Key Takeaways

- French Polynesia's territorial tax framework, administered under local fiscal rules rather than France's worldwide income regime, means a locally registered SAS or SARL is taxed only on income generated within the collectivity, directly limiting the cross-border tax exposure of foreign shareholders.

- Because the territory imposes no exchange controls on outbound capital, businesses incorporated in French Polynesia can repatriate dividends and profits to foreign parent entities without regulatory clearance or conversion restrictions.

- IP assets held through a French Polynesia entity benefit from protections enforceable under the French Commercial Code, giving rights-holders access to a mature civil law system that most competing Pacific jurisdictions cannot offer.

- The Registre du Commerce et des Sociétés in Papeete oversees incorporation of SAS structures that permit foreign majority ownership, removing the equity cap restrictions that constrain foreign investors in several alternative Pacific jurisdictions.

French Polynesia is an overseas collectivity of France, situated in the South Pacific Ocean roughly midway between California and Australia. This political status means the territory operates under French constitutional law while retaining a degree of local legislative autonomy through its own assembly, the Assemblée de la Polynésie française. Company registration falls under the oversight of the Registre du Commerce et des Sociétés (RCS) of Papeete, which administers the incorporation process for entities formed within the territory. Foreign businesses most commonly establish a Société par Actions Simplifiée (SAS) when entering the market.

The benefits of incorporating in French Polynesia draw partly from a territorial tax framework that applies local rates to income generated within the collectivity rather than worldwide earnings. Foreign ownership of locally registered companies is generally permitted, and the territory maintains an open posture toward foreign direct investment across multiple sectors. This article examines the principal advantages that French Polynesia company formation offers to businesses considering this jurisdiction for their regional or international operations.

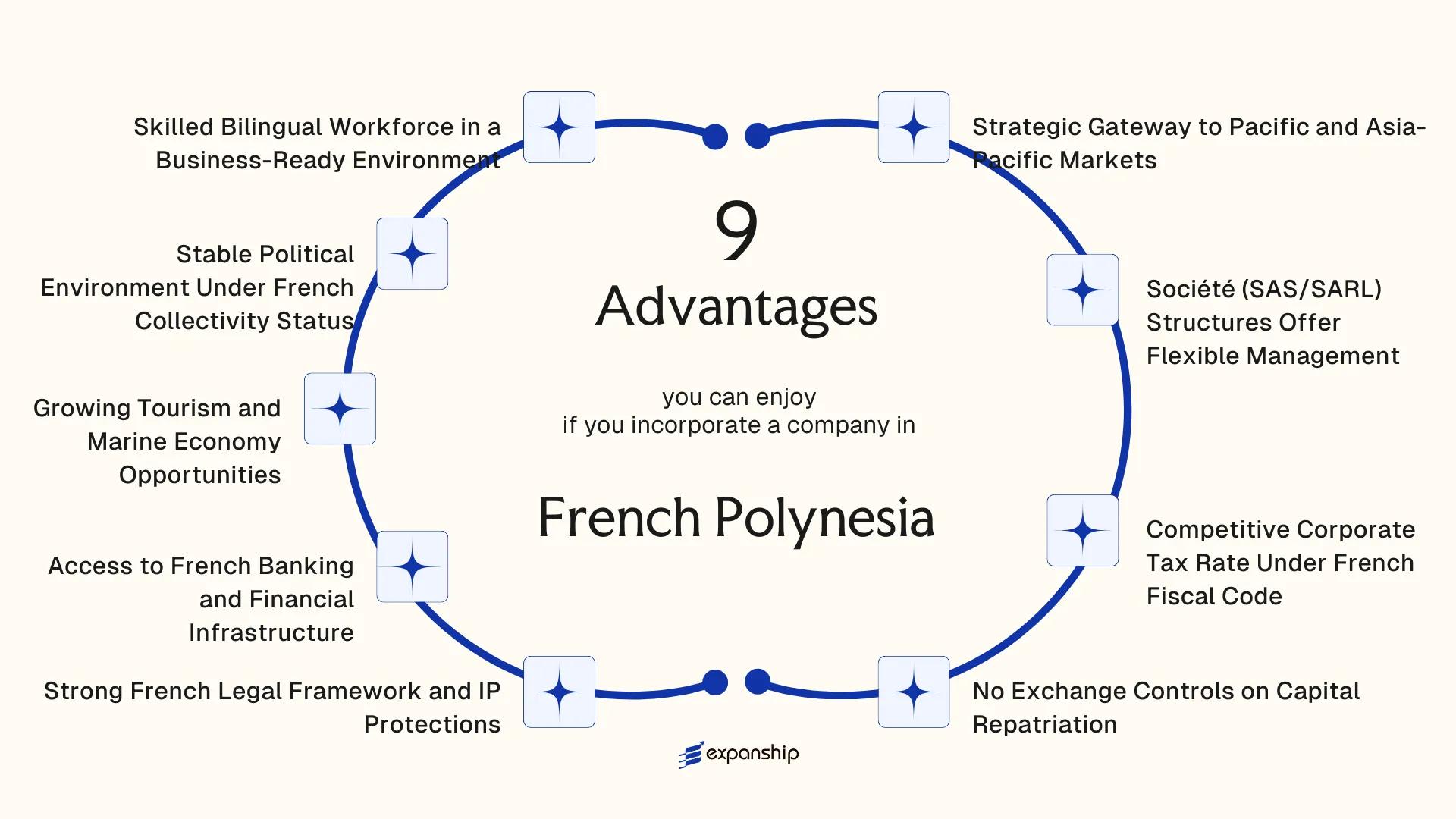

Strategic Gateway to Pacific and Asia-Pacific Markets

French Polynesia's geographic position places it within the Pacific basin, roughly equidistant between the Americas and Asia-Pacific trade corridors. For a business seeking French Polynesia Pacific market access advantages, this location provides tangible logistical and commercial reach that landlocked or single-region jurisdictions cannot replicate.

Position Within Pacific Trade Networks

Papeete, the territorial capital, functions as a significant maritime and air transit hub for the South Pacific. Air Tahiti Nui and international carriers maintain direct routes connecting the territory to Los Angeles, Auckland, and Tokyo, giving a company registered here direct access to multiple regional economic zones from a single base.

French Collectivity Status as a Commercial Bridge

As a French collectivity, the territory maintains regulatory alignment with French law while operating outside the EU customs territory. This means your entity can engage with both Francophone Pacific partners and Asia-Pacific counterparts without the full weight of EU trade restrictions applying to external commercial relationships.

Businesses oriented toward Pacific Island nations, French overseas territories, or markets across Southeast Asia can use a local entity to establish regional credibility backed by French institutional standards.

Your entity operates under a recognized French legal framework while maintaining commercial flexibility outside EU customs boundaries across Pacific trade routes.

Société (SAS/SARL) Structures Offer Flexible Management

Both the SAS (Société par Actions Simplifiée) and the SARL (Société à Responsabilité Limitée) are available to foreign investors incorporating in French Polynesia, and each carries structural advantages that directly affect how you govern and operate your business.

The SAS is particularly useful when governance flexibility matters. Its constitutive documents, the statuts, can define decision-making powers, share transfer conditions, and management appointment procedures in ways that standard civil codes would otherwise restrict. This means you can tailor shareholder voting thresholds and management authority to reflect your actual ownership arrangement rather than defaulting to rigid statutory defaults.

The SARL suits smaller or closely held operations. It imposes a defined management structure through a gérant, which provides clarity on authority without requiring a full board apparatus.

French Polynesia SAS SARL flexible management benefits are most visible in how these forms handle foreign shareholding. Neither structure mandates local directors as a statutory requirement, which reduces operational overhead for foreign-owned entities.

Relevant practical advantages include:

- Share capital requirements are low relative to the liability protection offered

- Statuts can be drafted in French without requiring local notarial certification for all amendments

- The gérant or president can be a non-resident legal person, not just an individual

Local corporate law derives from French metropolitan commercial law as extended to the territory, giving these structures a well-documented legal foundation.

Incorporate a Company in French Polynesia

Set up an SAS or SARL in French Polynesia with full compliance support across registration, statuts drafting, and ongoing corporate maintenance.

Competitive Corporate Tax Rate Under French Fiscal Code

French Polynesia corporate tax rate advantages stem from a fiscal structure that diverges meaningfully from metropolitan France. As an overseas collectivity, the territory administers its own tax code rather than applying French national taxation directly. Corporate income tax is levied locally under the Code des impôts de la Polynésie française, at a standard rate of 25% for most companies, with reduced rates applying to qualifying smaller entities.

| Entity Type | Applicable Rate | Basis |

|---|---|---|

| Standard companies | 25% | Net taxable profit |

| Small/medium enterprises (qualifying) | Reduced rate | Profit thresholds set by local tax code |

| Approved investment regime | Partial exemption | Subject to Direction des impôts approval |

For a foreign-owned entity, operating under the Code des impôts rather than the French general tax code means exposure to a self-contained regime administered by the Direction des impôts de la Polynésie française. This creates a degree of fiscal autonomy that allows your business to plan around rules specific to the territory rather than navigating the full complexity of metropolitan French fiscal law.

Approved investment projects can access partial tax exemptions under the local investment incentive framework, which the Direction des impôts oversees through a formal application process. Eligibility is tied to specific sectors and investment thresholds, so the benefit is conditional rather than automatic. That said, where a firm qualifies, the effective tax burden can fall substantially below the headline rate, which carries direct implications for after-tax returns on invested capital.

No Exchange Controls on Capital Repatriation

French Polynesia no capital repatriation restrictions stem directly from its status as a French collectivity. France abolished exchange controls in 1990 under the framework of European financial liberalisation, and that regime extends to this territory. As a result, there are no administrative authorisations required to transfer profits, dividends, or capital proceeds abroad.

For a foreign business owner, this means your returns are not locked within the territory. Capital invested can be withdrawn, and profits distributed to shareholders can be remitted internationally without regulatory interference or mandatory conversion requirements.

Transfers operate within the French franc CFP (XPF) zone, which is pegged at a fixed rate to the euro. That fixed peg eliminates currency conversion volatility between the local franc and the euro, giving your treasury operations a degree of predictability absent in freely floating Pacific currencies.

Under French monetary law, cross-border capital movements must still be declared to the Banque de France for statistical purposes when they exceed certain thresholds, but this is a reporting obligation, not a restriction.

Keep the following in mind:

- No prior approval needed to repatriate profits or dividends

- Declarations to Banque de France required above statutory thresholds

- XPF is pegged to EUR, removing bilateral conversion risk

- Verify current declaration thresholds with your financial institution before each transfer

Because XPF is pegged to the euro under a guaranteed convertibility arrangement overseen by the French Treasury, your capital exits the territory at a fixed rate — a feature more common to eurozone members than Pacific island jurisdictions.

Strong French Legal Framework and IP Protections

French Polynesia's French legal framework business benefits stem directly from its status as a collectivity of the French Republic. French civil law, including the Code civil and the Code de commerce, applies locally, giving your business a well-documented, predictable legal foundation that has been tested across centuries of commercial jurisprudence.

Civil Law Predictability for Commercial Operations

Contracts, corporate governance obligations, and dispute resolution procedures all operate under French law principles. Because the legal system mirrors metropolitan France in its core structure, foreign firms familiar with civil law traditions face minimal uncertainty when establishing obligations, enforcing agreements, or managing shareholder arrangements.

French courts apply consistent interpretive standards derived from the same body of law used across France's domestic territory, which reduces jurisdictional ambiguity for cross-border transactions.

IP Rights Under French and International Frameworks

Intellectual property protection advantages are substantial here because the Institut National de la Propriété Industrielle (INPI) framework extends to French Polynesia, covering trademarks, patents, and designs registered through French procedures. Registration through INPI grants enforceable rights that align with France's obligations under the Paris Convention and the TRIPS Agreement.

For a business holding proprietary technology, brand assets, or creative works, this means your IP rights sit within a legally enforceable structure backed by international treaty commitments. French civil law protections for companies also cover trade secrets and software under the same framework as continental France, without requiring a separate local registration process.

Structure Your Business Around French Polynesia's Legal Advantages

Speak with an Expanship specialist about how French civil law protections and IP frameworks apply to your specific business activities in French Polynesia.

Access to French Banking and Financial Infrastructure

Companies registered in French Polynesia gain access to French banking and financial infrastructure benefits for businesses that most Pacific Island jurisdictions cannot offer. Because the territory operates under French monetary sovereignty, local entities transact in euros, hold accounts with French metropolitan banks operating branches in Papeete, and access payment clearing systems tied to the Banque de France. That connection carries practical weight for any firm conducting cross-border business.

- Accounts held through French-affiliated banks are subject to French prudential supervision under the Autorité de Contrôle Prudentiel et de Résolution (ACPR), giving counterparties in Europe and North America a familiar regulatory reference point when assessing your company's banking relationships.

- The CFP franc (XPF), used locally alongside euro-denominated transactions, is pegged to the euro at a fixed rate, eliminating currency conversion risk on intra-French financial flows.

- Trade finance, letters of credit, and corporate lending products available through banks such as Banque de Polynésie and Banque Socredo operate under French commercial banking standards, which are accepted across the SEPA zone.

- A company incorporated here can open correspondent banking relationships with French metropolitan institutions more readily than an entity registered in a non-French Pacific territory, reducing friction when receiving payments from European clients or suppliers.

Growing Tourism and Marine Economy Opportunities

Tourism accounts for approximately 70% of French Polynesia's GDP, making it one of the most concentrated tourism-dependent economies in the Pacific. For foreign investors, this concentration signals a mature, institutionally supported sector where demand for ancillary services — hospitality technology, marine logistics, dive operations, and eco-tourism infrastructure — consistently outpaces local supply.

The territory's blue economy framework, which falls under France's broader maritime policy obligations, creates structured pathways for businesses in aquaculture, pearl farming, and deep-sea resource management. The black pearl industry, regulated under local territorial statutes, remains a significant commercial sector with established export channels through French customs protocols.

Visitor arrivals are predominantly long-haul, high-spending travelers from North America, Europe, and increasingly Northeast Asia. Your business benefits from a captive premium market without the low-margin, high-volume pressures that affect more mass-market destinations.

A foreign-owned SAS operating a marine tourism concession in Bora Bora with annual revenues of 50 million XPF would calculate corporate tax liability under the French Polynesian tax code administered by the Direction Générale des Impôts et des Douanes (DGID), with applicable sectoral incentives potentially reducing the effective rate below the standard territorial rate for qualifying tourism investments.

Stable Political Environment Under French Collectivity Status

French Polynesia political stability collectivity status benefits stem directly from its constitutional relationship with France. Under the Organic Law of 27 February 2004, the territory operates as an overseas collectivity (collectivité d'outremer) with substantial internal autonomy while remaining subject to French constitutional principles and French state authority over defense, foreign affairs, and public order.

This arrangement produces a governance structure that is materially different from fully independent Pacific island states. The French Republic's institutional oversight means your business operates under a legal and political baseline anchored in a G7-level sovereign state, reducing exposure to the abrupt regulatory shifts or currency crises that can affect independent jurisdictions in the region.

Local governance is handled by the Assemblée de la Polynésie française and the President of French Polynesia, who hold authority over economic policy, taxation, and commercial law within the collectivity. This division of powers is codified, not informal, which means the scope of local legislative authority is legally bounded and predictable.

- Political transitions at the local level do not alter French constitutional protections

- Property rights and contract enforcement remain anchored to French legal norms

- Investor disputes can escalate through French judicial channels when applicable

Local tax and commercial regulations are set by the Assemblée de la Polynésie française, not metropolitan France, so you must verify that any French fiscal provision you rely on is explicitly applicable within the collectivity's own legal code.

Skilled Bilingual Workforce in a Business-Ready Environment

French Polynesia bilingual workforce advantages for business are grounded in a structural linguistic reality: French is the official administrative and commercial language, while Tahitian holds co-official status, and English proficiency is widespread across the tourism, finance, and professional services sectors. For a foreign-owned entity, this means operational communication with French metropolitan institutions, local government bodies, and Pacific trading partners does not require intermediary translation layers.

The territory's education system follows the French national curriculum, administered under the Direction Générale de l'Education et des Formations (DGEE). Graduates enter the labor market with qualifications aligned to metropolitan French standards, which are recognized across EU member states and French overseas territories. This portability gives your firm access to a talent pool whose credentials carry cross-border credibility.

Local professional training is supported by institutions such as the Université de la Polynésie Française (UPF), which offers programs in law, economics, and management directly applicable to corporate operations. Hiring locally qualified staff means reduced onboarding friction for roles requiring familiarity with French civil law procedures and the local regulatory environment.

Key labor characteristics relevant to business incorporation and staffing:

- Employment contracts are governed by the Code du travail polynésien, a locally adapted version of the French Labor Code

- Social contributions are administered through the Caisse de Prévoyance Sociale (CPS)

- Minimum wage rates are set locally under the SMIG polynésien, distinct from the metropolitan SMIC

For companies requiring Pacific-facing operations, staff fluency across French, English, and Tahitian reduces the cost of multilingual customer service infrastructure.

Why French Polynesia Stands Out Against Rival Jurisdictions

Assessing French Polynesia against competing Pacific incorporation destinations reveals a specific competitive profile. The territories most relevant to compare are New Caledonia, Vanuatu, and Fiji, each attracting foreign investors pursuing Pacific market access, tourism-linked businesses, or offshore-adjacent structuring. These three jurisdictions share geographic proximity and a partially overlapping investor audience, making the comparison substantive rather than theoretical.

What the comparison shows is that French Polynesia's French legal underpinning, combined with EU-aligned banking standards, places it in a distinct regulatory tier relative to Vanuatu's lighter-touch offshore environment or Fiji's common law framework. For businesses where counterparty confidence and banking access matter, operating under the Code de Commerce and IEOM oversight carries weight that purely offshore structures in Vanuatu cannot replicate. New Caledonia presents a closer structural parallel, but its ongoing political uncertainty around independence referendums introduces a governance risk absent in French Polynesia's more settled collectivity status.

| Parameter | French Polynesia | Vanuatu | Fiji | New Caledonia |

|---|---|---|---|---|

| Legal framework | French civil law (Code de Commerce) | Mixed/offshore statute | English common law | French civil law |

| Currency stability | CFP Franc, pegged to EUR | Vanuatu Vatu (floating) | Fijian Dollar (floating) | CFP Franc, pegged to EUR |

| Banking supervision | IEOM (Institut d'Émission d'Outre-Mer) | Vanuatu Financial Services Commission | Reserve Bank of Fiji | IEOM |

| IP protection | French IP law + WIPO treaties | Limited domestic IP regime | Domestic IP law, WIPO member | French IP law + WIPO treaties |

| Political stability | French collectivity, settled governance | Independent republic, stable | Independent republic, generally stable | Active independence dispute |

| EU regulatory alignment | Yes, French fiscal code applicable | No | No | Yes |

Compliance Services for Companies in French Polynesia

Maintain your company's good standing under French Polynesian regulatory requirements, from annual filings to ongoing statutory obligations.

Conclusion

French Polynesia's position as a French collectivity gives incorporated entities access to a civil law framework derived from the French Commercial Code, capital repatriation without exchange controls, and banking infrastructure connected to metropolitan French institutions. These are structural features that few Pacific jurisdictions can replicate, and they directly reduce the legal and financial friction that foreign business owners typically face when operating across borders.

For businesses with genuine exposure to the Pacific economy, the benefits of incorporating in French Polynesia are tied to specific, verifiable conditions: no withholding tax on outbound dividends under certain configurations, SAS and SARL structures that allow foreign majority ownership, and IP protections enforceable under French law. Each of these factors has a direct bearing on how a foreign firm holds assets, distributes profits, and manages risk.

Whether a particular structure fits your situation depends on your industry, the volume of cross-border transactions you anticipate, and how your entity interacts with existing group structures or tax residency positions. French Polynesia company formation advantages are most material for businesses in maritime commerce, tourism infrastructure, or regional Pacific trade. The next step is translating the jurisdiction's structural features into a formation and compliance plan that reflects your specific circumstances.

Let Expanship Handle Your French Polynesia Company Formation

Expanship's French Polynesia company formation services cover the full scope of what foreign investors encounter when establishing an entity under the territory's regulatory framework — from structuring a Société par Actions Simplifiée (SAS) or Société à Responsabilité Limitée (SARL) to meeting ongoing compliance obligations administered through the Tribunal Mixte de Commerce and local registry authorities. Each step in this blog reflects a real procedural or legal requirement, and Expanship's role is to manage those requirements on your behalf.

Our service scope includes the following:

- Document preparation, notarization, and legalization for submission to local authorities

- Registered agent and registered office provision within the territory

- Government filing and liaison with the relevant commercial registry

- Post-incorporation compliance management, including annual reporting obligations

- Director and shareholder record maintenance under applicable French collectivity rules

- Banking introduction assistance to support account opening with institutions operating in Papeete

Expanship coordinates directly with the applicable registry and administrative bodies so that your entity is formed in accordance with the rules of the territoire rather than approximated against mainland French procedures, which differ in material respects.

Reach out through Expanship French Polynesia to discuss your formation requirements with a specialist.

Frequently Asked Questions (FAQ)

French Polynesia operates under a distinct fiscal regime separate from metropolitan France, with corporate tax administered locally rather than under the standard French Code général des impôts. The territory applies its own impôt sur les sociétés, with rates that differ from mainland French rates. Investors should verify the applicable rate and any sectoral exemptions directly with the Direction générale des impôts of French Polynesia, as rates and thresholds are subject to periodic revision by the Assemblée de la Polynésie française.

Registration timelines vary based on document completeness and the workload at the Registre du Commerce et des Sociétés (RCS) in Papeete, which handles commercial entity registration. In straightforward cases, the process can be completed within a few weeks from the date of submission of all required documents. Delays are common when notarized or apostilled foreign documents require translation into French before filing.

French Polynesian corporate law does not impose a blanket requirement for a locally resident gérant in an SARL, though the gérant must be reachable for official correspondence within the jurisdiction. If the gérant is a foreign national residing outside French Polynesia, additional compliance obligations may arise, particularly around professional licensing if the company intends to conduct regulated activities. The specific requirements depend on the business sector and the nature of the activity being registered.

As an overseas collectivity under Article 74 of the French Constitution, French Polynesia has its own institutional competence over many civil and commercial matters, though French civil law principles, including those governing contractual obligations, generally apply. Contracts governed by local law benefit from a legal framework derived from the French civil tradition, making dispute resolution predictable for counterparties familiar with that system. Judgments from French Polynesian courts can be enforced through established civil procedure mechanisms aligned with broader French legal standards.

No exchange controls restrict the transfer of dividends or capital from French Polynesia to foreign shareholders. The territory is part of the franc pacifique (XPF) zone, and transfers to accounts held in euros or other currencies are generally conducted through the standard international banking system without regulatory approval requirements. Withholding tax obligations on dividend distributions to non-resident shareholders should be confirmed against the applicable local tax rules administered by the Direction générale des impôts.

Intellectual property rights in French Polynesia are governed under the framework of French IP law, with the Institut National de la Propriété Industrielle (INPI) covering trademark and patent registrations that extend to French overseas territories and collectivities. This means a trademark registered through INPI in France can provide coverage in French Polynesia without a separate local filing. Copyright protections similarly follow French legal standards, offering a level of IP security consistent with one of the more established civil law systems globally.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.