Key Takeaways

- Oman's business entity framework is governed primarily by the Commercial Companies Law (Royal Decree No. 18/2019), administered by the Ministry of Commerce, Industry and Investment Promotion (MoCIIP).

- The Limited Liability Company is the most commonly registered structure for foreign-linked commercial activity under Omani law.

- Joint stock companies exist in two distinct forms — the publicly listed SAOG and the closed SAOC — each serving different capital and regulatory requirements.

- Branch and representative offices provide foreign firms with a legal presence in Oman without requiring the formation of a standalone Omani entity.

Introduction to Entity Types in Oman

Oman is an independent sovereign state located on the southeastern corner of the Arabian Peninsula, sharing borders with Saudi Arabia, the United Arab Emirates, and Yemen, with coastlines along the Arabian Sea and the Gulf of Oman. Company registration and corporate governance fall under the authority of the Ministry of Commerce, Industry and Investment Promotion (MoCIIP), which administers the Commercial Register and oversees compliance with the Commercial Companies Law.

The types of business entities in Oman are defined primarily under the Commercial Companies Law, most recently updated by Royal Decree No. 18/2019. Oman operates a territorial tax system, with corporate income tax applied to profits generated within the country's borders.

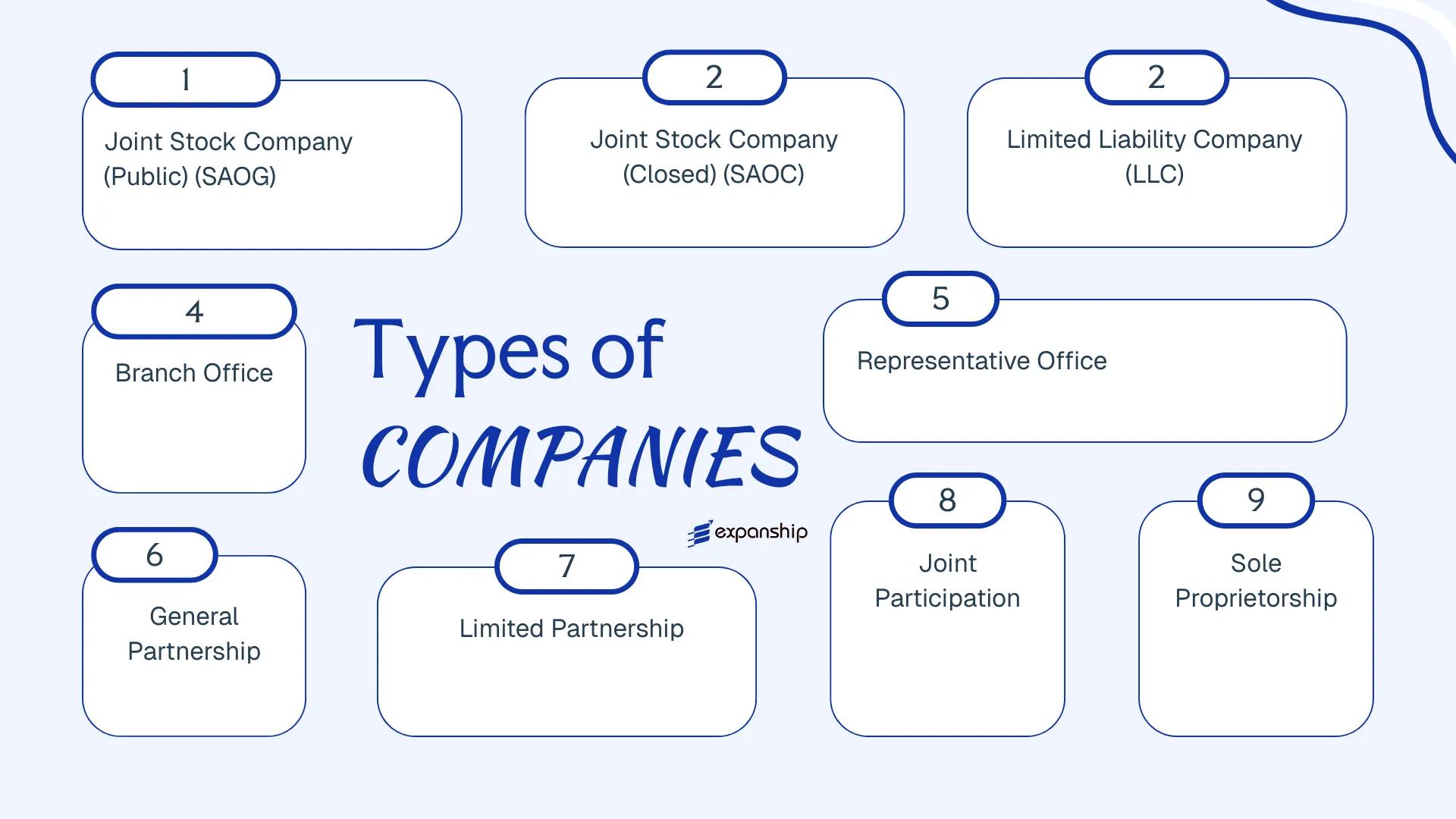

Businesses forming a legal presence here can choose from several structures: the Joint Stock Company (in both publicly listed SAOG and closed SAOC forms), the Limited Liability Company, the Branch Office, the Representative Office, the General Partnership, the Limited Partnership, the Joint Participation arrangement, and the Sole Proprietorship. Each subsequent section of this article examines one of these Omani legal entity structures — covering formation requirements, ownership rules, and applicable regulatory obligations.

An Overview of Business Structures in Oman

Oman's commercial law framework provides several distinct entity types for businesses seeking to establish a legal presence in the country. The primary legislation governing these structures is the Commercial Companies Law, issued by Royal Decree No. 18/2019, which consolidates and updates the rules for most corporate forms. Each structure carries different implications for ownership, liability, and permitted commercial activity.

Business Structures at a Glance

| Entity Type | Legal Form | Liability | Taxed / Exempt | Local Trading | Minimum Members | Regulatory Authority | Governing Act |

|---|---|---|---|---|---|---|---|

| Joint Stock Company (SAOG) | Public company | Limited to shares | Taxed | Yes | 3 founders | MCIPP / CMA | Royal Decree 18/2019 |

| Joint Stock Company (SAOC) | Closed company | Limited to shares | Taxed | Yes | 3 shareholders | MCIPP | Royal Decree 18/2019 |

| Limited Liability Company (LLC) | Private company | Limited to capital | Taxed | Yes | 1 shareholder | MCIPP | Royal Decree 18/2019 |

| Branch Office | Extension of parent | Parent bears liability | Taxed | Restricted | N/A | MCIPP | Royal Decree 18/2019 |

| Representative Office | Non-trading entity | Parent bears liability | Exempt | No | N/A | MCIPP | Royal Decree 18/2019 |

| General Partnership | Partnership | Unlimited | Taxed | Yes | 2 partners | MCIPP | Royal Decree 18/2019 |

| Limited Partnership | Partnership | Mixed | Taxed | Yes | 2 partners | MCIPP | Royal Decree 18/2019 |

| Joint Participation | Contractual arrangement | Per agreement | Taxed | Yes | 2 parties | MCIPP | Royal Decree 18/2019 |

| Sole Proprietorship | Individual trading | Unlimited personal | Taxed | Yes | 1 individual | MCIPP | Commercial Law |

Each of these structures is examined in full in the sections below.

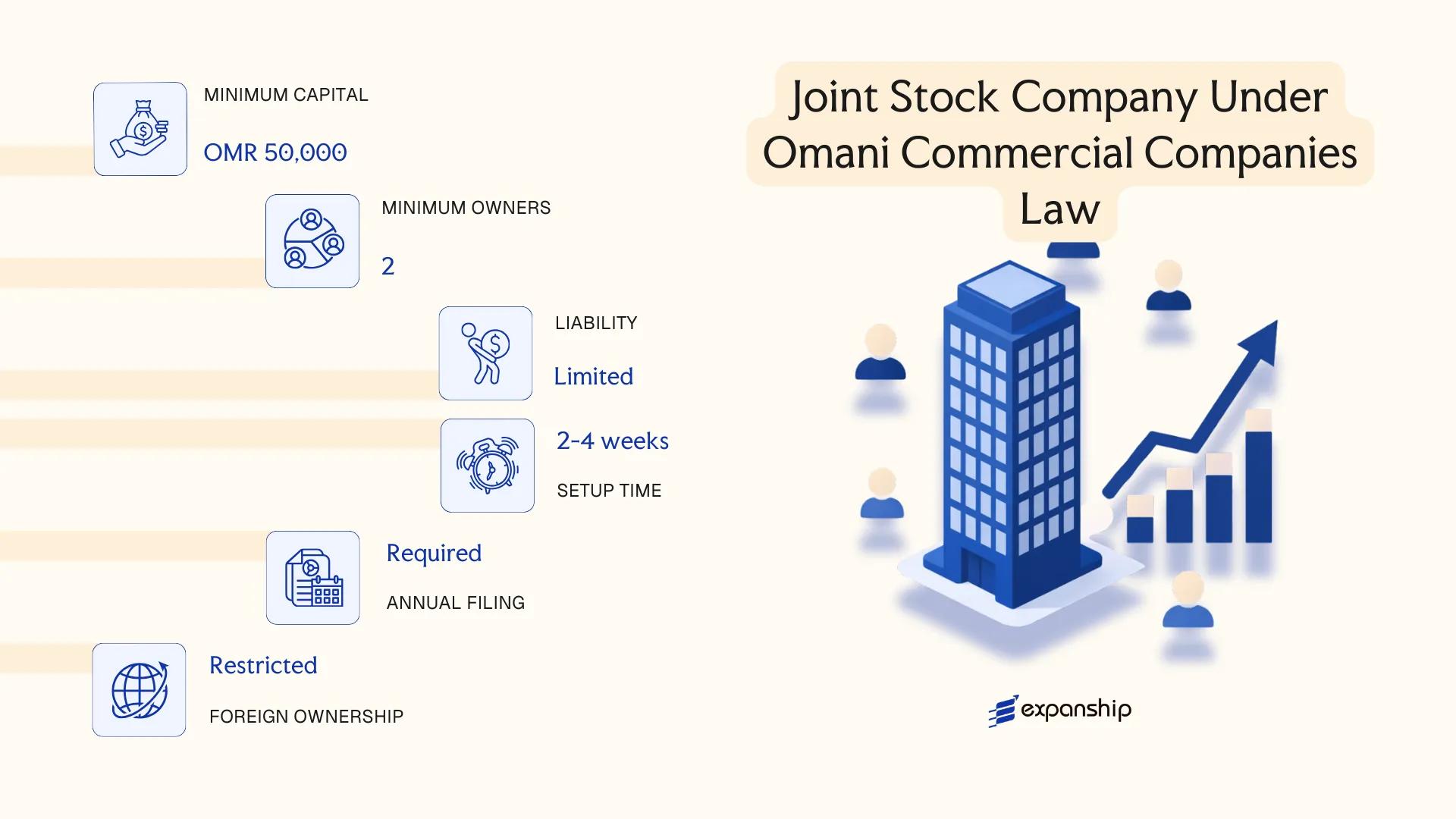

Joint Stock Company (SAOG and SAOC) Under Omani Commercial Companies Law

Governed by the Commercial Companies Law (Royal Decree No. 18/2019), the Oman joint stock company exists in two forms: the publicly listed SAOG (Société Anonyme Omanaise Générale) and the closed SAOC (Société Anonyme Omanaise Close). Both carry separate legal personality and confer limited liability on shareholders, meaning personal assets remain insulated from corporate obligations.

Shares in an SAOG are offered to the public and traded on the Muscat Stock Exchange, placing the entity under the supervision of the Capital Market Authority (CMA). The SAOC, by contrast, restricts share transfers and does not make public offerings, making it the more accessible structure for private investors.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Separate legal entity; limited liability | Shareholders liable only to the extent of their share contribution |

| Members | Shareholders; minimum 3 (SAOC) / minimum 40 founders (SAOG) | SAOG requires public subscription; SAOC shares are privately held |

| Local Presence | Registered office in Oman required | CMA registration required for SAOG; Ministry of Commerce for both |

| Capital | OMR 500,000 minimum (SAOC); OMR 2,000,000 minimum (SAOG) | Capital denominated in Omani Rial |

| Privacy | SAOG financials publicly disclosed; SAOC has greater confidentiality | CMA mandates periodic disclosure for listed entities |

Focus Points

- Taxation: Subject to Corporate Income Tax at 15% on net taxable income; VAT applies at 5% on taxable supplies; no withholding tax on dividends; stamp duty applies to certain instruments.

- Annual Compliance: Audited financial statements, annual general meetings, and CMA filings (SAOG) are mandatory each financial year.

- Economic Substance: Joint stock companies conducting relevant activities must satisfy Oman's economic substance requirements under the Income Tax Law framework.

- Restrictions: Foreign ownership caps may apply in certain sectors; SAOG shares cannot be transferred without CMA compliance.

- Conversion: An SAOC may convert to an SAOG subject to CMA approval and meeting the higher capital and shareholder thresholds.

Sub-Types

SAOG (Public Joint Stock Company)

Shares are listed and traded on the Muscat Stock Exchange, requiring ongoing CMA oversight, mandatory public disclosure, and a minimum capital of OMR 2,000,000. This structure suits large enterprises seeking access to public capital markets.

SAOC (Closed Joint Stock Company)

Share transfers are restricted to existing shareholders or approved parties, and no public subscription is permitted. The SAOC is typically used by larger private enterprises or joint ventures that require the corporate governance framework of a joint stock company without public market obligations.

When to Use This Structure

The joint stock company suits large-scale commercial operations, financial institutions, and ventures requiring significant capitalisation or structured governance. The SAOC offers corporate credibility with greater ownership control; the SAOG unlocks public financing but carries substantially higher compliance obligations.

Best suited for large private enterprises (SAOC) or businesses seeking to raise public capital through Oman's regulated markets (SAOG).

Company Incorporation in Oman

Incorporate a joint stock company or other business structure in Oman with end-to-end support from Expanship.

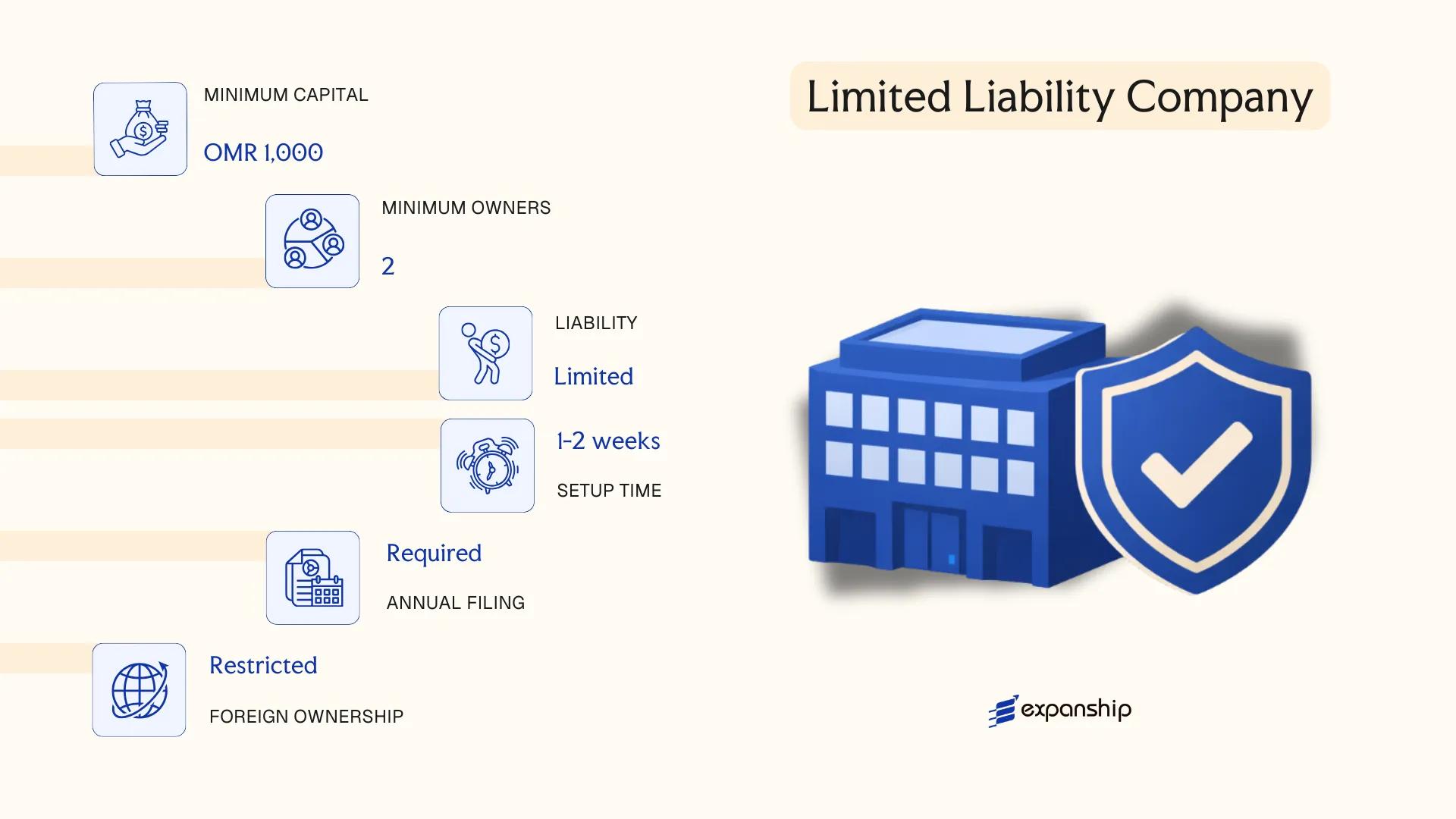

Limited Liability Company (LLC) Under the Commercial Companies Law

Oman LLC formation under the Commercial Companies Law (Royal Decree No. 18/2019) gives the entity separate legal personality, meaning the company holds rights and obligations distinct from its members. Liability is capped at each member's contribution to share capital, making this a hybrid structure that combines corporate protection with operational flexibility.

Registered under the Ministry of Commerce, Industry and Investment Promotion (MOCIIP), an LLC is the most widely used structure for foreign-invested commercial activity in the country.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Limited Liability Company (LLC) | Separate legal personality; governed by Royal Decree No. 18/2019 |

| Members | 2–40 members | Single-member LLC is not permitted; members hold "quotas," not shares |

| Management | One or more managers | Managers need not be members; a board of directors is optional |

| Local Presence | Registered office in Oman required | A physical address; P.O. Box alone is not sufficient |

| Capital | Minimum OMR 150,000 for majority foreign-owned entities; OMR 20,000 for Omani-majority | Denominated in Omani Rial; capital must be deposited before registration |

| Privacy | Member names disclosed in commercial register | No bearer quotas permitted |

Focus Points

- Taxation: Subject to 15% corporate income tax on net profits; VAT applies at 10% where applicable; no withholding tax on dividends, though interest and royalties may attract withholding obligations depending on the payment context.

- Economic Substance: Entities in certain sectors must satisfy Oman's Economic Substance Regulations, requiring adequate local activity and management.

- Annual Compliance: Audited financial statements required annually; renewal of commercial registration with MOCIIP each year.

- Treaty Access: Oman's double tax treaty network is accessible to resident LLCs, subject to beneficial ownership conditions.

- Foreign Ownership: Up to 100% foreign ownership is permitted in many sectors following the Foreign Capital Investment Law, though sector-specific restrictions apply.

Closing

An LLC suits trading, services, manufacturing, and joint venture activity where partners want liability protection without a public listing requirement. The structure offers genuine operational scope but carries a relatively high minimum capital threshold for majority foreign-owned entities, which can be a barrier for early-stage businesses.

Foreign investors seeking an operational presence in Oman with full or majority ownership, particularly in trading, services, or project-based sectors.

Foreign Business Presence in Oman [Branch Office, Representative Office]

Foreign business presence in Oman can be established without incorporating a separate legal entity. Foreign branch office registration in Oman is governed primarily by the Commercial Companies Law (Royal Decree No. 18/2019) and the Foreign Capital Investment Law (Royal Decree No. 50/2019), with registration administered through the Ministry of Commerce, Industry and Investment Promotion (MoCIIP). A branch carries no separate legal personality — the parent company remains fully liable for its obligations.

A representative office operates under similar regulatory oversight but is structurally more restricted. It cannot generate revenue or sign commercial contracts in its own capacity; its function is limited to market research, liaison, and promotional activities on behalf of the parent.

Key Characteristics

| Requirement | Branch Office | Representative Office |

|---|---|---|

| Legal Personality | None — extension of parent company | None — extension of parent company |

| Liability | Parent bears full liability | Parent bears full liability |

| Commercial Activity | Permitted within licensed scope | Prohibited — non-trading only |

| Local Representative | Mandatory Omani-registered agent or manager | Required |

| Registered Office | Physical address in Oman required | Physical address in Oman required |

| Capital Requirement | No statutory minimum, but proof of parent solvency required | None |

| Privacy | Parent company details are publicly disclosed | Parent company details are publicly disclosed |

Focus Points

- Taxation: Branches are subject to corporate income tax at 15% on Oman-sourced income; VAT at 5% applies where applicable; no withholding tax on remitted profits, though treaty access depends on the parent's jurisdiction.

- Economic Substance: No standalone substance regime applies specifically to branches, but activity must genuinely occur within the licensed scope.

- Annual Compliance: Branches must file audited financial statements and renew their commercial registration annually with MoCIIP.

- Restrictions: Representative offices may not invoice clients, hold inventory, or enter binding contracts — any commercial activity triggers reclassification risk.

- Conversion: A branch can be converted into an LLC or SAOC, subject to MoCIIP approval and satisfaction of applicable capitalisation requirements.

Sub-Types

Branch Office

Licensed to conduct the same business activities as its parent, a branch office can bid on government contracts and generate local revenue. Registration requires submission of the parent's constitutional documents, audited accounts, and a board resolution authorising the Oman operation.

Representative Office

Permitted solely for non-commercial functions, this structure suits firms conducting feasibility studies or managing relationships ahead of a larger market entry. It cannot employ more than a limited number of staff under most licensing frameworks and must be renewed periodically.

Closing Remarks

Both structures suit multinationals testing the market or executing project-specific work without the administrative burden of incorporating a standalone entity. The principal advantage is speed of setup; the key limitation is that neither form provides liability separation from the parent.

Foreign companies with existing contracts or project mandates in Oman, or those undertaking pre-entry market assessment, before committing to a locally incorporated entity.

Partnership Structures in Oman [General Partnership, Limited Partnership, Joint Participation]

Partnership structures under Omani law are governed by the Commercial Companies Law, Royal Decree No. 18/2019, which consolidates the rules for all recognised business forms in the Sultanate. Partnerships generally do not carry the same liability protections as limited liability companies, making the choice of structure a consequential decision for any investor or business owner.

Three distinct partnership forms exist under this legislation: the general partnership, the limited partnership, and the joint participation company. Each carries different implications for liability, governance, and the degree to which the entity is publicly identifiable.

Key Characteristics

| Requirement | General Partnership | Limited Partnership | Joint Participation Company |

|---|---|---|---|

| Legal Form | Separate legal personality | Separate legal personality | No separate legal personality; internal arrangement only |

| Members | Partners (min. 2); all bear unlimited joint liability | Partners (min. 2); at least 1 general partner (unlimited liability) and 1 limited partner | Participants (min. 2); not disclosed to third parties |

| Local Presence | Registered office in Oman required | Registered office in Oman required | No public registration required |

| Capital | No statutory minimum; denominated in Omani Rial (OMR) | No statutory minimum; limited partner's liability capped at capital contribution | No statutory minimum |

| Privacy | Partners named in commercial register | General partner publicly disclosed; limited partner identity may be protected | Fully private; arrangement not registered publicly |

Focus Points

- Taxation: Corporate income tax applies at 15% on net profit; VAT at 5% applies where turnover thresholds are met; withholding tax applies to certain payments to non-residents, including royalties and dividends.

- Liability exposure: General partners in both general and limited partnerships bear unlimited personal liability for firm obligations.

- Annual compliance: Partnerships must file audited financial statements and renew their commercial registration annually with the Ministry of Commerce, Industry and Investment Promotion (MoCIIP).

- Foreign ownership: General and limited partnerships may admit foreign partners, subject to foreign investment regulations and any applicable sector restrictions under the Foreign Capital Investment Law.

- Joint participation restrictions: Because the joint participation company has no legal personality, it cannot independently own property, enter contracts, or sue in its own name.

Sub-Types

General Partnership (Tadhamon)

All partners share unlimited, joint liability for the firm's debts. This form is typically used by professional service providers or family-owned trading businesses where partners are closely aligned and mutually accountable.

Limited Partnership (Tawsiya Basita)

At least one general partner retains unlimited liability while one or more limited partners contribute capital without participating in management. The limited partner's exposure is confined to the amount contributed, provided they do not engage in managing the business.

Joint Participation Company (Moshtaraka)

This is an undisclosed arrangement between two or more parties for a specific activity or project. It has no independent legal existence and operates entirely outside the public commercial register, making it suited to short-term joint ventures or one-off commercial projects.

Partnership structures are most commonly used for professional practices, family businesses, and short-term project-based collaborations. The absence of a statutory capital minimum offers flexibility, but unlimited liability in general partnerships represents a significant exposure for individual partners.

General and limited partnerships are best suited for closely held businesses or professional firms where partners have established trust and are comfortable with shared accountability.

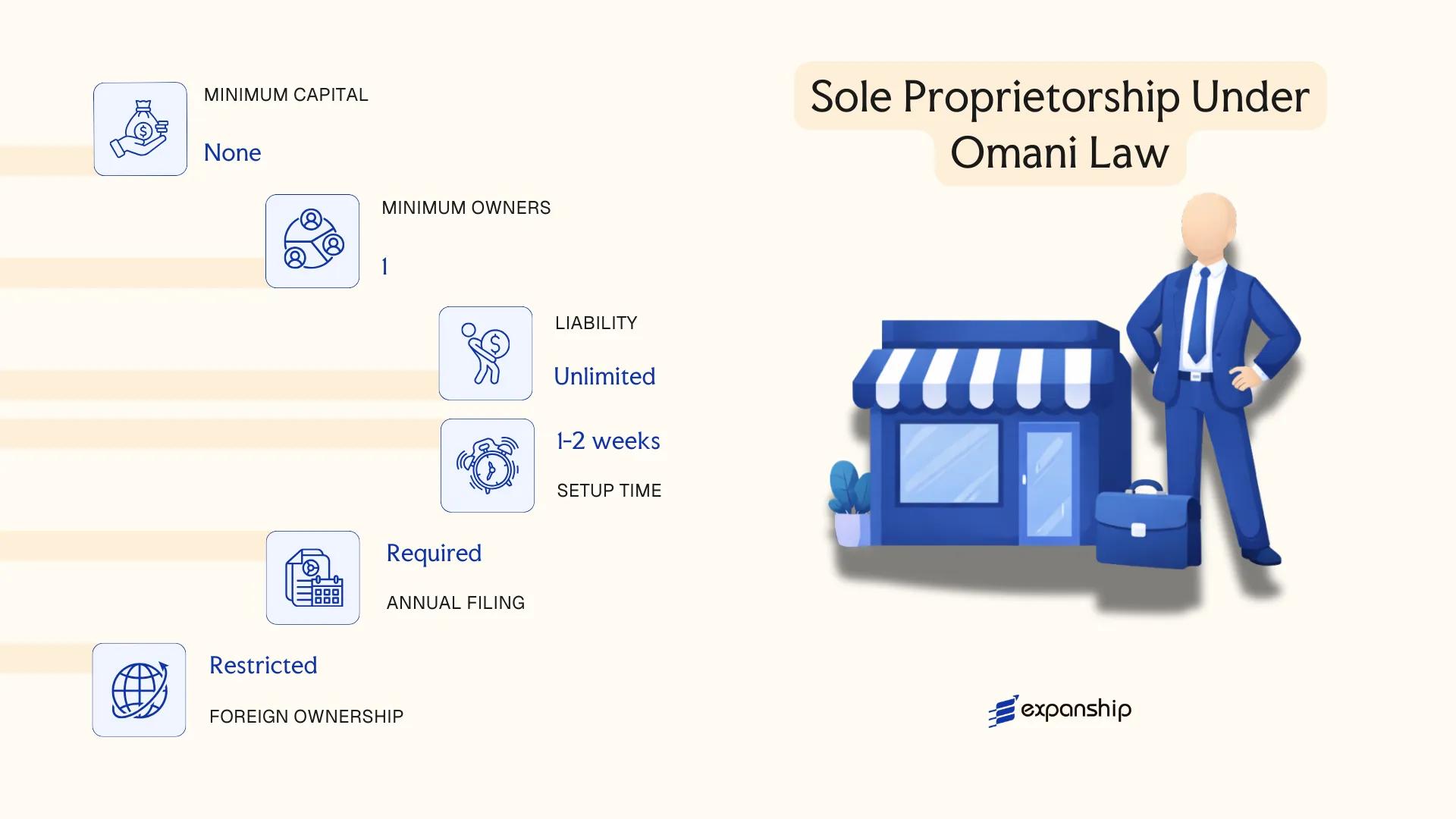

Sole Proprietorship Under Omani Law

Sole proprietorship registration in Oman is governed by the Commercial Companies Law (Royal Decree No. 18/2019) alongside the Commercial Register Law. Unlike incorporated entities, a sole proprietorship carries no separate legal personality — the business and its owner are treated as one legal unit, meaning personal assets are fully exposed to business liabilities.

Registration is handled through the Ministry of Commerce, Industry and Investment Promotion (MoCIIP), typically via the Invest Easy portal. Only Omani nationals may establish this structure; foreign nationals are not permitted to register as sole traders under current regulations.

Key Characteristics

| Requirement | Detail | Notes |

|---|---|---|

| Legal Form | Sole Proprietorship (Individual Establishment) | No separate legal personality from the owner |

| Proprietor | Single individual (Proprietor) | One owner only; no partners or shareholders |

| Nationality Requirement | Omani nationals only | Foreign individuals are excluded from this structure |

| Local Presence | Physical registered address required | Must maintain a local business address in Oman |

| Capital | No statutory minimum capital | Owner bears full financial exposure personally |

| Privacy | Owner's name appears in the Commercial Register | No confidentiality provisions apply |

Focus Points

- Taxation: Subject to personal income tax rules applicable to Omani individuals; corporate income tax at 15% applies if the business exceeds qualifying thresholds, while VAT registration is required upon breaching the OMR 38,500 annual supply threshold.

- Annual Compliance: Renewal of the Commercial Registration with MoCIIP is required annually; municipal licensing renewals may also apply depending on the activity.

- Conversion: The structure can be converted into an LLC or other registered entity, though this requires a fresh incorporation process rather than a direct statutory conversion.

- Treaty Access: As an unincorporated individual business, access to Oman's double taxation treaties is generally not available in the same manner as for incorporated entities.

- Restrictions: Certain licensed commercial activities are restricted to this structure or, conversely, may not be conducted through it — activity-specific approvals from sectoral regulators apply.

Closing

A sole proprietorship suits Omani nationals operating small-scale trading, service, or consultancy activities where low setup cost and direct operational control outweigh concerns about personal liability. The absence of limited liability protection is a material drawback for any business carrying meaningful financial or contractual risk.

This structure is most appropriate for Omani nationals running low-risk, owner-operated businesses with limited third-party liability exposure.

How to Choose the Right Entity Type in Oman

Understanding how to choose a business structure in Oman requires more than comparing formation costs — the wrong choice carries concrete legal and financial consequences that can be difficult to reverse.

Why Your Entity Choice Matters

The structure you register shapes your compliance obligations, tax position, and operational permissions from the outset.

- Selecting a representative office when you intend to conduct commercial transactions violates the permitted scope under the Commercial Companies Law, which can result in penalties or forced closure.

- Choosing an entity without the capacity to maintain employees or a physical presence, when Oman's tax authority (the Tax Authority of Oman) applies economic substance standards, can trigger reporting failures and potential fines.

- Forming a joint stock company when a single-member LLC would suffice imposes mandatory board composition requirements and audit obligations that generate unnecessary annual costs for small operations.

- Registering under a structure that restricts foreign ownership to a minority stake, without first obtaining approval under relevant sector-specific regulations, can invalidate the ownership arrangement entirely.

Key Factors to Consider

- Business Activity: Active trading, passive asset holding, and regulated sectors such as banking or insurance each require a distinct legal form under Omani commercial law.

- Ownership Structure: Single-owner operations and multi-party ventures have different governance requirements — an LLC accommodates flexible management, while a joint stock company mandates a formal board.

- Foreign Ownership Percentage: Certain activities permit 100% foreign ownership, while others impose local partner thresholds that directly determine which entity type is viable.

- Tax Position: Your eligibility for Oman's double taxation treaty network depends on the entity type and its residency status under the Income Tax Law.

- Substance Capacity: If your firm cannot realistically maintain staff and decision-making functions locally, the chosen structure must be compatible with that operational reality.

- Exit and Conversion: Not all Omani entity types permit straightforward conversion or redomiciliation — confirm this before formation if a future structural change is anticipated.

Compliance Services for Companies in Oman

Ongoing compliance support for Omani entities, including annual filings, renewal obligations, and regulatory reporting with the relevant authorities.

Conclusion

Selecting the right structure is one of the first binding decisions you make under Omani commercial law, and it shapes everything from ownership rights to liability exposure. This Oman company incorporation conclusion guide reflects a regulatory environment governed primarily by the Commercial Companies Law (Royal Decree 18/2019) and overseen by the Ministry of Commerce, Industry and Investment Promotion.

The Limited Liability Company remains the most commonly registered entity for foreign-linked commercial activity. Joint stock companies serve businesses requiring public capital or operating in regulated sectors. Branch and representative offices suit foreign firms testing the market or executing specific contracts. Partnership structures apply to professionals and closely held ventures, while sole proprietorships are reserved for Omani nationals in small-scale trade.

Oman's continued expansion of its bilateral investment treaty network and its VAT framework signal a regulatory direction toward greater international alignment, which affects how your business structure should be planned from the outset.

How Expanship Can Assist You

Expanship company formation services Oman cover the full process of establishing and maintaining a legal presence under the Commercial Companies Law, whether you are registering a Limited Liability Company with the Ministry of Commerce, Industry and Investment Promotion (MoCIIP) or structuring a foreign branch under OCIPED guidelines. Every entity type discussed in this blog carries distinct registration requirements, and our team works directly within those frameworks.

From initial document preparation to post-incorporation compliance, Expanship manages each stage on your behalf:

- Document preparation, notarization, and legalization

- Registered agent and registered office provision

- Government filing and MoCIIP liaison

- Commercial Registration and municipal license coordination

- Post-incorporation compliance management

- Banking introduction assistance

Reach out to Expanship Oman to discuss the right structure for your business.

Frequently Asked Questions (FAQ)

The Limited Liability Company (LLC) is the most frequently formed structure, largely because it permits foreign participation up to 70% in most sectors, requires a relatively accessible minimum capital, and suits a broad range of commercial activities under the Commercial Companies Law (Royal Decree 18/2019).

An LLC restricts share transferability and is closed to public subscription, while a Joint Stock Company (SAOG) may list on the Muscat Stock Exchange and raise capital publicly. Both structures are subject to corporate tax under the Income Tax Law, but the Joint Stock Company carries significantly heavier disclosure and governance obligations, including mandatory audited reporting to the Capital Market Authority.

Among locally registered structures, the LLC provides relatively limited public disclosure compared to a SAOG. Shareholder details are held in the Commercial Register maintained by the Ministry of Commerce, Industry and Investment Promotion, though nominee arrangements are not formally recognized under Omani law in the same manner as offshore jurisdictions.

No. A General Partnership requires at least two partners, and a Limited Partnership similarly demands a minimum of one general and one limited partner. An LLC may be formed by a single shareholder under the sole proprietorship LLC variant, while a Joint Stock Company requires a minimum of three founding shareholders.

Foreign nationals may establish an LLC, a Branch Office, or a Representative Office. Full foreign ownership is permitted in certain sectors under the Foreign Capital Investment Law (Royal Decree 50/2019), subject to ministerial approval. Branch Offices require a local service agent and are restricted from conducting activities beyond the parent company's registered scope.

Conversion is permitted under the Commercial Companies Law. An LLC may convert to a Joint Stock Company by satisfying applicable capital thresholds and governance requirements. The conversion process involves approval from the Ministry of Commerce, Industry and Investment Promotion and amendment of the constitutional documents.

LLCs and Joint Stock Companies hold distinct legal personality separate from their shareholders. General Partnerships do not create a legal entity fully separate from the partners, meaning partners bear personal liability for firm obligations. A Joint Participation arrangement has no legal personality whatsoever and exists solely as a contractual relationship between parties.

Legal Disclaimer

The information provided in this article is for general informational purposes only and does not constitute legal, tax, or professional advice. While we strive to ensure the accuracy and timeliness of the content, laws and regulations are subject to change, and the application of laws can vary widely based on specific facts and circumstances.

Readers should not act upon this information without seeking professional counsel tailored to their individual situation. Expanship and its authors disclaim any liability for actions taken or not taken based on the content of this article.

For specific advice regarding your business setup, compliance requirements, or any legal matters, please consult with qualified legal and tax professionals in the relevant jurisdiction.