate legal personality | Distinct from its partners in law |

| Members | Minimum 2 designated partners; no statutory maximum | At least one designated partner must be a natural person |

| Local Presence | Registered office address required in Pakistan | Must be maintained throughout the LLP's existence |

| Capital | PKR; no prescribed minimum capital | Governed by the LLP agreement between partners |

| Privacy | LLP agreement is not publicly filed | Partner details are on the public register |

Focus Points

- Taxation: Subject to corporate income tax at applicable rates; partners' shares may attract additional withholding tax obligations; sales tax applies where services are rendered.

- Annual Compliance: Annual return and statement of accounts must be filed with SECP each year.

- Conversion: An existing partnership or private company may convert to an LLP under prescribed procedures in the 2017 Act.

- Restrictions: Foreign nationals may participate subject to applicable foreign investment regulations and SECP requirements.

Closing

An LLP suits professional services firms, joint ventures, and businesses where partners want operational flexibility without the governance formality of a company structure. The key advantage is personal liability protection without mandatory share capital; however, the structure remains less familiar to international counterparties and may face scrutiny in cross-border financing arrangements.

LLP Pakistan formation is most appropriate for professional practices, consulting firms, and domestic joint ventures where partners prefer contractual flexibility over a formal corporate framework.

Partnerships [General Partnership, Limited Partnership]

Governed by the Partnership Act 1932, partnership firms in Pakistan do not hold separate legal personality. This means partners are personally liable for the firm's debts and obligations, with assets of individual partners exposed to creditors of the business.

Partnership firm registration Pakistan is handled through the Registrar of Firms, operating under provincial jurisdiction. While registration is not compulsory under the Act, an unregistered firm cannot file suit to enforce rights arising from a contract. Registration is therefore strongly advisable for any firm intending to conduct formal commercial activity.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated firm | No separate legal personality; partners are the firm |

| Members | Partners; minimum 2, maximum 20 (general business); 10 for banking firms | Limits set under the Partnership Act 1932 and Companies Act 2017 |

| Local Presence | Registered office address required for Registrar filing | Provincial registration; jurisdiction varies by province |

| Capital | No statutory minimum; denominated in PKR | Defined by partnership deed |

| Liability | Unlimited (general partners) | Limited partners have liability capped at their contribution |

| Privacy | Partnership deed is filed with the Registrar | Deed details become part of provincial record |

Focus Points

- Taxation: Firm income taxed at 35% corporate rate under the Income Tax Ordinance 2001; partners' profit shares may attract further personal income tax; withholding tax provisions apply to payments made by the firm.

- Annual Compliance: Tax return filing with the Federal Board of Revenue (FBR); no mandatory annual return to the Registrar post-registration.

- Treaty Access: Partnerships generally do not qualify as tax residents eligible for Pakistan's double tax treaty network, limiting treaty benefits.

- Conversion: A partnership cannot convert directly into a private limited company without dissolution and fresh incorporation under the Companies Act 2017.

- Restrictions: Foreign nationals face restrictions on forming or joining partnerships in regulated sectors; prior approval may be required from relevant sectoral authorities.

Sub-Types

General Partnership

All partners carry unlimited joint and several liability for firm obligations. Management rights are shared among partners unless the deed specifies otherwise. This structure is common in professional practices such as law and accountancy.

Limited Partnership

Recognised under the Partnership Act 1932, a limited partnership includes at least one general partner with unlimited liability and one or more limited partners whose liability is confined to their agreed capital contribution. Limited partners may not participate in management without losing their limited liability status.

Closing Paragraph and Recommendations

Partnerships suit smaller domestic ventures, professional service providers, and family-run businesses where the partners have a high degree of mutual trust and where the scale of activity does not justify the compliance overhead of a limited company. The primary drawback is unlimited personal liability for general partners, which exposes personal assets to business risk.

A partnership under the Partnership Act 1932 is best suited for small domestic businesses or licensed professionals seeking a low-cost, informally governed structure with a known co-partner.

Foreign Business Presence in Pakistan [Branch Office, Liaison Office, Project Office]

A foreign company branch office Pakistan registration is governed by the Companies Act, 2017, under which the Securities and Exchange Commission of Pakistan (SECP) regulates all forms of foreign business presence. Unlike a locally incorporated entity, a branch office, liaison office, and project office do not constitute separate legal persons — each remains an extension of the parent foreign company, which retains full liability for the operations conducted.

Registration is filed with SECP under Section 432 of the Companies Act, 2017, and foreign entities must submit certified constitutional documents, a board resolution authorising establishment, and details of the local authorised representative.

Key Characteristics

| Requirement | Branch Office | Liaison Office | Project Office |

|---|---|---|---|

| Legal Form | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality | Extension of foreign parent; no separate legal personality |

| Permitted Activities | Commercial and operational activities | Representative and promotional activities only; no revenue generation | Activities limited to scope of specific contract or project |

| Key Personnel | Authorised representative (local) required | Authorised representative (local) required | Authorised representative (local) required |

| Local Office | Registered local address mandatory | Registered local address mandatory | Registered local address mandatory |

| Capital | No minimum capital requirement; parent company bears financial responsibility | No minimum capital requirement | No minimum capital requirement |

| Duration | Ongoing, subject to annual renewal | Ongoing, subject to annual renewal | Tied to project duration; closes upon project completion |

Focus Points

- Taxation: Branch offices are subject to corporate income tax at 29% on Pakistan-sourced income; a branch remittance tax of 15% applies on after-tax profits transferred abroad; liaison offices generating no income are generally outside the corporate tax net, though transfer pricing rules may apply where intra-group charges exist.

- Compliance: All three forms must file annual returns with SECP; branch offices additionally submit audited accounts of the foreign parent.

- Treaty Access: Pakistan's double taxation agreements may reduce withholding tax rates on payments to the parent, but eligibility depends on the treaty partner and structure.

- Restrictions: Liaison offices are prohibited from commercial activity; conversion to a local company requires fresh incorporation and is not a direct structural conversion.

- Repatriation: Prior State Bank of Pakistan (SBP) approval may be required for profit remittances above prescribed thresholds.

Sub-Types

Branch Office

A branch office may conduct revenue-generating commercial operations in Pakistan on behalf of the foreign parent. It is the appropriate structure when the foreign entity intends to enter into contracts, invoice clients, or maintain operational staff locally.

Liaison Office

Liaison office setup Pakistan is limited strictly to non-commercial functions — market research, promoting the parent's products, or coordinating with local partners. No invoicing or revenue collection is permitted from within Pakistan.

Project Office

Project office registration Pakistan SECP applies where a foreign company has secured a specific contract — typically in construction, infrastructure, or energy — and requires a temporary local presence. The office's existence is tied directly to the contract term and must be wound down upon project completion.

These structures suit foreign businesses testing the local market or executing defined contracts without committing to full local incorporation. The primary advantage is operational speed — setup is faster than incorporating a new company. The binding limitation is that the parent entity remains fully liable for all obligations incurred.

Foreign business presence structures are best suited for multinational firms with specific project mandates or exploratory market intentions, rather than those seeking a permanent, scalable commercial operation.

Sole Proprietorship

Sole proprietorship registration in Pakistan does not fall under a single consolidated statute. Instead, the structure is governed indirectly through the Registration Act 1908, applicable sales tax and income tax provisions under the Income Tax Ordinance 2001, and local municipal registration requirements that vary by province. The business and its owner are legally the same person — there is no separate legal personality, and the proprietor bears unlimited personal liability for all obligations of the firm.

Registration is handled at the local level, typically through a district or municipal authority, and the proprietor must also register with the Federal Board of Revenue (FBR) to obtain a National Tax Number (NTN). A bank account in the business name generally requires proof of this registration alongside a valid CNIC.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated business | No separate legal personality; owner and business are one and the same |

| Members | Single proprietor | No minimum capital; no shareholders or directors |

| Local Presence | Physical address required | Municipal/district registration ties the business to a specific locality |

| Capital | PKR; no statutory minimum | Determined entirely by the proprietor |

| Privacy | No public filing of financials | Business records are not submitted to SECP or any central registry |

Focus Points

- Taxation: Subject to personal income tax under the Income Tax Ordinance 2001 at progressive rates; sales tax registration with FBR is required if annual turnover exceeds the prescribed threshold; no separate corporate tax applies.

- Annual Compliance: FBR income tax return filing is mandatory annually; provincial tax obligations may also apply depending on the nature of services rendered.

- Treaty Access: As an unincorporated entity with no separate legal personality, treaty benefits under Pakistan's double taxation agreements are generally not available.

- Conversion: Can be converted into a Private Limited Company or Single Member Company by incorporating a new entity under the Companies Act 2017; assets must be formally transferred.

- Restrictions: Foreign nationals cannot register a sole proprietorship in Pakistan; the structure is available only to Pakistani citizens holding a valid CNIC.

Recommendations

A sole proprietorship suits freelancers, consultants, and small traders operating domestically with modest turnover and no intention to raise external capital. The primary advantage is minimal setup cost and administrative simplicity; the principal drawback is unlimited personal liability, which exposes the owner's personal assets to any business debts or legal claims.

Pakistani nationals running low-risk, owner-operated businesses with no plans for external investment or cross-border operations.

How to Choose the Right Entity Type in Pakistan

Selecting the wrong structure from the outset has measurable legal and financial consequences — not just administrative inconvenience.

Why Your Entity Choice Matters

The Companies Act, 2017 governs most corporate entities in Pakistan and sets the framework within which the Securities and Exchange Commission of Pakistan (SECP) enforces compliance. Getting the entity selection wrong produces concrete outcomes:

- Registering a foreign branch when your operations require a locally incorporated entity can constitute a breach of the Act, exposing the business to penalties or de-registration by SECP.

- Choosing a structure without audit exemption eligibility — such as a Single Member Company above the prescribed thresholds — results in mandatory statutory audit costs even for single-person consultancy operations.

- Selecting an entity type that does not qualify as a Pakistani tax resident may forfeit access to withholding tax reductions under applicable double taxation treaties.

- Forming a private limited company when a partnership structure would suffice locks your business into annual SECP filing obligations, director duties, and statutory meeting requirements that partnerships do not carry.

Key Factors to Consider

- Business Activity: Active trading, regulated sector operations (banking, insurance, funds), and passive asset holding each point toward a distinct structure under Pakistani law.

- Ownership Configuration: A single founder points toward an SMC, while multiple parties with defined profit-sharing arrangements may find an LLP more operationally suited.

- Tax Residency and Treaty Access: Your entity must qualify as a Pakistani tax resident to benefit from the country's double taxation agreements — not all structures satisfy this requirement.

- Disclosure Tolerance: SECP maintains a public register of directors and shareholders for companies; partnerships offer comparatively less public exposure.

- Regulatory Licensing: Certain sectors require the sponsoring entity to hold a specific corporate form as a condition of licensing — confirm this before incorporating.

- Operational Substance: If your business cannot maintain a physical presence, staff, and local decision-making, structures with lower substance thresholds or no substance requirements should be prioritised.

Corporate Compliance Services in Pakistan

Ongoing SECP filings, annual returns, and statutory maintenance for companies and partnerships registered in Pakistan.

Conclusion

Selecting the right structure before incorporating a company in Pakistan determines not just your compliance obligations, but your tax exposure, governance requirements, and ability to raise capital. The Private Limited Company remains the most registered entity type under SECP, favored by resident entrepreneurs and foreign investors alike for its liability protection and operational flexibility. Single Member Companies serve solo founders who require a separate legal personality without partnership obligations. Public Limited Companies are suited to businesses seeking capital market access through the Pakistan Stock Exchange. For foreign entities establishing a non-trading presence, a Liaison Office offers a lower-commitment entry point, while a Branch Office suits those conducting active operations. Partnerships and sole proprietorships carry unlimited liability and are registered at the provincial level rather than through SECP. Ongoing reforms to the Companies Act 2017 and Pakistan's expanding tax treaty network continue to shape how foreign-owned entities are structured domestically.

How Expanship Can Assist You

Expanship company registration Pakistan services are built around the specific requirements of the Securities and Exchange Commission of Pakistan (SECP), which oversees the incorporation of private limited companies, public limited companies, single member companies, and LLPs under the Companies Act 2017. Your entity type determines the registration pathway, and Expanship works with you to match your business objectives to the right structure from the start.

From document preparation through to post-incorporation obligations, Pakistan business incorporation assistance covers every stage of the process:

- Document preparation and notarization

- Registered agent and registered office provision

- SECP filing and company registrar liaison

- National Tax Number (NTN) registration coordination

- Post-incorporation compliance management

- Banking introduction assistance

Ready to take the next step? Reach out to Expanship Pakistan to discuss your setup.

Frequently Asked Questions (FAQ)

The Private Limited Company is the most frequently incorporated structure under the Companies Act, 2017. It offers liability protection without the disclosure and governance obligations that apply to Public Limited Companies, making it the default choice for small to mid-sized enterprises.

A Branch Office is an extension of a foreign parent and does not constitute a separate legal entity under Pakistani law, whereas a Private Limited Company is locally incorporated and treated as a distinct legal person. Branches are generally restricted to the activities permitted in their SECP registration approval and carry the parent's tax exposure, while a Pvt. Ltd. is taxed as a resident entity and can trade freely in the local market.

The Single Member Company discloses minimal ownership detail in public filings relative to a multi-shareholder structure, though beneficial ownership disclosures are still required under SECP regulations. Nominee directorship is legally permissible, but nominee shareholding is subject to disclosure requirements under the Companies Act, 2017.

No. A Single Member Company requires only one natural person as shareholder, while a Private Limited Company requires a minimum of two shareholders. General and Limited Partnerships both require at least two partners, and a Limited Liability Partnership similarly cannot be formed by a sole individual.

Foreign individuals and entities may incorporate a Private Limited Company, Public Limited Company, or Single Member Company with 100% foreign ownership in most sectors, subject to sector-specific restrictions outlined in the Board of Investment's policy framework. Branch Offices and Liaison Offices are also available to foreign corporations, though each requires a separate SECP filing and approval process.

Conversion between certain structures is permitted. A Private Limited Company may re-register as a Public Limited Company under the Companies Act, 2017, and the reverse conversion is also possible subject to shareholder approval and SECP requirements. Conversion from a partnership to a company requires fresh incorporation rather than a statutory continuation process.

No. Sole Proprietorships and General Partnerships do not have legal personality distinct from their owners, meaning personal assets remain exposed to business liabilities. Private Limited Companies, Public Limited Companies, Single Member Companies, and LLPs all carry separate legal personality under their respective governing statutes.

A Sole Proprietorship carries the lightest compliance burden, with no annual filing requirement with the SECP and no mandatory audit. The trade-off is unlimited personal liability and the absence of a formal capital structure, which limits its suitability for businesses seeking external investment or contractual counterparties that require a registered corporate entity.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.