Key Takeaways

- Business entity types in French Polynesia are governed by French civil and commercial law adapted to local ordinances, with company registration administered by the Tribunal Mixte de Commerce de Papeete through the Registre du Commerce et des Sociétés (RCS).

- French Polynesia maintains its own fiscal regime entirely separate from metropolitan France, with distinct tax rates and exemptions rather than a zero- or territorial-tax structure.

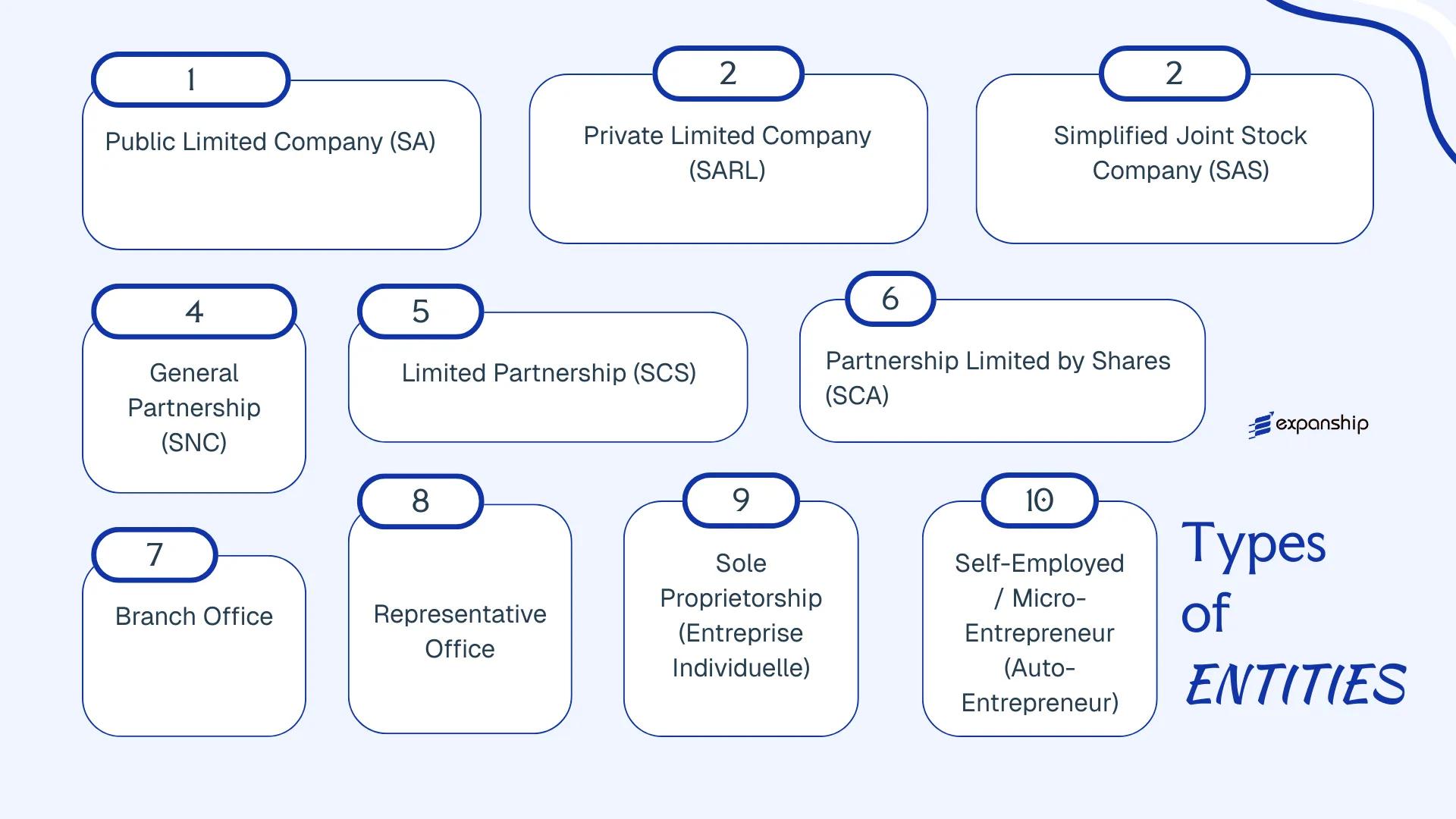

- Among the available structures — SA, SARL, SAS, SNC, SCS, SCA, Branch Office, Representative Office, Entreprise Individuelle, and Auto-Entrepreneur — the SARL is the most commonly registered entity across the territory.

- The SAS is the most structurally flexible option for investor-driven arrangements, while branch and representative offices allow foreign firms to establish a market presence without undertaking full local incorporation.

Introduction to Entity Types in French Polynesia

French Polynesia is an overseas collectivity of France, situated in the South Pacific Ocean roughly midway between California and Australia. Comprising more than 100 islands across five archipelagos, it operates under French constitutional law while retaining a degree of internal autonomy through its own statute of autonomy.

Business entity types in French Polynesia follow the French civil and commercial law framework, adapted to the local regulatory environment. Company registration falls under the jurisdiction of the Registre du Commerce et des Sociétés (RCS), administered through the Tribunal Mixte de Commerce de Papeete. Businesses operating here are also subject to the local tax code — Polynésie française maintains its own fiscal regime, separate from metropolitan France, with its own rates and exemptions rather than a straightforward zero- or territorial-tax posture.

Several corporate entity types are available to investors and entrepreneurs, including the Société Anonyme (SA), Société à Responsabilité Limitée (SARL), Société par Actions Simplifiée (SAS), Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA), Branch Office, Representative Office, Entreprise Individuelle, and Auto-Entrepreneur. Each structure carries distinct requirements around capital, liability, governance, and taxation. This article examines each form in detail to help your business identify the most appropriate structure.

An Overview of Business Structures in French Polynesia

French Polynesia recognises several distinct entity types under its corporate law framework, which draws from French metropolitan law as adapted through the statutes of autonomy governing the territory. The primary legislation is the Code de Commerce as applied locally, supplemented by territorial regulations issued by the Assemblée de la Polynésie française. Each structure carries different implications for liability, ownership, taxation, and permissible activities.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| SA | Public limited company | Limited to shares | Taxable (IS) | Yes | 7 shareholders | Direction des Affaires Économiques | Code de Commerce |

| SARL | Private limited company | Limited to shares | Taxable (IS) | Yes | 1–100 associates | Direction des Affaires Économiques | Code de Commerce |

| SAS | Simplified joint stock | Limited to shares | Taxable (IS) | Yes | 1+ shareholders | Direction des Affaires Économiques | Code de Commerce |

| SNC | General partnership | Unlimited, joint | Transparent | Yes | 2+ partners | Direction des Affaires Économiques | Code de Commerce |

| SCS | Limited partnership | Mixed liability | Transparent | Yes | 2+ partners | Direction des Affaires Économiques | Code de Commerce |

| SCA | Partnership limited by shares | Mixed liability | Taxable (IS) | Yes | 4+ partners | Direction des Affaires Économiques | Code de Commerce |

| Branch Office | Extension of foreign entity | Parent liable | Taxable (IS) | Yes | N/A | Direction des Affaires Économiques | Territorial regulations |

| Representative Office | Non-trading presence | Parent liable | Generally exempt | No | N/A | Direction des Affaires Économiques | Territorial regulations |

| Entreprise Individuelle | Sole proprietorship | Unlimited | IR (personal) | Yes | 1 individual | Direction des Affaires Économiques | Code de Commerce |

| Auto-Entrepreneur | Micro-enterprise regime | Unlimited | Flat-rate IR | Yes | 1 individual | Direction des Impôts et des Contributions Publiques | Territorial micro-enterprise rules |

Each of these structures is examined in full in the sections below.

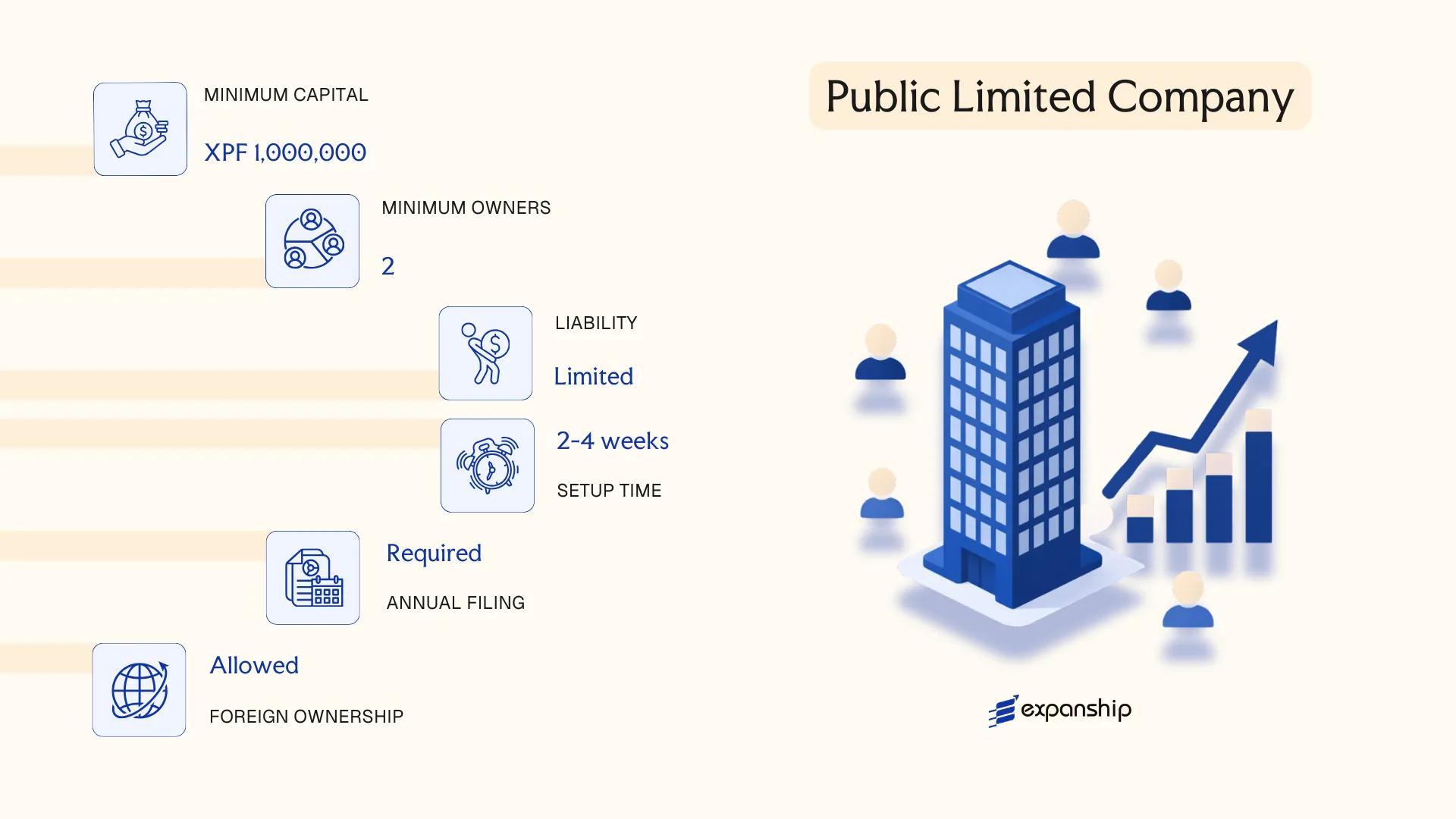

Société Anonyme (SA) — Public Limited Company

The Société Anonyme French Polynesia framework is governed by local commercial law adapted from the French Code de commerce, as applied and modified within the territory's autonomous legal order. As a distinct legal entity, the SA carries full separate legal personality, meaning it can contract, own assets, and incur liabilities in its own name independently of its shareholders.

Minimum capital requirements and governance obligations make this structure more demanding than simpler forms, but it accommodates public share issuance and multi-tiered management. Your business gains the capacity to issue transferable shares to a broad investor base, which is why larger commercial ventures and holding structures tend to favour this form.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société Anonyme (SA) | Incorporated entity with separate legal personality |

| Members | Shareholders (min. 7) | No statutory maximum; shares are freely transferable |

| Governance | Board of Directors (min. 3, max. 18) + General Manager | Alternatively, a Supervisory Board and Management Board structure may apply |

| Capital | Minimum XPF 1,000,000 (approx. EUR 8,380) | Must be fully subscribed; 50% paid up at incorporation |

| Local Presence | Registered office in French Polynesia required | No mandatory local director, but registered address is obligatory |

| Privacy | Shareholder and director details filed publicly | No beneficial ownership anonymity |

Focus Points

- Taxation: Subject to corporate income tax (Impôt sur les Sociétés) administered by the Direction Générale des Impôts et des Contributions Publiques (DGICP); standard rate applies to net profits, with specific withholding tax rates on dividends distributed to non-residents; no VAT at territorial level in the conventional sense, though a local consumption tax (Taxe sur la Valeur Ajoutée Polynésienne) may apply depending on activity.

- Compliance: Annual general meeting, statutory audit, and financial statement filing obligations apply; auditor (commissaire aux comptes) appointment is mandatory.

- Economic Substance: No specific OECD-style substance legislation is in force at the territorial level, but commercial activity must be genuinely conducted through the registered entity.

- Treaty Access: French Polynesia is an overseas collectivity and does not independently access France's tax treaty network; treaty benefits are generally unavailable to entities incorporated here.

- Conversion: An SA may be converted to an SAS or SARL under applicable local commercial law, subject to shareholder vote and regulatory notification.

Closing

The SA suits large-scale commercial operations, joint ventures requiring institutional investor participation, or holding structures where share transferability and formal governance are priorities. The principal limitation is administrative burden — the minimum shareholder threshold of seven and mandatory audit requirements make it impractical for small or closely held businesses.

Best suited for large enterprises, institutional joint ventures, or businesses anticipating public or multi-investor shareholding structures.

Company Incorporation in French Polynesia

Incorporate your Société Anonyme or other entity type in French Polynesia with end-to-end support from Expanship.

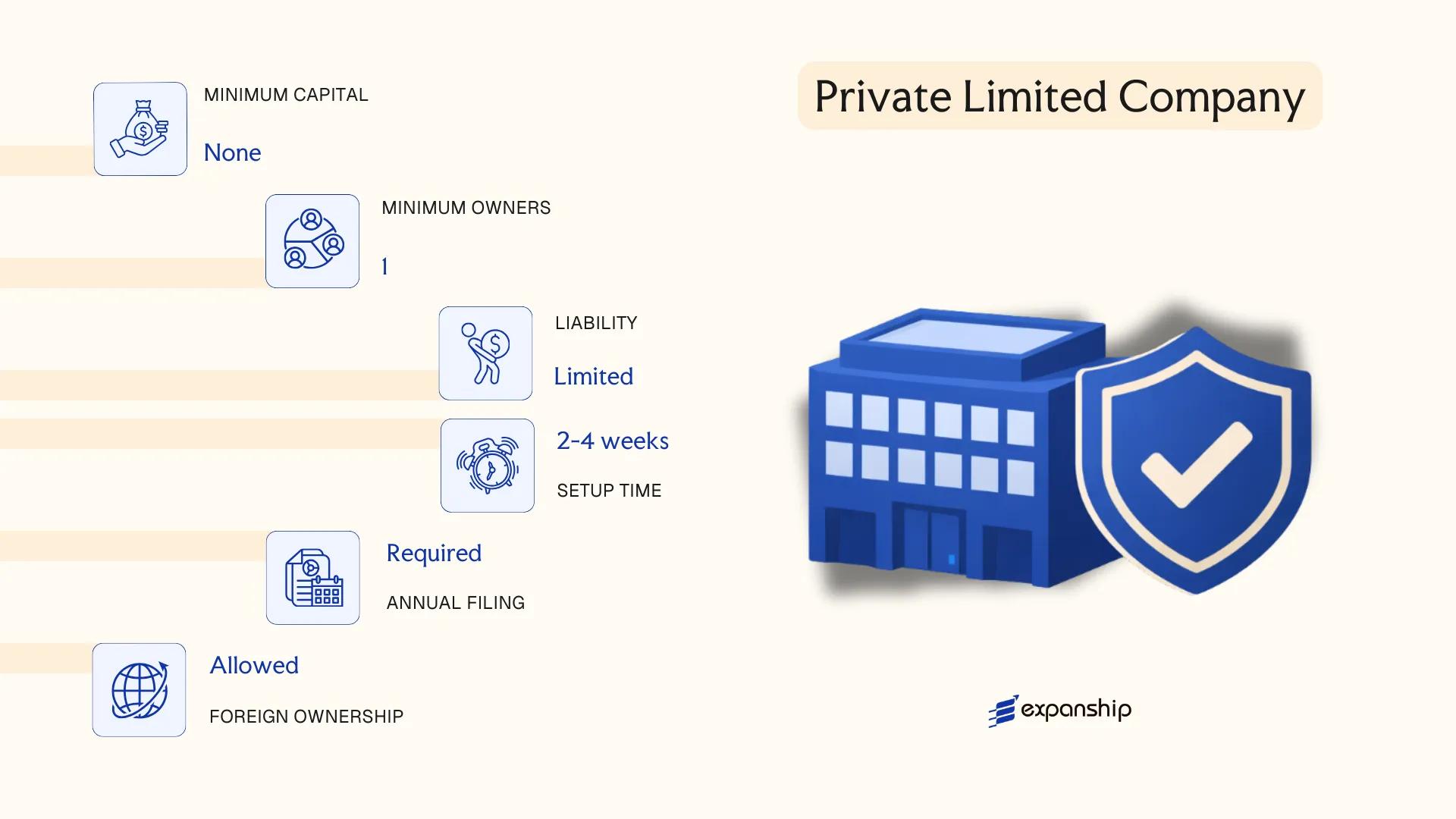

Société à Responsabilité Limitée (SARL) — Private Limited Company

The SARL French Polynesia private limited company structure is governed by the French commercial law framework, which applies to French Polynesia as a French overseas collectivity (collectivité d'outre-mer). The foundational rules derive from the French Code de commerce, adapted to local territorial conditions. Registration is handled through the Centre de Formalités des Entreprises (CFE) and recorded in the Registre du Commerce et des Sociétés (RCS) in Papeete.

As a hybrid structure, the SARL combines corporate limited liability with the operational flexibility typical of a partnership. Each associate's liability is capped at their capital contribution. The entity holds separate legal personality from the moment of registration.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société à Responsabilité Limitée | Separate legal personality upon RCS registration |

| Members | 1 to 100 associates (associés) | Single-member form is the EURL; managed by a gérant |

| Management | One or more gérants (managers) | Gérant need not be an associate; no board requirement |

| Capital | No statutory minimum (symbolic €1 possible) | Contributions in cash or kind; share transfers restricted |

| Local Presence | Registered office required in French Polynesia | Physical or legal address in Papeete or elsewhere in the territory |

| Privacy | Associate identities filed with RCS | Beneficial ownership disclosure applies under French AML rules |

Focus Points

- Taxation: Subject to Impôt sur les Sociétés (IS) at the territorial rate; VAT equivalent applies under local tax code; no separate withholding tax treaty network independent of France.

- Annual Compliance: Annual accounts must be filed; statutory audit required only above certain thresholds of turnover, headcount, or balance sheet size.

- Share Transfer Restrictions: Transfer of shares to third parties requires prior approval from associates holding at least half the share capital.

- Conversion: An SARL may be converted to an SA or SAS by shareholder decision, subject to meeting the relevant capital and governance thresholds.

- Economic Substance: No dedicated substance regime exists; standard territorial tax residency rules apply based on management and control.

Sub-Types

Entreprise Unipersonnelle à Responsabilité Limitée (EURL)

The EURL is the single-associate variant of the SARL. Structurally identical, it differs only in that one person holds all shares and typically serves as sole gérant, making it the standard vehicle for solo operators seeking limited liability without a multi-member structure.

The SARL suits small to medium trading operations, professional service firms, and family-held businesses where ownership control and restricted share transferability are priorities. Its principal constraint is the cap of 100 associates, which limits scalability for businesses anticipating broad equity participation.

The SARL is most appropriate for founders or small investor groups seeking limited liability with tight control over share transfers and a straightforward management structure.

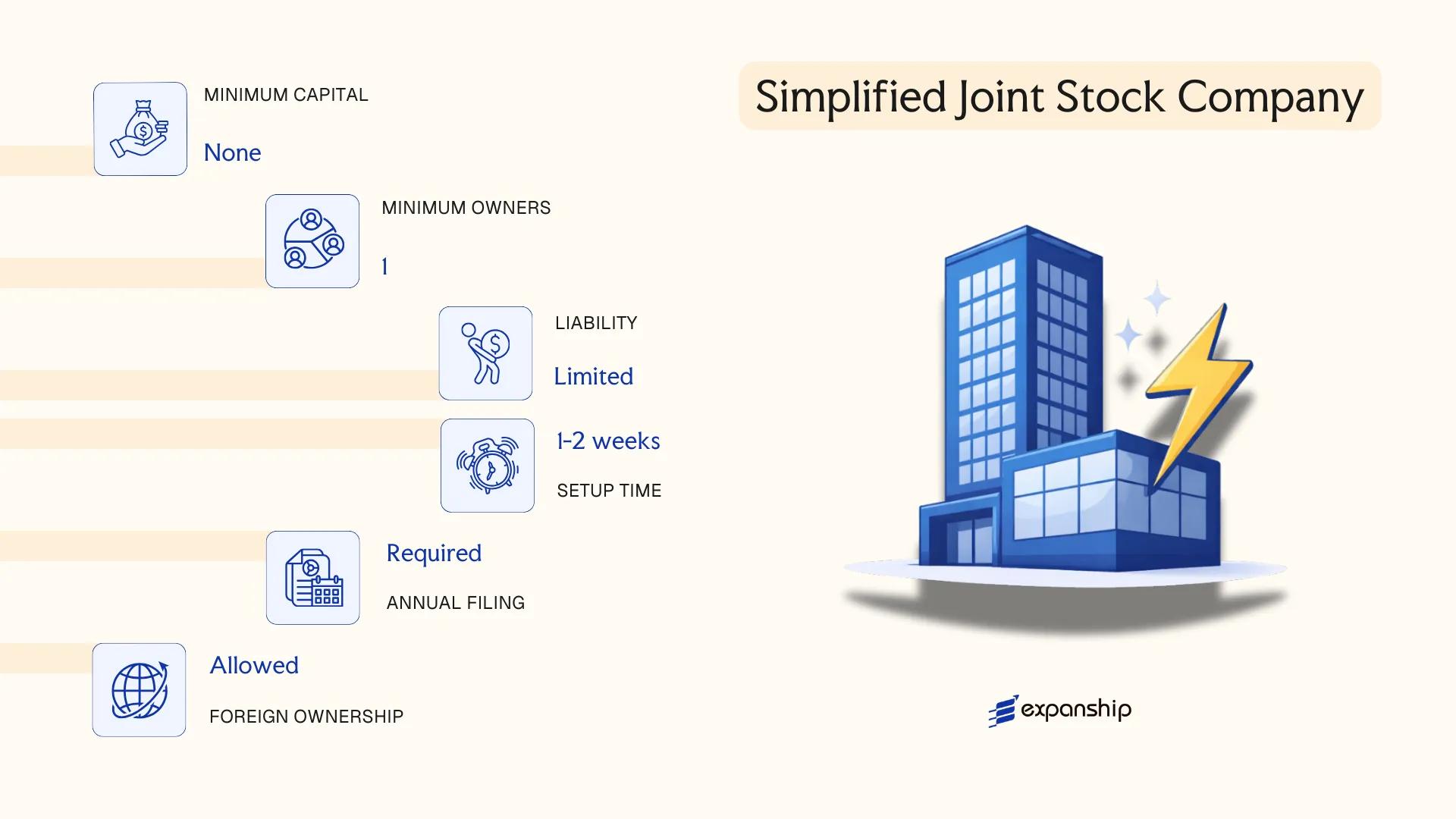

Société par Actions Simplifiée (SAS) — Simplified Joint Stock Company

The SAS company French Polynesia registration process is governed by the same legislative framework that applies across French overseas collectivities, drawing from the French Commercial Code as adapted under local territorial law. As a hybrid structure, the SAS combines the limited liability protections of a capital company with significant contractual freedom in governance, making it a distinct alternative to the SA.

Shareholders hold separate legal personality from the entity itself, meaning the firm can own assets, enter contracts, and incur obligations in its own name. Liability is confined to each shareholder's capital contribution.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Société par Actions Simplifiée | Hybrid capital company with contractual governance flexibility |

| Members | Shareholders; minimum 1, no maximum | Single-shareholder variant is the SASU |

| Management | President (mandatory); other officers optional | President can be an individual or a legal entity |

| Local Presence | Registered office in French Polynesia required | No statutory requirement for a local resident director |

| Share Capital | No legal minimum under general French commercial law | Statutes define the amount; shares are not publicly tradeable |

| Privacy | Shareholder identity disclosed in company statutes | Statutes filed with the Registre du Commerce et des Sociétés (RCS) |

Focus Points

- Taxation: Subject to Impôt sur les Sociétés (IS) at the standard territorial corporate rate; dividend distributions may attract withholding tax; VAT obligations apply based on activity type.

- Annual Compliance: Annual accounts must be filed with the RCS; a statutory auditor (commissaire aux comptes) is mandatory only above certain thresholds.

- Economic Substance: No specific economic substance regime comparable to common-law offshore jurisdictions applies, but the registered office must be genuinely maintained in the territory.

- Treaty Access: French Polynesia is not a party to France's tax treaty network in its own right; treaty access is limited and should be verified against the specific counterparty jurisdiction.

- Conversion: An SAS can generally be converted into an SA or SARL by shareholder resolution, subject to meeting the target structure's statutory requirements.

Closing

The SAS suits holding structures, joint ventures, and businesses requiring flexible shareholder arrangements without the formality of a public company. Its primary advantage is the degree of freedom afforded in drafting governance provisions within the statutes; the principal limitation is that shares cannot be offered to the public.

The SAS is most appropriate for investors and entrepreneurs seeking a contractually flexible corporate structure with limited liability, particularly for multi-party ventures or subsidiary arrangements under a larger group.

Partnerships [Société en Nom Collectif (SNC), Société en Commandite Simple (SCS), Société en Commandite par Actions (SCA)]

French Polynesia's partnership structures SNC SCS follow the same legislative foundation as metropolitan France, adapted through local statutes administered by the Direction des Affaires Économiques (DAE). Three distinct partnership forms are recognised: the Société en Nom Collectif (SNC), the Société en Commandite Simple (SCS), and the Société en Commandite par Actions (SCA). Each carries different liability profiles and governance structures, making the choice between them consequential rather than cosmetic.

All three forms possess separate legal personality upon registration with the Registre du Commerce et des Sociétés (RCS) in Papeete. Unlimited liability applies to at least one category of partner in each structure, which distinguishes partnerships from capital-based entities such as the SA or SARL.

Key Characteristics

| Requirement | SNC | SCS | SCA |

|---|---|---|---|

| Legal Form | General partnership | Limited partnership | Partnership limited by shares |

| Partners Referred To As | Associés (all general partners) | Associés commandités (general) / Associés commanditaires (limited) | Associés commandités (general) / Actionnaires (shareholders) |

| Minimum Members | 2 general partners | 1 general + 1 limited partner | 1 general partner + 3 shareholders |

| Liability | Unlimited, joint and several for all | Unlimited for commandités; limited to contribution for commanditaires | Unlimited for commandités; limited to share value for actionnaires |

| Share Capital | No statutory minimum | No statutory minimum | Minimum capital required (equivalent to SA thresholds) |

| Local Presence | Registered office in French Polynesia required | Registered office required | Registered office required |

| Privacy | Partner identities disclosed in RCS filings | Partner categories disclosed separately | Shareholder register maintained; general partners publicly identified |

Focus Points

- Taxation: Partnerships are generally treated as fiscally transparent under French Polynesian tax law; profits are taxed at the partner level, though specific local tax rates and impôt sur les sociétés applicability depend on the activity and partner status.

- Annual Compliance: Annual accounts must be filed with the RCS; SCA entities face additional reporting obligations comparable to those of an SA given their share-based structure.

- Economic Substance: No formal economic substance regime equivalent to certain Pacific territories applies, but commercial activity must be genuinely conducted from a registered local office.

- Conversion: An SNC may be converted to an SARL or SA through a formal amendment process registered with the RCS, subject to unanimous partner consent unless the articles provide otherwise.

- Restrictions: Foreign nationals acting as general partners (commandités) must comply with residency and professional licensing requirements enforced by the DAE.

Sub-Types

Société en Nom Collectif (SNC)

All partners hold unlimited, joint and several liability for company debts. This structure is typically used by professional firms or family-owned businesses where partners are willing to assume personal liability in exchange for full management participation.

Société en Commandite Simple (SCS)

The SCS splits partners into two classes: commandités bear unlimited liability and manage the business, while commanditaires contribute capital with liability capped at their investment and no management rights. This structure suits arrangements where passive investors fund an active operator.

Société en Commandite par Actions (SCA)

The SCA combines partnership governance with a share-based capital structure. Shares issued to actionnaires are transferable, making the SCA Société en Commandite par Actions useful for businesses seeking external capital while allowing commandités to retain operational control.

Closing

Partnership structures are used primarily by professional practices, family businesses, and investment vehicles where control concentration matters more than liability protection. The key advantage across all three forms is governance flexibility, particularly the SCA's ability to separate capital from control. The primary drawback is the unlimited personal liability carried by general partners, which creates material personal financial exposure.

SNC and SCS structures are best suited to closely held businesses or professional partnerships where all principals have an established working relationship and are prepared to assume personal liability.

Foreign Business Establishments [Branch Office, Representative Office]

A branch office French Polynesia foreign company structure does not constitute a separate legal entity — the parent company retains full liability for its operations. Registration is governed by the local commercial register (Registre du Commerce et des Sociétés, or RCS), administered under French law as extended to French Polynesia through territorial statutes. Unlike a locally incorporated firm, a branch has no independent legal personality.

Because French Polynesia is a French collectivité d'outre-mer, metropolitan French commercial law applies by extension, though certain territorial regulations may impose additional requirements on foreign business establishment French Polynesia activities.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Branch (succursale) — no separate legal personality | Parent bears all legal and financial liability |

| Representative | Appointed legal representative (mandataire) | Must be designated at RCS registration |

| Local Presence | Registered address in French Polynesia required | Physical office address; no resident agent system as in common law jurisdictions |

| Capital | No minimum capital requirement | Parent company's capital structure applies |

| Privacy | Parent company details publicly filed at RCS | Beneficial ownership visible through registration documents |

Focus Points

- Taxation: Subject to territorial income tax (impôt sur les bénéfices des sociétés) on locally sourced profits; VAT equivalent (taxe sur la valeur ajoutée, TVA) applies to transactions; withholding tax may apply to profit remittances to the parent.

- Annual Compliance: Annual accounts of the branch must be filed; parent company financial statements may also be required by the RCS.

- Treaty Access: France's tax treaty network does not automatically extend to French Polynesia; treaty benefits must be verified on a case-by-case basis.

- Restrictions: Certain regulated sectors require prior approval from territorial authorities before a foreign firm may operate.

Sub-Types

Branch Office (Succursale)

A succursale conducts full commercial operations and generates revenue in French Polynesia. It is taxed on locally derived profits and must register with the RCS before commencing activity.

Representative Office (Bureau de Représentation)

A representative office is limited to non-commercial activities such as market research, liaison, and promotion. It cannot conclude contracts or generate revenue directly; its scope is strictly preparatory or auxiliary.

Opening a branch suits foreign firms seeking direct market presence without incorporating a separate local entity. The primary advantage is operational continuity with the parent; the core limitation is unlimited parental liability exposure.

Best suited for established foreign companies testing the French Polynesian market or managing existing client relationships without committing to full local incorporation.

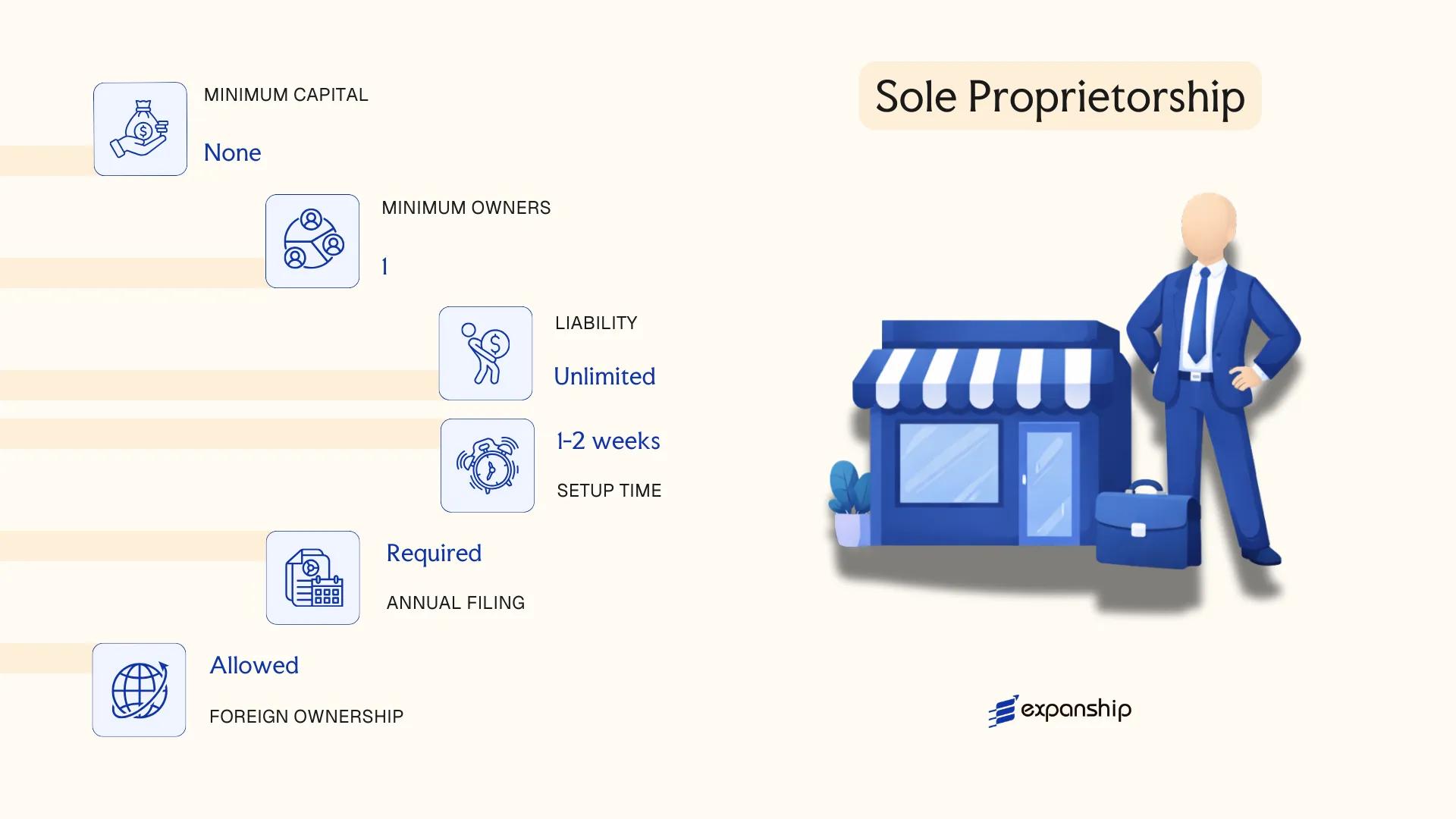

Sole Proprietorship [Entreprise Individuelle, Auto-Entrepreneur]

French Polynesia operates under French civil and commercial law, extended to the territory through its status as a Collectivité d'outre-mer. The sole proprietorship — Entreprise Individuelle (EI) — carries no separate legal personality; the proprietor and the business are legally identical, meaning personal assets remain exposed to professional liabilities. The simplified auto-entrepreneur regime, introduced in metropolitan France under the Loi de modernisation de l'économie (LME) of 2008 and subsequently adapted in French Polynesia, offers a reduced administrative framework for low-turnover self-employed activity.

Registration for both forms is handled through the Centre de Formalités des Entreprises (CFE), administered locally by the Chambre de Commerce, d'Industrie, des Services et des Métiers (CCISM) of French Polynesia.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Unincorporated sole proprietorship | No separate legal personality from the owner |

| Members | One proprietor | No shareholders; the owner operates in their own name |

| Local Presence | Registered business address required | Must be maintained within French Polynesia |

| Capital | No minimum capital requirement | No paid-up capital obligation |

| Liability | Unlimited personal liability | Professional and personal assets are jointly exposed |

| Privacy | Proprietor's identity publicly registered via CCISM | No confidentiality available |

Focus Points

- Taxation: Subject to the Impôt sur les Transactions (IT) for applicable turnover; income taxed under personal income tax (impôt sur le revenu) at the territorial level; the auto-entrepreneur regime applies simplified flat-rate contribution calculations based on gross receipts.

- Annual Compliance: Periodic turnover declarations required under the auto-entrepreneur regime; standard EI requires regular accounting submissions to tax authorities.

- Turnover Ceiling: The auto-entrepreneur status is subject to annual revenue thresholds set by local territorial regulations; exceeding these triggers reclassification to a standard EI or commercial company.

- Conversion: An EI can be converted into a SARL or SAS, though the process requires formal incorporation and asset transfer procedures.

- Treaty Access: As a Collectivité d'outre-mer, French Polynesia maintains a distinct fiscal regime; access to France's tax treaty network is not automatically extended.

Sub-Types

Entreprise Individuelle (EI)

The standard form for self-employed professionals and traders, requiring full accounting compliance and carrying unlimited personal liability without any revenue ceiling.

Auto-Entrepreneur (Micro-Entrepreneur)

A simplified variant capped at defined annual revenue thresholds, with fixed-rate social and tax contributions calculated on gross receipts, designed for occasional or small-scale commercial activity.

Both forms suit early-stage, single-operator businesses with limited capital exposure requirements. The principal advantage is minimal setup cost and administrative simplicity at launch; the clear limitation is the absence of liability protection, which exposes personal assets directly to business obligations.

Best suited for individual consultants, artisans, or small traders testing a local market before committing to a formal corporate structure.

How to Choose the Right Entity Type in French Polynesia

Choosing the right company structure in French Polynesia affects your tax position, liability exposure, regulatory obligations, and long-term operational flexibility in ways that are difficult to reverse after registration.

Why Your Entity Choice Matters

The structure you register has binding consequences.

- Selecting an entity without sufficient substance capacity when local economic presence rules apply can trigger reporting failures and associated financial penalties under applicable territorial tax provisions.

- Choosing a tax-exempt entity when your operations require access to France's tax treaty network means withholding tax reductions available under those treaties cannot be claimed by your entity.

- Registering a foreign branch when your business model requires full local trading rights may result in operating outside the permitted scope of that structure, exposing the firm to penalties or forced dissolution.

- Forming a capital company when your needs are primarily those of asset holding or succession planning creates annual shareholder and reporting obligations that a different structure might not impose.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors each correspond to distinct structures under French Polynesia's commercial law framework.

- Ownership and Management: A single founder may prefer the SARL for its simplified governance, while multi-party arrangements may require the formal board structure of an SA.

- Tax Objectives: Your eligibility for territorial tax regimes or treaty benefits depends directly on the entity type and its residency classification.

- Substance Capacity: If maintaining local employees, office space, and decision-making in the territory is not feasible, your entity selection must account for that constraint.

- Privacy Requirements: Disclosure obligations differ across structures; nominee arrangements may be required if shareholder confidentiality is a priority.

- Exit Strategy: Not all entity types permit redomiciliation or conversion, so your anticipated exit path should factor into the initial choice.

Compliance Services for Companies in French Polynesia

Maintain your entity's good standing with ongoing compliance support covering filings, reporting obligations, and regulatory requirements in French Polynesia.

Conclusion

Incorporating a company in French Polynesia means operating within a legal framework derived from French commercial law, adapted through local ordinances and administered by the Tribunal Mixte de Commerce de Papeete. Each entity form serves a distinct purpose: the SA suits larger enterprises requiring public capital access; the SARL remains the standard choice for small to mid-sized resident businesses; the SAS offers the greatest structural flexibility for investor-driven arrangements; the SNC and commandite forms address partnership structures with varied liability profiles; and branch or representative offices provide a path for foreign firms testing the market without local incorporation.

The SARL is the most commonly registered structure across the territory. French Polynesia's regulatory alignment with metropolitan French commercial standards continues to develop, and its status as a French collectivity gives it a degree of institutional credibility that informs how foreign counterparties and financial institutions assess locally incorporated entities. Expanship's team works directly with this regulatory environment on a regular basis.

How Expanship Can Assist You

Expanship's company formation services French Polynesia cover every structure examined in this guide — from the capital-intensive SA to the flexible SAS and the owner-managed SARL. Each entity type carries distinct filing requirements under the local commercial registry (Registre du Commerce et des Sociétés de Polynésie française), and our team handles those specifics directly.

From document preparation to post-registration obligations, our service scope includes:

- Preparation and legalization of constitutional documents

- Registered agent and registered office provision in Papeete

- Government filing and liaison with the RCS de Polynésie française

- Post-incorporation compliance management, including annual reporting

- Corporate bank account introduction assistance

Getting your entity registered correctly from the outset avoids costly corrections later. Reach out to Expanship French Polynesia to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

The Société à Responsabilité Limitée (SARL) is the most frequently registered structure. Its lower capital threshold and simplified governance make it accessible to small and medium-sized businesses without the administrative burden of a Société Anonyme.

Both structures permit local trading and are subject to corporate income tax under the same territorial tax framework administered by the Direction Générale des Impôts et des Contributions Publiques. The SA carries heavier ongoing obligations, including mandatory auditor appointment at lower thresholds and a minimum share capital of XPF 1,500,000, compared to XPF 100,000 for a SARL.

The Société par Actions Simplifiée (SAS) offers relatively greater confidentiality, as shareholder details are not always fully disclosed in publicly accessible registries. Nominee arrangements are legally permissible under French-derived corporate law applicable in the territory.

No. A Société en Nom Collectif (SNC) requires at least two partners, and the same applies to commandite structures. A SARL, SAS, or SA can each be formed by a single person, though the SA requires a minimum of seven shareholders.

Foreign nationals may incorporate a SARL, SAS, or SA without a local partner requirement, though certain regulated sectors may impose additional licensing conditions. Residency is not a general prerequisite for shareholding, but at least one director with adequate local administrative access is advisable for ongoing compliance with the Registre du Commerce et des Sociétés (RCS).

Conversion between structures such as SARL to SAS is generally recognised under French commercial law principles as applied in the territory, provided shareholder approval thresholds are met. Direct conversion from a partnership structure to a share-capital company involves greater procedural complexity and typically requires fresh RCS registration.

The SA, SARL, and SAS each hold distinct legal personality separate from their owners. General partnerships (SNC) and commandite structures also acquire legal personality upon registration, though partners in an SNC retain unlimited joint liability for the firm's obligations.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.