Key Takeaways

- French Polynesia's dual-layer governance — combining metropolitan French law under the Code de commerce with territorial ordinances from the Assembly of French Polynesia — creates overlapping compliance obligations that require monitoring two distinct legislative sources simultaneously.

- Foreign investors in sectors such as land development and fishing face ownership restrictions imposed at the territorial level, limiting the degree of control a non-resident entity can exercise over its French Polynesian operations.

- Operating costs in French Polynesia are structurally elevated due to the territory's geographic remoteness in the South Pacific, which inflates logistics, supply chain, and staffing expenses relative to most continental or near-shore jurisdictions.

- Businesses incorporated in French Polynesia must navigate French fiscal law alongside locally adapted tax provisions, producing a complex obligations framework that cannot be managed solely by reference to standard metropolitan French tax rules.

French Polynesia operates under a heavily regulated corporate environment, shaped by its status as a French overseas collectivity with substantial local autonomy. Understanding the disadvantages of incorporating in French Polynesia requires examining how that dual-layer governance — both territorial and metropolitan — creates compliance obligations that many foreign investors underestimate.

The drawbacks of company formation in French Polynesia span fiscal, structural, operational, and market-access dimensions, each addressed in the sections that follow.

Not all disadvantages apply equally. A small e-commerce firm faces different constraints than a foreign-owned entity seeking to operate in regulated sectors like land development or fishing.

The primary legal reference for commercial activity is the Code de commerce as applied through local adaptation. Territorial ordinances issued by the Assembly of French Polynesia can modify how certain provisions apply locally.

This article is most relevant to non-resident foreign investors and multinational firms evaluating French Polynesia as a base for Pacific regional operations or sector-specific business entry.

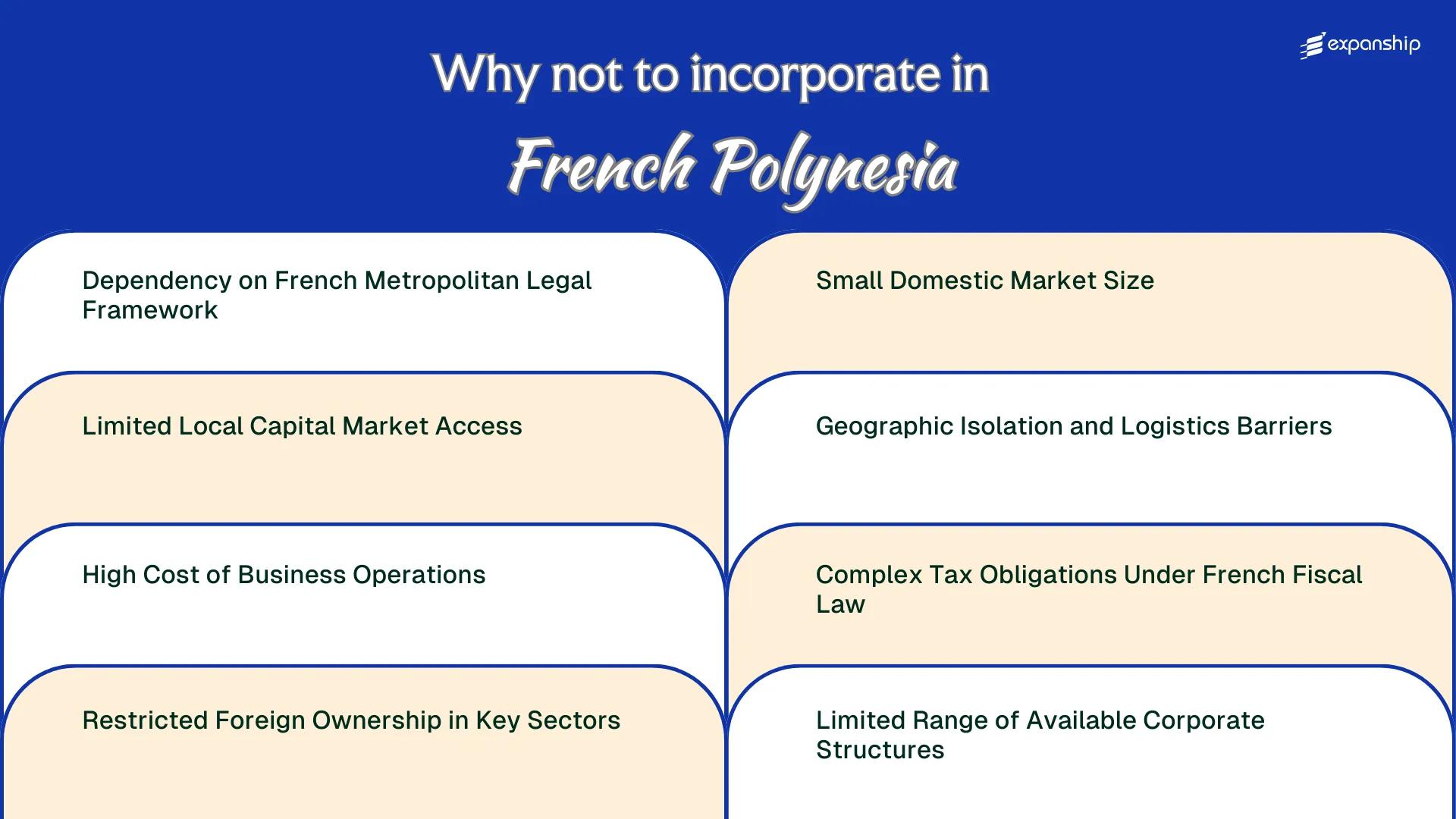

Dependency on French Metropolitan Legal Framework

Incorporating a business in French Polynesia exposes you to the French Polynesia French legal framework challenges that stem from its status as a collectivity under French constitutional law. The territory operates under a dual-layer legal structure where French metropolitan law applies alongside local statutes enacted by the Assemblée de la Polynésie française.

Metropolitan Law as the Governing Default

French civil law, particularly the Code de commerce and the Code civil, forms the baseline for corporate governance, contract enforcement, and liability. Where local legislation is silent, metropolitan French law fills the gap automatically, which means your compliance obligations extend well beyond what local authorities publish or enforce directly.

Compliance Burden Imposed on Foreign Entities

The French metropolitan law restrictions French Polynesia imposes through this layered structure require foreign businesses to track regulatory changes in both Papeete and Paris simultaneously. A rule amended by the French legislature can affect your entity's obligations in the territory without any formal local notification process alerting you to the change.

Foreign business owners must monitor French metropolitan legislative updates independently, as changes to the Code de commerce apply in French Polynesia without a separate local implementation notice.

Limited Local Capital Market Access

French Polynesia limited capital market access is a structural constraint that directly affects how your business can raise growth capital. The territory has no local stock exchange, which means equity financing through public listings is not available within the jurisdiction itself.

Companies seeking capital must turn to mainland France or international markets, both of which impose listing requirements, regulatory oversight from the Autorité des marchés financiers (AMF), and compliance costs that are disproportionate for small territorial entities.

Debt financing through local banks is available but limited in depth. The local banking sector, dominated by a small number of institutions, does not offer the credit volume or product variety that comparable businesses in metropolitan France or larger Pacific economies can access.

For a foreign-owned business, these constraints translate into specific operational friction:

- Raising equity capital requires engaging AMF-regulated structures, adding legal and filing costs that smaller firms cannot easily absorb.

- Local bank lending is often tied to territorial asset collateral, which a newly established foreign entity typically lacks.

- Venture capital and private equity activity within the territory is minimal, leaving growth-stage firms without accessible institutional investors.

Businesses structured as a Société par Actions Simplifiée (SAS) can issue shares privately, but private placement depth in the territory remains thin.

Company Incorporation in French Polynesia

Understand the corporate structures and regulatory requirements for establishing a business entity in French Polynesia.

High Cost of Business Operations

The high cost of business operations in French Polynesia is one of the most immediate financial pressures you will encounter as a foreign investor. The territory's price level is among the highest in the Pacific, driven by its near-total dependence on imported goods, energy, and materials.

Labor costs compound this pressure significantly. French Polynesia applies a local minimum wage, the SMIG (Salaire Minimum Interprofessionnel Garanti), set by the territorial government and adjusted periodically. Beyond base wages, employer social contributions under the Caisse de Prévoyance Sociale (CPS) add a substantial layer to your total payroll cost.

| Cost Factor | Approximate Burden | Implication |

|---|---|---|

| Employer CPS social contributions | Up to ~35% on top of gross salary | Significantly raises total labor cost per employee |

| Energy costs | Among highest in Pacific region | Elevated overhead for any production or office operation |

| Import duties on goods | Variable; applied under territorial customs code | Increases cost of any imported equipment or materials |

| SMIG minimum wage | Set above many comparable Pacific territories | Limits ability to hire at competitive regional rates |

Expensive business setup in French Polynesia extends beyond initial incorporation fees. Ongoing operational costs, including commercial lease rates in Papeete and utility expenses, consistently exceed what comparable firms pay in metropolitan France.

For firms relying on imported inputs, the French Polynesia customs regime adds further cost at the border. This applies even to equipment purchased from mainland France, as the territory operates a distinct customs zone under its organic statute.

Restricted Foreign Ownership in Key Sectors

Foreign ownership restrictions in French Polynesia apply most significantly in sectors tied to land use, natural resources, and culturally sensitive industries. The territory operates under a dual-layer regulatory system where both French metropolitan law and locally enacted statutes govern foreign participation, and the two do not always align cleanly.

Land ownership is the most direct constraint. Non-residents and foreign-controlled entities face structural barriers to acquiring freehold land, with local customary land tenure adding a further layer of restriction that sits outside standard civil law property frameworks.

Tourism infrastructure, fishing rights, and pearl farming — industries central to the local economy — carry sector-specific licensing requirements administered under Polynesian territorial authority. Foreign investors must obtain prior approvals that are not automatic and can be conditioned on local partnership arrangements.

- Foreign entities cannot assume freehold land acquisition rights equivalent to those held by residents

- Sector licenses in fishing and aquaculture are subject to territorial authority review under local statutes

- Joint venture or local partner requirements may be imposed as a condition of licensing approval

- Pearl farming operations fall under specific territorial regulations that restrict foreign-controlled management structures

French Polynesia's pearl farming sector, one of its most internationally recognized industries, is among the most tightly controlled for foreign participation despite having virtually no equivalent domestic regulatory model elsewhere in the Pacific.

Small Domestic Market Size

French Polynesia small domestic market limitations present a structural ceiling that most businesses encounter quickly after incorporation. The territory's population sits at approximately 280,000 people, concentrated primarily across Tahiti and a handful of other islands.

Scale Constraints on Revenue Potential

Consumer purchasing power is unevenly distributed across the archipelago, with outer island residents facing higher costs and lower incomes than those in Papeete. For a foreign-owned entity targeting local sales, that addressable base translates into a ceiling on domestic revenue that most market-entry models will struggle to justify against setup and operating costs.

Retail and service sectors are particularly exposed to this limitation. A firm that depends on volume-driven margins will find the limited consumer market in French Polynesia incompatible with standard international business models built around scale.

Structural Dependency on Export-Oriented Revenue

Viable businesses in the territory typically rely on exports or tourism spend rather than local consumption, which shifts operational complexity significantly. Your firm must then account for international logistics, foreign buyer relationships, and currency exposure that a domestic-only business would not face.

This dependency is not a matter of strategy preference. It reflects a structural reality: the small population drawbacks for any French Polynesia incorporation mean that domestic demand alone cannot underwrite a commercially sustainable operation for most sectors.

Assessing Market Viability Before You Incorporate in French Polynesia

Speak with our team about the commercial and structural realities of operating in French Polynesia before committing to incorporation.

Geographic Isolation and Logistics Barriers

French Polynesia's geographic isolation business problems are structural, not incidental — the territory's 118 islands span an area roughly the size of Western Europe, yet most are separated by vast stretches of the Pacific Ocean. Supply chain challenges for companies operating here are embedded in the physical geography itself.

- Inter-island freight between the archipelagos (Society, Tuamotu, Marquesas, Australes) depends on a limited number of cargo vessels and small aircraft, meaning your restocking cycles are longer and less predictable than in continental markets.

- All international cargo transits primarily through Papeete's Tahiti-Faaa airport or Papeete Port, creating a single-point bottleneck that amplifies delays from weather events or labor disruptions.

- The remote location risks for business inventory management are compounded by the fact that air freight to metropolitan France takes roughly 20+ hours of travel distance, pushing import lead times well beyond what most continental distribution networks require.

- Cold chain and perishable goods logistics face acute constraints given limited refrigerated storage infrastructure outside Tahiti.

Complex Tax Obligations Under French Fiscal Law

French Polynesia tax obligations drawbacks stem from a layered fiscal structure that combines locally enacted taxes with compliance expectations shaped by French metropolitan legal tradition. This creates a dual burden that foreign-incorporated entities rarely anticipate at the outset.

The territory operates its own tax code, administered by the Direction Générale des Impôts et des Douanes (DGID). Corporate income tax, the Impôt sur les Sociétés, applies at a standard rate of 25%, and businesses also face the Contribution de Solidarité Territoriale and sector-specific levies that compound the effective tax burden.

VAT equivalents apply through the Taxe sur la Valeur Ajoutée locale (TVA locale), with distinct rates across product and service categories. Misclassification under French fiscal law compliance standards exposes your firm to reassessment penalties.

Annual filing obligations require French-language documentation prepared under local accounting norms, which typically means retaining a licensed local accountant, adding to operational overhead.

A foreign-owned SARL generating 30 million XPF in annual revenue could face combined corporate tax, solidarity contributions, and indirect levies exceeding 35% of net profit, before accounting for mandatory accountant fees estimated at 400,000–600,000 XPF per year for compliant filings.

Limited Range of Available Corporate Structures

The limited corporate structures available in French Polynesia restrict how foreign investors can organize their operations from the outset. The territory applies French commercial law, principally the Code de Commerce, which means the menu of entity types mirrors metropolitan France rather than reflecting locally tailored options suited to a small island economy.

In practice, most businesses incorporate as either a Société à Responsabilité Limitée (SARL) or a Société par Actions Simplifiée (SAS). Both structures carry administrative obligations, including formal capital deposit requirements and registration through the Registre du Commerce et des Sociétés (RCS) in Papeete, that add friction without offering the flexibility found in offshore-oriented jurisdictions.

Structures common in other Pacific jurisdictions, such as limited liability partnerships or international business companies, have no direct equivalent under the applicable French legal framework. This absence limits structuring options for holding arrangements, joint ventures, or fund vehicles, forcing some foreign businesses into entity types that do not align with their operational or tax planning needs.

If your intended structure relies on a pass-through, partnership, or IBC-style entity, no equivalent exists under the French commercial law framework applied in French Polynesia, and your structure will need to be redesigned around SARL or SAS mechanics before registration can proceed.

Strategies to Overcome These Challenges

Overcoming French Polynesia incorporation challenges requires structural preparation rather than reactive adjustments. The disadvantages discussed across this blog share a common thread: most stem from the territory's dual regulatory exposure to both local Polynesian rules and metropolitan French law.

- Register your entity type against the specific sectoral restrictions enforced by the Direction Générale des Affaires Économiques before committing to a corporate structure.

- Elect your tax regime explicitly at incorporation, since the default application of territorial tax rules under the Code des impôts de la Polynésie française may not suit your operating model.

- Account for customs duty obligations under the tariff schedule administered by the Direction des Douanes in your pricing and supply chain cost modelling.

- Where foreign ownership caps apply, structure equity arrangements in advance to meet sector-specific thresholds set under local economic regulation.

- Plan working capital reserves to absorb the freight and logistics cost premiums that result from the territory's geographic position in the South Pacific.

Mitigation steps of this kind operate within a framework governed by the Direction des Affaires Juridiques and the relevant metropolitan oversight bodies. Structural decisions made at the point of incorporation carry long-term compliance consequences that are not easily unwound.

French Polynesia Still Worth It

French Polynesia carries real structural weight for foreign businesses: high operating costs, a small domestic market, restricted foreign ownership in protected sectors, and deep fiscal entanglement with French metropolitan law. Those constraints are documented and consequential. The territory still functions as a credible base for businesses oriented toward the Pacific region, maritime activity, or high-value tourism-adjacent services, provided your model accounts for the cost and compliance reality upfront.

| Pro | Con |

|---|---|

| French legal framework provides procedural stability and enforceable contract law | Corporate governance and compliance obligations follow French metropolitan standards, adding administrative overhead |

| Pacific regional positioning supports maritime and cross-border service activity | Geographic isolation raises logistics costs and limits access to suppliers, staff, and infrastructure |

| Established fiscal treaty framework through France reduces certain double-taxation exposure | Tax obligations under French Polynesian fiscal law require dual-layer compliance with both local and metropolitan rules |

| The SARL and SAS structures are internationally recognised corporate forms | Available entity types are limited; offshore or holding-specific vehicles common elsewhere are not accessible here |

| Stable political relationship with France provides regulatory continuity | Foreign ownership is restricted by law in sectors including land, fishing, and certain licensed industries |

Compliance Services for Companies in French Polynesia

Manage your ongoing compliance obligations under French Polynesian law, including annual filings, fiscal reporting, and corporate maintenance requirements.

Conclusion

The French Polynesia incorporation drawbacks summary is straightforward: this is a jurisdiction where the structural costs are real and the market constraints are fixed. Dual taxation exposure under the French fiscal framework, combined with restricted foreign ownership in sectors central to the local economy, creates a ceiling on how certain business models can be deployed here. The small consumer base compounds this further. Proper entity structuring and ongoing compliance support become less optional and more foundational to any viable operation in this territory.

Expanship and Your French Polynesia Expansion

French Polynesia company formation compliance support involves working within a specific set of obligations: territorial tax rules administered under French fiscal law, corporate structures governed largely by the French Commercial Code as locally applied, and sector restrictions that limit foreign participation in industries like land development and fishing. Expanship's role is to reduce the operational burden of tracking these requirements, not to change what they demand of your business.

Beyond incorporation, our team supports your entity across each stage of establishment and ongoing operation:

- Your company registration is handled with full document preparation tailored to the relevant territorial authority requirements.

- We provide registered agent and office services to satisfy local presence obligations.

- Our team manages government filings and liaises directly with regulatory bodies on your behalf.

- Post-incorporation compliance is monitored to keep your firm in good standing.

- Banking introduction assistance is available to help your business establish the relationships it needs.

- Tax registration and local authority liaison are coordinated to ensure your obligations are properly structured from the outset.

Reach out to Expanship French Polynesia to discuss your incorporation requirements.

Frequently Asked Questions (FAQ)

French Polynesia operates under its own tax regime administered by the Direction Générale des Impôts et des Contributions Publiques (DGICP), separate from metropolitan France's Direction Générale des Finances Publiques. However, because the territory's fiscal code draws heavily from French legal principles, your obligations can be complex to interpret without advisors familiar with both frameworks. Errors in classification or filing can trigger penalties under local tax enforcement procedures.

Operating costs in French Polynesia are substantially higher than in most Pacific Island jurisdictions due to the cost of imported goods, freight logistics, and above-average labor costs relative to the region. The territory does not benefit from the low-cost operational environments found in, for example, Vanuatu or the Cook Islands. This directly affects your overhead from day one.

Non-compliance with obligations administered by the DGICP can result in financial penalties, interest charges on unpaid tax, and in serious cases, criminal liability under applicable French-derived fiscal law. The absence of an extensive local tax treaty network means foreign parent companies cannot always offset these liabilities through treaty mechanisms. Penalties escalate the longer a compliance gap remains unaddressed.

French Polynesia's available structures, primarily the SARL, SAS, and SA derived from French company law, are broadly consistent with other French collectivities, so the limitation is not unique to the territory. The problem is that these forms were not designed for small Pacific markets and carry administrative requirements, such as mandatory auditing thresholds and capital rules, that can be disproportionate for early-stage foreign businesses. You have fewer structural alternatives compared to common law offshore jurisdictions.

Not entirely. Physical distance from major supply chains and the dependence on air and sea freight through Papeete means logistics costs are structurally embedded in your operating model. While digital service businesses are less affected, any company dealing in physical goods will face freight delays and import markups that cannot be engineered away through corporate structure alone.

French Polynesia has no local stock exchange, and domestic bank lending for foreign-owned entities is constrained by both limited competition among local financial institutions and conservative lending criteria. If your growth strategy depends on equity financing or credit facilities beyond what local banks offer, you will need to access capital through metropolitan French or international institutions, which introduces currency considerations and additional compliance layers.

With a population of approximately 280,000 spread across 118 islands, the addressable domestic market is structurally limited for most product or service categories. A business incorporated locally must typically orient toward tourism-dependent revenue, export markets, or regional Pacific trade to sustain growth, since domestic consumption alone rarely supports the overhead that comes with formal incorporation under French-derived corporate law.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.